Biofilm Coated Paperboard Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

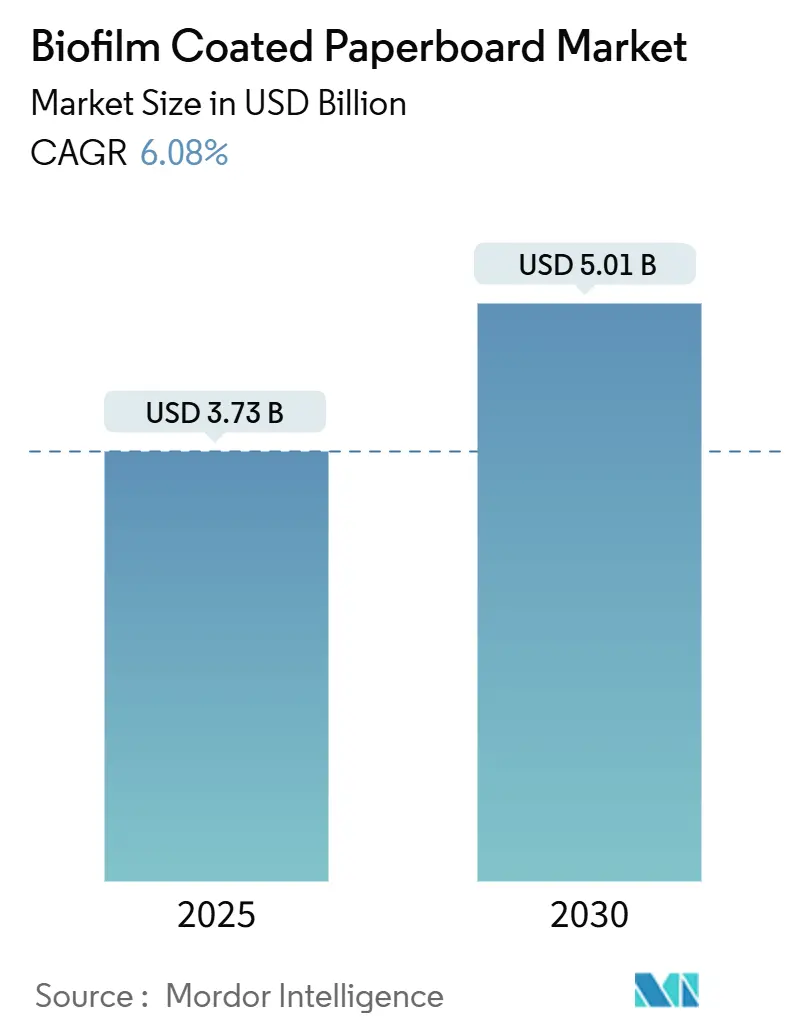

| Market Size (2025) | USD 3.73 Billion |

| Market Size (2030) | USD 5.01 Billion |

| Growth Rate (2025 - 2030) | 6.08% CAGR |

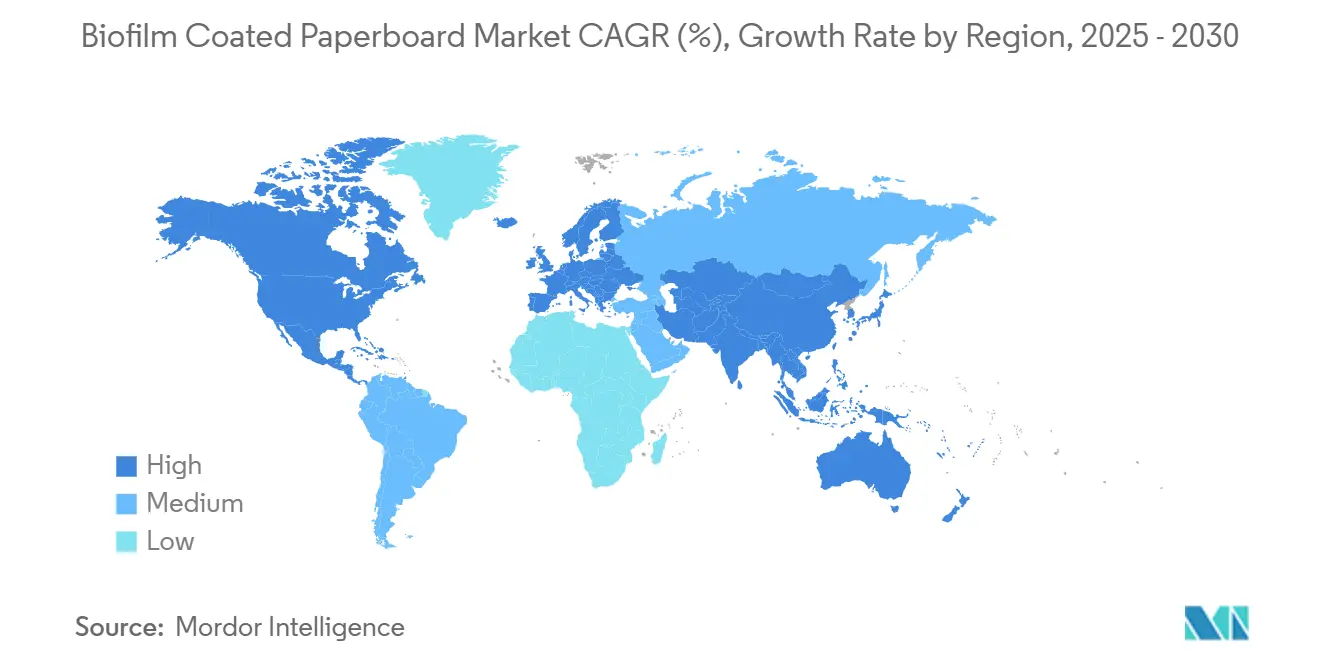

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biofilm Coated Paperboard Market Analysis by Mordor Intelligence

The biofilm coated paperboard market size reached USD 3.73 billion in 2025 and is forecast to rise to USD 5.01 billion by 2030, reflecting a 6.08% CAGR. Demand is propelled by the complete phase-out of PFAS grease-proofing substances in the United States, parallel restrictions in the European Union, and corporate commitments to recyclable or compostable packaging. Brand owners are accelerating material substitution, municipal composting mandates are widening, and e-commerce grocery volumes are lifting requirements for moisture-resistant fiber solutions that can be recycled or industrially composted. On the supply side, rapid scaling of PLA and emerging PHA capacity is narrowing the cost gap with polyethylene coatings, while converters experiment with dispersion techniques that lower complexity relative to legacy extrusion. At the same time, investors channel capital into integrated substrate-plus-coating assets that can deliver barrier performance without fluorochemicals and meet rising lifecycle scrutiny.

Key Report Takeaways

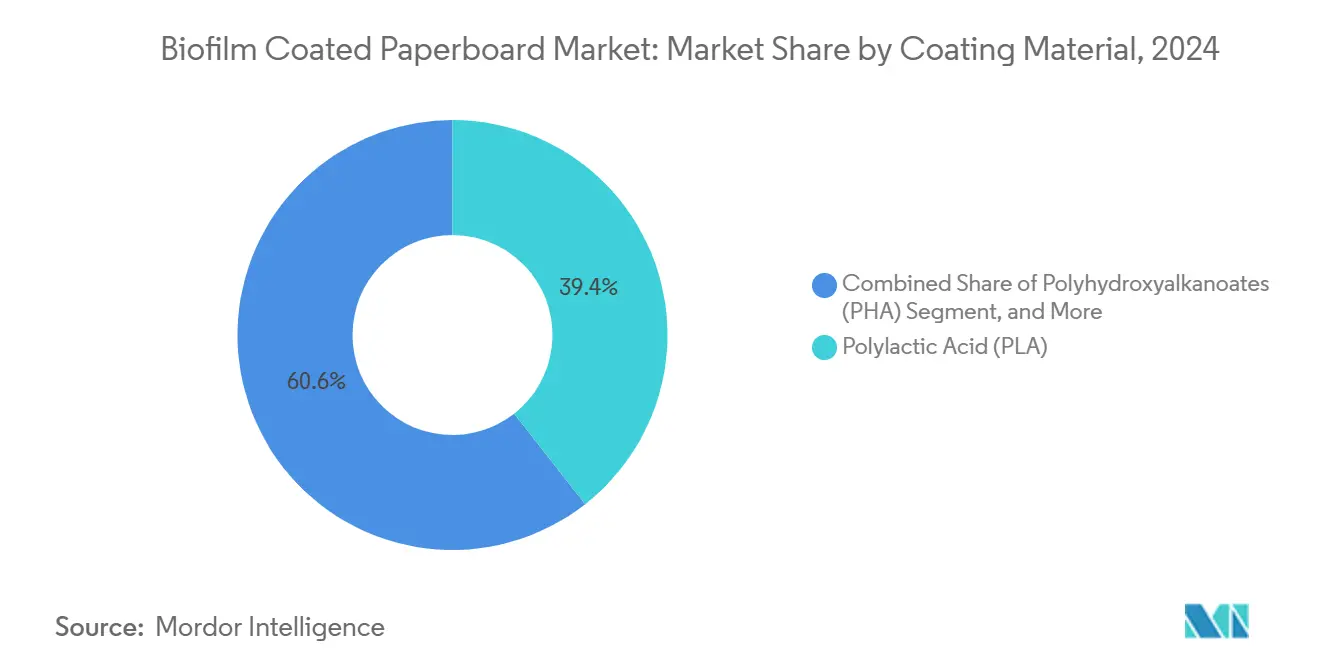

- By coating material, polylactic acid captured 39.42% of the biofilm coated paperboard market share in 2024.

- By paperboard grade, the biofilm coated paperboard market size for folding boxboard is projected to grow at a 6.43% CAGR between 2025-2030.

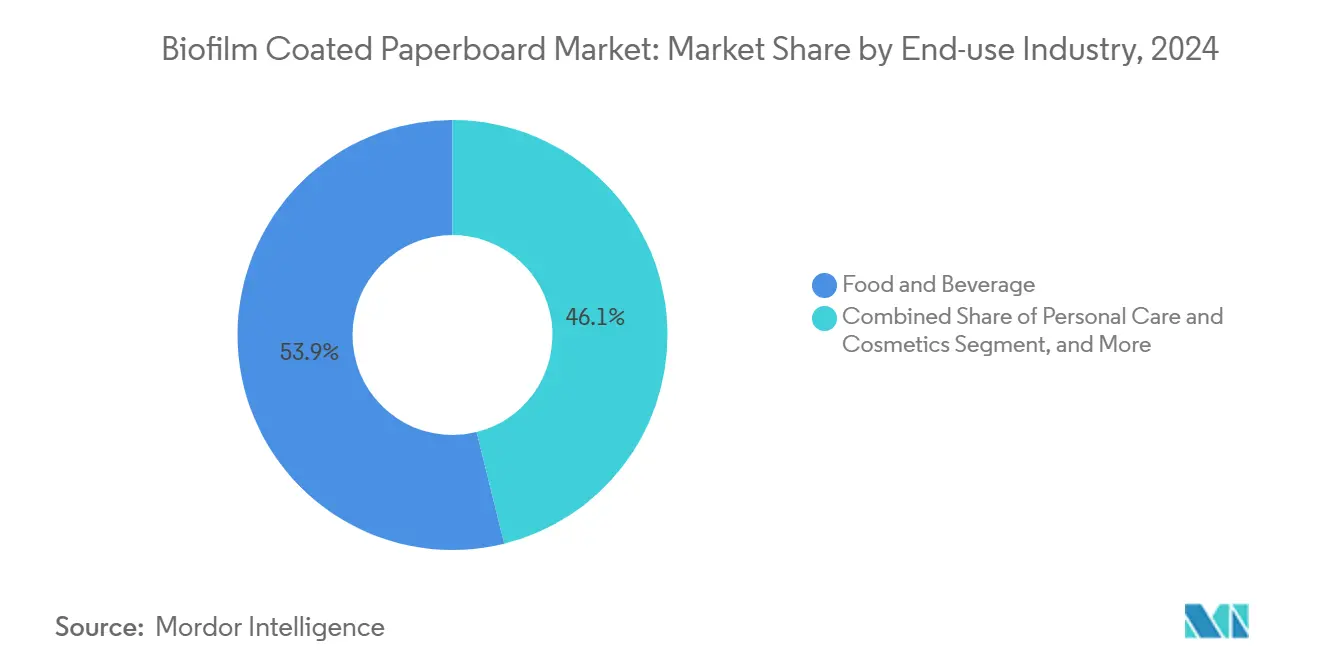

- By end use, food and beverage captured 53.86% of the biofilm coated paperboard market share in 2024.

- By coating method, the biofilm coated paperboard market size for dispersion/curtain coating is projected to grow at 6.17% CAGR between 2025-2030.

- By region, Europe captured 36.94% of the biofilm coated paperboard market share in 2024.

Global Biofilm Coated Paperboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for compostable food-service packaging | +1.2% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Brand owner commitments to 100% recyclable packaging by 2030 | +1.0% | Global, led by multinational consumer goods companies | Long term (≥ 4 years) |

| Regulatory bans on PFAS-lined paperboard | +1.5% | North America and EU core, expanding to APAC | Short term (≤ 2 years) |

| Cost parity improvements in bio-coating resins | +0.8% | Global manufacturing hubs, particularly APAC | Medium term (2-4 years) |

| Growth of e-commerce grocery requiring moisture-resistant board | +0.7% | North America and APAC, with EU following | Medium term (2-4 years) |

| Breweries shifting to fibre-based multipacks | +0.4% | Europe and North America, selective APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Compostable Food-Service Packaging

Mandates in major U.S. cities require certified compostable serviceware, turning quick-service restaurants into early adopters of bio-coated formats. Extended Producer Responsibility laws in California and Washington impose fees linked to packaging end-of-life outcomes, reinforcing the shift toward fiber substrates that can enter municipal organics programs. Certifications from the Biodegradable Products Institute have become de-facto spec-sheet requirements, giving compliant mills a pricing premium that offsets bio-resin costs. European municipalities mirror the trend through source-separated organics collection, while Canadian provinces incorporate compostability metrics into single-use packaging guidelines. Together these policies underpin consistent volume growth for compostable cups, clamshells and wraps, all reliant on grease and moisture barriers delivered by plant-based coatings.

Brand Owner Commitments to 100% Recyclable Packaging by 2030

Global consumer-goods companies embed recyclability targets into annual incentive structures and supplier scorecards. Procter & Gamble ties executive remuneration to absolute emissions cuts and packaging footprint reductions. Coca-Cola’s pledge for 100% recyclable packaging by 2025 cascades through contract manufacturers, who must now validate material circularity in every procurement tender. Retailers such as Walmart incorporate recyclability thresholds into category line reviews, effectively pushing brand-owner requirements onto private-label vendors. The cumulative buying power of these multinationals assures scale for biofilm coated paperboard market offerings even before full regulatory enforcement arrives.

Regulatory Bans on PFAS-Lined Paperboard

The U.S. FDA has revoked 35 Food Contact Notifications covering fluorinated grease-proofing agents, with a sell-through deadline of June 2025.[1]Human Foods Program, “Market Phase-Out of Grease-Proofing Substances Containing PFAS,” FDA, fda.gov Simultaneously, upcoming EU rules cap individual PFAS at 25 ppb in food packaging, ending the practice of relocating production to laxer regions. Because compliance failure can lead to import blocks, global food brands are standardising on single material solutions that satisfy every jurisdiction. This harmonisation directly accelerates adoption of bio-coating platforms such as PLA and PHA that already possess Generally Recognized as Safe (GRAS) status for food contact.

Cost Parity Improvements in Bio-Coating Resins

Scale economics have lowered industrial PLA production costs by more than 25% since 2020, driven by sugar-to-PLA conversion efficiencies now at 1.6 kg to 1 kg output.[2]TotalEnergies Corbion, “Sustainable Sourcing of Feedstocks for Bioplastics,” totalenergies-corbion.com PHA processes tapping micro-algal feedstocks promise further gains because of high lipid content and on-site CO₂ utilisation, insulating resin costs from agricultural commodity swings. Capital outlays for dispersion coating lines are falling as equipment vendors commercialise retrofit modules compatible with existing paperboard machines, eroding the price advantage enjoyed by polyethylene extrusion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited industrial composting infrastructure | -0.9% | Global, with acute gaps in developing markets | Long term (≥ 4 years) |

| Higher converting complexity versus extrusion PE | -0.6% | Global manufacturing centers | Medium term (2-4 years) |

| Supply volatility of plant-based feedstocks | -0.5% | Global, concentrated in agricultural regions | Short term (≤ 2 years) |

| Barrier-performance gaps vs. fluorochemicals | -0.7% | Global, critical in high-performance applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Industrial Composting Infrastructure

The U.S. EPA estimates a USD 36–43 billion funding gap to modernise the nation’s recycling and organics processing network. Rural areas lack commercial composters, so compostable cups often end in landfills where anaerobic conditions slow degradation. Europe enjoys denser collection coverage but still faces contamination challenges that raise gate fees. Developing regions have even thinner infrastructure, curbing near-term demand for compostable bio-coated grades. Without predictable end-of-life pathways, brand owners risk greenwashing accusations, complicating portfolio decisions.

Higher Converting Complexity Versus Extrusion PE

Bio-coated products often need tighter process windows. PHBV, for instance, requires precise temperature profiling and plasticiser control to achieve a sub-10 µm layer with adequate bond strength. Converters lacking capital for infrared dryers or corona treatment upgrades cannot guarantee run-speed efficiency. The incremental set-up time raises operating costs and discourages small and mid-size firms from switching away from polyethylene, dampening uptake among fragmented converter bases in Asia and Latin America.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coating Material: PLA Dominance Faces PHA Challenge

PLA accounted for 39.42% of the biofilm coated paperboard market in 2024 thanks to established resin supply chains, existing FDA clearances, and converter familiarity. The segment is valued at USD 1.47 billion in 2025, and its biofilm coated paperboard market size for PLA coatings is projected to reach USD 1.85 billion by 2030. However, growth moderates to a 5.3% CAGR as brand owners diversify toward more readily biodegradable solutions.

PHA remains a smaller base yet is forecast to record a 7.02% CAGR, placing its 2030 revenue at USD 640 million. Demand benefits from marine-safe claims and burgeoning Asian fermentation capacity. Starch blends serve cost-sensitive applications, while cellulose films maintain niche usage where print fidelity is paramount. Other oligomeric coatings, including PBS and PEF, address speciality oxygen-barrier needs but are constrained by limited resin output.

By Paperboard Grade: SBS Leadership Under FBB Pressure

Solid Bleached Sulfate held 44.71% share of the biofilm coated paperboard market size in 2024, equal to USD 1.67 billion. High brightness and smoothness make SBS the default for premium retail packs. Capacity additions such as Stora Enso’s Oulu conversion will reinforce supply. Yet Folding Boxboard, valued at USD 820 million in 2025, advances at a 6.43% CAGR as grocery e-commerce favours its stiffness-to-weight ratio. Coated Unbleached Kraft retains industrial end-uses, whereas White Top and specialty grades fill regional or functional niches. Producers continue light-weighting across all grades to mitigate fiber cost and meet carbon-reduction goals.

By End-use Industry: Food-Service Surges

Food and Beverage generated USD 2.01 billion in revenue in 2025, leveraging deep relationships between integrated mills and multinational consumer-goods firms. Its long production runs favour extrusion coating. Still, Food-service shows stronger momentum, moving from USD 950 million in 2025 toward USD 1.33 billion by 2030 on a 6.94% CAGR. Quick-service restaurant cups, trays and wraps all face PFAS removal deadlines, and certified compostability brings an upsell margin rarely available in retail channels. Personal Care, Household and Industrial Goods remain exploratory spaces, though upscale cosmetic brands deploy bio-coated cartons to align with clean-beauty positioning.

By Coating Method: Extrusion Retains Scale Advantage

Extrusion controlled 59.63% of the 2024 revenue pool owing to ubiquitous line installations and decades of operator know-how. The segment accounts for USD 2.22 billion of the biofilm coated paperboard market size in 2025. However, dispersion and curtain systems are projected to trim extrusion’s share below 55% by 2030 as converters prioritise lower oven temperatures and enhanced repulpability. Laminating keeps a foothold in multilayer barrier structures such as retort pouches but suffers from higher unit costs and recyclability concerns.

Geography Analysis

Europe contributed USD 1.38 billion in 2025, commanding 36.94% of global revenue, buoyed by PFAS limits set for August 2026 and landfill taxes that penalise plastic-polyethylene composites.[3]RRMA, “EU Packaging Law to Impose Strict PFAS Restrictions,” rrma-global.org Producers such as Stora Enso and Smurfit WestRock invest in on-site bio-coating assets to secure integrated supply and cut freight emissions. Retailers add fibre scorecards to private-label tenders, accelerating material migration even in price-sensitive value chains. The region also benefits from mature kerbside collection and growing anaerobic digestion capacity that can process certified compostable board.

Asia-Pacific is the fastest climber, rising from USD 920 million in 2025 to a projected USD 1.34 billion by 2030 on a 7.78% CAGR. E-commerce grocery networks expand cold-chain capabilities, and breweries in Japan, South Korea and Australia adopt fiber multipacks to comply with plastic-ring bans. China’s five-year plan references “white pollution” mitigation, encouraging city-level pilots that restrict single-use plastics in food delivery. Meanwhile, Thailand and Indonesia incentivise bio-based resin plants through tax holidays, giving regional converters local supply of PLA and PHA at competitive pricing.

North America continues steady growth, supported by FDA PFAS withdrawal and state-level composting mandates. Market expansion moderates after the 2025 compliance spike, yet ongoing investment in organics processing will gradually unlock rural adoption. Latin America and the Middle East & Africa lag, held back by currency volatility and insufficient waste infrastructure, though multinational beverage brand trials suggest an eventual tipping point once local composting capacity materialises.

Competitive Landscape

The top five suppliers, Stora Enso, Smurfit WestRock, Graphic Packaging International, Metsä Board, and Mondi, controlled nearly 60% of installed coating capacity in 2024, reflecting a moderately concentrated structure. Stora Enso is ploughing EUR 1 billion into Oulu to lift premium SBS output, signalling faith in long-run fibre substitution even amid short-term resin volatility. Smurfit WestRock’s USD 400 million synergy program focuses on harmonising sustainability standards across its merged footprint, enabling platform selling of PFAS-free boards. Graphic Packaging has allocated USD 1 billion for a Waco recycled paperboard mill capable of inline dispersion coating to meet circular-economy scorecards.

Mid-tier mills pursue licensing deals with bio-resin developers to differentiate via proprietary barrier recipes. Start-ups like Melodea commercialise cellulose nanocrystal coatings compatible with curtain processes, aiming to close oxygen- and fat-barrier gaps versus fluorochemicals. Equipment vendors develop hybrid lines that toggle between extrusion and water-based modes, letting converters match coating method to order profile without incremental floor space. M&A activity stays focused on vertical plays; no pure-play bio-coating company has yet reached IPO scale.

Biofilm Coated Paperboard Industry Leaders

Stora Enso Oyj

Smurfit WestRock plc

Metsa Group

Graphic Packaging International, LLC

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Stora Enso reports that its EUR 1 billion (USD 1.08 billion) Oulu consumer board investment remains on schedule for full capacity by 2027.

- February 2025: Smurfit WestRock announces FY 2024 results and notes a USD 400 million synergy program linked to sustainable packaging expansion.

- January 2025: FDA confirms 35 PFAS food-contact authorisations are no longer effective, setting a June 30 2025 sell-through deadline for existing inventory.

- August 2024: Sappi posts Q3 FY24 EBITDA of USD 151 million, highlighting rebound in North American packaging demand.

Global Biofilm Coated Paperboard Market Report Scope

| Polylactic Acid (PLA) |

| Polyhydroxyalkanoates (PHA) |

| Starch and Starch Blends |

| Cellulose-based Films |

| Other Coating Materials (PBS, PEF, etc.) |

| Solid Bleached Sulfate (SBS) |

| Folding Boxboard (FBB) |

| Coated Unbleached Kraft (CUK) |

| White Top and Others Paperboard Grades |

| Food and Beverage |

| Food-service |

| Personal Care and Cosmetics |

| Household and Industrial Goods |

| Other End-use Industries |

| Extrusion Coating |

| Dispersion / Curtain Coating |

| Laminating |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Coating Material | Polylactic Acid (PLA) | ||

| Polyhydroxyalkanoates (PHA) | |||

| Starch and Starch Blends | |||

| Cellulose-based Films | |||

| Other Coating Materials (PBS, PEF, etc.) | |||

| By Paperboard Grade | Solid Bleached Sulfate (SBS) | ||

| Folding Boxboard (FBB) | |||

| Coated Unbleached Kraft (CUK) | |||

| White Top and Others Paperboard Grades | |||

| By End-use Industry | Food and Beverage | ||

| Food-service | |||

| Personal Care and Cosmetics | |||

| Household and Industrial Goods | |||

| Other End-use Industries | |||

| By Coating Method | Extrusion Coating | ||

| Dispersion / Curtain Coating | |||

| Laminating | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the biofilm coated paperboard market in 2025?

It is valued at USD 3.73 billion, with a 6.08% CAGR forecast to 2030.

Which coating material leads sales?

PLA coatings hold 39.42% of 2024 revenue but face faster growth from PHA.

What region is expanding the fastest?

Asia-Pacific is forecast to record a 7.78% CAGR through 2030 thanks to e-commerce and brewery demand.

Why are bio-coated boards replacing PFAS liners?

FDA revocations and EU ppb-level limits eliminate fluorochemical options, forcing rapid substitution.

Who are the dominant suppliers?

Stora Enso, Smurfit WestRock, Graphic Packaging International, Metsä Board and Mondi together control nearly 60% of capacity.

What is the main obstacle to wider adoption?

Limited industrial composting infrastructure, especially in developing regions, slows penetration despite regulatory support.

Page last updated on: