Skin Resurfacing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

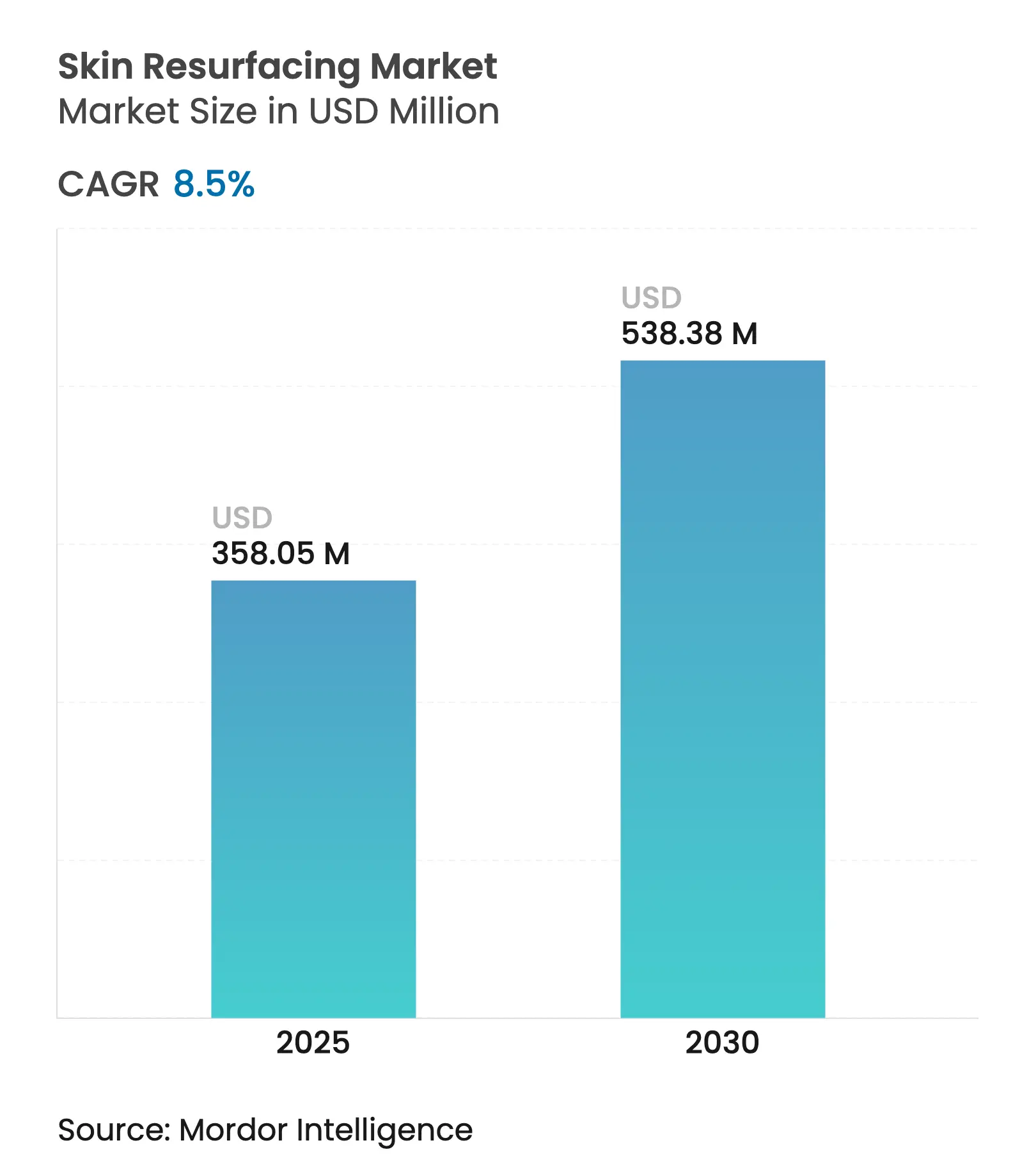

| Market Size (2025) | USD 358.05 Million |

| Market Size (2030) | USD 538.38 Million |

| Growth Rate (2025 - 2030) | 8.50 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Skin Resurfacing Market Analysis by Mordor Intelligence

Demographic aging continues to steer patients toward less invasive solutions, while rapid product innovation keeps the competitive bar high. Integrated laser-radiofrequency systems, artificial intelligence guidance, and hybrid ablative–non-ablative modalities demonstrate how technology enhances outcomes and reduces recovery times. Growth also reflects rising male participation, the proliferation of medical spas in the Asia-Pacific region, and stronger digital marketing that normalizes aesthetic procedures among younger adults. Together, these forces position the skin resurfacing market for steady, broad-based expansion during the forecast horizon.

Key Report Takeaways

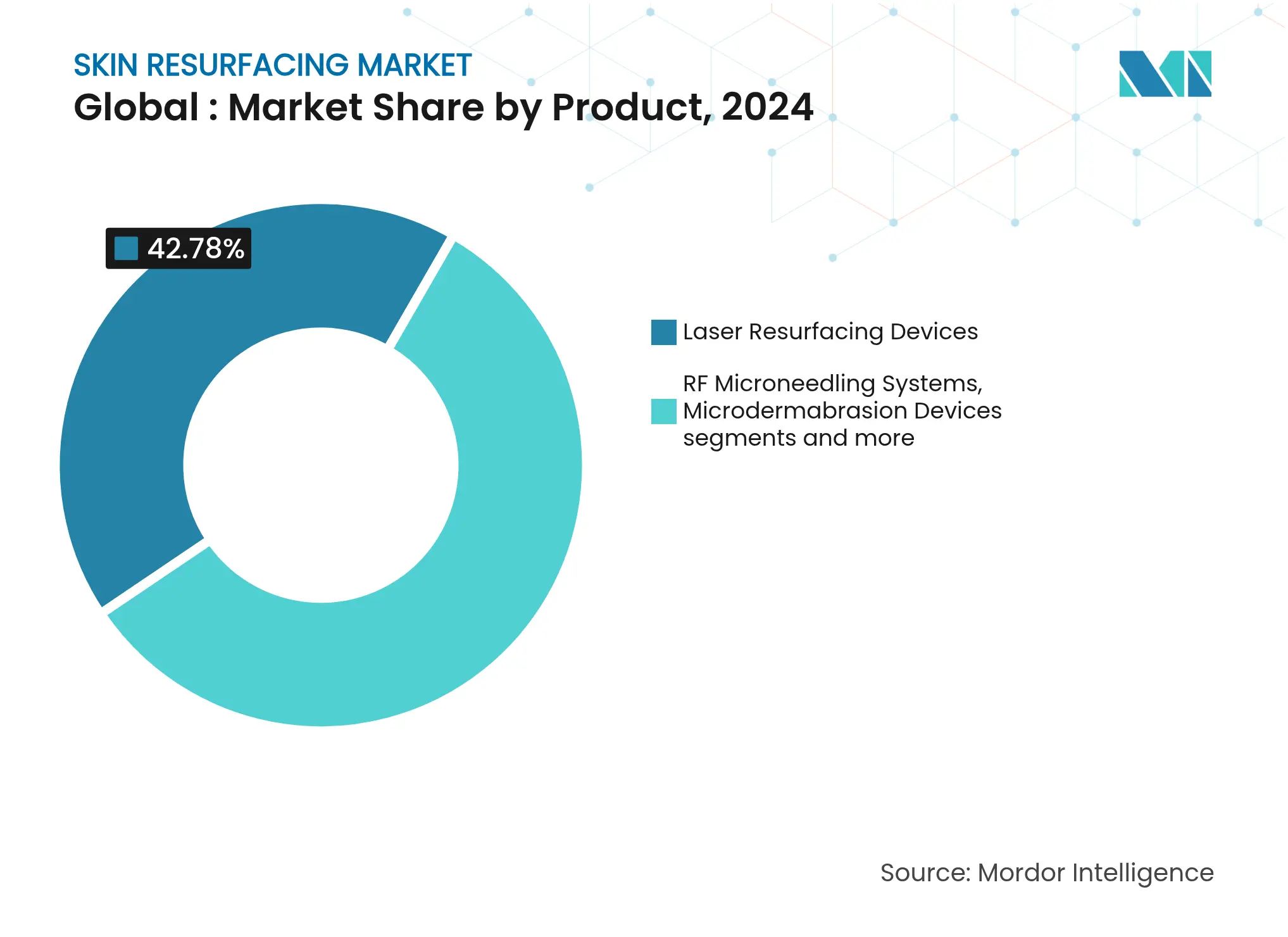

By product type, laser resurfacing devices held 42.78% of the skin resurfacing market share in 2024, while RF microneedling systems are projected to grow at a 9.16% CAGR through 2030.

By technology, ablative platforms commanded a 56.10% share of the skin resurfacing market size in 2024; however, non-ablative systems are expected to expand at a 9.57% CAGR to 2030.

By application, wrinkle and fine-line reduction accounted for 38.16% of the skin resurfacing market size in 2024; scar and acne scar revision is forecast to grow at the fastest rate, with a 10.01% CAGR.

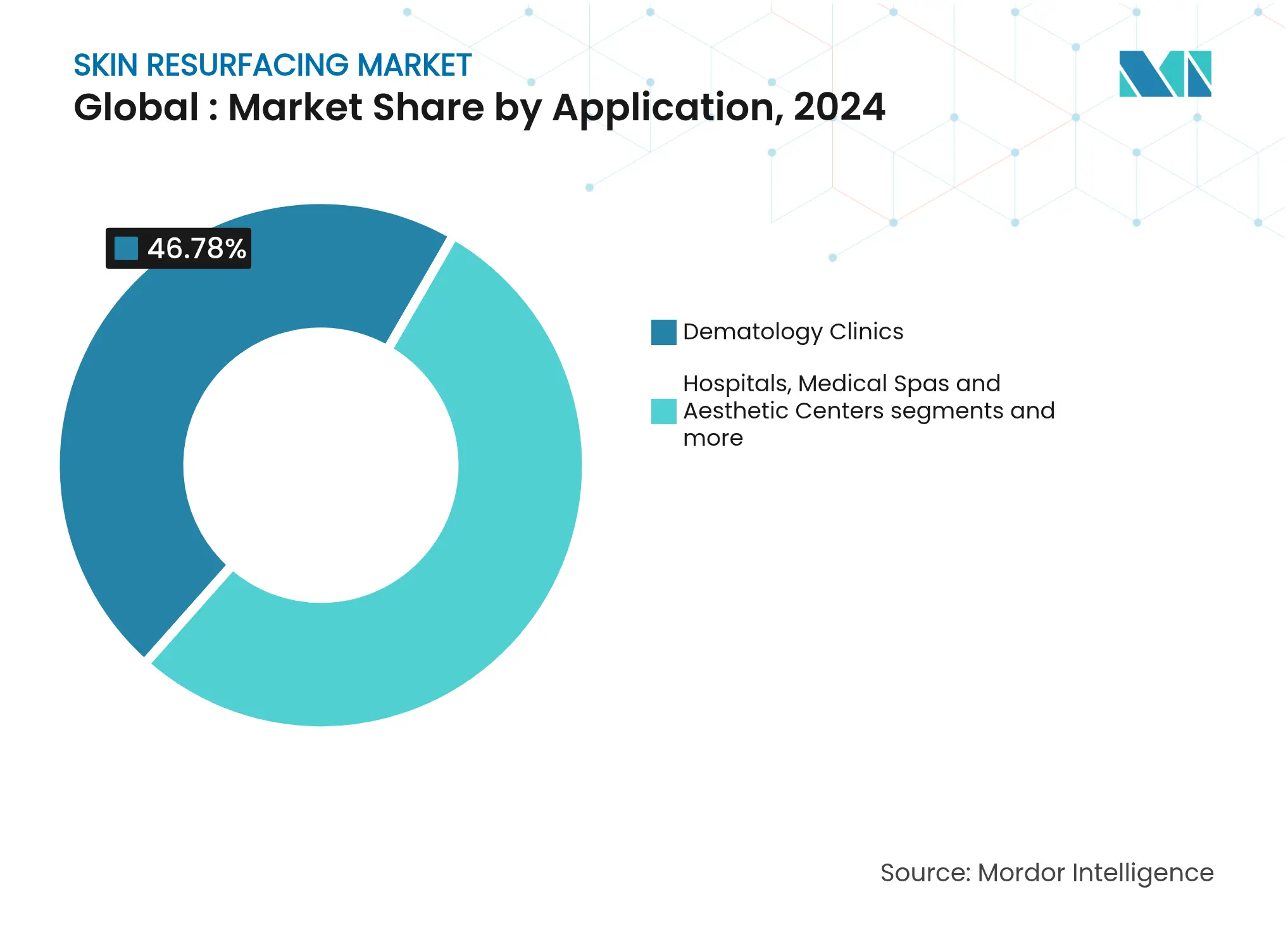

By end user, dermatology clinics captured a 46.78% revenue share in 2024, whereas medical spas are expected to advance at a 10.46% CAGR through 2030.

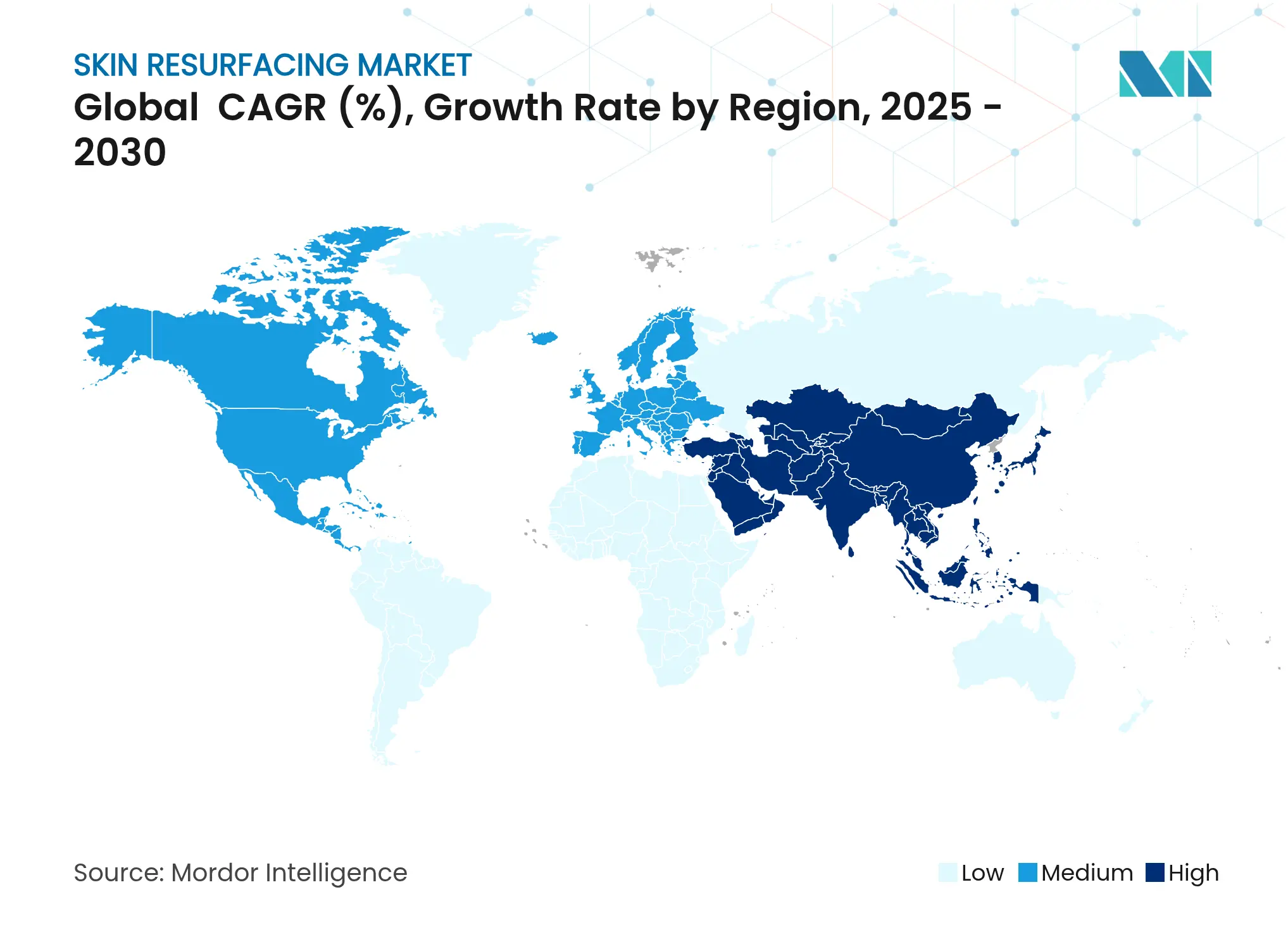

By geography, North America led with a 36.89% share in 2024; Asia-Pacific is the fastest-growing region at a 10.93% CAGR to 2030.

Global Skin Resurfacing Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Aging-driven demand for minimally-invasive aesthetics Aging-driven demand for minimally-invasive aesthetics | +2.1% | Global, with concentration in North America & Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:Global, with concentration in North America & Europe | Impact Timeline:Long term (≥ 4 years) |

Surge in combination treatments (laser + RF microneedling) Surge in combination treatments (laser + RF microneedling) | +1.8% | Global, led by North America, expanding to APAC | Medium term (2-4 years) | |||

Rising male consumer adoption of cosmetic procedures Rising male consumer adoption of cosmetic procedures | +1.2% | North America & Europe core, emerging in APAC | Medium term (2-4 years) | |||

Rapid expansion of medical-spa chains in Asia-Pacific Rapid expansion of medical-spa chains in Asia-Pacific | +1.5% | APAC core, spill-over to MEA | Short term (≤ 2 years) | |||

AI-guided laser platforms improving treatment outcomes AI-guided laser platforms improving treatment outcomes | +0.9% | Global, early adoption in developed markets | Long term (≥ 4 years) | |||

ESG-linked preference for low-consumable devices ESG-linked preference for low-consumable devices | +0.4% | Europe & North America, expanding globally | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Aging-driven demand for minimally-invasive aesthetics

Global population aging accelerates interest in procedures that rejuvenate appearance without surgical downtime. The Aesthetic Society recorded a 14% increase in nonsurgical aesthetic procedures from 2020 to 2024, underscoring durable demand. Fractional CO₂ lasers further validate this preference by delivering superior scar management when used within one month post-surgery, according to peer-reviewed studies. Improved safety profiles encourage older patients to seek preventive care earlier, reinforcing long-term procedure adoption.

Surge in combination treatments (laser + RF microneedling)

Pairing fractional lasers with radiofrequency microneedling lifts collagen stimulation while moderating epidermal damage. A four-and-a-half-year safety review found no adverse events when RF microneedling was combined with cosmetic injectables, highlighting the modality’s versatility. Manufacturers now embed both energies in single consoles, enabling clinics to offer multi-effect sessions that reduce overall chair time and boost revenue per patient.

Rising male consumer adoption of cosmetic procedures

An 18-year analysis of online search behavior shows marked growth in male interest for microneedling, chemical peels, and laser resurfacing. Clinics adapt by tailoring protocols to thicker male dermis and by adjusting marketing language toward workplace and lifestyle benefits. The trend broadens the skin resurfacing market beyond its traditional female core, diversifying clinic revenue streams.

Rapid expansion of medical-spa chains in Asia-Pacific

Asia-Pacific cafés-style medical spas multiply quickly; global facility counts climbed from 8,899 in 2020 to 10,488 in 2024, with per-unit revenue averaging USD 1.398 million. China illustrates the surge: 91% of high-income residents maintained or increased aesthetic spending in 2024. New venues purchase mid-tier laser platforms in volume, enlarging the installed base and spurring regional distributor growth

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capital cost of laser workstations High capital cost of laser workstations | -1.4% | Global, particularly affecting emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.4% | Geographic Relevance:Global, particularly affecting emerging markets | Impact Timeline:Medium term (2-4 years) |

Stringent device safety regulations & lengthier approvals Stringent device safety regulations & lengthier approvals | -0.8% | Global, most restrictive in North America & Europe | Long term (≥ 4 years) | |||

Limited reimbursement for aesthetic indications Limited reimbursement for aesthetic indications | -1.1% | North America & Europe primarily | Long term (≥ 4 years) | |||

Growing popularity of home-use resurfacing gadgets Growing popularity of home-use resurfacing gadgets | -0.6% | Global, led by developed markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High capital cost of laser workstations

Professional-grade resurfacing consoles cost USD 100,000–500,000 before maintenance and training outlays. Upcoming U.S. Quality System Regulation Amendments effective 2026 will further lift compliance expenditure, raising manufacturer list prices[1]Source: Federal Register, “Medical Devices; Quality System Regulation Amendments,” federalregister.gov . Smaller practices therefore delay purchases or opt for lower-priced single-energy tools, slowing penetration in cost-sensitive locales

Limited reimbursement for aesthetic indications

Most private insurers define wrinkle and acne-scar treatments as cosmetic; Aetna’s coverage policies typify the stance[2]Source: Aetna, “Clinical Policy Bulletin #0038: Cosmetic Surgery,” aetna.com . Because patients self-fund, volumes correlate tightly with disposable income. The absence of billing codes for novel hybrid procedures compounds the barrier, limiting technology adoption among clinics reliant on predictable payor revenue.

Segment Analysis

By Product: RF Microneedling Drives Innovation

Laser resurfacing devices generated 42.78% of 2024 revenue, keeping them the commercial anchor of the skin resurfacing market. They benefit from broad clinical familiarity and premium price points that lift average selling prices. RF microneedling systems, however, are projected to grow at a 9.16% CAGR, reflecting clinician enthusiasm for shorter downtime and versatile protocols. AI-enabled depth control enables practitioners to match energy delivery to dermal thickness, thereby improving safety for individuals with darker skin phenotypes. The combined momentum positions RF units as central to incremental demand even as lasers preserve headline revenue status.

Platform integration also advances. Multimodal workstations now combine fractional laser, bipolar RF, and IPL in a single footprint, enabling clinics to add services without requiring multiple capital purchases. As bundled consoles roll out, the skin resurfacing market gains resilience because purchasers can serve a broader range of indications from a single asset.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Non-ablative Gains Momentum

Ablative systems held a 56.10% revenue share in 2024, a testament to their proven efficacy in deep scar revision and the treatment of pronounced rhytides. They command higher treatment prices, sustaining device ROI. Non-ablative platforms, in contrast, are expected to expand at a 9.57% CAGR as patients value weekend-length recovery windows and reduced risk of post-inflammatory hyperpigmentation. Advanced 1550 nm fractional lasers stimulate dermal collagen without vaporizing surface tissue, enabling lip and perioral rejuvenation for working professionals.

Hybrid solutions blur traditional boundaries: temperature-modulated CO₂ lasers deliver fractional patterns that limit thermal diffusion, merging ablative precision with non-ablative safety. Such convergence reinforces the skin resurfacing market as manufacturers differentiate through parameter flexibility rather than energy type alone.

By Application: Scar Revision Accelerates

Wrinkle and fine-line reduction represented 38.16% of the skin resurfacing market size in 2024, confirming its role as the foundational indication. Scar and acne scar revision, however, is forecast to post the quickest 10.01% CAGR through 2030. Devices like Cutera’s AviClear, the first FDA-cleared energy tool targeting inflammatory acne, illustrate how preventive treatment reduces future scarring while addressing active pathology. Heightened social media visibility around acne solutions channels younger cohorts toward professional therapy, enlarging lifetime value for clinics.

Greater efficacy in pigment modulation also drives the uptake of melasma treatment. The 577 nm yellow laser demonstrates notable clearance of epidermal lesions with minimal recurrence, thereby broadening candidate eligibility among Fitzpatrick skin types IV–VI. These advances collectively expand the therapeutic envelope and drive application-led volume growth.

Note: Segment shares of all individual segments available upon report purchase

By End User: Medical Spas Lead Growth

Dermatology clinics retained 46.78% of 2024 revenue, underpinned by board-certified oversight and the capacity to handle complex presentations. Medical spas, however, are projected to grow at a 10.46% CAGR as consumers gravitate toward boutique environments offering bundled wellness experiences. Eighty-four percent of spa owners forecast further revenue gains in 2025, and repeat-visit rates rose to 73% in 2024. The model supports subscription skin programs that lock in predictable income while upselling resurfacing packages.

Hospitals remain relevant for medically indicated resurfacing, such as burn scar revision, yet their growth is modest. Home-use gadgets proliferate but deliver lower fluence and require professional guidance; systematic reviews note variable efficacy, sustaining demand for in-office procedures. Clinics increasingly pair professional care with curated at-home regimens, carving out an ecosystem rather than facing displacement.

Geography Analysis

North America generated the largest 36.89% share of the skin resurfacing market in 2024, driven by high disposable incomes, a dense network of providers, and a robust training infrastructure. The region’s medical-spa count surpassed 10,000 outlets, with average site revenue of USD 1.398 million. FDA rule changes slated for 2026 will standardize quality systems and diversify clinical trial cohorts, potentially increasing development costs but enhancing public confidence once approvals are obtained.

Asia-Pacific is on course for a 10.93% CAGR, outpacing all other regions. Urban millennials in China, Japan, and South Korea are allocating a growing portion of their discretionary income to preventive aesthetics; 91% of high-income Chinese consumers either maintained or increased their spending on cosmetic procedures in 2024. National regulators in South Korea and Singapore fast-track device clearance when domestic manufacturing is involved, accelerating market entry for local innovators. With the broader regional med-tech sector projected to reach USD 190 billion by 2025, suppliers are prioritizing distributor partnerships and localized education to convert latent demand.

Europe delivers steady mid-single-digit growth anchored by stringent safety culture and a well-insured patient base. Demand also reflects environmental stewardship; clinics in Germany and the Nordics increasingly specify low-consumable handpieces to meet internal ESG goals. South America and the Middle East & Africa remain emerging but compelling. Brazil’s long-standing cosmetic culture sustains procedure tourism, while Saudi Arabia’s approval of Cytrellis’s Micro-Coring platform signals policy support for device-based aesthetics. Collectively, these geographies provide expansion corridors that diversify manufacturer revenue beyond core Western markets.

Competitive Landscape

Market Concentration

The skin resurfacing industry features moderate concentration. Incumbents such as Lumenis, Candela Medical, and Cynosure leverage multi-decade clinical datasets and extensive service networks to defend share. Continuous portfolio renewal is essential; Lumenis launched FoLix in January 2025, adapting fractional laser know-how to hair-loss treatment and thereby cross-selling into dermatology clients.

Strategic mergers alter positioning. The April 2024 tie-up between Cynosure and Lutronic combined complementary wavelengths, doubling the installed base in Asia and enabling broader training reach and parts availability. Private equity interest remains high; MedSpa Partners’ June 2025 clinic acquisition in Canada exemplifies roll-up models that centralize purchasing and accelerate device replacement cycles.

Artificial intelligence differentiates early movers. The MIRIA Skin Treatment System integrates predictive analytics that adjust pulse energy per pixel in real time, seeking better outcomes with fewer passes. Firms investing in software roadmaps as vigorously as in optics or RF generators are more likely to secure premium pricing and long-term maintenance contracts.

Skin Resurfacing Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cytrellis Biosystems won clearances in Canada and Saudi Arabia for its ellacor Micro-Coring system, broadening distribution footprints

- November 2024: Lumenis France signed a distribution pact with X-Derma, expanding sales coverage in Europe.

- June 2024: Lumenis introduced FoLix, the first FDA-cleared fractional laser for androgenetic alopecia, opening a new revenue stream beyond traditional skin resurfacing.

Table of Contents for Skin Resurfacing Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Aging-driven demand for minimally-invasive aesthetics

- 4.2.2Surge in combination treatments (laser + RF microneedling)

- 4.2.3Rising male consumer adoption of cosmetic procedures

- 4.2.4Rapid expansion of medical-spa chains in Asia-Pacific

- 4.2.5AI-guided laser platforms improving treatment outcomes

- 4.2.6ESG-linked preference for low-consumable devices

- 4.3Market Restraints

- 4.3.1High capital cost of laser workstations

- 4.3.2Stringent device safety regulations & lengthier approvals

- 4.3.3Limited reimbursement for aesthetic indications

- 4.3.4Growing popularity of home-use resurfacing gadgets

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Suppliers

- 4.7.3Bargaining Power of Buyers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product

- 5.1.1Laser Resurfacing Devices

- 5.1.2RF Microneedling Systems

- 5.1.3Microdermabrasion Devices

- 5.1.4Chemical Peel Solutions & Kits

- 5.2By Technology

- 5.2.1Ablative

- 5.2.2Non-Ablative

- 5.3By Application

- 5.3.1Wrinkle & Fine-Line Reduction

- 5.3.2Scar & Acne-Scar Revision

- 5.3.3Hyper-Pigmentation / Melasma

- 5.3.4Skin Tightening & Texture Improvement

- 5.4By End User

- 5.4.1Dermatology Clinics

- 5.4.2Hospitals

- 5.4.3Medical Spas & Aesthetic Centers

- 5.4.4Home-Use / Consumer

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2India

- 5.5.3.3Japan

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4South America

- 5.5.4.1Brazil

- 5.5.4.2Argentina

- 5.5.4.3Rest of South America

- 5.5.5Middle East and Africa

- 5.5.5.1GCC

- 5.5.5.2South Africa

- 5.5.5.3Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Lumenis

- 6.3.2Candela Medical

- 6.3.3Cynosure

- 6.3.4Alma Lasers

- 6.3.5Cutera

- 6.3.6Sciton

- 6.3.7Lutronic

- 6.3.8Bausch Health – Solta Medical

- 6.3.9InMode

- 6.3.10Fotona

- 6.3.11Aerolase

- 6.3.12Bison Medical

- 6.3.13Venus Concept

- 6.3.14Sharplight Technologies

- 6.3.15DEKA M.E.L.A.

- 6.3.16Jeisys Medical

- 6.3.17Alma – Sisram Medical

- 6.3.18Aerolase Corporation

- 6.3.19BTL Aesthetics

- 6.3.20Syneron Medical

- 6.3.21Cutera Japan K.K.

- 6.3.22Asclepion Laser

- 6.3.23Shanghai Fosun Pharmaceutical – Sisram

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Skin Resurfacing Market Report Scope

As per the scope of the market, skin resurfacing is a type of skincare procedure performed by a dermatologist or physician to help improve skin texture and appearance. Skin resurfacing is a proven way to help reduce wrinkles, age spots, acne scars, and other blemishes as well as tighten skin and balance tone.

The Skin Resurfacing Market is segmented by product, application, type, and end-user. By product, the market is segmented into laser skin resurfacing machine, CO2 skin resurfacing machine, laser tips, and others. By application, the market is categorized into wrinkles, aging, skin pigmentation, acne, and other scars and others. Based on type, the market is bifurcated into ablative and non-ablative. By end-user, the market is segmented into hospitals, clinics, and others. By geography the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report offers the value in USD for the above segments.