Agricultural Lubricants Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

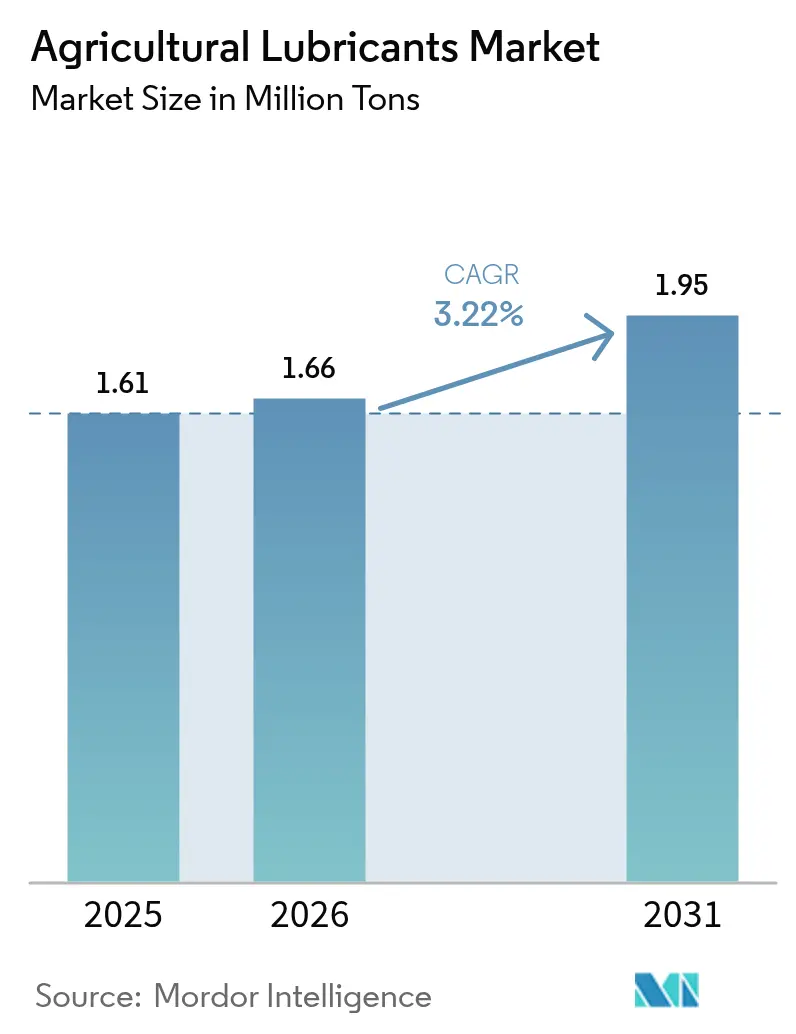

| Market Volume (2026) | 1.66 Million tons |

| Market Volume (2031) | 1.95 Million tons |

| Growth Rate (2026 - 2031) | 3.22% CAGR |

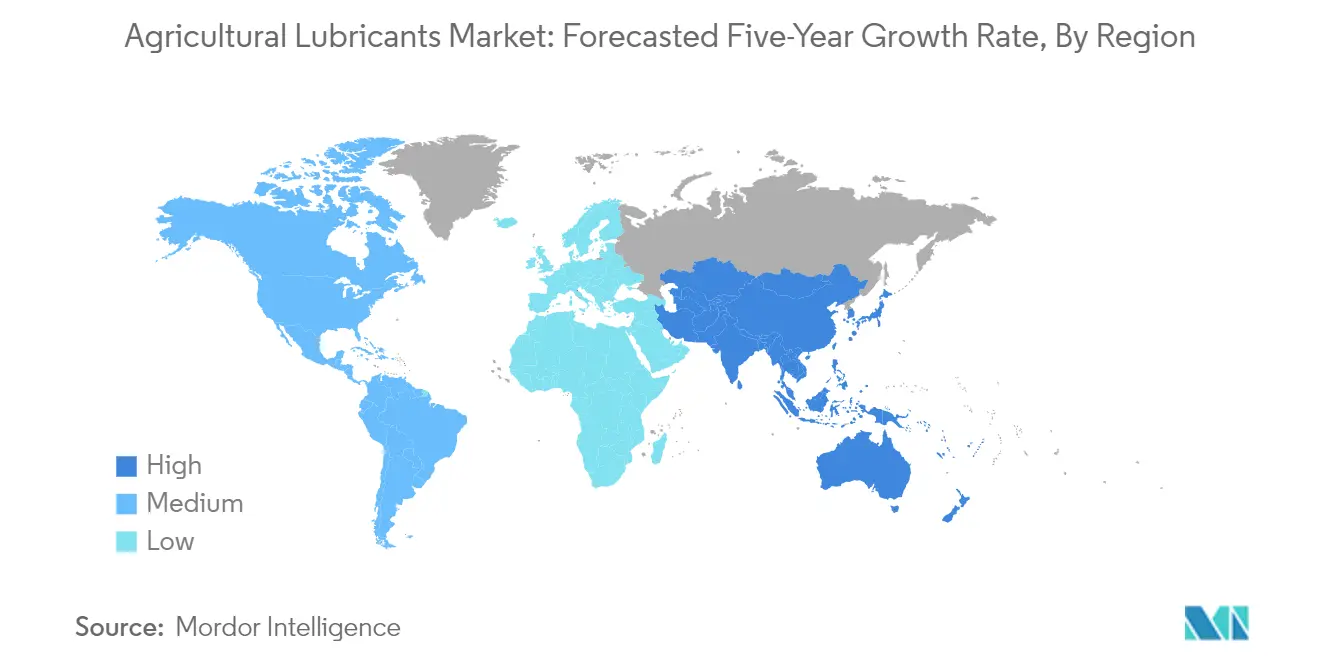

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Lubricants Market Analysis by Mordor Intelligence

The Agricultural Lubricants Market size was valued at 1.61 Million tons in 2025 and estimated to grow from 1.66 Million tons in 2026 to reach 1.95 Million tons by 2031, at a CAGR of 3.22% during the forecast period (2026-2031).

The agricultural lubricants market is experiencing significant transformation driven by shifting global agricultural patterns and increasing food security concerns. Major agricultural equipment manufacturers are expanding their production capabilities to meet rising global grain demand, particularly from Europe and the United States, which are seeking alternative grain sources from the Americas and Africa. This trend is evidenced in Colombia, where agricultural machinery sales have recently increased significantly due to growing international demand for grains. The agricultural sector's evolution has led to increased adoption of sophisticated machinery, creating a parallel demand for high-performance agricultural lubricants.

Technological advancements in agricultural equipment are reshaping the agricultural lubricants market landscape, with manufacturers focusing on developing products compatible with modern machinery. In France, according to AXEMA, tractor sales increased by 2.2% in 2022, with a notable trend toward higher-power tractors in the 150-300 hp range increasing by 16%. This shift toward more powerful and technologically advanced equipment has created demand for specialized ag lubricants that can handle increased performance requirements while ensuring optimal equipment protection and longevity. Major equipment manufacturers are increasingly incorporating smart technologies and precision farming capabilities, necessitating advanced lubricant formulations.

The industry is witnessing a strong push toward environmental sustainability and bio-based solutions. Agricultural machinery manufacturers are investing in electric and hybrid technology development, as exemplified by CNH Industrial Italia's EUR 39.4 million investment in developing electric hybrid tractor technology at their Modena plant in 2022. This technological shift is driving innovation in lubricant formulations, with manufacturers developing products that are both environmentally friendly and capable of meeting the specific requirements of new-generation machinery.

The agricultural lubricants market is characterized by significant regional variations in equipment adoption and lubricant requirements. In South Africa, the market demonstrated robust growth with 9,181 new tractors sold in 2022, marking a 17% increase from 2021 and the highest sales in 40 years. Similarly, in Argentina, the agricultural machinery sector showed remarkable growth, with sales reaching ARS 83,180 million in the third quarter of 2022, representing a 69.8% increase over the same period in 2021. These regional developments reflect the growing mechanization of agriculture globally and the corresponding increase in demand for specialized ag lubricants suited to local operating conditions and equipment types.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agricultural Lubricants Market Trends and Insights

Provision of Subsidy for Farm Machinery by the Indian and Chinese Governments

The Indian and Chinese governments have implemented comprehensive subsidy programs to support farmers in acquiring agricultural machinery, which has become a significant driver for the agricultural lubricants market. In India, from 2014-15 to March 2022, the government allocated INR 5,490.82 crore (USD 736 million) for agricultural mechanization, with the number of subsidized machines and equipment delivered to farmers increasing from 1,378,755 in January 2022 to 1,388,314 in December 2022. The state of Madhya Pradesh introduced the MP Kisan Anudan Yojana in 2022, offering grants ranging from INR 30,000 to INR 60,000 for new technical farming equipment, with women farmers receiving higher benefits of 30% to 50% subsidy.

The Chinese government has demonstrated a similar commitment by allocating CNY 19 billion (~USD 2.94 billion) in 2021 for agricultural machinery subsidies, representing an increase of CNY 2 billion from 2020. Under China's "Made in China 2025" plan, the country aims to exceed CNY 800 billion in agricultural machinery output by 2025, positioning itself as the world's largest agricultural equipment manufacturer. The government has also initiated programs to replace old agricultural machinery that consumes excessive energy and causes pollution, offering subsidies for tractors, combine harvesters, paddy transplanters, feed and grass shredders, and motorized sprayers across the country, which in turn boosts demand for tractor lubricants.

Increasing Farm Mechanization Rates in Developing Countries

Farm mechanization has become a crucial component of agricultural modernization in developing countries, driving significant growth in the agricultural oils market. The mechanization levels vary significantly across regions, with developed nations like the United States achieving 95% mechanization, while developing countries show varying rates - Brazil at 75%, China at 57%, and India at 40-45%. This disparity presents substantial growth opportunities as developing nations continue to advance their agricultural sectors. In China, the number of large and medium (LM) tractors reached 4.98 million units in 2021, representing a 4% increase from 4.77 million units in 2020, demonstrating the rapid pace of mechanization.

The trend towards increased mechanization is particularly evident in India, where the tractor industry is valued at approximately INR 39,000 crores (~USD 4,790 million), accounting for around 10% of the global industry. The country's growing focus on mechanization is reflected in its export performance, with tractor exports reaching a historic high of 131,850 units in 2022, a 6% increase from 2021, representing approximately 2.1% of global tractor sales. This transformation is supported by various government initiatives, including the Sub Mission on Agricultural Mechanization (SMAM) launched in 2014-15, which has facilitated the establishment of 27,828 Custom Hiring Centers (CHC) from 2014-15 to 2020-21, making agricultural machinery more accessible to small and marginal farmers, thereby increasing the demand for farm lubricants.

Increasing Cost of Farm Labor

The rising cost of farm labor has emerged as a significant driver for agricultural mechanization and, consequently, the agricultural lubricants market. This trend is particularly evident in China, where the agricultural workforce has shown a consistent decline, with only 22.9% of the total workforce employed in the agricultural sector in 2021, representing a 2.9% decrease from 2020. The shrinking agricultural labor force has led to increased labor costs, compelling farmers to adopt mechanized solutions for maintaining productivity levels and managing operational expenses effectively.

The impact of rising labor costs is further amplified by rapid urbanization trends, with the global urban population expected to increase from 57% in 2022 to 68% by 2050. This demographic shift is particularly significant in Asia and Africa, which are projected to account for 90% of this urban growth, leading to a substantial decline in available agricultural labor. The combination of decreasing labor availability and increasing wages has accelerated the adoption of agricultural machinery, particularly in developing regions where traditional farming methods are being replaced by mechanized solutions. This transition has created a sustained demand for tractor lubricants, as farmers increasingly rely on machinery to maintain productivity levels while managing labor costs effectively.

Segment Analysis

Engine Oil Segment in Agricultural Lubricants Market

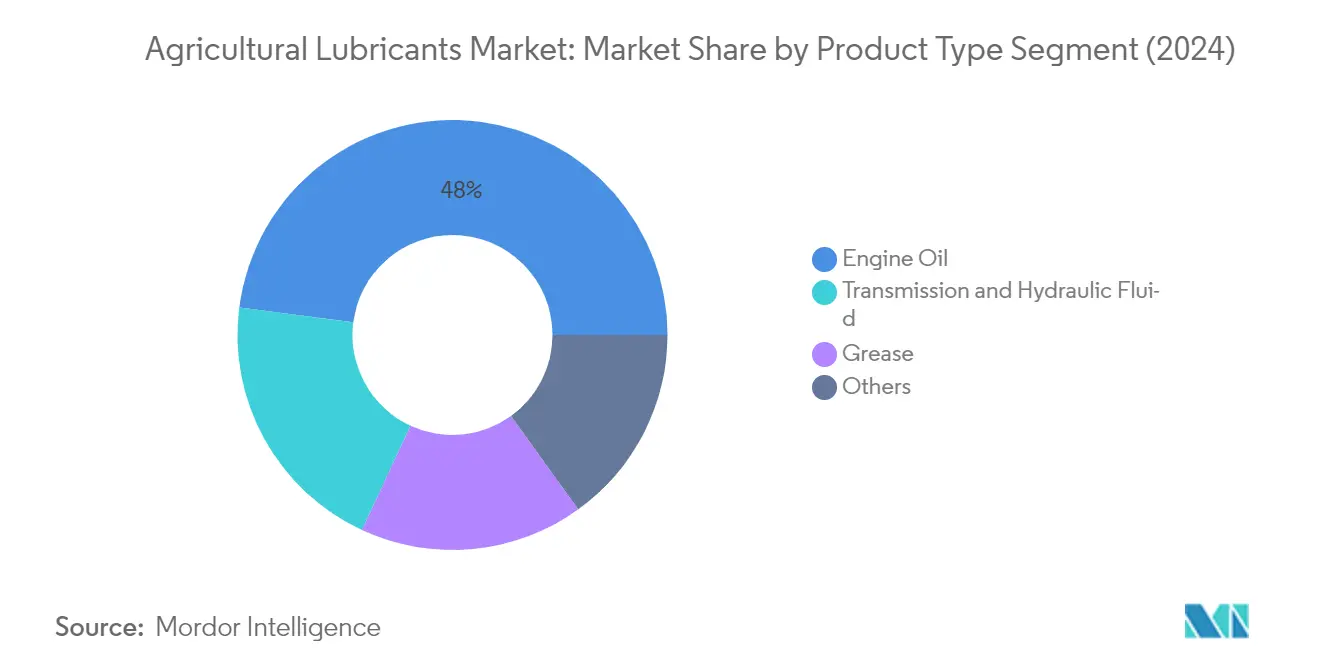

Engine oil dominates the agricultural lubricants market, commanding approximately 47.20% of the total market share in 2025. This segment's prominence is driven by the essential role agricultural engine oil plays in protecting and maintaining agricultural machinery engines, particularly in tractors and heavy farming equipment. Engine oils prevent the agglomeration of soot, provide protective films on moving metal surfaces, deliver deposit and corrosion protection, and neutralize harmful acids. The segment's leadership position is further strengthened by the increasing mechanization rates in developing countries and the rising adoption of advanced agricultural machinery. Modern agricultural engine oils are specifically formulated to meet the demanding requirements of both turbocharged and naturally aspirated diesel engines, while also offering enhanced thermal stability and oxidation resistance for extended engine life.

Transmission and Hydraulic Fluid Segment in Agricultural Lubricants Market

The transmission and hydraulic fluid segment represents a vital component of the agricultural lubricants market, with products specifically designed to ensure optimal performance in agricultural machinery's transmission systems and hydraulic operations. These fluids are crucial for maintaining efficient power transfer and protecting critical components in modern farming equipment. The segment is experiencing steady growth driven by the increasing complexity of agricultural machinery and the rising demand for high-performance transmission systems. Manufacturers are focusing on developing advanced formulations that offer improved oxidation stability, better air release properties, and enhanced pump life. The growing trend toward automated and precision farming equipment is further boosting the demand for high-quality agricultural hydraulic oil that can maintain consistent performance under varying operating conditions.

Remaining Segments in Product Type Segmentation

The remaining segments in the agricultural lubricants market include agricultural grease and other specialty products, each serving specific applications in farming equipment. Agricultural greases play a crucial role in providing lubrication for bearings, chassis components, and other mechanical parts that require consistent lubrication under heavy loads and adverse conditions. The other products segment encompasses specialized lubricants such as chain oils, vacuum pump oils, and various other application-specific products. These segments are essential for maintaining the overall efficiency and longevity of agricultural equipment, with manufacturers continuously developing new formulations to meet the evolving needs of modern farming machinery and environmental regulations.

Geography Analysis

The Asia-Pacific region represents the largest and most dynamic agricultural lubricants market globally, driven by increasing farm mechanization rates and government support for agricultural equipment adoption. Countries like China and India are leading the transformation through various subsidy schemes and policies promoting farm equipment usage. Japan and South Korea, despite their smaller agricultural sectors, maintain steady demand through high-tech farming practices. The region's diversity in farming practices, from large-scale mechanized operations to small-scale farming, creates varied demands for agricultural lubricants across different applications, including engine oils, transmission fluids, and hydraulic oils.

India dominates the Asia-Pacific agricultural lubricants landscape as the largest market in the region. The country's agricultural sector is undergoing rapid mechanization, supported by government initiatives like the Sub Mission on Agricultural Mechanization (SMAM) and various state-level subsidy programs. With approximately 44.60% share of the regional market in 2025, India's dominance is driven by its massive agricultural base and increasing tractor sales. The country's position is further strengthened by its status as one of the world's largest tractor manufacturers, with domestic companies expanding their production capabilities and international players establishing local manufacturing facilities.

India also leads the region in terms of growth potential, with a projected CAGR of approximately 4.86% during 2026-2031. This growth is fueled by increasing farm mechanization rates, currently at 40-45% compared to developed nations' 90%, indicating significant room for expansion. The country's agricultural machinery industry is witnessing substantial investments in manufacturing facilities, particularly in the tractor segment. The government's focus on increasing food production and improving agricultural productivity through mechanization continues to drive demand for agricultural machinery, consequently boosting the agricultural lubricants market.

North America represents a mature agricultural lubricants market, characterized by high mechanization rates and advanced farming practices. The region's market is driven by the presence of large commercial farms, sophisticated agricultural equipment, and strict maintenance requirements. The United States, Canada, and Mexico each contribute uniquely to the market dynamics, with varying agricultural practices and equipment usage patterns. The region's focus on precision farming and sustainable agricultural practices influences the demand for high-performance and environmentally friendly agricultural lubricants.

The United States stands as the dominant force in North America's agricultural lubricants market, commanding approximately 81.75% of the regional market share in 2025. The country's leadership position is supported by its vast agricultural land, high mechanization rates, and advanced farming practices. American farmers' emphasis on equipment maintenance and optimization of agricultural operations drives the demand for high-quality lubricants. The presence of major agricultural equipment manufacturers and lubricant producers further strengthens the market infrastructure.

Mexico emerges as the fastest-growing market in North America, driven by ongoing modernization of its agricultural sector and increasing adoption of mechanized farming practices. The country's agricultural sector is experiencing significant transformation through technology adoption and equipment modernization. Mexico's strategic position in agricultural trade and government initiatives to boost agricultural productivity are creating new opportunities for agricultural lubricant manufacturers. The growing emphasis on efficient farming practices and increasing investment in agricultural machinery continue to drive market growth.

Europe's agricultural lubricants market is characterized by its sophisticated farming practices and high mechanization levels across the region. The market landscape varies significantly from the advanced agricultural sectors of Germany and France to the evolving markets in Eastern Europe. The region's strict environmental regulations and emphasis on sustainable farming practices influence the development and adoption of agricultural oils. Countries across the region are witnessing varying levels of market development based on their agricultural modernization stages and equipment usage patterns.

France leads the European agricultural lubricants market, leveraging its position as one of the largest agricultural producers in Europe. The country's agricultural sector is characterized by large-scale farming operations and high mechanization rates. French farmers' focus on equipment maintenance and optimization of agricultural operations drives the demand for premium quality lubricants. The presence of major agricultural equipment manufacturers and strong distribution networks further strengthens the market position.

Germany shows the most promising growth trajectory in the European agricultural lubricants market. The country's agricultural sector is undergoing continuous modernization with increasing adoption of advanced farming equipment and precision agriculture practices. German farmers' emphasis on equipment efficiency and maintenance creates steady demand for high-performance lubricants. The strong presence of agricultural machinery manufacturers and ongoing technological advancements in the farming sector support market growth.

The Rest of World region, encompassing markets across South America, the Middle East, and Africa, presents diverse opportunities in the agricultural lubricants sector. Each region brings unique characteristics to the market, from Brazil's large-scale mechanized farming to the emerging agricultural sectors in Middle Eastern countries. Saudi Arabia leads in terms of market size, while Brazil shows the fastest growth potential. The increasing focus on agricultural modernization and government initiatives to boost farming efficiency drive market growth across these regions. The adoption of modern farming equipment and practices continues to create new opportunities for agricultural lubricant manufacturers.

Competitive Landscape

Top Companies in Agricultural Lubricants Market

The agricultural lubricants market is dominated by major oil and gas companies, including Shell Plc, Exxon Mobil Corporation, Chevron Corporation, TotalEnergies, FUCHS, and BP Plc. These companies focus on developing innovative lubricant solutions specifically designed for modern agricultural machinery and equipment. Product development efforts are centered around creating environmentally friendly and biodegradable lubricants while maintaining high-performance standards. Companies are strengthening their distribution networks and partnerships with agricultural equipment manufacturers to enhance market presence. Strategic investments in research and development facilities, particularly in key regions like Asia-Pacific, Europe, and North America, demonstrate the industry's commitment to technological advancement. Market leaders are also expanding their product portfolios through acquisitions and collaborations to offer comprehensive lubrication solutions for various agricultural applications.

Consolidated Market with Strong Regional Players

The agricultural lubricants market exhibits a consolidated structure at the global level, with multinational oil and gas conglomerates controlling a significant portion of the market share. These large corporations leverage their extensive manufacturing capabilities, established distribution networks, and strong relationships with OEMs to maintain their market positions. Regional and local players, particularly in emerging markets, maintain competitive positions through specialized product offerings and a deep understanding of local farming practices and requirements. The market has witnessed several strategic mergers and acquisitions, such as the creation of HF Sinclair Corporation through the merger of HollyFrontier Corporation and Holly Energy, aimed at strengthening market presence and expanding geographical reach.

The competitive landscape is characterized by varying levels of integration across the value chain, with many leading players being backward integrated into base oil production. This integration provides these companies with better control over raw material costs and quality, while also enabling them to respond more effectively to market demands. Companies are increasingly focusing on developing region-specific product portfolios and establishing local manufacturing facilities to better serve different agricultural markets. The presence of strong regional brands and the importance of local distribution networks create significant barriers to entry for new players, while also providing opportunities for strategic partnerships and collaborations.

Innovation and Sustainability Drive Future Success

Success in the agricultural lubricants market increasingly depends on companies' ability to develop sustainable and high-performance products while maintaining cost competitiveness. Market leaders are investing in research and development to create advanced lubricant formulations that meet evolving equipment requirements and environmental regulations. Companies are also focusing on strengthening their technical support services and customer relationships through digital platforms and specialized agricultural sector expertise. The development of bio-based lubricants and products with extended drain intervals represents a key differentiator for companies looking to gain market share.

For new entrants and smaller players, success lies in identifying and serving niche market segments with specialized products and services. Companies need to develop strong relationships with agricultural equipment manufacturers and local distributors to establish market presence. The increasing focus on sustainable farming practices and environmental regulations presents opportunities for companies to differentiate themselves through eco-friendly product offerings. Building a strong technical service network and providing comprehensive customer support are becoming crucial factors for success in this market. Companies also need to maintain flexibility in their operations to adapt to changing agricultural practices and seasonal demand variations.

Agricultural Lubricants Industry Leaders

Shell plc

Fuchs

Exxon Mobil Corporation

TotalEnergies SE

BP p.l.c.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2023: Phillips 66 acquired Hunt & Sons Inc., a diversified petroleum distribution company based in Sacramento, California. The company specializes in commercial fleet fueling services, bulk fuel supply, and comprehensive lubricant solutions for industrial, commercial, agricultural, and automotive use.

- March 2023: Exxon Mobil Corporation announced that it invested nearly USD 110 million to build a lubricant manufacturing plant at the Maharashtra Industrial Development Corporation’s Isambe Industrial Area in Raigad, India.

- August 2022: Phillips 66 announced that it submitted a non-binding proposal to the board of directors of DCP Midstream's general partner, offering to buy all publicly held common units of DCP Midstream for cash. Phillips 66 is proposing USD 34.75 in compensation for each outstanding publicly-held common unit of DCP Midstream. It was part of a deal structured as a merger of DCP Midstream with an indirect subsidiary of Phillips 66, with DCP Midstream surviving.

- March 2022: HollyFrontier Corporation and Holly Energy created HF Sinclair Corporation, followed by the acquisition of Sinclair Oil Corporation and Sinclair Transportation Company. It was to enhance the company's lubricants business and strengthen its presence in the competitive market.

- March 2022: Morris Lubricants launched an innovative new range of advanced multifunctional lubricants designed to cover the majority of agricultural requirements. Applications for these lubricants included engines, gearboxes, hydraulics, and oil-immersed brake systems in a wide variety of agricultural equipment.

Global Agricultural Lubricants Market Report Scope

Agriculture-specific lubricants are designed to avoid contamination, protect machinery from oxidation, corrosion, and rust, and provide longer oil drain intervals, resulting in lower oil usage. Using the proper lubricants boosts equipment uptime and ensures operational reliability regardless of weather or terrain.

The global agricultural lubricants market is segmented by product type and geography (Asia-Pacific, North America, Europe, and the rest of the world). By product type, the market is segmented into engine oil, transmission, hydraulic fluid, and grease. The report also covers the market size and forecasts for the agricultural lubricants market in 12 countries across major regions.

The market size and forecasts for agriculture lubricants are provided in terms of volume (tons) for all the above segments.

| Engine Oil |

| Transmission and Hydraulic Fluid |

| Grease |

| Other Product Types |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Rest of the World |

| Product Type | Engine Oil | |

| Transmission and Hydraulic Fluid | ||

| Grease | ||

| Other Product Types | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Rest of the World | ||

Key Questions Answered in the Report

How big is the Agriculture Lubricants Market?

The Agriculture Lubricants Market size is expected to reach 1.66 million tons in 2026 and grow at a CAGR of 3.22% to reach 1.95 million tons by 2031.

What is the current Agriculture Lubricants Market size?

In 2026, the Agriculture Lubricants Market size is expected to reach 1.66 million tons.

Who are the key players in Agriculture Lubricants Market?

Shell plc, Fuchs, Exxon Mobil Corporation, TotalEnergies SE and BP p.l.c. are the major companies operating in the Agriculture Lubricants Market.

Which is the fastest growing region in Agriculture Lubricants Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Agriculture Lubricants Market?

In 2026, the Asia Pacific accounts for the largest market share in Agriculture Lubricants Market.

What years does this Agriculture Lubricants Market cover, and what was the market size in 2025?

In 2025, the Agriculture Lubricants Market size was estimated at 1.66 million tons. The report covers the Agriculture Lubricants Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Agriculture Lubricants Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: