Big Data Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 28.05 Billion |

| Market Size (2031) | USD 30.25 Billion |

| Growth Rate (2026 - 2031) | 1.52% CAGR |

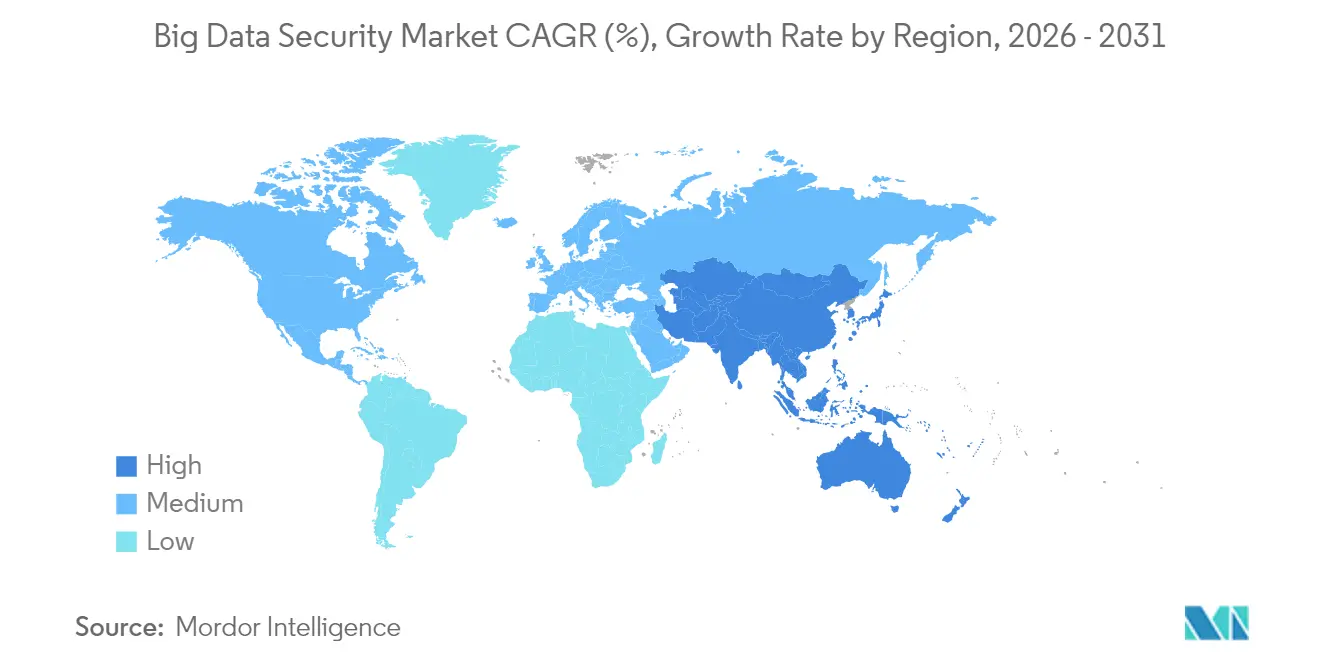

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Big Data Security Market Analysis by Mordor Intelligence

The Big Data Security Market size market is expected to grow from USD 27.63 billion in 2025 to USD 28.05 billion in 2026 and is forecast to reach USD 30.25 billion by 2031 at 1.52% CAGR over 2026-2031.

Accelerated adoption stems from rising cyber-attack frequency, stricter data-protection laws, and the shift of petabyte-scale workloads to public clouds that demand zero-trust controls. Enterprises now treat data-centric security as a board-level priority as AI-enabled breaches, ransomware, and supply-chain intrusions elevate operational and financial risk. Healthcare, manufacturing, and financial services face the highest breach costs, which pushes capital toward encryption, tokenization, and AI-powered analytics. Meanwhile, platform vendors consolidate point tools to reduce complexity and offset the cybersecurity talent shortfall, while data-sovereignty rules in Asia Pacific spark record data-center investment.

Key Report Takeaways

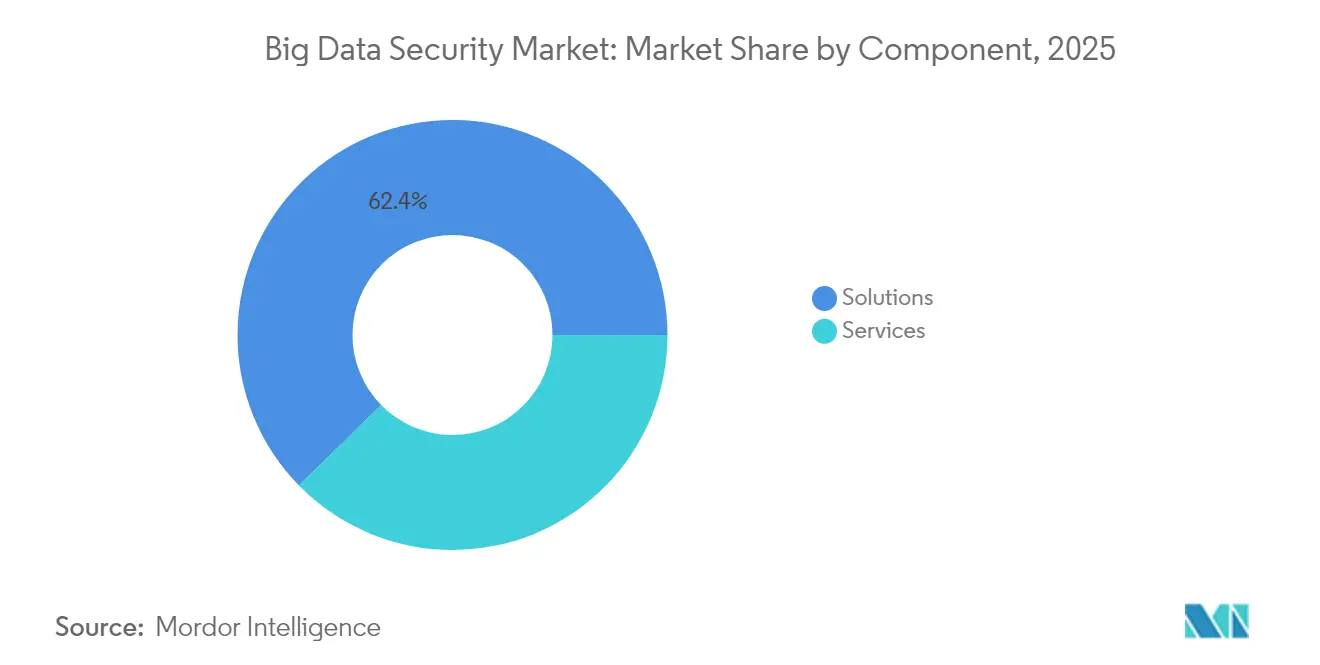

- By component, Solutions led with 62.35% revenue share in 2025; Services is projected to expand at a 18.72% CAGR to 2031.

- By organization size, Large Enterprises held 68.75% of the big data security market share in 2025, while Small and Medium Enterprises are growing at a 19.55% CAGR through 2031.

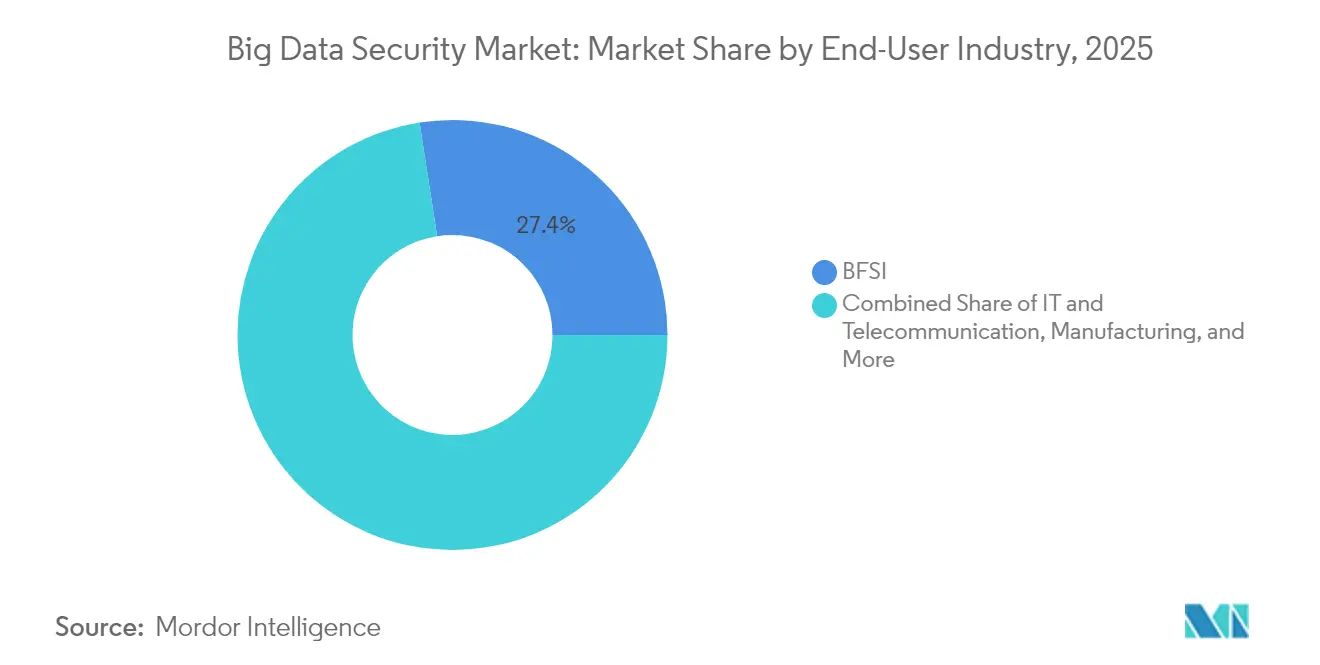

- By end-user industry, the BFSI segment commanded 27.45% share of the big data security market size in 2025, whereas Healthcare and Life Sciences are advancing at an 18.61% CAGR to 2031.

- By deployment mode, Cloud deployment accounted for 57.45% share of the big data security market size in 2025 and is rising at a 18.96% CAGR through 2031.

- By geography, North America dominated with 40.95% revenue share in 2025; Asia Pacific is forecast to grow at a 20.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Big Data Security Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surging IoT, mobile, and cloud logs overwhelm legacy controls, driving next‑gen data‑centric security adoption | +3.20% | Global (strong in North America, EU, APAC) | Short term (≤ 2 years) |

| AI-enabled breaches, double‑extortion ransomware, and supply‑chain attacks force bigger budgets for big‑data security analytics | +4.20% | North America & EU (spreading globally) | Short term (≤ 2 years) |

| GDPR, CCPA, PDPA, and dozens of new national laws mandate encryption, masking, and audit trails at petabyte scale | +3.00% | EU, North America, APAC | Long term (≥ 4 years) |

| Shift of data lakes to public cloud accelerates demand for cloud‑native security, zero‑trust, and shared‑responsibility tooling | +3.70% | Global | Medium term (2–4 years) |

| Enterprises scramble to secure massive proprietary datasets used for LLM training to avoid model leakage and IP loss | +3.10% | North America, EU, China | Short term (≤ 2 years) |

| Retail‑media, healthcare, and ad‑tech firms require encryption‑in‑use to share insights without exposing raw data | +2.40% | Global (notably North America, EU) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

AI-enabled breaches drive enterprise security budget reallocations

Ransomware groups now weaponize generative AI for rapid credential theft and social-engineering campaigns that bypass legacy defenses. Manufacturing downtime has surpassed USD 22,000 per minute during major incidents, prompting boards to lift security budgets well above prior allocations. Data-breach costs in industrial domains climbed to USD 5.56 million in 2024, eclipsing general IT-spending growth and fueling demand for real-time analytics that detect lateral movement. Financial institutions concede that current allocations of only 13% of IT spend underfund defenses, with experts urging a shift toward 20% to keep pace with attacker automation. Across critical infrastructure, AI-powered security operations centers report 30% faster incident resolution once machine-learning correlation replaces manual triage. The result is sustained top-line expansion for the big data security market as enterprises reprioritize funding.

GDPR and national data laws mandate petabyte-scale compliance infrastructure

Europe’s GDPR, California’s CCPA, and similar statutes in Asia Pacific now obligate encryption, masking, and audit trails across ever-larger datasets. China’s 2025 enhancements add real-time compliance audits for finance and insurance firms, tightening penalties for lax controls[1]Bird & Bird, “China Releases Draft Measures on Personal Information Compliance,” twobirds.com. European organizations have raised information-security budgets to 9% of total IT outlays under the NIS2 Directive, while average regional breach costs reached EUR 4.4 million in 2025. In the United States, the Department of Health and Human Services proposed USD 100 million for sector-wide cybersecurity coordination in its FY 2026 plan. As compliance moves from policy to technical enforcement, demand increases for scalable encryption, tokenization, and immutable logging key revenue streams within the big data security market.

Cloud data lakes accelerate zero-trust architecture adoption

Eighty-one percent of organizations intend to implement zero-trust by 2026 as VPN weaknesses proliferate. Cloud migration exposes shared-responsibility gaps that only cloud-native security can close, and providers now embed advanced threat intelligence into storage, analytics, and identity layers. North American enterprises are replacing legacy VPNs at a record pace, while Asia Pacific governments channel sovereign-cloud subsidies toward hyperscale builds. Cloudflare prevented an average of 385 million daily attacks in Japan during Q1 2025, illustrating both the threat landscape and the effectiveness of integrated edge defenses. These shifts reinforce the cloud’s structural advantage and enlarge the addressable big data security market.

LLM training in data protection becomes a strategic imperative

The 2024 exposure of proprietary AI training data underscored the risk of model leakage and intellectual-property theft. Nation-state groups such as Midnight Blizzard have since escalated espionage against corporate code repositories and email systems, leading firms to harden build pipelines and isolate training corpora. China’s AI-training data services could scale from USD 261 million in 2023 to USD 2.3 billion by 2032, heightening global competition for compliant datasets. Vendors answer with SecureLLM frameworks that merge differential privacy with lightweight cryptography, allowing model accuracy without exposing personal information.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Scarcity of data-security engineers and data scientists inflates project timelines and MSSP costs | –2.6% | Global, esp. North America & EU | Long term (≥ 4 years) |

| Orchestrating encryption, SIEM, IAM, and data-governance tools across hybrid estates strains CapEx/OpEx budgets | –2.0% | Global, SME-centric | Medium term (2–4 years) |

| Divergent residency laws (e.g., China CSL, Russia FZ-242) block unified global security architectures | –1.5% | High relevance in APAC & Russia | Long term (≥ 4 years) |

| Federated learning and homomorphic encryption reduce need for centralized data stores, tempering spend on classic big-data security stacks | –1.2% | Global, tech-forward enterprises | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity talent shortage constrains market growth

Thirty-two percent of EU organizations cannot fill essential cybersecurity roles, driving reliance on managed security service providers. Japan’s operators collaborate with Cloudflare to supply turnkey zero-trust services that offset staffing gaps for SMEs. Microsoft’s Secure Future Initiative applies 34,000 engineers to AI-driven automation, improving incident response by 30% and showcasing how hyperscalers compensate for scarce expertise. Although automation eases workloads, chronic shortages slow deployment and limit the near-term scale-up of the big data security market.

Tool-orchestration complexity strains enterprise budgets

A typical enterprise now manages separate encryption, SIEM, IAM, and governance tools, and business-partner breaches add 12% to average incident costs when integrations lag. Manufacturing firms respond by setting up dedicated supply-chain risk teams, yet tooling sprawl persists[2]Supply Chain Management Review, “Manufacturers Build Cyber-Resilient Supply Chains,” scmr.com. SMEs suffer disproportionately; nearly 60% of ransomware victims fall in this category, often lacking funds for holistic orchestration. Consolidation exemplified by Cisco’s USD 28 billion acquisition of Splunk reflects customer demand for unified platforms that reduce spend and complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services growth outpaces Solutions expansion

Solutions held 62.35% of 2025 revenue, driven by robust demand for encryption, tokenization, and SIEM suites. At the same time, Services is set to grow at 18.72% CAGR as organizations outsource 24/7 monitoring and compliance integration. Talent scarcity and platform complexity push enterprises toward managed detection and response, consulting, and integration contracts. Vendors bundle these offerings with cloud subscriptions, enabling predictable OpEx and faster implementation cycles. As a result, the big data security market will continue to reflect service-led value creation throughout the forecast period.

Managed Security Services show the highest traction, while Advisory and Integration engagements surge as firms re-architect data lakes on cloud foundations. Data encryption and tokenization software remains the volume driver within Solutions, propelled by regulatory mandates. SIEM platforms evolve with AI inference that reduces alert fatigue, and IAM upgrades underpin zero-trust rollouts. The convergence of platform features signals ongoing consolidation in the big data security market as players chase end-to-end control points.

By Organization Size: SME adoption accelerates democratization

Large Enterprises dominated in 2025 with 68.75% revenue, reflecting multi-region operations and stringent compliance obligations. Yet SMEs are forecast to post a 19.55% CAGR, highlighting cloud subscription models that lower entry barriers. Hyperscalers now embed enterprise-grade encryption, key management, and behavior analytics into baseline plans, letting resource-constrained firms access capabilities once exclusive to Fortune 500 peers. This shift broadens the customer base, sustaining double-digit expansion in the big data security market.

For large organizations, investments focus on advanced analytics, homomorphic encryption pilots, and AI-powered SOCs that mine petabyte-scale logs. Some institutions maintain teams exceeding 1,000 security specialists, underscoring the depth of in-house expertise. SMEs, by contrast, emphasize turnkey managed services that offload complexity. Vendors tailoring price points and automation to this segment stand to capture an outsized share as the big data security industry matures.

By End-User Industry: Healthcare momentum challenges BFSI primacy

The BFSI sector accounted for 27.45% revenue in 2025, owing to longstanding regulatory regimes and high data-at-risk thresholds. Healthcare, however, is projected to grow at 18.61% CAGR, catalysed by record breach volumes, patient-data sensitivity, and tighter enforcement that mirrors financial-sector scrutiny. Manufacturing follows closely, motivated by Industry 4.0 integration and supply-chain attack resilience mandates. Government, aerospace, retail, and telecom segments expand steadily as each adopts zero-trust reference architectures and strengthens encryption for sensitive workloads.

In healthcare, ransomware has disrupted critical care and driven average incident costs beyond USD 4 million, compelling leadership to fast-track AI-assisted monitoring and immutable backups. BFSI firms upgrade post-quantum encryption pilots and automated compliance tooling. Collectively, sector-specific pressures ensure robust demand across verticals, reinforcing the breadth of the big data security market.

By Deployment Mode: Cloud delivery cements structural advantage

Cloud deployment captured 57.45% revenue share in 2025 and is set for a 18.96% CAGR. Organizations trust hyperscale providers for infrastructure hardening and global compliance attestations, freeing internal teams to focus on application-layer protections. AWS reached a USD 100 billion annualized run rate in Q1 2025 as data-lake workloads moved en masse to S3, Redshift, and Lake Formation services. Microsoft’s cloud revenue climbed 20% year over year to USD 42.4 billion in Q3 FY 2025, illustrating the scale tailwind.

On-premises implementations persist in defense, highly regulated finance, and critical-infrastructure contexts where air-gapping remains mandatory. Even there, hybrid models emerge, sensitive compute stays onsite while analytics pipelines extend into sovereign-cloud environments. The dynamic keeps both deployment options relevant, but the faster trajectory resides with cloud, underpinning sustained growth in the big data security market.

Geography Analysis

North America held 40.95% of 2025 revenue, benefiting from early zero-trust adoption, a dense vendor ecosystem, and mature breach-notification laws. Growth moderates as large enterprises complete initial cloud migrations, yet ongoing AI-security pilots maintain spending momentum. Europe follows, propelled by GDPR enforcement and the NIS2 Directive, with information-security allocations now 9% of total IT budgets. Regulatory certainty fuels demand even as economic headwinds weigh on discretionary IT projects.

Asia Pacific is forecast for a 20.15% CAGR through 2031, reflecting sovereign-cloud investments and domestic-technology mandates. AWS’s pledge of 2.26 trillion yen (USD 15.3 billion) to expand Japanese regions by 2027 exemplifies its hyperscale commitment. Oracle separately plans USD 8 billion in local data centers to meet economic-security guidelines. China’s information-security market could hit 37 trillion yuan by 2027 as state bodies prioritize indigenous tooling. Governments across the region encourage local data processing to spur security product adoption, enlarging the big data security market size in emerging economies.

The Middle East, Africa, and Latin America represent smaller bases but show rising adoption as cloud coverage widens and financial-sector modernization policies advance. Gulf Cooperation Council states issue new cyber regulations tied to Vision 2030 agendas, while Brazil’s LGPD inspires neighbouring countries to legislate. Although infrastructure gaps temper growth, rising digital-banking penetration creates latent demand that the big data security market can tap as connectivity improves.

Regulatory Landscape

Big data security deployments are shaped by privacy, critical-infrastructure, and federal assurance frameworks that translate into technical requirements such as encryption, masking, immutable logging, and demonstrable access controls at scale. In the United States, OMB Memorandum M-25-04 (FY 2025 guidance) reinforces federal information security and privacy management expectations, while June 2026 National Security Presidential Memorandum NSPM-12 sets cybersecurity requirements for National Security Systems, aligned to meet or exceed NIST standards and to use secure configuration baselines for cloud providers hosting such workloads.

Standards and assurance programs are shifting from periodic attestations toward continuous, automated verification. FedRAMP 2026 consolidated rules emphasize persistent automated security assessment and configuration enforcement for cloud services, and NIST updates such as SP 800-70r5 (May 2026) and the final public draft of SP 800-172r3 (May 2026) refine baseline checklists and enhance requirements for protecting Controlled Unclassified Information. In the European Union, Regulation (EU) 2024/1689 (AI Act) adds mandatory cybersecurity, robustness, and data-governance obligations for high-risk AI systems, which raises the compliance bar for securing training and operational datasets used in big data and AI pipelines.

Value Chain Analysis

The value chain for big data security spans data platform and infrastructure layers (cloud, data lakehouse, database, and storage), security control vendors (encryption and tokenization, IAM/PAM, SIEM and security analytics, and data security posture management), and services partners that deploy and run controls in hybrid environments. Hyperscalers and database and data-platform providers increasingly embed native controls, such as key management, data discovery, classification, and telemetry hooks. Security vendors monetize through software subscriptions and usage-based analytics, supported by consulting, integration, and managed detection and response for 24/7 operations.

Implementation and run-stage dependencies create bottlenecks around toolchain integration, skills shortages, and third-party risk involving suppliers and data-sharing partners. Partnerships also show roles converging around AI-era data pipelines and security operations, including February 2026 collaboration between VAST Data and CrowdStrike (with NVIDIA) to secure AI lifecycle pipelines, March 2026 CrowdStrike partnerships supporting sovereign cloud deployment on STACKIT with Schwarz Digits, and June 2026 expansions where Cognizant integrated CrowdStrike Falcon into its AI Factory and managed services, and Atos joined CrowdStrike Project QuiltWorks to address frontier AI risk. Overall, these actions support a shift toward packaging big data security as interoperable platforms plus managed services, rather than standalone point products.

Competitive Landscape

The market exhibits moderate consolidation as platform players pursue end-to-end coverage. Cisco’s USD 28 billion acquisition of Splunk extended its observability and SIEM reach. Palo Alto Networks bought IBM’s QRadar SaaS assets to accelerate Cortex XSIAM development and unlock AI-driven correlation across petabyte-scale logs. Microsoft dedicates 34,000 engineers to its Secure Future Initiative, integrating Security Copilot into Azure and M365 suites to deliver 30% faster incident remediation. AWS embeds GuardDuty, Macie, and Detective deeper into its analytics stack, promoting architectural stickiness.

Patent filings in homomorphic encryption, confidential computing, and post-quantum algorithms signal the next battleground for differentiation. Start-ups address vertical niches healthcare data-de-identification, AI model governance, and OT network monitoring while incumbents weigh tuck-in acquisitions. Customers increasingly favor unified platforms that collapse SIEM, SOAR, and data-security posture management into a single console to mitigate skills shortages. Competitive intensity therefore revolves around breadth of coverage, AI efficacy, and regulatory alignment, sustaining innovation within the big data security market.

Big Data Security Industry Leaders

Oracle Corporation

Microsoft Corporation

Broadcom Inc. (Symantec Corporation)

IBM Corporation

Amazon Web Services

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One opportunity is in security controls that sit closer to the data plane and AI workflows, where organizations need policy enforcement, monitoring, and governance across data lakes, lakehouses, and databases used for analytics and LLM training. Vendor actions in 2026 reflect this direction. Oracle introduced Oracle Deep Data Security for Oracle AI Database 26ai (May 2026) to enforce authorization policies directly in the database for AI agents and users, while Microsoft expanded the Microsoft Sentinel data lake to support federated ingestion from Microsoft Fabric, ADLS, and Azure Databricks (April 2026), supporting longer retention and analytics across large-scale telemetry. These releases open up space for data-layer authorization, continuous posture management, and security analytics built around cloud-native data architectures.

A second opportunity is tool consolidation and managed delivery for organizations that cannot staff specialized data security engineering teams, particularly as workloads spread across clouds and sovereign environments. Examples include multi-year identity-security deployments such as BIO-key PortalGuard for Mozambique interbank payments infrastructure operator SIMO (February 2026) and enterprise zero-trust rollouts such as LTM deploying Cisco Secure Access for 80,000 users (June 2026), both indicating ongoing investment in identity-driven access and policy enforcement. Standards adoption also provides a packaging path for vendors and service providers to sell repeatable compliance offerings, including ISO/IEC 27701:2025 for privacy information management systems and ISO/IEC 27018:2025 guidance for protecting PII in public cloud processing contexts.

Recent Industry Developments

- May 2026: Oracle launched Oracle Deep Data Security for Oracle AI Database 26ai, adding database-native security controls that use declarative SQL policies for authorization. The release targets AI agent access patterns by pushing enforcement into the data layer rather than relying only on application logic, aligning with enterprise needs to secure training and analytics datasets.

- April 2026: Microsoft expanded Microsoft Sentinel data lake capabilities to support federated data ingestion from Microsoft Fabric, Azure Data Lake Storage, and Azure Databricks. This strengthens cloud-native security data retention and analytics pipelines that support AI-assisted detection across high-volume telemetry.

- July 2024: IBM Consulting and Microsoft announced collaboration to help clients modernize security operations and address cloud identity threats. The partnership supports large-scale integration and managed delivery of security controls, reinforcing services-led adoption for complex hybrid big data environments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers tools and services used to protect big data environments, where large and fast-moving datasets are stored, processed, and analyzed, across on-premise and cloud setups. Revenue is captured for security functions that directly reduce risk of data misuse, theft, and unauthorized access.

Scope exclusions: We exclude generic IT security spend that is not deployed to secure big data platforms, analytics pipelines, or the underlying data stores.

Segmentation Overview

- By Component

- Solutions

- Data Encryption and Tokenization

- Security Intelligence/SIEM

- IAM and PAM

- Intrusion Detection/Prevention

- Data Masking and Obfuscation

- Services

- Consulting and Integration

- Managed Security Services

- Training and Support

- Solutions

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By End-user Industry

- Banking, Financial Services and Insurance (BFSI)

- IT and Telecommunication

- Manufacturing

- Healthcare and Life Sciences

- Aerospace and Defense

- Government and Public Sector

- Retail and E-commerce

- By Deployment Mode

- On-premise

- Cloud

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Mexico

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to pin down the demand backdrop and the spending pool that big data security can realistically attach to. We rely on public references such as NIST cybersecurity guidance, ISO standards notes, US SEC filings for security spending commentary, and government or statistical portals such as OECD and World Bank for macro indicators that shape IT budgets.

To avoid relying on one lens, the sizing inputs are cross-checked using sources such as publications from US IT and cyber agencies, open datasets on breaches and incidents where available, peer-reviewed journals for security adoption themes, and trade association materials that describe data management and compliance expectations. We also use company filings, investor decks, product documentation, and a paid subscription focused on company financials and news to validate timelines, product positioning, and regional exposure. These sources are illustrative, and we reviewed many additional public references for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions and fill gaps on adoption intensity, typical deployment patterns, and pricing movement. We spoke with solution owners, channel partners, enterprise security leaders, and technical managers across APAC, EMEA, and the Americas, so the regional buying differences and compliance drivers feed into the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 18% | APAC: 42% |

| Mid tier: 49% | Functional/Unit leaders: 32% | EMEA: 37% |

| Smaller Players: 19% | Managers: 50% | Americas: 21% |

Market-Sizing & Forecasting

The core model uses a top-down approach where overall enterprise security and data infrastructure spending is reconstructed by region, then filtered through the share attributable to protecting big data platforms and pipelines. Once the demand pool is built, it is split by deployment and major end-use patterns to keep the totals realistic.

To keep the number anchored, results are corroborated with selective bottom-up approximations, such as sampled vendor revenue mapping, channel checks, and simple ASP times estimated volume for common big data security use cases. Inputs that matter most include cloud adoption in data workloads, growth in data lake and analytics usage, security tool consolidation trends, compliance pressure in regulated industries, and expected shifts in subscription pricing. Where provider revenue disclosure is incomplete, gaps are handled by applying conservative penetration ranges, which are validated through interviews and then reviewed against regional IT spending signals.

For forecasting, scenario analysis is used to reflect different speeds of cloud migration, compliance enforcement, and security budget prioritization, and then the chosen path is aligned to the consensus view shared by interviewed practitioners. The outcome is a market trajectory that can be explained step by step and recalculated when key indicators change.

Data Validation & Update Cycle

Validation is done through multiple checks so the final totals do not depend on one dataset or one assumption. We compare outputs against independent signals such as enterprise IT spending direction, cloud workload mix, and security category budget splits, and then any unusual jumps are reviewed until the driver is clearly understood.

Before sign-off, the model and assumptions go through internal review, and follow-up outreach is triggered when primary feedback shows a large variance versus desk inputs. Reports are refreshed annually, and interim updates are made when material events change spending patterns or regulatory expectations. Right before delivery, a final pass is completed so clients receive the most current view that can be traced back to clear inputs.

Mordor Intelligence's Big Data Security Market Size Compared With Other Published Estimates

Published market sizes for big data security can look far apart because the included spending pool is not consistent, and because the forecast starting year and currency timing vary across studies. Differences also come from how firms treat deployment mix, whether services are counted broadly, and how they validate pricing movement over time.

Adjacent categories like general endpoint, perimeter, and network security are often rolled into some estimates, but they sit outside Mordor Intelligence's scope unless they are directly deployed to secure big data platforms, data lakes, and analytics pipelines. Another gap driver is how aggressive the assumed cloud shift is, since higher cloud weight can push up recurring spend faster when subscription pricing is applied too broadly or refreshed infrequently.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 28.05 B (2026) | |

| Global Research Publisher A | USD 24.13 B (2024) | Uses an earlier base year and a faster growth window, and its bucket definition can lean toward software-led spending without consistently separating big data specific controls from broader security tooling. |

| Industry Advisory B | USD 30.59 B (2024) | Reports a larger 2024 value that may reflect wider technology mapping and a higher assumed cloud share, and the segmentation emphasis can cause double counting when multiple security technologies are grouped under one spend line. |

The spread in the table is mainly explained by what is counted as big data security versus nearby security categories, and by how quickly cloud-driven pricing is assumed to ramp. Our method keeps the total tied to a defined big data workload security pool, and then checks it against practical adoption and pricing inputs gathered through primary validation.

Key Questions Answered in the Report

What is the current size of the big data security market?

The market is worth USD 28.05 billion in 2026 and is projected to grow to USD 30.25 billion by 2031.

Which segment leads the big data security market?

Solutions hold the largest share at 62.35% of 2025 revenue, but Services is the fastest-growing segment with a 18.72% CAGR.

Why is Asia Pacific growing faster than other regions?

Sovereign-cloud investments, data-localization mandates, and large-scale hyperscaler spending drive a 20.15% CAGR for Asia Pacific through 2031.

How does zero-trust architecture influence market demand?

Zero-trust adoption replaces vulnerable VPNs and legacy perimeter defenses, accelerating demand for cloud-native security and AI-enabled analytics.

What challenges limit market growth?

Key restraints include a worldwide shortage of skilled cybersecurity professionals and the high cost of orchestrating multiple security tools across hybrid environments.

Which industries are investing most in big data security?

BFSI maintains the largest spending, but Healthcare shows the fastest growth due to escalating breach costs and regulatory pressure.

Page last updated on: