Spandex Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

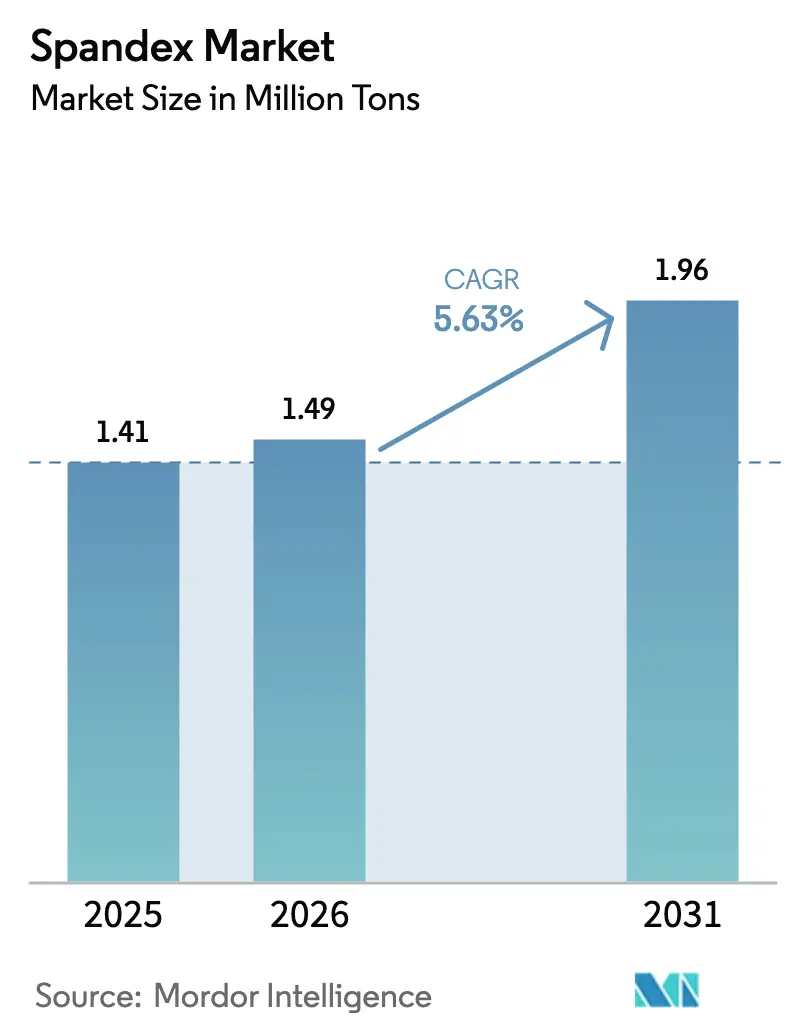

| Market Volume (2026) | 1.49 Million tons |

| Market Volume (2031) | 1.96 Million tons |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

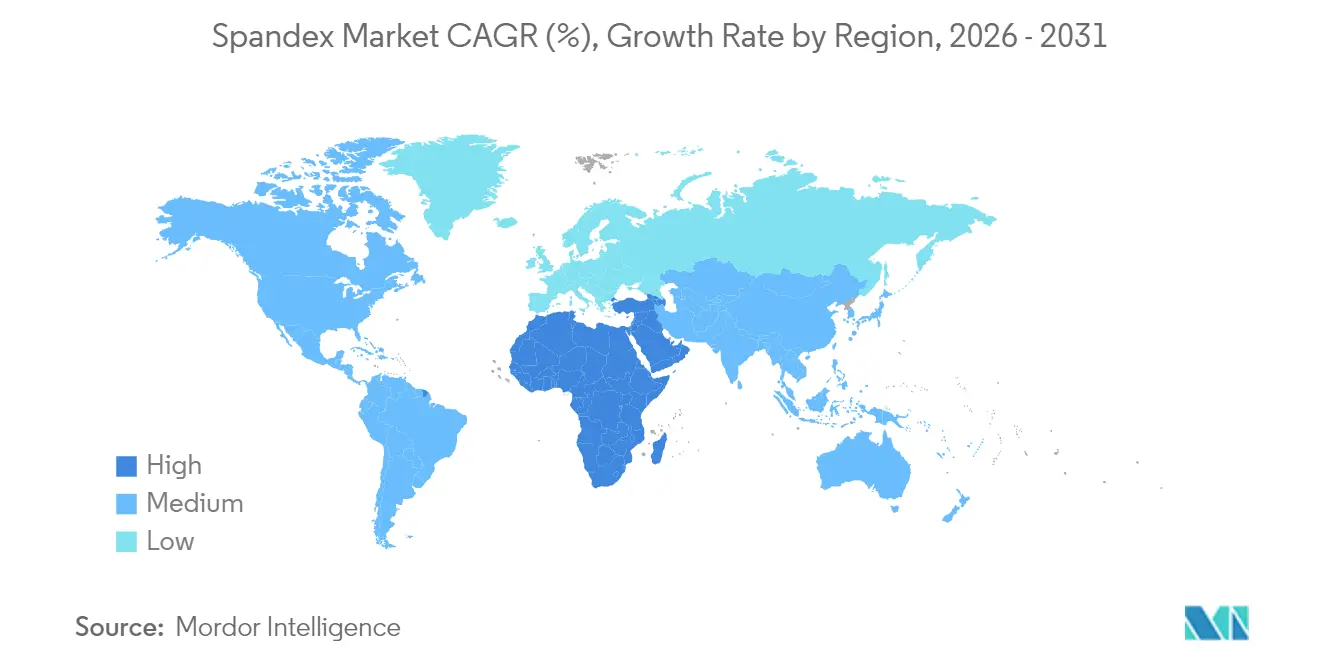

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spandex Market Analysis by Mordor Intelligence

The Spandex Market size was valued at 1.41 million tons in 2025 and estimated to grow from 1.49 million tons in 2026 to reach 1.96 million tons by 2031, at a CAGR of 5.63% during the forecast period (2026-2031). This sustained expansion rests on rising demand for stretch-enhanced fabrics across apparel, medical, and emerging technical textile uses, with athleisure, seamless knitting, and circular-economy mandates acting as the primary growth engines. Producers also leverage bio-based polyurethane chemistry to future-proof operations against tightening sustainability regulations, while raw-material price volatility keeps margins under pressure. Capacity additions in Asia-Pacific continue to influence global pricing, yet the Middle-East and Africa’s fast‐growing production base signals a gradual geographic rebalancing of the spandex market.

Key Report Takeaways

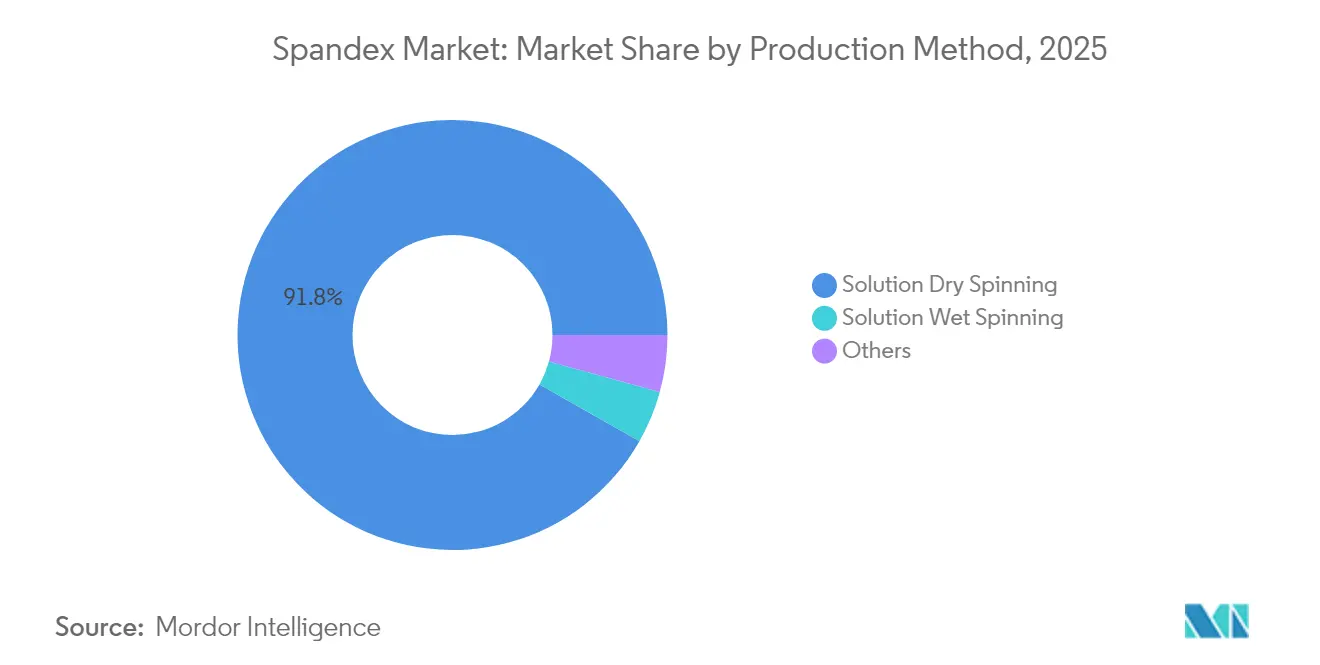

- By production method, solution dry spinning held 91.78% spandex market share in 2025; alternative methods under “Others” are forecast to grow at 6.08% CAGR through 2031.

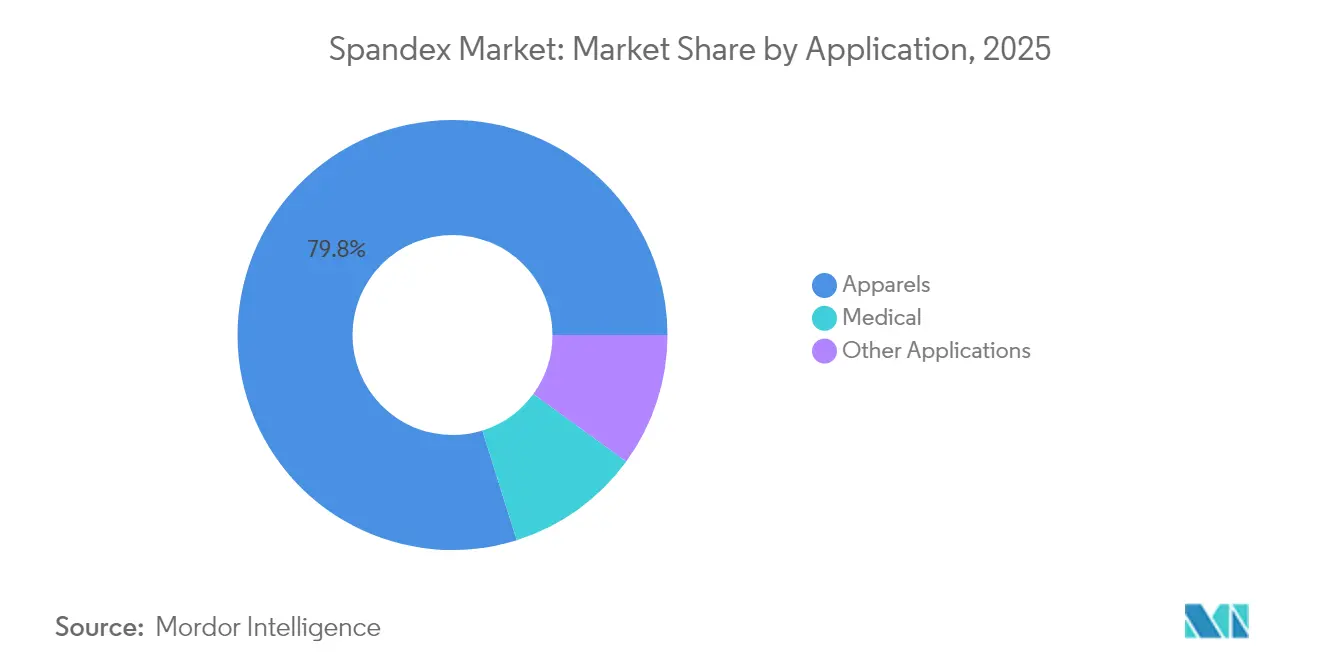

- By application, apparel controlled 79.83% of the spandex market size in 2025, while medical applications are projected to expand at a 6.22% CAGR to 2031.

- By geography, Asia-Pacific led with 63.88% revenue share of the spandex market size in 2025; the Middle-East and Africa are expected to post the fastest growth at 6.11% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Spandex Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising penetration of athleisure and performance wear | +2.1% | Global; strongest in North America and Europe | Medium term (2-4 years) |

| Government-backed investments in textile clusters | +1.3% | Asia-Pacific core; spill-over to Middle-East and Africa | Long term (≥ 4 years) |

| Medical compression garments demand surge post-COVID | +1.0% | Global; concentrated in developed markets | Short term (≤ 2 years) |

| Rapid uptake of seamless knitting technology | +0.8% | Asia-Pacific manufacturing hubs; expanding globally | Medium term (2-4 years) |

| Bio-based diisocyanate breakthroughs | +0.6% | Europe and North America leading; Asia-Pacific following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Penetration of Athleisure and Performance Wear

Athleisure’s rise from niche to mainstream has pushed spandex demand far beyond traditional sportswear. Performance apparel growth is driven by consumers who expect office-to-gym versatility. Remote-work culture reinforced casual dress codes, while direct-to-consumer brands accelerated innovation loops that reward fiber suppliers able to deliver consistent stretch, recovery, and moisture-management performance. Luxury labels such as Lululemon logged 25% year-over-year increases in technical fabric launches, underscoring how premium positioning no longer excludes high-function textiles[1]American Chemical Society, “Spinning Artificial Spider Silk into Next-Generation Medical Materials,” sciencedaily.com .

Government-Backed Investments in Textile Clusters

National industrial policies in Egypt, Vietnam, and Bangladesh channel low-cost financing, tax holidays, and workforce training into integrated textile parks. These clusters shorten lead times and improve quality control by co-locating spinning, weaving, and finishing operations, thereby anchoring long-term demand for spandex suppliers that establish local feedstock and fiber facilities. Similar incentives in Turkey and India reinforce the structural role of textiles in employment generation, ensuring that spandex market demand remains resilient across economic cycles.

Medical Compression Garments Demand Surge Post-COVID

Expanded outpatient care and heightened awareness of circulatory disorders have lifted prescription volumes of graduated compression hosiery and sleeves. Aging populations in the United States, Germany, and Japan rely on long-term compression therapy, while insurance coverage has broadened patient access. New spandex grades enable precise pressure gradients without sacrificing comfort or breathability, aligning with medical-device standards and reinforcing the fiber’s repositioning from fashion accessory to essential healthcare component.

Rapid Uptake of Seamless Knitting Technology

Seamless knitting eliminates cut-and-sew waste, supporting material savings and superior fit. Machines demand uniform tension and heat stability, prompting spandex producers to fine-tune polymer architecture for consistent processing. Adoption accelerates under sustainability mandates and consumer comfort preferences, with major sportswear brands shifting entire product lines to seamless platforms. Fiber suppliers able to guarantee tight denier control and low-defect rates secure multi-year yarn supply contracts.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying NGO pressure over micro-plastic pollution | -1.2% | Europe and North America; spreading globally | Medium term (2-4 years) |

| Petrochemical feedstock price volatility | -0.9% | Global; highest in import-dependent regions | Short term (≤ 2 years) |

| Supply-demand imbalance from China capacity additions | -0.7% | Global; strongest in Asia-Pacific and export markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying NGO Pressure Over Micro-Plastic Pollution

Environmental groups spotlight microfiber shedding—up to 700,000 particles per wash—driving European Union rules on filtration and labeling. Consumer sentiment shifts toward natural or recycled options, compelling brands to specify low-shedding or biodegradable spandex variants. Compliance costs rise as producers add coating steps or invest in intrinsic biodegradation technologies, potentially narrowing price competitiveness versus alternative fibers.

Petrochemical Feedstock Price Volatility

TDI and MDI costs swung 15-20% quarter-to-quarter in 2024, with January 2025 spot hikes of USD 200–300 per ton forcing fiber makers to renegotiate supply contracts or absorb margin pressure[2]ECHEMI, “Global MDI and TDI Price Increases: January 2025 Developments,” echemi.com . Geopolitical risk premiums in key feedstock regions further muddy cost forecasting, prompting companies to expand raw-material sourcing footprints and carry higher inventories to safeguard continuous operation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Method: Dry Spinning Maintains Technical Edge

Solution dry spinning commanded 91.78% spandex market share in 2025, reflecting its superior fiber uniformity, tensile strength, and dye uptake. The segment benefits from process control systems that minimize denier variability, a critical parameter for high-performance wearables. Aligning with sustainability targets, next-generation dry spinning lines reduce energy consumption by up to 20%, lowering specific carbon emissions. Alternative methods grouped under “Others” are projected to expand at a 6.08% CAGR through 2031 as solvent-free melt electrospinning and centrifugal techniques mature, albeit from a low base.

Emerging processes prioritize closed-loop solvent recovery and bio-based polymer integration, but scalability hurdles persist. Melt electrospinning’s promise of solvent elimination suits regulatory pressure on VOC emissions, yet faces fiber-uniformity challenges at industrial speeds. Centrifugal spinning delivers high throughput but falls short on fine-denier control required for premium intimates and medical devices. Accordingly, established dry-spinning producers invest in hybrid pilot lines while safeguarding their dominant positions through proprietary polyurethane formulations that embed specific elasticity-retention profiles.

By Application: Medical Emerges as Growth Engine

Apparel remained the volume leader, accounting for 79.83% of the spandex market size in 2025. Nevertheless, medical uses are slated to clock a 6.22% CAGR, making healthcare the fastest-growing segment through 2031. Compression stockings, wound-dressing wraps, and orthopedic braces require tightly controlled modulus values, encouraging long-term supplier agreements and relatively stable pricing structures.

Beyond compression therapy, hospital supply chains increasingly specify antimicrobial spandex blends for postoperative garments, further expanding medical adoption. Other niche applications-industrial filters, automotive seat covers, and smart-textile substrates-provide additional demand optionality. Apparel growth in mature economies moderates as athleisure penetration approaches saturation, but performance differentiation through moisture management, UV resistance, and bio-derived content keeps the category integral to the long-run trajectory of the spandex market.

Geography Analysis

Asia-Pacific retained a 63.88% share of the spandex market size in 2025, underpinned by China’s integrated feedstock-to-fabric chain, South Korea’s advanced polymer research and development, and India’s expanding spinning capacity. Regional producers benefit from proximity to petrochemical clusters and dense export logistics networks. Yet Chinese overcapacity periodically depresses average selling prices, pushing mills to chase operational efficiency and product diversification. Environmental upgrades mandated by updated emission norms require capital expenditure that may accelerate regional consolidation.

The Middle-East and Africa are forecast to deliver the highest CAGR at 6.11% during 2026-2031. Egypt’s integrated textile park projects and Saudi Arabia’s Vision 2030 incentives attract overseas investors keen on duty-free access to European and U.S. markets. Competitive electricity tariffs and modern port infrastructure further elevate the region as an emerging spandex market production hub.

The European Union’s Digital Product Passport and extended producer responsibility frameworks stimulate demand for low-impact elastomers and localized recycling loops. Nearshoring trends in Mexico and Central Europe offer quick-turn replenishment advantages that complement, rather than replace, Asia-centric bulk supply chains. South America, anchored by Brazil, shows moderate growth as domestic sportswear brands scale and public healthcare systems embrace compression therapies.

Competitive Landscape

The spandex market remains moderately consolidated. Scale economies in polyurethane synthesis and high-speed spinning lines protect incumbents from new entrants. Hyosung’s USD 1 billion investment in Vietnam to produce bio-based BDO exemplifies forward integration into greener feedstocks, reinforcing cost leadership while addressing customer sustainability scorecards. Regulatory compliance continues to act as both an entry barrier and a differentiator. Producers holding OEKO-TEX Standard 100 and ISO 14001 certifications gain preferred-supplier status among global brands. Patent filings on bio-derived diisocyanates and solvent-free spinning reached record highs in 2025, indicating that the innovation race is centered on lowering the environmental footprint while maintaining fiber performance.

Spandex Industry Leaders

HYOSUNG

Huafon Chemical Co., Ltd.

The LYCRA Company

Asahi Kasei Corporation

TAEKWANG INDUSTRIAL CO., LTD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: HYOSUNG announced transitioning its bio-based spandex feedstock from corn to sugarcane to enhance sustainability. The shift to sugarcane-based bio-BDO, developed in partnership with Geno, will reduce carbon emissions and improve supply chain efficiency. Production at Hyosung’s Vietnam plant is set to begin in early 2026, with a capacity of up to 50,000 tons.

- March 2025: At CIDPEX 2025, HYOSUNG introduced advanced CREORA spandex diaper solutions, emphasizing improved comfort, fit, and manufacturing efficiency. With superior creep resistance and high elongation, the spandex ensures leak prevention and optimal performance in hygiene products. To meet rising global demand, Hyosung has expanded diaper spandex production to India and Turkiye, targeting a total capacity of 11,000 tons by 2026.

Global Spandex Market Report Scope

Spandex (also known as Elastane Fiber) is a synthetic polymer that contains at least 85% polyurethane and is made up of a long-chain polyglycol combined with a short di-isocyanate. Spandex has excellent stretchability and is a strong, light, and versatile fiber. The Global Spandex Market is segmented by production method, application and geography. By production method, the market is segmented into Solution Dry Spinning, Solution Wet Spinning, and Others. By Application, the market is segmented into Apparels, Medical, and Other Applications. The report also covers the market size and forecasts for the Global Spandex Market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD Million).

| Solution Dry Spinning |

| Solution Wet Spinning |

| Others |

| Apparels |

| Medical |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Production Method | Solution Dry Spinning | |

| Solution Wet Spinning | ||

| Others | ||

| By Application | Apparels | |

| Medical | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the spandex market in 2026?

The spandex market size reached 1.49 million tons in 2026 and is forecast to hit 1.96 million tons by 2031.

Which production method dominates the current supply?

Solution dry spinning delivers 91.78% of global output, thanks to its fiber-quality and energy-efficiency profile.

What is the fastest-growing application for spandex?

Medical compression garments are projected to grow at a 6.22% CAGR between 2026-2031, outpacing apparel.

Which region will grow quickest through 2031?

The Middle-East and Africa lead with a forecast 6.11% CAGR, supported by government-backed textile-cluster investments.

How are sustainability pressures shaping spandex innovation?

Producers are scaling bio-based diisocyanate chemistry and solvent-free spinning techniques to lower carbon footprints and meet EU sustainability mandates.

Page last updated on: