Biofuel Enzymes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

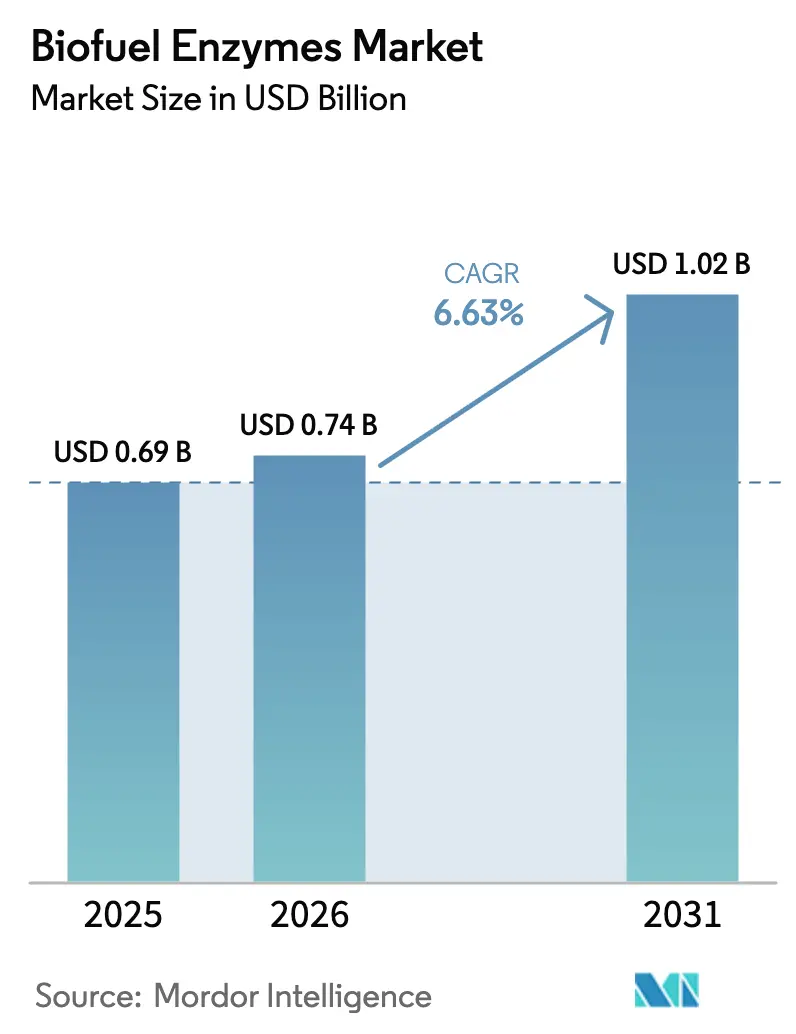

| Market Size (2026) | USD 0.74 Billion |

| Market Size (2031) | USD 1.02 Billion |

| Growth Rate (2026 - 2031) | 6.63% CAGR |

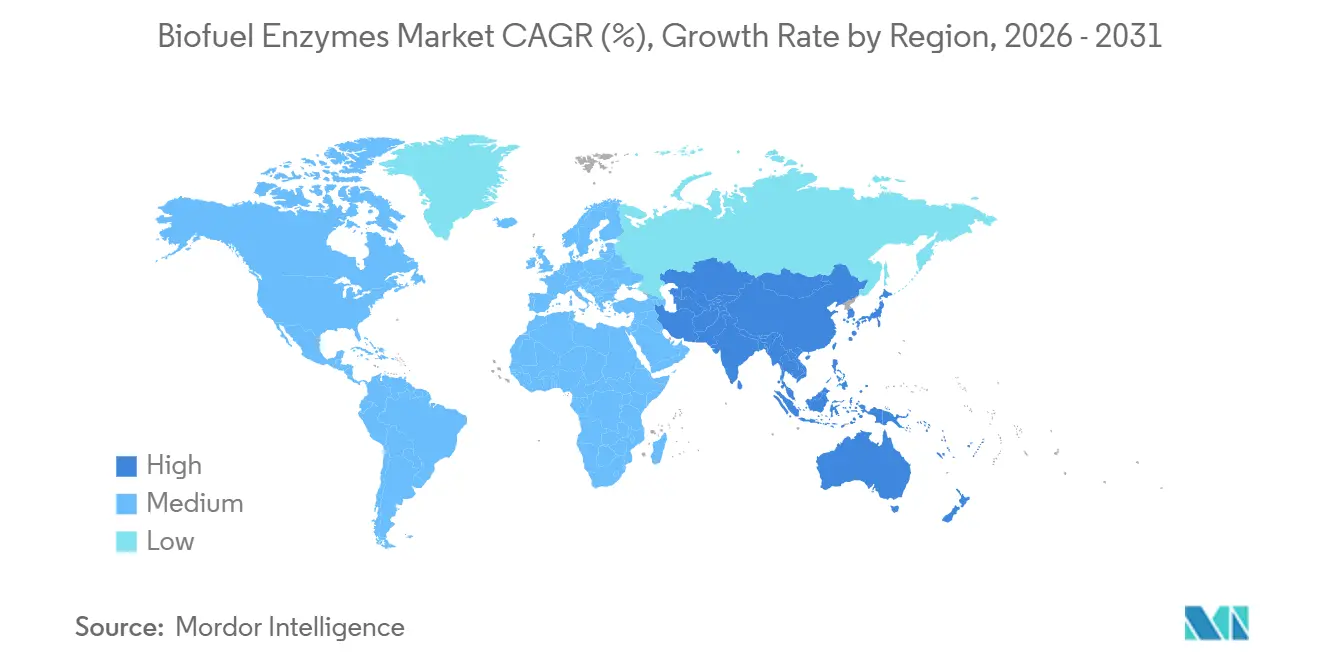

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

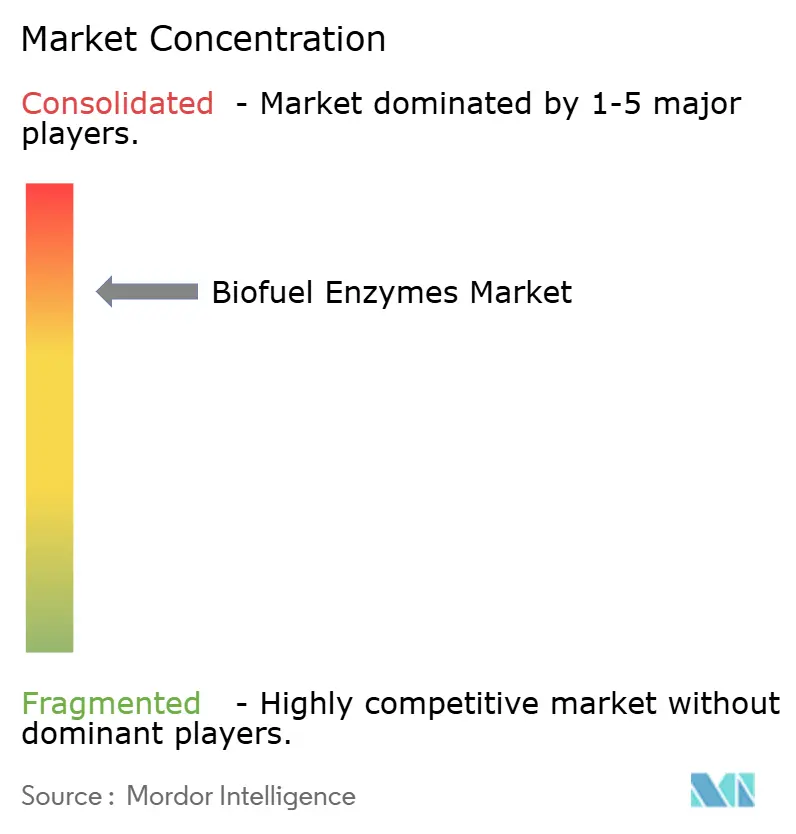

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biofuel Enzymes Market Analysis by Mordor Intelligence

The Biofuel Enzymes Market size is projected to expand from USD 0.69 billion in 2025 and USD 0.74 billion in 2026 to USD 1.02 billion by 2031, registering a CAGR of 6.63% between 2026 to 2031. Mandated renewable fuel volumes in the United States, India and the European Union are expanding the addressable pool of biofuels, while R&D breakthroughs in thermostable cellulases continue to compress cost per gallon for cellulosic ethanol. Mature corn-ethanol infrastructure in North America underpins sizeable baseline demand, but the fastest incremental growth is moving to Asia-Pacific as China and India accelerate ethanol blending targets. On-site enzyme manufacture, consolidated bioprocessing pilots and enzyme cocktails that unlock waste oils and high-ash residues are reshaping competitive strategies for both incumbents and emerging biotechnology firms. Capital spending announcements by leading suppliers signal confidence that policy support and technology gains will sustain mid-single-digit volume expansion through the decade.

Key Report Takeaways

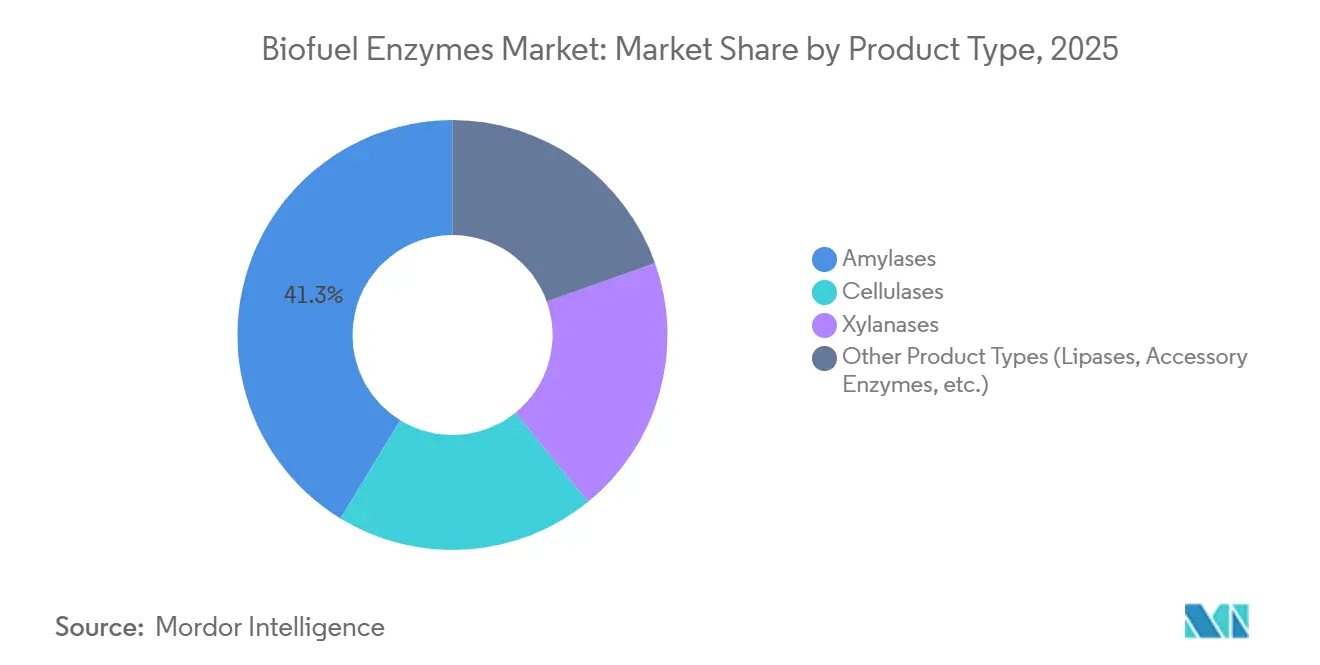

- By product type, amylases led with 41.27% revenue share in 2025; cellulases are forecast to expand at an 8.67% CAGR to 2031.

- By feedstock, starch crops accounted for 40.35% of the biofuel enzymes market share in 2025, while algae is advancing at a 9.68% CAGR through 2031.

- By technology, free enzyme catalysis captured 50.81% of the biofuel enzymes market size in 2025 and consolidated bioprocessing is projected to climb at a 9.79% CAGR between 2026-2031.

- By application, corn/starch-based ethanol represented 45.78% of revenue in 2025; lignocellulosic ethanol is progressing at an 8.49% CAGR to 2031.

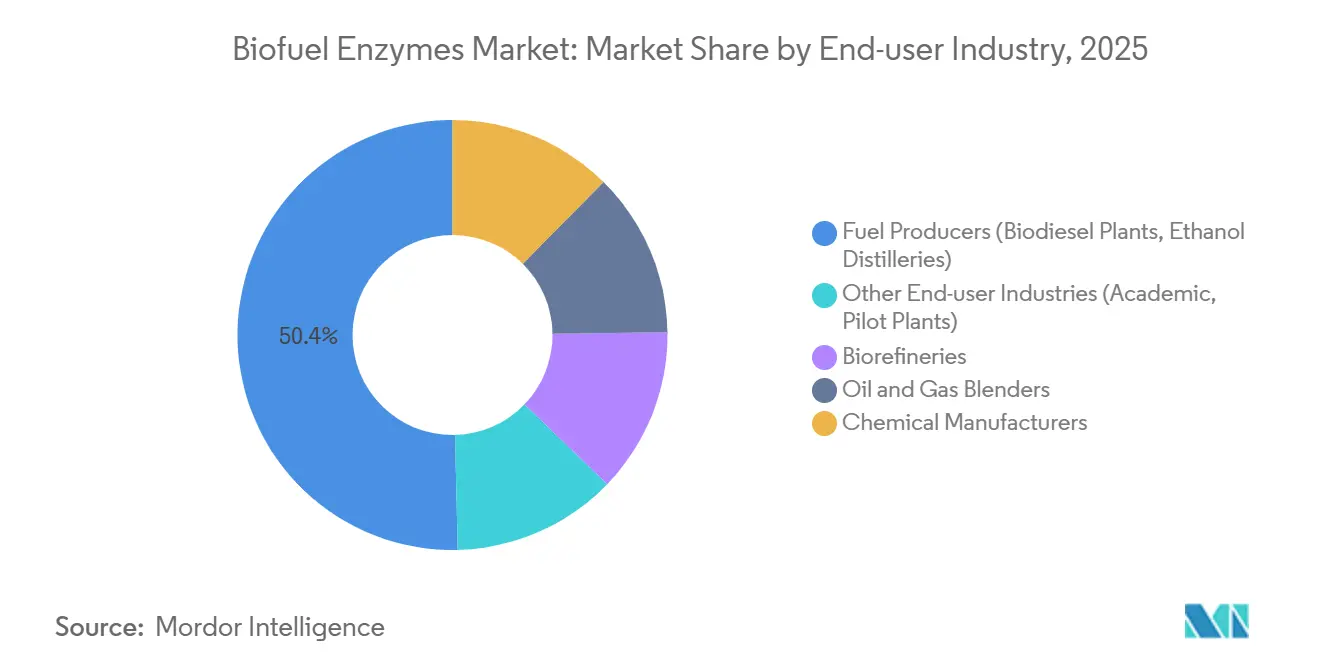

- By end-user, fuel producers held 50.39% revenue in 2025, whereas biorefineries are growing at an 8.45% CAGR to 2031.

- By geography, North America commanded 35.55% revenue in 2025; Asia-Pacific is the fastest region, expanding at a 7.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biofuel Enzymes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Biodiesel Blending Mandates | +1.2% | Global, with concentration in North America, EU, Brazil, Indonesia, Malaysia | Medium term (2-4 years) |

| Expanding Demand for Second-Generation (Cellulosic) Ethanol | +1.5% | North America, EU, China, India | Long term (≥ 4 years) |

| Rapid Advances in Enzyme Engineering and Directed Evolution | +1.3% | Global, led by North America and EU R&D hubs | Medium term (2-4 years) |

| On-Site Enzyme Production Lowering Operating Costs | +0.9% | North America, Brazil, China | Short term (≤ 2 years) |

| Biorefinery Integration with Advanced Pretreatment Platforms | +1.0% | North America, EU, Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Biodiesel Blending Mandates

Regulatory mandates are recalibrating enzyme demand as biodiesel blending ratios rise faster than ethanol obligations in several jurisdictions. The European Union’s Renewable Energy Directive III requires advanced biofuels to supply 5.5% of transport energy by 2030, a threshold that pushes enzymatic transesterification of waste oils and tallow into the mainstream. Indonesia’s B35 program consumes roughly 14 million metric tons of crude palm oil annually, incentivizing lipase enzymes that convert high-free-fat-acid feedstocks without costly pre-esterification. Brazil lifted its biodiesel blend to B15 in 2025, widening substrate diversity and opening opportunities for enzyme formulations that handle soybean oil, tallow and used cooking oil interchangeably. The U.S. Environmental Protection Agency set 2026 biomass-based diesel at 3.35 billion gallons, rewarding enzyme suppliers capable of lowering catalyst cost below USD 0.08 per gallon[1]U.S. Environmental Protection Agency, “2026 Renewable Volume Obligations,” epa.gov . California’s Low Carbon Fuel Standard multiplies credit values for fuels derived from waste fats, propelling demand for lipases tolerant of moisture and impurities.

Expanding Demand for Second-Generation (Cellulosic) Ethanol

Commercial deployment of cellulosic ethanol plants is multiplying enzyme consumption per gallon of fuel. The U.S. Department of Energy awarded USD 118 million in 2025 to projects targeting cellulase cost reductions below USD 0.30 per gallon by 2030. POET-DSM’s Project LIBERTY produced 22 million gallons of cellulosic ethanol in 2025 and consumed about 110 metric tons of cellulase and xylanase, proving full-scale economics once plants run near nameplate capacity. India contracted 500 million liters of second-generation ethanol from rice straw and bagasse, demanding cocktails optimized for high-ash feedstocks. China approved 600,000 metric tons per year of cellulosic capacity with on-site enzyme plants to avoid cold-chain costs in northern provinces. The European Commission’s Innovation Fund invested EUR 150 million in sunliquid technology that co-locates enzyme production with pretreatment and fermentation, cutting supply-chain overhead by 40%.

Rapid Advances in Enzyme Engineering and Directed Evolution

Protein-engineering breakthroughs are lifting specific activity, thermostability and inhibitor tolerance. A 2025 study showed CRISPR-edited Trichoderma reesei cellulase genes raised activity 34%, enabling loading cuts from 15 to 10 mg per g of biomass without yield loss. Novonesis cut development cycles in half using machine-learning-guided directed evolution, accelerating time-to-market for region-specific cocktails. DuPont’s new xylanase operates at 70 °C, allowing simultaneous saccharification and fermentation that eliminates cooling costs of USD 0.04 per gallon. Techno-economic modeling from the U.S. National Renewable Energy Laboratory suggests next-generation cellulases can shave USD 0.12 per gallon off minimum ethanol selling price, putting cellulosic fuels on parity with corn ethanol in unsubsidized markets. Patent activity mirrors the trend, with dsm-firmenich filing 12 patents in 2025 for AI-designed lipases targeting biodiesel from waste oils.

On-Site Enzyme Production Lowering Operating Costs

Biorefineries are internalizing enzyme manufacture to avoid cold-chain logistics and tune blends in real time. Project LIBERTY’s on-site fermentation slashed purchased enzyme expense by 25%. Raízen’s Bonfim complex produces 500 metric tons of cellulase per year from molasses and bagasse hydrolysate, driving cost to USD 0.18 per gallon for second-generation ethanol. A DOE-led consortium is piloting modular production skids that retrofit existing distilleries and aim for enzyme cost below USD 0.25 per gallon. Cofco Biochemical’s Zhaodong site in China now makes its own amylase, cutting spend by 18% and stabilizing supply in peak seasons. In-house plants also allow formula tweaks within hours when lignin or moisture levels shift, a responsiveness impossible with centralized supply chains.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Enzyme Production and Immobilization Costs | -0.8% | Global, particularly impacting emerging markets in Asia-Pacific and South America | Medium term (2-4 years) |

| Feedstock Price Volatility Dampening Enzyme Demand Visibility | -0.6% | North America, South America, Asia-Pacific | Short term (≤ 2 years) |

| Competitive Pressure from Thermo-Chemical Conversion Routes | -0.5% | North America, EU, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Enzyme Production and Immobilization Costs

Fermentation, purification and formulation represent up to half of delivered enzyme cost, challenging adoption in price-sensitive regions. NREL pegged cellulase production at USD 4.50-6.00 per kg in 2025, equal to USD 0.45-0.60 per gallon of cellulosic ethanol, eroding margins whenever oil trades below USD 70 per barrel[2]National Renewable Energy Laboratory, “Cellulase Cost and Performance Targets,” nrel.gov . Immobilized systems allow catalyst reuse but require USD 2-5 million for carriers and retrofits, a barrier for mid-sized mills. Advanced Enzyme Technologies noted recovery and recycling add 15-20% to enzyme outlay and only 30% of plants have installed the hardware. Indian distilleries operating on USD 0.08-0.12 per liter margins often choose lower-grade enzymes that slow throughput. Tropical supply chains face refrigerated transport surcharges of USD 0.50-0.80 per kg, pricing out small biodiesel producers.

Feedstock Price Volatility Dampening Enzyme Demand Visibility

Corn, sugarcane and palm oil trade in wide bands, disrupting enzyme purchasing plans. U.S. corn futures swung 62% in 2025 as drought and Chinese import demand whipsawed prices, prompting ethanol plants to throttle runs and defer enzyme orders. Brazilian mills shifted to sugar when export prices exceeded USD 0.20 per pound, trimming enzyme use 12% during peak sugar months. Indonesian palm oil prices spiked to USD 1,350 per metric ton during El Niño, forcing biodiesel capacity idling and an 8-10% enzyme demand dip. Corn-stover collection fell 18% in 2025 after wet harvests limited field access, slashing cellulase consumption at cellulosic plants. Suppliers now offer contracts indexed to feedstock costs, but the mechanism shifts margin risk and complicates capacity planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cellulases Drive Next-Generation Shift

Cellulases are projected to grow at 8.67% between 2026-2031, outpacing all other enzyme categories as policy targets drive lignocellulosic ethanol build-out. Amylases retained 41.27% revenue share in 2025, a legacy of corn and wheat starch dominance in North America and Asia-Pacific. Xylanases and accessory enzymes are being bundled with cellulases to maximize hemicellulose conversion, while lipase development focuses on biodiesel from waste oils and animal fats.

Demand dynamics are diverging by region. U.S. corn-ethanol plants remain the cornerstone for amylase volumes, yet suppliers are diverting R&D budgets toward thermostable cellulases that maintain activity above 65 °C to cut cooling energy. Patent filings for cellulases rose 27% in 2025 versus 8% for amylases, underscoring the pivot. Lipases, although smaller in value, underpin emerging palm-oil biodiesel markets in Southeast Asia and waste-oil transesterification in Europe. Suppliers are marketing enzyme packages that integrate laccases or pectinases to loosen lignin and pectin matrices in tough biomass such as softwood or algal cell walls.

By Feedstock: Algae Emerges as High-Growth Frontier

Starch crops generated 40.35% revenue in 2025, yet their share is gradually eroding in favor of residues, energy crops and algae. The biofuel enzymes market share linked to algae carries the highest 9.68% CAGR forecast through 2031 as aviation mandates favor low-carbon lipids. Agricultural residues hold vast potential but are constrained by enzyme cost per gallon; next-generation cocktails demonstrated by NREL that lower dosage to 12 mg g-1 promise to unlock this segment.

Suppliers are tailoring formulations to high-ash rice straw in India and moisture-rich corn stover in the U.S., while Scandinavian firms develop cold-adapted cellulases for forestry residues processed at 15-20 °C. Waste cooking oil conversion is another bright spot, with lipases handling 15% free-fatty-acid streams without caustic pretreatment, saving USD 0.10 per gallon in European biodiesel plants. Algal biofuel pilots are demanding cellulases that break tough cell walls and lipases that free intracellular lipids without energy-intensive drying, a niche where early-stage suppliers are positioning for first-mover advantage.

By Technology: Consolidated Bioprocessing Redefines Economics

Free enzyme catalysis accounted for 50.81% of 2025 revenue, yet consolidated bioprocessing (CBP) is forecast to post the fastest 9.79% CAGR through 2031. The biofuel enzymes market size tied to CBP is embryonic but could multiply once engineered microbes reach industrial titers. Immobilized systems, although promising 30-40% cost savings, still face capital hurdles and limited retrofits.

On-site enzyme production is scaling quickly; twelve commercial plants adopted integrated fermentation in 2025, squeezing logistics costs and allowing real-time recipe tuning. Continuous-flow micro-reactors and modular hydrolysis units are in pilot phase, offering throughput gains for distributed biorefineries. CBP projects funded by DOE aim for ethanol selling prices under USD 1.00 per gallon, a target that would upend current procurement models. However, CBP organisms require further metabolic tuning to match industrial yeast ethanol tolerance, keeping free enzyme catalysis dominant for most of the forecast period.

By Application: Lignocellulosic Ethanol Gains Policy Tailwinds

Corn/starch-based ethanol retained 45.78% revenue in 2025, yet lignocellulosic ethanol is set to expand faster at an 8.49% CAGR on the back of favorable carbon-intensity credits in the U.S. and Brazil. California awards cellulosic ethanol credits worth USD 0.40-0.60 per gallon, absorbing higher enzyme costs. Biodiesel remains sizeable as Indonesia, Malaysia and the EU raise blending ratios, with enzyme demand pivoting to lipases that can tackle waste oils containing 8-15% free fatty acids.

Emerging applications include biogas upgrading, where enzymes boost anaerobic digestion rates, and biochemical intermediates such as bio-succinic acid produced via enzyme-assisted fermentation. Specialty enzymes for leather and textiles carve out niche revenue streams but remain small relative to fuel applications. Policy equivalence factors (1.5x for cellulosic ethanol in the U.S.) are steering investment toward lignocellulosic pathways that expand the total addressable market for cellulases and accessory enzymes.

By End-user Industry: Biorefineries Integrate Upstream

Fuel producers, chiefly ethanol distilleries and biodiesel plants, controlled 50.39% revenue in 2025, but biorefineries show the strongest 8.45% CAGR outlook. The biofuel enzymes market size captured by biorefineries will rise as facilities co-locate pretreatment, hydrolysis, fermentation and enzyme production. POET secures enzymes via multi-year contracts indexed to corn prices, stabilizing dollar-per-gallon costs even in volatile grain cycles. Raízen spreads enzyme expenditure across electricity and lignin-derivative revenue, diluting cost impact.

Chemical manufacturers and consumer-goods companies are nascent yet strategic customers, adopting enzymatic routes to biochemicals and surfactants. Academic pilot plants, though small, remain essential for validating new cocktails on unconventional feedstocks. Licensing deals for on-site fermentation strains and process know-how represent an emerging revenue stream for suppliers as more end-users pursue vertical integration.

Geography Analysis

North America captured 35.55% revenue in 2025, underpinned by 15.4 billion gallons of U.S. corn ethanol and the continent’s deepest R&D ecosystem. The 2026 EPA mandate sets 590 million gallons of cellulosic biofuel, sustaining cellulase demand despite political debate over Renewable Fuel Standard targets. Canada’s Clean Fuel Regulations support wheat-straw ethanol, while Mexico’s E10 blend in metro areas fosters sugarcane-derived demand. Research institutions such as NREL and the Great Lakes Bioenergy Research Center published 134 enzyme papers in 2025, feeding a pipeline of licensed variants.

Asia-Pacific is the fastest-growing region at 7.98% CAGR through 2031 as China and India crank up ethanol blends and Southeast Asia boosts palm-oil biodiesel. China’s E10 rollout across 15 provinces adds 4 billion liters of ethanol demand and needs roughly 20,000 metric tons of amylase annually. India’s E20 target will double ethanol consumption to 10 billion liters by 2030, driving enzymes across 400 distilleries. Japan, South Korea and ASEAN economies layer additional fuel standards that diversify enzyme portfolios toward rice straw and waste cooking oil.

Europe benefits from mature biodiesel capacity and Renewable Energy Directive III’s 5.5% advanced-fuel sub-target, but growth is moderating as blending plateaus. Germany produced 3.2 million tons of biodiesel in 2025, leveraging lipases for rapeseed and used oil. France reached 95% E10 penetration, while the U.K. incentivizes double-counting of waste-based fuels. NORDIC countries push forestry-residue ethanol, requiring cold-active cellulases. Italy’s 600,000 ton advanced-biofuel capacity at Eni sites underscores ongoing, albeit slower, demand creation.

South America is anchored by Brazil’s 32 billion liters of sugarcane ethanol and RenovaBio credit scheme that values second-generation capacity at 2.5× first-generation. Raízen’s Bonfim plant alone consumes 410 metric tons of cellulase yearly and demonstrates economic viability for bagasse-to-ethanol conversion. Argentina’s soybean-oil biodiesel hits 2.1 million tons and explores lipase routes to cut energy costs. Colombia and Paraguay expand sugarcane distillation but remain smaller enzyme consumers.

Middle East and Africa remain emergent. Saudi Arabia targets 2 billion liters of waste-oil biofuel by 2030 under Public Investment Fund backing, while South Africa’s E10 and B5 mandates stimulate modest enzyme imports. The UAE pilots high-salinity algae fuels, requiring novel lipase and cellulase blends.

Competitive Landscape

The biofuel enzymes market displays high concentration: Novonesis Group, DuPont, AB Enzymes, Lallemand Inc. and dsm-firmenich command roughly 80% of global revenue. Novonesis filed 47 enzyme patents in 2025, 18 focused on thermostable cellulases operating above 65 °C, and is expanding Nebraska capacity by 40% to secure U.S. cellulosic ethanol supply. DuPont’s Accellerase TRIO delivers 92% glucose yield at 30% lower loading on corn stover, offering premium pricing power. dsm-firmenich’s acquisition of Amano Enzyme’s biofuel portfolio broadens lipase reach in Asia-Pacific.

Niche innovators exploit feedstock niches. MetGen Oy provides lignin-modifying enzymes that raise softwood glucose yield 12%, while Agrivida explores plant-integrated enzymes expressed in transgenic corn. Zymergen engineers cellulases with 40% higher specific activity, licensing to biorefineries for on-site production. On-site fermentation threatens logistics-based advantages of incumbents but opens licensing revenue for strain owners. Consolidated bioprocessing could disrupt the entire procurement model within a decade, yet performance gaps in ethanol tolerance keep it in development.

Strategic moves include Novonesis’ USD 75 million Nebraska expansion, DuPont-Raízen co-development pact and dsm-firmenich’s Amano acquisition. Financing rounds such as Iogen’s USD 250 million debt package and Advanced Enzyme Technologies’ new Indian plant underline capital commitment across the value chain.

Biofuel Enzymes Industry Leaders

AB Enzymes

DuPont

Lallemand Inc.

Novozymes A/S (Novonesis Group)

dsm-firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Celtic Renewables partnered with Enzyme Supplies Limited to incorporate its enzyme formulations into the company's bio-refining process. Enzyme Supplies Limited's customized enzymatic solutions were integrated into Celtic Renewables' patented acetone-butanol-ethanol (ABE) fermentation process.

- May 2025: Scientists from the Brazilian Center for Research in Energy and Materials (CNPEM), in collaboration with partners in Brazil and internationally, discovered an enzyme capable of transforming biofuel production processes. The enzyme, named CelOCE, was developed at CNPEM and was prepared for immediate application in industrial operations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the biofuel enzymes market as the value generated from sales of industrial-grade enzymes, principally amylases, cellulases, lipases, and related hydrolases, used to convert lipid, starch, and lignocellulosic feedstocks into biodiesel, starch-based ethanol, and advanced (cellulosic) ethanol. According to Mordor Intelligence analysts, the scope spans free, immobilized, and on-site produced catalysts supplied to fuel producers, biorefineries, and research pilots across every region.

Scope exclusion: laboratory reagents and enzymes adopted in non-fuel industries such as food processing, detergents, animal feed, and pharmaceuticals are outside this study.

Segmentation Overview

- By Product Type

- Amylases

- Cellulases

- Xylanases

- Other Product Types (Lipases, Accessory Enzymes, etc.)

- By Feedstock

- Starch Crops

- Sugar Crops

- Waste Cooking Oil and Grease

- Agricultural Residues

- Energy Crops (Switchgrass, Miscanthus)

- Forestry Residues

- Algae

- By Technology

- Free Enzyme Catalysis

- Immobilized Enzyme Systems

- Consolidated Bioprocessing (CBP)

- On-site Enzyme Production

- Continuous-flow Micro-reactor Systems

- By Application

- Corn/Starch-based Ethanol

- Biodiesel

- Lignocellulosic Ethanol

- Leather and Textile

- Other Applications (Biogas/Renewable Natural Gas, Biochemicals (e.g., biobutanol), etc.)

- By End-user Industry

- Fuel Producers (Biodiesel Plants, Ethanol Distilleries)

- Biorefineries

- Oil and Gas Blenders

- Chemical Manufacturers

- Other End-user Industries (Academic, Pilot Plants)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then interview enzyme technologists at biorefineries, process integrators, and policy experts across North America, Brazil, the EU, China, and India. These conversations verify actual enzyme dosages, price trends, and adoption hurdles, and they calibrate growth drivers uncovered in secondary work.

Desk Research

We start with extensive desk work, drawing on open datasets from the US Department of Energy's Bioenergy Technologies Office, the European Environment Agency, and India's Ministry of New and Renewable Energy, which reveal feedstock supply, blending mandates, and installed biofuel capacity. Trade association portals such as the Renewable Fuels Association, European Biodiesel Board, and the International Energy Agency Bioenergy Task update yearly production and consumption statistics that anchor volume estimates.

Company 10-Ks, investor decks, patent libraries accessed through Questel, and shipment intelligence from Volza allow us to benchmark average selling prices and check emerging process technologies. D&B Hoovers and Dow Jones Factiva supplement revenue splits, while peer-reviewed journals captured through Google Scholar clarify enzyme loadings and conversion yields. This list is illustrative; many other publicly available and subscription assets supported evidence gathering and validation.

Market-Sizing & Forecasting

A combined top-down and bottom-up approach is applied. National bioethanol and biodiesel output, adjusted for trade and feedstock mix, creates a demand pool that is multiplied by interview-validated dosage rates and weighted average selling prices. Supplier roll-ups and channel checks provide a bottom-up reasonableness screen before totals are finalized. Key variables include mandated blending percentages, second-generation plant capacity additions, average enzyme cost per gallon of ethanol, lipid feed price spreads, carbon credit trajectories, and technological shift toward consolidated bioprocessing. Multivariate regression with scenario analysis projects each driver, and missing datapoints are bridged through nearest available proxies agreed upon with domain experts.

Data Validation & Update Cycle

Outputs pass variance checks against historical series and independent indicators. Senior reviewers audit assumptions, question anomalies, and request re-contact where deviations exceed preset thresholds. We refresh the model each year and issue interim updates when policy or capacity announcements materially alter the outlook, ensuring purchasers receive the latest view.

Why Mordor's Biofuel Enzymes Baseline Earns Confidence

Published estimates often vary because firms select different product mixes, forecast horizons, and dosage assumptions.

Key gap drivers include: some publishers fold broader industrial enzymes revenues into the total, others model only bioethanol or only biodiesel, and a few assume aggressive price erosion without validating producer contracts. Mordor reports only enzymes sold directly for fuel production, updates pricing every six months through channel calls, and aligns currency conversions to the average fiscal-year exchange rate rather than spot.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 698.9 million (2025) | Mordor Intelligence | - |

| USD 753.6 million (2025) | Global Consultancy A | Includes laboratory enzyme kits and minor energy applications |

| USD 690.8 million (2024) | Industry Association B | Uses fixed 2020 average selling prices with no currency re-indexing |

| USD 1.89 billion (2025) | Trade Journal C | Aggregates all industrial enzymes for bioeconomy, not fuel-specific |

These contrasts show that when the right scope, fresh pricing, and transparent variables are applied, Mordor delivers a balanced, reproducible baseline clients can trust for planning and investment decisions.

Key Questions Answered in the Report

What is the estimated value of biofuel enzymes in 2026, and how large could the market become by 2031?

The market is valued at USD 0.74 billion in 2026 and is projected to reach USD 1.02 billion by 2031 on a 6.63% CAGR trajectory.

Which enzyme category shows the strongest growth outlook over 2026-2031?

Cellulases lead the expansion, with an expected 8.67% CAGR as lignocellulosic ethanol capacity moves from pilot to commercial scale.

Which geographic region is poised for the quickest demand acceleration?

Asia-Pacific is forecast to grow at about 7.98% a year, driven by China’s E10 and India’s E20 ethanol programs plus expanding palm-oil biodiesel in Southeast Asia.

What operational shift offers the greatest potential to cut enzyme procurement costs?

On-site enzyme production at biorefineries can trim purchased enzyme expense by roughly 20-25% while enabling real-time formulation tweaks.

Page last updated on: