Motorcycle Advanced Rider Assistance System Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

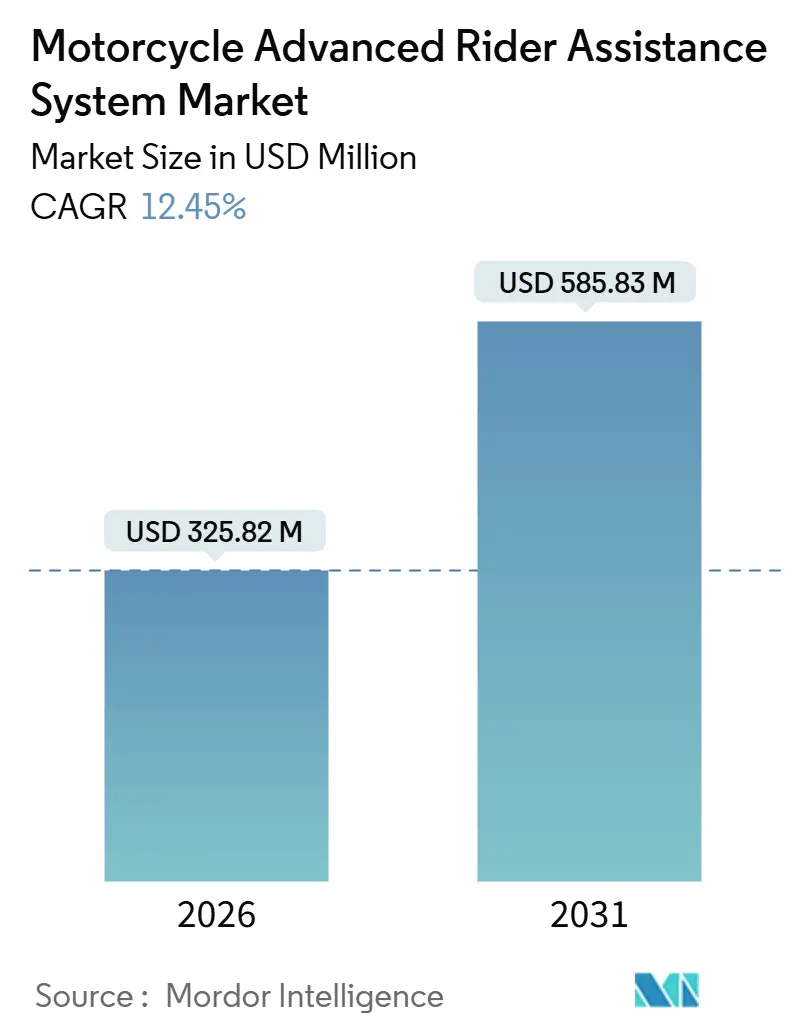

| Market Size (2026) | USD 325.82 Million |

| Market Size (2031) | USD 585.83 Million |

| Growth Rate (2026 - 2031) | 12.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Motorcycle Advanced Rider Assistance System Market Analysis by Mordor Intelligence

The motorcycle advanced rider assistance system market size stands at USD 325.82 million in 2026 and is projected to reach USD 585.83 million by 2031, advancing at an impressive 12.45% CAGR during the forecast period. Growth is powered by three converging forces: regulatory mandates that mandate collision-mitigation features on mid-displacement platforms, rapid declines in sensor costs that approach automotive parity, and original-equipment-manufacturer (OEM) platform-sharing programs that amortize radar and LiDAR integration across multiple model lines. Tier-1 suppliers now deliver 210-meter front-radar modules at price points viable for motorcycles above 500 cc, enabling mainstream touring and adventure models to debut adaptive cruise control, forward-collision warnings, and emergency-braking assist. India’s draft G.S.R. 415(E) requires anti-lock braking systems (ABS) on L2 motorcycles, laying a sensor and electronic-control foundation that accelerates advanced rider-assist rollouts[1]Ministry of Road Transport and Highways, “G.S.R. 415(E) – Draft ABS Requirements for L2-Category Motorcycles,” Government of India, morth.nic.in. Meanwhile, Europe’s Euro 7 framework mandates on-board monitoring and anti-tampering measures, which indirectly spur demand for electronic control units (ECUs) capable of executing multiple rider-assist algorithms.

Key Report Takeaways

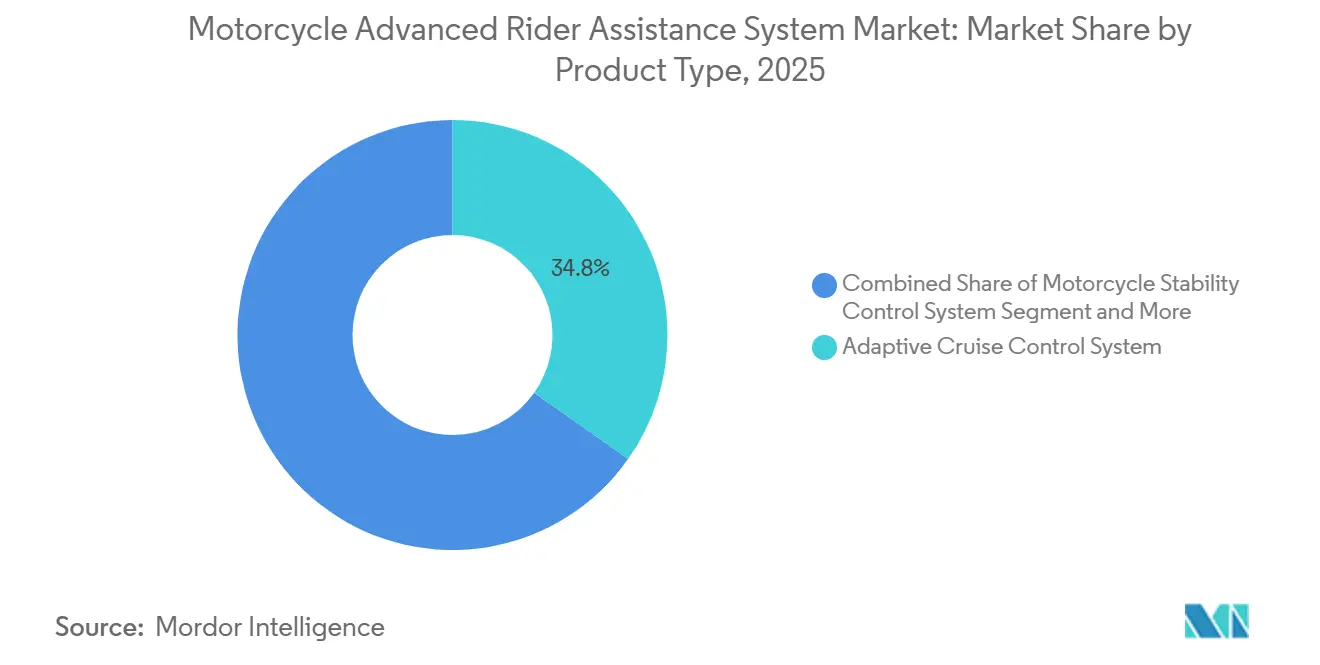

- By product type, adaptive cruise control systems accounted for 34.79% of the motorcycle advanced rider assistance system market share in 2025, while forward-collision warning systems are forecast to expand at a 15.04% CAGR through 2031.

- By sensor, radar captured 32.74% of the motorcycle advanced rider assistance system market share in 2025; LiDAR is projected to grow at a 18.42% CAGR between 2026 and 2031.

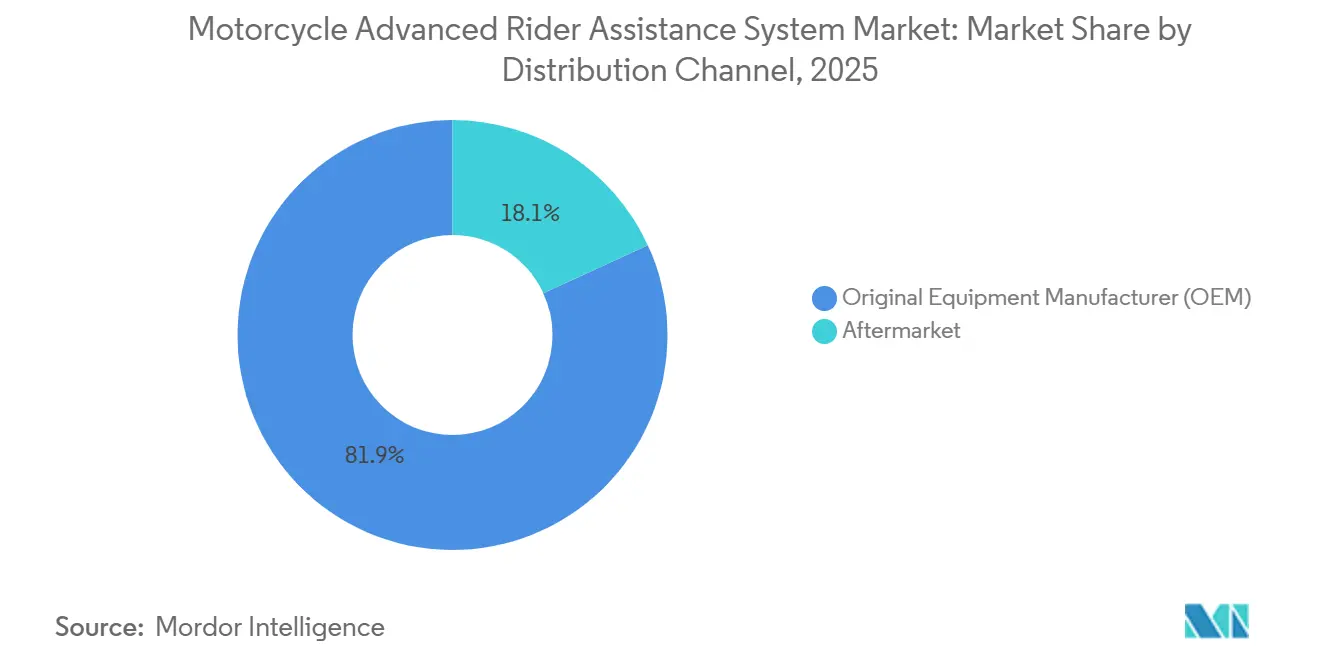

- By distribution channel, OEM sales commanded 81.86% of the motorcycle advanced rider assistance system market share in 2025, yet aftermarket retrofits are set to grow at a 13.52% CAGR through 2031.

- By component, electronic control units accounted for 38.88% of the motorcycle advanced rider assistance system market share in 2025, whereas gear assistors will grow at a 14.07% CAGR through 2031.

- By geography, Europe led with 31.72% of the motorcycle advanced rider assistance system market share in 2025, and Asia-Pacific is forecasted to record the fastest 13.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Motorcycle Advanced Rider Assistance System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining LiDAR Sensor Pricing | +2.8% | Global, with early adoption in Europe and Asia-Pacific premium segments | Medium term (2-4 years) |

| ARAS Suites | +2.5% | Europe, Asia-Pacific (India, China, ASEAN), North America | Medium term (2-4 years) |

| Premium Touring and Adventure Bikes | +2.2% | ASEAN (Thailand, Vietnam, Indonesia, Philippines), spill-over to India | Long term (≥ 4 years) |

| Motorcycle-Safety Mandates | +2.0% | Europe (Euro 7), India (BS6/draft BS7 ABS mandates), ASEAN (harmonization) | Short term (≤ 2 years) |

| V2X-Enabled OTA Updates | +1.5% | Global, with pilot deployments in Europe, North America, and China | Long term (≥ 4 years) |

| Telematics Discounts | +1.2% | Europe (Greece, Italy), North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline in Motorcycle LiDAR Sensor Pricing

Automotive-grade LiDAR modules cost significantly less than they did in 2015, allowing suppliers to offer solid-state units tailored for two-wheelers at prices that rival those of 77 GHz radar. The latest generation of Bosch front-radar achieves a 210-meter detection range, extending coverage by 50 meters relative to the prior unit and improving reaction time in touring scenarios. Chinese harmonization standard T/CECC 028-2024 defines six ARAS capability levels, pushing local OEMs to source modular sensors that drop seamlessly into cross-platform architectures. As premium touring and adventure motorcycles above 500 cc adopt these sensors, economies of scale further compress costs, accelerating adoption in lower price bands. The trajectory confirms a structural cost-advantage pathway that sustains double-digit growth for the motorcycle advanced rider assistance system market.

OEM Platform-Sharing to Embed ARAS Suites at Scale

Major motorcycle makers deploy standard frames, engines, and electronic systems across multiple models, enabling rider-assist hardware to spread across entire line-ups. A flagship case integrates adaptive cruise, group-ride assist, riding-distance assist, and emergency-brake assist within the same ECU and harness, cutting unit costs, engineering time, and certification fees. Yamaha Motor’s Advanced Motorcycle Stabilisation Assist System (AMSAS) illustrates in-house verticalization: a 6-axis inertial measurement unit (IMU) and dual actuators deliver low-speed balance control and seamlessly plug into existing YZF-R25 frames without chassis changes. Supplier–OEM collaborations built on automotive ISO 26262 toolchains shorten functional-safety validation, allowing rapid scale-ups across mid-displacement categories that dominate sales volumes in Asia-Pacific. Platform-sharing thereby locks in sustained demand for ARAS modules throughout the forecast period.

Rising Demand for Premium Touring and Adventure Bikes in ASEAN

Electrification targets in Thailand, Vietnam, and the Philippines are stimulating premium motorcycle purchases among consumers who value safety and connectivity over price. Electric powertrains typically operate on 48-V architectures, leaving ample headroom for continuous radar scanning, vision processing, and V2X communication. Regional sales of large touring and adventure models climbed sharply in early 2025 as riders sought lane-change assistance, blind-spot alerts, and adaptive cruise control to navigate crowded urban corridors and extended highway journeys. Local authorities encourage tech adoption through preferential registration fees and fleet electrification subsidies, thereby expanding the addressable market for the motorcycle advanced rider assistance system. With ASEAN riders traveling thousands of kilometers per year for leisure and commerce, demand for fatigue-reduction and collision-avoidance technologies is rising rapidly.

Stricter Euro 7 and Bharat Stage 7 Motorcycle-Safety Mandates

Europe’s Euro 7 regulation, phased from 2025, obliges on-board monitoring, driver warnings, and anti-tampering functions, nudging OEMs to integrate ECUs capable of multiple rider-assist tasks. India’s draft G.S.R. 415(E) proposes mandatory ABS on all L2 motorcycles, a pivotal prerequisite for forward-collision warning and emergency-braking assist. Convergence toward UN Regulation 171 on Direct Control Advanced Safety (DCAS) systems ensures standard global test protocols, shortening homologation times and lowering compliance costs. Functional-safety certification under ISO 26262 has become the baseline, further institutionalizing electronic rider-assistance across value chains. Collectively, these mandates embed ARAS features as standard equipment, immediately lifting penetration rates in the motorcycle advanced rider assistance system market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensor-Fusion Latency | -1.8% | Global, particularly affecting high-performance and sport-touring segments | Medium term (2-4 years) |

| Limited 12-V Electrical Headroom | -1.5% | Asia-Pacific (India, China, ASEAN), South America, Africa | Long term (≥ 4 years) |

| Consumer Privacy Concerns | -0.8% | Europe (GDPR), North America, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Retro-Fit Kit Regulatory Ambiguity | -0.6% | Europe, North America, with spill-over to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Sensor-Fusion Latency at Lean Angles

During steep cornering, motorcycles can exceed 45-degree lean angles, shifting the radar and camera fields of view away from the road ahead. Peer-reviewed work shows false-positive spikes and longer object-classification latency when roll, pitch, and yaw change rapidly, forcing conservative warning thresholds that diminish rider confidence. ISO 26262 demands sub-200-millisecond end-to-end latency, yet many multi-sensor stacks struggle to meet this standard under aggressive sport-riding. Bosch’s emergency-brake assist improves rear-end collision avoidance but raises rider-stability concerns when automatic braking triggers during active lean. Solving these physics-driven challenges requires adaptive algorithms that blend IMU data with predictive trajectory modeling, an R&D priority expected to take several product cycles.

Limited 12-V Electrical Headroom on Commuter Motorcycles

Most 100-cc to 150-cc commuter motorcycles rely on 12-V systems with power budgets under 300 W, leaving little margin for continuous radar (20–40 W), camera (30–50 W), and V2X (10–20 W) loads. Upgrading to 48-V architectures adds USD 150–200 in batteries and converters, exceeding the bill-of-materials targets for price-sensitive segments. New e-clutch ECUs add another 15–20 W, intensifying the power deficit. OEMs must either redesign electronics or wait for ultra-low-power sensors, slowing deployment in the highest-volume market bands and restraining overall expansion of the motorcycle advanced rider assistance system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Collision Mitigation Drives Near-Term Adoption

Adaptive cruise control systems, which held 34.79% of the motorcycle advanced rider assistance system market share in 2025, remain dominant thanks to touring riders who value automatic gap-keeping in mixed traffic. Forward-collision warning systems are projected to grow at 15.04% annually from 2026 to 2031, the quickest pace within product categories. Their ascent aligns with Euro 7 monitoring mandates and draft Indian ABS rules, pushing OEMs to embed front-radar modules coupled with predictive braking algorithms. Motorcycle stability control systems, integrating tilt-aware braking and traction management, expand as sensor costs fall and sport-touring customers demand corner-safe braking. Blind-spot detection, previously a passenger-car exclusive, is now available on high-trim adventure bikes that use rear radar to flag overtaking vehicles.

Niche features such as group-ride assist and riding-distance assist cater to organized touring communities and, though small today, illustrate the ecosystem’s shift from pure safety to convenience and social riding features. The product portfolio paints a two-track evolution. Collision-mitigation capabilities become baseline for regulatory compliance and insurance incentives, ensuring broad penetration across mid- and high-displacement motorcycles. Comfort-oriented features differentiate premium models, allowing OEMs to tier trim levels and sell subscription-based feature unlocks via OTA updates. Competitive positioning, therefore, hinges on a balanced offering that satisfies regulators, riders, and recurring-revenue ambitions inside the motorcycle advanced rider assistance system market.

By Sensor: LiDAR Gains as Automotive Volumes Drive Cost Curves

Radar modules held 32.74% of the motorcycle advanced rider assistance system market share in 2025 due to proven all-weather performance and a relatively low cost. Yet LiDAR revenue is forecast to rise at an 18.42% CAGR as solid-state designs fall below USD 200, providing motorcycles with 3-D point clouds that improve lane-merging and rear-collision estimation accuracy. Image sensors remain hampered by limited mounting options and exposure to glare, rain, and vibration, although machine-learning-enhanced de-noising now salvages more frames for algorithmic use. Ultrasonic sensors, useful at distances of less than 5 meters, remain confined to parking-assist add-ons. Infrared night-vision remains a luxury option for a small subset of long-distance touring bikes.

Technological convergence steers the sector toward radar-centric arrays complemented by LiDAR for high-resolution mapping and cameras for visual classification. Standard-setting bodies encourage harmonized sensor suites, reducing bespoke engineering and securing multi-vendor supply resilience. Continued automotive volume drives down costs, ensuring sensor diversification without jeopardizing profit margins inside the motorcycle advanced rider assistance system market.

By Distribution Channel: Aftermarket Gains as Retrofit Clarity Improves

OEMs commanded 81.86% of the motorcycle advanced rider assistance system market share in 2025 because clean-sheet integration better meets type-approval hurdles, functional-safety validation, and CAN bus messaging demands. Yet aftermarket solutions are projected to climb at 13.52% CAGR through 2031, propelled by startups offering adhesive radar pods and camera kits that link to smartphone dashboards. Regulatory bodies now draft inspection manuals that outline wiring, mounting, and diagnostic-trouble-code requirements, lowering barriers for third-party installers.

Riders of older or low-trim motorcycles, especially in emerging Asian megacities, value bolt-on blind-spot, forward-collision, and lane-change warning functions that raise daily commute safety without new-bike expenditures. Over time, an ecosystem of certified installers, telematics insurers, and ride-share operators will broaden aftermarket reach. However, OEM dominance will remain in premium touring and adventure segments where ARAS features arrive factory-fitted, software-activated, and bundled with extended warranties. The interplay between factory-installed systems and aftermarket kits underpins the continued expansion of the motorcycle advanced rider assistance system market.

By Component: Gear Assistors Surge as E-Clutch ECUs Enable Automation

Electronic control units accounted for 38.88% of the motorcycle advanced rider assistance system market share in 2025, serving as the fusion hub for sensor inputs and actuator commands. Their share gradually tapers as ECUs shift from high-margin stand-alone boxes to commoditized network nodes that leverage over-the-air updates for feature unlocks. Gear assistors, driven by the advent of electronic clutches, will increase at a 14.07% CAGR; automated clutch actuation integrates seamlessly with stop-and-go adaptive cruise and hill-start assist, reducing rider fatigue in congested traffic. Sensor modules drop in absolute price but maintain healthy value contribution, driven by rising volume and multi-sensor arrays on high-end models.

Ancillary components, actuators, harnesses, and power-management units must evolve toward ultra-low-watt designs to fit 12-V commuter motorcycles, reinforcing R&D investments in miniaturization. As automation deepens, the component hierarchy rearranges: software-defined ECUs become the subscription gateway. At the same time, gear assistors translate algorithms into tactile rider benefits such as smoother shifts and clutch-free low-speed maneuvers. This evolution cements a robust revenue mix, sustaining the broader motorcycle advanced rider assistance system market.

Geography Analysis

Europe controlled 31.72% of the motorcycle advanced rider assistance system market share in 2025 and is projected to expand at 9.78% through 2031. The continent’s strict Euro 7 mandates obligate on-board monitoring and data logging, pushing OEMs to embed multi-sensor ECUs and advanced diagnostics[2]“Regulation (EU) 168/2013 – Type-Approval for L-Category Vehicles,” European Union, eur-lex.europa.eu. Premium brands headquartered in Germany, Italy, and Austria equip touring and adventure models with adaptive cruise, blind-spot detection, and emergency-brake assist as standard, ensuring regulatory compliance while meeting consumer expectations. Data-privacy directives under Europe’s GDPR prompt software features such as local video storage, consent screens, and automatic anonymization, adding cost but also boosting user trust. Insurance carriers accelerate uptake by offering double-digit policy discounts for ARAS-equipped bikes, reinforcing a virtuous cycle of safety and commercial incentives.

Asia-Pacific is forecast to grow at a 13.15% CAGR through 2031, the fastest worldwide. India’s impending ABS requirement for L2 motorcycles, China’s six-tier intelligence classification, and expanding electrification targets across Southeast Asia jointly create the ideal conditions for rider-assist proliferation. Local producers scale sensor packages into commuter and sport models, leveraging regionally low labor and manufacturing costs to hit sub-USD 150 sensor unit thresholds. Japanese OEMs now integrate traction control and tilt-aware braking across mid-displacement offerings, while Chinese automotive brands migrating into high-end motorcycles port over car-grade digital cockpits and ADAS stacks. As charging infrastructure for electric bikes improves, 48-V architectures unlock ample electrical headroom, enabling the integration of radar and LiDAR on mainstream platforms.

North America advances at 8.88% owing to an entrenched motorcycle touring culture and insurance telematics incentives that slash premiums by as much as half for ARAS-equipped riders. Stateside regulators adopt UN DCAS protocols to harmonize testing, simplifying OEM homologation for cross-Atlantic models. Western Asia posts an 11.61% rise amid affluent consumers in the Gulf who favor premium touring machines with lane-change and blind-spot alerts for long stretches of highway. South America, Africa, and Russia lag, with premium-segment penetration remaining limited and homologation pathways for retrofit kits still in development. Even so, improving disposable income and early pilots of safety features hint at latent demand that could accelerate should financing and regulatory clarity emerge.

Competitive Landscape

The motorcycle advanced rider assistance system market shows moderate concentration: Bosch and Continental lead, yet newcomer dynamics indicate future dilution. Bosch deploys ISO 26262-compliant ARAS suites developed initially for automobiles, using standard radar hardware across passenger-car and motorcycle lines to maximize scale economies. Continental, meanwhile, targets fast-growing Asian markets, leveraging local production to achieve competitive price points suitable for mid-displacement bikes.

Vision-centric startup Roadio offers camera-based retrofit kits that deliver forward-collision and lane-deviation warnings through smartphone dashboards, bypassing proprietary CAN bus interfaces and appealing to tech-savvy riders upgrading older motorcycles. Yamaha Motor’s integrated innovation strategy under its “Jin-Ki Kanno x Jin-Ki Anzen” vision leverages robotics, artificial intelligence, and sensor expertise to develop proprietary rider-assist features. The firm’s AMSAS prototype stabilizes motorcycles at walking pace with coordinated drive and steering actuators, a differentiator unmatched by traditional Tier-1s[3]“Yamaha Motor Co., Ltd. Integrated Report 2024,” Yamaha Motor, yamaha-motor.com.

Automotive mega-suppliers ZF, Denso, and Autoliv signal entry, repurposing vast ADAS portfolios for two-wheeler dynamics and raising the bar for feature completeness. Standards harmonization via UN Regulation 171 favors firms with global certification capabilities, while limited 12-V power budgets spur a race for low-current radar chips and ultra-efficient ECUs. Competitive intensity is therefore projected to tighten, gradually redistributing share toward agile players that blend hardware scale, software over-the-air agility, and regional production footprints.

Motorcycle Advanced Rider Assistance System Industry Leaders

Continental AG

ZF Friendrichafen AG

Robert Bosch GmbH

BMW Motorrad

Denso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Ultraviolette Automotive launched the X47 dual-purpose motorcycle in India with “UV Hypersense,” a 77 GHz rear-facing radar that detects blind spots up to 200 meters.

- August 2025: Ola Electric unveiled the Diamondhead prototype, India’s first electric motorcycle, featuring advanced rider-assistance systems.

- June 2025: Luna Systems announced low-cost computer-vision rider-assist kits tailored for Indian road conditions, targeting mass-market commuter bikes.

Global Motorcycle Advanced Rider Assistance System Market Report Scope

The motorcycle advanced rider assistance system market has been segmented by product type, sensor, distribution channel, component, and geography. By product type, the market is segmented into adaptive cruise control systems, motorcycle stability control systems, forward-collision warning systems, blind spot detection systems, and other product types. By sensor, the market is segmented into LiDAR, image, ultrasonic, radar, and infrared. By distribution channel, the market is segmented into OEM and aftermarket. By component, the market is segmented into electronic control units, sensors, gear assistors, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle-East, and Africa. The report provides market size and forecasts in terms of value (USD).

| Adaptive Cruise Control System |

| Motorcycle Stability Control System |

| Forward Collision Warning System |

| Blind Spot Detection System |

| Other Product Types |

| LiDAR |

| Image |

| Ultrasonic |

| Radar |

| Infrared |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| Electronic Control Unit (ECU) |

| Sensors |

| Gear Assistors |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Adaptive Cruise Control System | |

| Motorcycle Stability Control System | ||

| Forward Collision Warning System | ||

| Blind Spot Detection System | ||

| Other Product Types | ||

| By Sensor | LiDAR | |

| Image | ||

| Ultrasonic | ||

| Radar | ||

| Infrared | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Component | Electronic Control Unit (ECU) | |

| Sensors | ||

| Gear Assistors | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the motorcycle advanced rider assistance system market in 2031?

The market is forecast to reach USD 585.83 million by 2031.

Which product category will expand the fastest by 2031?

Forward-collision warning systems are expected to grow at a 15.04% CAGR, the highest among product types.

Why is Asia-Pacific the fastest-growing region?

New safety mandates, rapid electrification, and cost-optimized platform-sharing spur a 13.15% CAGR across the region.

How do regulatory frameworks influence adoption?

Euro 7 and India’s draft ABS rules require electronic monitoring and braking infrastructure that make ARAS functions integral to compliance.

What technological hurdle most limits mass-market uptake?

Limited 12-V electrical capacity on commuter motorcycles constrains power-hungry radar and vision modules until ultra-low-power designs mature.

Page last updated on: