Coated Recycled Board Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

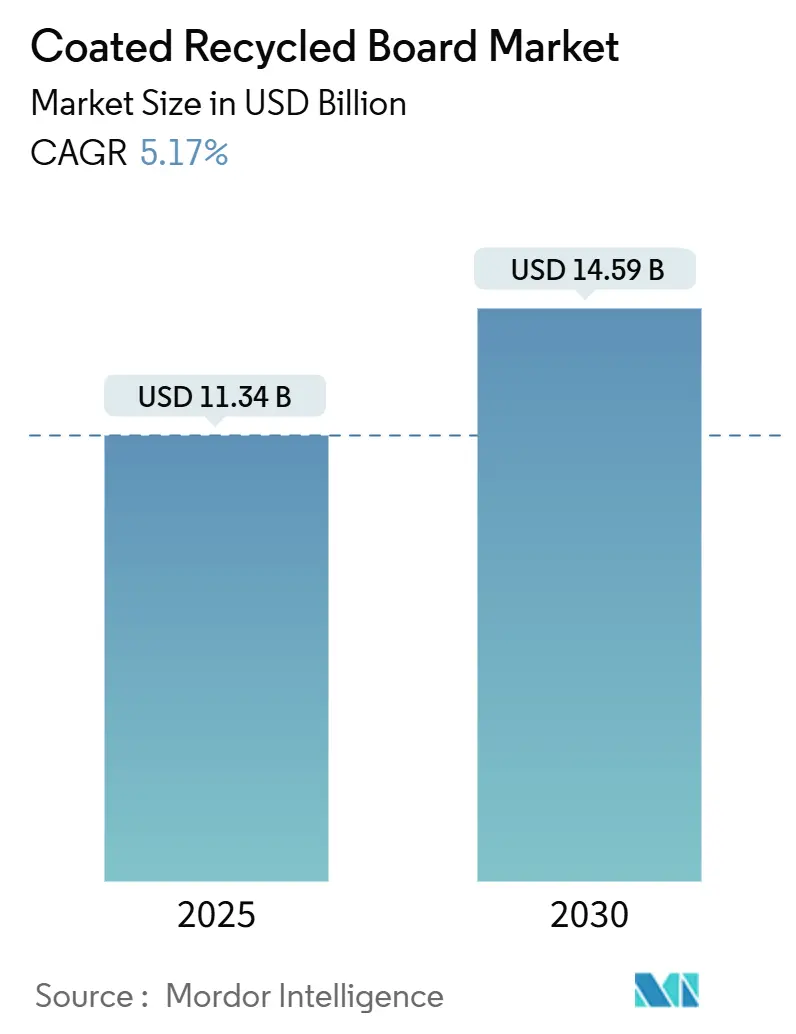

| Market Size (2025) | USD 11.34 Billion |

| Market Size (2030) | USD 14.59 Billion |

| Growth Rate (2025 - 2030) | 5.17% CAGR |

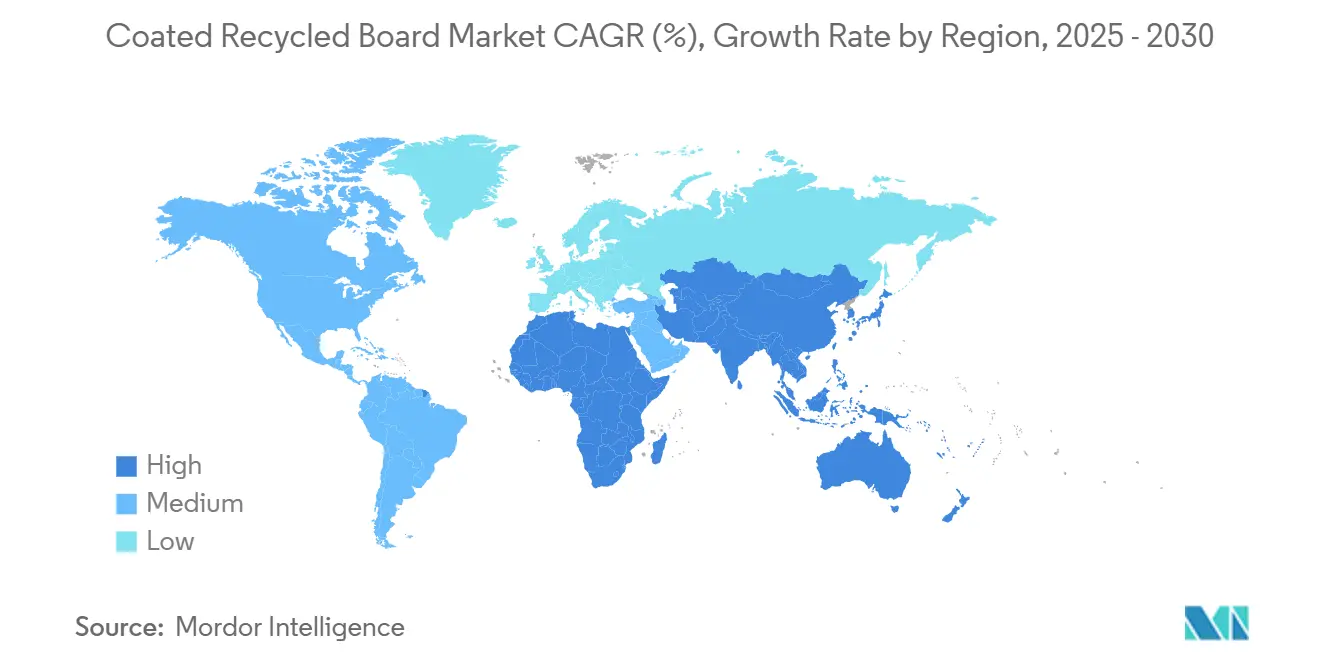

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coated Recycled Board Market Analysis by Mordor Intelligence

The coated recycled board market reached USD 11.34 billion in 2025 and is forecast to attain USD 14.59 billion by 2030, advancing at a 5.17% CAGR. This trajectory stems from regulatory pressure for 70% recyclability under the EU’s PPWR, surging e-commerce volumes, and cost advantages over virgin pulp. Robust capacity additions across Asia-Pacific, strategic machine conversions from idle newsprint, and adoption of barrier coatings that mitigate MOSH/MOAH migration further underpin demand. Meanwhile, recovered-paper price volatility and performance gaps versus premium virgin boards moderate near-term margins, yet long-term opportunities persist as sustainability mandates accelerate material substitution toward circular models.[1]New Zealand Ministry of Foreign Affairs and Trade, “New EU rules on packaging and waste will transform its Supply Chain,” mfat.govt.nz

Key Report Takeaways

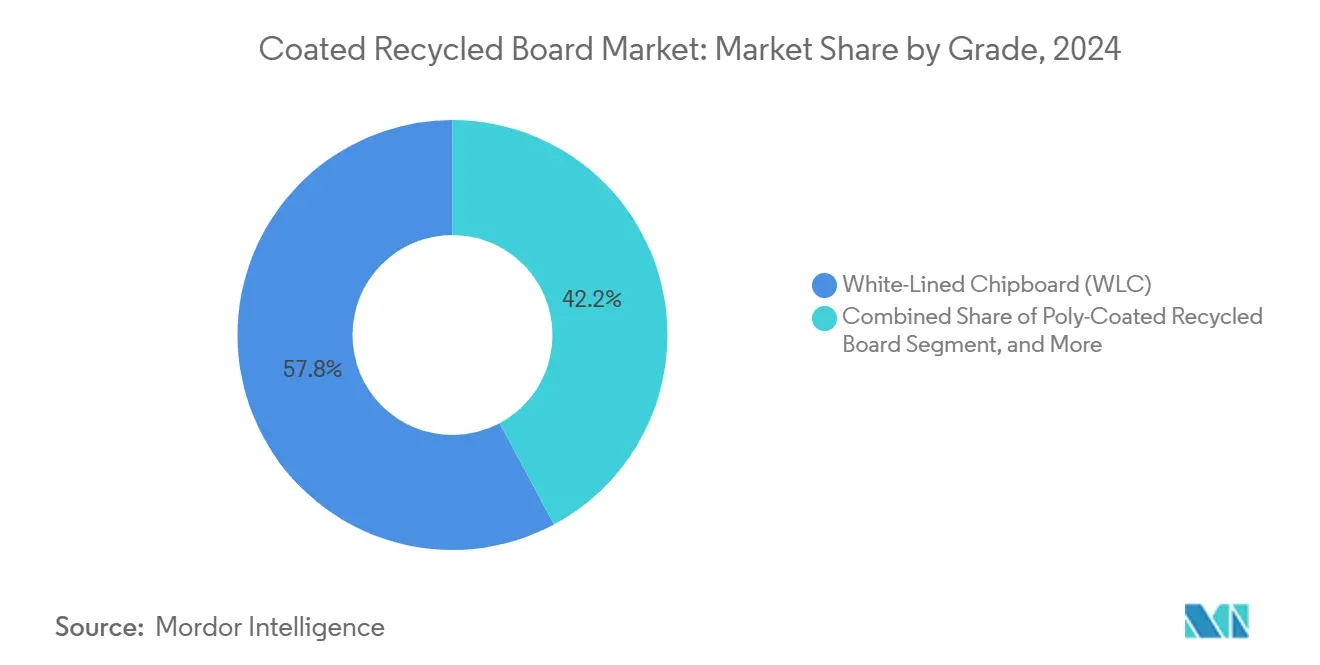

- By grade, white-lined chipboard captured 57.82% of the coated recycled board market share in 2024.

- By end-use, the coated recycled board market size for the personal care and cosmetics segment is projected to grow at a 6.64% CAGR between 2025-2030.

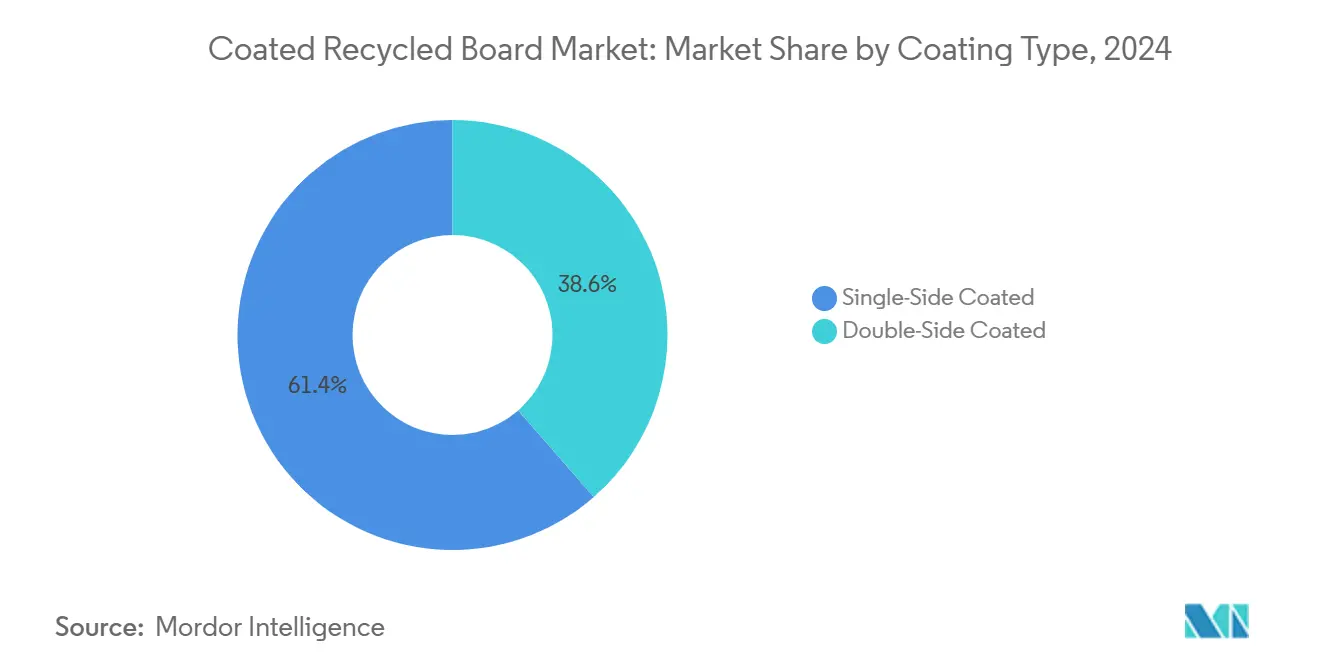

- By coating type, single-sided coated captured 61.41% of the coated recycled board market share in 2024.

- By basis weight, the coated recycled board market size for the sub-200 gsm boards segment is projected to grow at a 6.01% CAGR between 2025-2030.

- By geography, the Asia-Pacific captured 54.06% of the coated recycled board market share in 2024.

Global Coated Recycled Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability-led demand in food and beverage packaging | +1.2% | Global, EU and North America leading | Medium term (2-4 years) |

| Rising virgin-pulp prices boosting recycled fiber economics | +0.8% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| E-commerce growth driving lightweight folding cartons | +0.7% | Global, APAC and North America core | Medium term (2-4 years) |

| Plastics bans on detergent packs shifting to CRB | +0.4% | EU and North America, expanding to APAC | Long term (≥ 4 years) |

| High-graphic digital water-based inks enabling CRB | +0.3% | Global, developed markets | Medium term (2-4 years) |

| Conversion of idle newsprint machines to CRB | +0.2% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sustainability-led demand in food and beverage packaging

Global packaging directives that require 70% recyclability and restrict PFAS are propelling brand owners toward fiber-based substrates. Advanced coatings now curb MOSH/MOAH migration, enabling coated recycled board to meet food-contact norms.[2]Packaging Law, “The New EU Packaging and Packaging Waste Regulation – Highlights and Challenges Ahead,” packaginglaw.com Pro Carton reports a 91% recycling rate for cartons, providing a carbon footprint edge versus alternatives. Graphic Packaging eliminated 450 million plastic packs in 2023, signalling momentum among large converters. Premium food brands leverage the substrate’s sustainable image to justify price premiums, counteracting historical performance limitations.

Rising virgin-pulp prices boosting recycled fiber economics

Elevated virgin-pulp costs make recycled fiber financially attractive. WestRock consumes 4.7 million tons of recovered fiber annually, insulating its cost base. Thirty North American mills plan expansions that could absorb an extra 5 million tons of old corrugated containers, reflecting confidence in feedstock supply. Mayr-Melnhof sources 54% of its fiber from recycled streams, stabilizing margins. Reduced energy use in recycled processing and maturing collection networks widen the arbitrage.

E-commerce growth driving lightweight folding cartons

Rapid parcel volumes require packaging that balances durability with dimensional-weight limits. Cascades’ Bear Island mill adds 465,000 short tons of lightweight recycled containerboard aimed at e-commerce applications. International Paper processes over 7 million tons of recovered paper to meet this channel’s needs. Superior printability supports branding and “unboxing” experiences prized by online retailers.

Plastics bans on detergent packs shifting to CRB

Single-use plastics legislation in the EU is pushing household and laundry care brands toward fiber alternatives. ITC’s ‘Filo’ line targets this shift with moisture-resistant board replacing plastic pouches. The bans create mid-term demand as companies redesign packaging to comply.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Brightness and stiffness limits versus premium boards | -0.6% | Global, premium segments | Long term (≥ 4 years) |

| Volatile recovered-paper collection rates | -0.4% | Global, regional variations | Short term (≤ 2 years) |

| EU MOSH/MOAH migration limits on recycled board | -0.3% | EU, expanding globally | Medium term (2-4 years) |

| Rise of molded-fiber trays cannibalizing low-caliper CRB | -0.2% | Global, food service focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Brightness and stiffness limits versus premium boards

Recycled content boards trail virgin alternatives by 5-10 ISO points in brightness and 10-15% in stiffness, restricting adoption in luxury goods. Metsä Board confirmed premium-segment customers still prefer fresh fiber for appearance-critical packs. Stora Enso is investing EUR 1 billion (USD 1.08 billion) to raise recycled board performance, yet a gap remains until next-generation coatings emerge.

Volatile recovered-paper collection rates

Fluctuating feedstock supply inflates cost risk. The U.S. PPI for recycled paperboard hit 412.949 in March 2025, underscoring volatility. Prinzhorn manages 2.7 million tonnes of recycled input yet still faces quality swings that hamper efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade - White-Lined Chipboard retains scale while Poly-Coated accelerates

White-Lined Chipboard accounted for 57.82% of the coated recycled board market size in 2024 because its balance of cost and print quality fits mass-market packaging needs. Poly-Coated Recycled Board is the fastest-growing variant, advancing at 5.94% CAGR as barrier enhancements open moisture-sensitive food applications. Clay-Coated News Back and niche specialty grades serve industrial and automotive demand pockets. Graphic Packaging’s USD 1 billion Waco mill underlines confidence in grade diversification strategies.[3]Graphic Packaging Holding Company, “Form 10-K 2023,” graphicpkg.com

Enhanced coatings narrow historical performance gaps. Producers integrate in-house lamination to capture margins, reflecting a wider shift within the coated recycled board industry toward value-added products. In Asia-Pacific, stringent print standards push suppliers to refine coating uniformity, strengthening long-term prospects for Poly-Coated grades.

By End-use Industry - Food and beverage leads; personal care surges

Food and beverage packaging held 36.04% of the coated recycled board market share in 2024, benefiting from strict recyclability targets and consumers seeking fiber-based alternatives to plastic. Personal care and cosmetics are projected at a 6.64% CAGR as luxury brands adopt eco-labels to justify premium pricing. Household and laundry care gains from plastic-ban spillovers, while healthcare adoption remains cautious due to regulatory sterility demands.

ITC’s launch of molded-fiber and recycled board solutions exemplifies fast-moving consumer goods pivoting toward sustainable substrates. As brand owners elevate sustainability rankings, coated recycled board market penetration into secondary electronics packaging is rising, particularly in the Asia-Pacific region, where e-commerce growth aligns with green mandates.

By Coating Type - Single-side dominates; double-side gains premium traction

Single-sided coated products represented 61.41% of global volumes in 2024 due to cost advantages, where only the print surface needs barrier properties. Double-sided coated variants are set to rise at a 5.63% CAGR, aimed at cosmetics, electronics, and gift boxes demanding high-definition graphics on both faces. Stora Enso’s Oulu upgrade boosts double-coated capacity, highlighting this shift.

Digital aqueous inks enhance print fidelity, making recycled boards viable for luxury segments. As converters chase higher margins, in-line coating stations become standard, reinforcing vertical integration across the coated recycled board market.

By Basis Weight - Mid-range leads; lightweight fuels e-commerce

Boards in the 201-300 gsm bracket captured 38.93% of the coated recycled board market size in 2024, balancing stiffness and cost across diverse segments. Sub-200 gsm offerings, expanding at 6.01% CAGR, cater to lightweight e-commerce cartons that trim freight charges. Cascades’ Bear Island line is optimized for this window, reflecting demand for weight-efficient formats.

While heavier grades remain essential for industrial packaging, material-reduction targets are steering brands toward slimmer boards. Advances in fiber treatment sustain compression strength even at lower grammage, widening the addressable scope within the coated recycled board industry.

Geography Analysis

Asia-Pacific controlled 54.06% of global revenue in 2024 and is forecast to grow at 7.13% CAGR through 2030. Nippon Paper aims for JPY 650 billion (USD 4.3 billion) in packaging sales by FY2030, reinforcing regional momentum. China’s Shandong Sun Paper generated CNY 20.524 billion (USD 2.85 billion) in H1 2024, underscoring its scale. In India, ITC’s Paperboards, Paper and Packaging arm delivered INR 2,072.85 crores (USD 249.7 million) in FY2024 revenue, and commissioned a molded-fiber plant to diversify offerings.

North America features mature recycling systems and sizable incumbents. International Paper processes 7 million tons of recovered paper annually, while the Smurfit WestRock merger creates a USD 34 billion heavyweight pursuing USD 400 million in annual synergies. Graphic Packaging’s USD 1 billion Waco facility will lift regional supply and introduce next-generation coating capability.

Europe’s regulatory stringency under the PPWR accelerates fiber adoption. Stora Enso’s EUR 1 billion (USD 1.08 billion) upgrade at Oulu, Billerud’s SEK 11,101 million (USD 12,600 million) Q1 2025 sales, and Mayr-Melnhof’s 52% recycled-fiber cartonboard share showcase a deeply embedded circular economy. Latin America and MEA remain nascent yet attractive as sustainability policies crystallize and urbanization boosts packaged goods demand.

Competitive Landscape

The coated recycled board market is moderately consolidated. The top five companies command nearly 55% of capacity, leveraging scale in recovered fiber procurement and advanced coating technologies. The transformational Smurfit Kappa-WestRock merger underscores a quest for operational synergies, procurement leverage, and geographic breadth. Graphic Packaging’s simultaneous investments and rationalizations reveal a focus on network efficiency.

Technology is a crucible for advantage. Stora Enso’s high-graphic lines, Norske Skog’s newsprint conversions, and Koehler’s specialty coating pilots illustrate how incumbents repurpose assets to chase growth niches. Barrier enhancement, MOSH/MOAH mitigation, and digital print receptivity are central innovation axes.

Supply-chain security drives vertical integration. Mills acquire collection networks or partner with material recovery facilities to tame feedstock volatility. Producers that assure traceable, low-contamination recovered fiber strengthen resilience and brand credibility in regulated sectors such as food and personal care.

Coated Recycled Board Industry Leaders

Graphic Packaging International, LLC

Smurfit WestRock PLC

Greif, Inc.

Mayr-Melnhof Karton AG

Nine Dragons Paper (Holdings) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Norske Skog updated on its EUR 320 million (USD 346 million) Golbey conversion to 550,000 tonnes recycled containerboard capacity.

- February 2025: The EU adopted Regulation (EU) 2025/40 mandating 70% recyclability by 2030 and curbing PFAS in food-contact packs.

- February 2025: Smurfit WestRock confirmed USD 7.5 billion Q4 2024 sales and outlined USD 400 million synergy capture.

- January 2025: Stora Enso reported EUR 2,362 million (USD 2,556 million) Q1 2025 sales and advanced its Oulu consumer packaging board ramp-up.

Global Coated Recycled Board Market Report Scope

| White-Lined Chipboard (WLC) |

| Clay-Coated News Back (CCNB) |

| Poly-Coated Recycled Board |

| Other Grades |

| Food and Beverage |

| Household and Laundry Care |

| Personal Care and Cosmetics |

| Healthcare and Pharma |

| Consumer Electronics |

| Industrial and Automotive |

| Other End-use Industries |

| Single-Side Coated |

| Double-Side Coated |

| Less than 200 gsm |

| 201-300 gsm |

| 301-400 gsm |

| More than 400 gsm |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Grade | White-Lined Chipboard (WLC) | ||

| Clay-Coated News Back (CCNB) | |||

| Poly-Coated Recycled Board | |||

| Other Grades | |||

| By End-use Industry | Food and Beverage | ||

| Household and Laundry Care | |||

| Personal Care and Cosmetics | |||

| Healthcare and Pharma | |||

| Consumer Electronics | |||

| Industrial and Automotive | |||

| Other End-use Industries | |||

| By Coating Type | Single-Side Coated | ||

| Double-Side Coated | |||

| By Basis Weight | Less than 200 gsm | ||

| 201-300 gsm | |||

| 301-400 gsm | |||

| More than 400 gsm | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the coated recycled board market in 2025?

It stands at USD 11.34 billion and is set to expand to USD 14.59 billion by 2030.

What is the forecast CAGR for coated recycled board through 2030?

The market is projected to post a 5.17% CAGR during 2025-2030.

Which region leads demand for coated recycled board?

Asia-Pacific holds 54.06% revenue share and is the fastest-growing at 7.13% CAGR.

Which end-use segment is growing fastest?

Personal care and cosmetics packaging is advancing at 6.64% CAGR due to premium sustainable branding.

What impact do EU regulations have on packaging materials?

The PPWR mandates 70% recyclability by 2030 and limits PFAS, accelerating adoption of fiber-based substrates.

Page last updated on: