Biomedical 3D Printing Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

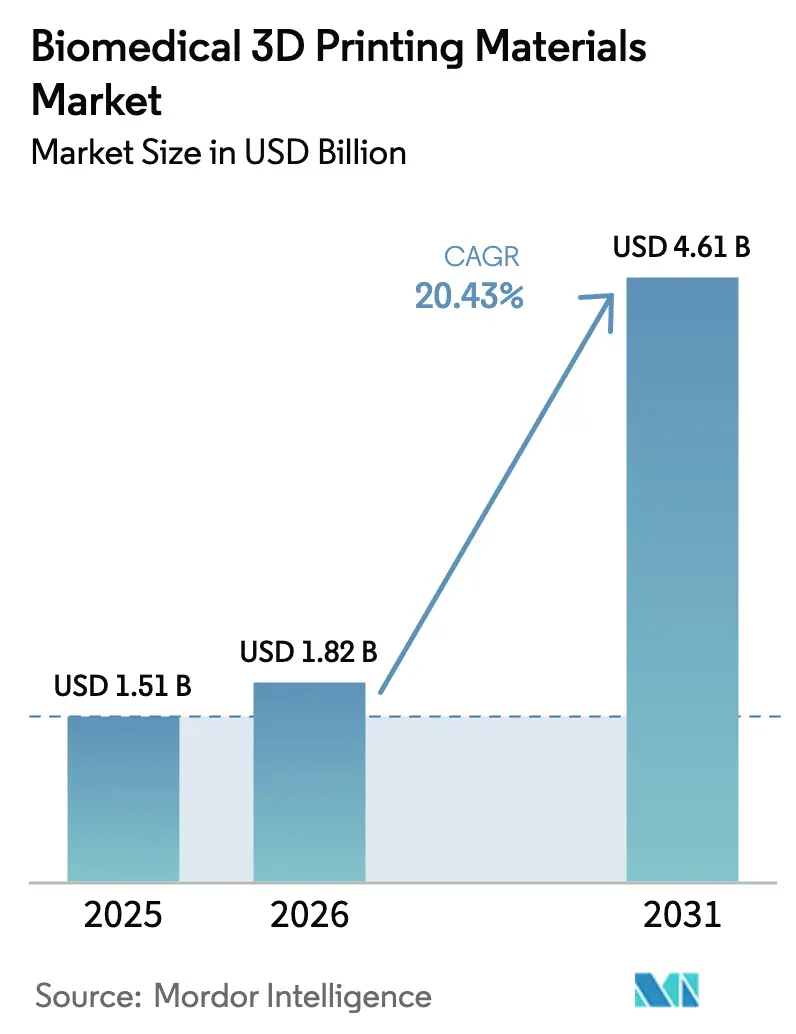

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 4.61 Billion |

| Growth Rate (2026 - 2031) | 20.43% CAGR |

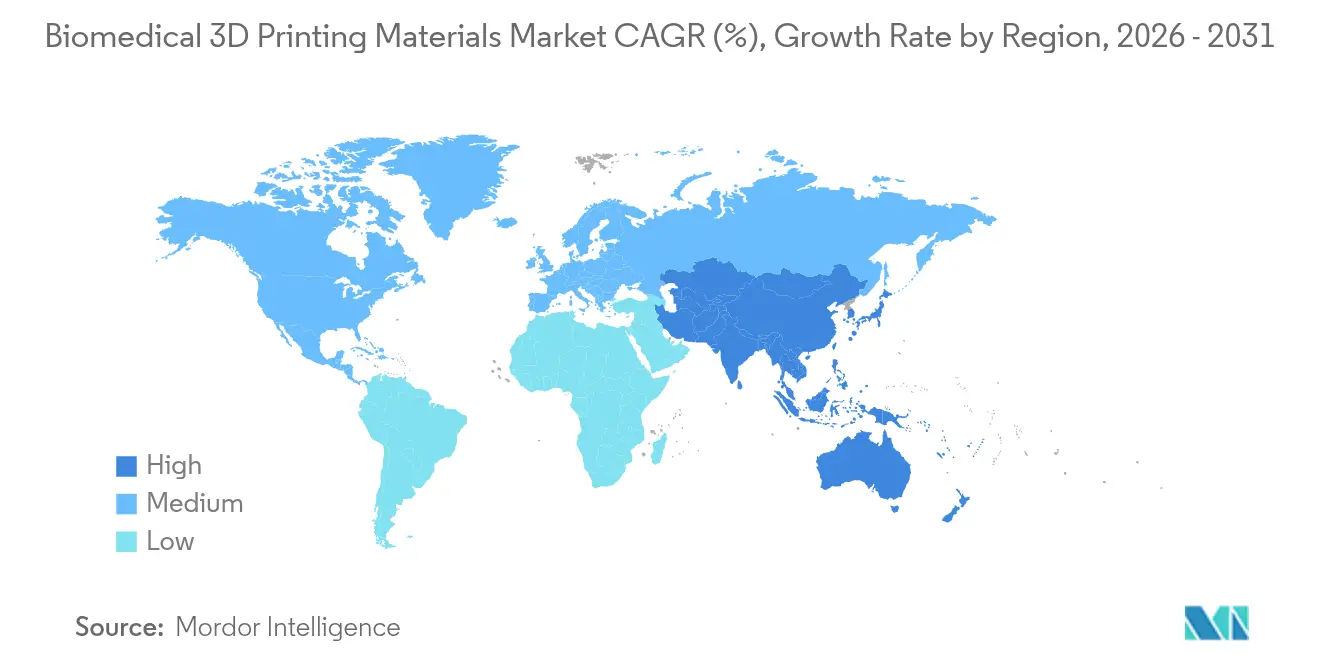

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biomedical 3D Printing Materials Market Analysis by Mordor Intelligence

The biomedical 3D printing materials market size was valued at USD 1.51 billion in 2025 and estimated to grow from USD 1.82 billion in 2026 to reach USD 4.61 billion by 2031, at a CAGR of 20.43% during the forecast period (2026-2031). The expansion mirrors the fast-growing alignment of additive manufacturing with precision medicine, stronger demand for patient-specific devices, and clearer regulatory guidance that shortens product approval cycles. Growth is further propelled by advances in high-performance polymers, growing hospital-based production capabilities, and expanding use in dental, hearing, and tissue-engineering applications. Intensifying collaboration between material suppliers and printer manufacturers is shrinking development timelines while raising entry barriers for smaller firms. Regional momentum remains strongest in North America, yet Asia-Pacific is adding capacity quickly as healthcare infrastructure scales up. Competitive dynamics point toward gradual consolidation, with polymer science expertise, regulatory support services, and global production footprints emerging as durable differentiators.

Key Report Takeaways

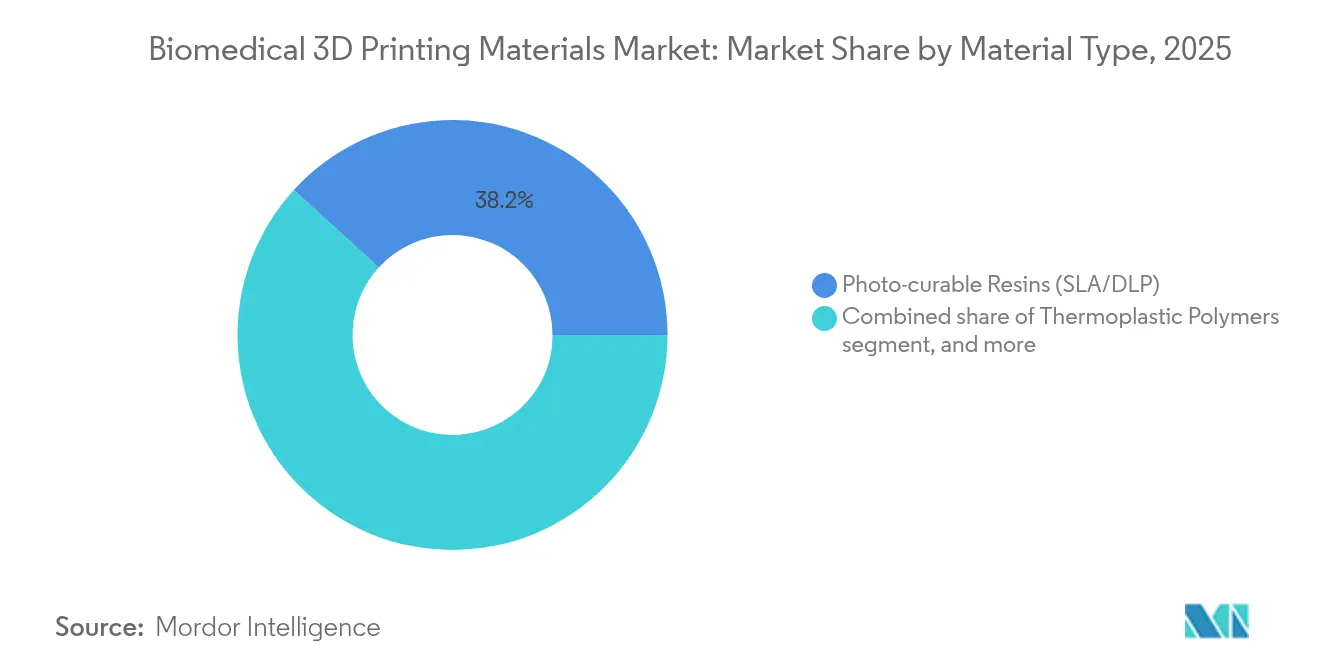

- By material type, photo-curable resins led with 38.21% revenue share in 2025; hydrogels and bio-inks are advancing at a 21.66% CAGR to 2031.

- By application, implants and prostheses held 40.95% of the biomedical 3D printing materials market share in 2025, while tissue and organ engineering is expanding at a 22.85% CAGR through 2031.

- By form, powder feedstocks accounted for 43.74% of the 2025 biomedical 3D printing materials market size; pellet and granulate formats are set to grow 21.65% annually to 2031.

- By geography, North America captured 44.52% of regional demand in 2025; Asia-Pacific is forecast to post a 20.91% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biomedical 3D Printing Materials Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing healthcare adoption of patient-specific implants | +3.0% | Global; strongest in North America & Western Europe | Medium term (2-4 years) |

| Expanding application scope in dental and hearing devices | +2.7% | Global; rapid uptake across Asia-Pacific | Short term (≤2 years) |

| Advances in medical-grade polymer and metal feedstocks | +3.9% | North America & Europe lead; APAC catching up | Long term (≥4 years) |

| Favorable regulatory pathways for additively manufactured devices | +2.8% | Primarily United States & European Union | Medium term (2-4 years) |

| Increasing investments in bioprinting and tissue engineering | +3.4% | Global research hubs (U.S., EU, China, Singapore) | Long term (≥4 years) |

| Rising demand for point-of-care manufacturing in hospitals | +2.6% | Early adopters in U.S. & EU; expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Healthcare Adoption of Patient-Specific Implants

Personalized medicine is translating from concept to clinical routine as hospitals deploy additive manufacturing suites that fabricate implants tailored to each patient’s anatomy. 3D Systems produced the first point-of-care 3D-printed PEEK facial implant cleared under European regulation, demonstrating that on-site manufacturing can satisfy stringent quality requirements while shrinking surgical lead times. Early adopters report fewer revision surgeries and higher patient satisfaction, outcomes that reinforce premium pricing for bespoke devices. Clinicians also benefit from streamlined digital workflows linking imaging, design, and printing. Material suppliers that certify high-performance polymers such as PEEK, PEKK, and medical-grade titanium powders gain recurring revenue because surgeons prefer validated feedstocks and traceable supply chains. Competitive advantage tilts toward firms that couple polymer science with turnkey regulatory documentation, a combination smaller entrants find hard to replicate.

Expanding Application Scope in Dental and Hearing Devices

Digital dentistry and audiology have become pathfinders for large-scale customization. Sonova shifted to fully additive production for custom-fit hearing shells, surpassing 10 million units in partnership with Materialise’s automated design pipeline[1]Source: Materialise NV, “Materialise Powers 10 Million 3D-Printed Hearing Aids,” materialise.com. This conversion proves that industrial-volume additive workflows can meet tight cost targets and high throughput while protecting biocompatibility. Dental laboratories now rely on photopolymers that match gum shades, ceramics that mimic enamel, and clear resins that resist salivary enzymes. Material innovation has broadened service menus to include night guards, surgical guides, and aligner molds fabricated within 24 hours. These successes convince investors that adjacent medical specialties such as orthotics or maxillofacial implants can scale similarly once material systems pass regulatory muster.

Advances in Medical-Grade Polymer and Metal Feedstocks

New formulations extend the service envelope of additive parts in the operating room. Stratasys introduced VICTREX AM 200, a PEEK blend engineered for reliable fused deposition without compromising sterilization resistance. Evonik’s RESOMER line tailors degradation profiles so bioresorbable implants match tissue-healing timelines, lowering the need for follow-up surgeries[2]Source: Evonik Industries AG, “RESOMER® Filament Portfolio for Medical 3D Printing,” evonik.com. On the metal side, tighter powder-size distributions and surface chemistry controls improve osseointegration of 3D-printed titanium joints. Suppliers are experimenting with composite pellets that embed reinforcing carbon fibers or bioactive ceramics, enabling functionally graded structures within a single print. As materials grow more sophisticated, qualification protocols lengthen, amplifying the value of deep regulatory competence.

Favorable Regulatory Pathways for Additively Manufactured Devices

The FDA’s additive manufacturing guidance spells out recommended testing for sterility, mechanical integrity, and biocompatibility, giving innovators a predictable clearance roadmap[3]U.S. Food & Drug Administration, “Technical Considerations for Additive Manufactured Medical Devices,” fda.gov. Europe’s Medical Device Regulation similarly addresses layer-wise manufacturing variables, harmonizing quality expectations across member states. Standardized ISO 14155 language for clinical investigations now references additive considerations, reducing interpretation risks for implant trials. Clearer rules reduce capital uncertainty and unlock R&D budgets once tied up in contingency planning. Suppliers able to furnish complete validation toolkits win preferred-vendor status because hospital engineers must document every material lot used for patient treatment.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of biomedical printing materials | -2.1% | Global; most acute in price-sensitive emerging markets | Short term (≤2 years) |

| Regulatory and quality compliance complexities | -1.9% | Worldwide; region-specific variations | Medium term (2-4 years) |

| Limited mechanical performance of hydrogel bio-inks | -1.6% | Global R&D centers; early-stage clinical sites | Long term (≥4 years) |

| Supply constraints for implant-grade high-performance polymers | -2.0% | North America & Europe; growing concern in APAC | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Cost of Biomedical Printing Materials

Medical-grade polymers and metals cost 300-500% more than industrial counterparts because they undergo extra purification, batch testing, and documentation. In lower-income regions, hospitals often postpone adoption even when clinical need is evident. Material expenses weigh heaviest in single-use surgical guides where consumption per procedure is high. Suppliers are exploring recycled powder programs and larger production runs to capture scale economies, but tight change-control rules slow price declines. Until costs fall, payers may cover only implants but not ancillary printed tools, capping near-term volume growth.

Regulatory and Quality Compliance Complexities

Manufacturers juggle disparate rules: FDA 510(k), European MDR, China’s NMPA, and country-specific conformity assessments. Each jurisdiction demands unique dossiers, accelerating spending on experts and test labs. Additive’s layer-by-layer nature complicates traditional batch inspection because even minor printer deviations can alter part density or surface roughness. Quality-assurance teams must deploy CT scanning, melt-viscosity checks, and lot-traceable digital files, raising overhead. Smaller players often outsource compliance, stretching timelines and budgets, while multinationals convert regulatory mastery into a competitive tall barrier.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Hydrogels Power a Bioprinting Breakthrough

Hydrogels and bio-inks are projected to post a 21.66% CAGR to 2031, narrowing the gap with photo-curable resins that maintained 38.21% of 2025 demand. Hospitals are turning to cell-laden gels for soft-tissue constructs, elevating volumes despite small part sizes. The biomedical 3D printing materials market size for hydrogels is rising as tissue-engineering pilots shift to limited commercial release. In contrast, photo-curable resins remain clinic staples for surgical guides and dental aligner molds because they balance speed and cost.

High-performance polymers such as PEEK safeguard load-bearing spinal cages and craniomaxillofacial plates where sterilization resistance is paramount. Bioceramics like hydroxyapatite foster bone ingrowth in dental implants, though volumes remain niche. Composite feedstocks that fuse bioresorbable polymers with beta-TCP particles open new possibilities for hybrid scaffolds. Metals continue to dominate orthopedic load cases; however, finer powders and hot-isostatic-press post-processing reduce residual porosity, bringing biomechanical parity closer to forged parts. The expanding palette compels device makers to master multiple print technologies, pushing many toward partnerships with vertically integrated material vendors.

By Application: Tissue Engineering Races Ahead of Traditional Implants

Implants and prostheses still represented 40.95% of the biomedical 3D printing materials market share in 2025, yet tissue and organ engineering is climbing faster at 22.85% CAGR as laboratories translate scaffold science into clinical grafts. Growth stems from bio-inks that degrade in sync with cell proliferation, yielding native tissue that replaces the printed matrix. Parallel progress in vascularization techniques removes a key barrier to viable thick tissues, further buoying material demand.

Dental and hearing devices supply a steady base load because custom fit dictates additive workflows. Surgical prototyping and anatomical models thrive in teaching hospitals that value reduced theater times. Drug-delivery devices start from low volumes but carry high margins due to precise dose control. Orthotic and wearable segments lean on nylon and TPU blends for flexible braces tailored to each patient’s biomechanics, promising spillover growth as sports medicine embraces individualized protective gear.

By Form: Pellets Challenge Powder Dominance

Powders commanded 43.74% of market revenue in 2025, favored for laser and electron-beam melting of metal and high-temperature polymers. Still, pellet and granulate formats are expanding at 21.65% annually as screw-extrusion printers achieve medical-grade repeatability. The biomedical 3D printing materials market size tied to pellets benefits from lower raw-material prices and simpler handling compared with inert-gas-sealed powder drums.

Filaments keep relevance in point-of-care settings because desktop printers run reliably with limited operator expertise. Liquids and resins remain essential for sub-50 micron resolution in dental crowns and clear orthodontic trays. Multi-form portfolios let suppliers tap diverse workflows: centralized powder-bed fusion for complex load-bearing implants and decentralized filament extrusion for quick-turn surgical tools.

Geography Analysis

North America retained 44.52% of global demand in 2025, underpinned by high procedure reimbursement, U.S. FDA clarity, and integrated hospital supply chains that adopt new materials quickly. Large academic centers run onsite print labs, anchoring supplier partnerships that speed bench-to-bedside translation. The region increasingly exports design expertise to satellite clinics, broadening indirect material pull. Yet payers pressure clinicians to justify premium materials, pushing vendors to supply cost-effectiveness data tied to lower revision rates.

Europe exhibits balanced growth as Medical Device Regulation harmonizes documentation across 27 countries, lowering repeat testing. Germany anchors material R&D with government grants backing bio-based chemistries that serve both healthcare and sustainability goals. France and the Netherlands invest in composite scaffold trials targeting cartilage repair. The biomedical 3D printing materials market size tied to European dental labs increases steadily because aligner services prefer locally sourced CE-marked resins.

Asia-Pacific is the fastest riser at 20.91% CAGR through 2031. China designates bioprinting as a strategic technology, channeling provincial subsidies into pilot lines for collagen bio-inks. Japan’s aging populace demands customized orthopedic implants, while domestic firms leverage precision robotics to automate printer operation. India focuses on cost-effective filaments and pellet systems for fracture fixation plates in tier-two hospitals. Regulatory heterogeneity remains an obstacle, though ASEAN mutual-recognition talks may ease regional clearance for approved materials.

Competitive Landscape

Market concentration is moderate. Global chemical leaders such as BASF, Evonik, and DSM leverage polymer science to roll out ISO-class clean-room compounding lines. BASF’s shift toward bio-based monomers shrinks product carbon footprints while keeping mechanical performance intact. Evonik differentiates with RESOMER bioresorbables matched to tissue-healing calendars, capturing surgeons’ interest for temporary fixation devices.

Additive-focused firms like Stratasys, 3D Systems, and Formlabs supply integrated ecosystems that bundle printers, validated materials, and workflow software. Stratasys expanded its Neo800+ stereolithography line and unveiled the Fortus filament-drying cabinet to minimize moisture-related defects. 3D Systems ties clinical consulting to its VESTAKEEP PEEK platform, allowing hospitals to print cranial plates internally under strict quality protocols.

Specialists emerge in fast-growing niches. CollPlant pilots rhCollagen bio-inks with Stratasys printers to pioneer regenerative breast implants. Start-ups targeting functionally graded scaffolds patent composite pellets combining carbon fiber with bioactive ceramics, aiming to leapfrog incumbent mono-material offerings. Mergers and supply agreements are rising as large suppliers lock in exclusive printer compatibility, signaling a march toward tighter vertical integration.

Biomedical 3D Printing Materials Industry Leaders

3D Systems Inc.

GE Healthcae

Evonik Industries AG

Formlabs Inc.

Stratasys Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: 3D Systems produced the first point-of-care 3D-printed PEEK facial implant with University Hospital Basel, demonstrating regulatory-compliant hospital manufacturing.

- April 2025: Stratasys launched the Neo800+ printer and VICTREX AM 200 PEEK at RAPID + TCT 2025, broadening medical-grade polymer choices.

- December 2024: 3D Systems debuted the PSLA 270 platform and Figure 4 Rigid Composite White resin to serve high-speed prototyping demands.

- November 2024: Stratasys released new FDM and P3 materials, including Ultracur3D RG 3280 ceramic-filled resin for injection-molding inserts.

- November 2024: BASF introduced Ultramid T7000 for advanced metal replacement, expanding polymer choices for structural 3D parts

- August 2024: CollPlant and Stratasys initiated pre-clinical testing of rhCollagen bio-printed breast implants targeting a USD 3 billion opportunity.

Global Biomedical 3D Printing Materials Market Report Scope

As per the scope of the report, biomedical 3D printing refers to the process of using 3D printing technology to create objects, structures, or implants that are compatible with living tissues and can be safely used in biological or medical applications. It involves the fabrication of three-dimensional objects using materials that are non-toxic, non-allergenic, and have minimal adverse effects on biological systems.

The biomedical 3d printing materials market is segmented by material type, application, form, and geography. The market is segmented by material type into polymer, metal, and other material types. The market is segmented by application into implants & prosthesis, prototyping & surgical guides, tissue engineering, hearing aids, and other applications. By form, the market is segmented into powder and liquid. The market is segmented by geography into North America, Europe, Asia-Pacific, and the Rest of the World. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Photo-curable Resins (SLA/DLP) |

| Thermoplastic Polymers (PLA, PCL, ABS, PETG) |

| High-performance Polymers (PEEK, PEKK, Ultem) |

| Metals & Alloys (Ti-6Al-4V, Co-Cr, SS316L) |

| Bioceramics (HA, ZrO?, TCP) |

| Hydrogels & Bio-inks |

| Composite & Nanocomposite Blends |

| Implants & Prostheses |

| Prototyping & Surgical Guides |

| Tissue & Organ Engineering |

| Dental & Hearing Aids |

| Drug-delivery & Pharmaceutical Testing |

| Orthotics & Wearables |

| Filament |

| Powder |

| Liquid / Resin |

| Pellet & Granulate |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material Type | Photo-curable Resins (SLA/DLP) | |

| Thermoplastic Polymers (PLA, PCL, ABS, PETG) | ||

| High-performance Polymers (PEEK, PEKK, Ultem) | ||

| Metals & Alloys (Ti-6Al-4V, Co-Cr, SS316L) | ||

| Bioceramics (HA, ZrO?, TCP) | ||

| Hydrogels & Bio-inks | ||

| Composite & Nanocomposite Blends | ||

| By Application | Implants & Prostheses | |

| Prototyping & Surgical Guides | ||

| Tissue & Organ Engineering | ||

| Dental & Hearing Aids | ||

| Drug-delivery & Pharmaceutical Testing | ||

| Orthotics & Wearables | ||

| By Form | Filament | |

| Powder | ||

| Liquid / Resin | ||

| Pellet & Granulate | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the biomedical 3D printing materials market expected to grow through 2031?

The global segment is forecast to expand at a 20.43% CAGR, climbing from USD 1.82 billion in 2026 to USD 4.61 billion by 2031.

Which material category currently generates the highest sales?

Photo-curable resins hold 38.21% of 2025 revenue thanks to their dominance in dental and surgical-guide printing.

What application area is projected to expand the most quickly?

Tissue and organ engineering shows the strongest momentum with a 22.85% CAGR through 2031 as bioprinting technologies mature.

Why are pellets gaining traction over powders?

Pellet feedstocks reduce raw-material cost and waste in extrusion-based systems, growing 21.65% annually to 2031.

Which region is the fastest-growing consumer of medical-grade 3D printing materials?

Asia-Pacific leads with a projected 20.91% CAGR, fueled by expanding healthcare infrastructure and government innovation programs.

What main factor keeps some hospitals from adopting additive implants sooner?

The high cost of certified biomedical feedstocksÑoften 300-500% above industrial gradesÑlimits uptake in price-sensitive markets.

Page last updated on: