Thin Film Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

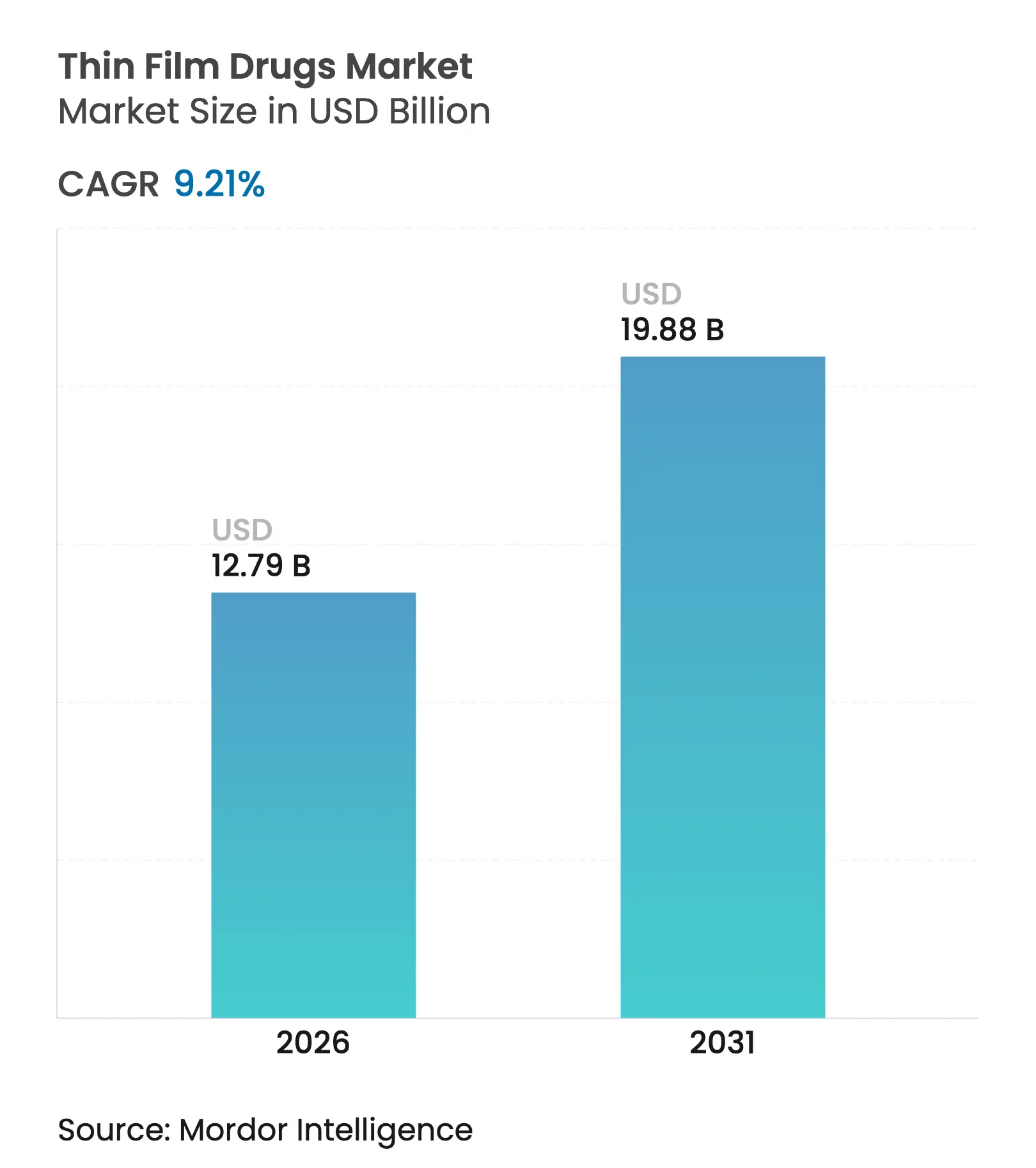

| Market Size (2026) | USD 12.79 Billion |

| Market Size (2031) | USD 19.88 Billion |

| Growth Rate (2026 - 2031) | 9.21 % CAGR |

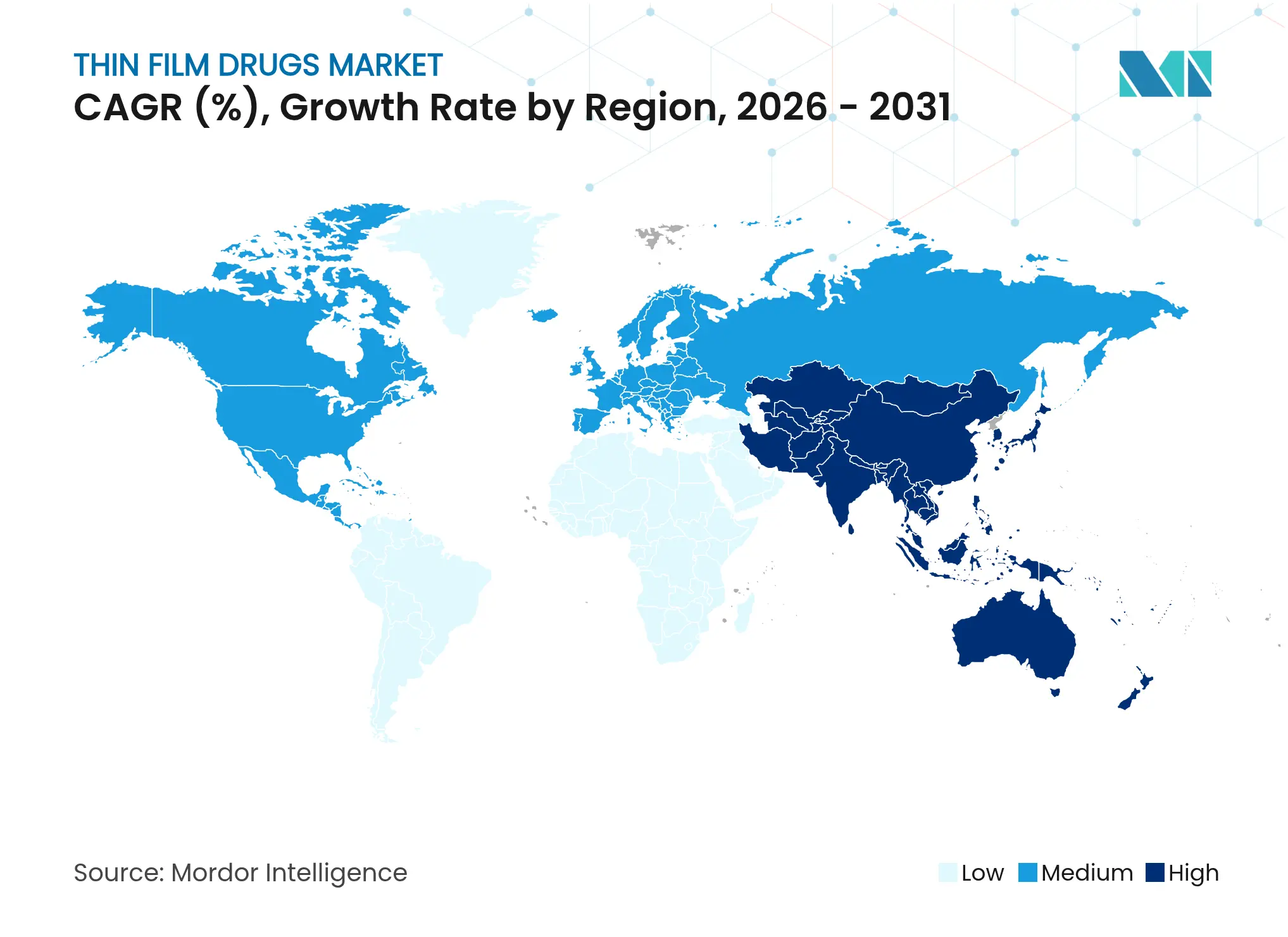

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

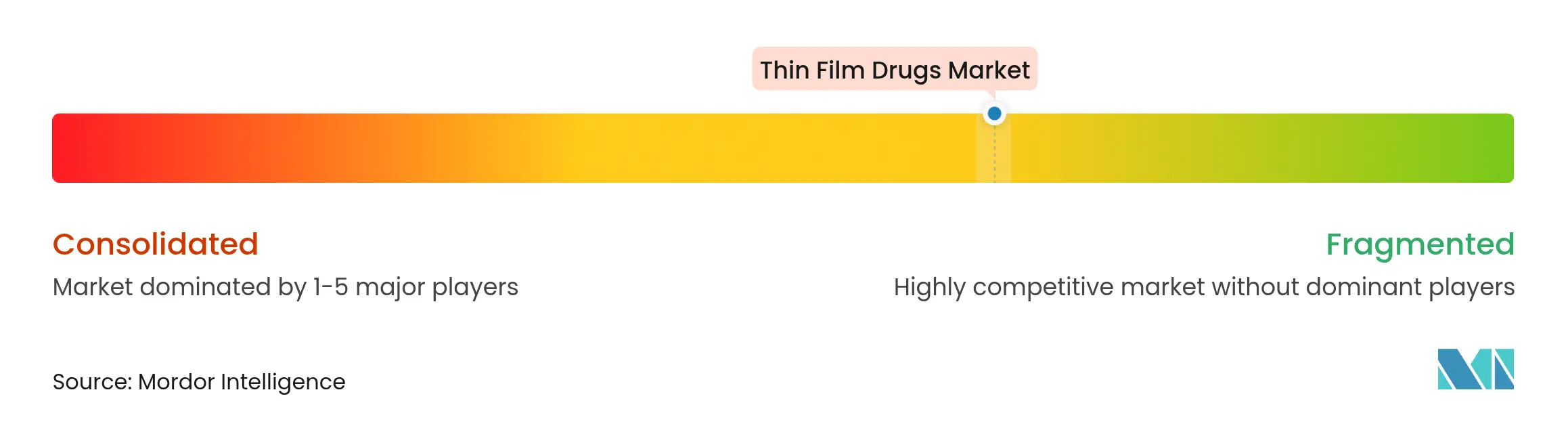

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Thin Film Drugs Market Analysis by Mordor Intelligence

The thin film drug market size is expected to grow from USD 11.71 billion in 2025 to USD 12.79 billion in 2026 and is forecast to reach USD 19.88 billion by 2031 at 9.21% CAGR over 2026-2031. Demand growth stems from an aging global population, mounting dysphagia prevalence, and regulatory encouragement for patient-centric formulations. Manufacturers are capitalizing on superior adherence profiles, rapid onset of action, and the ability to tailor dose strengths for vulnerable groups. Investments in hot-melt extrusion and solvent-casting lines are lowering production costs, while microneedle innovations position the technology to address chronic disease management needs in outpatient settings. Competitive strategies emphasize partnerships between formulation specialists and large pharmaceutical companies to shorten development timelines and widen therapeutic scope.

Key Report Takeaways

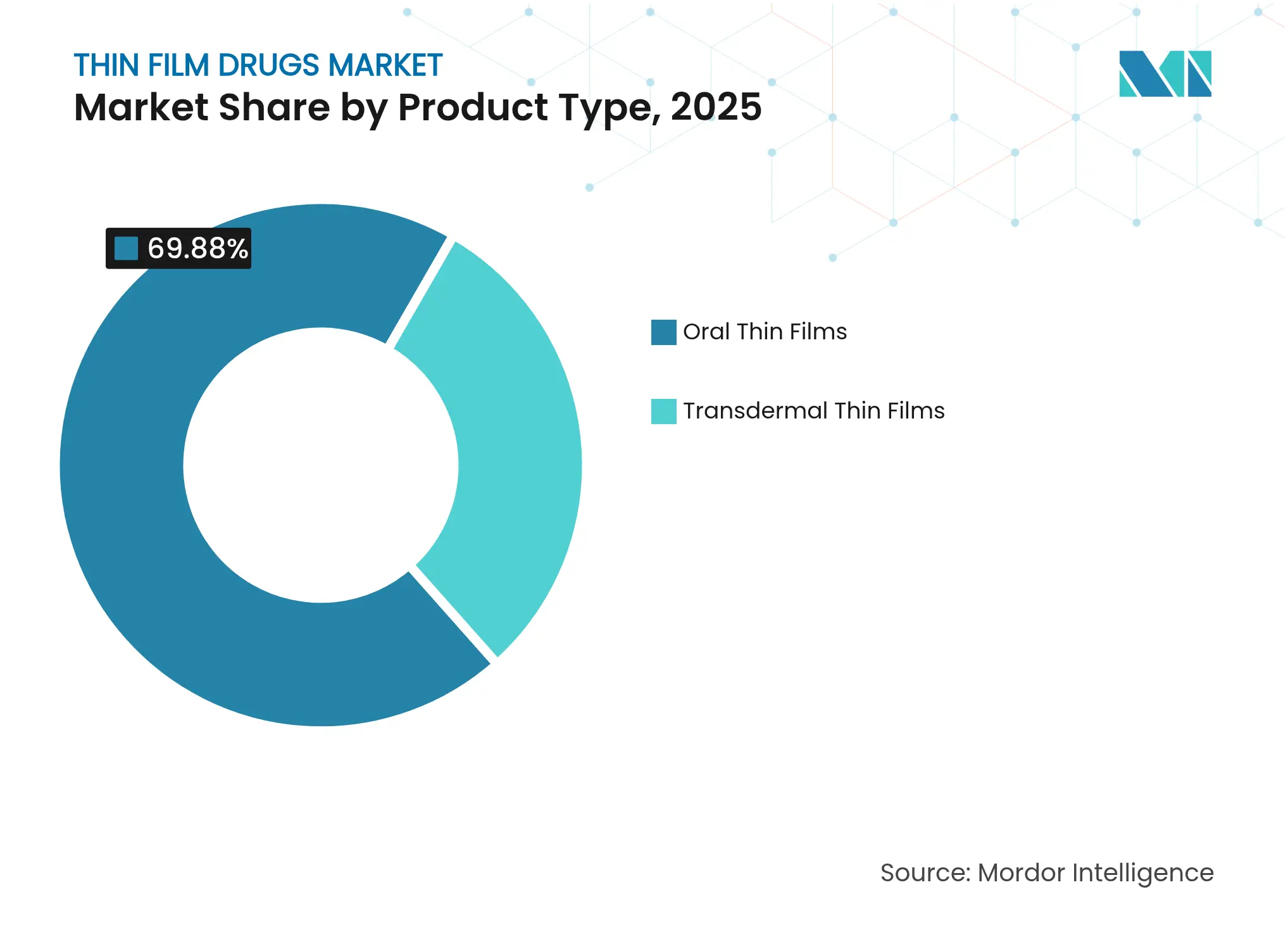

- By product category, oral thin films led with 69.88% of thin film drug market share in 2025; transdermal thin films are projected to expand at a 13.42% CAGR through 2031.

- By therapeutic indication, opioid use disorder captured 36.08% of the thin film drug market size in 2025, while chronic pain is forecast to grow at 11.67% CAGR between 2026 and 2031.

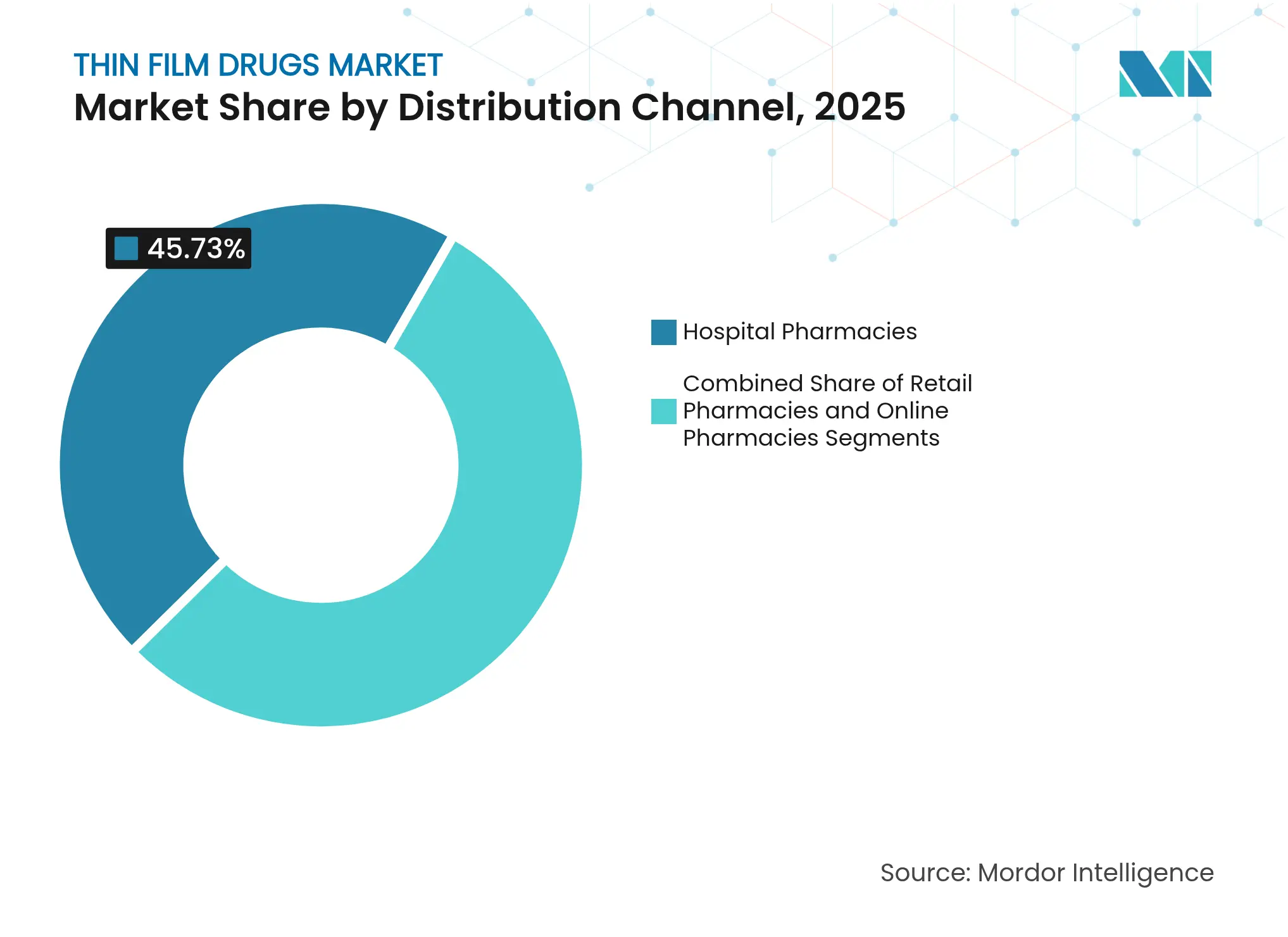

- By distribution channel, hospital pharmacies accounted for 45.73% of the thin film drug market size in 2025; online pharmacies post the highest projected CAGR at 15.35% to 2031.

- By drug type, prescription formats held 71.44% of the thin film drug market size in 2025, whereas over-the-counter variants are advancing at 12.42% CAGR.

- By geography, North America contributed 40.96% of 2025 revenue, whereas Asia-Pacific is on track for a 10.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thin Film Drugs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of dysphagia & geriatric population

Rising prevalence of dysphagia & geriatric population

| +2.1% | Global; strongest in North America and Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+2.1%

| Geographic Relevance:

Global; strongest in North America and Europe

| Impact Timeline:

Long term (≥ 4 years)

|

Increasing approvals & investments in thin-film

therapeutics

Increasing approvals & investments in thin-film

therapeutics

| +1.8% | North America and Europe; Asia-Pacific emerging | Medium term (2-4 years) | |||

Superior patient compliance versus conventional dosage

forms

Superior patient compliance versus conventional dosage

forms

| +1.4% | Global | Medium term (2-4 years) | |||

Opioid-harm-reduction policies accelerating buccal film

uptake

Opioid-harm-reduction policies accelerating buccal film

uptake

| +0.9% | North America primary; Europe secondary | Short term (≤ 2 years) | |||

Hot-melt-extrusion HPMC grades enable higher-dose,

heat-sensitive APIs

Hot-melt-extrusion HPMC grades enable higher-dose,

heat-sensitive APIs

| +0.7% | Global manufacturing hubs | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence Of Dysphagia & Geriatric Population

Dysphagia affects 36.9% of nursing-home residents and 27% of older adults, creating a large cohort unable to swallow conventional tablets[1]Norio Watanabe et al., “Survey of Dysphagia and Related Medications in Nursing Home Residents,” Journal of Pharmaceutical Health Care and Sciences, JPHCS.BIOMEDCENTRAL.COM. Beyond age-related issues, neurological disorders and post-surgical complications amplify demand for alternate dosage forms. Health systems incur significant costs from aspiration pneumonia and non-adherence, prompting reimbursement support for film formulations. Pediatric use cases reinforce universal applicability, while community pharmacists using EAT-10 screening tools now flag swallowing issues earlier, broadening product access points.

Increasing Approvals & Investments In Thin-Film Therapeutics

RizaFilm’s 2024 FDA clearance for migraine relief underlined the agency’s confidence in thin film platforms. Aquestive’s NDA for Anaphylm demonstrates how sublingual epinephrine could disrupt autoinjectors through needle-free delivery[2]“Aquestive Completes NDA Submission for Anaphylm,” Aquestive Therapeutics, AQUESTIVE.COM. Large companies channel new spending into U.S. manufacturing: Johnson & Johnson alone announced USD 55 billion for advanced dosage capabilities, signaling sustained capital flow toward film technologies. Clearer bioequivalence guidelines now reduce regulatory uncertainty, encouraging venture capital to back specialized developers.

Superior Patient Compliance Versus Conventional Dosage Forms

Clinical data show orodispersible formulations lower hospitalization odds by 64.5% and relapse by 63.2% in non-adherent psychiatric patients. Thin films dissolve quickly, avoid water, and allow taste masking, boosting acceptance among children and the elderly. Payers reward therapies that cut readmissions, enabling premium pricing. Manufacturers highlight compliance benefits to differentiate from generic tablets, particularly where adherence drives therapeutic outcomes.

Opioid-Harm-Reduction Policies Accelerating Buccal Film Uptake

Federal initiatives prioritizing medication-assisted treatment have expanded buprenorphine coverage, and buccal films reduce diversion risk compared with tablets. Evidence that extended-release buprenorphine aids fentanyl-using populations further validates film approaches. Public-health alignment assures steady procurement, anchoring revenue visibility for producers through 2030.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Availability of substitute dosage forms (ODTs,

injectables)

Availability of substitute dosage forms (ODTs,

injectables)

| -1.6% | Global | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-1.6%

| Geographic Relevance:

Global

| Impact Timeline:

Medium term (2-4 years)

|

Moisture-sensitivity driving high-cost barrier packaging

Moisture-sensitivity driving high-cost barrier packaging

| -1.2% | Global manufacturing hubs | Long term (≥ 4 years) | |||

Limited solvent-casting capacity for high-potency APIs

Limited solvent-casting capacity for high-potency APIs

| -0.8% | North America & Europe manufacturing centers | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Availability Of Substitute Dosage Forms (ODTs, Injectables)

Orally disintegrating tablets enjoy mature production lines and lower costs, curbing thin film uptake in price-sensitive categories. European Pharmacopoeia recognition of ODTs ensures streamlined approvals, while injectables remain dominant where precise pharmacokinetics matter, such as oncology. Established infrastructure and falling generic prices limit thin film pricing power when convenience alone is the differentiator.

Moisture-Sensitivity Driving High-Cost Barrier Packaging

Thin films are hygroscopic, so firms often allocate 15-20% of product cost to barrier packs. Research warns that some coatings can accelerate degradation, pushing developers toward custom multilayer formats. Reliance on single suppliers for specialty foils adds supply risk, and complex packaging undermines sustainability targets, pressuring manufacturers to invest in formulation tweaks that tolerate higher humidity.

Segment Analysis

By Product Type: Oral Films Dominate Despite Transdermal Acceleration

Oral films captured 69.88% of thin film drug market share in 2025 thanks to straightforward regulatory paths and cost-effective solvent-casting lines. Transdermal formats post a 13.42% CAGR to 2031 as microneedle-integrated patches broaden drug classes deliverable through skin.

Manufacturers can scale oral films rapidly, leveraging hot-melt extrusion to incorporate poorly soluble APIs. Transdermal films require precise micro-fabrication and adhesive engineering, limiting large-scale output today. Nonetheless, vaccine delivery and hormone therapy trials are yielding positive acceptance data, indicating transdermal systems will narrow the gap during the forecast horizon.

Note: Segment shares of all individual segments available upon report purchase

By Indication: Opioid Crisis Drives Market Leadership

Opioid use disorder dominated with 36.08% of thin film drug market size in 2025 because buprenorphine films align with government harm-reduction goals. Chronic pain films exhibit the fastest 11.67% CAGR as prescribers pivot to non-opioid molecules that benefit from rapid oromucosal absorption.

Migraine therapies gain traction after RizaFilm’s clearance, enabling in-home treatment during nausea episodes. Sublingual immunotherapy films in allergy care and emergency systemic delivery for anaphylaxis show promise, diversifying the clinical portfolio. Collectively, these indications reinforce a broad therapeutic runway for the thin film drug market.

By Distribution Channel: Online Growth Disrupts Traditional Patterns

Hospital pharmacies retained 45.73% of thin film drug market size in 2025 because controlled substances and specialty drugs require clinical oversight. Online pharmacies post 15.35% CAGR, fueled by telehealth adoption and relaxed shipping regulations for temperature-stable films.

Retail chains bridge routine prescriptions, but digital platforms now integrate medication adherence tools, offering refill reminders tailored to film regimens. For immobile patients or rural communities, mail-order fulfillment circumvents access barriers, further expanding the thin film drug market.

Note: Segment shares of all individual segments available upon report purchase

By Drug Type: Prescription Dominance Reflects Complexity

Prescription films commanded 71.44% share in 2025, reflecting stringent dosing requirements and reimbursement frameworks that support higher prices. Over-the-counter products rise at 12.42% CAGR as taste-masked vitamins and antihistamines transition to consumer aisles.

Improved manufacturing yields reduce cost per dose, making OTC conversion economically viable. However, regulatory agencies insist on extensive consumer-use evidence, so large firms with deep clinical datasets hold an advantage in switching pathways.

Geography Analysis

North America led with 40.96% share in 2025, supported by FDA guidance that clarifies bioequivalence and stability expectations. Robust insurance coverage and specialty pharmacy networks expedite market entry, while sizable investments in continuous manufacturing ensure domestic capacity for rapid scale-up.

Europe maintains second position through centralized approvals that streamline multi-country launches. Emphasis on patient safety and high adherence among seniors underpins demand. Regional CDMOs specialize in solvent-casting and HME, serving global supply chains.

Asia-Pacific posts 10.38% CAGR to 2031, propelled by regulatory harmonization and expanded manufacturing grants in China, India, and South Korea. Lower labor costs and government incentives attract technology-transfer deals, positioning the region as a production hub for global thin film drug market exports. Rising healthcare spending and urbanization open large patient pools receptive to convenient dosage forms.

Competitive Landscape

Market Concentration

The thin film drug market is moderately fragmented. Pioneers such as Aquestive Therapeutics and Indivior leverage proprietary solvents, laminate structures, and taste-masking chemistries to guard intellectual property. Exclusive supply contracts with large pharma partners ensure stable order books.

Emerging players focus on microneedle patches and polymer science to broaden application areas beyond oral mucosa. Partnerships dominate strategy: innovator firms license film technologies to companies seeking lifecycle management for expiring brands. Large multinationals increasingly acquire specialty formulators to secure manufacturing know-how and de-risk development.

Competition centers on dose-loading efficiency, dissolution time, and packaging advancements. Companies able to integrate continuous HME with real-time analytics gain a cost edge. Others court differentiation through flavor profiles and child-resistant yet senior-friendly single-dose pouches.

Thin Film Drugs Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BioNxt Solutions Inc. launched a feasibility study to create an oral dissolvable film of semaglutide targeting diabetes and obesity patients.

- June 2025: IntelGenx rebranded to Nualtis, aligning corporate identity with its long-term oral film strategy.

Table of Contents for Thin Film Drugs Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence Of Dysphagia & Geriatric Population

- 4.2.2Increasing Approvals & Investments In Thin-Film Therapeutics

- 4.2.3Superior Patient Compliance Versus Conventional Dosage Forms

- 4.2.4Opioid-Harm-Reduction Policies Accelerating Buccal Film Uptake

- 4.2.5Hot-Melt-Extrusion HPMC Grades Enable Higher-Dose, Heat-Sensitive APIs

- 4.3Market Restraints

- 4.3.1Availability Of Substitute Dosage Forms (ODTs, Injectables)

- 4.3.2Moisture-Sensitivity Driving High-Cost Barrier Packaging

- 4.3.3Limited Solvent-Casting Capacity For High-Potency APIs

- 4.4Technological Outlook

- 4.5Porter's Five Forces

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product Type

- 5.1.1Oral Thin Films

- 5.1.1.1Orodispersible Films

- 5.1.1.2Sublingual Films

- 5.1.1.3Buccal Films

- 5.1.2Transdermal Thin Films

- 5.1.2.1Passive Patches

- 5.1.2.2Active / Microneedle-assisted Patches

- 5.2By Indication

- 5.2.1Schizophrenia

- 5.2.2Migraine

- 5.2.3Opioid Use Disorder

- 5.2.4Nausea & Vomiting

- 5.2.5Chronic Pain

- 5.2.6Allergy & Asthma

- 5.3By Distribution Channel

- 5.3.1Hospital Pharmacies

- 5.3.2Retail Pharmacies

- 5.3.3Online Pharmacies

- 5.4By Drug Type

- 5.4.1Prescription (Rx)

- 5.4.2Over-the-Counter (OTC)

- 5.5Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Indivior PLC

- 6.3.2Aquestive Therapeutics

- 6.3.3ZIM Laboratories

- 6.3.4Kindeva

- 6.3.5BioDelivery Sciences Intl.

- 6.3.6Nualtis

- 6.3.7Tesa SE (Tesa Labtec)

- 6.3.8Pfizer Inc.

- 6.3.9Novartis AG

- 6.3.10Viatris Inc

- 6.3.11GSK plc

- 6.3.12Cure Pharmaceutical

- 6.3.13ARx LLC

- 6.3.14Solvay SA

- 6.3.15Sumitomo Dainippon Pharma

- 6.3.163D Matrix Ltd

- 6.3.17MonoSol Rx / Catalent

- 6.3.18Adhex Pharma

- 6.3.19Tapemark LLC

- 6.3.20Lohmann Therapie-Systeme

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Global Thin Film Drugs Market Report Scope

As per the report's scope, thin film drugs have surfaced as an alternative to tablets or capsules due to their efficient therapeutic results. The drugs are made of polymers that quickly dissolve when kept in the mouth or buccal cavity, supplying the drug directly to the systemic circulation in the body. The Thin Film Drugs Market is segmented by Product Type (Oral Thin Film, Transdermal Thin Film), By Indication (Schizophrenia, Migraine, Opioid Dependence, and Others), and by geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The by eport also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.