Biliary Atresia Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

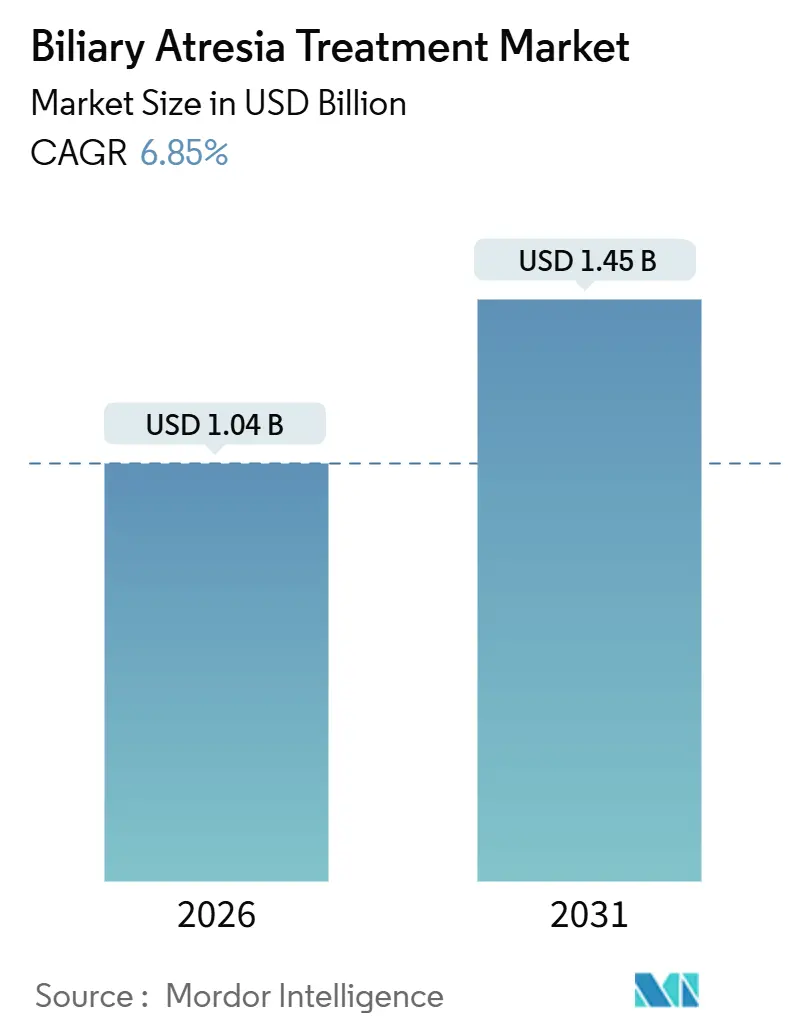

| Market Size (2026) | USD 1.04 Billion |

| Market Size (2031) | USD 1.45 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

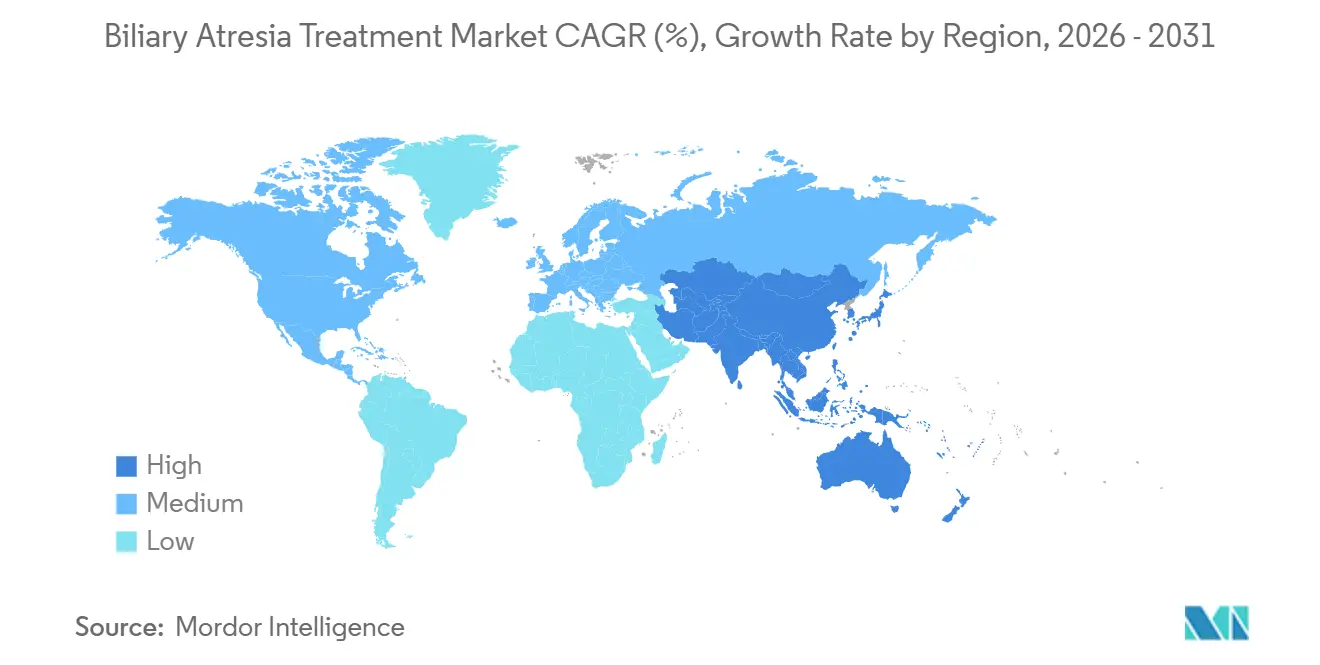

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biliary Atresia Treatment Market Analysis by Mordor Intelligence

The Biliary Atresia Treatment Market size is estimated at USD 1.04 billion in 2026, and is expected to reach USD 1.45 billion by 2031, at a CAGR of 6.85% during the forecast period (2026-2031).

Heightened neonatal screening, rapid uptake of living-donor transplantation protocols, and the arrival of ileal bile acid transporter (IBAT) inhibitors are accelerating revenue expansion across every major care setting. Mandatory direct bilirubin testing compresses time-to-diagnosis, while robotic Kasai techniques lessen surgical trauma, shorten stays, and improve native-liver survival. TransMedics’ normothermic machine perfusion is widening the donor pool, and expanded payer coverage for orphan drugs is lifting pharmacotherapy adoption curves. Competitive rivalry remains moderate because high-volume transplant centers and a small cohort of specialty pharmaceutical firms dominate clinical expertise and channel access.

Key Report Takeaways

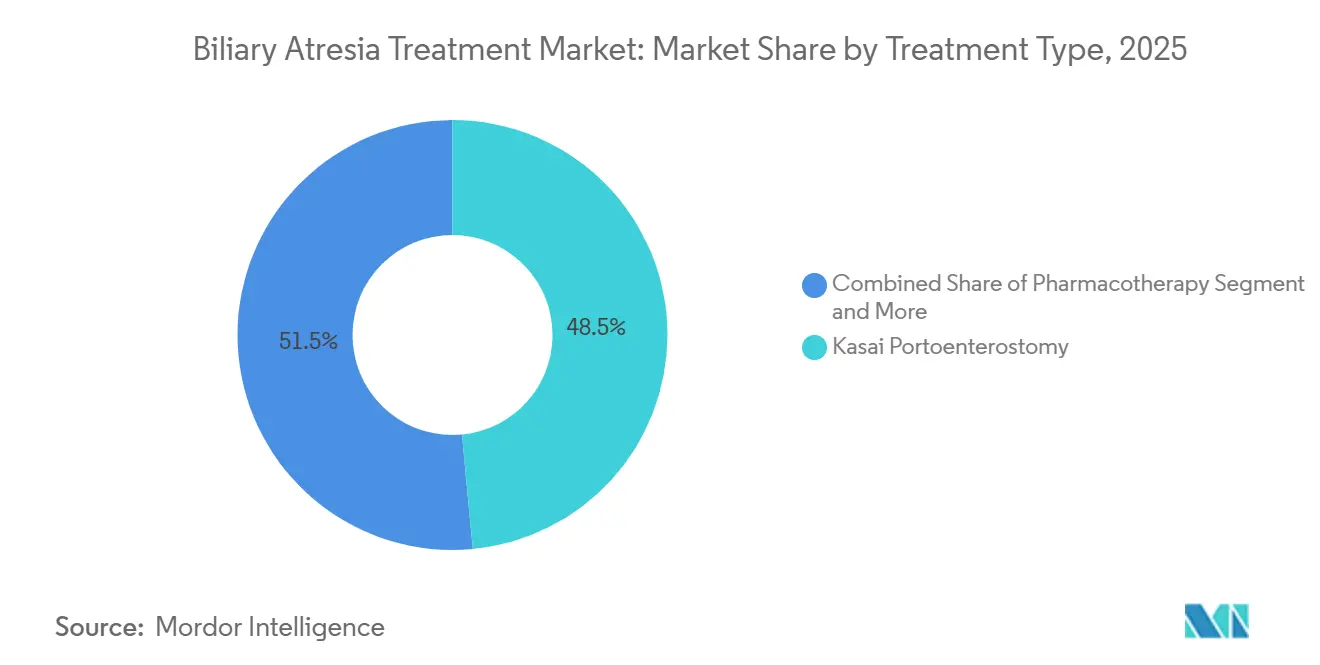

- Kasai portoenterostomy generated 48.55% of biliary atresia treatment market share in 2025, whereas pharmacotherapy is climbing fastest at an 11.25% CAGR through 2031.

- Open surgery accounted for 44.53% of Kasai procedure revenue in 2025, yet laparoscopic Kasai is advancing at an 11.85% CAGR, the quickest among procedures.

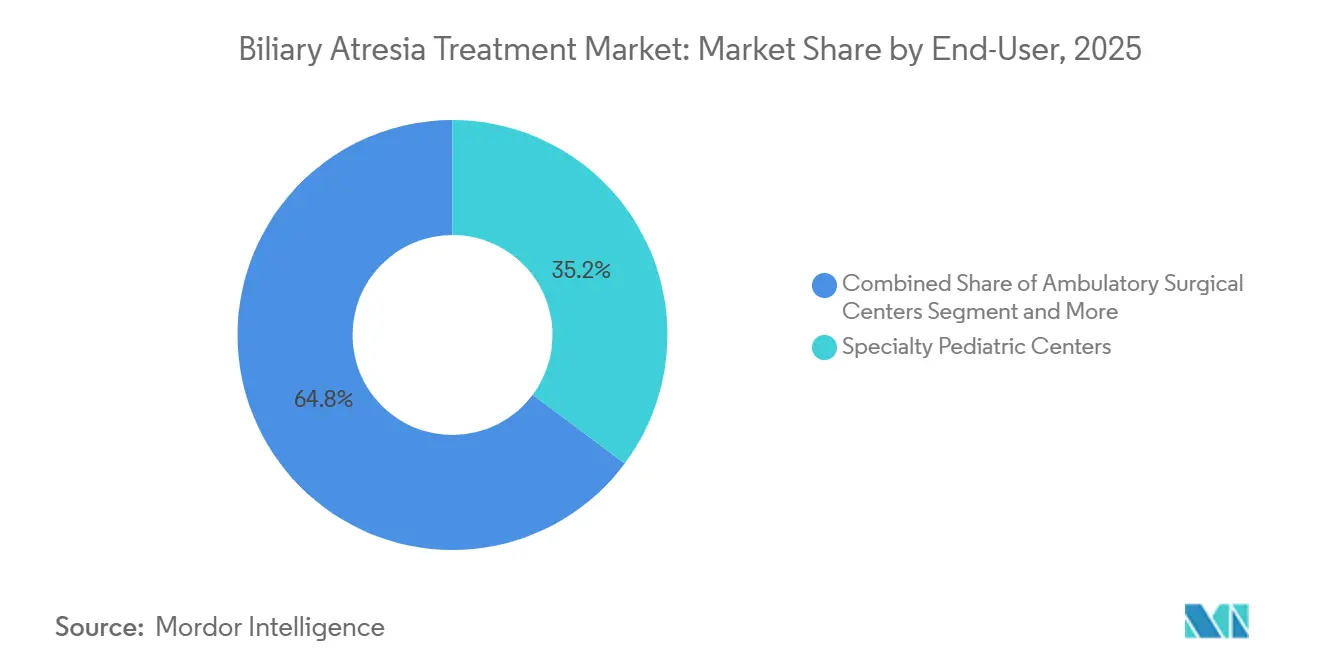

- Specialty pediatric centers held 35.23% of end-user revenue in 2025, while ambulatory surgical centers are expanding at a 10.15% CAGR through 2031.

- North America captured 38.15% of 2025 revenue, but Asia-Pacific is forecast to post the highest 9.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biliary Atresia Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of neonatal cholestatic disorders | +0.8% | Global, highest detection gains in Asia-Pacific | Medium term (2-4 years) |

| Growing success rates for living-donor liver transplantation | +1.2% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| New IBAT-inhibitor drug approvals & pipeline momentum | +1.5% | North America, Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Mandatory neonatal direct bilirubin screening | +1.0% | Taiwan, Japan, select U.S. states, pilots in China and India | Medium term (2-4 years) |

| Expansion of reimbursement for pediatric rare-disease drugs | +0.9% | North America, Europe, select Middle East markets | Short term (≤ 2 years) |

| 3-D printing for patient-specific Kasai planning | +0.6% | North America, Europe, Asia-Pacific academic centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Neonatal Cholestatic Disorders

Universal direct bilirubin screening has made prolonged jaundice a red-flag condition, triggering earlier hepatology referrals and pushing surgical intervention inside the critical 60-day window. Taiwan’s stool color card program reached 99.9% newborn coverage by 2024, cutting median Kasai age from 61 days to 52 days and raising five-year native-liver survival from 35% to 47%. The American Academy of Pediatrics updated 2024 guidance to recommend immediate direct bilirubin testing for any infant whose jaundice persists beyond 14 days, harmonizing U.S. practice with Asia-Pacific norms[1]Clinical Practice Guideline—Evaluation of Cholestatic Jaundice in Infants, American Academy of Pediatrics, aap.org. Japan’s updated card plus mobile-app protocol further lowered median diagnostic age to 48 days, proving that visual tools coupled with digital prompts tighten referral pathways. These early-detection gains stimulate procedure volumes and extend pharmacotherapy windows, especially in high-birth-rate countries. However, rural facilities in China and India still face logistic hurdles in distributing cards and accessing specialist labs, capping near-term upside.

Growing Success Rates for Living-Donor Liver Transplantation

Five-year graft survival now exceeds 85% in high-volume programs, turning living-donor transplantation into the preferred rescue therapy when Kasai fails. OPTN data show biliary atresia composing 37.3% of all U.S. pediatric liver transplants in 2025, with living-donor grafts rising to 42%, up from 38% in 2024. Living donation bypasses cadaveric waitlists that averaged 180 days in 2025, and shorter cold ischemia time cuts ischemic biliary complications. Microsurgical techniques plus 3-D vascular modeling trimmed portal-vein complication incidence to 8% in 2025 from 12% in 2020. Regulatory and reimbursement frameworks in North America, Europe, Japan, and South Korea support donor evaluation cost coverage, sustaining procedure growth. Expanded living-donor capacity also relieves pressure on a pediatric cadaveric organ pool that remains chronically under-supplied.

New IBAT-Inhibitor Drug Approvals & Pipeline Momentum

IBAT inhibitors redefine post-Kasai management by targeting pruritus and bile-acid buildup in patients who still possess native livers. The FDA cleared odevixibat in 2021, extended indications in 2024, and the EMA followed with Kayfanda approval in June 2024[2]Odevixibat for Alagille Syndrome, European Medicines Agency, ema.europa.eu. Maralixibat won FDA clearance in 2024 for Alagille syndrome and entered Phase 3 trials for biliary atresia, with top-line data due 2027. A 2025 cohort showed odevixibat cutting serum bile acids by 70% and pruritus scores by 60%, delaying transplant listing by 18 months. Next-generation molecules promise better bioavailability and fewer gastrointestinal events, widening the pharmacotherapy segment. Orphan-drug incentives, expedited reviews, and rare-pediatric-disease vouchers compress time-to-market, giving drug makers accelerated revenue capture.

Mandatory Neonatal Direct Bilirubin Screening

Direct bilirubin metrics are now a compulsory data point in many newborn checklists, tightening diagnostic windows. The Canadian Paediatric Society’s 2024 directive locked in uniform screening at two weeks of age, matching U.S. timing. Universal card distribution in Taiwan and Japan proves national public-health involvement accelerates early surgery impact. Pilot projects in Shanghai, Delhi, and Bangalore hospitals since 2024 show promising parental compliance, but rural diffusion lags due to fewer trained nurses and longer lab turnaround times. As additional provinces mandate screening, Asia-Pacific procedure volumes will rise, reinforcing the biliary atresia treatment market growth trend. Yet program success hinges on simultaneous capacity building at referral centers capable of completing Kasai before day 60.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of pediatric liver transplantation | –1.2% | Global, most acute in low- and middle-income economies | Long term (≥ 4 years) |

| Shortage of suitable pediatric donor organs | –1.5% | Global, acute in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Low awareness & delayed diagnosis in low-income economies | –0.8% | Sub-Saharan Africa, South Asia, rural Latin America | Medium term (2-4 years) |

| Post-operative complications & lifelong immunosuppression burden | –1.0% | Global, higher complication rates in resource-constrained settings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Pediatric Liver Transplantation

Transplant charges run from USD 500,000 to USD 1.2 million in the United States, with an added USD 30,000–50,000 annually for follow-up immunosuppression[3]Liver Transplant Cost Analysis, United Network for Organ Sharing, unos.org. Living-donor pathways increase hospital bills by another USD 100,000–150,000 because both donor and recipient need operating rooms and recovery beds. In India, a USD 80,000 average fee still dwarfs mean household income, forcing crowdfunding or charity appeals. Reimbursement caps in some U.S. private plans and European cost-containment policies exacerbate access disparities. High sticker prices slow procedure adoption in lower-income countries, dragging down global biliary atresia treatment market growth.

Shortage of Suitable Pediatric Donor Organs

Waitlist mortality for infants under one year reached 6.0 deaths per 100 patient-years in 2025, with 50 children removed or deceased while awaiting grafts in the United States. Only donors under 10 years match recipient size, and family consent rates for pediatric donation hover at 55% in the U.S. and 40% in Europe. Cultural hesitancy depresses deceased donation availability in Asia-Pacific and Middle East markets, making living donation the dominant channel. TransMedics’ machine perfusion shrank ischemic biliary complication incidence to 1.3% at six months, enabling marginal graft use, but adoption remains limited to affluent centers. Supply constraints therefore cap transplant volume potential even where surgical capacity exists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Pharmacotherapy Reshapes Post-Kasai Care

Kasai portoenterostomy delivered 48.55% of 2025 revenue, maintaining its status as the frontline intervention when diagnosis occurs before day 60. Pharmacotherapy, however, is on course to record an 11.25% CAGR through 2031, making it the fastest-growing modality in the biliary atresia treatment market. IBAT inhibitors such as odevixibat and maralixibat have reduced serum bile acids by 70% and deferred transplant listing by 18 months, reframing drug therapy as a transplant-bridging strategy. Meanwhile, liver transplantation generated a significant percentage of treatment dollars in 2025, yet its growth is limited by donor scarcity and high cost structures. Adjunct nutritional regimens, from medium-chain triglyceride formulas to fat-soluble vitamin infusions, round out the remaining 15% share, sustaining modest single-digit expansion.

Pharmacotherapy’s ascendance is rooted in payer acceptance and orphan-drug incentives that shorten commercialization cycles in the biliary atresia treatment market. Living-donor grafts lift transplant success but cannot match the scalability of pills or suspensions, ensuring drugs win share year after year. Robotic Kasai procedures extend surgical candidacy to infants under 10 kg, but IBAT inhibitors remain necessary for many patients who retain their native livers after surgery. With at least three next-generation inhibitors in preclinical stages, the biliary atresia treatment industry is preparing for a deeper therapeutic arsenal that could push pharmacotherapy revenue beyond surgical take. Nevertheless, surgical innovation will keep Kasai and transplant lines resilient, preventing outright displacement.

By Procedure: Laparoscopic Kasai Gains Traction

Open Kasai surgery controlled 44.53% of 2025 procedure revenue, yet its grip loosens as minimally invasive options rise. Laparoscopic Kasai will grow at an 11.85% CAGR to 2031, the best performance among procedures in the biliary atresia treatment market. A 2025 systematic review showed comparable bile-flow success with a 25% lower transfusion rate in infants under 10 kg when laparoscopy or robotic assistance was used. Living-donor liver transplantation now represents a significant percentage of transplant procedures, and normothermic perfusion reduces marginal graft discard, further lifting living-donor volumes.

The da Vinci Xi and similar platforms provide articulated instruments that navigate the neonatal porta hepatis with precision, cutting incision length and improving cosmetic outcomes. As more centers gain access to robotic equipment, conversion from open to laparoscopic Kasai will accelerate, reinforcing the overall minimally invasive surgery wave sweeping the biliary atresia treatment market. Machine perfusion technology similarly expands total transplantable organ supply, syncing with laparoscopic gains to elevate total procedure revenue. Financial barriers and training curves remain hurdles, but procedural innovation’s pull appears durable across high-income regions and selected Asia-Pacific hubs.

By End-User: Ambulatory Centers Expand Adjunct Care

Tertiary hospitals generated roughly 45% of 2025 revenue, reflecting their tight coupling with transplant theaters and intensive post-operative monitoring. Specialty pediatric centers followed at 35.23%, driven by concentrated Kasai and transplant caseloads and multidisciplinary expertise. Ambulatory surgical centers, although smaller, will register the fastest 10.15% CAGR through 2031 in the biliary atresia treatment market. These outpatient sites handle IBAT inhibitor infusions, nutrition counseling, and routine immunosuppression checks, lowering inpatient costs and improving family convenience.

Research institutes accounted for the remaining percentage of 2025 revenue, sustained by clinical-trial activity for maralixibat and pipeline IBAT candidates. Tertiary hospitals in Asia-Pacific—such as Asan Medical Center—are investing in living-donor suites to trim waitlist mortality, fortifying their revenue base. Yet payer pushback against extended hospital stays channels routine follow-up toward ambulatory centers, a trend likely to accelerate once remote monitoring platforms mature. The biliary atresia treatment market size attributed to outpatient care will therefore rise as stakeholders prioritize value-based reimbursement models.

Geography Analysis

North America commanded 38.15% of 2025 revenue due to the highest transplant volumes worldwide, rapid IBAT inhibitor uptake, and broad rare-disease drug coverage. Living-donor grafts already form 42% of pediatric liver transplants in the region, aided by comprehensive insurance reimbursement and mature donor-evaluation frameworks. Robust clinical-trial networks centered at Boston Children’s Hospital and Cincinnati Children’s funnel patients into pre-approval expanded-access programs, further inflating pharmacotherapy revenue. Cadaveric donation rates of 35 donors per million population also buffer supply shortages more effectively than elsewhere.

Europe contributes roughly significant percentage of the biliary atresia treatment market, leveraging universal health systems that guarantee Kasai and transplant access. Nevertheless, average deceased donation sits at 20 donors per million, restraining transplant expansion. Living-donor programs are scaling in Germany, France, and the United Kingdom, but cultural reticence keeps volumes below North American levels. EMA and NICE approvals for IBAT inhibitors smooth reimbursement pathways, yet post-Brexit regulatory divergence injects modest uncertainty into United Kingdom launch timelines.

Asia-Pacific will exhibit the fastest 9.51% CAGR to 2031 as screening programs in Taiwan and Japan mature and pilots in China and India broaden. Taiwan’s card initiative cut Kasai age to 52 days and pushed five-year native-liver survival to 47%. Japan’s app-enhanced cards shaved diagnostic age further, and both markets enjoy strong living-donor infrastructures. China and India possess enormous birth cohorts, so even partial screening penetration delivers large absolute procedure growth. Yet rural care deficits and slower drug reimbursement temper full-scale acceleration.

Middle East & Africa held about minor percentage of 2025 revenue, with living-donor operations exceeding 80% of pediatric transplants owing to cultural barriers to deceased donation. High transplant costs and limited IBAT inhibitor reimbursement keep growth subdued. South America’s share mirrors similar challenges: Brazil’s public system funds Kasai and transplant but struggles with donor rates, while Argentina maintains sporadic screening pilot programs. Overall, geography-specific drivers collectively reinforce the upward trajectory of the biliary atresia treatment market size, but donor availability and payer reimbursement remain decisive growth levers.

Competitive Landscape

Academic transplant powerhouses anchor the supply side of the biliary atresia treatment market. Boston Children’s, Children’s Hospital of Philadelphia, and Cincinnati Children’s performed most U.S. pediatric liver transplants in 2025, leveraging surgical talent, advanced imaging, and integrated hepatology units. Their commanding volumes secure referral dominance and grant early visibility into investigational therapies. Asia-Pacific centers—Kyoto University Hospital and Asan Medical Center—mirror this model for living-donor grafts, pushing surgical boundaries and feeding regional procedural growth.

Pharmaceutical rivalry centers on IBAT inhibitors. Ipsen (Albireo) commercialized odevixibat, while Mirum Pharmaceuticals markets maralixibat and runs Phase 3 trials in biliary atresia. Both firms exploit orphan-drug exclusivity and rare-disease vouchers to protect early-stage margins. Pipeline contenders develop second-generation molecules with improved gastrointestinal tolerability, signalling multi-brand competition by 2028. Supply-chain partnerships with specialty pharmacies and hospital dispensing units lock in formulary positioning and adherence programs, creating stickier revenue lines within the biliary atresia treatment industry.

Device innovators enlarge procedural capabilities. Intuitive Surgical’s da Vinci platform brings wristed instruments into neonatal dimensions, enabling laparoscopic Kasai in infants under 10 kg. TransMedics’ Organ Care System slashes ischemic biliary complications to 1.3% at six months, permitting broader use of marginal or distant donor livers. Emerging 3-D printing vendors provide anatomical models that trim operating time and elevate trainee competence, enticing tertiary centers aiming to differentiate quality metrics. Competitive strategies converge on clinical-evidence generation, technology bundling, and payer aligned value propositions, sustaining moderate industry concentration.

Biliary Atresia Treatment Industry Leaders

Ipsen (Albireo Pharma)

Mirum Pharmaceuticals

Takeda Pharmaceutical

TransMedics

Children’s Hospital of Philadelphia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Nagoya University researchers showed that minimally invasive laparoscopic surgery significantly cut blood loss and advanced jaundice recovery versus open surgery for biliary atresia.

- February 2025: The American Academy of Pediatrics issued new guidance that gives pediatricians a streamlined framework for early biliary atresia recognition.

Global Biliary Atresia Treatment Market Report Scope

As per the scope of the report, biliary atresia is a rare congenital liver condition in which the bile ducts outside the liver are abnormally developed or blocked, leading to bile buildup, liver damage, and cirrhosis. Treatment typically involves surgical procedures such as the Kasai portoenterostomy to restore bile flow, and in advanced cases, liver transplantation may be necessary.

The segmentation of the biliary atresia treatment market is categorized by treatment type, procedure, end-user, and geography. By treatment type, the market includes kasai portoenterostomy, liver transplant, pharmacotherapy, and adjunct nutritional/supportive care. By procedure, it is segmented into open surgery kasai, laparoscopic kasai, cadaveric-donor liver transplant, and living-donor liver transplant. By end-user, the market is divided into tertiary hospitals, specialty pediatric centers, ambulatory surgical centers, and research & academic institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Kasai Portoenterostomy |

| Liver Transplant |

| Pharmacotherapy |

| Adjunct Nutritional / Supportive Care |

| Open Surgery Kasai |

| Laparoscopic Kasai |

| Cadaveric-donor Liver Transplant |

| Living-donor Liver Transplant |

| Tertiary Hospitals |

| Specialty Pediatric Centers |

| Ambulatory Surgical Centers |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Kasai Portoenterostomy | |

| Liver Transplant | ||

| Pharmacotherapy | ||

| Adjunct Nutritional / Supportive Care | ||

| By Procedure | Open Surgery Kasai | |

| Laparoscopic Kasai | ||

| Cadaveric-donor Liver Transplant | ||

| Living-donor Liver Transplant | ||

| By End-user | Tertiary Hospitals | |

| Specialty Pediatric Centers | ||

| Ambulatory Surgical Centers | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the biliary atresia treatment market in 2031?

The market is forecast to reach USD 1.45 billion by 2031, reflecting a 6.85% CAGR over the 2026-2031 period.

How important is pharmacotherapy in delaying liver transplantation for biliary atresia?

IBAT inhibitors have reduced serum bile acids by 70% and postponed transplant listing by 18 months in post-Kasai patients, demonstrating their role as effective bridge therapy.

Which geographic region will grow fastest through 2031?

Asia-Pacific is expected to post the highest 9.51% CAGR due to expanded neonatal screening and living-donor transplant capacity.

Why are living-donor liver transplants rising?

Living-donor procedures bypass cadaveric waitlists, shorten cold ischemia time, and now achieve 85% five-year graft survival, making them the preferred option when Kasai fails.

What limits global transplant volumes?

Scarcity of size-matched pediatric donor organs and high procedure costs drive waitlist mortality and cap transplant growth, despite surgical advances.

How are robotic platforms changing Kasai surgery?

Systems like da Vinci Xi allow precise laparoscopic Kasai in infants under 10 kg, reducing blood loss and hospital stays compared with open surgery.

Page last updated on: