Contactless Biometric Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 31.89 Billion |

| Market Size (2031) | USD 77.46 Billion |

| Growth Rate (2026 - 2031) | 19.43% CAGR |

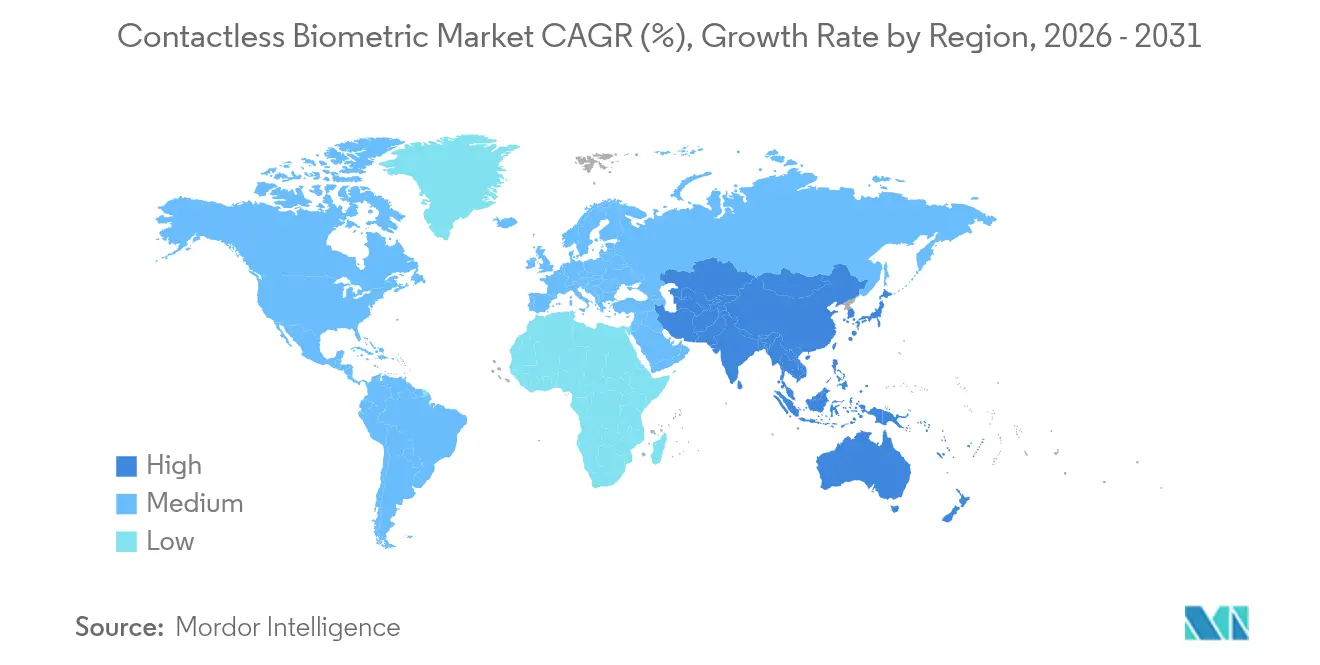

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

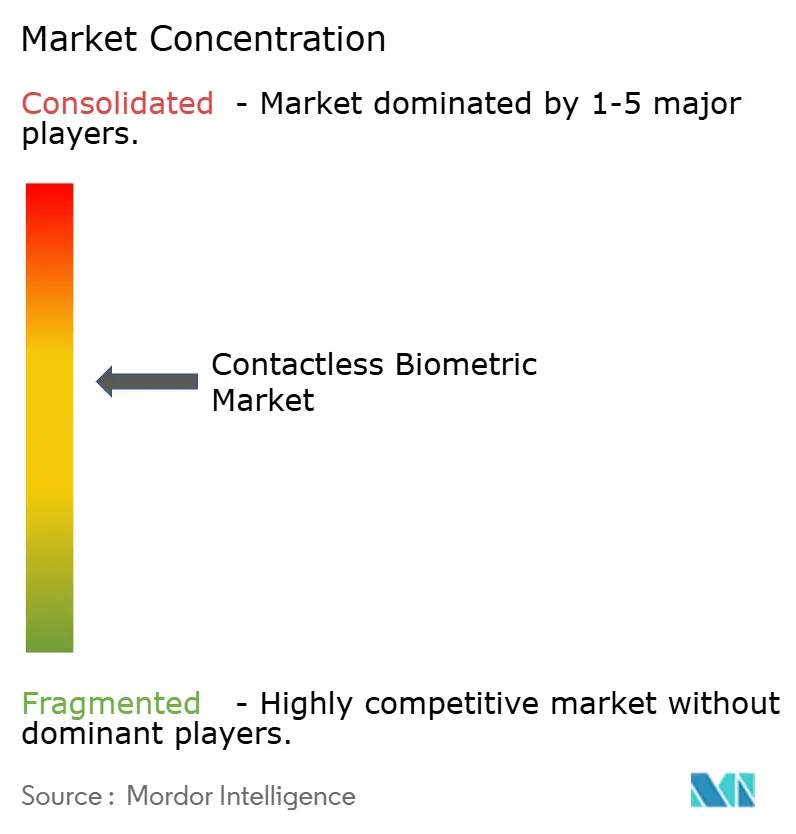

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Contactless Biometric Market Analysis by Mordor Intelligence

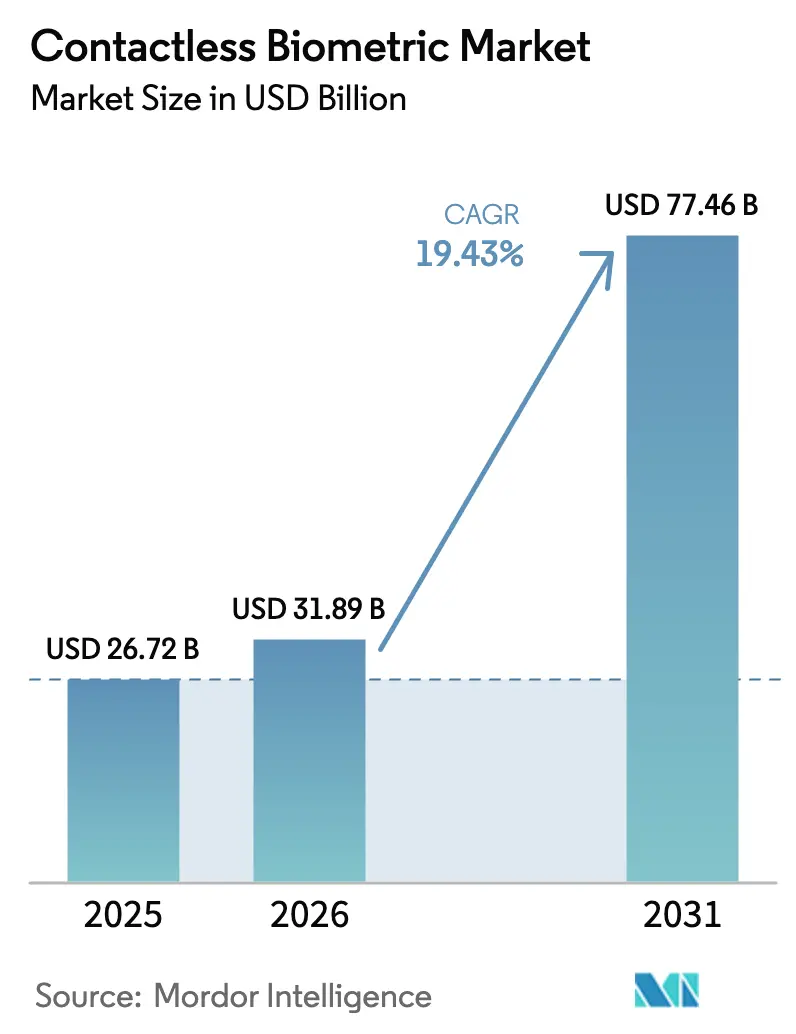

The contactless biometric market size is expected to grow from USD 26.72 billion in 2025 to USD 31.89 billion in 2026 and is forecast to reach USD 77.46 billion by 2031 at 19.43% CAGR over 2026-2031. Adoption accelerates as public agencies codify digital-ID mandates, enterprises migrate from badge-based systems, and edge-AI chips now execute multimodal authentication locally with sub-100 millisecond latency. Airports, hospitals, and large employers are retrofitting gates and kiosks to remove touch points, while smartphone OEMs embed 3-D facial and ultrasonic fingerprint modules that normalize touchless verification in everyday life. Component shortages in time-of-flight sensors are easing after new fabs came online in 2025, yet algorithmic bias remains under scrutiny, prompting vendors to release balanced training datasets and bias-mitigation APIs. M&A activity is brisk as incumbents pursue vertically-integrated stacks that bundle sensors, algorithms, and orchestration software, positioning themselves for bundled procurement cycles. Consequently, the contactless biometric market is evolving from point solutions to platform ecosystems anchored in privacy-by-design architectures.

Key Report Takeaways

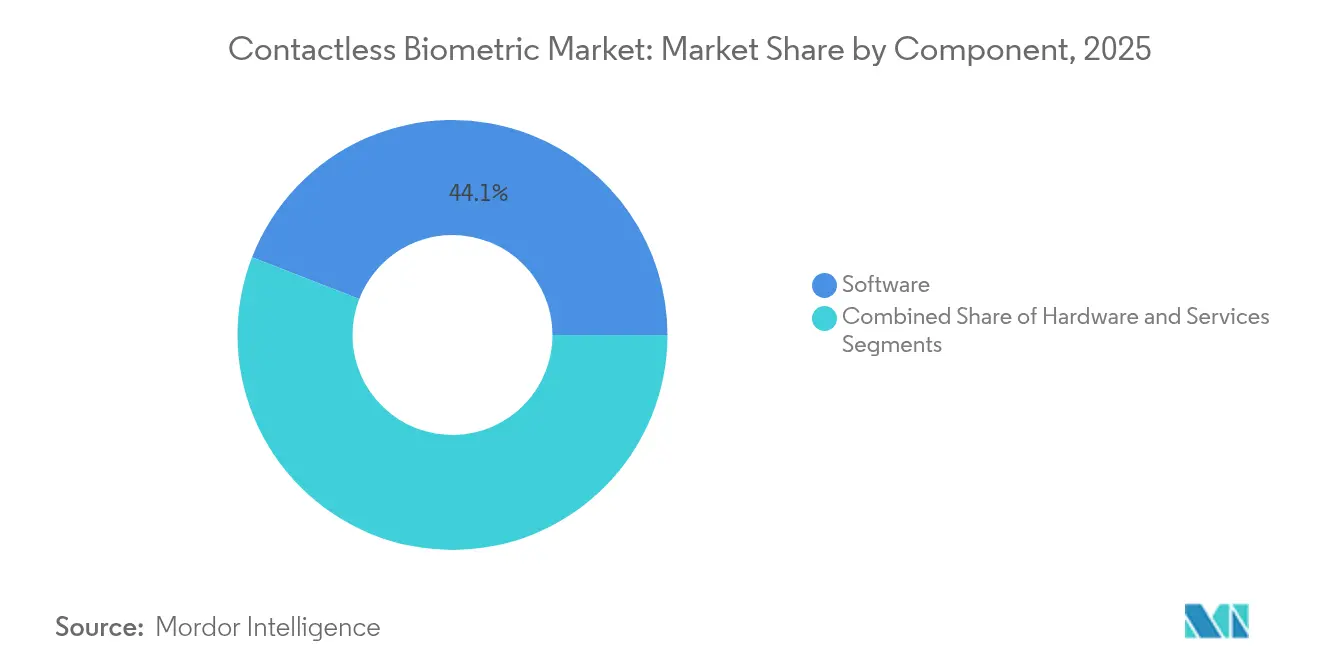

- By component, software led with 44.12% revenue share of the contactless biometric market in 2025; services are expanding fastest at a 20.2% CAGR through 2031.

- By technology, facial recognition captured 37.65% of the contactless biometric market share in 2025, while iris recognition is forecast to grow at 20.75% CAGR to 2031.

- By application, payments and transactions command a 21.08% CAGR, outpacing access-control’s established 41.12% revenue base.

- By end-user, healthcare recorded the highest projected growth, with the segment’s contactless biometric market size expected to rise at 20.15% CAGR to 2031.

- By geography, Asia-Pacific registers the fastest growth at 19.95% CAGR, yet North America retained 35.74% revenue share of the contactless biometric market size in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Contactless Biometric Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government digital-ID mandates accelerating touchless enrollment | +4.2% | Global, with early adoption in Australia, EU, South Korea | Medium term (2-4 years) |

| Airport e-gate roll-outs boosting border-control deployments | +3.8% | North America, Europe, Asia-Pacific core | Short term (≤ 2 years) |

| Smartphone OEM shift to 3-D facial unlock and ultrasonic in-display prints | +3.5% | Global, concentrated in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Healthcare infection-control push for biometric patient ID | +2.9% | Global, with accelerated adoption in developed markets | Short term (≤ 2 years) |

| Surge in biometric payment cards and wallets across APAC fintechs | +2.7% | Asia-Pacific core, spill-over to Latin America | Medium term (2-4 years) |

| Edge-AI multimodal fusion unlocking defense and critical-infra adoption | +2.1% | North America, Europe, select APAC defense markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Digital-ID Mandates Accelerating Touchless Enrollment

National digital-identity frameworks transform the contactless biometric market by converting optional upgrades into statutory requirements. Australia’s Digital ID Act 2024 specifies liveness detection and spoof-resistance thresholds, triggering immediate procurement of touchless enrollment booths across federal agencies.[1]Department of Finance (Australia), "Digital ID Bill Passes Parliament," finance.gov.au The EU Digital Identity Regulation obliges member states to issue biometric wallets to every citizen by 2026, underpinned by EUR 46 million (USD 49.6 million) pilot funding. South Korea issued 2.22 million mobile IDs by March 2025, integrating them with Samsung Wallet for dual public-private acceptance. Collectively, these mandates embed long-cycle demand into the contactless biometric market and catalyze ecosystem standardization.

Airport E-Gate Roll-Outs Boosting Border-Control Deployments

Travel rebounds push border agencies to replace manual checks with high-throughput touchless lanes. The UK Border Force began facial-recognition e-gate trials in 2024 to allow document-free entry, mirroring earlier deployments in Singapore and Dubai. NEC’s kiosks at Haneda Airport authenticate moving passengers at up to 100 per minute, illustrating scalability for hub airports. The momentum positions the contactless biometric market as indispensable infrastructure for global mobility.

Smartphone OEM Shift to 3-D Facial Unlock and Ultrasonic In-Display Prints

Samsung’s 63D depth sensor and allied ultrasonic fingerprint modules elevate on-device security, shipping in flagship models assembled in South-East Asia. As hundreds of millions of phones adopt these features annually, consumer familiarity with touchless verification converts into enterprise acceptance, broadening the contactless biometric market addressable base.

Healthcare Infection-Control Push for Biometric Patient ID

Fujitsu’s PalmSecure deployment in Hong Kong hospitals delivers 99.9999% match accuracy while eliminating card handling.[2]Samsung Electronic, "PalmSecure Case Study Hong Kong Hospitals," fujitsu.com Hospitals worldwide institutionalize hygienic workflows first introduced during COVID-19, ensuring sustained 20.8% CAGR for healthcare’s share of the contactless biometric market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR/CPRA privacy limits on biometric data retention | -2.8% | Europe, California, with global spillover effects | Medium term (2-4 years) |

| Algorithm bias—higher FAR/FRR on darker skin tones hindering Africa uptake | -1.9% | Africa, with secondary effects in diverse markets globally | Long term (≥ 4 years) |

| Spoof-resistant liveness tests inflating certification costs | -1.6% | Global, with higher impact in regulated industries | Short term (≤ 2 years) |

| ToF/IR sensor supply shortages elevating BOM costs | -1.4% | Global, concentrated in Asia-Pacific supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

GDPR/CPRA Privacy Limits on Biometric Data Retention

The UK GDPR and EU AI Act classify biometric identifiers as special-category data requiring explicit consent and purpose limitation, forcing vendors to redesign architectures for on-device matching and zero-knowledge proofs.[3]Information Commissioner’s Office, "Biometric Data Guidance: Recognition," ico.org.uk California’s CPRA and Illinois’ BIPA expose retailers to statutory damages, leading several U.S. chains to pause facial analytics roll-outs. Compliance overhead dampens smaller suppliers’ ability to compete in the contactless biometric market.

Algorithm Bias—Higher FAR/FRR on Darker Skin Tones Hindering Africa Uptake

NIST and DHS studies confirm error-rate skews tied to skin lightness, gender, and age, undermining public trust in regions with diverse demographics. African governments defer some public-sector tenders until vendors certify bias-mitigated models, moderating regional growth for the contactless biometric market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Integration

Software generated 44.12% of 2025 revenue, underscoring its centrality in orchestrating multimodal fusion across sensors. Services are forecast to grow at 20.2% as integrators manage algorithm tuning, privacy compliance, and lifecycle support. The contactless biometric market size for software is projected to reach USD 34.58 billion by 2031, reflecting sustained license renewals. Concurrently, hardware margins compress as depth-sensor costs fall 18% year-on-year. Fixed-price SaaS contracts and edge inference libraries create sticky revenue, encouraging vendors to bundle software in multi-year enterprise agreements across the contactless biometric market.

Hardware’s commoditization shifts differentiation up-stack, pushing OEMs to invest in SDK ecosystems and developer portals. NEC’s Bio-IDiom suite integrates facial, iris, voice, and ear acoustic modules under a unified API, enabling customers to flex modalities without re-platforming. Services teams then calibrate on-site lighting, network latency, and demographic datasets, a value-add segment now running at double-digit margins inside the contactless biometric market.

By Technology: Facial Recognition Leads Despite Iris Surge

Facial recognition maintained 37.65% share in 2025 thanks to ubiquitous cameras and high user acceptance. Iris solutions, however, are expanding at 20.75% CAGR on the back of liquid-lens optics that shrink module depth to under 5 mm. This trajectory nudges the contactless biometric market toward multimodal-first designs that fuse face and iris for 1-in-100 million false-acceptance probability.

Contactless fingerprint remains niche where hygiene overrides accuracy, while palm-vein gains traction in healthcare because sub-dermal patterns resist spoofing. Vendors therefore position fusion engines that score each modality and deliver an aggregated confidence threshold, aligning with ISO/IEC 30107 liveness standards. The contactless biometric market consequently rewards suppliers that maintain modality-agnostic inference pipelines.

By End-User: Government Sector Anchors Healthcare Expansion

Government agencies held 30.05% of 2025 revenue, underpinned by border-control refurbishments and national ID roll-outs. Healthcare is forecast to post 20.15% CAGR, lifting its contactless biometric market share from 12.10% in 2025 to 16.85% in 2031 as infection-control protocols formalize.

Financial-services deployments stabilize at mid-teens growth as biometric payment cards graduate from pilots to mass issuance. Consumer electronics shipments dwarf all other verticals in unit terms yet yield lower ASPs, compelling OEMs to monetize through app-store authentication fees. Transportation operators, particularly rail networks in Japan, embed face-through gates to cut dwell times during peak hours, reinforcing government partnerships that reverberate across the contactless biometric market.

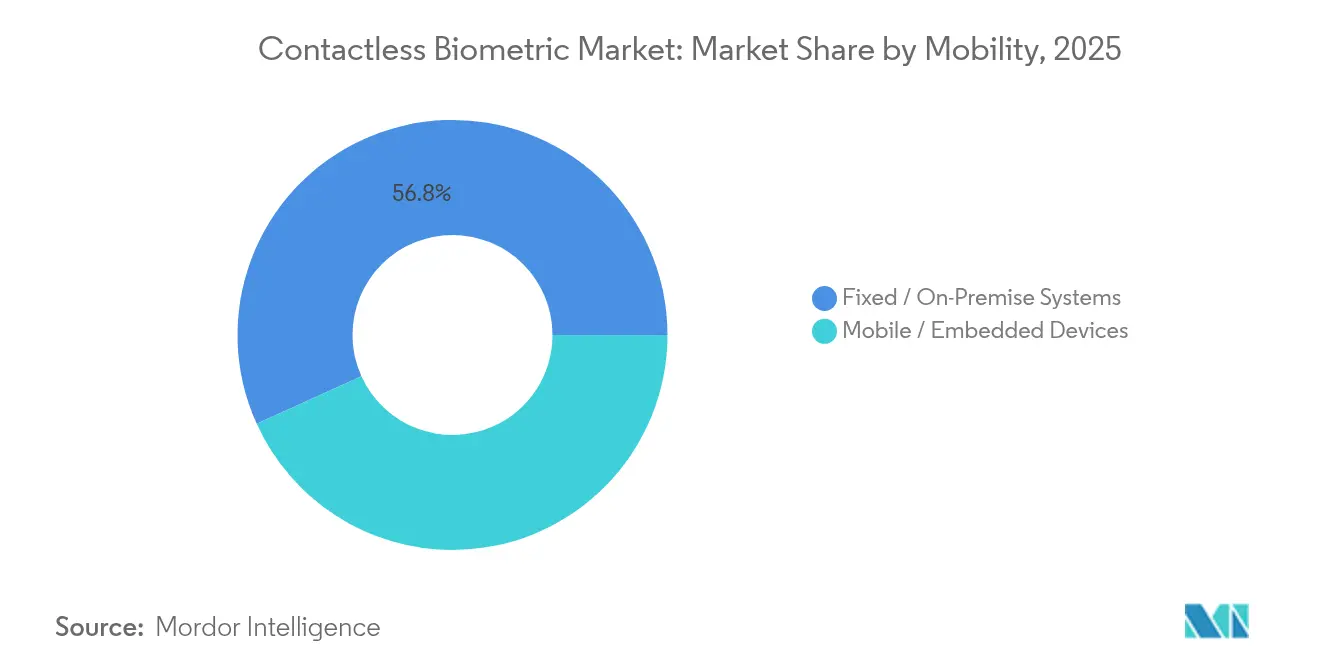

By Mobility: Fixed Systems Dominate Mobile Growth

Fixed installations accounted for 56.78% of 2025 revenue, favored by enterprises that mandate controlled lighting and power budgets. Mobile and embedded form factors grow at 20.75% CAGR on the back of smartphone proliferation and automotive-grade processors. The contactless biometric market size for mobile implementations is projected to expand from USD 11.55 billion in 2025 to USD 35.79 billion by 2031.

Walk-through gates in Osaka subway stations authenticate 70 passengers per minute, proving that fixed systems will remain the gold standard for ultra-high throughput. Yet edge-AI NPUs inside phones now execute liveness checks on-device, enabling merchants to offload server costs. The crossroads of fixed reliability and mobile ubiquity is spurring hybrid architectures where user-enrolled templates reside on secure elements, then synchronize with facility-grade controllers, further enlarging the contactless biometric market.

By Application: Access Control Foundation Supports Payment Innovation

Access control retained 41.12% of revenue in 2025, anchored by corporate campuses and data-center man-traps. Payments and transactions, however, are poised to eclipse time-and-attendance by 2028, racing ahead at 21.08% CAGR. The contactless biometric market size for payment applications is estimated at USD 15.94 billion in 2031, supported by Mastercard’s plan to retire static card numbers.

Law-enforcement deployments stabilize as body-worn cameras gain built-in face search for field officers, feeding suspect-matching queries to local edge nodes. Healthcare applications harmonize access control with electronic medical records, letting clinicians retrieve charts via palm-vein scans without touching keyboards. This convergence transforms the contactless biometric market from siloed use cases into an omnichannel identity backbone.

Geography Analysis

North America captured 35.74% of 2025 revenue, propelled by TSA biometric lanes across 22 airports and federal grants that underwrite algorithm testing. The contactless biometric market in the region benefits from mature data-protection statutes that define procurement criteria, giving incumbents predictable certification pathways. Asia-Pacific, by contrast, adds the most absolute dollars through 2031, expanding at 19.95% CAGR on the strength of India’s Aadhaar-linked wallets and China’s e-CNY pilots that embed face verification at point of sale.

Europe’s regulatory discipline tempers growth yet ensures multi-year contracts once compliance hurdles are cleared. EU-wide entry-exit systems, now projected for spring 2025, will funnel high-volume orders for e-gates and mobile enrollment kits. Latin America adopts touchless biometrics to broaden financial inclusion; Brazil’s PIX network trialed facial checks for instant payments, signaling fresh demand outside traditional security budgets. Africa’s uptake trails due to bias concerns and patchy broadband, but pan-African passport plans could unlock pent-up demand, making the contactless biometric market a catalyst for cross-border trade facilitation.

Across all regions, governments channel pandemic-era recovery funds into digital infrastructure, often stipulating domestic data residency that favors edge-compute deployments. Vendors that offer privacy-preserving analytics therefore gain advantage as sovereign clouds proliferate, underpinning expansion of the contactless biometric market.

Competitive Landscape

The contactless biometric market exhibits moderate concentration: the five largest vendors collectively hold about 42% revenue, meriting a market concentration score of 6. NEC tops NIST accuracy tables at 99.88%, reinforcing its preferred-bidder status for aviation contracts. Idemia, Thales, and Assa Abloy pursue portfolio gaps via bolt-on deals; Assa Abloy’s acquisition of 3millID and Third Millennium integrates door hardware with cloud identity orchestration, illustrating value-chain convergence. Samsung and Apple leverage device ecosystems to seed consumer adoption, then license APIs to banks and transit operators—an ecosystem play that converts hardware reach into recurring authentication fees. Start-ups such as authID raise capital to specialize in AI-driven liveness detection that counters deep-fake threats, aiming to white-label their engines to card networks. Competitive intensity now shifts toward bias-mitigation toolkits and post-quantum encryption to future-proof template storage, differentiators likely to reshape the contactless biometric market over the next planning horizon.

Contactless Biometric Industry Leaders

-

Touchless Biometric Systems AG

-

IDEMIA SAS

-

nVIAsoft Corporation

-

Fujitsu Limited

-

NEC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Onsemi released Hyperlux ID iToF sensors that extend accurate depth capture to 30 m, enabling longer-range passive liveness checks; leading OEMs secure early-access supply deals to fortify their edge-AI roadmaps.

- March 2025: South Korea completed nationwide mobile-ID rollout, embedding blockchain security and biometric verification; banks anticipate lower KYC costs and immediate user onboarding.

- February 2025: Mastercard initiated a phased migration from 16-digit numbers to biometric-token checkout, positioning its network as a fraud-resilient rail while reducing issuer liability.

- January 2025: Assa Abloy acquired 3millID and Third Millennium to deepen HID’s biometric reader and middleware stack, illustrating a horizontal expansion strategy toward end-to-end access solutions.

Global Contactless Biometric Market Report Scope

Contactless biometrics refers to a technology that enables the identification and authentication of individuals based on their unique physical or behavioral characteristics without the need for physical contact.

The contactless biometric market is segmented by component (hardware, software, services), by end-user (government, BFSI, consumer electronics, healthcare, logistics & transportation, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware |

| Software |

| Services |

| Facial Recognition |

| Iris Recognition |

| Contactless Fingerprint |

| Voice Recognition |

| Palm and Vein |

| Multimodal Fusion |

| Fixed / On-Premise Systems |

| Mobile / Embedded Devices |

| Access Control |

| Payments and Transactions |

| Law Enforcement and Border Control |

| Time and Attendance |

| Patient Identification |

| Government and Public Sector |

| BFSI |

| Consumer Electronics |

| Healthcare |

| Transportation and Logistics |

| Retail and E-commerce |

| Other Industrial |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Nordics | |

| Germany | ||

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Technology | Facial Recognition | ||

| Iris Recognition | |||

| Contactless Fingerprint | |||

| Voice Recognition | |||

| Palm and Vein | |||

| Multimodal Fusion | |||

| By Mobility | Fixed / On-Premise Systems | ||

| Mobile / Embedded Devices | |||

| By Application | Access Control | ||

| Payments and Transactions | |||

| Law Enforcement and Border Control | |||

| Time and Attendance | |||

| Patient Identification | |||

| By End-user | Government and Public Sector | ||

| BFSI | |||

| Consumer Electronics | |||

| Healthcare | |||

| Transportation and Logistics | |||

| Retail and E-commerce | |||

| Other Industrial | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Nordics | ||

| Germany | |||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the contactless biometric market by 2031?

The market is forecast to reach USD 77.46 billion by 2031, reflecting a 19.43% CAGR.

Which segment is expanding fastest within the contactless biometric market?

Payments and transactions lead with a 21.08% CAGR as biometric wallets and cards scale across Asia-Pacific.

How are privacy regulations influencing supplier strategies?

GDPR and CPRA compel vendors to adopt on-device processing and data-minimization workflows, increasing development costs but enhancing user trust.

Why is algorithm bias considered a restraint?

Higher error rates for darker skin tones undermine acceptance in diverse regions, prompting mandatory bias-mitigation before public-sector roll-outs.

Page last updated on: