Recombinant Factor C Assay Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

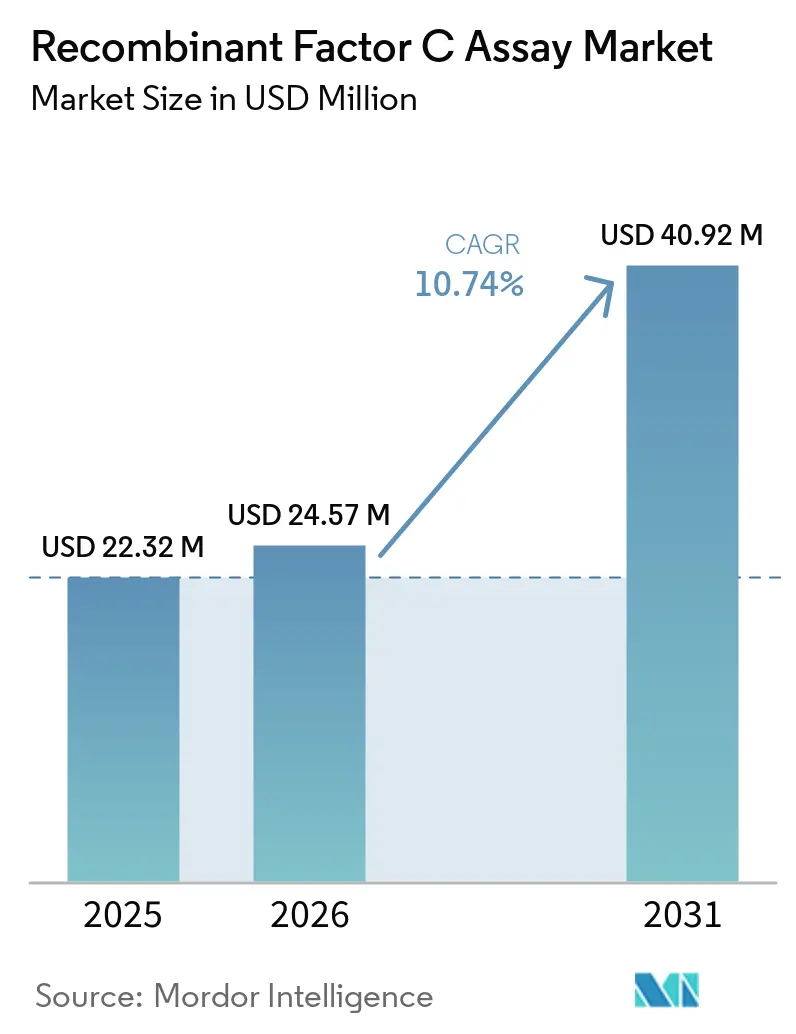

| Market Size (2026) | USD 24.57 Million |

| Market Size (2031) | USD 40.92 Million |

| Growth Rate (2026 - 2031) | 10.74% CAGR |

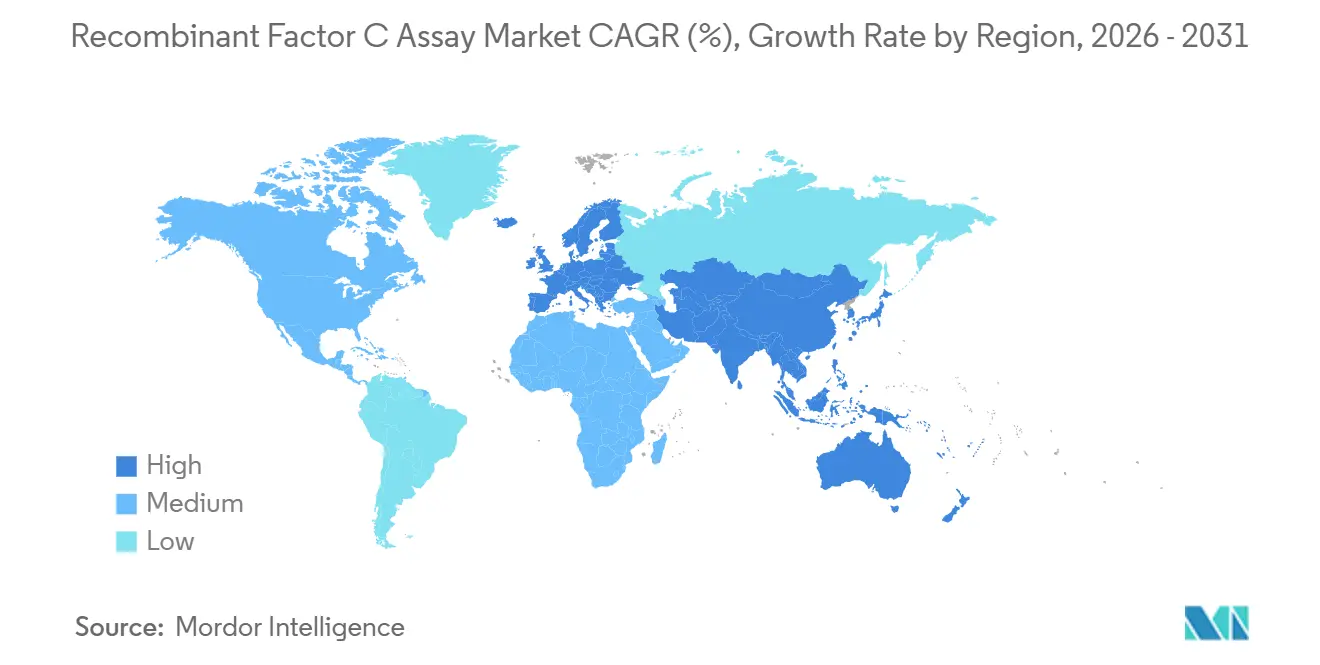

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recombinant Factor C Assay Market Analysis by Mordor Intelligence

The Recombinant Factor C Assay Market size is projected to be USD 22.32 million in 2025, USD 24.57 million in 2026, and reach USD 40.92 million by 2031, growing at a CAGR of 10.74% from 2026 to 2031.

Pharmacopeial acceptance across the United States and Europe is now formalized, which changes inspection certainty and accelerates validation roadmaps for regulated manufacturers. Conservation and ESG scrutiny of horseshoe crab dependence keeps pressure on legacy LAL workflows, with recent harvest tallies making biodiversity risk more visible to boards and investors. Concurrently, QC lab automation and digital traceability are reducing operator variability and audit burden, while modern fluorescence microplate readers cut cycle times for 96-well plates to seconds, which helps time-sensitive biologics and advanced therapies. Regional heterogeneity still imposes dual-method comparability for multi-market submissions, which sustains a dual-technology reality in the near term.

Key Report Takeaways

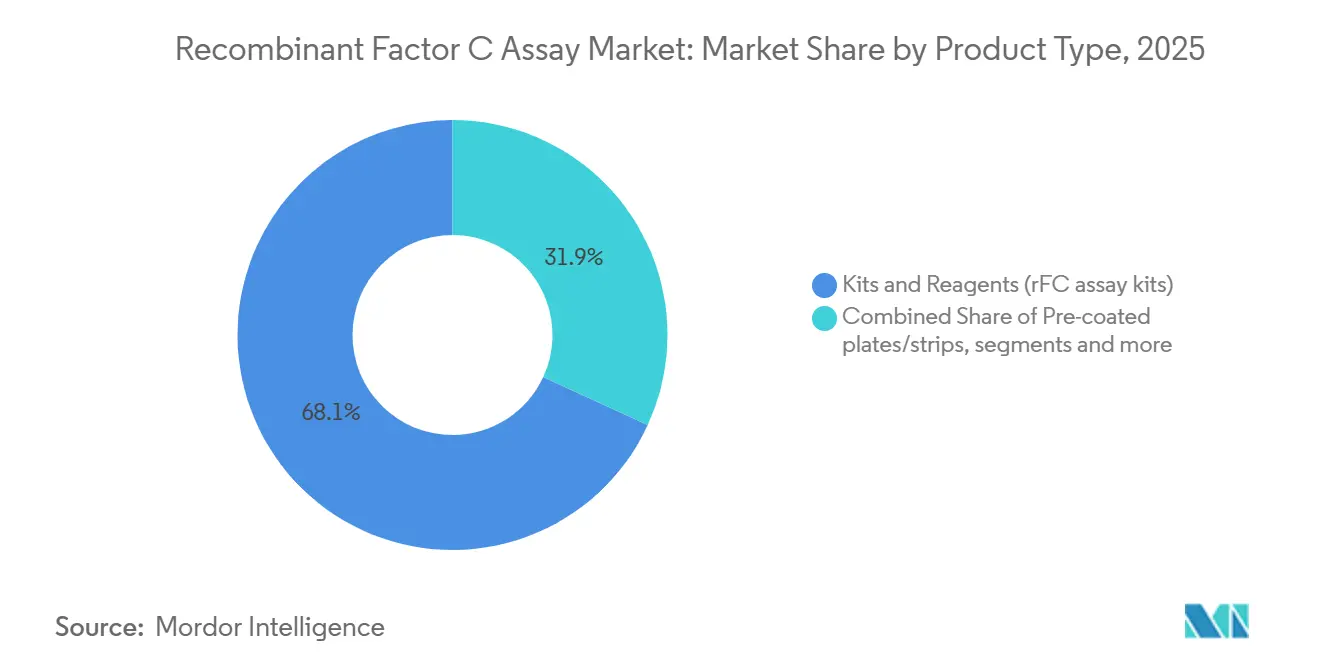

- By product type, kits and reagents led with 68.12% revenue share in 2025. Automation and compliance software is projected to post the fastest growth at a 12.56% CAGR through 2031.

- By application, in-process water and raw-materials testing accounted for a 35.61% share of the recombinant Factor C assay market size in 2025. Advanced therapies quality control is forecast to expand at a 12.09% CAGR to 2031.

- By end user, pharma and biotech manufacturers held the largest share at 55.41% in 2025. The same segment is expected to record the highest growth at a 13.14% CAGR through 2031.

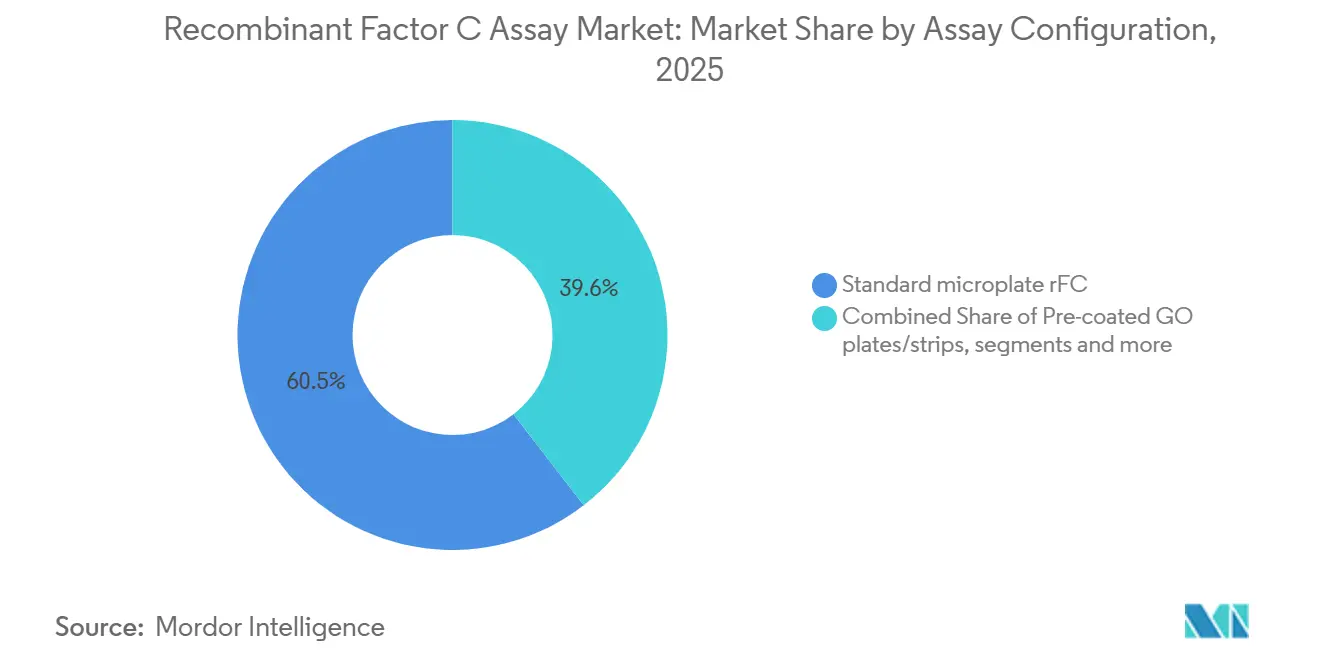

- By assay configuration, standard microplate formats commanded 60.45% share in 2025. Automation-integrated workflows are projected to grow at a 13.45% CAGR through 2031.

- By throughput tier, high-volume QC labs led with 55.09% of 2025 demand. Mid-volume facilities are expected to grow fastest at an 11.24% CAGR to 2031.

- By geography, North America held 42.17% of the recombinant Factor C assay market share in 2025. Asia-Pacific is projected to be the fastest-growing region at a 12.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Recombinant Factor C Assay Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharmacopeial acceptance accelerates mainstream adoption | +2.8% | Global, with early gains in North America and Europe | Medium term (2-4 years) |

| ESG and conservation pressures to replace LAL with animal-free rFC | +2.1% | North America and Europe core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| First FDA drug release using rFC builds confidence in regulated use | +1.5% | Global | Short term (≤ 2 years) |

| QC lab automation and digital traceability reduce OPEX and speed validation | +2.3% | North America, Western Europe, Asia-Pacific urban hubs | Medium term (2-4 years) |

| Enterprise supply-chain risk diversification and multi-sourcing favor rFC | +1.2% | Global, concentrated in biopharma clusters | Medium term (2-4 years) |

| Beta-glucan independence reduces invalid and OOS retesting burden | +1.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pharmacopeial Acceptance Accelerates Mainstream Adoption

Formal recognition of non-animal endotoxin methods in USP Chapter 86, effective May 1, 2025, removes the key barrier of inspection uncertainty for manufacturers in the United States[1]United States Pharmacopeia, “Chapter for endotoxin testing using non-animal derived reagents published for early adoption,” USP, usp.org . Alignment on water testing has become a catalyst because it represents a high-volume, lower-risk starting point for rFC deployment under routine GMP. Japan, South Korea, and China still operate with language that ranges from under consideration to advisory status, which leaves global suppliers running dual-method comparability in those markets. The net effect is a tiered adoption curve that moves faster in North America and Europe and more cautiously across parts of Asia until further harmonization takes effect.

ESG and Conservation Pressures to Replace LAL with Animal-Free rFC

Horseshoe crab harvest data has sharpened the sustainability debate, with the biomedical harvest in 2022 and bait harvest in 2024 highlighting biodiversity risks that are now tracked by investors and industry coalitions. Corporate ESG programs increasingly view rFC adoption as a measurable action to mitigate ecosystem impact while maintaining quality standards for patient safety, which aligns with the 3Rs principle used by European regulators. The reduction in dependence on wildlife-derived reagents also helps de-risk supply chains that are sensitive to seasonal and regulatory shocks in fishery management. Sector initiatives and purchaser expectations are adding momentum to in-house policy updates that specify animal-free methods where compendial paths are open. As users expand rFC to time-critical releases, they benefit from fewer beta-glucan related false positives, which reduces waste and rework and improves sustainability metrics in practice.

QC Lab Automation and Digital Traceability Reduce OPEX and Speed Validation

Modern fluorescence plate readers now auto-calibrate each well to optimal sensitivity, which removes manual gain-setting and compresses full-plate read times for rFC runs to near real time. Robotics integration can push automation above 90% for sample and dilution handling, which shifts analyst effort from pipetting to review and decision-making. Data integrity platforms log each action with role-based access and audit trails, which helps reduce observations tied to 21 CFR Part 11 gaps during inspections. Automated workflows can also lower invalid rates by limiting beta-glucan interference and operator variability, which shortens hold times for sensitive biologics. Combined hardware and software upgrades therefore support the shift in the recombinant Factor C assay market where speed, traceability, and repeatability are now core purchase criteria for QC leaders.

Beta-Glucan Independence Reduces Invalid and OOS Retesting Burden

Classical LAL methods include Factor G, which can react with beta-glucans from cellulose or plant-derived matrices and trigger false positives that drive out-of-specification events and retests. rFC is independent of Factor G, which lowers the rate of invalid runs in matrices with known beta-glucan loads such as certain excipients and filter trains. This characteristic also improves method suitability for products that need tight endotoxin limits, especially where rapid turnaround is essential. The outcome is fewer batch holds and less material waste, which improves cycle times in high-throughput facilities using the recombinant Factor C assay market as an operational lever. With integrated software, audit-ready logs of each result can be generated on demand for reviewers, which helps maintain consistency during regulatory audits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Validation and comparability workload with heterogeneous regional acceptance | -1.8% | Global, acute in Japan, China, South Korea | Medium term (2-4 years) |

| Gel-clot dominance and cost constraints in parts of Asia, Africa, South America | -1.3% | Asia-Pacific excluding Japan, Africa, Latin America | Long term (≥ 4 years) |

| Higher rFC kit costs and fluorescence reader capex for small labs | -0.8% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Inter-supplier variability and product-matrix effects slow standardization | -0.6% | Global, particularly multi-region manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Validation and Comparability Workload with Heterogeneous Regional Acceptance

Manufacturers targeting multiple regulatory jurisdictions face a heavier validation plan because compendial language remains misaligned outside the United States and Europe. China frames rFC in guidance as a principle rather than a binding requirement, and Japan is still evaluating comparative evidence, which sustains dual-method comparability studies for regional dossiers. These programs require multi-lot recovery evaluations and trending analyses, which extend timelines for routine release and for submissions that cross multiple markets. Some product classes also present matrix effects that tighten dilution windows for rFC, which raises the method-suitability workload for complex vaccines and vectors. Until broader harmonization is achieved, large sponsors will continue to run LAL and rFC in parallel for certain markets, which sustains higher operating costs for global portfolios.

Gel-Clot Dominance and Cost Constraints in Parts of Asia, Africa, South America

Legacy gel-clot methods remain common where single-parameter endpoint tests satisfy local expectations and where quantitative instrumentation is less prevalent. In these settings, regulators do not always enforce modernized pharmacopeial chapters, which reduces the forcing function that drove adoption in the United States and Europe. Supply-side economics also influence purchase decisions when wildlife-derived reagents remain available at lower apparent prices, even as conservation bodies flag sustainability concerns. Workforce skills and infrastructure shape adoption as well because rFC kinetics and fluorescence interpretation assume consistent power, temperature control, and trained analysts. Over time, the recombinant Factor C assay market gains from falling hardware costs and vendor training, but short-term dynamics keep a dual-technology landscape intact across cost-sensitive regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumable Reagents Lead, Software Posts Steepest Growth

Kits and reagents held the largest share at 68.12% of 2025 revenue, anchored by recurring use that scales with test volume across large biopharma QC operations. Vendors in the recombinant Factor C assay market emphasize format innovations such as pre-optimized substrates and immobilized controls that reduce operator variability in plate-based assays. Instruments and readers showed healthy replacement demand as QC groups retired aging turbidimeters and standardized on multimode fluorescence systems from established suppliers in North America and Europe. Automation and compliance software is projected to deliver the fastest growth at a 12.56% CAGR through 2031 as 21 CFR Part 11 enforcement drives electronic signatures, audit trails, and LIMS integrations across regulated sites. Contract testing services remain a practical route for smaller firms that need method suitability or overflow capacity without full in-house investment, which keeps service demand relevant to the recombinant Factor C assay market.

The recombinant Factor C assay industry continues to migrate toward software-enabled workflows that make complex testing repeatable and audit-ready at scale. Pre-validated software packages translate into shorter validation cycles for change controls and submissions, which reduces friction during inspections. Reader innovations like enhanced dynamic range enable mixed high and low signals on a single plate without manual gain steps, which protects accuracy on first pass for diverse matrices. Across buyers, service models and training support adoption among mid-size QC labs that prefer staged transitions rather than full automation in one step, which diversifies the recombinant Factor C assay market with hybrid operating models.

By Application: In-Process Dominates, Advanced Therapies Surge

In-process water and raw-materials testing captured 35.61% of activity in 2025 and remains the most frequent use case because purified water and buffers account for a large share of daily BET volume in regulated plants. Many adopters begin with water testing because compendial pathways are clear and matrix effects are limited, which creates a safe entry point to validate rFC under routine conditions. Finished product release stays more complex since matrix interferences and dilution limits can alter method suitability, which raises the stakes for first-pass success. Device testing remains a steady segment due to ISO and FDA expectations for extract testing and risk management, where animal-free methods align with broader regulatory goals for the recombinant Factor C assay market[2]ACROBiosystems, “Comparability Between Recombinant Factor C and Traditional LAL Assay in Endotoxin Detection,” ACROBiosystems, acrobiosystems.com .

Advanced therapies quality control is projected to expand at a 12.09% CAGR as sponsors scale autologous and allogeneic platforms with very short release windows that cannot absorb retests. EMA’s updated guidance for investigational ATMPs strengthens expectations around contamination controls in clinical production, which aligns well with fast, animal-free BET pipelines. Where beta-glucan exposure is likely due to filters, excipients, or process trains, rFC’s independence from Factor G reduces false positives and shortens hold times. In this context, the recombinant Factor C assay market provides a practical route to improve release reliability for cell and gene therapy workflows that cannot tolerate delays.

By End User: Pharma and Biotech Manufacturers Dominate, CDMOs Gaining

Pharma and biotech manufacturers accounted for 55.41% of demand in 2025 due to the scale of in-house QC labs and the footprint of biologics and sterile injectables in commercial pipelines. These facilities maintain high test frequencies and prioritize automation that reduces analyst time and invalid rates, which strengthens adoption for compliant rFC platforms in the recombinant Factor C assay market. This end-user segment is forecast to grow at 13.14% as new biologics require validated BET at each stage from in-process to final release, where digital traceability and audit readiness are now standard expectations.

CDMOs and CMOs highlight dual-method capability for sponsors that need flexibility during tech transfer and submission planning, which positions rFC as both a sustainability and performance differentiator. Medical device manufacturers engage selectively where device-extract matrices and packaging risks have created beta-glucan interference, which gives rFC a targeted advantage in specific workflows. Across end users, the recombinant Factor C assay market benefits from enterprise policies that embed animal-free methods into site standards once validation experience accumulates and inspection outcomes normalize.

By Assay Configuration: Microplate Standard Leads, Automation Fastest

Standard microplate rFC configurations led with 60.45% of 2025 revenue, reflecting their role as the workhorse platform for mid-to-high volume labs that require throughput and LIMS connectivity. Full-plate reads on modern instruments take seconds, which compresses turnaround and supports the recombinant Factor C assay market where speed and repeatability are material to batch disposition. Pre-coated formats reduce setup time and operator variability by shipping with fixed standards or controls that hydrate in-place, which simplifies repeatability in validated environments.

Automation-integrated workflows are projected to achieve the fastest growth at a 13.45% CAGR as robotics and readers integrate with compliant software to create near end-to-end automation. Integrated systems that prepare dilutions, load plates, and capture secure data help minimize OOS events and shorten review cycles, which shifts headcount from repetitive tasks to investigation and release. This trend aligns with the recombinant Factor C assay industry as buyers seek scalability and predictability for submission timelines and inspections.

By Throughput Tier: High-Volume Labs Lead, Mid-Volume Accelerates

High-volume QC labs accounted for 55.09% of demand in 2025 because large campuses run extensive BET programs that align with integrated robotics and digital traceability. These facilities rely on the recombinant Factor C assay market to reduce retests and enable faster decision-making on holds, which optimizes working capital in biologics operations. The operational benefits include consistent kinetics across plates and secure audit trails that can be generated quickly during inspections.

Mid-volume labs are expected to grow at an 11.24% CAGR as biotechs move from CRO reliance to in-house QC that balances instrument cost with workflow gains. Pre-validated kits and standardized protocols from suppliers reduce validation timelines, which makes transitions more feasible for lean teams. This dynamic broadens access to the recombinant Factor C assay market and supports the long-run shift to animal-free QC.

Geography Analysis

North America held 42.17% of the recombinant Factor C assay market share in 2025 due to early alignment with USP Chapter 86 and concentrated biopharma manufacturing across key hubs. The region benefits from a robust ecosystem of QC automation providers and software vendors that support 21 CFR Part 11 compliance, which increases the readiness to adopt rFC in validated workflows. Public conservation data on horseshoe crabs resonates across stakeholders, which supports corporate policies that favor non-animal reagents for sustainability and supply chain resilience. North American CDMOs list recombinant methods in their service portfolios, which helps smaller sponsors transition without full on-site investments[3]Gilles Gauvry, “USP Chapter 86 Bacterial Endotoxins Test Using Recombinant Reagents,” ERDG via ASMFC, asmfc.org .

EMA’s updated expectations for ATMPs in clinical production reinforce the value of rapid, animal-free endotoxin testing across cell and gene therapy programs. Across the region, capital planning cycles and replacement schedules shape the pace of transition as older turbidimetric readers give way to multimode fluorescence in GMP facilities.

Asia-Pacific is projected to grow faster than the global average as India and China scale biologics and biosimilar manufacturing capacity and as regional suppliers localize reagent production. Regulatory language remains more conservative in several countries, which sustains dual-method comparability where rFC is advisory rather than compendial, as reflected in current China guidance. Japan continues to examine comparative evidence for recombinant methods, and emerging regulatory updates in South Korea signal more alignment with U.S. expectations in the near term. As harmonization advances, the recombinant Factor C assay market will gain from faster validations and lower reliance on wildlife-derived reagents across regional manufacturing centers.

Competitive Landscape

The market remains fragmented because many QC buyers are transitioning from legacy LAL methods on different timelines and because regional regulatory heterogeneity shapes the validation burden. First movers include suppliers that combine reagents with automation and compliant software to deliver turnkey packages designed for regulated plants in North America and Europe. Reader vendors highlight enhanced dynamic range and speed benefits that collapse 96-well reads to seconds and remove manual gain settings, which underpins productivity cases for rFC adoption. Distributors and regional integrators also fill gaps by packaging instruments, consumables, and support into complete QC solutions for mid-volume labs.

Strategic launches reflect a shift to animal-free rapid testing in cartridge and automated plate formats. In January 2024, Charles River introduced Endosafe Trillium recombinant cartridges that deliver rapid BET and integrate with existing Endosafe systems, which lowers adoption barriers for legacy users. Vendors also emphasize data integrity by embedding audit trails, role-based access, and automated result flagging, which aims to reduce inspection findings tied to electronic records. In pre-validated plate formats, suppliers promote standardized controls to reduce day-to-day variability across analysts and sites.

Recombinant Factor C Assay Industry Leaders

ACROBiosystems Co., Ltd.

Bioendo rFC Endotoxin Test Kit

bioMérieux SA

GenScript Biotech Corporation

Lonza Group AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The European Pharmacopoeia Commission incorporated recombinant Factor C into general chapter 2.6.14 Bacterial endotoxins of the European Pharmacopoeia as one of seven methods, reinforcing patient safety and sustainability aligned with the 3Rs principle. This change follows the discontinuation of the rabbit pyrogen test from January 1, 2026, and gives users a reliable, animal-free alternative.

- May 2025: The United States Pharmacopeia made Chapter 86 Bacterial Endotoxins Test Using Recombinant Reagents official, permitting rFC and rCR as alternatives to LAL for compendial testing.

- January 2024: Charles River Laboratories launched Endosafe Trillium recombinant cartridges, the first rapid animal-free BET in cartridge format, with beta-study equivalency to LAL and compatibility with existing Endosafe instruments, targeting time-sensitive biologics that need fast batch release.

Global Recombinant Factor C Assay Market Report Scope

As per the scope of the report, the Recombinant Factor C (rFC) assay, a sustainable and highly specific alternative to Limulus Amebocyte Lysate (LAL) tests, is revolutionizing bacterial endotoxin detection. By utilizing a recombinant version of the Factor C enzyme cloned from horseshoe crabs, the assay simplifies the process into a single enzymatic step, delivering fluorescence-based readings with precision and efficiency. The recombinant factor C (rFC) assay market is segmented by product type, application, end user, assay configuration, throughput tier, and geography. By product type, the market is segmented as kits & reagents (rFC assay kits), pre-coated plates/strips, instruments & readers, automation & compliance software, and contract testing services. By application, the market is segmented into in-process water & raw materials, final drug product release, advanced therapies (cell/gene therapy) QC, medical device BET, and others. By end user type, the market is segmented as pharma & biotech manufacturers, CDMOs/CMOs, medical device manufacturers, and others. By assay configuration, the market is segmented as standard microplate rFC, pre-coated GO plates/strips, and automation-integrated rFC workflows. By throughput tier, the market is segmented as high-volume QC labs, mid-volume labs, and low-volume/point workflows. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Kits & Reagents (rFC assay kits) |

| Pre-coated plates/strips |

| Instruments & Readers |

| Automation & Compliance Software |

| Contract Testing Services |

| In-process water & raw materials |

| Final drug product release |

| Advanced therapies (cell/gene therapy) QC |

| Medical device BET |

| Others |

| Pharma & Biotech manufacturers |

| CDMOs/CMOs |

| Medical device manufacturers |

| Others |

| Standard microplate rFC |

| Pre-coated GO plates/strips |

| Automation-integrated rFC workflows |

| High-volume QC labs |

| Mid-volume labs |

| Low-volume/point workflows |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Kits & Reagents (rFC assay kits) | |

| Pre-coated plates/strips | ||

| Instruments & Readers | ||

| Automation & Compliance Software | ||

| Contract Testing Services | ||

| By Application | In-process water & raw materials | |

| Final drug product release | ||

| Advanced therapies (cell/gene therapy) QC | ||

| Medical device BET | ||

| Others | ||

| By End User | Pharma & Biotech manufacturers | |

| CDMOs/CMOs | ||

| Medical device manufacturers | ||

| Others | ||

| By Assay Configuration | Standard microplate rFC | |

| Pre-coated GO plates/strips | ||

| Automation-integrated rFC workflows | ||

| By Throughput Tier | High-volume QC labs | |

| Mid-volume labs | ||

| Low-volume/point workflows | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the recombinant Factor C assay market growth outlook through 2031?

The recombinant Factor C assay market size is projected to reach USD 40.92 million by 2031, with a 10.74% CAGR over 2026 to 2031 based on maturing pharmacopeial acceptance, ESG pressure, and QC automation.

Which regions are leading and growing fastest in this space?

North America led with 42.17% share in 2025 due to early USP Chapter 86 alignment, while Asia-Pacific is projected to grow fastest as regional manufacturing scales and regulatory language evolves.

What applications are most important for adoption in QC?

In-process water and raw-materials testing holds the largest share because of high daily test volumes, and advanced therapies quality control is the fastest growing application given tight release windows and contamination limits.

What assay configurations are preferred by QC labs?

Standard microplate rFC formats lead due to throughput and LIMS connectivity, while automation-integrated workflows grow fastest with robotics, rapid readers, and compliant software for end-to-end traceability.

What are the main barriers to wider adoption in 2026?

Validation workload across heterogeneous regulations and legacy gel-clot cost advantages in some regions remain key challenges, which sustain dual-method comparability and slower transitions in cost-sensitive markets.

How is automation influencing buyer decisions?

Buyers favor platforms that integrate robotics, rapid fluorescence readers, and compliant data systems to reduce invalid runs and shorten audit cycles, which supports growth in the recombinant Factor C assay market.

Page last updated on: