Juicers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

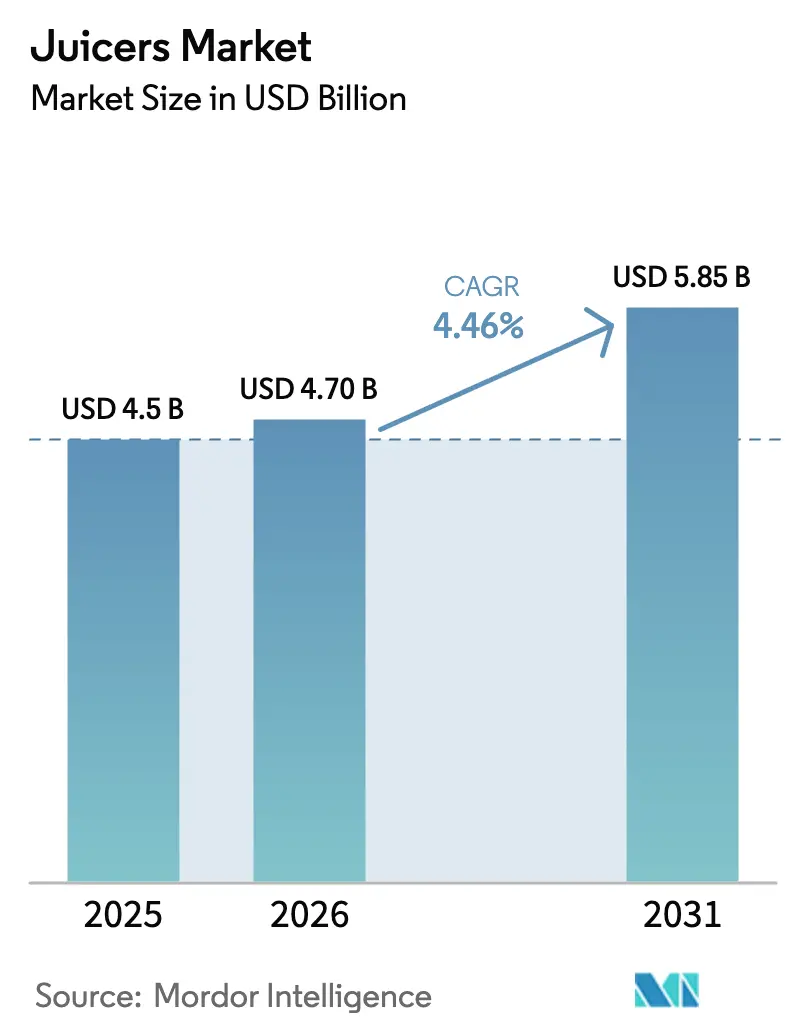

| Market Size (2026) | USD 4.70 Billion |

| Market Size (2031) | USD 5.85 Billion |

| Growth Rate (2026 - 2031) | 4.46% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Juicers Market Analysis by Mordor Intelligence

The juicers market size is expected to grow from USD 4.50 billion in 2025 to USD 4.70 billion in 2026 and is forecast to reach USD 5.85 billion by 2031, growing at a CAGR of 4.46% from 2026 to 2031. A steady growth path reflects durable shifts in household wellness routines and convenient access via digital channels that lower search costs and widen assortments. Regulatory changes in the European Union, especially the Right to Repair framework that will have full effect by July 2026, are pushing manufacturers to design repairable assemblies, ensure spare parts availability, and extend warranties when consumers choose repair during the original coverage period[1]European Commission, “Right to Repair Initiative and Consumer Law Updates,” European Commission, commission.europa.eu . Ingredient-contact rules in Europe that restrict bisphenols are also moving product roadmaps toward BPA-free polymers and stainless steel in food-contact pathways. Brand strategies in the juicers market are now centered on ease of cleaning, serviceability, and premium materials that can sustain pricing power while meeting compliance expectations.

Key Report Takeaways

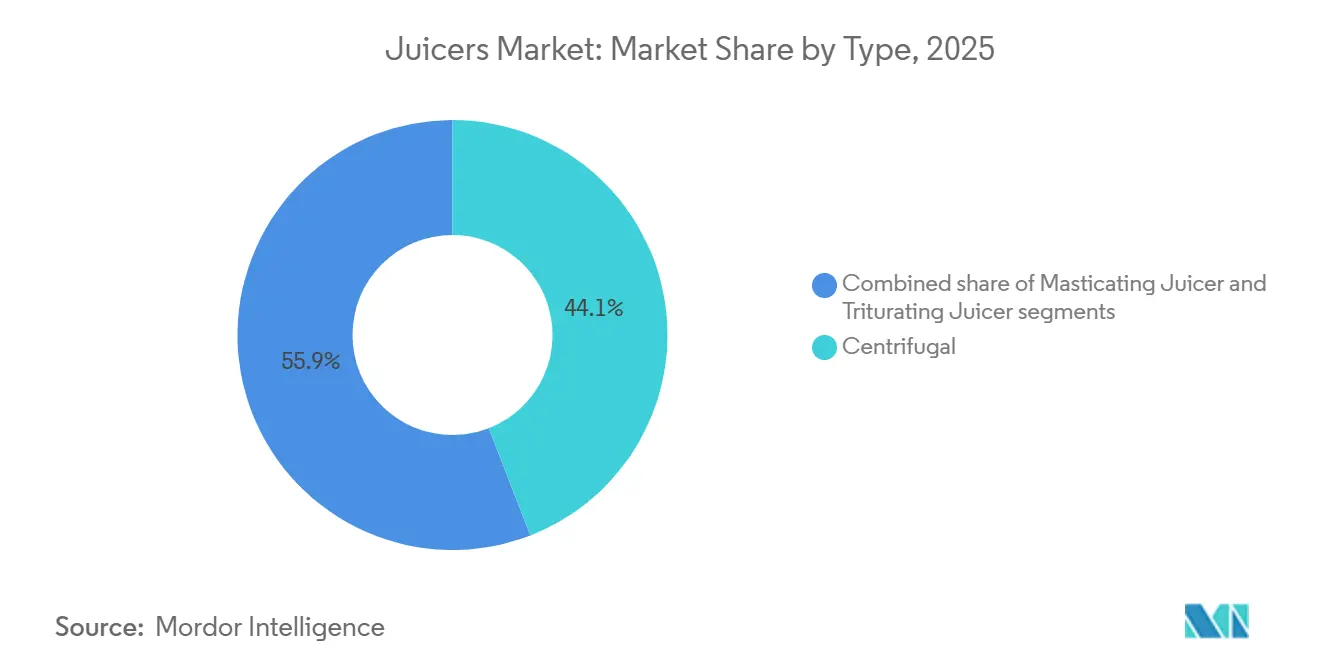

- By type, centrifugal juicers led with 44.14% of juicers market share in 2025. Masticating and triturating models are projected to record the highest CAGR at 6.81% through 2031.

- By category type, electric juicers accounted for 79.91% of category revenue in 2025. Electric models are projected to grow at a 4.97% CAGR through 2031.

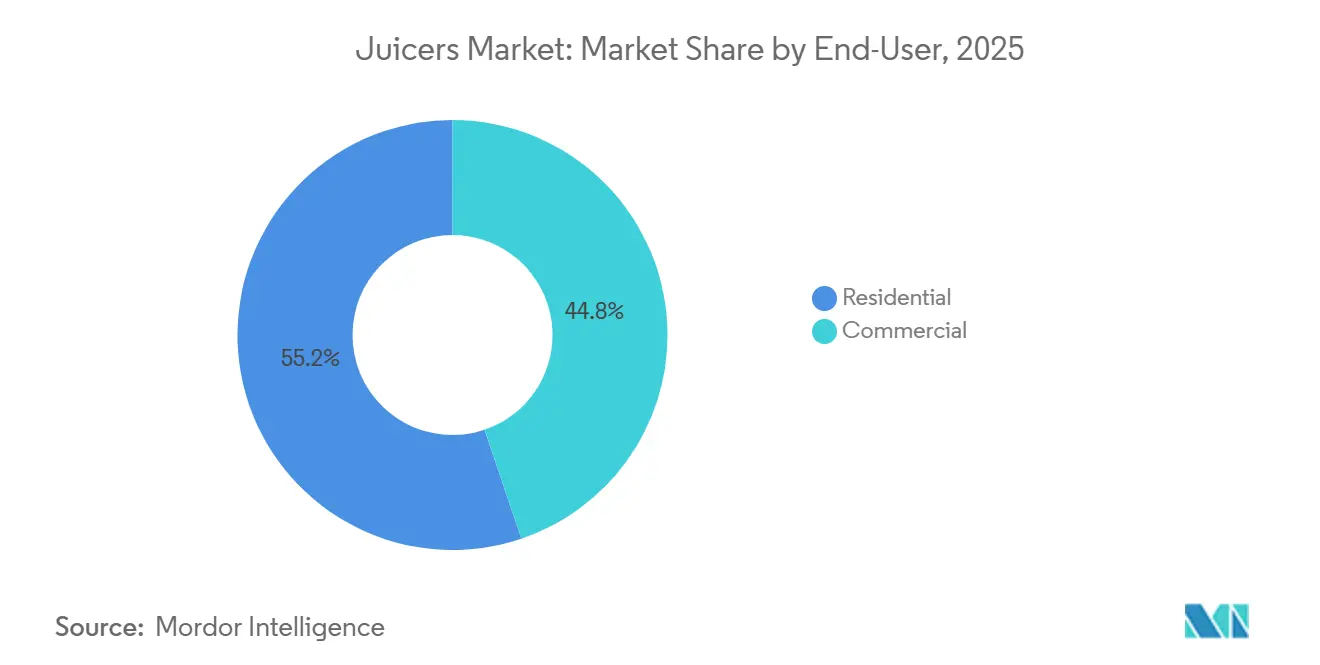

- By end-user, residential held 55.21% of the juicers market size in 2025. The commercial segment is forecast to expand at a 5.12% CAGR to 2031.

- By distribution channel, specialty stores led with a 26.91% share in 2025. Online retail is the fastest-growing channel at a projected 6.45% CAGR to 2031.

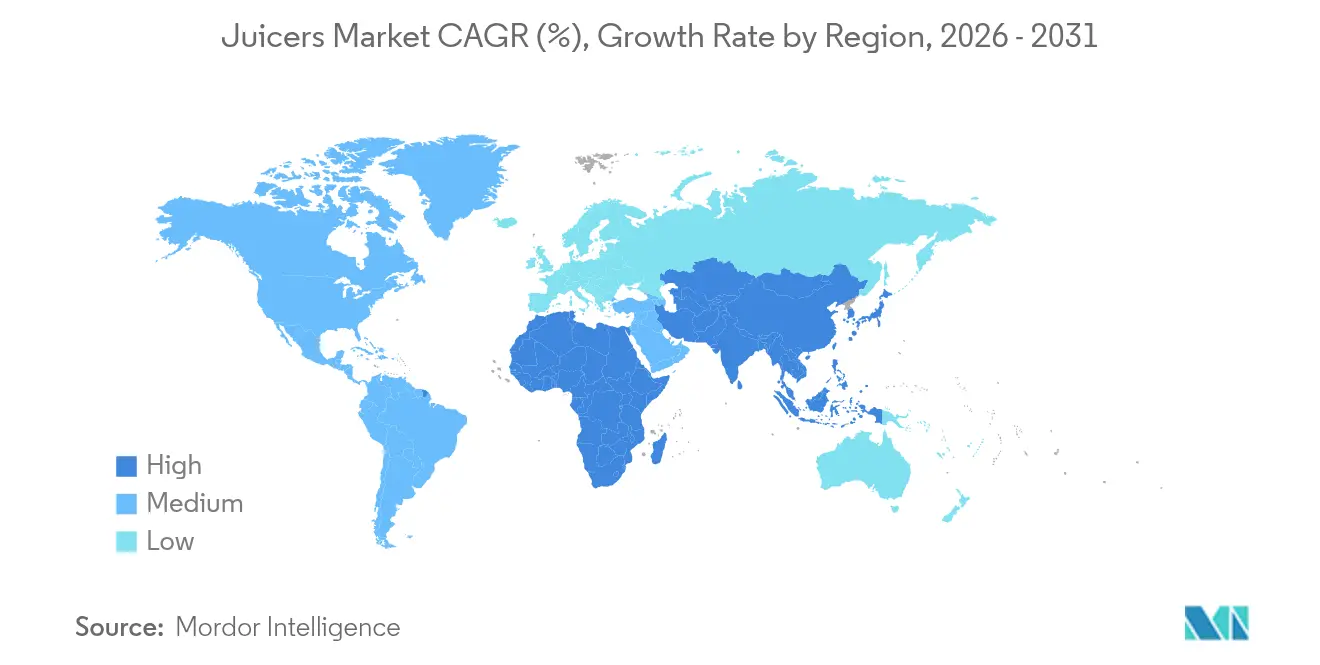

- By geography, Europe held a 21.26% share in 2025. Asia-Pacific is the fastest-growing region with a 6.92% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Juicers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-conscious consumption is pushing home juicing and cold-press adoption | +1.8% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Electric-convenience preference sustaining upgrade cycles across mid-price bands | +1.2% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Modern retail breadth and e-commerce fulfillment are improving access and promotions | +1.0% | Asia-Pacific core, spill-over to MEA | Short term (≤ 2 years) |

| EU Right to Repair spurring durable, repairable designs and aftersales ecosystems | +0.6% | Europe has, secondary influence on North America | Medium term (2-4 years) |

| Food-contact chemical restrictions are accelerating the shift to BPA-free or Tritan and steel | +0.4% | Europe and North America, with gradual Asia-Pacific adoption | Medium term (2-4 years) |

| Expansion of juice bars and on-premises beverage programs in QSR | +0.5% | North America and Europe, emerging in urban Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health-Conscious Consumption Pushing Home Juicing and Cold-Press Adoption

Households continue to prioritize wellness routines, which sustains interest in fresh juice preparation at home and supports premium models that preserve nutrients at lower heat and oxidation. Fresh juice programs also expand in foodservice, a trend supported by equipment makers that publish throughput and yield gains for commercial operators who emphasize freshness. As this preference for less processed beverages matures, the juicers market finds recurring demand from consumers who want higher yields and clarity about ingredient quality. Nutrient preservation narratives also align with stricter food-contact standards in major markets, which reinforces a premium tilt in materials and component choices. These preferences encourage brands to improve auger design, filtration geometry, and flow paths that minimize heat build-up while maintaining convenience in everyday use. The result is a clear emphasis on models that balance gentle extraction with fast cleaning routines to support daily consumption.

Electric-Convenience Preference Sustaining Upgrade Cycles Across Mid-Price Bands

Electric formats continue to anchor the juicers market because one-touch operation, safety interlocks, and variable speeds fit the needs of time-pressed urban households. Recent product cycles emphasize automated cleaning and smart pulp ejection to reduce post-use effort, a design shift highlighted in new launches from established brands that position ease of maintenance as a top-tier feature for repeat use. Right to Repair rules in Europe reinforce this direction by encouraging modular motor assemblies and field-replaceable parts so products remain in service longer at reasonable cost. The combination of convenience and repairability allows brands to stretch replacement cycles while protecting brand equity through long-lived assemblies. In parallel, the juicers market shows steady adoption of premium materials in contact zones to withstand acidic ingredients and maintain optical clarity under repeated cleaning[2]Eastman, “Tritan Renew Copolyester for Durable Consumer Goods,” Eastman Chemical Company, eastman.com . These engineering choices support reliable uptime and smooth user experiences that keep electric units at the center of upgrade decisions.

Modern Retail Breadth and E-Commerce Fulfillment Improving Access and Promotions

Digital channels remain a growth engine for the juicers market as online platforms simplify comparison shopping and deliver broader assortments with dynamic pricing and rich content. In the United States, online accounted for a large share of small kitchen appliance retail in 2025 and is expanding at a healthy pace through 2031, which sustains discovery and replenishment behavior for premium products. Brands are investing in product pages with videos, assembly walkthroughs, and hygiene features that reduce perceived risk at checkout. Promotions remain frequent across major retail events, which shift category mix toward better-featured SKUs that can defend price points even when discounts are common. The juicers market benefits from ratings and reviews that highlight real-world cleanability and noise levels, two attributes that drive repeat usage. Fulfillment speed and simple returns policies complete the bundle that moves first-time buyers into the category, and nudges repeat upgrades on predictable cycles.

EU Right to Repair Spurring Durable, Repairable Designs and Aftersales Ecosystems

The European Union’s Right to Repair framework requires manufacturers to provide repairs within a reasonable time and at reasonable prices and extends warranty coverage by twelve months when the consumer chooses repair during the original period, which directly influences small appliance design choices. Product roadmaps now emphasize modularity in motors, gear trains, and control boards so common failures can be addressed without replacing entire units. This shift aligns the juicers market with service-friendly architectures that keep products in households longer and reduce e-waste. It also changes the economics of spare parts management as brands plan multi-year stocking and service documentation that supports authorized networks. Parallel moves in intellectual property, such as patent enforcement by premium slow-juicer brands in Europe, reinforce differentiation around wide chutes, drive systems, and automated feeding that raise yield and convenience. Over time, these repairability and IP trends concentrate value creation in designs that can be serviced and upgraded rather than discarded.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cleaning complexity and time burden limit repeat usage and purchase intent | -0.7% | Global, particularly acute in Asia-Pacific urban markets | Short term (≤ 2 years) |

| Raw material and component cost volatility is raising retail prices and dampening demand | -0.5% | Global, the strongest impact in North America and Europe | Medium term (2-4 years) |

| WEEE or EPR compliance adds take-back, labeling, and recycling costs in core markets | -0.3% | Europe, expanding to North America | Medium term (2-4 years) |

| Ready-to-drink juices and multifunction blenders | -0.4% | Global, especially mature markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cleaning Complexity and Time Burden Limiting Repeat Usage and Purchase Intent

Consumer feedback often centers on the time and effort required to disassemble, clean, and reassemble juice extraction components after each use. Manufacturers respond with automated rinse modes, simplified baskets, and smart pulp ejections that limit hand scrubbing and reduce residue build-up during back-to-back servings. Recognition for specific products highlights progress in ease-of-use and cleaning, which signals to buyers that trade-offs between yield and maintenance are narrowing. These improvements are most salient for slow-juicer formats where fine screens and augers trap fibrous material. Despite upgrades, part counts, and mesh cleaning still deter some households from daily use, which depresses repeat-usage rates over time. The juicers market, therefore, places cleanability and part durability at the center of its design and messaging strategies to address this behavioral barrier.

Raw Material and Component Cost Volatility Raising Retail Prices and Dampening Demand

Volatility in input costs for steel, copper, and electronic components puts pressure on retail pricing and promotional schedules for appliance categories. Stainless steel grades used in cutting elements and filter baskets have shown meaningful price swings, which complicates cost planning for mid-price models. Shipping and logistics conditions that remain above pre-2019 baselines keep landed costs elevated for many import-dependent markets. These factors can compress margins or force price increases that reduce demand at entry points where consumers are most price sensitive. Conversely, premium units that advertise long life and serviceable assemblies can defend price points better when buyers evaluate the total cost of ownership. The juicers market continues to balance pricing discipline with feature upgrades as suppliers manage materials and freight variability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Masticating Models Leverage Nutrient Claims Despite Centrifugal Reach

Centrifugal juicers commanded 44.14% of the juicers market size in 2025, supported by their faster extraction process, affordability, and suitability for everyday household use. Meanwhile, masticating and triturating juicers accounted for 6.81% of the market share in 2025, driven by rising consumer preference for higher juice yield, nutrient retention, and cold-press juicing technology. Entry-level centrifugal designs remain the most broadly distributed and are often the first step into the category through general merchandise and grocery channels. Premium masticating models continue to grow based on yield and nutrient preservation claims that resonate with wellness-focused buyers who accept slower cycles for better output quality. Awards and product recognition reinforce these perceived benefits, which help newcomers understand the value of wide chutes, optimized augers, and easy-clean strainers. Twin-gear triturating formats serve enthusiasts who want maximum extraction and low oxidation in leafy greens and fibrous produce, although assembly complexity and price concentrate adoption among hobbyists.

Commercial-grade citrus units targeting hotels, cafes, and convenience formats demonstrate how specialized designs serve high-volume use cases where reliability and throughput define payback[3]JBT Corporation, “Commercial Citrus Juicing Systems,” JBT Corporation, jbtc.com . As adoption spreads, the juicers market continues to split by use case, with centrifugal models anchoring volume sales and masticating models increasing value share by pairing quiet operation with cleaner juice profiles. Brands focus on stronger drive units, reinforced screens, and smoother pulp paths to reduce friction that might otherwise cause returns. This approach positions slow-juicer formats as credible upgrades in households that seek longevity and service support. Masticating and triturating offerings now emphasize simple part geometry, tool-free disassembly, and dishwasher-safe bowls to address cleaning hurdles. This reduces after-use barriers that previously limited weekday adoption. In parallel, centrifugal lines are improving the precision of cutting baskets and balancing for lower vibration, which makes them feel more premium in daily use. The juicers market also sees standardization around pulp channels and juice spouts that resist clogging across fruit densities. Over time, the incremental engineering of these touchpoints can shift purchasing from first-cost to life-cycle value. That shift sets the stage for periodic upgrades centered on quieter motors and better filtration rather than raw speed alone.

By Category Type: Electric Variants Sustain Share Through Convenience and Smart Features

Electric juicers commanded 79.91% of the juicers market size in 2025 and are projected to sustain a 4.97% CAGR to 2031 as households prioritize one-touch operation, consistent speed control, and safety interlocks. Product updates now include automated rinse modes and smarter pulp ejection, so users spend less time scrubbing mesh, which improves satisfaction and repeat use across the ownership cycle. Manual presses hold a role in low-electricity or outdoor contexts, yet most new buyers who value convenience shift into electric at the first upgrade. As compliance regimes expand in Europe, brands align electric designs to repairability norms through modular motors and accessible control boards. Clear material disclosure and food-contact safety claims also feature more heavily in product pages to reduce perceived risk from plastics in daily juice preparation. The result is a steady innovation cadence where cleaning, serviceability, and compliance messaging support a durable share in electric models.

Within the electric, premium sub-segments compete on lower noise and precise speed mapping for leafy greens, citrus, and hard roots. Manufacturers communicate life expectancy and service paths to justify higher price points and reduce anxiety about replacement timing. The juicers market sees the adoption of high-clarity copolyesters and stainless steel for contact parts to improve strength under acidic conditions and repeated dishwasher exposure. These material choices strengthen the case for longer ownership, which aligns with repair-friendly regulations. Retailers in digital channels surface these features through side-by-side comparison tools and verified reviews that specifically mention cleaning and durability, two attributes that influence conversion. Over the forecast, the balance of simplicity and robust materials continues to anchor electric as the default choice for broad household adoption.

By End-User: Commercial Segment Outpaces Residential Through Beverage Expansion

Residential end-users accounted for 55.21% of the juicers market size in 2025 as health-oriented routines and at-home preparation habits remained popular after the pandemic period. The commercial segment is set to grow at 5.12% CAGR through 2031 as juice bars, cafes, and quick-service restaurants add fresh options that command meaningful premiums and expand daypart traffic. Equipment makers publish throughput and yield advantages that compress payback periods, which encourages broader menu placement in high-volume locations. Feature sets in commercial units focus on self-clean routines, rugged strainers, and drive trains built for continuous use. In turn, those design choices filter down into top-tier residential models marketed for longevity and low maintenance. This linkage gives consumers more confidence to invest in higher-spec units that promise daily convenience without heavy cleaning.

Operators in foodservice environments weigh up time and cleaning speed heavily because idle minutes reduce revenue. Commercial launches now emphasize easy disassembly and automated rinsing that keeps units ready between orders. Residential buyers notice these technologies through store demos and online content that show faster cleanup. The juicers market, therefore, positions cleaning and reliability as common advantages that address both home and away-from-home use. Over time, repairable assemblies and documented spare parts paths will win favor in both segments since they protect lifetime value. These dynamics keep premium models at the center of category growth while entry models support ongoing household trial.

By Distribution Channel: Online Retail Captures Share Through Assortment Depth and Content

Online retail continues to expand faster than other channels in the juicers market as shoppers compare features, read reviews, and access broader assortments in one session. In the United States, online sales captured a large share of small appliance sales in 2025 and are set for sustained growth through 2031, which positions digital discovery as the primary path into premium models. Specialty stores remain important for in-person trials and explainers on cleaning and service paths. Supermarkets and hypermarkets provide seasonal lifts tied to wellness periods that highlight starter models and bundled accessories. The digital shelf complements these pushes by hosting how-to content that lowers first-use friction.

Brands coordinate pricing and fulfillment across channels to avoid consumer confusion and protect premium positioning. Omnichannel options such as same-day pickup help neutralize delivery gaps and appeal to buyers who want immediate ownership. The juicers market also benefits from social proof as verified ratings highlight noise, cleaning, and materials, which can make or break premium purchase decisions. In emerging markets where digital payments broaden, online becomes a primary route for first-time buyers who want selection breadth without long travel. These shifts support a structural tilt toward digital even as stores keep a role in education and service support.

Geography Analysis

Europe held 21.26% of the juicers market size in 2025 as premium twin-gear and masticating formats aligned with wellness trends and rising attention to repairability. The EU Right to Repair framework, transposed by July 31, 2026, requires reasonable repair options, spare parts access, and warranty extension when repair is chosen during the original coverage period, which reinforces modular design and longer lifecycles. A separate EU regulation in force since January 2025 restricts bisphenols in food-contact materials, which accelerates the shift to BPA-free polymers and stainless steel in contact pathways. Producer responsibility rules under WEEE add registration, labeling, and take-back obligations that favor brands with established reverse logistics and recovery partners. Program updates for online marketplaces tighten oversight for third-party sales into the region, raising compliance needs for cross-border shipments. Input cost movements in stainless steel influence pricing strategies for mid-range SKUs that depend on mesh and blade assemblies made from steel grades tuned for corrosion resistance. These regulatory and cost inputs reinforce a premium and compliance-forward approach that shapes product choices, messaging, and service depth in Europe.

Asia-Pacific is the fastest-growing region at a 6.92% CAGR during 2026 to 2031 as rising incomes, digital retail access, and health-seeking behaviors bring first-time buyers into the category. Local manufacturing capabilities across major appliance hubs support competitive pricing, while digital discovery compresses the time from research to purchase. Premium slow-juicer formats gain traction in dense urban centers where wellness cues are strong, and consumers prioritize yield and taste clarity. Entry-level centrifugal units continue to support household trial, after which buyers migrate to masticating models when cleaning and noise improvements feel meaningful. The juicers market in Asia-Pacific also benefits from retailer education that showcases side-by-side comparisons of juice yield and oxidation control, which makes performance differences easier to understand.

North America shows steady upgrade cycles in both residential and commercial settings as consumers trade up to quieter and easier-to-clean models. Digital retail accounts for a large and growing share of small kitchen appliance sales in the United States, which channels discovery into premium features and durable assemblies. Commercial demand focuses on uptime, cleaning simplicity, and consistent output, where operator economics depend on speed and yield. In the Middle East and Africa, import dependence remains high for small appliances, which makes pricing sensitive to freight conditions and currency movements. Gradual emergence of local assembly in select markets aims to mitigate these swings over time. The juicers market continues to scale through online education, warranty clarity, and availability of spare parts, which helps address hesitations in regions where service infrastructure is still developing.

Competitive Landscape

The juicers market is highly fragmented. Competitive intensity is shaped by a broad set of international and regional brands that pursue different playbooks around design, materials, and service. Large appliance players leverage retail reach and established after-sales networks to compete with convenience and value within the juicers market. Specialists in premium slow-juicer formats focus on nutrient preservation, low oxidation, quieter operation, and easy-clean designs that maintain performance while cutting maintenance time. Commercial suppliers prioritize rugged assemblies and self-clean features that reduce downtime in high-traffic locations. Reputation in cleaning performance and serviceability is a core differentiator in both home and commercial segments. Over time, material choices and compliance clarity are becoming as important as speed or juice yield in purchase decisions.

Specific product moves show an industry leaning into performance and service life. A notable commercial launch improved citrus throughput and yield, which clarifies payback logic for operators adding fresh juice to menus. Premium slow-juicer brands continue to enforce IP rights around wide-feed and hands-free innovations to protect distinct design advantages in Europe[4]Kuvings, “Patent Protection and Product Innovations,” Kuvings, kuvings.com . Some consumer models have been recognized for convenience and performance, which signals that cleaning and ease-of-use gains are reaching buyers and reviewers who shape perception. Commercial line expansions also target energy use and uptime as input costs and labor conditions evolve for foodservice operators. Taken together, these moves highlight cleaning simplicity, reliability, and compliance-ready materials as levers to win share in the juicers market.

Regulatory developments and material transitions shape long-term strategies. Right to Repair requirements in Europe favor brands that document repair procedures and ensure multi-year access to spare parts through authorized networks. Food-contact restrictions accelerate the adoption of BPA-free copolyesters and stainless steel, with suppliers underscoring chemical resistance and recycled content credentials where feasible. These themes align with owner expectations for safe materials and fair service paths across product life. The juicers market will likely reward companies that pair smart self-cleaning, repairable assemblies, and clear compliance disclosures with competitive pricing and strong retail education. This combination positions leaders to defend premium price points and reduce returns, while enabling new entrants to focus on differentiated cleaning and material claims to establish credibility.

Juicers Industry Leaders

Breville Group Limited (Sage in Europe)

Versuni (Philips Domestic Appliances) – Philips-branded juicers

Hurom Co., Ltd.

Kuvings (NUC Electronics)

Hamilton Beach Brands Holding Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Panasonic Corporation showcased compact, high-speed commercial juicers in Japan, featuring automated pulp ejection and IoT-enabled maintenance alerts designed for high-throughput food-service environments, reflecting the company's push into the commercial segment where equipment uptime directly impacts revenue.

- February 2026: Kuvings (NUC Electronics) successfully concluded participation in Ambiente 2026, held January 29, 2026, where it showcased the AUTO10S hands-free slow juicer. The company also presented the AUTO10 Plus at The Inspired Home Show 2026 in Chicago on February 24, 2026, reinforcing its strategy to leverage trade shows for commercial-buyer discoveries despite representing under 5 percent of unit volumes.

- October 2025: JBT Marel launched the Fresh'n Squeeze 1800 Citrus Juicer, capable of extracting 50 ounces per minute and yielding 50 percent more juice per orange, targeting commercial citrus programs where labor costs and waste reduction deliver payback in fewer than nine operating days for a USD 2,000 unit.

- November 2024: Hurom Co., Ltd. received recognition from Forbes, which named the H400 "Best Kitchen Product 2024," following the H200's "Best Juicer Overall" award in 2023 and the E50ST's 2025 Red Dot Design Award, reinforcing the brand's premium positioning and design-led differentiation.

Global Juicers Market Report Scope

Home gadgets called juicers are used to extract juice from fruits and vegetables. The device extracts fresh fruit or vegetable juice by pressing or crushing the produce through a mesh filter and separating the pulp from the liquid. The global juicers market report focuses on the market dynamics, trends, and demand for juicers in the market. The report offers an in-depth analysis of the key trends, segments, opportunities, and factors that are driving the market. Additionally, the key profiles of the major players in the global market are provided in detail.

The Juicers Market is segmented by type, category type, end user, distribution channel, and geography. By type, the market is divided into centrifugal juicers, masticating juicers, triturating juicers, and others. By category type, the market is categorized into manual juicers and electric juicers. By end user, the market is segmented into residential and commercial segments. By distribution channel, the market is divided into supermarkets/hypermarkets, specialty stores, online, and other distribution channels. Geographically, the market analysis covers North America, South America, Europe, Asia-Pacific, and the Middle East & Africa. The report provides market size and forecasts for the juicers market in value (USD) across all the above segments.

| Centrifugal Juicer |

| Masticating Juicer |

| Triturating Juicer |

| Others |

| Manual Juicers |

| Electric Juicers |

| Commercial |

| Residential |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online |

| Other Distribution Channels |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Type | Centrifugal Juicer | |

| Masticating Juicer | ||

| Triturating Juicer | ||

| Others | ||

| By Category Type | Manual Juicers | |

| Electric Juicers | ||

| By End-User | Commercial | |

| Residential | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the size and growth outlook for the juicers market to 2031?

The juicers market size was USD 4.5 billion in 2025 and is projected to reach USD 5.85 billion by 2031 at a 4.46% CAGR over 2026 to 2031.

Which region is expected to grow fastest in the juicers market?

Asia-Pacific is the fastest-growing region with a 6.92% CAGR through 2031, supported by rising incomes, digital retail access, and health-seeking behavior.

What regulatory shifts are most relevant to juicers design and materials?

The EU Right to Repair framework and new restrictions on bisphenols in food-contact materials are reshaping design for repairability and accelerating the adoption of BPA-free polymers and stainless steel.

How are commercial use cases influencing the juicers market?

Food service adoption is rising as new citrus systems demonstrate higher throughput and yield, improving payback and pushing design improvements that later reach residential models.

What features most affect buying decisions for premium juicers?

Cleaning simplicity, materials in contact zones, quiet operation, and clear service paths are the attributes that most often sway premium buyers in the juicers market.

Page last updated on: