Market Overview

| Study Period | 2021 - 2031 |

|---|---|

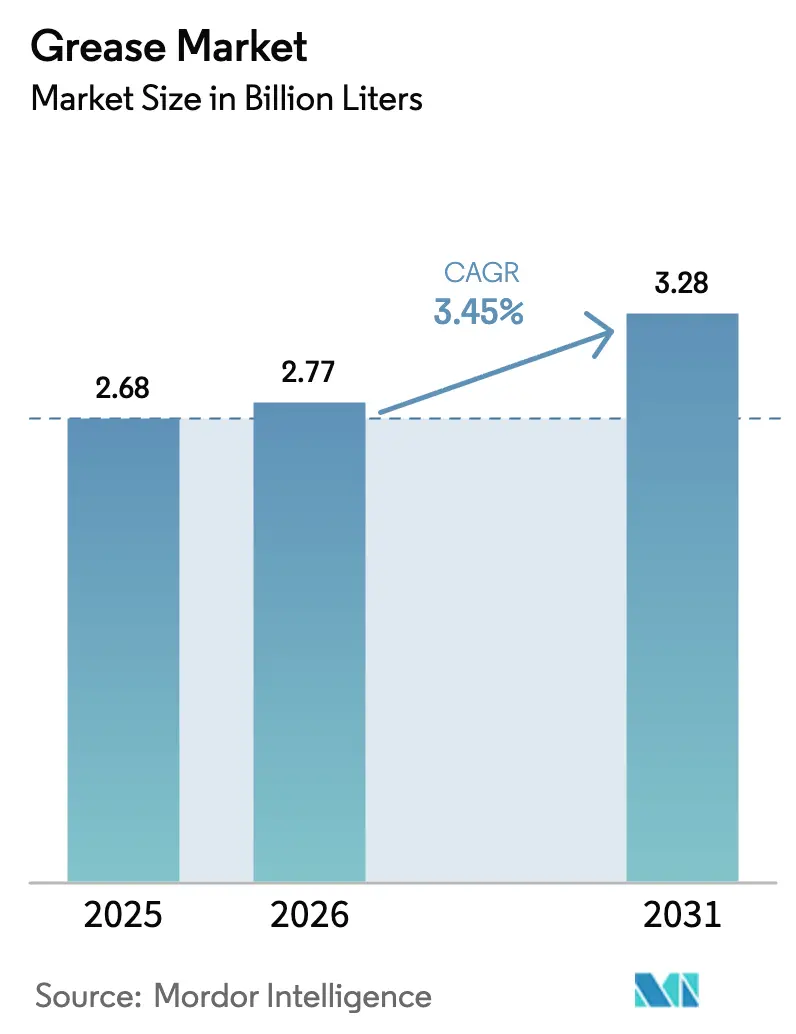

| Market Volume (2026) | 2.77 Billion liters |

| Market Volume (2031) | 3.28 Billion liters |

| Growth Rate (2026 - 2031) | 3.45% CAGR |

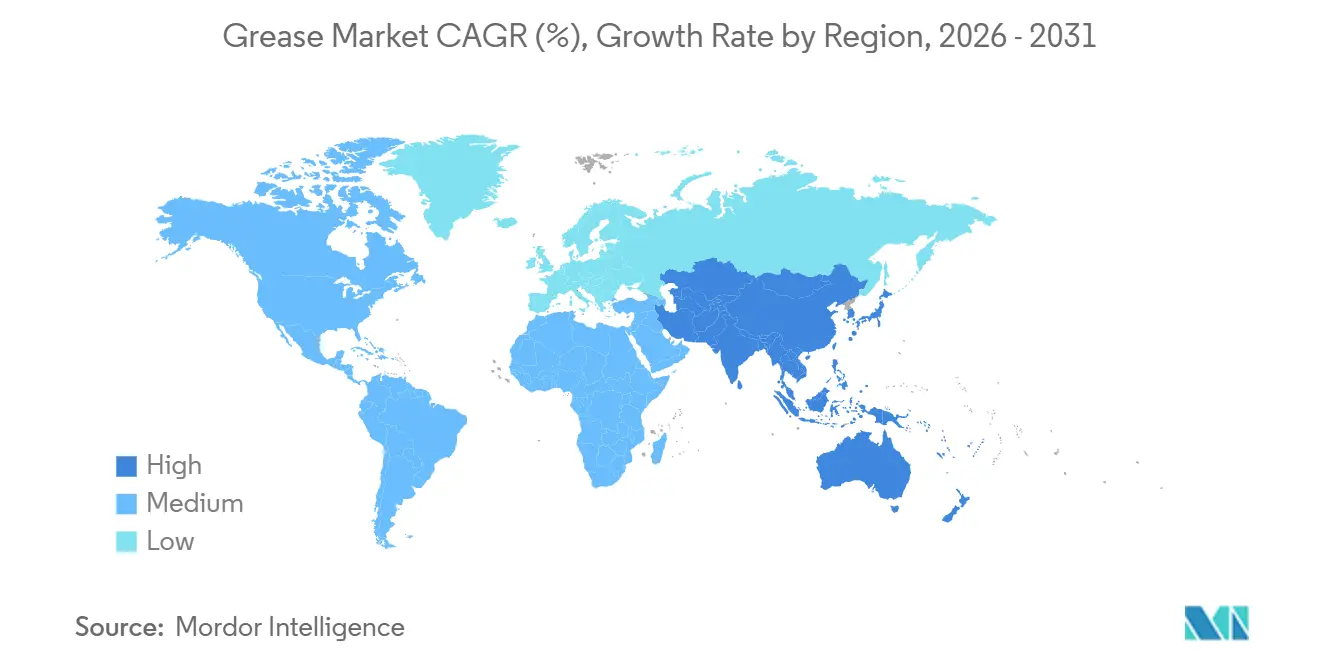

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Grease Market Analysis by Mordor Intelligence

The Grease Market size was valued at 2.68 Billion liters in 2025 and is estimated to grow from 2.77 Billion liters in 2026 to reach 3.28 Billion liters by 2031, at a CAGR of 3.45% during the forecast period (2026-2031). This growth reflects ongoing industrialization, surging demand for water-resistant marine grades, and the rapid pivot toward calcium-sulfonate and polyurea chemistries that buffer buyers from lithium-carbonate price swings. Food-processing plants are replacing legacy lithium soaps with NSF H1-certified formulations to mitigate contamination risk, while wind-turbine fleets and electric-vehicle powertrains favor synthetic-oil greases that perform from -40°C to +150°C. Offshore deep-water drilling rigs in the Gulf of Mexico, Brazil, and West Africa now specify calcium-complex grades capable of withstanding cyclic loads and seawater washout, pulling specialty marine volumes into double-digit growth. Parallel investments in re-refined Group II and Group III base-oil projects lower input costs for high-performance products, maintaining manufacturer margins even as competitive intensity rises.

Key Report Takeaways

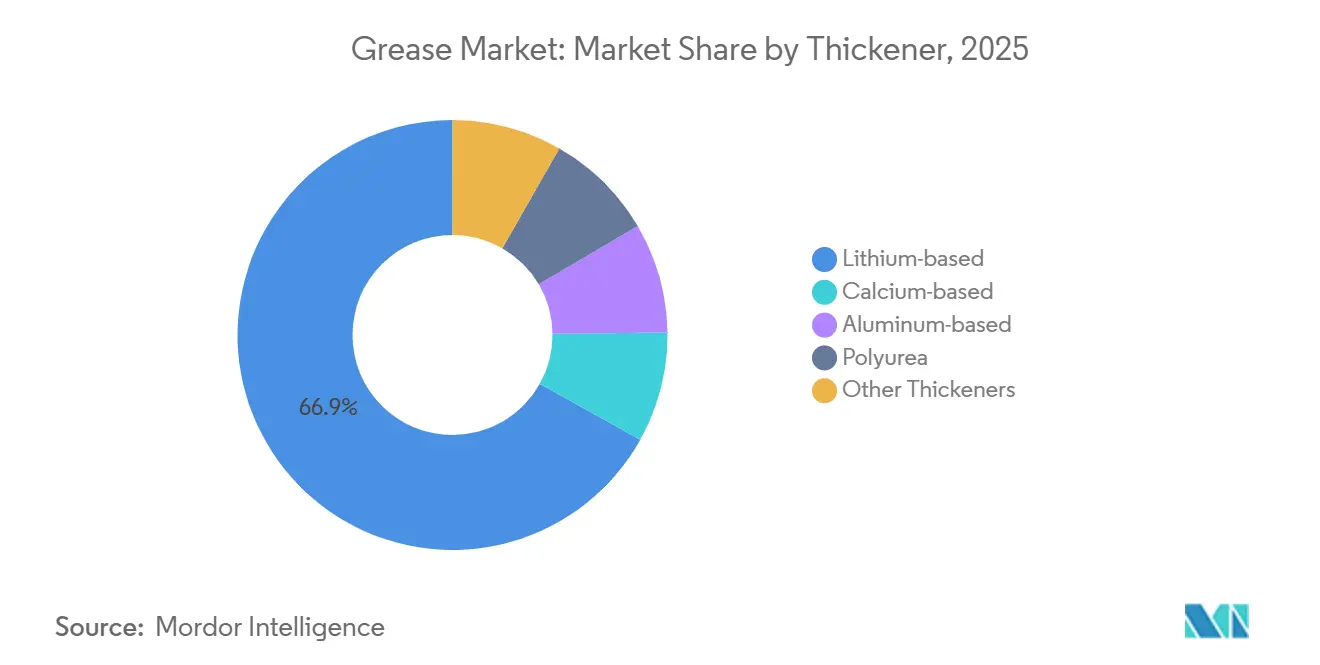

- By thickener, lithium-based accounted for 66.89% of the grease market size in 2025, while calcium-based is advancing at a 8.22% CAGR through 2031.

- By product type, mineral oils accounted for 75.19% of the grease market size in 2025; the synthetic oil segment is advancing at a 4.51% CAGR through 2031.

- By performance grade, high-temperature greases held 36.68% of the grease market size in 2025 and are forecast to grow at a 6.61% CAGR through 2031.

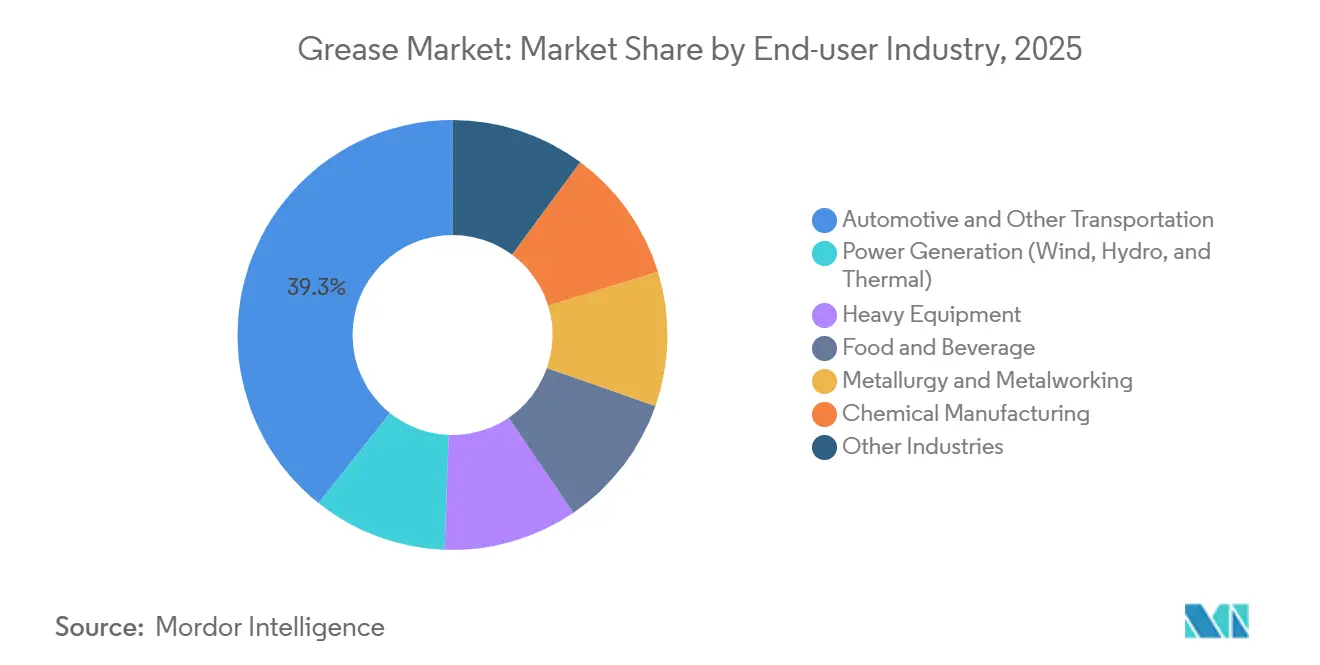

- By end-user, automotive and transportation commanded 39.28% of the grease market size in 2025, while power generation is the fastest-expanding end-user at a 4.82% CAGR through 2031.

- By geography, Asia Pacific dominated with 49.75% of the grease market share in 2025 and is outpacing all other regions at a 4.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Grease Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hygienic food-grade lubrication uptake | +0.8% | North America, Europe, global food hubs | Medium term (2-4 years) |

| EV e-powertrain bearing shift | +0.9% | Asia-Pacific core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Offshore deep-water drilling demand | +0.6% | Gulf of Mexico, Brazil, Middle East and Africa | Short term (≤ 2 years) |

| Construction equipment expansion | +0.7% | China, India, ASEAN, Middle East | Medium term (2-4 years) |

| Power-generation investments | +0.5% | Europe offshore wind, Asia-Pacific hydro and thermal plants | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hygienic Food-Grade Lubrication Uptake in Processing Lines

Demand for NSF H1-certified aluminum-complex and calcium-sulfonate greases is climbing because regulatory inspections now treat lubricant selection as a preventive control. Processing plants that handle dairy, brewing, and ready-meal products factor potential recall costs into total-cost-of-ownership analysis, making the 15-25% price premium acceptable. These grades maintain oxidation stability above 150 °C and resist steam-cleaning washout, preventing metallic-soap taste migration. ISO 21469 audits in Europe and North America accelerate adoption as multinational brands unify global hygiene standards. Vendors that offer bundled food-grade grease, technical support, and documentation gain preferred-supplier status with processors seeking audit readiness[1]NSF International, “NSF/ANSI 21469 Certified Lubricants List,” nsf.org.

EV E-Powertrain Bearing Shift to Lithium-Complex & Calcium-Sulfonate Greases

Electric-vehicle motors run at 10,000–15,000 rpm and impose electrical conductivity as well as mixed-rolling conditions that legacy lithium soaps cannot handle. Calcium-sulfonate and lithium-complex greases doped with ionic-liquid additives cut friction losses by up to 45%, reducing rotor temperature and extending driving range. Battery-pack assembly lines in China specify calcium systems to avoid additional lithium-carbonate exposure, a hedge that became standard after the commodity’s 2022-2024 price whiplash. Automakers are locking multi-year contracts for these chemistries, insulating bills of materials from raw-material swings. Polyurea formulations, which remain consistent from -40°C to +180°C, are gaining ground in wheel-bearing and CV-joint applications because they resist water washout.

Offshore Deep-Water Drilling Boosting Water-Resistant Marine Greases

Production start-ups at fields exceeding 1,500 m depth depend on calcium-complex grades with dropping points above 260°C. Blowout-preventer actuators, riser tensioners, and drill-string threads consume 200–300 kg of grease per rig each month. Operators increasingly mandate products meeting ISO 12924 for biodegradability alongside API RP 5A3 thread-compound standards. Calcium-sulfonate formulations surpass lithium soaps in cyclic-load and seawater-washout resistance, improving safety margins. Supply contracts frequently bundle grease with on-site lubrication audits, cementing long-term vendor relationships[2]Chevron Corporation, “Anchor Project Overview,” chevron.com.

Construction Equipment Boom Driving Extreme-Pressure Greases

Megaproject pipelines in India, Indonesia, and Gulf countries elevate excavator and crane utilization above 80%, pushing annual per-machine grease demand to 75–100 kg. Equipment makers now recommend NLGI Grade 2 greases featuring oxidation stability above 200 hours in ASTM D942 testing. Molybdenum-disulfide and graphite help sustain loads over 3,000 MPa when hydrodynamic films collapse. EU REACH restrictions on boron-nitride and PFAS additives compel formulators to adopt organic friction modifiers instead, triggering costly reformulations but opening white space for calcium-sulfonate solutions. Vendors able to certify compliance win a share in fleet contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lithium-carbonate price volatility | -0.4% | Global, acute in Asia-Pacific and North America | Short term (≤ 2 years) |

| EU REACH tightening on PFAS & boron nitride | -0.3% | Europe with spill-over to North America | Medium term (2-4 years) |

| Low penetration of automatic lubrication | -0.2% | South America and parts of Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lithium-Carbonate Cost Volatility Due to Battery-Sector Competition

Spot prices dropped from USD 80,000/t in 2022 to USD 10,000-12,000/t in 2024 when new Chinese brine projects outpaced EV uptake. Grease blenders locked into high-cost contracts saw margins shrink by 200–300 basis points and lengthened purchasing lead times from eight to sixteen weeks. The shock fueled diversification toward calcium-sulfonate and polyurea thickeners that lack battery-sector linkage. Procurement teams now dual-source to cap exposure, but the experience underscores structural fragility in lithium-soap economics. Although prices stabilized by late 2024, risk premiums remain embedded in supplier agreements.

EU REACH Tightening on PFAS & Boron-Nitride Additives

The February 2023 proposal to restrict many PFAS and boron compounds under Annex XVII affects extreme-pressure and high-temperature grades. Some substances phase out by 2026, others later, yet formulators have already moved to substitute chemistries to avoid stranded inventory. Calcium-sulfonate complexes can replace PFAS-laden additives in most cases, though four-ball-wear tests show a 10–15% loss in load-carrying capacity. Multinational OEMs adopt the strictest common denominator, effectively exporting European standards to Asia-Pacific and North America. R&D budgets for specialty greases rose 15–20% to accelerate compliant product launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Thickener: Calcium Formulations Hedge Lithium Exposure

Lithium-based greases maintained a 66.89% grease market share in 2025 as decades of OEM approvals anchor their position. However, calcium-sulfonate greases are advancing at an 8.22% CAGR because they deliver dropping points beyond 260°C, superior water resistance, and excellent four-ball-wear results. Marine, mining, and steel-mill operators adopt them to avoid washout and heavy-load failures. Chevron’s Rykon launch in 2024 targets this space with a load-carrying capacity that surpasses lithium complexes, catalyzing further substitution. Aluminum-complex grades occupy niche high-temperature services such as kiln bearings where 250°C stability offsets a 20–30% price premium. Polyurea chemistries progress as the preferred solution for EV wheel bearings and turbine yaw drives thanks to oxidation resistance over -40°C to +180°C cycles. Specialty thickeners like bentonite and silica gel underpin NSF H1 clean-room applications, reinforcing supplier portfolios.

Calcium and polyurea adoption mirrors procurement strategies that diversify away from lithium-carbonate volatility. Buyers draw dual-sourcing frameworks that blend lithium complexes with calcium equivalents, shifting market-share trajectories through 2031. Polyurea use in wind turbines also supports extended maintenance intervals, cutting downtime and lowering lifecycle cost. Together, these trends raise the calcium-sulfonate and polyurea slices of the grease market size while lithium-based dominance erodes steadily.

By Product Type: Synthetic Oils Gain Ground in Extreme Environments

Mineral-oil greases still account for 75.19% of 2025 volume, yet synthetic formulations grow at 4.51% CAGR as performance needs outstrip conventional limits. Polyalphaolefin and ester bases carry viscosity indices above 140 and resist oxidation beyond 1,000 hours, enabling 12-month turbine relubrication cycles. ExxonMobil’s 2025 re-refined Group II and Group III project in France and the Netherlands lowers synthetic input cost by 10–15%, narrowing historical price gaps with mineral products. Bio-based greases, while niche, secure mandates in forestry and marine zones that enforce low aquatic toxicity under ISO 12924. This segment’s momentum demonstrates that total-cost-of-ownership considerations can outweigh higher unit prices when equipment downtime is critical.

Mineral oil grades continue to dominate automotive chassis lubrication and general industrial services where cost sensitivity prevails. However, as synthetic prices fall and OEM drain intervals lengthen, substitution edges upward. Bio-based products face the steepest adoption curve due to 50–70% price premiums and narrower temperature windows, yet regulatory carrots and sticks are expanding their footprint. Overall, synthetic expansion segments lift the synthetic share of the grease market size year over year.

By Performance Grade: High-Temperature Formulations Lead Volume and Growth

High-temperature greases commanded 36.68% of the 2025 volume and carry a 6.61% CAGR outlook. Steel mills, glass furnaces, and cement kilns run bearings above 200 °C where lithium soaps liquefy, making calcium-sulfonate and polyurea complexes the default choice. Extreme-pressure grades support mining and construction equipment facing loads above 3,000 MPa, though REACH-driven additive reformulations challenge legacy offerings. Low-temperature greases cater to Nordic wind farms and Canadian mining, where -40°C conditions prevail, cementing polyurea’s arctic credentials.

The high-temperature segment benefits from India’s drive to 180 million t of steel by 2030, while low-temperature demand rises with offshore wind installations in the North Sea and Baltic. EU additive restrictions shave performance margins for some extreme-pressure products, spurring R&D into organic modifiers. These dynamics collectively elevate performance-grade differentiation as a key battleground for competitive advantage within the grease market.

By End-User Industry: Power Generation Outpaces Automotive Growth

Automotive and other transportation segments represented 39.28% of 2025 demand, but power-generation assets will grow faster at a 4.82% CAGR as wind, hydro, and thermal fleets age. A single wind turbine consumes 200–300 kg of grease across its life cycle, and the projected 500 GW of new renewable installations through 2030 signals 50,000–60,000 t of incremental volume. OEMs such as Vestas and Siemens Gamesa specify polyurea or lithium-complex products that stretch relubrication intervals, lowering maintenance costs. Construction equipment remains buoyant on Asian and Middle Eastern infrastructure pipelines, raising per-machine grease consumption. Food and beverage processors accelerate NSF H1 adoption, steering demand toward aluminum-complex and calcium-sulfonate bases. Metallurgy and metalworking players migrate from boron-nitride additives to compliant calcium complexes under REACH guidance.

Collectively, these shifts recalibrate the industry mix, with power generation, construction, and food processing chipping away at automotive’s share while supplying higher-margin outlets for specialty formulators. The result is a gradual uptick in average selling price, even as overall grease market share continues to evolve.

Geography Analysis

Asia-Pacific held 49.75% of global volume in 2025 and is forecast to post a 4.39% CAGR. Chinese manufacturing exceeds 30 million vehicles a year, with BYD assembly lines now using calcium-sulfonate greases in cooling modules to reduce exposure to lithium swings. India’s National Infrastructure Pipeline drives extreme-pressure consumption in excavator and crane fleets operating above 80% utilization. Japan and South Korea transition automotive exports to EV platforms, embedding polyurea and lithium-complex solutions that lower bearing friction by 45%. Shell’s 12,000 t Indonesian plant and triple-capacity Thailand site reinforce regional supply security, reflecting long-term confidence in ASEAN industrial growth.

North America benefits from near-shoring that boosts Mexican vehicle production past 4 million units in 2024, encouraging local grease sourcing. The United States leads shale drilling and food-grade adoption, while onshore wind corridors in Texas and the Great Plains absorb synthetic volumes. Chevron’s Anchor field in the Gulf of Mexico consumes marine grades engineered for deep-water loads. Canadian mining operations require arctic-rated greases for sub-zero environments, leaning on polyurea and synthetic PAO chemistries.

Europe presents a mixed picture. German automotive output softened in 2025, yet offshore wind build-outs in the North Sea and Baltic accelerate. Nordic nations demand arctic-grade greases with -50°C pour points, while Turkey’s reconstruction surge spurs extreme-pressure uptake. EU REACH rules on PFAS and boron nitride reshape product portfolios and inflate R&D costs, but offer competitive edge to compliant suppliers.

South America is anchored by Brazil, where Petrobras pre-salt projects fuel marine grease demand. Argentina’s lithium-mining belt boosts extreme-pressure consumption in crushing and conveyor lines. The Middle East and Africa expand construction equipment and power-generation fleets under Saudi Vision 2030 and South African mining investments, respectively. FUCHS’s 40% capacity addition in South Africa evidences confidence in sub-Saharan growth.

Value Chain Analysis

The grease value chain runs from upstream feedstocks, including mineral base oils and PAO/esters, thickener precursors for lithium, calcium-sulfonate, aluminum-complex and polyurea systems, and additive packages such as EP/antiwear, corrosion inhibitors and antioxidants, through formulation, blending, and quality control, then packaging into cartridges, pails, drums, and bulk deliveries. Industry associations such as NLGI and ELGI, along with OEM and specification bodies, act as demand-shaping nodes since licensing and approvals narrow which base stocks and additive systems can be used in critical applications.

In 2026, base oil and additive availability emerged as a key operating bottleneck for grease blenders, with ILMA highlighting tightness in base oil supply and reduced formulation flexibility when specific approved base stocks are constrained. Disruptions tied to Middle East-origin Group III supply and logistics have reinforced a shift away from just-in-time replenishment, pushing firms toward longer-term contracts, higher inventory buffers, and diversified routing. Downstream, distributors, industrial service providers, and OEM-aligned workshops remain pivotal channels for reaching automotive, heavy equipment, marine, and power-generation end users.

Competitive Landscape

The Grease Market is moderately fragmented. BP commenced a sale process for Castrol in May 2025 within a broader USD 20 billion divestment program, signaling that integrated majors reassess downstream assets. Klüber Lubrication’s October 2025 merger with OKS merges food-grade and high-performance portfolios under the Freudenberg umbrella, creating a wider technical service network. Regional independents fill niche gaps in food-grade, low-temperature, and biodegradable segments. Their agility allows rapid compliance with emerging standards, while large players leverage scale and base-oil integration to defend share. Overall, competitive intensity rises as customers demand both sustainability credentials and cost certainty.

Grease Industry Leaders

Exxon Mobil Corporation

Chevron Corporation

BP p.l.c.

FUCHS

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The clearest opportunities cluster where buyers are actively requalifying chemistries to reduce dependence on lithium thickeners and to meet higher-temperature and water-resistance requirements, particularly in offshore, marine, and heavy-load applications where calcium-sulfonate complex greases are being specified as alternatives to lithium soaps. There is also product-side whitespace around compliant additive systems, as the EU REACH proposal (Annex XVII, February 2023) has already driven reformulation work away from PFAS and certain boron compounds, increasing demand for suppliers that can provide validated EP performance with substitute chemistries.

On the supply side, investments and localization moves support near-term commercialization of higher-performance grease formulations, especially synthetics and specialty grades that rely on stable additive and base-oil availability. Examples include LANXESS inaugurating a lubricant additives blending plant in Jhagadia, Gujarat (April 2026), and Luberef targeting the second half of 2026 for startup of expanded base oils capacity at Yanbu to reach 1.53 million tonnes per year, both of which tighten the link between regional additives/base-oil supply and grease blender competitiveness. North American basestock availability is also broadening, with NYCO confirming its Newnan, Georgia facility is fully operational for NYCOBASE synthetic esters (March 2026), supporting formulators serving EV-related driveline components and extended-drain industrial assets.

Recent Industry Developments

- July 2026: Chevron and ZL Chemicals announced a technology licensing agreement covering advanced chemical surfactant technology. While this is not a grease product launch, the agreement expands Chevron's technology options for performance chemistry platforms that can influence lubricant and grease formulation pathways and differentiation.

- September 2025: Kluber Lubrication acquired TriboServ GmbH & Co. KG, a specialist in automatic lubricators and customized lubrication systems. The acquisition expands Kluber's ability to bundle grease supply with automated delivery hardware and services, supporting longer relubrication intervals and tighter control of consumption in industrial fleets.

- June 2024: Shell announced plans to triple grease production capacity at its Thailand facility to 15,000 tonnes per year. The expansion increases Southeast Asia supply availability for industrial and automotive greases and helps reduce lead times for regional customers as demand grows across ASEAN manufacturing hubs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the grease market is defined as lubricating grease consumed across automotive and industrial uses, counted at the point of sale into end users, and measured in revenue for the defined geography and period.

Scope exclusions: We exclude vacuum specific greases and medical implant greases that sit outside mainstream industrial and automotive demand patterns.

Segmentation Overview

- By Thickener

- Lithium-based

- Calcium-based

- Aluminum-based

- Polyurea

- Other Thickeners

- By Product type

- Mineral Oil

- Synthetic Oil

- Bio-based Oil

- By Performance Grade

- High-Temperature Greases

- Low-Temperature & Arctic-Grade Greases

- Extreme-Pressure & Heavy-Load Greases

- By End-user Industry

- Automotive & Other Transportation

- Power Generation (Wind, Hydro, Thermal)

- Heavy Equipment

- Food & Beverage

- Metallurgy & Metalworking

- Chemical Manufacturing

- Other Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Malaysia

- Thailand

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- NORDIC Countries

- Turkey

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Nigeria

- Egypt

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the basic demand map and to avoid guessing on what drives grease consumption. We referenced public sources such as USGS and other national geology agencies for base oil and additives context, UN Comtrade and national customs portals for trade flows linked to lubricants and feedstocks, and energy and industry statistics from sources such as the IEA and World Bank.

We also reviewed product approvals and technical references from bodies such as NLGI, plus food grade guidance where relevant, and then cross-checked directional trends using company annual reports, investor presentations, and reputable press. For hard to compile items, such as corporate revenue splits or patent intensity around thickener systems, paid subscriptions for company financials and patent databases were used only as supporting inputs. The sources listed above are illustrative, and many other public datasets and documents were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary discussions were used to stress-test what we saw in public data, especially around application mix, pricing moves, and substitution between grease types when operating conditions change. We spoke with a balanced mix of manufacturers, blenders, distributors, and large end users across APAC, EMEA, and the Americas, and then re-contact was done when responses created a meaningful swing in the model assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 16% | APAC: 49% |

| Mid tier: 44% | Functional/Unit leaders: 37% | EMEA: 29% |

| Smaller Players: 22% | Managers: 47% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up logic. On the top-down side, we reconstructed demand by linking lubricant and grease consumption signals to end-use activity, then allocating the grease share by application intensity across automotive maintenance and industrial equipment. After the demand pool was formed, it was translated into market value using region-level pricing logic, followed by currency normalization.

To keep the model grounded, several grease-specific inputs were tracked (illustrative), including automotive parc and service intervals that drive relubrication volumes, industrial output and equipment utilization in sectors that are grease heavy, penetration of centralized lubrication systems, thickener preference shifts (for example, lithium versus calcium and polyurea), and base oil and additive cost movement that influences pricing. Bottom-up checks were then used selectively, such as rolling up sampled supplier revenues where disclosure exists, and validating implied liters per site through distributor and workshop channel checks. Where gaps appeared, we used conservative ranges and re-checked them in interviews.

For forecasting, scenario analysis was used because grease demand tends to move with industrial cycles and vehicle maintenance patterns, and then those scenarios were tied back to expert views on production growth, fleet trends, and expected pricing pass-through. Where a variable looked unstable, assumptions were kept simple and updated only when multiple independent signals pointed in the same direction.

Data Validation & Update Cycle

Outputs were validated by comparing the final totals against independent signals, such as trade movements, industrial production direction, and the implied per-unit consumption rates that should look reasonable for the main end uses. When a country or end-use result looked out of line, the drivers were reviewed, inputs were re-checked, and relevant experts were contacted again before sign-off.

Each report is refreshed annually, and interim updates are made when material events affect demand, supply, or pricing. Before delivery, a fresh analyst pass is completed so the numbers reflect the latest available public data and the most recent primary feedback.

Mordor Intelligence's Grease Market Size Compared With Other Published Estimates

Published grease market numbers can differ even when they sound like they measure the same thing, since the unit of measure, the year used, and what gets counted as grease are not always aligned. The spread is usually explained by scope choices, pricing treatment, and how much validation is done on the activity drivers behind demand.

The main gap comes from unit selection and conversion, where Mordor Intelligence keeps the core grease definition tight and avoids forcing a liters-based demand build into a revenue figure through broad, one-size pricing assumptions across regions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.77 B (2026) | |

| Industry Publisher A | USD 6.00 B (2024) | Reports a value-based total with its own product scope and pricing build, which can lift the number if adjacent lubricant categories or broader channel markups are included, and if currency timing is not normalized the same way. |

| Industry Publisher B | USD 6.40 B (2024) | Uses a revenue view with a longer forecast window, and differences can come from how base oil cost pass-through is modeled, how regional ASPs are applied, and whether industrial and automotive mixes are updated with fresh end-user checks. |

Taken together, the table shows that the biggest driver of variance is not growth rate math, but what is being measured and how it is converted into a single headline number. By tying assumptions back to observable demand indicators and then validating them with real market feedback, the estimate stays traceable and repeatable even when inputs need to be refreshed.

Key Questions Answered in the Report

What is the current grease market size and projected growth through 2031?

The grease market size is 2.77 billion liters in 2026 and is forecast to reach 3.28 billion liters by 2031 at a 3.45% CAGR.

Which thickener type is expected to grow the fastest?

Calcium-based greases are projected to advance at an 8.22% CAGR as users hedge against lithium-carbonate price swings.

Why are synthetic-oil greases gaining popularity?

Polyalphaolefin and ester-based products offer wider temperature ranges and longer relubrication intervals, lowering total ownership cost despite higher unit prices.

How will EU REACH rules affect grease formulations?

Restrictions on PFAS and boron nitride force formulators to adopt alternative chemistries, raising R&D spending and accelerating launches of compliant products.

Which region will contribute the most incremental volume?

Asia-Pacific, led by China, India, and ASEAN countries, is projected to add the largest incremental volume on a 4.39% CAGR to 2031.

Page last updated on: