Androgens And Anabolic Steroids Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

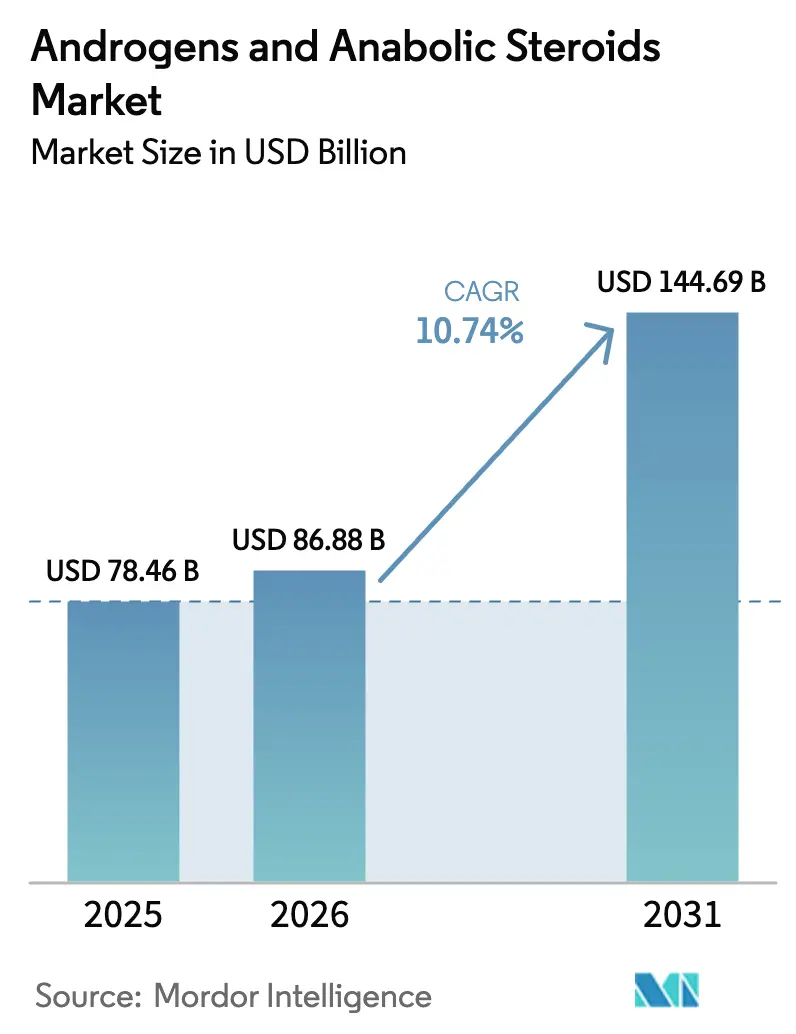

| Market Size (2026) | USD 86.88 Billion |

| Market Size (2031) | USD 144.69 Billion |

| Growth Rate (2026 - 2031) | 10.74% CAGR |

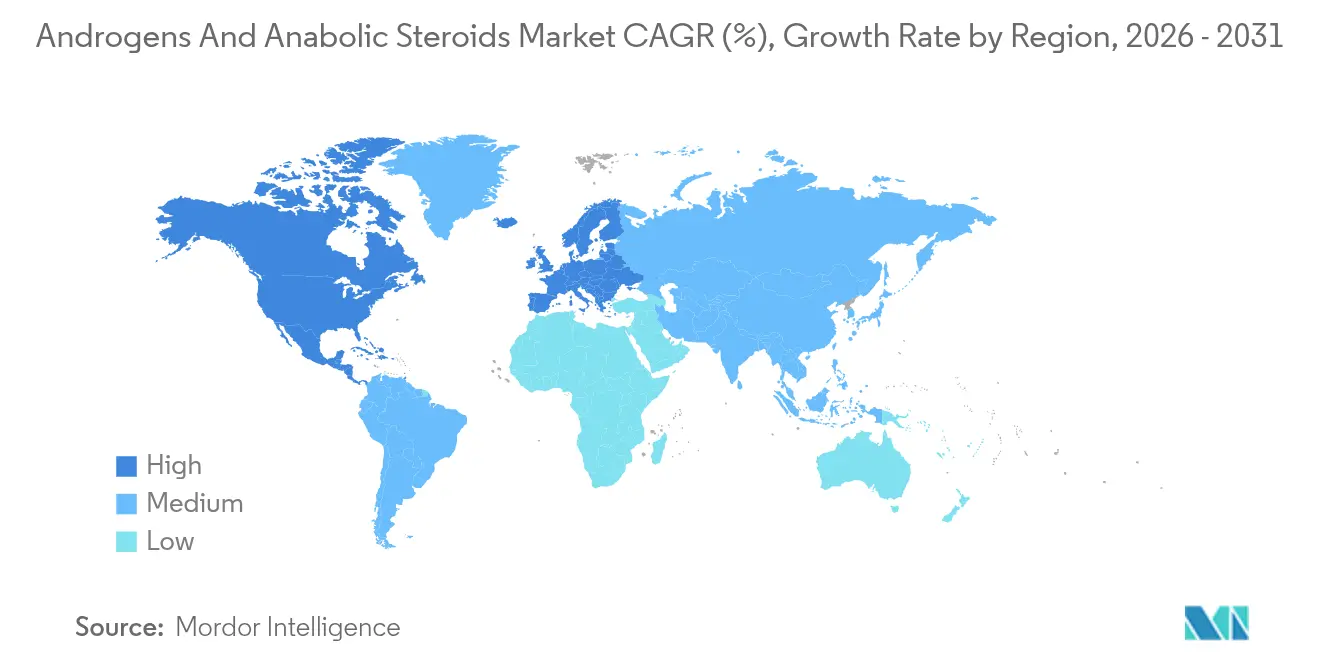

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

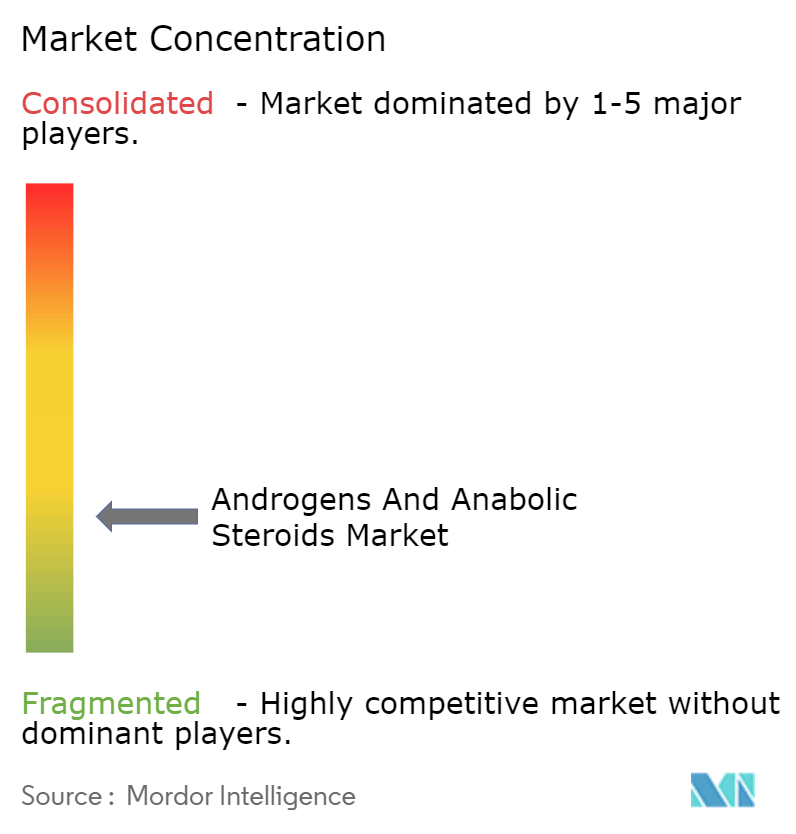

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Androgens And Anabolic Steroids Market Analysis by Mordor Intelligence

The androgens and anabolic steroids market size is expected to grow from USD 78.46 billion in 2025 to USD 86.88 billion in 2026 and is forecast to reach USD 144.69 billion by 2031 at 10.74% CAGR over 2026-2031. Current expansion is shaped by three forces: (1) the FDA’s February 2025 removal of testosterone black-box warnings, which has enlarged the eligible patient pool; (2) rapid uptake of long-acting, transdermal, and oral delivery technologies that improve adherence and broaden clinical settings; and (3) demographic ageing, with 38.7% of men aged 45 and above presenting biochemical hypogonadism, a level that materially widens therapeutic demand. Competitive intensity remains moderate as patent-protected innovators defend entrenched brands while specialist start-ups pursue oral bioavailability breakthroughs. Counterfeit proliferation and variable global scheduling rules restrain market momentum but have not altered the upward revenue trajectory.

Key Report Takeaways

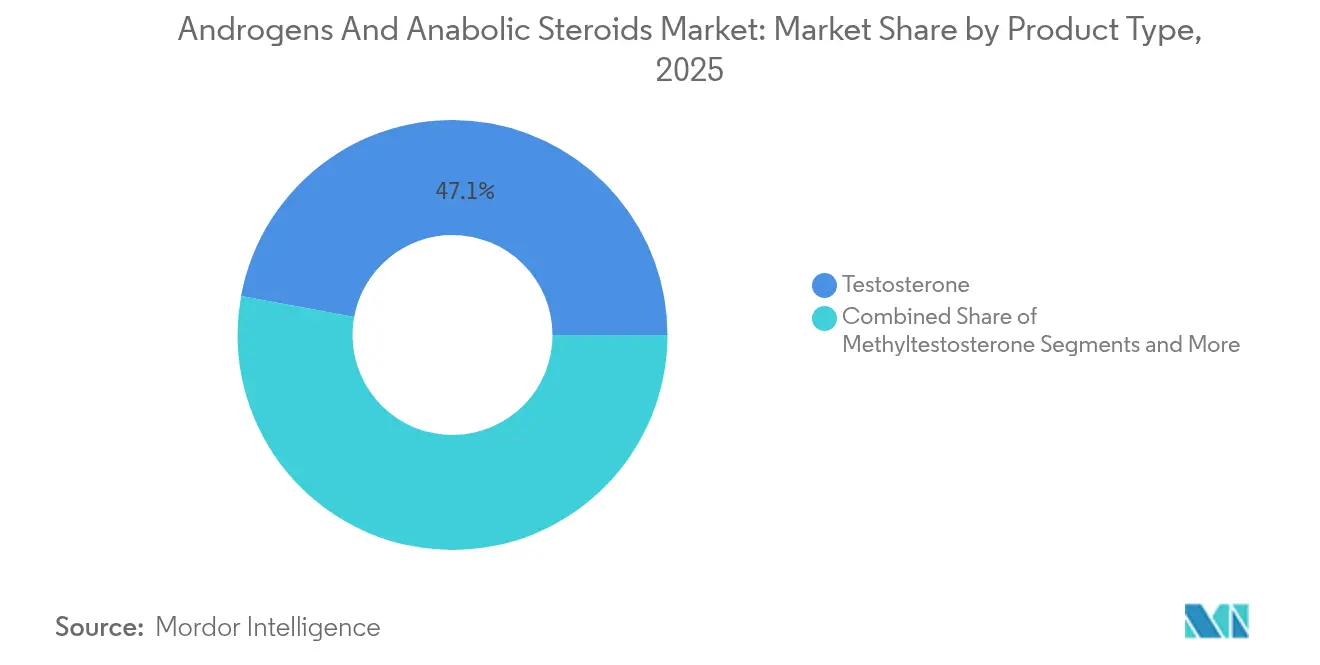

- By product type, testosterone led with 47.10% of the androgens and anabolic steroids market share in 2025, whereas oxandrolone is projected to grow at 11.32% CAGR through 2031

- By application, hypogonadism captured 54.30% share of the androgens and anabolic steroids market size in 2025; anemia treatment is expected to expand at 11.55% CAGR by 2031

- By route of administration, injectables held 61.40% share in 2025, while topical and transdermal systems are forecast to advance at 11.78% CAGR to 2031

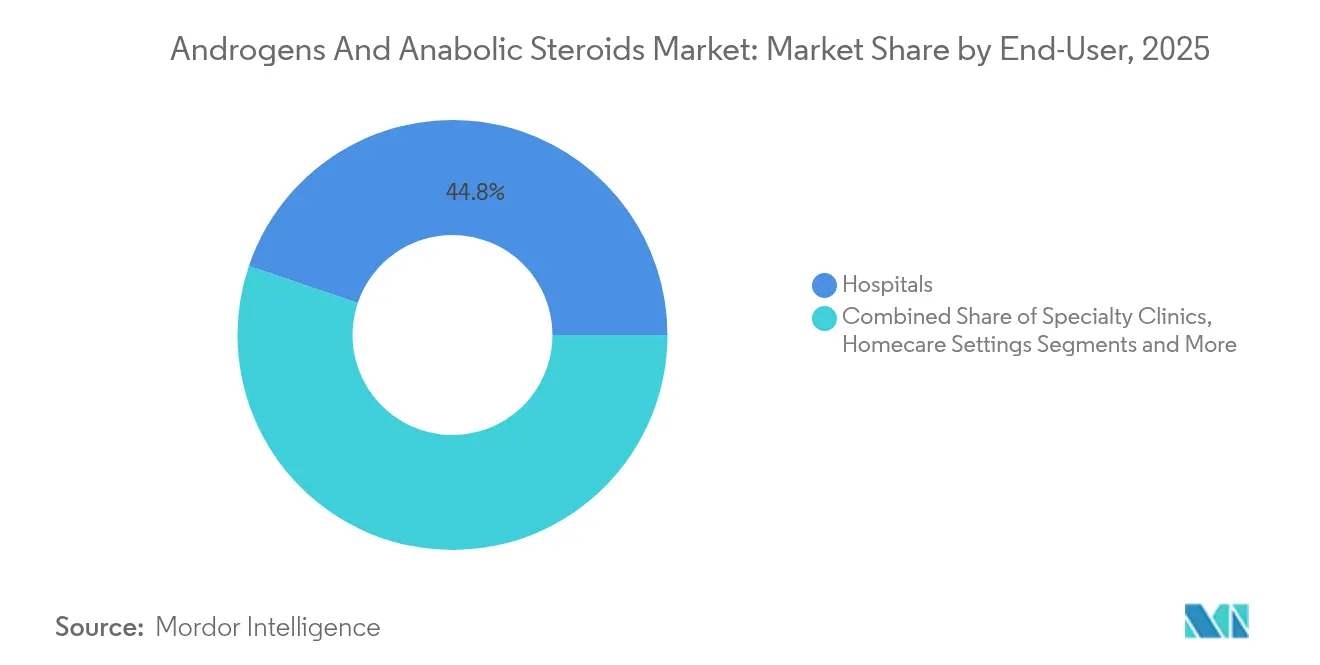

- By end-user, hospitals dominated with 44.80% revenue in 2025; home-care settings are poised for a 12.02% CAGR during 2026-2031

- By distribution channel, retail pharmacies accounted for 45.60% sales in 2025, and online pharmacies record the fastest 12.30% CAGR to 2031

- By geography, North America commanded 43.40% revenue in 2025, whereas Asia-Pacific is on track for a 12.62% CAGR up to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Androgens And Anabolic Steroids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Hypogonadism & Aging Male Population | +2.8% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| High Adoption In Sports & Bodybuilding | +1.9% | Global, concentrated in North America & Australia | Medium term (2-4 years) |

| Technological Advancements In Long-Acting & Transdermal Delivery | +2.1% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Emergence Of Sarms-Driven Interest In Anabolic Therapies | +1.4% | Global, early adoption in North America | Long term (≥ 4 years) |

| Increasing Female Androgen Therapy For HSDD | +1.2% | North America & Australia, limited EU adoption | Medium term (2-4 years) |

| Expansion Of Tele-Prescribing Platforms | +1.6% | North America & EU, emerging in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Hypogonadism & Ageing Male Population

Hypogonadism prevalence climbs with each decade of life, affecting one in five men in their 60 s and roughly one in two beyond 80 years. The Baltimore Longitudinal Study of Aging tracks an average 1% annual testosterone decline after age 30. The TRAVERSE cardiovascular-safety trial allayed historical risk concerns, encouraging primary-care physicians to treat symptomatic deficiency more readily [1]K. Grossmann, “TRAVERSE Trial Primary Results,” World Journal of Men’s Health, wjmh.org . United Nations projections show the global male population aged ≥65 doubling by 2050, positioning demographic ageing as a durable growth engine for the androgens and anabolic steroids market.

High Adoption in Sports & Bodybuilding

Cyber Juice uncovered thousands of monthly steroid shipments across 90 arrests in 2024 [2]Operation Cyber Juice Press Release, World Anti-Doping Agency, wada-ama.org. Legitimate sports-medicine use remains tethered to therapeutic-use exemptions that allow physiological testosterone maintenance in elite competitors. Switzerland’s 2024 drug-checking programme found 52% of sampled anabolic products counterfeit, illustrating quality-control gaps. Although regulatory bodies intensify policing, social-media-driven bodybuilding culture keeps discretionary demand resilient.

Technological Advances in Long-Acting & Transdermal Delivery

Three delivery innovations reshape patient experience: quarterly testosterone undecanoate injections, six-month subcutaneous pellets, and once-weekly transdermal patches such as the TEPI platform. Oral KYZATREX employs lymphatic absorption to avoid hepatic first-pass loss and has secured patent protection through 2040. Pfizer’s solvent-reduction manufacturing upgrades cut production waste by 50% and support greener supply chains. Collectively, these advances lift adherence, smooth serum-level fluctuations, and widen prescriber comfort.

Emergence of SARMs-Driven Interest in Anabolic Therapies

Selective androgen-receptor modulators deliver tissue-selective anabolic benefits with reduced virilisation. Phase III enobosarm trials report lean-mass gains and functional-mobility improvements in elderly cohorts. Regulatory oversight remains unsettled; the FDA prosecutes unapproved consumer sales, exemplified by 2025 seizures at Warrior Labz SARMs. Legitimate pipelines target cachexia, osteoporosis, and sarcopenia, charting a future competitive frontier inside the androgens and anabolic steroids industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Classification & Scheduling | -1.8% | Global, most restrictive in North America | Long term (≥ 4 years) |

| Adverse Side-Effect Profile & Litigation Risk | -1.3% | North America & EU, limited impact in APAC | Medium term (2-4 years) |

| Proliferation Of Counterfeit Online Steroid Products | -1.1% | Global, highest impact in emerging markets | Short term (≤ 2 years) |

| Uptake Of Non-Hormonal Muscle-Building Alternatives | -0.9% | North America & EU, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Classification & Scheduling

Schedule III status mandates special prescriber registration, controlled-substance ordering systems, and quota-bound manufacturing limits issued annually by the DEA [3]Drugs.com, “KYZATREX Product Monograph,” drugs.com . Pending telemedicine rules may further restrict remote initiation of testosterone therapy. Outside the United States, Europe enforces its own pharmacovigilance protocols, while Australia classifies most anabolics as Schedule 4 prescription drugs. Compliance burden elevates operating costs and elongates time-to-market for innovators.

Adverse Side-Effect Profile & Litigation Risk

Labeling now flags risks of atrial fibrillation, pulmonary embolism, and blood-pressure elevation, prompting cardiology clearance before therapy initiation. The post-TRAVERSE safety update eased macro cardiovascular fears yet introduced new monitoring mandates. Past U.S. mass-tort actions over undisclosed heart-attack risk heighten legal vigilance. Prescribers balance metabolic and quality-of-life gains against these liabilities, a calculus that tempers the overall growth curve of the androgens and anabolic steroids market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Testosterone Dominance Faces Diversification

Testosterone commanded 47.10% of 2025 revenue, confirming its primacy in the androgens and anabolic steroids market. Oxandrolone is poised for the sharpest 11.32% CAGR over 2026-2031, propelled by favorable anabolic-to-androgenic ratios in female and pediatric care. Methyltestosterone addresses niche acute indications that need swift serum elevation, whereas nandrolone and stanozolol treat wasting syndromes and hereditary angioedema. The arrival of oral KYZATREX signals technical maturity sufficient to challenge injectable hegemony.

Pipeline breadth is widening beyond legacy molecules. Selective androgen modulators and modified undecanoate esters illustrate how molecular tweaking can sustain patent life while refining safety. Production cost differentials between synthetic and bio-identical APIs steer pricing strategies, yet the androgens and anabolic steroids market size for testosterone itself is still projected to climb at near 8.6% CAGR because of sustained first-line preference amid guideline familiarity.

By Application: Hypogonadism Leadership Amid Therapeutic Expansion

Hypogonadism accounted for 54.30% of 2025 spend, anchoring clinical demand. Anaemia therapy is set to grow 11.55% CAGR, leveraging testosterone’s erythropoietic ability in chronic-disease cohorts. Breast-cancer uses remain niche yet clinically essential for estrogen-receptor–positive subtypes. Exploratory trials investigate metabolic, frailty, and sarcopenia indications, hinting at continual broadening of the androgens and anabolic steroids market.

In diabetes prevention, the TRAVERSE substudy showed testosterone therapy halved conversion from pre-diabetes to diabetes in hypogonadal men, a signal drawing endocrinology interest. Female hypoactive sexual-desire disorder gained regulatory foothold in Australia, sparking off-label curiosity elsewhere. As evidence accumulates across multi-system endpoints, the application palette increasingly extends therapeutic relevance beyond urology and andrology clinics.

By Route of Administration: Injectable Dominance Challenged by Innovation

Injectables retained 61.40% share in 2025, reflecting predictable pharmacokinetics and physician familiarity. Nonetheless, transdermal gels, patches, and sprays should register the fastest 11.78% CAGR, supported by improved bioavailability and cosmetic acceptability. Oral formulations, historically limited by hepatic first-pass metabolism, gain fresh momentum via lymphatic-absorption chemistry. Implantable pellets furnish ultra-long coverage for adherence-challenged patients.

Manufacturers counter compliance gaps using prefilled syringes and autoinjectors that cut clinic visit frequency. These advances suggest that the injectables cohort will cede incremental share, although its absolute value inside the androgens and anabolic steroids market size remains on an upward curve given category-wide growth.

By End-User: Hospital Leadership Amid Care Decentralisation

Hospitals generated 44.80% of global revenue in 2025 thanks to initial diagnostic work-ups and IV loading protocols. Home-care settings, empowered by telemedicine and self-injection education, will grow fastest at 12.02% CAGR. Specialty clinics offer subscription-based hormone optimisation programmes, blending lab testing with compounded therapies. Fitness centres flirt with medical partnerships yet remain regulated away from direct dispensing.

Tele-prescribing platforms integrate e-commerce pharmacies, wearable monitoring, and asynchronous consultations, consolidating a holistic patient journey. While decentralising care fragments volumes across sites, hospitals still anchor complex comorbidity management, sustaining their leading chunk of the androgens and anabolic steroids market.

By Distribution Channel: Retail Pharmacy Dominance Amid Digital Transformation

Retail chains handled 45.60% of 2025 scripts, leveraging insurance-network ties and last-mile convenience. Online pharmacies will accelerate at 12.30% CAGR, propelled by direct-to-consumer advertising and discrete delivery. Hospital pharmacies serve inpatient dosing and discharge kits. Specialty pharmacies carve value through adherence coaching and prior-authorisation support.

Regulators tighten e-pharmacy licensing for controlled substances, yet secure telehealth ecosystems mitigate diversion risk. Fake product crackdowns boost credibility of legitimate platforms, thereby expanding the trusted addressable pool inside the androgens and anabolic steroids market.

Geography Analysis

North America captured 43.40% of 2025 revenue, underpinned by robust insurance coverage, physician familiarity, and the pivotal FDA label revision that eliminated the cardiovascular black-box warning. The United States alone drives more than 80% of regional turnover, while Canada’s provincial reimbursement and Mexico’s medical-tourism corridors add incremental demand. Ageing demographics and high obesity prevalence reinforce a stable clinical caseload.

Europe ranks second, benefiting from advanced healthcare systems, yet conservative prescribing norms temper penetration. The European Medicines Agency concluded its testosterone review without extra cardiovascula¬r restrictions, maintaining market stability. Germany leads prescription volumes, whereas Spain gains manufacturing prominence through new hormone-therapy facilities backed by Besins Healthcare.

Asia-Pacific is the fastest-growing arena at a 12.62% CAGR. China’s ageing male cohort and rising disposable incomes shape outsized potential, while Japan’s reimbursement clarity supports mature adoption. Australia’s approval of female testosterone therapy signals regulatory openness to novel indications. India’s bulk-drug capacity attracts contract-manufacturing mandates, and South Korea’s telemedicine infrastructure fosters remote initiation programmes, collectively pushing regional contribution upward in the androgens and anabolic steroids market.

Competitive Landscape

Market concentration is moderate. AbbVie safeguards AndroGel and coordinates newer injectables, Bayer co-develops long-acting undecanoate, and Pfizer invests in eco-efficient synthesis lines. Endo International repositions Aveed in niche endocrinology channels. Generic challengers such as Teva and Cipla exploit timeline lapses in patent coverage to grow share through bioequivalent injectables. Marius Pharmaceuticals differentiates with oral KYZATREX, supported by patents extending to 2040.

Strategic moves illustrate defensive patenting and forward integration. AbbVie signed supply agreements with leading telehealth platforms to secure channel control, while Bayer partnered with Medherant for TEPI patch co-development. Pfizer’s green-chemistry retrofits underscore sustainability positioning. Start-up entrants pursue selective androgen modulators that may leapfrog testosterone’s side-effect profile, potentially redrawing the androgens and anabolic steroids industry competitive map post-2030.

Collaboration dominates R&D funding because multiyear cardiovascular-safety registries demand pooled resources. Licensing of Lipocine’s TLANDO to Verity Pharma signals willingness to outsource commercial execution for niche formulations. Market entry barriers remain material owing to DEA scheduling, complex manufacturing, and the necessity for long-term safety data; however, sustained demographic tailwinds continue to feed new-entrant pipelines.

Androgens And Anabolic Steroids Industry Leaders

Pfizer Inc.

Abbvie Inc.

Endo Pharmaceuticals Inc.

Teva Pharmaceuticals

Cipla Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The FDA granted Fast Track designation to LPCN 1148 for sarcopenia in decompensated cirrhosis patients.

- June 2024: Mangoceuticals introduced oral dissolvable tablets of enclomiphene citrate, pregnenolone, and DHEA in the United States.

- February 2024: Lipocine transferred U.S. commercialization of TLANDO to Verity Pharma, ensuring continuity of its titration-free oral TRT option.

Global Androgens And Anabolic Steroids Market Report Scope

According to the scope, androgens are natural hormones crucial for male development and reproduction. In contrast, anabolic steroids are synthetic substances developed to replicate these effects, primarily focusing on muscle growth and tissue repair. These steroids are utilized to address delayed puberty in adolescent males, breast cancer in females, and conditions like hypogonadism and impotence in males. Additionally, they treat anemia, osteoporosis, weight loss, and various other disorders related to hormonal imbalances.

The androgens and anabolic steroids market is segmented by product type, application, route of administration, end-user, distribution channel, and geography. By product type, the market is segmented into testosterone, methyltestosterone, oxandrolone, and other anabolic steroids. By application, the market is segmented into hypogonadism, anemia, breast cancer, and other applications. By route of administration, the market is segmented into oral, injectable, and other routes of administration. By end-user, the market is segmented into hospitals, specialty clinics, homecare settings and other end users. By distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market size is provided in terms of USD value.

| Testosterone | Cypionate |

| Enanthate | |

| Undecanoate | |

| Methyltestosterone | |

| Oxandrolone | |

| Other Anabolic Steroids |

| Hypogonadism |

| Anemia |

| Breast Cancer |

| Other Applications |

| Oral | |

| Injectable | |

| Topical & Transdermal | Gel |

| Patch | |

| Implantable Pellets |

| Hospitals |

| Specialty Clinics |

| Homecare Settings |

| Fitness Centers & Gyms |

| Tele-health Platforms |

| Hospital Pharmacy |

| Retail Pharmacy |

| Online Pharmacy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Testosterone | Cypionate |

| Enanthate | ||

| Undecanoate | ||

| Methyltestosterone | ||

| Oxandrolone | ||

| Other Anabolic Steroids | ||

| By Application | Hypogonadism | |

| Anemia | ||

| Breast Cancer | ||

| Other Applications | ||

| By Route of Administration | Oral | |

| Injectable | ||

| Topical & Transdermal | Gel | |

| Patch | ||

| Implantable Pellets | ||

| By End-User | Hospitals | |

| Specialty Clinics | ||

| Homecare Settings | ||

| Fitness Centers & Gyms | ||

| Tele-health Platforms | ||

| By Distribution Channel | Hospital Pharmacy | |

| Retail Pharmacy | ||

| Online Pharmacy | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Androgens And Anabolic Steroids Market?

The Androgens And Anabolic Steroids Market size is expected to reach USD 86.88 billion in 2026 and grow at a CAGR of 10.74% to reach USD 144.69 billion by 2031.

Which product type generates the most revenue?

Testosterone leads with 47.10% share in 2025, although oxandrolone is the fastest-growing molecule through 2031.

Who are the key players in Androgens And Anabolic Steroids Market?

Pfizer Inc., Abbvie Inc., Endo Pharmaceuticals Inc., Teva Pharmaceuticals and Cipla Limited are the major companies operating in the Androgens And Anabolic Steroids Market.

Which is the fastest growing region in Androgens And Anabolic Steroids Market?

Asia-Pacific is forecast to register a 12.62% CAGR, outpacing all other regions up to 2031.

Which region has the biggest share in Androgens And Anabolic Steroids Market?

In 2025, the North America accounts for the largest market share in Androgens And Anabolic Steroids Market.

Page last updated on: