Bicomponent Fiber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

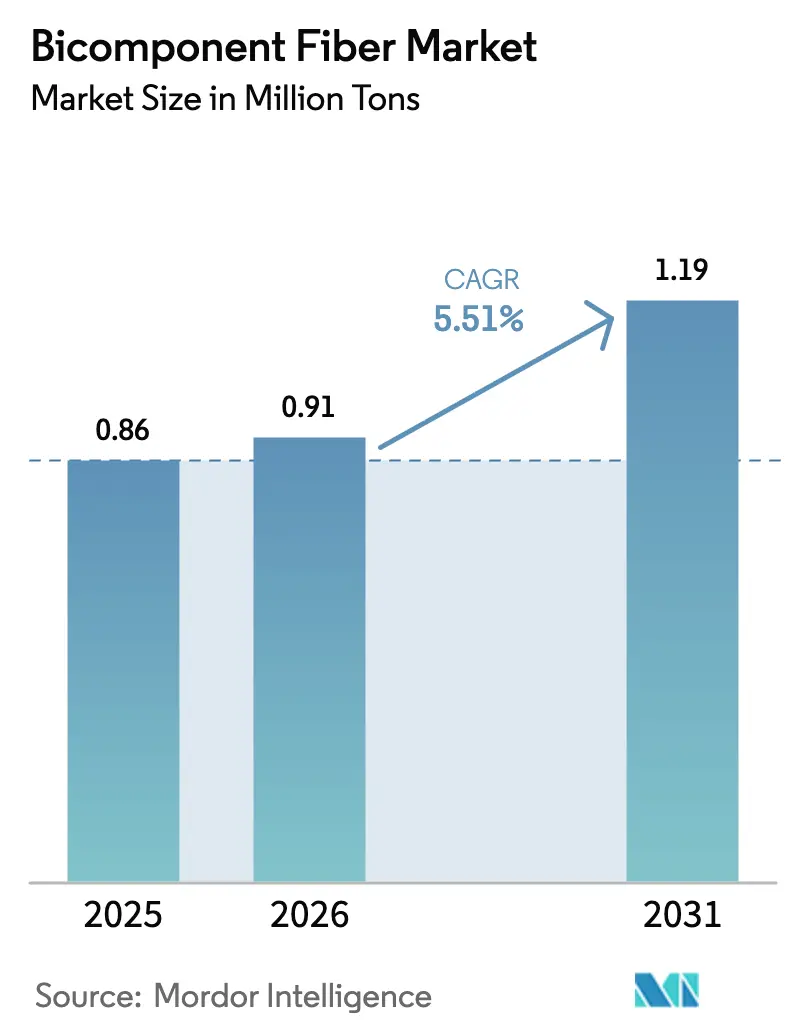

| Market Volume (2026) | 0.91 Million tons |

| Market Volume (2031) | 1.19 Million tons |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

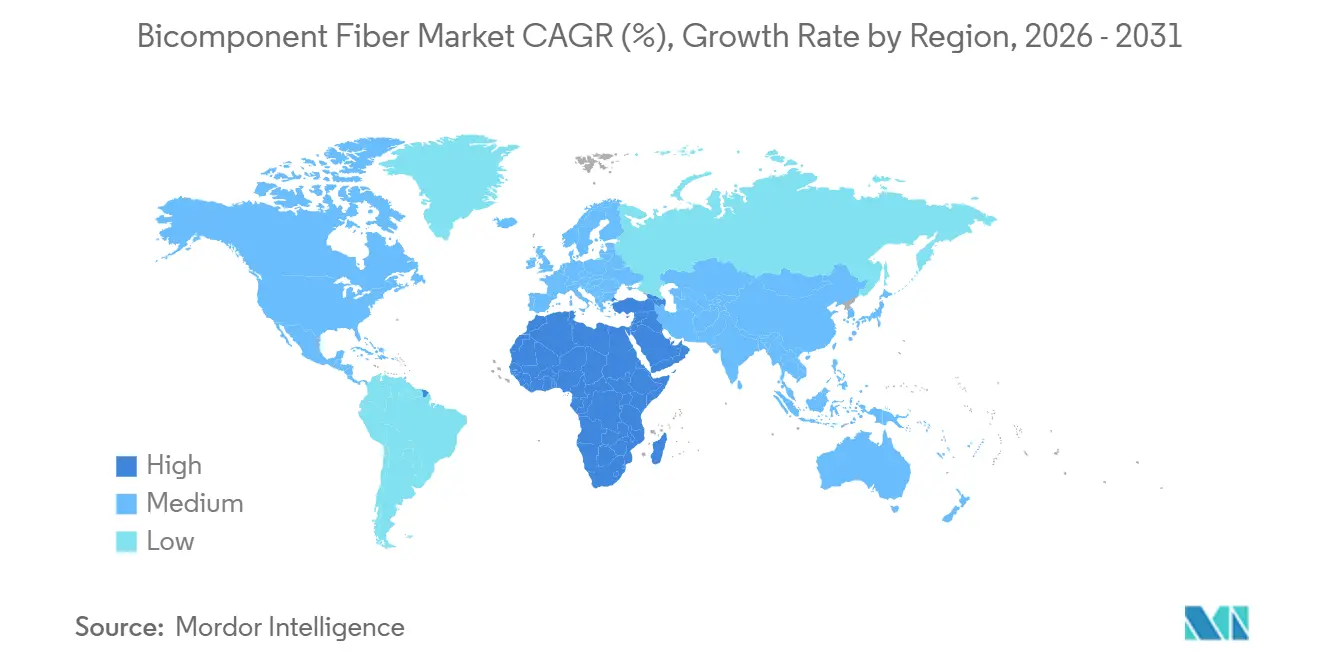

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bicomponent Fiber Market Analysis by Mordor Intelligence

The Bicomponent Fiber Market size is expected to increase from 0.86 million tons in 2025 to 0.91 million tons in 2026 and reach 1.19 million tons by 2031, growing at a CAGR of 5.51% over 2026-2031. Robust hygiene-product uptake across emerging economies, rising automotive demand for lightweight acoustic substrates, and regulatory incentives for recyclable textiles underpin this expansion. Polyethylene/Polypropylene (PE/PP) blends continue to anchor the bicomponent fiber market because their 30°C–40°C melt-point differential enables cost-effective thermal bonding, yet momentum is clearly shifting toward Polyethylene/Polyethylene Terephthalate (PE/PET) constructions that satisfy monomaterial recyclability targets in food packaging and battery separators. Islands-in-the-sea structures are emerging as the go-to solution for ultra-fine filtration and microfiber synthetic-suede, while Asia-Pacific remains the volume leader thanks to large-scale nonwoven investments in China, India, and Thailand. At the same time, extended producer responsibility (EPR) frameworks in Europe and circular-economy strategies among global brands are directing capital toward chemically recycled PET and monomaterial polyolefin-based fibers that simplify end-of-life processing.

Key Report Takeaways

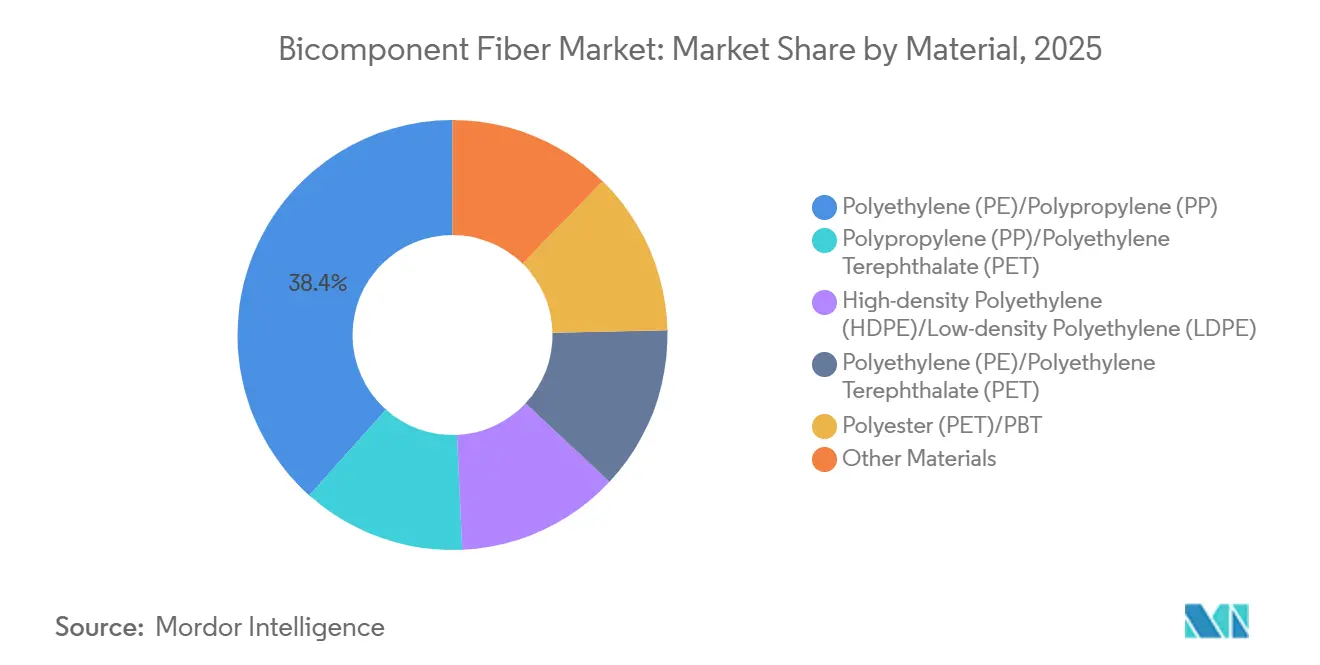

- By material, Polyethylene (PE)/Polypropylene (PP) blends captured 38.40% bicomponent fiber market share in 2025, whereas Polyethylene (PE)/Polyethylene Terephthalate (PET) combinations are projected to register the fastest 6.45% CAGR during the forecast period (2026-2031).

- By structure, sheath-core architectures led with 47.20% of 2025 volume, while islands-in-the-sea fibers are forecast to advance at a 6.58% CAGR during the forecast period (2026-2031).

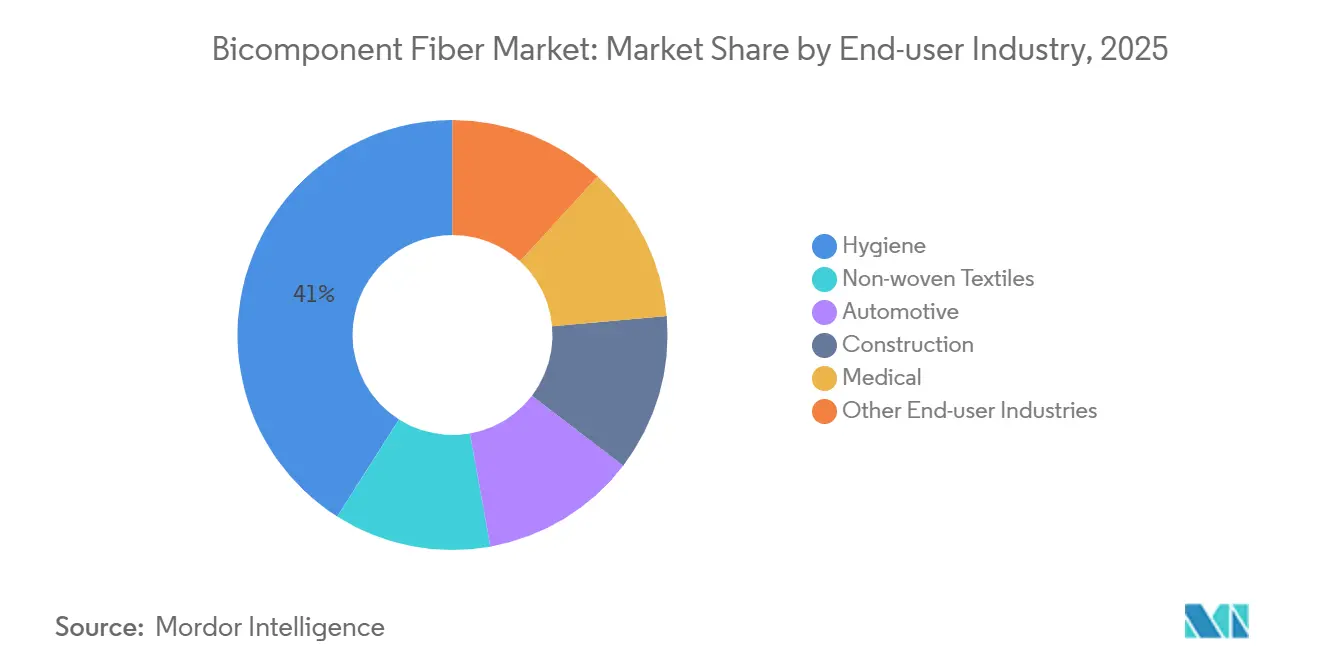

- By end-use, hygiene applications accounted for 41.00% of 2025 demand, yet medical textiles are set to post the highest 6.71% CAGR during the forecast period (2026-2031).

- By geography, Asia-Pacific commanded 46.50% of 2025 consumption and the Middle East & Africa is poised to expand at a 6.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bicomponent Fiber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption in hygiene products | +1.2% | Global, with APAC and MEA leading penetration gains | Medium term (2-4 years) |

| Rising demand from non-woven textiles | +1.0% | APAC core, spill-over to North America automotive | Short term (≤ 2 years) |

| Sustainability-driven shift to recyclable fibers | +0.9% | Europe and North America, regulatory push in EU | Long term (≥ 4 years) |

| Low-melt sheath-core fibers for battery separators | +0.6% | APAC (China, South Korea), early R&D in North America | Long term (≥ 4 years) |

| Use in 3D-printed composite reinforcement | +0.4% | North America and Europe aerospace/automotive clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption in Hygiene Products

Demographic aging, especially in Europe, Japan, and North America, is increasing per-capita uptake of adult-incontinence briefs, pads, and liners. Thermally bonded PE/PP sheath-core nonwovens enable thinner cores, faster fluid acquisition, and reduced skin irritation, giving hygiene brands a cost-performance edge. Multinationals continue to localize diaper and feminine-care production in India, Indonesia, and Nigeria, stimulating regional demand for bicomponent staple and spunbond fibers. Indian converters alone commissioned more than 4 billion diaper unit capacity between 2025 and 2026, relying on domestic PE/PP supply chains for acquisition and distribution layers. As unit costs fall, penetration is widening beyond metropolitan centers into tier-2 cities and rural districts, reinforcing a multiyear runway for volume growth. These vectors together lift hygiene’s share of the bicomponent fiber market while improving capacity utilization across Asia-Pacific lines.

Rising Demand from Nonwoven Textiles

Automotive interior suppliers are substituting polyurethane foams with islands-in-the-sea bicomponent microfibers that offer suede-like surfaces at lower mass, satisfying electric-vehicle lightweighting goals. Industry data show automotive nonwoven consumption on track to reach 1.8 million tons in 2026, with headliners and door-panel laminates absorbing a growing share. Filtration is another high-value slot; after alkaline splitting, islands-in-the-sea filaments create sub-micron pores that boost efficiency in HVAC (heating, ventilation, and air conditioning) and liquid filtration. Regional manufacturers such as TWE Group commissioned scalable spunbond platforms in Bhopal during 2025, aiming to meet both domestic and export demand[1]TWE Group, “Press Release—Bhopal Plant Launch,” twe-group.com. Capital investment in spunlace for wipes and medical fabrics across Western China further cements Asia-Pacific’s leadership in nonwovens, driving incremental demand for sheath-core binders with reliable wet-strength performance.

Sustainability-Driven Shift to Recyclable Fibers

Europe’s EPR directive for textiles, effective October 2025, sets eco-modulated fees that penalize non-recyclable constructions and introduces mandatory separate collection by 2028[2]European Commission, “Directive (EU) 2025/2195 on Textile EPR,” europa.eu. Brands therefore prefer PE/PE or PP/PP bicomponent constructs that bypass polymer-separation steps, while chemically recycled PET is gaining ground in high-tenacity applications. Oerlikon Barmag and Evonik launched a joint development program in January 2025 aimed at closing mechanical-property gaps between virgin and recycled PET for seatbelt yarns. Indorama Ventures’ November 2025 joint venture with Jiaren to install 100,000 tons per year of textile-grade recycled PET underlines a commitment to circular feedstocks. As targets tighten, 10% recycled content by 2028, 15% by 2030, and 30% by 2035, demand for recyclable bicomponent fibers is likely to accelerate, embedding sustainability as a primary growth lever across the Bicomponent Fiber market.

Low-Melt Sheath-Core Fibers for Battery Separators

Thermal-shutdown separators based on low-melt polyethylene sheaths around high-melt polypropylene or PET cores exhibit controlled pore closure and robust puncture strength, key for next-generation high-voltage lithium-ion cells. Pilot lines in South Korea and China are moving toward 2028-2030 commercialization windows as automakers push for safer, thinner, and more heat-resistant battery architectures. Fiber-based separators can be produced on modified spunbond or melt-blown equipment, promising cost advantages over ceramic-coated films once scaling hurdles are overcome. Battery OEMs (Original Equipment Manufacturers) increasingly collaborate with fiber specialists to benchmark dimensional stability, electrolyte wettability, and proprietary surface treatments. If pilot results hold, demand could open a new multi-kiloton niche within the bicomponent fiber market, benefiting suppliers that already master low-shrinkage polyolefin processing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost and CAPEX intensity | -0.7% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Volatile polyolefin and PET feedstock prices | -0.5% | Global, with APAC and Europe most exposed | Short term (≤ 2 years) |

| Limited high-temperature bicomponent spinning capacity | -0.3% | Global, concentrated among fewer than 10 licensors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production Cost and CAPEX Intensity

Dual-extrusion lines, precision metering pumps, and custom spinnerets lift capital outlays 30%-50% above single-polymer alternatives, making greenfield investments difficult for mid-tier converters. Teijin’s expansion at TPL Thailand, completed in late 2025, illustrates the financial scale, 700 tons per year of conjugate-filament capacity required specialized quench systems and advanced control loops, locking in lengthy depreciation schedules. High interest rates in Europe and parts of South America further stretch project hurdle rates, favoring vertically integrated multinationals that spread amortization across hygiene, medical, and filtration portfolios. The absence of standardized tooling for novel bio-based or recycled polymer pairs prolongs research and development cycles, adding engineering cost before a single commercial kilogram is shipped. These factors collectively shave growth potential off the bicomponent fiber market in capex-constrained regions.

Volatile Polyolefin and PET Feedstock Prices

Polypropylene spot prices spiked in Europe during March 2026 after Middle Eastern supply disruptions, while China’s PP benchmark rose month on month, compressing converters’ spreads under fixed-price hygiene contracts. By contrast, global PET oversupply in 2025 pushed Chinese operating rates down to 75%, creating a price inversion that benefited virgin-resin buyers but punished firms investing in premium recycled PET that trades at a 15%-25% uplift. Divergent trends oblige spinners to hedge both polymers, tying up working capital in inventory and derivatives. Sharp feedstock swings also complicate customer negotiations for quarterly or annual pass-through mechanisms, lengthening sales cycles and damping margin visibility across the Bicomponent Fiber market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: PE/PP Retains Scale While PE/PET Leads Growth

The Bicomponent Fiber market size for PE/PP blends represented 38.40% of total volume in 2025, thanks to their dominant use in diaper topsheets, acquisition-distribution layers, and thermal-bonding webs. Their moderate melt-point gap ensures strong inter-fiber bonding without jeopardizing softness, keeping PE/PP the workhorse material in commodity hygiene nonwovens. Even so, PE/PET pairings are on track for a 6.45% CAGR during the forecast period (2026-2031) as brand owners seek monomaterial packaging and recyclable battery separators. These combinations merge PET’s stiffness with PE’s low-temperature flow, satisfying both handling and end-of-life criteria in pouch, lid, and overwrap formats.

Sequential advancements are also unfolding in PP/PET acoustic felts for automotive headliners, HDPE/LDPE breathable films for cable-wrap and roofing membranes, and Polyester/PBT blends for high-temperature filtration. Specialty patents filed during 2025-2026 introduced bio-based polyethylene and PLA as sheath components to raise renewable content above 30%, yet volumes remain small. As new recycling targets loom, material choices are expected to tilt toward constructions that ease chemical or mechanical separation, a pivot already visible in European converter trials adopting mono-polyolefin architectures that hit the 10% recycled-content threshold.

By Structure Type: Sheath-Core Dominates but Islands-in-the-Sea Accelerate

In 2025, sheath-core designs held 47.20% of global output, confirming their versatility across acquisition layers, thermal-bonding points, and breathable barriers within the bicomponent fiber market. A low-melt sheath encapsulates a higher-tenacity core, permitting in-line bonding without additives and achieving bulk softness, features prized by diaper and wipe producers. Side-by-side fibers follow, enabling split microfilaments that mimic natural suede in dashboards and door trims.

Islands-in-the-sea constructions, comprising dozens of 0.05 denier islands within a soluble matrix, are forecast to log a 6.58% CAGR to 2031. Post-processing yields microfiber surfaces with more than 1 m²/g surface area, critical for sub-micron filtration and high-end cleaning wipes. The complexity of spinning up to 256 capillaries per filament restricts global capacity to roughly 15 manufacturing sites, anchoring premium pricing power for incumbents. Niche architectures, segmented pie, hollow sheath-core, multilayer, serve flame-resistant textiles and drug-delivery scaffolds, highlighting structural diversity that allows suppliers to tailor fibers to very specific performance windows.

By End-user Industry: Hygiene Still Leads, Medical Gaining Speed

Hygiene maintained a 41.00% share of global consumption in 2025, led by diapers, feminine pads, and adult incontinence briefs built around PE/PP sheath-core spunbond and melt-blown layers. Although birth rates are tapering in developed economies, aging populations offset the decline by lifting demand for absorbent adult products, sustaining baseline volume growth. Medical textiles are projected to climb at a 6.71% CAGR during the forecast period (2026-2031) as ISO 10993 test batteries and FDA (Food and Drug Administration) reclassification of surgical gowns to Class II devices push hospitals toward higher-barrier SMS laminates that rely on bicomponent binders for both softness and splash resistance.

Automotive nonwovens are thriving on electric-vehicle programs that seek lighter, quieter interiors. Splittable side-by-side fibers fill suede seating, pillar wraps, and headliners, while sheath-core polypropylene felts dampen road noise. Construction, agriculture, and electronics absorb the remainder, including geotextile drains, crop covers, and fiber-based battery separators. Across segments, Extended Producer Responsibility (EPR) rules and recycled-content targets are now primary design parameters, accelerating a shift toward mono-polymer or chemically recycled feedstocks that can document cradle-to-gate carbon footprints.

Geography Analysis

Asia-Pacific supplied 46.50% of global volume in 2025. Chinese converters expanded spunlace and spunbond capacity throughout 2025-2026, while Indian hygiene producers opened multi-billion-unit diaper plants in Gujarat and Rajasthan, lifting local offtake for PE/PP sheath-core fibers. Japan’s Toray and Teijin advanced islands-in-the-sea and conjugate-filament technologies, powering specialty exports to aerospace and filtration customers. South Korea’s battery-separator R&D ecosystem complements these strengths, positioning the sub-region as the innovation nucleus of the bicomponent fiber market

In North America, enforcement of ANSI/AAMI PB70 barrier levels and ISO 10993 biocompatibility tests elevates quality bars, favoring domestic suppliers who can assure lot-level traceability. Indorama Ventures’ Georgia site, integrated into the FiberVisions network, shortens lead times for hygiene customers managing lean inventories. Automotive lightweighting programs continue to open new outlets, especially as electric-vehicle manufacturers specify microfiber acoustics and low-VOC interior textiles.

In Europe, the EPR regulation that took effect in October 2025 imposes eco-modulated fees and staged recycled-content thresholds, 10% by 2028, 15% by 2030, and 30% by 2035, reshaping material roadmaps. Oerlikon Barmag’s partnership with Evonik to commercialize recycled-PET spinning lines by 2030 exemplifies supplier moves to align with circular-economy objectives. The region’s automotive supply chain is also migrating toward splittable microfiber seat fabrics to meet interior emission and weight targets.

The Middle East and Africa, though smaller today, is projected to share Asia-Pacific’s 6.56% CAGR through 2031. Rising birth rates and still-low hygiene penetration combine with growing disposable incomes to unlock diaper and feminine-care consumption. Gulf Cooperation Council industrial policy is encouraging localized assembly of hygiene finished goods, creating a pull effect for regional fiber capacity. South Africa’s export-oriented auto industry, meanwhile, is adopting bicomponent acoustic felts to comply with European noise standards.

South America's market share is led by Brazil’s expanding hygiene market and Argentina’s cost-competitive spunbond exports. Currency volatility tempers investment enthusiasm, yet regional converters exploit favorable labor and energy economics to serve North American commodity grades.

Competitive Landscape

The Bicomponent Fiber market is moderately fragmented. Strategic merger and acquisition activity is expected to continue as suppliers chase scale, portfolio breadth, and recycled feedstock access. Licensing of high-temperature engineering-polymer pairs remains concentrated among fewer than ten firms, preserving high entry barriers in specialty segments yet creating potential bottlenecks if automotive and battery demand jump faster than capacity additions.

Bicomponent Fiber Industry Leaders

Indorama Ventures Public Company Limited

KURARAY CO., LTD.

Freudenberg Performance Materials

TEIJIN LIMITED

Sichuan Huvis

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The Fiber and Polymer Science Lab at the Nonwovens Institute (NWI) enhanced its capabilities by installing a Hills, Inc. LBS-330 Lab Scale Bicomponent Melt Extrusion Unit. This upgrade significantly strengthens NWI's pilot-scale spunmelt development and prototyping services for its members, customers, and academic collaborators.

- March 2026: Asahi Kasei showcased Cubit 3D spacer fabrics at Techtextil 2026 in Frankfurt (April 21-24), combining PET with polytrimethylene terephthalate (PTT) and polyamide connecting threads to target footwear and automotive-seating applications demanding breathability and impact absorption.

Global Bicomponent Fiber Market Report Scope

Bicomponent fiber, or heterophil fiber, is a special class of synthetic fiber manufactured using two different polymers and then extruded as a single filament. This fiber combines the benefits of two polymers to obtain fibers with unique properties, such as effective thermal bonding, fine fibers, unique cross-section, easy customization, and others.

The Bicomponent Fiber market is segmented by material, structure types, end-user industry, and geography. By material, the market is segmented into polyethylene (PE)/polypropylene (PP), polypropylene PP/polyethylene terephthalate (PET), high-density polyethylene (HDPE)/low-density polyethylene (LDPE), polyethylene (PE)/polyethylene terephthalate (PET), polyester (PET)/PBT, and other materials. By structure types, the market is segmented into shell-core, side-by-side, islands in the sea, and other structure types. By end-user industry, the market is segmented into non-woven textiles, automotive, hygiene, construction, medical, and other end-user industries. The report also covers the market size and forecasts for bicomponent fiber in 15 countries across major regions. The market sizes and forecasts are provided in terms of volume (tons).

| Polyethylene (PE)/Polypropylene (PP) |

| Polypropylene (PP)/Polyethylene Terephthalate (PET) |

| High-density Polyethylene (HDPE)/Low-density Polyethylene (LDPE) |

| Polyethylene (PE)/Polyethylene Terephthalate (PET) |

| Polyester (PET)/PBT |

| Other Materials |

| Sheath-core |

| Side-by-Side |

| Islands in the Sea |

| Other Structure Types |

| Non-woven Textiles |

| Automotive |

| Hygiene |

| Construction |

| Medical |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material | Polyethylene (PE)/Polypropylene (PP) | |

| Polypropylene (PP)/Polyethylene Terephthalate (PET) | ||

| High-density Polyethylene (HDPE)/Low-density Polyethylene (LDPE) | ||

| Polyethylene (PE)/Polyethylene Terephthalate (PET) | ||

| Polyester (PET)/PBT | ||

| Other Materials | ||

| By Structure Type | Sheath-core | |

| Side-by-Side | ||

| Islands in the Sea | ||

| Other Structure Types | ||

| By End-user Industry | Non-woven Textiles | |

| Automotive | ||

| Hygiene | ||

| Construction | ||

| Medical | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global demand for bicomponent fibers be by 2031?

Bicomponent fiber market size is projected to reach 1.19 million tons by 2031, expanding at a 5.51% CAGR from 2026.

Which material pairing is growing fastest?

PE/PET bicomponent fibers are forecast to record a 6.45% CAGR through 2031, outpacing other pairings due to monomaterial recyclability and battery-separator trials.

What end-use segment offers the highest growth potential?

Medical textiles lead growth with a projected 6.71% CAGR through 2031 as stricter ISO 10993 and FDA rules lift barrier and biocompatibility requirements.

Which region is expected to add capacity most quickly?

Asia-Pacific continues to dominate capacity additions, driven by China’s spunlace investments and India’s hygiene-sector expansion, supporting a 6.56% regional CAGR.

Page last updated on: