Global Human Growth Hormone (HGH) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

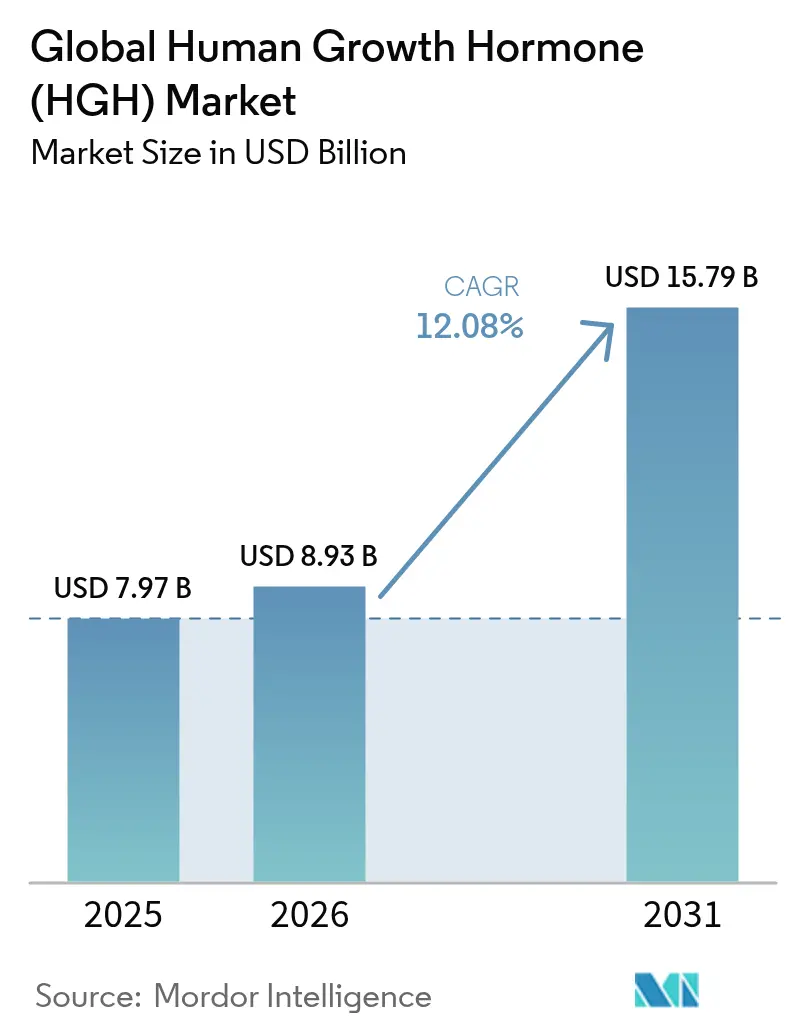

| Market Size (2026) | USD 8.93 Billion |

| Market Size (2031) | USD 15.79 Billion |

| Growth Rate (2026 - 2031) | 12.08% CAGR |

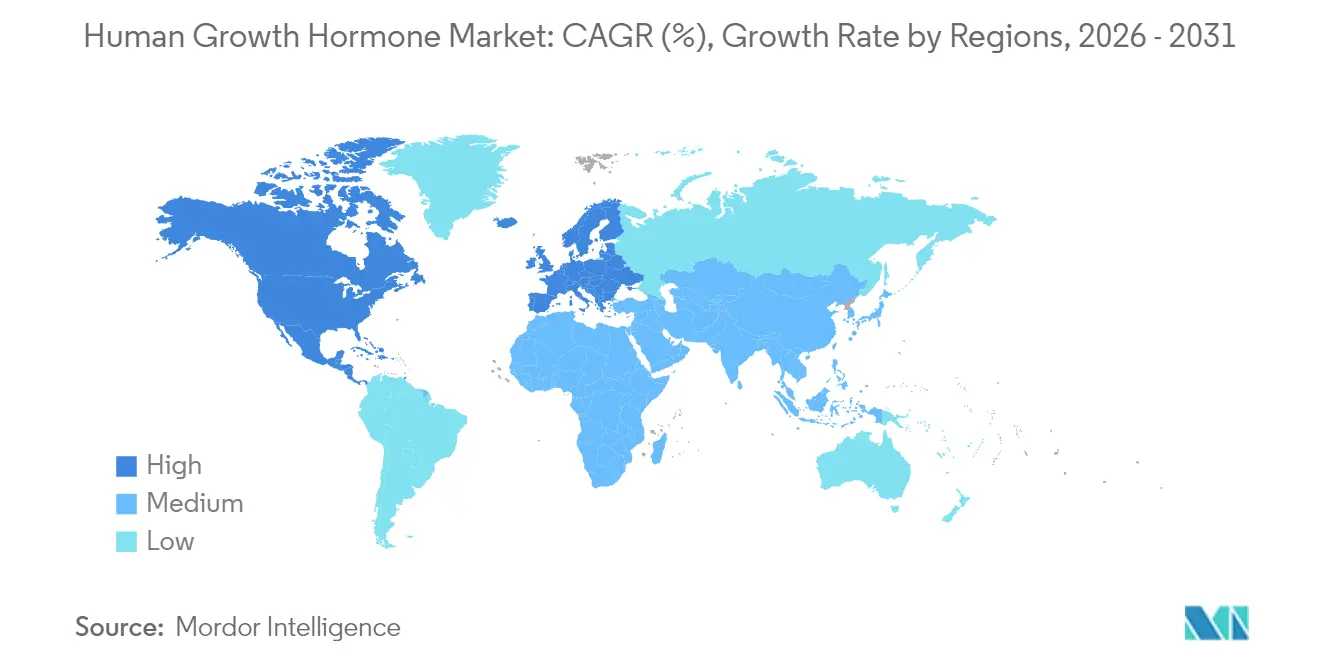

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Human Growth Hormone (HGH) Market Analysis by Mordor Intelligence

The human growth hormone market size is expected to grow from USD 7.97 billion in 2025 to USD 8.93 billion in 2026 and is forecast to reach USD 15.79 billion by 2031 at 12.08% CAGR over 2026-2031. Sustained progress in long-acting formulations, widening clinical indications that now span pediatric and adult populations, and multi-billion-dollar manufacturing expansions undertaken by several originator companies are the primary forces behind this growth. The competitive focus has shifted toward weekly products that reduce injection burden, while biosimilar launches simultaneously introduce aggressive price competition. Supply shortages that began in 2022 have prompted accelerated capacity projects, positioning well-capitalized firms to gain volume advantage once new lines come onstream. At the same time, digital health solutions that support adherence monitoring are being deployed to reinforce real-world outcomes and protect premium pricing within the human growth hormone market.

Key Report Takeaways

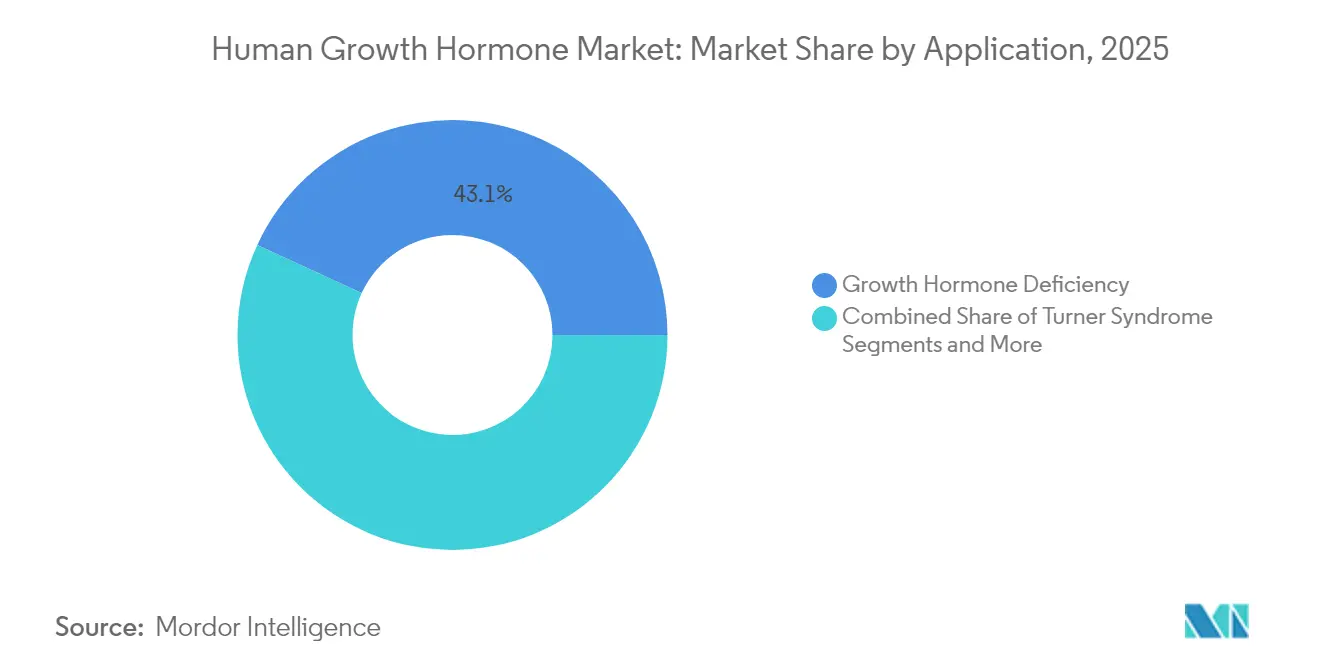

- By application, growth hormone deficiency held 43.12% of the human growth hormone market share in 2025, while idiopathic short stature is set to expand at a 12.61% CAGR through 2031.

- By route of administration, subcutaneous products commanded 64.98% share of the human growth hormone market size in 2025; oral / buccal candidates are projected to advance at 13.05% CAGR to 2031.

- By formulation, daily somatropin retained 71.62% share in 2025, whereas long-acting products are growing at a 13.38% CAGR over the same period.

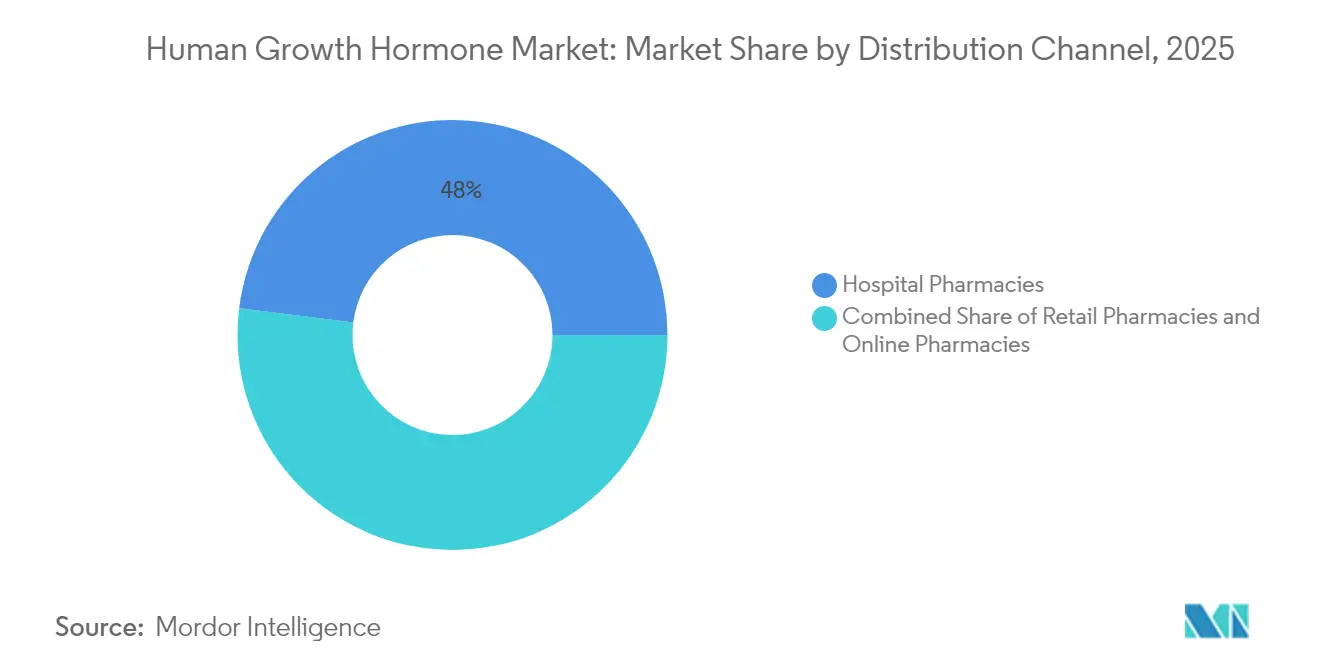

- By distribution channel, hospital pharmacies controlled 48.01% revenue in 2025, yet online pharmacies record the highest forecast CAGR at 13.62% to 2031.

- By patient type, pediatric cases represented 61.88% of total prescriptions in 2025, and the adult segment is rising at a 13.42% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Human Growth Hormone (HGH) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Development and uptake of long-acting rhGH formulations | +2.8% | Global, early adoption in North America and EU | Medium term (2-4 years) |

| Rising prevalence of growth hormone deficiency and related disorders | +2.1% | Global, higher impact in emerging markets | Long term (≥ 4 years) |

| Expanding adult and anti-aging off-label demand | +1.9% | North America and EU | Short term (≤ 2 years) |

| Continued advances in recombinant DNA and protein-engineering platforms | +1.4% | Global, concentrated in major pharma hubs | Long term (≥ 4 years) |

| Gradual inclusion of rhGH in reimbursement formularies | +1.2% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Rare-disease fast-track incentives | +0.8% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Development and Uptake of Long-Acting rhGH Formulations

Weekly products such as Skytrofa, Ngenla, and Sogroya obtained both FDA and EMA authorizations between 2020 and 2023 and are redefining adherence expectations. Clinicians view the improved convenience as a critical determinant of long-term height velocity, which is particularly meaningful in pediatric care. Health systems also register downstream cost savings tied to better adherence, though payers flag the 15-25% price premium and subject prescriptions to prior authorization. Despite cost tensions, ongoing safety surveillance has yet to identify signals that offset the compliance benefit, underpinning durable adoption prospects inside the human growth hormone market.

Rising Prevalence of Growth Hormone Deficiency and Related Disorders

Standardized IGF-1 testing, broader stimulation-test availability, and heightened physician education are lifting diagnostic rates across pediatric and adult cohorts. Adult growth hormone deficiency—once under-recognized—is now frequently screened due to its links with metabolic syndrome and cardiovascular risk. Advanced genetic sequencing helps clinicians detect Turner syndrome, Prader-Willi syndrome, and small-for-gestational-age cases earlier, which translates into longer therapy duration per patient. Research that connects adequate growth hormone levels with bone health and cognitive performance further widens the clinical rationale for continued therapy into adulthood [1]Frontiers in Endocrinology, “Emerging Roles of GH in Adult Metabolism,” frontiersin.org.

Expanding Adult and Anti-Aging Off-Label Demand

Industry estimates place adult prescriptions for non-approved indications at almost one-third of United States volume, creating a USD 1.5-2 billion shadow segment. Specialized clinics market perceived body-composition and anti-aging benefits, fuelling demand despite FDA warnings. Regulators have intensified import alerts against unapproved injectables, yet consumer interest remains strong and spills over into legitimate adult GHD evaluation. Endocrinologists report higher referral numbers, and validated deficiency cases now start treatment earlier, supporting volume growth in the regulated channel [2]US Food and Drug Administration, “Drug Shortage: Norditropin,” fda.gov.

Continued Advances in Recombinant DNA and Protein-Engineering Platforms

Platform technologies, notably TransCon, are extending half-life without altering the native somatropin molecule, thereby preserving biological fidelity while enabling weekly or longer dosing. Novo Nordisk signed a USD 285 million agreement to exploit TransCon for additional metabolic indications, reflecting industry confidence in the approach. Upstream, optimized cell lines and purification improvements drive higher yield and lower per-gram cost, allowing both originators and biosimilar players to navigate price pressure within the human growth hormone market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy cost | -2.3% | Emerging markets, selective impact in developed markets | Medium term (2-4 years) |

| Adverse effects and safety concerns of chronic rhGH therapy | -1.8% | Global, heightened scrutiny in EU | Long term (≥ 4 years) |

| Regulatory uncertainty | -1.4% | North America and EU | Short term (≤ 2 years) |

| Counterfeit and grey-market rhGH | -1.1% | Global, focus on unregulated online channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse Effects and Safety Concerns of Chronic rhGH Therapy

Post-marketing data draw attention to glucose intolerance, edema, and unresolved debates over potential cancer risk in adults on prolonged therapy. The PATRO biosimilar registry continues to publish safety updates that guide physician decision-making [3]Center for Biosimilars, “PATRO Registry Safety Data,” centerforbiosimilars.com . EMA and FDA have attached rigorous long-term surveillance requirements to long-acting approvals, prompting prescribers to adopt more detailed baseline risk assessments and ongoing metabolic monitoring. While safety signals have remained manageable, the extra administrative load may deter uptake in borderline cases and moderates the overall growth trajectory of the human growth hormone market.

High Therapy Cost

Annual drug expenditure typically ranges from USD 20,000 to USD 60,000 per patient, with full cost of care sometimes surpassing USD 80,000 when monitoring and specialist visits are included. Payers now enforce step-therapy protocols that prioritize lower-cost daily biosimilars over premium long-acting products. Although biosimilars such as Omnitrope deliver 10-15% list-price savings, they have not compressed prices enough to open widespread access in lower-income countries. Out-of-pocket exposure therefore remains a formidable barrier in emerging markets despite patient-assistance programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: GHD Dominance Faces ISS Challenge

Growth hormone deficiency generated the largest revenue pool and held 43.12% of total 2025 sales, confirming its entrenched clinical standing. The breadth of clinical data, standardized dosing algorithms, and long-standing reimbursement support sustain its leadership. Nonetheless, idiopathic short stature is recording a 12.61% CAGR through 2031 and is compressing the gap. Endocrinologists are expanding the qualifying height-standard-deviation window, and payers are gradually conceding coverage following favorable long-term efficacy publications. Turner syndrome and Prader-Willi syndrome supply stable but lower-volume demand, supported by orphan-drug policies that guarantee continued access. Chronic renal insufficiency as a use case is receding in relative importance as transplantation outcomes improve.

Continued indication diversification promotes portfolio strategies that tailor dosing devices, titration software, and support programs to each distinct cohort. Companies that align product presentation with condition-specific pathways stand to reinforce their positions within the human growth hormone market. Growth hormone deficiency accounted for 43.12% of the human growth hormone market size in 2025, underlining its weight in corporate planning.

By Route of Administration: Subcutaneous Supremacy Under Oral Threat

Subcutaneous delivery maintained 64.98% share during 2025, enjoying decades of physician familiarity, reliable bioavailability, and integrated nurse-training infrastructure. Its scale attracts biosimilar competition, which increases price transparency but still preserves moderate margin because clinical inertia keeps daily injectables entrenched. Intravenous or intramuscular administration is confined to inpatient settings.

Oral / buccal candidates, led by LUM-201, promise a 13.05% CAGR that could meaningfully disrupt the current hierarchy once phase 3 data mature. If efficacy endpoints match injectable standards, payers may support rapid substitution due to superior adherence potential. For now, subcutaneous devices are evolving toward thinner needles and digital diary integration, which may slow near-term oral encroachment.

By Formulation: Long-Acting Revolution Accelerates

Daily somatropin still claims 71.62% revenue because of incumbent status, robust evidence, and biosimilar affordability. The reference category benefits from entrenched procurement pathways in public systems that bundle dosing devices and education services. However, weekly and monthly products are compounding at 13.38% CAGR through 2031. Initial uptake concentrates in North America and Europe where payers are more willing to balance higher acquisition cost against documented adherence gains. Long-acting launches also enjoy marketing momentum tied to improved quality-of-life scores, an increasingly decisive metric in health-technology assessments.

Future pipeline candidates seek to extend dosing intervals even further, aiming for once-monthly administration that could lock in patient loyalty and raise switching costs. Long-acting products are therefore positioned to secure a larger slice of future human growth hormone market size.

By Distribution Channel: Hospital Pharmacies Lead Digital Disruption

Hospital pharmacies distribute 48.01% of global units thanks to tight coupling between specialist visits and on-site dispensing. Their embedded prior-authorization workflows simplify payer evidence submissions and guarantee cold-chain integrity. Retail chains supplement supply for stable pediatric patients but face higher reimbursement paperwork and lower margins. Specialty pharmacies fill a bridging role where nurse-led adherence coaching is valued.

Online pharmacies occupy a small base yet are scaling at 13.62% CAGR on consumer appetite for home delivery, video consultations, and integrated refill reminders. Regulators are expanding licensing requirements and auditing that segment because counterfeit risk is disproportionately high online. Established manufacturers now partner with licensed digital platforms to safeguard product authenticity and shape the narrative in this evolving piece of the human growth hormone market.

By Patient Type: Adult Segment Challenges Pediatric Dominance

Pediatric cases represented 61.88% of 2025 volumes and remain the reference population in most treatment guidelines. Early diagnosis under school growth-monitoring programs and insurer support for childhood height outcomes anchor pediatric demand. However, adult applications are advancing at a 13.42% CAGR through 2031 as metabolic sequelae of untreated adult GHD gain scientific clarity. Cardiovascular, bone-density, and mental-health benefits are driving refreshed guidelines that advocate replacement in documented deficiency. Reimbursement hurdles are stricter, requiring confirmatory stimulation tests and periodic efficacy review, but rising patient awareness sustains momentum.

Adult uptake diversifies revenue streams and offsets demographic headwinds in birth-rate cooling markets. Adult applications accounted for 38.12% of the human growth hormone market size in 2025 and are projected to narrow the gap over the next five years.

Geography Analysis

North America controlled 41.72% of global turnover in 2025. United States payers granted relatively broad coverage after evidence linked improved adherence with long-run cost containment, which accelerated early adoption of Skytrofa, Ngenla, and Sogroya. Canada followed with health-technology assessments that accepted weekly dosing on quality-of-life grounds within the public system. Mexico is beginning to expand insurance formularies, though cost sensitivity caps near-term penetration of premium products.

Europe contributes a sizable portion of the human growth hormone market through harmonized EMA approvals and well-structured orphan-drug incentives. Germany leads uptake of long-acting molecules and maintains robust post-marketing registries that influence safety perceptions across the continent. France and the United Kingdom enforce strict cost-effectiveness thresholds, which intensify biosimilar competition and moderate net price. Eastern European countries gradually add rhGH to reimbursement lists, leveraging pooled procurement to gain price concessions.

Asia-Pacific is growing fastest at 14.05% CAGR. China registers strong demand following insurance-catalog additions and domestic manufacturing that compresses price. Japan’s mature specialist network supports stable high-value consumption, and longitudinal patient registries contribute pivotal safety data. India, despite infrastructure gaps, shows meaningful growth as private insurance penetration rises and diagnostics improve. Local capacity investments by multinational firms aim to shorten supply lead-times and insulate the human growth hormone market against global shortages.

Regulatory Landscape

Human growth hormone (somatropin) remains regulated as a prescription biologic in major markets, with full biologics quality and post-marketing controls (for example, FDA BLA pathways and CGMP compliance in the United States, and EMA Marketing Authorisation plus pharmacovigilance obligations in the European Union). Regulatory scrutiny has tightened for long-acting products approved between 2020 and 2023, including Skytrofa and Sogroya in EMA EPARs and comparable weekly pathways in the United States. Long-term surveillance requirements have been attached to label expansions and life-cycle changes.

Enforcement also affects channel behavior. In April 2026, the US FDA updated Import Alert 66-71 to strengthen detention without physical examination for unapproved HGH imports, and clarified that lyophilized HGH powders are treated as finished biologic drug products rather than APIs, narrowing pathways used to support unauthorized supply. In Europe, life-cycle activity continues, with EMA actions in 2026 related to Sogroya variations and indication expansions. This reinforces that growth hormone franchise growth increasingly depends on formal label expansions, safety monitoring, and manufacturing compliance rather than informal or compounded supply.

Value Chain Analysis

The HGH value chain starts with recombinant expression, commonly using microbial systems such as Escherichia coli or Pichia pastoris, followed by downstream purification to biologic-grade specifications. Multi-step chromatography and stringent removal of endotoxins and host-cell impurities are key cost and yield drivers, after which manufacturers move to formulation and, for many presentations, lyophilisation before fill-finish into vials or pen-compatible cartridges. Because the market is injection-led, device integration (pens, needles, and training kits) and cold-chain logistics are critical enablers up to hospital and specialty pharmacy dispensing.

Regulation and supply integrity constrain the chain at multiple points. The April 2026 FDA update to Import Alert 66-71 increases compliance risk for unauthorized imports and reinforces a clear separation between the regulated prescription market and gray channels, affecting freight handling, wholesaler controls, and online pharmacy oversight. In July 2026, the FDA proposed registration-related changes to improve supply chain transparency, including requirements affecting foreign API site registration and distributed manufacturing. This adds operational diligence for globally sourced inputs and multi-site manufacturing networks.

Competitive Landscape

The market is moderately concentrated, with originators retaining high share through portfolio breadth, scale manufacturing, and sophisticated patient-support systems. Novo Nordisk allotted USD 4.1 billion to enlarge United States capacity, while Eli Lilly committed USD 3 billion to injector-formulation lines, moves designed to mitigate shortages and underpin future volume growth. Ascendis Pharma leverages its TransCon platform to commercialize Skytrofa and negotiates platform collaborations, most recently with Novo Nordisk for metabolic programs.

Biosimilar players, headed by Sandoz, are escalating price rivalry; Sandoz posted 29% biosimilar revenue growth in first-half 2024 on Omnitrope strength and pipeline expansion to 28 molecules. Their growth pressures reference pricing, yet supply constraints mean discounts remain moderate in practice. Technology differentiation is now the core battleground as companies layer digital-health ecosystems—needle-free devices, adherence apps, connected pens—to capture clinician loyalty. Oral candidates from Lumos Pharma present a structural threat to injectable incumbents and could spark a fresh wave of competitive realignment should late-stage data prove compelling.

White-space opportunities persist in cardiovascular and cognitive-health indications where mechanistic evidence is accumulating. Companies that secure such labels could unlock add-on revenue while further entrenching share in the human growth hormone market.

Global Human Growth Hormone (HGH) Industry Leaders

AnkeBio Co. Ltd

Eli Lilly and Company

Ferring BV

Novo Nordisk AS

Ipsen S.A.

- *Disclaimer: Major Players sorted in no particular order

_Market_landscape.webp)

Market Opportunities and Future Outlook

Indication expansion tied to long-acting growth hormone is a near-term commercialization lever, particularly in pediatric short stature populations beyond classical GHD. In February 2026, the FDA approved Novo Nordisk's Sogroya (somapacitan-beco) for three additional pediatric indications: idiopathic short stature, short stature born small for gestational age without catch-up growth by age 2, and growth failure associated with Noonan syndrome. In Europe, EMA activity in 2026 around Sogroya variations and CHMP opinioning supports continued momentum for label broadening, giving manufacturers a route to grow within regulated channels while supporting reimbursement dossiers with outcomes and adherence narratives linked to weekly dosing.

Pipeline and manufacturing whitespace remains concentrated in differentiated long-acting biology and delivery ecosystems that protect adherence and traceability in a market exposed to counterfeits and online leakage. The report scope also highlights multi-billion-dollar manufacturing expansions by originator companies as a response to shortages that began in 2022, which can help well-capitalized firms secure more reliable supply allocations for hospital and specialty pharmacies. Separately, Phase 3-stage long-acting candidates (including Fc-fusion approaches) indicate ongoing competitive entry in weekly regimens, while digital adherence support and authentication partnerships with licensed online platforms target a documented risk area in the distribution mix.

Recent Industry Developments

- April 2026: Anhui Anke Biotechnology (Group) Co., Ltd. held a Phase III investigator meeting in Hefei for its Somatropin-Fc Fusion Protein Injection, a long-acting growth hormone candidate. The milestone supports AnkeBio's progression toward a weekly regimen and adds another late-stage contender to the long-acting segment that is reshaping competitive differentiation beyond daily somatropin.

- February 2026: Novo Nordisk announced that the FDA approved Sogroya (somapacitan-beco) for three additional pediatric indications, idiopathic short stature, short stature born small for gestational age without catch-up growth by age 2, and growth failure associated with Noonan syndrome. The broader label expands the addressable treated population for a once-weekly product and strengthens life-cycle management against daily therapies and emerging long-acting competitors.

- March 2024: Aeterna Zentaris completed recruitment in its Phase 3 macimorelin trial for diagnosing childhood onset growth hormone deficiency. Advancing a non-invasive diagnostic pathway can influence referral and confirmation workflows in pediatric endocrinology, with downstream implications for earlier initiation and monitoring of prescribed somatropin therapy in regulated channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues from human growth hormone therapies (somatropin) used in clinical care, across approved pediatric and adult indications, and supplied through regulated healthcare channels. Values are tracked at manufacturer level, with normalizing for discounts and mix shifts where data is available.

Scope exclusions: Excludes non-prescription anti-aging use, gray-market peptide vials, and sports performance misuse.

Segmentation Overview

- By Application

- Growth Hormone Deficiency

- Turner Syndrome

- Idiopathic Short Stature

- Prader-Willi Syndrome

- Small for Gestational Age

- Chronic Renal Insufficiency

- By Route of Administration

- Subcutaneous

- Intravenous

- Intramuscular

- Oral / Buccal

- By Formulation

- Short-acting

- Long-acting

- By Distribution Channel

- Hospital Pharmacies

- Retail & Specialty Pharmacies

- Online Pharmacies

- By Patient Type

- Pediatric

- Adult

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building the demand pool and treatment context, then mapping supply and pricing patterns that can be checked year by year. Public sources were used to anchor epidemiology and therapy usage, such as CDC and NIH publications, NCBI research abstracts, and FDA and EMA drug labels and safety updates, along with OECD health statistics.

On the supply side, we reviewed company filings, annual reports, investor presentations, and press releases to track portfolio coverage and the timing of launches or biosimilar entries. In a few cases, paid subscriptions for company financials and patent databases were used to cross-check product lineage and ownership changes that can affect reported sales. Where relevant, we also referred to World Bank macro indicators and customs level trade statistics to validate regional availability signals. The desk source list is illustrative, and many other public references were consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm real prescribing and access realities, especially where public data does not show net pricing, switching behavior, and therapy persistence. We spoke with a mix of manufacturers, distributors, clinicians, payers, and pharmacy channel experts across APAC, EMEA, and the Americas, so assumptions could be pressure-tested and adjusted before the final model was locked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 12% | APAC: 51% |

| Mid tier: 56% | Functional/Unit leaders: 35% | EMEA: 31% |

| Smaller Players: 14% | Managers: 53% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was first constructed with a top-down approach, combining diagnosis prevalence, treated-patient shares, and therapy duration to reconstruct addressable prescription volume by region and indication. Those volumes were then translated into value using a blended net price path that reflects dose patterns, payer controls, and the split between daily and long-acting products.

To keep outputs grounded, we corroborated totals with selective bottom-up approximations, including supplier revenue roll-ups from public financials, channel checks on formulary access, and sampled ASP times estimated patient counts in key countries. Where data was thin for smaller markets, gaps were handled with proxy indicators such as endocrine specialist density, public reimbursement coverage, and historic uptake curves from comparable launches.

Forecasting leaned on scenario analysis, since policy changes and long-acting adoption can shift growth faster than simple trend lines suggest. Key inputs varied and validated through expert consensus included pediatric versus adult diagnosis rates, persistence and adherence differences by regimen, biosimilar penetration, dose escalation patterns, and currency timing for regional consolidation into USD.

Data Validation & Update Cycle

Model outputs were checked against independent signals, including reported therapy sales trends, regulatory approvals and label expansions, and regional reimbursement updates that affect patient access. Where an estimate looked out of range, the underlying drivers were re-checked, and respondents were re-contacted if the variance could not be explained through a clear pricing or volume shift.

A multi-step review was followed so assumptions, formulas, and year-to-year movements could be traced and challenged before sign-off. The report is refreshed annually, and interim updates are triggered when there are material events such as major approvals, safety actions, or meaningful pricing changes. Before delivery, a final pass is performed to ensure the latest public and primary signals are reflected in the outputs.

Mordor Intelligence's Human Growth Hormone Market Estimate Compared With Other Published Estimates

Published market values for human growth hormone often do not match because the counted product basket and the point of pricing in the value chain are not consistent. Differences also come from the base year used, whether estimates assume faster long-acting uptake, and how discounts and payer controls are modeled.

Anti-aging clinic use and gray-market peptide formats are outside Mordor Intelligence's scope, which is why some broader figures that include those revenues can appear larger even in the same year. Another common driver is whether delivery devices are counted as part of therapy revenue, and whether values are captured at list price versus a net price that reflects rebates and tendering. Currency conversion timing and refresh cadence also create gaps when markets move quickly after approvals or reimbursement decisions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.93 B (2026) | |

| Industry Publisher A | USD 9.11 B (2026) | Uses a nearby year value but appears to apply a broader interpretation of revenue capture, which can lean closer to list pricing and include a wider set of channel markups. |

| Market Tracker B | USD 6.76 B (2024) | Different base year and a longer forecast window, with limited clarity on net pricing adjustments and mix effects, which can compress the starting value when compared across years. |

The table shows that the spread is mainly explained by what is included in the counted revenue pool, how net price is treated versus list price, and which year is used for the snapshot. By keeping the demand pool tied to diagnosed and treated patients, and then validating totals with supplier and channel signals, our estimate stays traceable to inputs that can be re-checked when the market changes.

Key Questions Answered in the Report

What is the current Global Human Growth Hormone (HGH) Market size?

The human growth hormone market size reached USD 8.93 billion in 2026 and is forecast to expand to USD 15.79 billion by 2031.

Who are the key players in Global Human Growth Hormone (HGH) Market?

AnkeBio Co. Ltd, Eli Lilly and Company, Ferring BV, Novo Nordisk AS and Ipsen S.A. are the major companies operating in the Global Human Growth Hormone (HGH) Market.

How fast are long-acting growth hormone formulations growing?

Long-acting weekly or monthly products are registering a 13.38% CAGR from 2026 to 2031, the highest among all formulation types.

Which region has the biggest share in Global Human Growth Hormone (HGH) Market?

In 2025, the North America accounts for the largest market share in Global Human Growth Hormone (HGH) Market.

Page last updated on: