Biodegradable Polymer Coated Urea Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

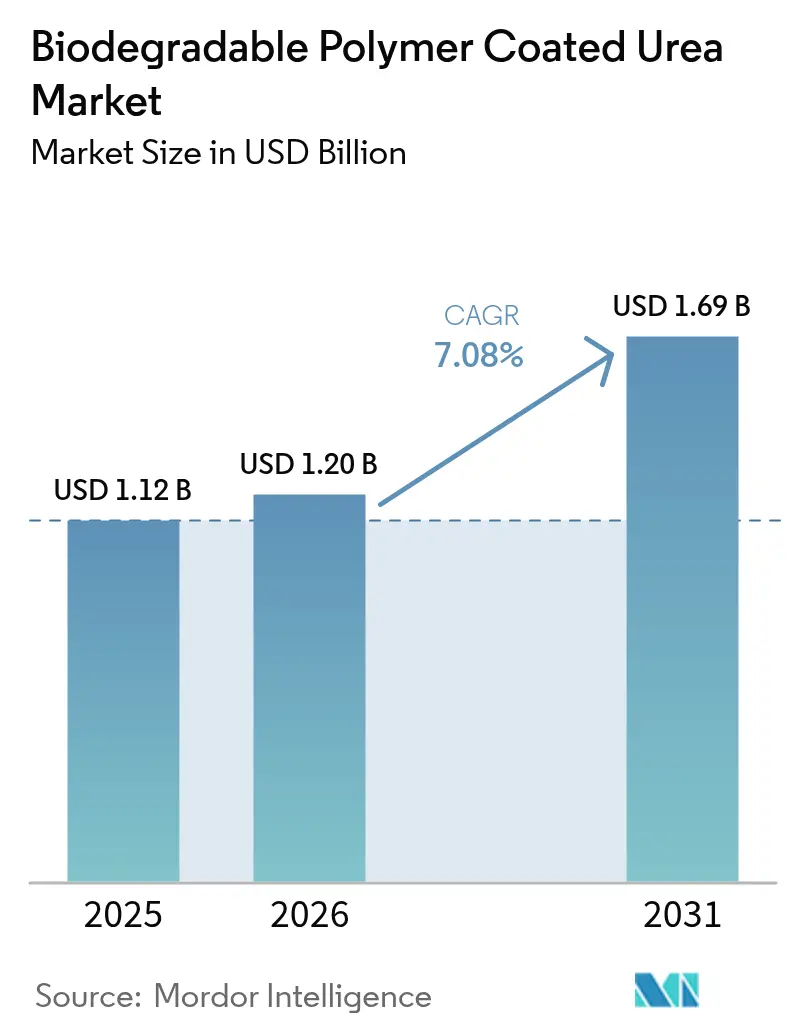

| Market Size (2026) | USD 1.2 Billion |

| Market Size (2031) | USD 1.69 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biodegradable Polymer Coated Urea Market Analysis by Mordor Intelligence

The biodegradable polymer coated urea market size was valued at USD 1.12 billion in 2025 and estimated to grow from USD 1.2 billion in 2026 to reach USD 1.69 billion by 2031, at a CAGR of 7.08% during the forecast period (2026-2031). Current expansion builds on rising regulatory pressure to improve nitrogen-use efficiency, widening price spreads between conventional and controlled-release products, and a pivot toward premium specialty crops across Asia-Pacific. Policymakers in the European Union, China, and India are tightening nutrient-loss thresholds, which raises compliance costs for granular urea but directly benefits coated grades. Parallel advances in bio-polymer micro-encapsulation have lowered nutrient-release variability, addressing the chief agronomic concern that historically limited adoption. At the same time, verified carbon credits linked to slow-release fertilizers now trade between USD 15 and USD 25 per metric ton CO₂ equivalent, adding a fresh incentive layer for early movers. These converging forces position the biodegradable polymer coated urea market for durable, policy-anchored growth over the forecast horizon.

Key Report Takeaways

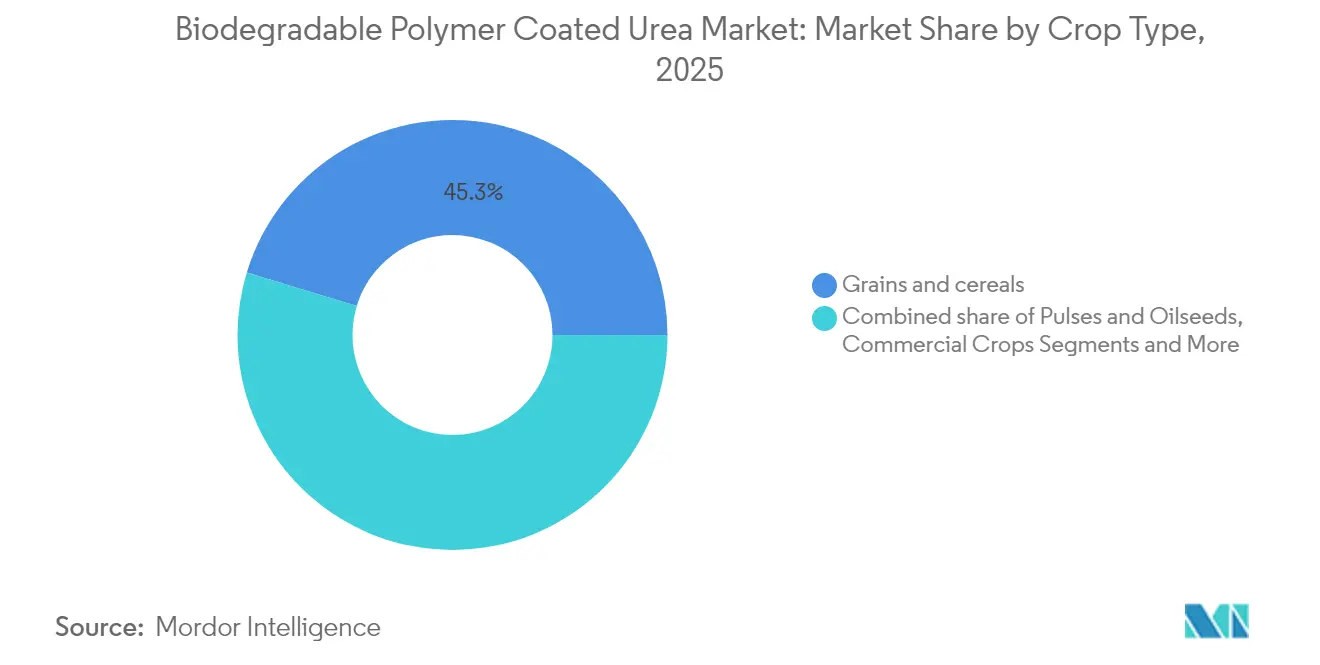

- By crop type, grains and cereals accounted for 45.30% of the biodegradable polymer coated urea market size in 2025, while fruits and vegetables are forecast to expand at a 10.22% CAGR through 2031.

- By polymer type, polylactic acid secured 32.60% of the biodegradable polymer coated urea market share in 2025, whereas polycaprolactone is advancing at an 10.98% CAGR to 2031.

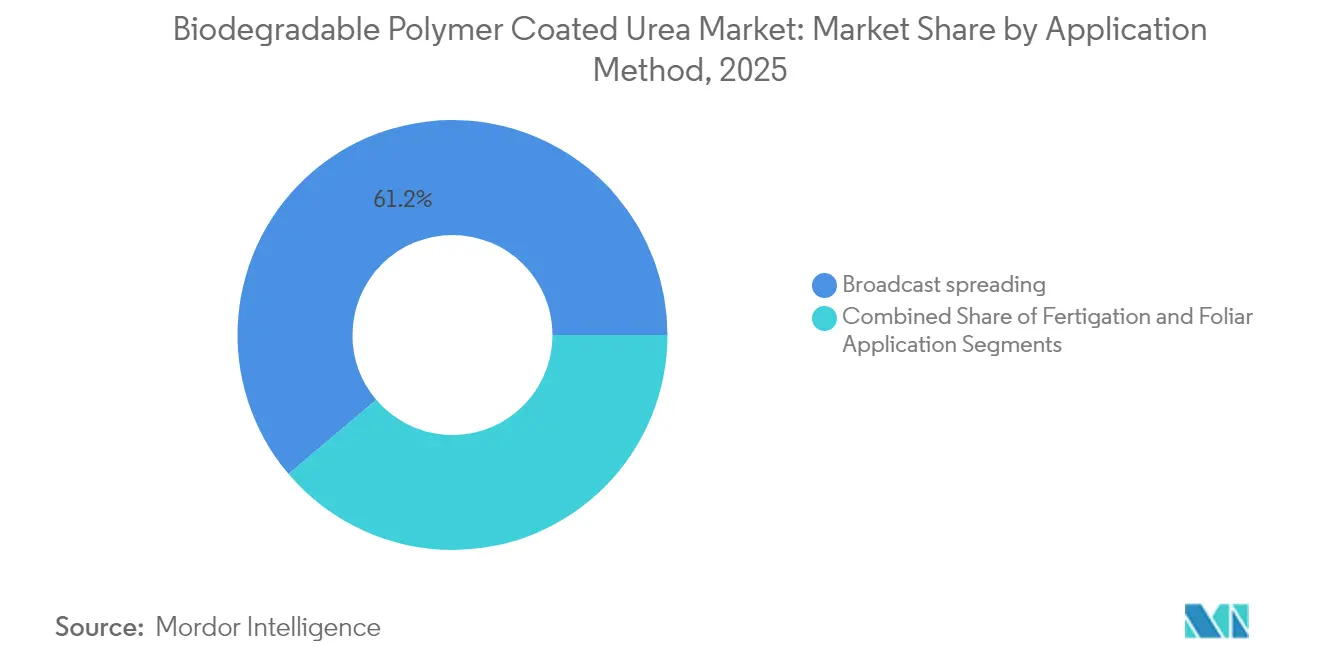

- By application method, broadcast spreading held 61.20% share of the biodegradable polymer coated urea market in 2025, and fertigation is projected to grow at a 12.18% CAGR through 2031.

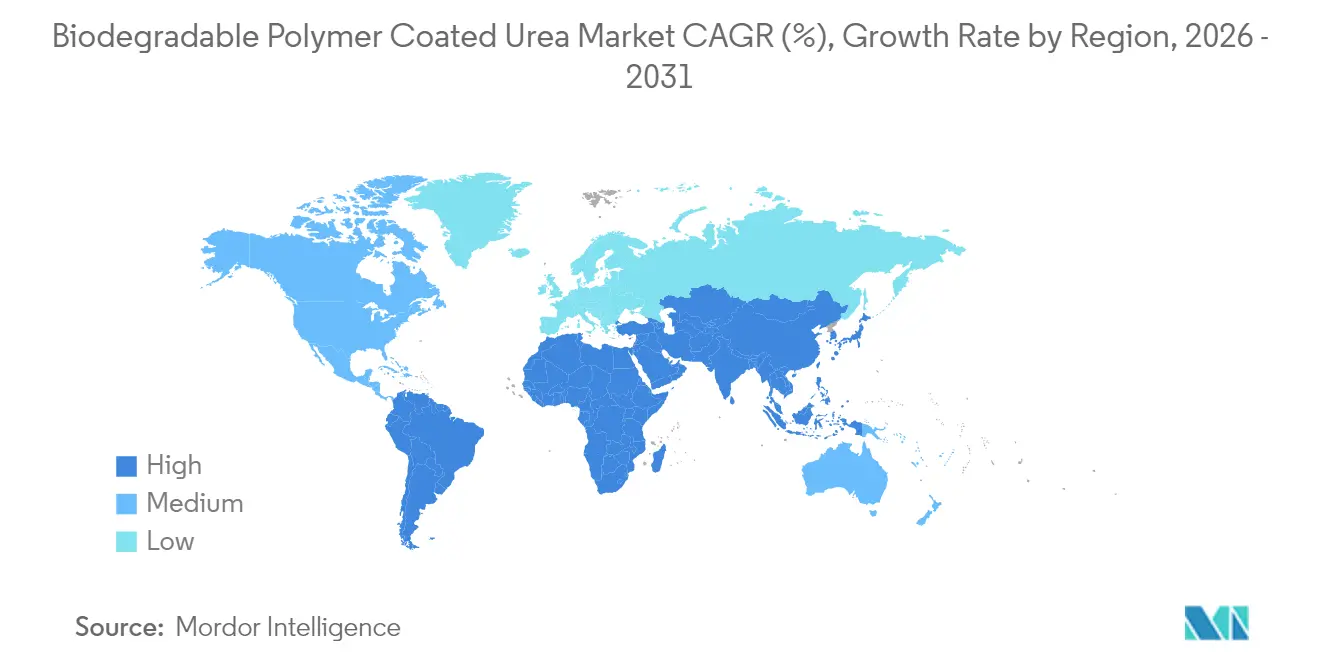

- By geography, Asia-Pacific led with 37.50% revenue share of the biodegradable polymer coated urea market in 2025; the Middle East is the fastest-growing region at a 9.56% CAGR to 2031.

- The top five producers together controlled a significant share of the biodegradable polymer coated urea market in 2024, signaling moderate consolidation and persistent white-space potential in emerging markets.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biodegradable Polymer Coated Urea Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push for nitrogen-use-efficiency fertilizers | +1.8% | Global, strongest in the EU and North America | Medium term (2-4 years) |

| Surge in specialty crop acreage in the Asia-Pacific | +1.5% | Asia-Pacific core, spillover to the Middle East | Long term (≥ 4 years) |

| Farmer incentives under 4R nutrient stewardship programs | +1.2% | North America and Europe | Short term (≤ 2 years) |

| Breakthroughs in bio-polymer micro-encapsulation | +0.9% | Global, led by developed markets | Medium term (2-4 years) |

| Carbon-credit monetization for slow-release fertilizers | +0.8% | North America, EU, Australia | Long term (≥ 4 years) |

| Corporate net-zero procurement of low-N₂O fertilizers | +0.6% | Global supply chains, OECD focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Nitrogen-Use-Efficiency Fertilizers

Amendments to the European Union Nitrates Directive in 2024 capped on-farm nitrogen application at 170 kg per hectare, compelling growers to adopt controlled-release inputs that curb volatilization[1]Source: European Commission, “Nitrates Directive Implementation,” ec.europa.eu. Germany followed by pledging a 29% ammonia-emission cut by 2030, creating a direct pull for slow-release formulations that demonstrate lower atmospheric losses. China mirrored this stance by requiring large farming enterprises to certify nitrogen-use efficiency, anchoring demand in a market responsible for nearly one-third of global urea consumption. These synchronized mandates elevate the biodegradable polymer coated urea market as a compliance tool rather than an optional premium input. Consequently, distributors now bundle regulatory advisory services with coated urea contracts, signaling that policy enforcement will remain a durable demand driver over the medium term.

Surge in Specialty Crop Acreage in Asia-Pacific

Asia-Pacific fruit and vegetable exports rose sharply in 2024, with Vietnam alone posting USD 6.8 billion in shipments, a 22% year-on-year gain. Specialty growers in Thailand, Vietnam, and the Philippines command price premiums that offset the cost differential between coated and conventional urea. Because export destinations enforce strict residue limits, producers use controlled-release inputs to minimize late-season nitrate spikes. This calculus anchors the biodegradable polymer coated urea market in high-value crops, even as field-crop penetration remains limited. Over time, secondary spillovers into floriculture and protected cultivation are likely, given aligned quality and environmental requirements.

Farmer Incentives Under 4R Nutrient Stewardship Programs

The United States Department of Agriculture allocated USD 2.1 billion in 2024 through its Environmental Quality Incentives Program, covering up to 75% of coated-urea costs on participating farms[2]Source: USDA Natural Resources Conservation Service, “Environmental Quality Incentives Program,” usda.gov. Similar schemes in Canada offer CAD 25,000 (USD 18,500) per farm, reducing financial barriers during initial adoption phases. Because these subsidies are tied to verifiable nutrient-use benchmarks, they create behavioral lock-in that often persists after payments lapse. The resulting market pull shortens payback periods for coating plants, accelerating capacity expansions and new-product rollouts. Evidence from early program cohorts shows a 23% rise in coated-urea repeat purchases after the second growing season, underscoring subsidy effectiveness in seeding lasting demand.

Breakthroughs in Bio-Polymer Micro-Encapsulation

Recent polymer science advances lowered nutrient-release variability to below 10%, overcoming a long-standing agronomic obstacle. Dual-layer polycaprolactone (PCL) coatings now embed an immediate-release outer shell and a 90-day controlled-release core, effectively condensing multi-pass fertilizer schedules into a single application. Polylactic acid (PLA) variants have added temperature-responsive additives that synchronize degradation with crop growth stages, minimizing nutrient wastage. These innovations have slashed labor costs tied to multiple field passes and improved yield predictability, reinforcing the value proposition for growers who face rising wage pressures. As patents proliferate, coating suppliers differentiate on release-curve precision rather than simply on biodegradability claims.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price premiums over conventional urea | -2.1% | Global, most acute in developing markets | Short term (≤ 2 years) |

| Regulatory ambiguity around biodegradable claims | -1.3% | Global, varying by jurisdiction | Medium term (2-4 years) |

| Enzyme-coated urea as a low-cost substitute | -0.8% | North America and Europe | Medium term (2-4 years) |

| Supply-chain dependency on bio-polymer feedstocks | -0.6% | Global, concentrated in polymer producers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Price Premiums Over Conventional Urea

Conventional granular urea averaged USD 425 per metric ton in 2024, whereas bio-degradable polymer coated grades traded between USD 1,200 and USD 1,400, reflecting higher manufacturing and polymer feedstock costs. For low-margin field crops, yield gains of 10-15% rarely outweigh such premiums, confining adoption mainly to high-value horticulture or subsidy-backed acreage. Although carbon-credit revenue and labor savings partially offset the gap, sticker-shock remains a formidable hurdle, particularly in markets with limited credit access. Suppliers have responded by launching smaller pack sizes and seasonal discount programs, but these measures only marginally ease cost concerns.

Regulatory Ambiguity Around Biodegradable Claims

The European Union requires 90% degradation within 180 days in defined soil conditions, whereas United States protocols allow longer timelines and varied substrates. This inconsistency complicates cross-border trade and forces manufacturers to run multiple certification tracks, inflating compliance costs. Farmers, uncertain about labeled environmental benefits, sometimes postpone switching until local guidelines clarify acceptable degradation metrics. The ambiguity also exposes suppliers to reputational risk if claims fail third-party verification, prompting more cautious product rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Specialty Crops Drive Premium Adoption

Grains and cereals held a 45.30% share of the biodegradable polymer coated urea market size in 2025, a function of sheer acreage despite cost headwinds. Within this broad segment, adoption concentrates in high-nitrogen cereals like rice and corn, where controlled release delivers measurable yield bumps. Conversely, fruits and vegetables expand at a 10.22% CAGR to 2031 as growers aim for residue compliance in export markets and exploit the value uplift stemming from higher produce grades. Premium crops such as durian, dragon fruit, and table grapes achieve revenue densities above USD 15,000 per hectare, enabling rapid payback on coated-urea investments. Pulses and oilseeds show moderate uptake because biological nitrogen fixation partially offsets synthetic input needs, though growers in rotation systems appreciate the benefit of synchronizing nutrient availability with peak legume demand. Turf and ornamentals, though niche, remain a steady market due to urban landscaping mandates that cap nutrient run-off in municipal areas.

The fruits and vegetables cohort illustrates why the biodegradable polymer coated urea market resonates with specialty agriculture. Precision nutrient timing reduces physiological disorders and cosmetic blemishes, enhancing pack-out rates and export acceptance. Growers integrate coated urea within fertigation programs to align nitrogen supply with critical growth phases, halving application trips and lowering labor costs. For grains, adoption hinges on policy incentives and carbon-credit stacking rather than yield economics alone, underscoring variable penetration across crop types.

By Polymer Type: PLA Dominance Faces PCL Innovation

Polylactic acid retained 32.60% of the biodegradable polymer coated urea market share in 2025 due to a mature upstream corn-starch supply chain and wide regulatory acceptance. Its compostability credentials align with organic certification schemes, cementing its status in premium horticulture. However, performance in colder climates suffers as low soil temperatures slow degradation, occasionally delaying nutrient release. Polycaprolactone addresses this limitation by offering more predictable release curves across temperature ranges, underpinning its 10.98% CAGR through 2031. PCL’s dual-layer architectures combine immediate nutrient availability with 90-day slow-release tails, mirroring split-application benefits in a single pass.

Starch-based polymers carve a budget-friendly niche but trade off precision for affordability, finding utility in row crops within subsidy programs. Polyhydroxyalkanoates and protein-based coatings remain at pilot scale, constrained by high production costs and limited regulatory clarity. Ultimately, polymer choice is becoming crop- and climate-specific; suppliers now provide modular coating platforms that tailor degradation kinetics to local agronomic requirements, signaling a shift from one-size-fits-all to portfolio selling.

By Application Method: Infrastructure Constraints Limit Precision

Broadcast spreading dominated 61.20% of the biodegradable polymer coated urea market size in 2025 because it leverages existing farm machinery and demands minimal farmer training. While this method offers operational simplicity, it reduces the agronomic upside of slow-release coatings by failing to localize nutrients near the root zone. Fertigation, growing at 12.18% CAGR, maximizes payback by delivering nutrients through drip or sprinkler systems directly into the rhizosphere, achieving up to 90% nutrient-use efficiency. Its penetration, however, is gated by the high capital cost of irrigation infrastructure, particularly in developing regions where credit constraints remain acute.

Foliar application represents the smallest segment but is prized in stress-management protocols, enabling rapid uptake when environmental shocks threaten yield formation. Equipment manufacturers now integrate coated-urea compatibility into variable-rate applicators and digital-decision platforms, enabling data-guided timing that further enhances input efficiencies. As precision agriculture matures, the biodegradable polymer coated urea market stands to scale beyond broadcast norms into more sophisticated delivery methods, raising average revenue per unit.

Geography Analysis

Asia-Pacific sustained a 37.50% revenue share of the biodegradable polymer coated urea market in 2025, bolstered by government modernization programs that subsidize controlled-release inputs and tie them to irrigation upgrades. China’s provincial eco-agriculture zones reimburse up to 50% of coated-urea costs, embedding nitrogen-use efficiency into performance metrics for local extension officers. India’s Pradhan Mantri Krishi Sinchayee Yojana links drip-irrigation grants with nutrient-delivery targets, galvanizing fertigation-based adoption. High specialty-crop density across Vietnam, Thailand, and the Philippines reinforces regional demand by aligning revenue potential with premium input costs.

The Middle East is the fastest-growing regional cluster, poised for a 9.56% CAGR through 2031, underpinned by food-security strategies and acute water scarcity. Saudi Arabia earmarked USD 8 billion for sustainable farming technologies under Vision 2030, prioritizing efficient fertilizers that curtail water evaporation losses. The United Arab Emirates advances vertical-farming complexes that specify controlled-release urea for closed-loop hydroponic systems where nutrient precision determines overall system economics. While limited arable land caps absolute volume, the high per-hectare spend elevates regional value contribution to the global biodegradable polymer coated urea market.

North America and Europe remain mature but steady adopters, advancing at 6.05% and 5.28% CAGRs, respectively. Both regions rely on environmental compliance and carbon-market integration to justify input premiums. USDA cost-share programs, coupled with calcium ammonium nitrate restrictions in nitrate-vulnerable zones across the European Union, sustain baseline demand. Africa, with an 8.73% CAGR, showcases donor-funded pilots that blend fertilizer access with soil-health restoration, though logistics gaps and limited farmer education continue to dampen scalability. Collectively, geographic diversification shields the biodegradable polymer coated urea market from regional policy reversals and price shocks.

Regulatory Landscape

Regulation is tightening around both nitrogen-loss performance and the environmental persistence of fertilizer coatings, bringing biodegradable polymer coated urea into mainstream compliance discussions. In the European Union, the Fertilising Products Regulation (EU) 2019/1009 is tied to the bloc's microplastics restrictions and sets biodegradability conditions for polymers used in fertilising products, with requirements applying from 17 October 2028. The European Commission also adopted Delegated Regulation (EU) 2024/2790 on 23 July 2024, amending Annex II of Regulation (EU) 2019/1009 to recognize degradable polymers meeting Appendix 15 of REACH Annex XVII, pushing suppliers toward formal certification of coating biodegradation in defined soil conditions.

Outside Europe, policy tools combine product registration controls with growing scrutiny of coating fate in soils. In China, the Ministry of Agriculture and Rural Affairs (MARA) tightened field-trial standards for new fertilizer registration applications effective 1 January 2026, raising the evidence burden for controlled-release products seeking approvals. In the United States, US EPA research released in April 2026 highlighted that polymer-coated fertilizers can show slow biodegradation under field conditions, reinforcing the risk that biodegradability claims and microplastic accumulation become a more explicit compliance checkpoint. This raises the strategic value of coatings that can document degradation performance across protocols and geographies.

Competitive Landscape

The top five suppliers controlled the majority market share of global revenue in 2024, characterizing the biodegradable polymer coated urea market as moderately concentrated. Global fertilizer majors leverage integrated ammonia production, polymer manufacturing, and distribution networks to extract scale efficiencies. Regional specialists counter with crop-specific formulations and fast innovation cycles, targeting niche segments like high-latitude cereals or tropical horticulture. Patent filings for biodegradable polymer coatings expanded 34% in 2024, signaling aggressive intellectual-property positioning around release kinetics and temperature-responsive additives.

Strategic investment patterns point to vertical integration and regional acquisitions. Nutrien’s USD 150 million expansion in Saskatchewan adds advanced coating lines that raise North American capacity by 40% while shifting the cost curve downward. ICL’s takeover of a Brazilian specialty-fertilizer unit embeds local manufacturing and sidesteps import duties, enhancing competitiveness in South American fruit markets. Meanwhile, Yara’s joint venture with Kingfa Sci. and Tech. Targets cost-competitive starch-based coatings, a direct bid for mass-market grain applications in Asia. Technology alliances are also proliferating; Pursell Agritech partners with marine-biopolymer researchers to pioneer coastal-crop solutions, underscoring the value of diversified polymer feedstocks.

Competitive risks center on enzyme-coated substitutes and feedstock volatility. Mosaic’s EPA-approved MicroEssentials Bio line integrates enzymes within biodegradable matrices, blurring the line between the two technologies and potentially eroding price premiums. Supply disruptions in corn or caprolactone markets can compress margins, prompting suppliers to secure multi-year offtake contracts or invest in captive polymer capacity. Overall, defensive moves against substitute encroachment and proactive hedging against raw-material shocks will shape leadership stability in the biodegradable polymer coated urea market over the next five years.

Biodegradable Polymer Coated Urea Industry Leaders

Nutrien Ltd

Koch Agronomic Services LLC

ICL Specialty Fertilizers Ltd

J. R. Simplot Company

Haifa Chemicals Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity is reformulating coated urea portfolios to meet the EU's October 2028 polymer biodegradability requirements under the Fertilising Products Regulation, while aligning performance claims with measurable nitrogen-use-efficiency outcomes. Suppliers that can document coating degradation and nutrient-release curves across soil and climate conditions can simplify cross-border commercialization where biodegradability protocols differ. ICL's move to establish a dedicated production line at its Heerlen facility in the Netherlands for its eqo.x biodegradable coating technology highlights how established controlled-release fertilizer infrastructure is being adapted for certified biodegradable coatings rather than built from scratch.

Technology whitespace is also forming around new resin systems and IP that balance durability in handling with verified end-of-life biodegradation in soil. In South Korea, the Rural Development Administration disclosed in February 2026 that it developed biodegradable resin-coated slow-dissolving fertilizer technology, supported by field trials on rice paddies that reported large reductions in fertilizer usage and methane emissions, showing how performance and sustainability claims can be packaged together for adoption programs. Alongside this, manufacturers are filing patents and publishing validations around alternative biodegradable polymers, including Nousbo Co., Ltd. registering a second patent in June 2026 for controlled-release fertilizers using PBAT manufacturing technology, plus academic work in 2026 evaluating PBS and PCL coated urea systems. Together, these developments support product differentiation beyond commodity coated-urea positioning.

Recent Industry Developments

- June 2026: Nousbo Co., Ltd. registered a second patent covering manufacturing technology for controlled-release coated fertilizers using a biodegradable PBAT-based coating. The added IP strengthens process defensibility for biopolymer coatings and supports differentiation as buyers and regulators increase scrutiny of coating fate in soil.

- March 2026: Fauji Fertilizer Company (FFC) disclosed in its Annual Report 2025 that it is developing a biodegradable polymer-coated urea targeted at soil moisture conservation, with a stated plan to launch in Q3 2026. The disclosure points to pipeline activity from a large integrated producer in an arid-agriculture use case where controlled-release performance and moisture management can be bundled into one product proposition.

- July 2024: Yara International ASA formed a joint venture with Kingfa Sci. and Tech. to commercialize starch-based coatings aimed at Chinese grain producers, with a pilot plant slated for 2026. The partnership links fertilizer distribution reach with polymer-material scale capabilities, targeting lower-cost biodegradable coating pathways for higher-volume row-crop applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenue generated from sales of urea fertilizer granules or prills that are coated with biodegradable polymers to control nitrogen release in soil and improve nitrogen use efficiency, across agriculture and turf uses, and measured at the point of sale by producers and distributors.

Scope exclusions: Excludes conventional uncoated urea and non-biodegradable polymer coated urea products.

Segmentation Overview

- By Crop Type

- Grains and Cereals

- Pulses and Oilseeds

- Commercial Crops

- Fruits and Vegetables

- Turf and Ornamentals

- By Polymer Type

- Polylactic Acid (PLA)

- Polycaprolactone (PCL)

- Starch-based Polymers

- Other Biodegradable Polymers

- By Application Method

- Broadcast Spreading

- Fertigation

- Foliar Application

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping how biodegradable coated urea is produced, sold, and regulated, so the model uses consistent units and comparable pricing logic across regions. We leaned on public references such as FAOSTAT fertilizer and crop statistics, USDA and other agriculture ministry notes on nutrient management, Eurostat and national statistical offices for trade and price signals, and customs import-export data where fertilizer codes can be tracked at a high level.

To tighten assumptions, we also reviewed sources such as peer-reviewed agronomy journals covering nitrogen loss reduction and controlled release performance, association publications from fertilizer and farm input bodies, and company filings or investor presentations that discuss coated fertilizer revenue mix and capacity additions. In places where public disclosures were thin, a paid subscription focused on company financials and a shipment-level trade database were used selectively to sanity check supplier presence and cross-border flows. These desk sources are not exhaustive, and many other references were used to collect data, validate figures, and clarify unclear points.

Primary Interviews and Surveys

Primary inputs were gathered through expert interviews and structured surveys with fertilizer producers, coating material suppliers, distributors, agronomists, and large farm operators, and then the learnings were compared across APAC, EMEA, and the Americas to avoid region-specific bias. We used these conversations to confirm adoption levels by crop intensity, typical coating premiums, channel margins, and the practical pace at which biodegradable coatings are replacing other controlled release formats.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 43% |

| Mid tier: 41% | Functional/Unit leaders: 26% | EMEA: 37% |

| Smaller Players: 22% | Managers: 60% | Americas: 20% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where national fertilizer consumption and cropping intensity signals are translated into a realistic demand pool for controlled release urea, and then narrowed to the biodegradable coated share using adoption rates validated with interviews. Once that demand pool was constructed, pricing was applied using region-specific average selling price ranges, adjusted for coating premiums, product mix, and channel markups.

To keep the totals practical, we corroborated results with selective bottom-up approximations, including supplier capacity and output indications, distributor channel checks, and sampled price quotes multiplied by estimated volumes in high-use crop belts. Inputs that mattered most in the model included urea application rates by major crops, irrigated acreage trends, nutrient loss and leaching constraints that push slow release use, relative price spread between coated and uncoated urea, and policy signals such as nutrient management guidelines and subsidy programs tied to efficiency fertilizers. For forecasting, scenario analysis was used and then anchored with an exponential smoothing view of near-term demand, because adoption can shift when price gaps narrow or when regulations tighten. Where supplier-level data was missing, gaps were handled by using regional penetration bands and then re-tested with primary feedback until the implied volumes looked consistent with known distribution capacity.

Data Validation & Update Cycle

Outputs are checked through multiple passes, starting with unit consistency checks (tons to value) and then cross-checking growth rates against independent indicators such as urea price cycles, crop planting trends, and import reliance in net-deficit regions. If a country total looks out of line, we revisit the assumptions, re-check conversion factors, and re-contact relevant respondents to confirm whether the issue is pricing, mix, or adoption.

Before sign-off, the model is reviewed by another analyst for variance flags and logic breaks, and then the final numbers are aligned with the latest available public updates. Reports are refreshed annually, and interim updates are made when major events occur, such as policy changes, sharp raw material price moves, or notable capacity expansions. Right before delivery, a final review pass is done so clients receive the most current view.

Mordor Intelligence's Bio Degradable Polymer Coated Urea Market Size Compared Against Other Published Estimates

Published market sizes for biodegradable polymer coated urea can differ a lot because the counted product set is not always the same, and because firms apply different price points and adoption curves across regions. Differences also show up when one study uses older urea pricing, or when another study treats distributors and end users differently in the revenue chain.

Non-biodegradable polymer coated urea sits outside Mordor Intelligence's scope, which reduces the total versus sources that blend all polymer coated controlled release urea into one number without separating coating biodegradability. Other gaps typically come from whether turf and ornamental use is counted as a core demand bucket, whether pricing is taken at factory gate or at the channel level, and how fast the coating premium is assumed to compress over the forecast period.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.12 B (2025) | |

| Regional Consultancy A | USD 0.64 B (2024) | Uses an earlier base year and a narrower adoption lens, and the writeup does not clarify if turf and high-value horticulture are included, which can understate demand in mature regions. |

| Trade Publisher B | USD 2.35 B (2025) | Appears to include adjacent coated fertilizer uses beyond biodegradable urea, and it is unclear whether revenue is captured at retail level, which can inflate the value versus producer and distributor sales. |

The spread across sources is mostly explained by product inclusion rules and how revenue is captured along the sales chain, followed by base-year pricing and adoption assumptions. By keeping the demand pool tied to crop-driven urea usage and then validating the biodegradable coated share through interviews, the estimate stays traceable to clear volumes, premiums, and region-level uptake patterns.

Key Questions Answered in the Report

What is the projected value of the bio degradable polymer-coated urea market in 2031?

It is forecast to reach USD 1.69 billion by 2031, underpinned by a 7.08% CAGR between 2026 and 2031.

Which crop segment is expanding the fastest?

Fruits and vegetables are growing at a 10.22% CAGR, driven by export market residue standards and higher per-hectare revenues.

Why are polylactic acid coatings widely used?

PLA commands 32.60% share because it has an established supply chain, meets compostability standards, and is accepted under organic certification schemes.

Which region is growing quickest?

The Middle East leads regional growth at 9.56% CAGR owing to water-scarcity pressures and food-security investments.

Page last updated on: