Air Brake System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

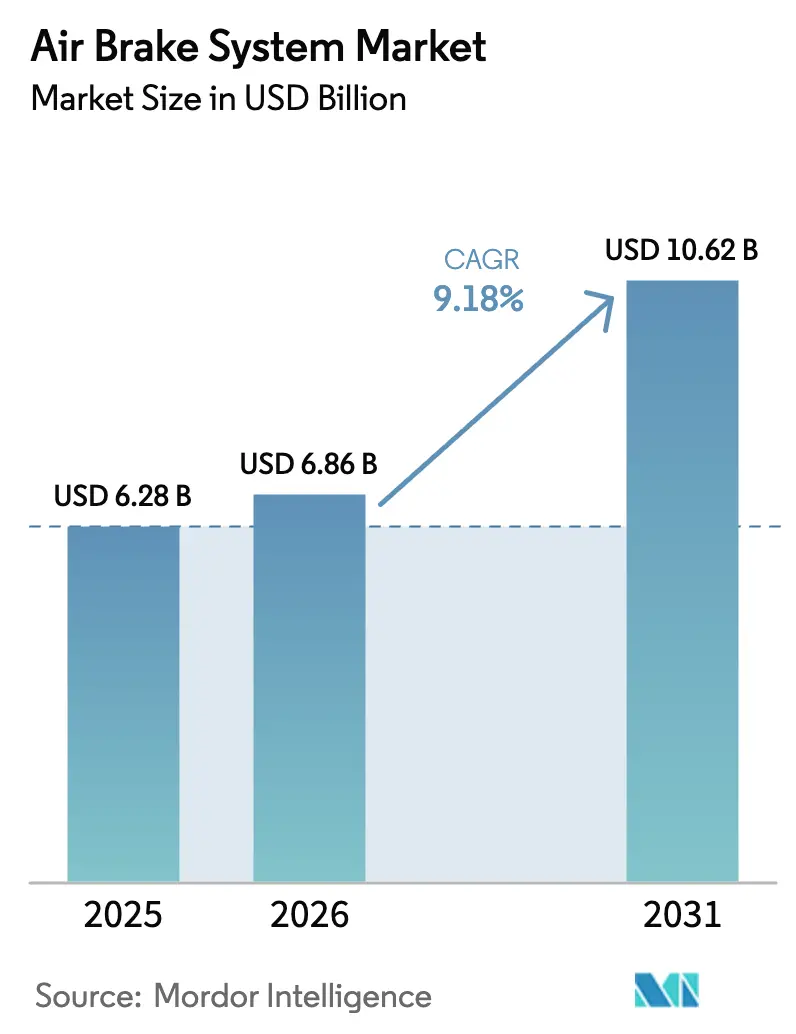

| Market Size (2026) | USD 6.86 Billion |

| Market Size (2031) | USD 10.62 Billion |

| Growth Rate (2026 - 2031) | 9.18% CAGR |

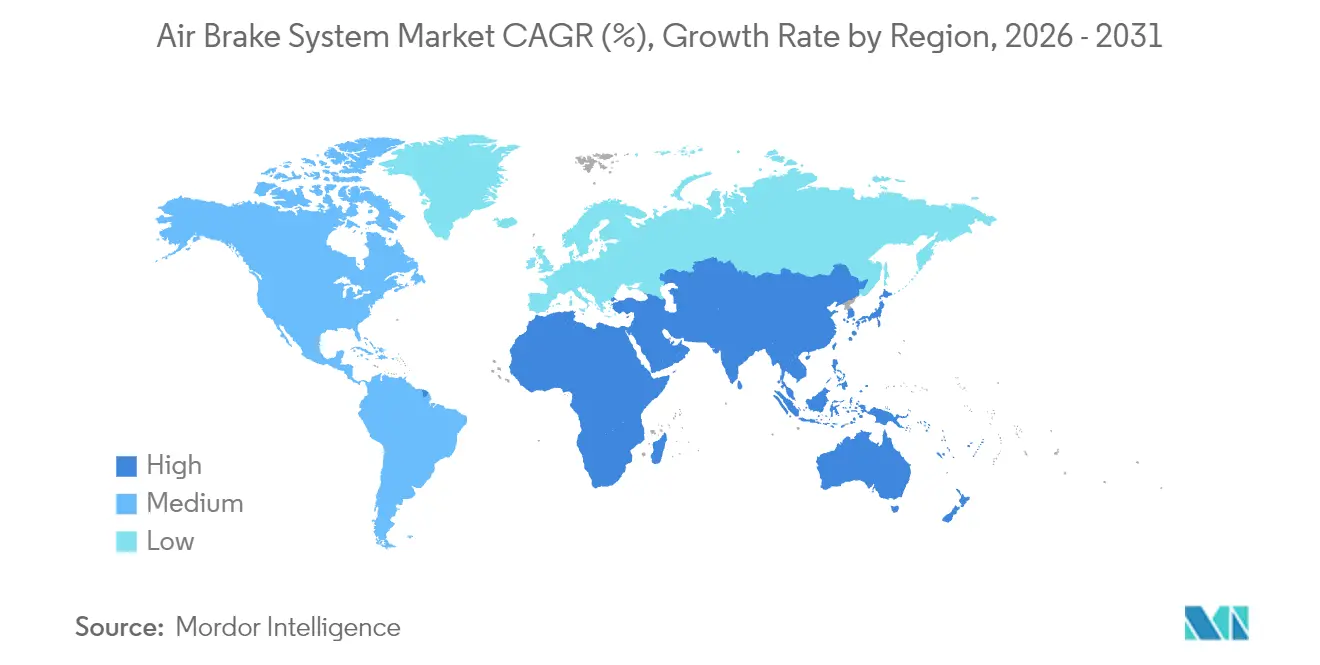

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

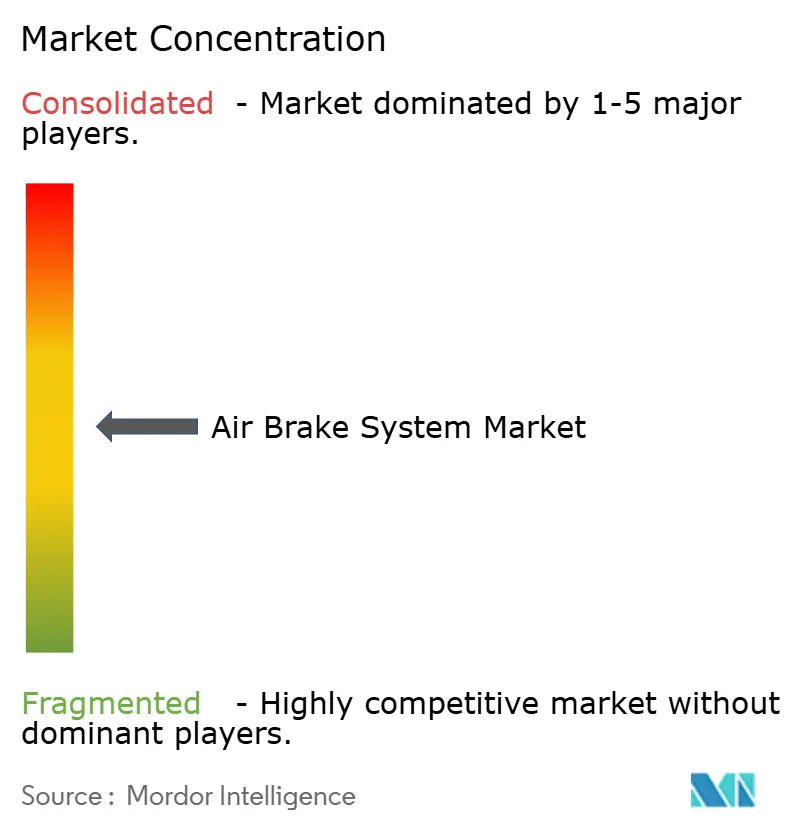

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Air Brake System Market Analysis by Mordor Intelligence

The global Air Brake Systems market size was valued at USD 6.28 billion in 2025 and estimated to grow from USD 6.86 billion in 2026 to reach USD 10.62 billion by 2031, at a CAGR of 9.18% during the forecast period (2026-2031). Regulatory catalysts such as the United States Environmental Protection Agency’s Phase 3 greenhouse-gas standards for heavy-duty vehicles, which begin with model year 2027, are accelerating OEM investment in electropneumatic architectures supporting diesel and zero-emission powertrains. Integration of advanced driver assistance systems (ADAS) has further raised precision-braking requirements, pushing suppliers to develop electronic control units (ECUs) and sensor suites that synchronize with automatic emergency braking (AEB) functionality. Compressor redesign shifting from engine-driven to electric cuts parasitic losses and readies vehicles for hydrogen fuel-cell or battery-electric operation. These technology inflections, coupled with fleet demand for lower total cost of ownership, are reshaping competitive dynamics and tipping procurement choices toward disc-brake or hybrid configurations in long-haul applications across every major air brake systems market region.

Key Report Takeaways

- By brake type, air drum brake systems led with 45.78% of the air brake systems market share in 2025, while electropneumatic solutions posted the fastest 8.55% CAGR to 2031.

- By vehicle type, light commercial vehicles captured 34.88% of the air brake systems market revenue in 2025; heavy-duty trucks are projected to grow at a 7.52% CAGR through 2031.

- By component, compressor systems commanded a 30.92% share of the air brake systems market size in 2025; ECUs & sensors are on track for a 13.05% CAGR to 2031.

- By sales channel, OEM installations retained 67.48% of the air brake systems market size in 2025 as the aftermarket expands at a 9.94% CAGR, given aging fleets and electronic component complexity.

- By geography, Asia-Pacific held 44.83% of the air brake systems market share in 2025, whereas Africa is forecast to register a 9.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Air Brake System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification-Ready Pneumatic Architectures | +2.1% | Global; strongest in the EU & California | Medium term (2-4 years) |

| Regulatory Push for Zero-Emission Heavy Trucks | +1.8% | North America & EU, expanding into APAC | Long term (≥ 4 years) |

| Rising Adoption of ADAS Requires Higher-Precision Braking | +1.5% | Global, led by developed markets | Short term (≤ 2 years) |

| Fleet Demand for Total-Cost-of-Ownership Reduction Via Air-disc Conversion | +1.2% | North America & EU; emerging in APAC | Medium term (2-4 years) |

| Smart Compressor Integration With Telematics | +0.8% | Global; early uptake in North America | Short term (≤ 2 years) |

| Hydrogen Fuel-Cell Truck Programs Need Oil-Free Air Supply | +0.6% | EU & California; pilots in Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification-Ready Pneumatic Architectures

OEMs are re-engineering brake systems so the pneumatic circuit integrates seamlessly with battery-electric and hydrogen fuel-cell drivetrains. ZF secured orders to deploy brake-by-wire hardware across nearly 5 million vehicles, proving large-scale viability and giving fleets an immediate path to regenerative braking compatibility[1]“ZF Wins Brake-by-Wire Order for 5 Million Vehicles,”, ZF Friedrichshafen AG, zf.com. Canada’s support of VMAC’s high-voltage compressor program signals national prioritization of electric auxiliary components. Electric compressors eliminate crankshaft drag, improving range and lowering carbon intensity, while integrated thermal-management software coordinates regenerative and friction braking to avoid heat buildup during repeated stops. As these systems migrate from pilot fleets in Europe to series production worldwide, suppliers that master modular electric compressor platforms will secure recurring software-update revenue streams throughout the air brake systems market.

Regulatory Push for Zero-Emission Heavy Trucks

The EPA’s Phase 3 standards target a 25% reduction in carbon dioxide for Class 8 trucks by 2032 and dovetail with California’s Advanced Clean Trucks regulation, forcing manufacturers to redesign pneumatic systems for oil-free operation[2]“Greenhouse Gas Emissions Standards for Heavy-Duty Vehicles Phase 3,”, Environmental Protection Agency, epa.gov. The European Union’s CO₂ standards echo these targets and embed compliance incentives that reward vehicles with energy-efficient braking. Suppliers must therefore substitute lubricated compressors with dry-running units while enlarging air-storage capacity to balance fluctuating demands from electric regenerative cycles. Regulatory clarity over a 10-year horizon encourages fleet pre-orders of hydrogen prototypes, pushing the air brake systems market toward faster adoption of electropneumatic valves that maintain precise pressure at lower duty cycles.

Rising Adoption of ADAS Requires Higher-Precision Braking

NHTSA’s proposed rule mandating AEB for trucks above 10,000 lb GVWR seeks to avert more than 19,000 annual crashes and compels brake actuation within milliseconds during an imminent collision [3]“Notice of Proposed Rulemaking for Automatic Emergency Braking in Heavy Vehicles,”, National Highway Traffic Safety Administration, nhtsa.gov. The EU General Safety Regulation, effective July 2024, mirrors these functional outcomes, creating harmonized test protocols across continents. Freightliner’s fifth-generation Cascadia integrates brake-by-wire logic alongside a backup pneumatic circuit, showcasing redundancy that satisfies both functional-safety and cybersecurity standards[4]“Next-Generation Freightliner Cascadia Debuts with Intelligent Braking,”, Daimler Truck AG, daimlertruck.com. These requirements lift ECU shipments and encourage the placement of additional wheel-end sensors, directly expanding revenue potential across the air brake systems market.

Fleet Demand for Total-Cost-of-Ownership Reduction Via Air-disc Conversion

Extended brake-shoe life, faster pad changes, and superior fade resistance make air disc brakes attractive to for-hire carriers in the air brake system market. Operators cite reduced downtime during pad swaps and greater confidence on mountainous grades, which boosts residual values. Conversion momentum is spreading into trailers and rigid vocational vehicles in emerging Asian markets, translating into aftermarket demand for stainless-steel caliper upgrade kits and ceramic pad formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Maintenance Cost Of Air-Brake Lines & Valves | -1.4% | Global; elevated burden in emerging markets | Short term (≤ 2 years) |

| Disc-Brake Heat-Fade Issues In Tropical Climates | -0.9% | Southeast Asia & Africa | Medium term (2-4 years) |

| Supply-Chain Crunch For Cast-Iron Components | -0.7% | North America & EU | Short term (≤ 2 years) |

| Cybersecurity Risks In Electronically Controlled Braking | -0.5% | Developed markets with high telematics penetration | Medium term (2-4 years |

| Source: Mordor Intelligence | |||

High Maintenance Cost of Air-brake Lines and Valves

The growing count of electronically modulated valves and sensors raises workshop bills, especially in fleets that lack calibrated diagnostic tools. Knorr-Bremse expanded aftermarket revenue to 30.1% of commercial-vehicle sales during 2024, highlighting rising service demand knorr-bremse.com. Bendix’s ACom AE tool offers fault-code overlays for global scalable air-treatment modules, but technicians require new certifications, which limits adoption velocity in emerging economies. Higher-specification nylon hoses, moisture separation cartridges, and firmware licensing fees add recurring costs that temper the near-term growth of the air brake systems market.

Disc-brake Heat-fade Issues in Tropical Climates

Brake-disc temperatures can exceed 400°C in stop-and-go driving, as thermal-modeling studies demonstrate. Persistent humidity and ambient temperatures above 40°C reduce cooling rates, leading to pad glazing and rotor micro-cracks. Fleets in Southeast Asia and sub-Saharan Africa report more frequent pad replacement versus temperate regions, prompting operators to stick with drum brakes that shed heat through mass rather than surface convection. Suppliers are trialing silicon-carbide rotors and vented splash shields, yet the incremental cost slows conversion and dampens regional uptake within the air brake systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Brake Type: Electropneumatic Systems Accelerate Market Shift

Air drum brake designs retained 45.78% of the air brake systems market size in 2025, reflecting cost efficiency and widespread service familiarity. Disc variants penetrated long-haul tractors after NHTSA’s stricter stopping-distance rule but still sit below drums in absolute volume. The electropneumatic subset, although only a fraction today, is growing fastest at an 8.55% CAGR as AEB, lane-keeping, and platooning pilots demand millisecond-level pressure modulation. Hybrid drum-disc configurations fill a transitional niche for fleets that want disc performance on steer axles yet still rely on lower-maintenance drums on drive axles. Because precision controllers can trim air consumption by 15%, electropneumatic solutions are drawing interest from battery-electric chassis that must conserve auxiliary energy, broadening their relevance across the air brake systems industry.

Traditional drum platforms are not standing still. Large cast-iron suppliers are machining weight-optimized webs to offset the barrel-shaped mass penalties that hamper fuel economy. Conversely, disc advocates emphasize rotor offset designs and bolt-on caliper modules that accelerate pad swaps, claiming 25% labor reduction per wheel end. From 2026 to 2031, retrofit kits featuring electronic slack-adjuster sensors are forecast to lift aftermarket revenue, enabling meaningful cross-selling of data analytics to predict lining wear. This interplay suggests a balanced coexistence, yet the value pool will migrate toward software-supported disc and electropneumatic variants, keeping the air brake systems market in flux for the rest of the decade.

By Vehicle Type: Heavy-Duty Trucks Pull Technology Adoption Forward

Light commercial vehicles represented the largest 34.88% slice of the 2025 air brake systems market size, owing to urban delivery growth, especially in Asia’s e-commerce corridors. Frequent stop-start duty cycles demand rapid pressure recovery, driving OEM preference for two-stage compressors paired with modular air-dryers. Though lower in unit sales, heavy-duty trucks are forecast to expand at 7.52% CAGR, underpinned by zero-emission targets that obligate oil-free compressors, redundant ECUs, and high-accuracy pressure sensors. The segment also acts as an innovation incubator: Daimler’s 600 kWh eActros 600 adopts blended regenerative and friction braking, which forces suppliers to fine-tune air-pressure thresholds based on battery state of charge.

Rigid vocational vehicles and dump trucks often operate in dusty, abrasive environments that shorten disc-seal life, making a role for self-adjusting drum assemblies. Buses and coaches prioritize passenger comfort and safety, adopting electropneumatic logic that minimizes pitch during panic stops. Off-highway and mining haulers require high-capacity dual-circuit chambers rated beyond 30 bar, with sealed slack adjusters that withstand mud ingress. Broadening use-cases across every class ensures that product portfolios must remain modular, defending margins as the air brake systems market diversifies by duty cycle and regulatory overlay.

By Component: Electronic Control Units Anchor Digital Transformation

Compressor systems still held 30.92% of the air brake systems market share in 2025, but that lead is narrowing as the spotlight shifts to software-defined ECUs. Electronic control units and sensors are outpacing all other components with a 13.05% CAGR because they mediate data between ADAS radars, telematics gateways, and wheel actuators. Governor valves are integrating MEMS pressure transducers, creating closed-loop circuits that automatically compensate for altitude and humidity fluctuations. Storage tanks now ship with RFID tags that log cycle counts, feeding fleet management platforms with real-time health scores.

Slack-adjuster manufacturers have developed integrated wear indicators, enabling visual inspection without invasive measurements, a boon for technicians operating strict roadside inspection windows. Brake chambers, once a mature commodity, are being re-engineered with composite housings to shave 20% weight, improving payload. Together, these innovations raise the electronics content per axle and translate into a higher average-selling price, positioning the electronic component tier as the profit engine of the air brake systems industry for the rest of the decade.

By Sales Channel: Aftermarket Revenue Rises with System Complexity

OEM fitment dominated at 67.48% of the air brake system market share in 2025 because electropneumatic valves and sensor fusion routines must be calibrated before the vehicle leaves the assembly line. Yet the aftermarket is growing quicker at 9.94% CAGR as fleets extend asset life amid high new-truck prices and prioritize predictive maintenance. Sensor fault codes, valve recalibrations, and over-the-air firmware renewals are recurring revenue streams for suppliers like Bendix, which broadened its training academy footprint to narrow the technician skills gap. For parts distributors, stocking policies are shifting from bulk drums and shoes to smaller, higher-margin electronic modules that require climate-controlled storage.

Remanufactured compressors with upgraded brushless motors present an attractive lower-cost option for mid-life overhauls, and this sub-segment is starting to cannibalize new-part demand in North America. In developing regions, gray-market valves and counterfeit ECU housings remain challenging; however, regulatory crackdowns and stricter warranty enforcement are expected to steer buyers back toward authorized channels. Overall, rising system sophistication will prevent price erosion and sustain double-digit value growth on the aftermarket side of the air brake systems market.

Geography Analysis

Asia-Pacific controlled 44.83% of the air brake systems market in 2025, anchored by China’s outsized commercial-vehicle production and India’s sprawling highway modernization. Chinese OEMs are quickly integrating ECUs and dry compressors to backstop the country’s 2030 electrification quotas, while Japanese tier-ones supply precision sensors that feed predictive-maintenance dashboards. In Southeast Asia, the tropical climate challenges disc-brake cooling, prompting joint-development programs between suppliers and local assemblers to customize rotor coatings and vent geometries.

Africa, though starting from a modest base, is forecast to post a 9.88% CAGR through 2031in the air brake system market due to rapid urbanization, mining-sector expansion, and pan-African trade corridors that demand modern trucks with reliable braking. South Africa and Nigeria are spearheading regulatory harmonization, gradually raising brake-performance standards to align with ECE R13 provisions. Disc-fade concerns under high ambient heat have slowed advanced-brake deployment, but pilot fleets in Kenya are trialing hybrid drum-disc setups paired with water-piqued cooling shields to mitigate temperature spikes.

North America and Europe exhibit mature but technology-intensive demand patterns. EPA Phase 3 and the EU’s zero-emission mandates compel a shift toward electropneumatic brake-by-wire architectures, fostering premium pricing. The retrofit market remains vibrant because tightening AEB and lane-departure regulations apply to in-service vehicles, guaranteeing recurring revenue. Supply-chain kinks for cast-iron drums and valves were pronounced in 2024, yet capacity additions in Mexico and Eastern Europe are easing bottlenecks. Consequently, the air brake systems market will mirror regional policy stringency, technology readiness, and climate considerations across these three economic blocs.

Competitive Landscape

The air brake systems market is moderately concentrated, with the top tier distinguished by system-integration know-how and global production footprints. Cummins’ absorption of Meritor’s braking portfolio in 2024 formed a vertically integrated powertrain giant capable of synchronizing engine, transmission, and brake parameters, adding cross-component torque management advantages[5]“Cummins Completes Acquisition of Meritor,”, Cummins Inc., cummins.com.

ZF Friedrichshafen AG’s strategic realignment centers on brake-by-wire, leveraging synergies from its chassis-control lineage to win multi-year contracts covering almost 5 million vehicles. Hendrickson’s 2024 acquisition of Motor Wheel and Crewson improved its wheel-end breadth while preserving backward compatibility for aftermarket customers. On the innovation fringe, Canadian firm VMAC Global Technology Inc. commercializes 800-V electric compressors to serve niche battery-electric chassis segments, illustrating a pathway for specialized entrants in the air brake system market. Cybersecurity is emerging as a white-space battleground as fleets seek intrusion-resilient ECU firmware; university-led penetration tests exposed vulnerabilities in electronic logging devices that can jump via Wi-Fi, spurring joint task forces with Tier 1 suppliers.

Margins hinge on securing long-term supply agreements that bundle hardware, software, and over-the-air update services. The largest players use scale to lock in raw-material contracts, buffering against cast-iron price volatility, while medium-sized firms differentiate via region-specific application engineering. Collectively, these dynamics keep the competitive intensity high and preserve room for technological differentiation within the air brake systems industry.

Air Brake System Industry Leaders

ZF Friedrichshafen AG

Knorr-Bremse AG

Haldex AB

Wabtec Corporation

Cummins Inc. (Meritor Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Cummins showcased an integrated heavy-duty powertrain, combining the X15 Euro 6 engine, Endurant transmission, and Meritor brake modules into a unified high-performance package.

- March 2025: ZF announced a significant order to integrate brake-by-wire systems into nearly 5 million vehicles, emphasizing the commercial readiness of electropneumatic control architectures.

- February 2025: Daimler Truck introduced the fifth-generation Freightliner Cascadia, an advanced vehicle equipped with the innovative Intelligent Braking Control System. This system integrates the precision of brake-by-wire technology with a pneumatic backup, providing enhanced safety and reliability through an additional layer of redundancy. The Freightliner Cascadia exemplifies cutting-edge engineering, representing a significant step forward in heavy-duty truck performance and safety standards.

- February 2025: VMAC introduced a groundbreaking series of High-Voltage Electric Vehicle air-brake compressors, marking a pivotal leap in automotive technology. The Canadian government has injected a hefty USD 2.28 million in federal funding, propelling the swift commercialization of these cutting-edge compressors. This financial backing highlights a deepening dedication to advancing the electric vehicle sector and refining braking systems, ensuring a safer and more efficient driving journey.

Global Air Brake System Market Report Scope

Air brake systems utilize compressed air to put pressure on the brake pads, effectively slowing down or stopping a vehicle. They are widely used in commercial vehicles and railways. The driver's foot pressure activates the system through a tensile diaphragm located inside a brake chamber.

The air brake system market is segmented by brake type, vehicle type, component, and geography. The market is segmented by Brake Type into drum air brakes and disc air brakes. The market is segmented by vehicle type into rigid-body trucks, heavy-duty trucks, semi-trailer tractors, buses, and others. By component, the market is segmented into compressor, governor, storage tank, slack adjuster, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, the market sizing and forecast have been done based on the value (USD).

| Drum Air Brake |

| Disc Air Brake |

| Hybrid Drum-Disc Systems |

| Electropneumatic (E-PBS) |

| Light Commercial Vehicles |

| Medium-Duty Trucks |

| Heavy-Duty Trucks |

| Buses & Coaches |

| Off-Highway & Mining Trucks |

| Compressor |

| Governor & Valves |

| Storage Tank |

| Slack Adjuster |

| Brake Chamber |

| Electronic Control Unit & Sensors |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Kenya | |

| Morocco | |

| Algeria | |

| Rest of Africa |

| By Brake Type | Drum Air Brake | |

| Disc Air Brake | ||

| Hybrid Drum-Disc Systems | ||

| Electropneumatic (E-PBS) | ||

| By Vehicle Type | Light Commercial Vehicles | |

| Medium-Duty Trucks | ||

| Heavy-Duty Trucks | ||

| Buses & Coaches | ||

| Off-Highway & Mining Trucks | ||

| By Component | Compressor | |

| Governor & Valves | ||

| Storage Tank | ||

| Slack Adjuster | ||

| Brake Chamber | ||

| Electronic Control Unit & Sensors | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Kenya | ||

| Morocco | ||

| Algeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the global air brake systems market?

The air brake systems market is valued at USD 6.86 billion in 2026.

Which region holds the largest share of the air brake systems market?

Asia-Pacific leads with 44.83% of global revenue, bolstered by China’s commercial-vehicle output and India’s logistics expansion.

Why are electropneumatic brake systems gaining momentum?

They support ADAS, automatic emergency braking mandates, and zero-emission powertrains, driving the segment’s 8.55% CAGR.

What regulations are shaping future demand for advanced air brake technologies?

EPA Phase 3 greenhouse-gas rules in the United States, California’s Advanced Clean Trucks regulation, and the EU General Safety Regulation are compelling fleets to adopt precision, oil-free braking solutions.

How is aftermarket demand likely to evolve?

Aging fleets and the rising complexity of ECUs and sensors are pushing the aftermarket channel to grow at a 9.94% CAGR through 2031.

Page last updated on: