Bio-degradable Polymer Coated NPK Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

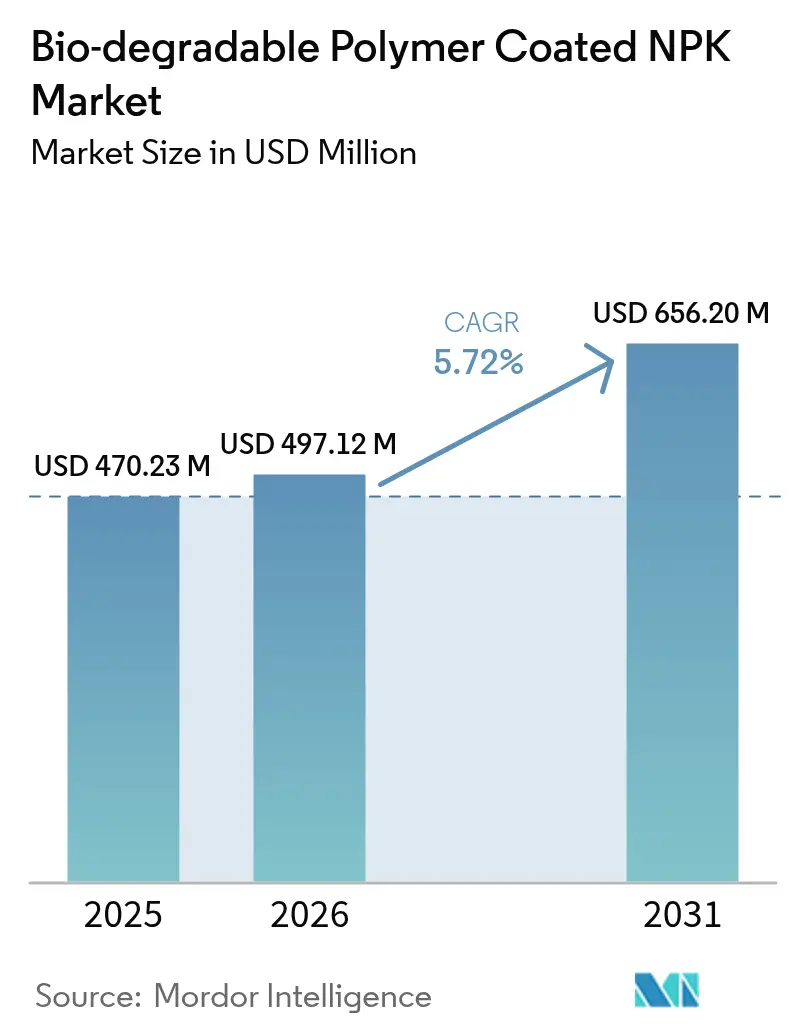

| Market Size (2026) | USD 497.12 Million |

| Market Size (2031) | USD 656.2 Million |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

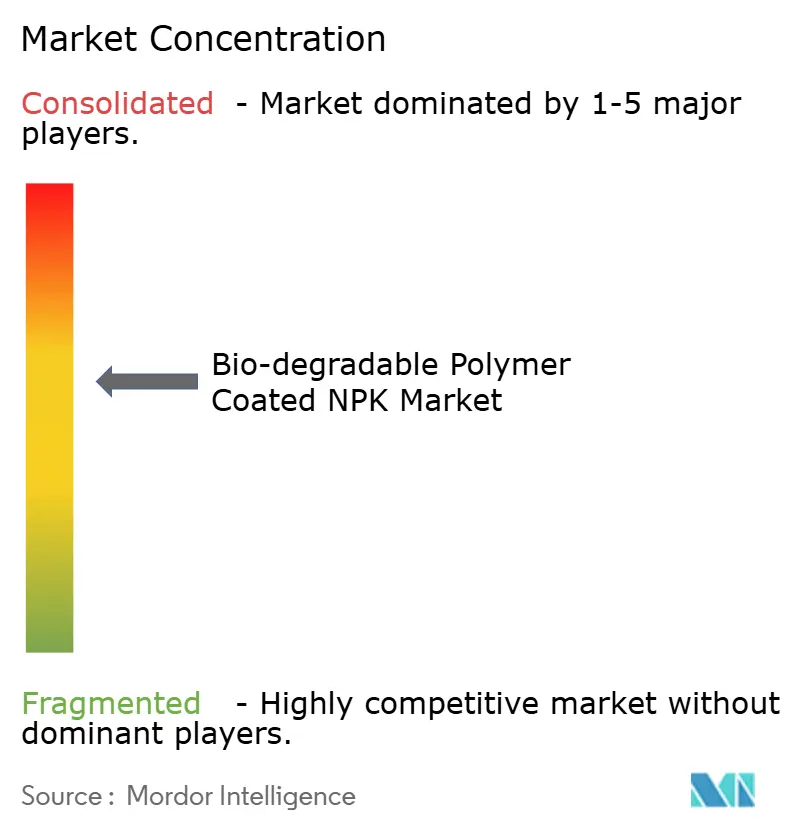

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bio-degradable Polymer Coated NPK Market Analysis by Mordor Intelligence

The bio-degradable polymer coated NPK market size in 2026 is estimated at USD 497.12 million, growing from 2025 value of USD 470.23 million with 2031 projections showing USD 656.2 million, growing at 5.72% CAGR over 2026-2031. A confluence of regulatory pressure, incentive programs that reward carbon-smart inputs, and the practical benefit of fewer field passes is reshaping procurement strategies across large commodity operations and high-value specialty crops. North America already enforces strict caps on nutrient runoff, while Europe and parts of Asia implement hard deadlines for microplastic bans, setting clear compliance timelines for manufacturers. Growers are also integrating coated granules with sensor-driven variable-rate platforms, creating a product-plus-service ecosystem that blurs the line between fertilizer and farm management software. Together, these forces position the bio-degradable polymer coated NPK market as a critical enabler of regenerative and precision agriculture rather than a niche environmental choice.

Key Report Takeaways

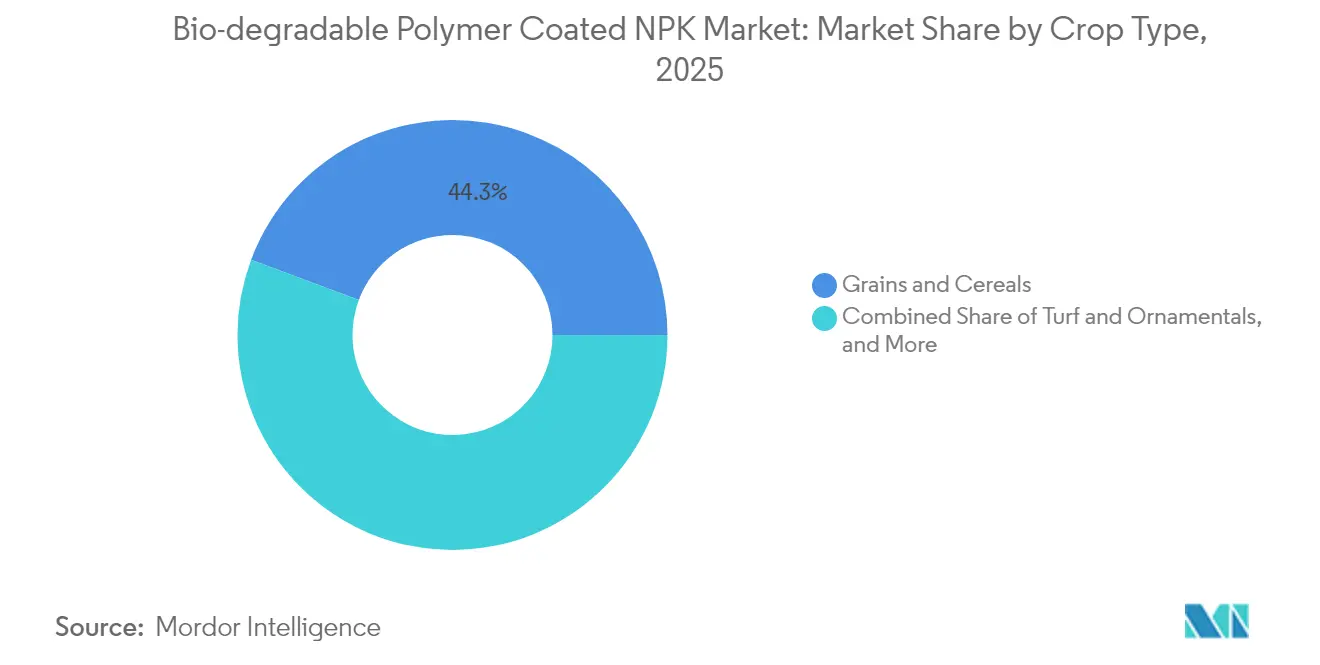

- By crop type, grains and cereals led with 44.30% of the bio-degradable polymer coated NPK market share in 2025, while turf and ornamentals are set to advance at a 7.45% CAGR through 2031.

- By geography, North America accounted for 33.40% of the bio-degradable polymer coated NPK market size in 2025, whereas Asia-Pacific is forecast to expand at an 8.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bio-degradable Polymer Coated NPK Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Need to raise nutrient-use efficiency amid fertilizer-runoff caps | +1.2% | Global, strongest in North America and Europe | Medium term (2–4 years) |

| Government incentives for carbon-smart and precision nutrition | +0.9% | North America, Europe, Japan, and South Korea | Short term (≤ 2 years) |

| Regulatory bans on micro-plastic coatings | +1.5% | Europe, expanding to Asia-Pacific and select South American jurisdictions | Long term (≥ 4 years) |

| Cost optimization via reduced application rounds | +0.7% | North America, Australia, and Brazil | Medium term (2–4 years) |

| Integration with sensor-enabled smart fertilization systems | +0.6% | North America, Europe, Japan, and Australia | Long term (≥ 4 years) |

| Shift toward regenerative farming and soil-health KPIs | +0.8% | Global, early adoption in North America, Europe, and New Zealand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Need to Raise Nutrient-Use Efficiency Amid Fertilizer-Runoff Caps

Escalating nitrogen and phosphorus discharge limits compel growers to match nutrient release with crop uptake windows. The United States Environmental Protection Agency has tightened Total Maximum Daily Load allocations across Midwestern watersheds, prompting corn and soybean producers to cut leaching or face penalties [1]Source: United States Environmental Protection Agency, “Total Maximum Daily Load Program,” epa.gov. Bio-degradable polymer coatings lengthen release to as much as 180 days, allowing 15–25% fertilizer rate reductions without yield loss. Comparable rules under the European Union Nitrates Directive accelerate the switch in Germany, France, and the Netherlands, where CEN/TS 17700 verification confirms controlled-release performance. Consequently, institutional pressure, rather than voluntary stewardship, now drives adoption in intensive production systems.

Government Incentives for Carbon-Smart and Precision Nutrition

Public funding lowers growers’ payback periods on coated NPK purchases. The United States Department of Agriculture earmarked funds for climate-smart commodity pilots that include controlled-release inputs. Taiwan covers up to 30% of the farm-gate cost when growers document emission cuts [2]Source: Taiwan Ministry of Agriculture, “Carbon Reduction Subsidy Programs,” moa.gov.tw. Washington State reimburses USD 50 per acre for compliant products, pushing specialty-crop nutrition toward biodegradable coatings. These incentives compress payback periods for growers, making the economics of bio-degradable coated NPK competitive with conventional options in regions where carbon credits or sustainability premiums are accessible. The strategic implication is that markets with robust public support will see faster penetration rates, while regions lacking subsidy frameworks will lag until coating costs decline through scale economies.

Regulatory Bans on Micro-Plastic Coatings

Legislative action against persistent polymer residues is accelerating the transition to bio-degradable alternatives. The European Union finalized amendments to Regulation 2019/1009 in 2024, mandating that all fertilizer coatings meet biodegradability criteria under EN 13432 or equivalent standards by 2028, effectively banning the use of polyethylene and polypropylene shells. Japan's Ministry of Economy, Trade, and Industry published guidelines in 2024 encouraging the replacement of conventional polymer coatings with bio-based materials, citing concerns over microplastic accumulation in paddy soils [3]Source: Japan Ministry of Economy, Trade and Industry, “Guidelines for Bio-based Agricultural Materials,” meti.go.jp. California is drafting aligned rules for specialty crops, creating a hard reformulation deadline that shifts R&D toward polylactic acid, polyhydroxyalkanoate, and starch blends.

Cost Optimization via Reduced Application Rounds

Labor and equipment costs associated with multiple fertilizer applications are driving large-scale growers toward single-application controlled-release solutions. Brazilian sugarcane producers are adopting bio-degradable coated NPK to eliminate mid-season topdressing, cutting tractor passes, and soil compaction while maintaining cane yield and sucrose content. Australian wheat growers report similar savings, with controlled-release formulations allowing pre-plant application that covers the entire growing season and eliminates the need for in-season nitrogen top-ups. The economic advantage compounds in regions with high labor costs or where equipment availability constrains timely application, making bio-degradable coated NPK a strategic input for operations focused on operational efficiency rather than sustainability alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing versus conventional NPK | -1.0% | Global, with acute impact in South Asia, sub-Saharan Africa, and smallholder-dominated regions | Short term (≤ 2 years) |

| Limited farmer awareness in smallholder systems | -0.6% | South Asia, sub-Saharan Africa, and Southeast Asia | Medium term (2-4 years) |

| Shorter shelf-life of bio-based coatings in humid tropics | -0.4% | Southeast Asia, Central America, and West Africa | Medium term (2-4 years) |

| Scale-up challenges for bio-polymer supply chains | -0.5% | Global, with bottlenecks in PLA and PHA production capacity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing Versus Conventional NPK

Bio-degradable polymer coated NPK typically commands a 20 to 40% price premium over conventional granular fertilizers, creating an adoption barrier in price-sensitive markets. Smallholder farmers in South Asia and sub-Saharan Africa, who operate on razor-thin margins and lack access to credit, prioritize upfront cost over long-term efficiency gains. A 2024 survey by the International Fertilizer Development Center found that only 12% of smallholder maize growers in Kenya were willing to pay more than a 15% premium for controlled-release products, even when extension agents demonstrated yield benefits. Until production volumes rise and raw material costs fall, adoption tends to skew toward large operations and high-value crops.

Limited Farmer Awareness in Smallholder Systems

Extension services in many developing regions have yet to incorporate bio-degradable coated fertilizers into training curricula, leaving smallholders unaware of the agronomic and economic benefits. The knowledge gap is compounded by limited demonstration trials and a lack of localized data on crop response, making it difficult for farmers to assess whether the premium is justified under their specific soil and climate conditions. Manufacturers and development agencies are beginning to address this constraint through farmer field schools and participatory research, but scaling these efforts to reach millions of smallholders will require sustained investment and coordination with national agricultural ministries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Grains Anchor Demand, Turf Leads Growth

Grains and cereals generated 44.30% of 2025 revenue, confirming their status as the core consumption base for the bio-degradable polymer coated NPK market. Extensive university field trials on wheat, rice, and corn validate 15–25% nitrogen savings at parity yields, strengthening the case for premium inputs. Large agribusinesses integrate coated NPK with variable-rate seeders to reduce the number of side-dress passes and mitigate runoff fines. Grains also benefit from policies that peg crop insurance to documented nutrient stewardship, turning compliance into a revenue-protection tactic. Pulses and oilseeds are trailing grains but are moving steadily upward as export buyers require stewardship audits on soybeans and chickpeas. Commercial crops, such as sugarcane, coffee, and cotton, utilize coated NPK, enabling estates to amortize costs and document soil health improvements for certification premiums.

Turf and ornamentals represent a smaller value pool today but are on track for a 7.45% CAGR, the highest among segments. Municipalities mandate low-runoff landscaping, and professional contractors absorb price premiums in exchange for labor savings, as one application can cover an entire growing season. Sports venues, golf courses, and campus grounds departments are increasingly specifying products verified under ISO 14001 environmental management, reinforcing demand elasticity and accelerating technological turnover. Fruits and vegetables remain niche users. Uptake is concentrated in controlled environments where nutrient precision has a direct influence on grade and shelf life.

Geography Analysis

North America held a 33.40% share of the bio-degradable polymer coated NPK market in 2025, underpinned by EPA runoff regulation and incentive schemes that reimburse compliant inputs. United States corn and soybean farms averaging over 400 hectares amortize price premiums through lower labor and fuel outlays. Canada scales adoption in canola rotations, supported by federal greenhouse-gas reduction payments. Mexico’s use centers on export-oriented greenhouse vegetables whose buyers demand residue-free certifications.

The Asia-Pacific region is projected to post an 8.07% CAGR through 2031, the fastest regional pace. Japan’s crop-science subsidies and strict recycling culture push rice and greenhouse vegetables toward bio-degradable coatings. China’s 14th Five-Year Plan pilots in Jiangsu and Shandong penalize excess nitrogen, prompting wheat and corn growers to switch to compliant blends. Australia applies coated NPK in horticulture and turf to curb leaching into reef catchments, whereas concerns over shelf life and limited extension reach hinder the uptake in Southeast Asia.

Europe accelerates because Regulation 2019/1009 sets a 2028 biodegradability deadline. Germany, France, and the Netherlands deploy coated fertilizers in intensive vegetable and potato farms, whereas Russia lags due to weaker enforcement and a scarce supply of bio-polymer. South America sees selective use, Brazilian sugarcane and soy estates leverage coated NPK for labor savings, whereas Argentina’s macro volatility slows investment. The Middle East and Africa remain emergent, with high-value export horticulture in Israel, Turkey, and South Africa driving pocket adoption, where water scarcity elevates the need for nutrient precision.

Regulatory Landscape

Regulation is increasingly shaping which coated fertilizers qualify for sale, with the European Union providing the clearest compliance clock for polymer coatings. Under Regulation (EU) 2019/1009 and the European Commission amendments adopted in 2024 for polymers in Component Material Category (CMC) 9, coating agents used to control nutrient release must meet defined biodegradability criteria (aligned to standards such as EN 13432 or equivalent). Supplier guidance ties the practical market deadline to October 2028, pushing manufacturers active in the EU to validate biodegradation performance in relevant environments and to transition away from persistent polyethylene and polypropylene-type shells.

In North America, runoff and water-quality compliance continues to drive nutrient management requirements at the watershed level, while policy discussions around plant-input definitions progress. The Plant Biostimulant Act of 2025 (S.1907/H.R.3783) proposes a consistent definition for plant biostimulants under FIFRA, explicitly excluding substances intended as plant nutrients or soil amendments, which should clarify product positioning for companies spanning fertilizer and adjacent input categories. At the global level, the FAO and the International Fertilizer Association renewed their Memorandum of Understanding in June 2026 to advance the International Code of Conduct for the Sustainable Use and Management of Fertilizers, reinforcing a shared framework around nutrient-use efficiency, soil health, and data transparency that governments and industry use to shape programs and procurement criteria.

Competitive Landscape

The bio-degradable polymer coated NPK market is moderately consolidated. Global majors, including Haifa Group, ICL Group Ltd., J.R. Simplot Company, DeltaChem GmbH, and Florikan ESA LLC, defend their shares through proprietary chemistries and embedded distributor networks. They increasingly bundle coated NPK with sensors, variable-rate applicators, and agronomic consulting to migrate revenue from product margins to service contracts. Regional formulators pursue starch- and chitosan-based blends tailored to local crops and climates, gaining speed without the overhead of multinational compliance processes.

Technology differentiation pivots on patent portfolios, filings related to soil and fertilizer management reached 23,736 families in 2024, led by BASF SE, Yara International ASA, and Locus Solutions. Haifa’s forthcoming plant will triple its bio-based capacity, positioning it to meet the demand spikes in Europe. Yara’s IBM partnership exemplifies convergence between chemistry and digital agronomy, while Nutrien trials bio-degradable coatings on ESN Smart Nitrogen to safeguard a flagship brand. Entry barriers rise as CEN/TS 17700 functional verification and EN 13432 biodegradability become table stakes, favoring firms with accredited in-house labs.

Emerging disruptors target turf and ornamentals, where faster sales cycles and higher willingness to pay enable lean go-to-market models. Although scaling across commodity grains will demand secure bio-polymer supply chains and field-validated agronomy support. Mergers, joint ventures, and licensing deals around polymer technology are likely as incumbents shore up intellectual property and secure feedstock.

Bio-degradable Polymer Coated NPK Industry Leaders

Haifa Group

DeltaChem GmbH

Florikan ESA LLC

ICL Group Ltd.

J.R. Simplot Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The most immediate whitespace is in reformulation and verification pathways for EU-bound products, since the October 2028 biodegradability compliance deadline under Regulation (EU) 2019/1009 (CMC 9 polymer criteria adopted in 2024) is pushing portfolio upgrades away from conventional polymer shells toward biodegradable coatings. This creates room for suppliers that can provide coatings with documented soil and water biodegradation, plus controlled-release performance that aligns with testing and certification requirements. Service partners that support verification, certification, and agronomic protocols tied to CEN/TS 17700 functional verification and EN 13432-type biodegradability standards are also positioned to capture incremental demand.

On the technology front, R&D is widening the set of bio-based and hybrid materials that can address performance and climate constraints, including humid-tropic shelf-life and coating stability. In 2026, published research highlighted starch-based controlled-release sachets (Brazil), double-coated biochar fertilizers using corn starch and soybean wax, and alginate-based hybrid hydrogels for dual delivery, reflecting active innovation in starch, cellulose derivatives, and chitosan systems that can be adapted to NPK granules. Commercially, this supports opportunities in high-value crops and turf and ornamentals, where labor savings from fewer applications and compliance-driven specifications are already influencing purchasing decisions. It also opens licensing and supply-chain opportunities for bio-polymer producers dealing with scale-up bottlenecks in PLA and PHA capacity.

Recent Industry Developments

- January 2026: ICL Group highlighted eqo.x as a core biodegradable coating technology positioned for controlled-release fertilizers under the EU biodegradability criteria that take effect in 2028. The communication strengthened ICL's product-level differentiation around biodegradability verification alongside nutrient-use efficiency claims, helping distributors and growers map product choices to the approaching compliance deadline.

- February 2025: Haifa Group inaugurated a Multicote controlled-release fertilizer blending facility in Uberlandia, Brazil, expanding localized production and formulation capability for CRFs. The move improves regional responsiveness for crop-specific NPK programs and reduces logistics friction for large commercial farms that use coated fertilizers to cut application rounds.

- November 2024: ICL Group publicly welcomed the European Commission's delegated act on biodegradability criteria for fertilizer coating agents, stating that its eqo.x and eqo.s technologies align with the October 2028 compliance date. This signaled early product readiness for EU market requirements and raised the competitive bar for coated NPK suppliers selling into jurisdictions tightening microplastic-related rules.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of bio-degradable polymer coated NPK fertilizer products sold for crop nutrition, where the coating is designed to break down after nutrient release and reduce losses through leaching and volatilization.

Scope exclusions: We exclude conventional (non-biodegradable) polymer coated NPK, uncoated NPK blends, and broader controlled-release fertilizers that are not NPK based.

Segmentation Overview

- By Crop Type

- Grains and Cereals

- Pulses and Oilseeds

- Commercial Crops

- Fruits and Vegetables

- Turf and Ornamentals

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- Australia

- Rest of Asia-Pacific

- Middle East

- Turkey

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

For desk research, we map the nutrient and coating landscape, then narrow it to coated NPK products that match the bio-degradable definition used in this study. Public sources are used to set the outside boundaries for the model, including fertilizer consumption trends, crop area and yield signals, and trade flows that suggest demand shifts by region.

The sources we refer to include official agriculture statistics (such as USDA, FAOSTAT, and national agriculture ministries), international trade databases (such as UN Comtrade), and guidance documents from regulators and standards bodies that touch biodegradable materials and fertilizer use. We also use peer-reviewed agronomy and soil science journals to sanity check release-duration ranges and typical application behavior, and we review company annual reports, investor presentations, and reputable press for capacity, product positioning, and pricing commentary. Where needed, subscription company financials and intelligence, patent databases, and shipment-level import and export data are used to close gaps and cross-check directional claims. These examples are not exhaustive, and other public and internal references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test assumptions that desk research cannot fully settle, especially around adoption pace, price premiums versus standard NPK, and where biodegradable coatings are actually preferred in the field. We speak with producers, distributors, agronomists, and large end users across major consuming regions, so the demand signals are not driven by a single crop or geography.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | APAC: 51% |

| Mid tier: 53% | Functional/Unit leaders: 33% | EMEA: 30% |

| Smaller Players: 14% | Managers: 53% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand-pool approach where crop area and fertilization intensity are converted into an addressable NPK tonnage base, which is then filtered by the penetration of biodegradable coated formats. Because real adoption is uneven, the penetration layer is adjusted by region using signals that matter on the ground, including high-value crop share, irrigation intensity, soil and rainfall related nutrient-loss risk, and the presence of nutrient-efficiency programs that influence product choice.

Those demand totals are then corroborated with selective bottom-up checks, such as roll-ups from a sample of suppliers and channels, and a price times volume approximation using typical coated-NPK price premiums shared by trade and interview sources. Forecasts are produced using scenario analysis supported by expert views, where the main levers are cropped area shifts, fertilizer affordability, regulation and biodegradability standards movement, and coating cost trends. When country-level information is thin, the model uses proxy indicators from similar agronomic zones and is rebalanced during validation so the regional totals remain realistic.

Data Validation & Update Cycle

Outputs are validated through a set of cross-checks, so volumes and values do not drift away from known fertilizer demand signals and trade patterns. We look for outliers in implied coated share, pricing progression, and regional growth rates, and then investigate the drivers before numbers are finalized.

A multi-step internal review is followed, and we re-contact interviewees when new disclosures, regulation changes, or major capacity moves create a visible break from earlier assumptions. The report is refreshed annually, and interim updates are made when material events occur. Right before delivery, a fresh analyst pass is completed so clients receive the most current view.

Mordor Intelligence's Bio Degradable Polymer Coated Npk Market Size Versus Other Published Estimates

It is normal to see different market values for the same topic because each publisher draws the boundary in its own way, and then uses a different timing for prices, currency, and adoption. Differences also come from how strongly the model assumes coated products replace standard NPK, and whether the estimate is built from agronomic demand signals or from a broader category roll-up.

By tracking adoption at the crop and region level and refreshing price premiums with channel feedback, Mordor Intelligence keeps the total tied to coated NPK usage rather than mixing in adjacent controlled-release products or non-biodegradable coatings.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 497.12 M (2026) | |

| Industry Research Outlet A | USD 550.30 M (2025) | This estimate appears to anchor on a different base year and uses a faster growth path, with broader application and channel framing that can pull in related coated fertilizer demand beyond strictly bio-degradable coated NPK. |

| Global Consultancy B | USD 565.98 M (2025) | The sizing seems to apply a higher assumed penetration and premium pricing earlier in the forecast window, and it also shows mixed base-year references, which can shift the stated 2025 value upward when converted and aggregated. |

Across the three values, the spread is mainly explained by boundary choices and timing, not by a disagreement that the market is growing. When the model is anchored to an addressable NPK demand pool and the coating penetration is validated with field inputs, the resulting number stays easier to trace and repeat year to year.

Key Questions Answered in the Report

What is the projected value of the bio-degradable polymer coated NPK market by 2031?

It is forecast to reach USD 656.2 million by 2031, supported by a 5.72% CAGR.

Which region currently leads demand for bio-degradable coated NPK fertilizers?

North America holds a 33.40% share due to stringent runoff regulation and incentive programs.

Which crop segment is the fastest growing user of bio-degradable polymer coated NPK?

Turf and ornamentals are projected to expand at a 7.45% CAGR through 2031 as municipalities tighten water-quality rules.

Why do smallholders in South Asia and sub-Saharan Africa adopt coated NPK more slowly?

Premium pricing and limited extension support constrain uptake despite agronomic benefits.

How are manufacturers overcoming supply constraints of bio-polymers?

Firms such as Haifa are investing in dedicated plants and exploring starch- and chitosan-based alternatives to widen feedstock options.

Page last updated on: