Nylon Monofilament Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

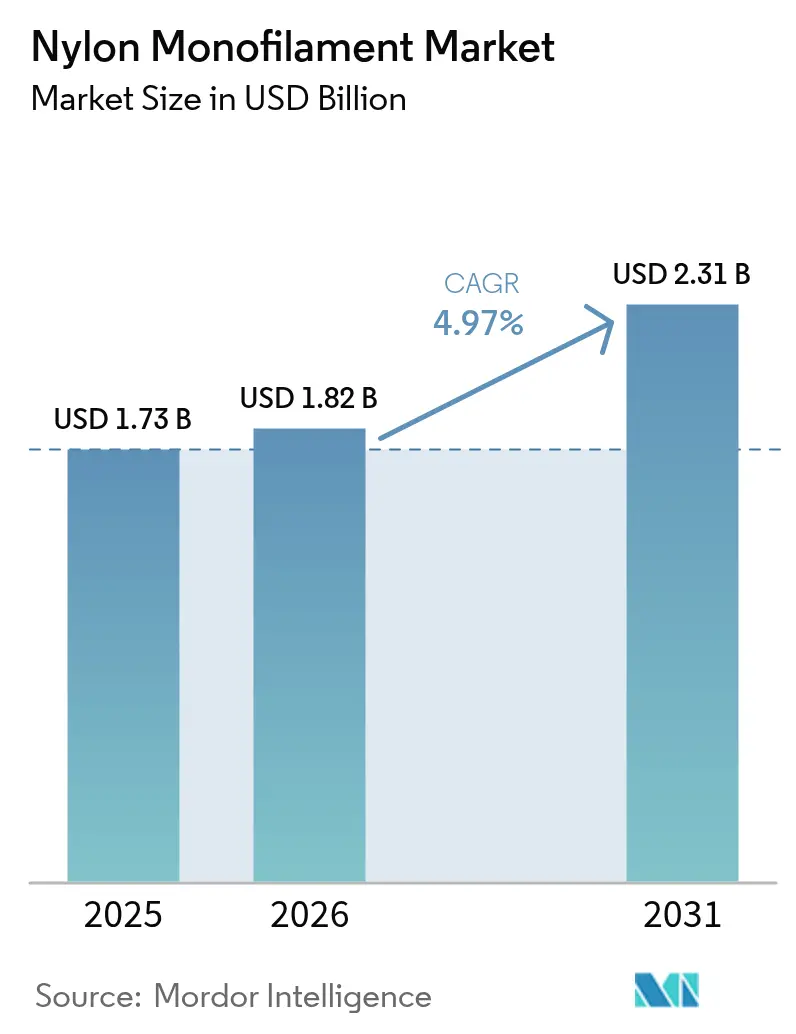

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.31 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

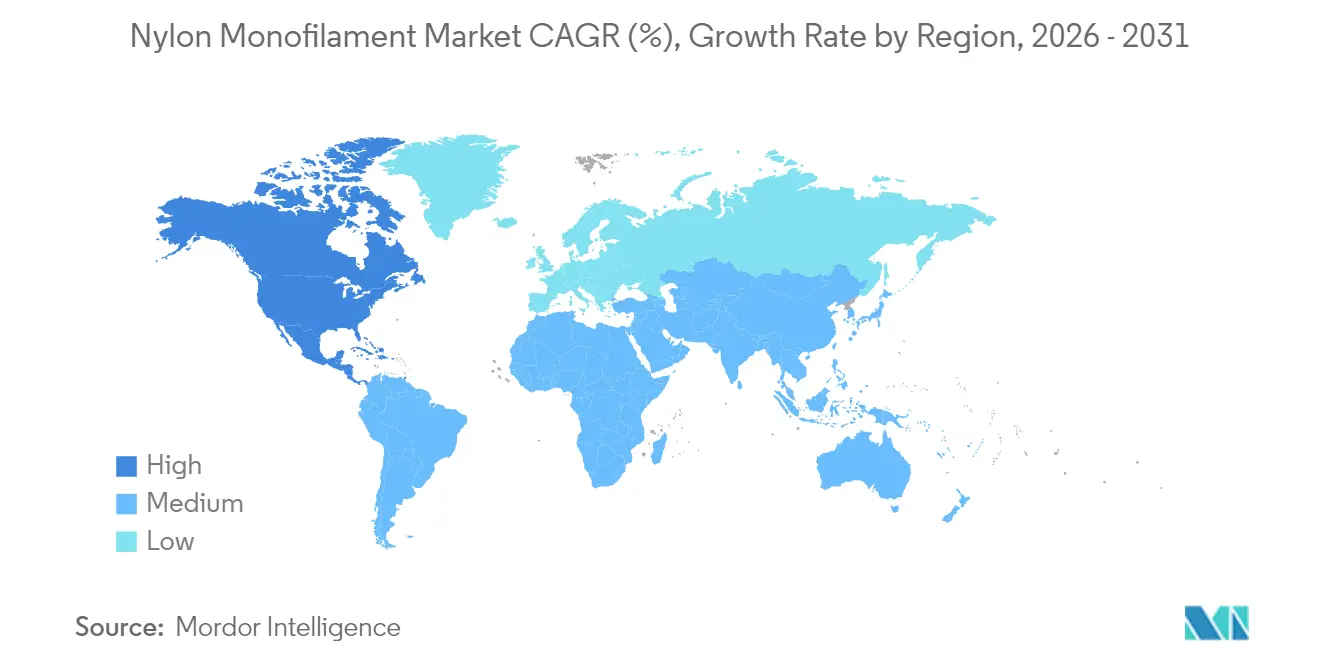

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nylon Monofilament Market Analysis by Mordor Intelligence

The Nylon Monofilament Market size was valued at USD 1.73 billion in 2025 and estimated to grow from USD 1.82 billion in 2026 to reach USD 2.31 billion by 2031, at a CAGR of 4.97% during the forecast period (2026-2031). Demand resilience is anchored in the material’s high tensile strength, chemical resistance, and processability, qualities that give the nylon monofilament market an entrenched role across fishing, medical, automotive, and consumer applications. Continuous investments in vertically integrated supply chains cushion the sector against raw-material volatility, while regulatory scrutiny over microplastics redirects innovation toward bio-based and recycled grades rather than displacing volume outright. Competitive dynamics remain moderately fragmented; however, recent consolidation signals a trend toward scale efficiencies in feedstock sourcing and specialty product development. Growth pockets are most visible in North America, where electric-vehicle (EV) lightweighting and advanced medical devices draw on FDA-approved nylon grades, and in Asia-Pacific, where large-scale fishing and textile operations keep baseline consumption high.

Key Report Takeaways

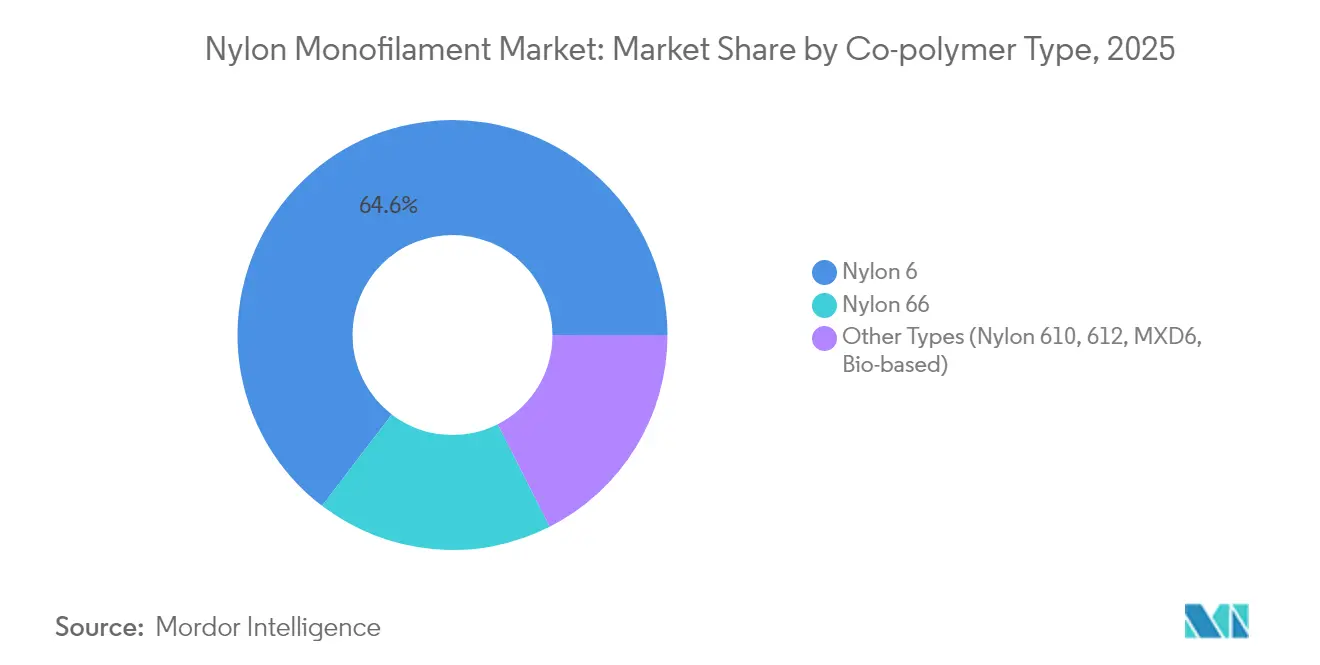

- By co-polymer type, Nylon 6 captured 64.62% of nylon monofilament market share in 2025, whereas Nylon 66 is expanding at a 5.28% CAGR through 2031.

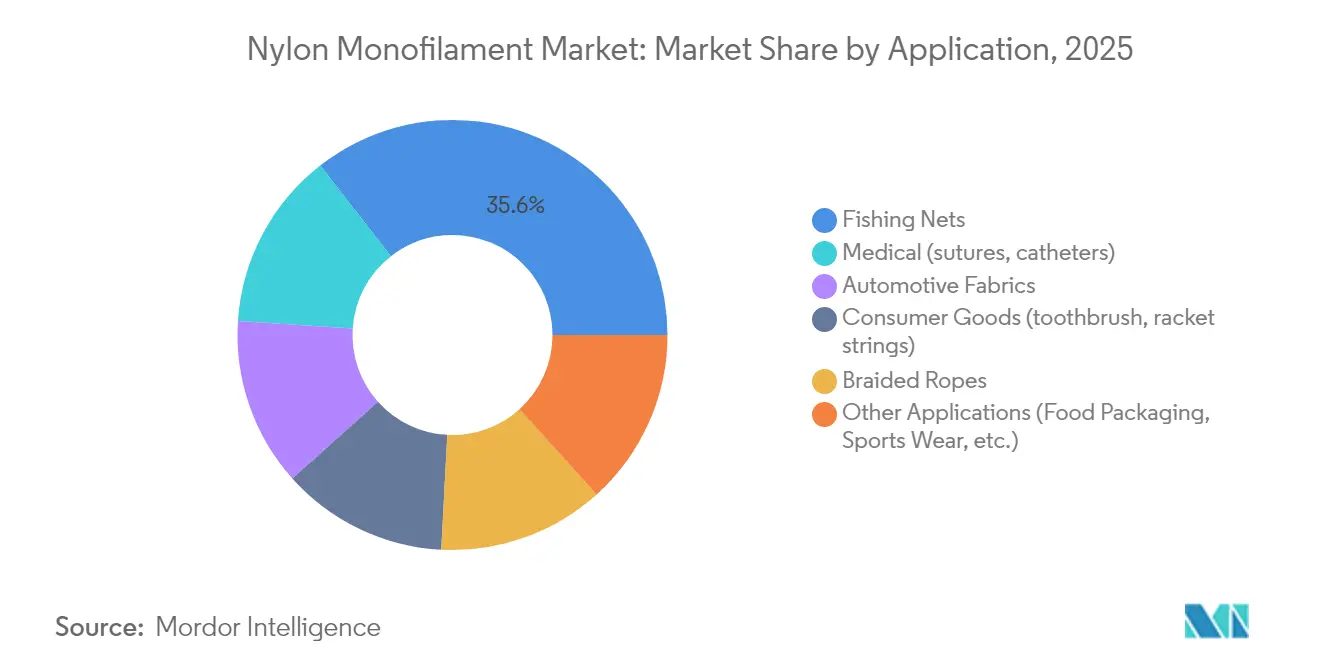

- By application, fishing nets accounted for 35.55% of the nylon monofilament market size in 2025, while medical uses are projected to grow at 6.42% CAGR between 2026 and 2031.

- By geography, Asia-Pacific held 32.88% revenue share in 2025, yet North America is set to record a 5.55% CAGR over the same forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nylon Monofilament Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand in fishing nets & aquaculture | +1.8% | Global, with APAC core concentration | Long term (≥ 4 years) |

| Surge in automotive lightweight components | +1.2% | North America & Europe primary, APAC manufacturing | Medium term (2-4 years) |

| Expansion in healthcare & surgical sutures | +1.0% | Global, with North America & Europe leading adoption | Medium term (2-4 years) |

| Growth in consumer goods (toothbrush bristles) | +0.4% | Global, with developed markets leading premium adoption | Short term (≤ 2 years) |

| 3-D printing & additive manufacturing adoption | +0.3% | North America & Europe innovation centers, global spillover | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand in Fishing Nets & Aquaculture

Expansion of global aquaculture continues to underpin nylon monofilament market growth as operators prioritize gear durability and catch efficiency. Nylon constitutes 76% of fishing-equipment polymers, and monofilament nets outperform multifilament alternatives by maintaining tensile strength under prolonged saltwater exposure. Although Norway is trialing biodegradable gillnets, field data show a 40% drop in catch efficiency and elevated costs, limiting near-term displacement. Field studies further reveal only 3-6% strength loss when nets are immersed in 10% peracetic-acid baths used in fish-farm disinfection, reinforcing nylon’s durability advantage. Regulatory latency in Southeast Asian markets and the immediate economic gains from longer-lasting gear sustain volume growth even as Europe tightens environmental standards. Emerging biodegradable grades that achieve 92% marine degradation within a year remain commercially niche due to inferior mechanical properties.

Surge in Automotive Lightweight Components

Vehicle electrification accelerates the substitution of metal with engineering plastics, and nylon monofilament products such as bearing cages, cable ties, and functional trim contribute measurable weight savings. TECHNYL 4EARTH, manufactured by Domo, delivers up to 80% CO₂ reduction during production without sacrificing modulus or heat resistance. Celanese has introduced glass-fiber reinforced PA66 resins that enable direct metal replacement, offering the fatigue performance EV platforms require[1]Celanese Corporation, “Glass-Fiber Reinforced PA66 for EV Components,” celanese.com. Global OEMs favor nylon because its supply chain is entrenched and pricing mechanisms are well understood, reducing the switching risk relative to newer bio-based options. High qualification costs, tight dimensional tolerances, and regulatory certification needs keep entry barriers high and underpin a stable 1.2-point contribution to the nylon monofilament market CAGR.

Expansion in Healthcare & Surgical Sutures

Nylon monofilament’s biocompatibility, low tissue reactivity, and predictably slow hydrolytic strength decay (15-20% per annum) make it indispensable for microsurgical sutures and catheter components. FDA clearances across multiple nylon grades simplify supplier audits and expedite device approvals[2]European Commission, “Proposal on Microplastic Pellet Emissions,” europa.eu. The move toward single-use medical devices after the COVID-19 pandemic sustains demand, as hospitals emphasize infection control. Ethylene-oxide and e-beam sterilization cycles leave tensile properties intact, supporting broader adoption in minimally invasive and robotic surgery kits. While polyglycolic-acid and polydioxanone threads are biodegradable, surgeons still specify nylon where non-absorbable retention strength is clinically necessary.

Growth in Consumer Goods & 3D Printing Adoption

Personal-care brands specify premium nylon bristles for toothbrushes and cosmetic brushes, emphasizing both aesthetics and longevity. Celanese’s Tynex RS line incorporates bio-based feedstocks to answer sustainability preferences without compromising stiffness. In additive manufacturing, demand for specialty nylon filaments rises alongside a 2030 3D-printing revenue forecast of USD 78 billion, and Braskem’s takeover of taulman3D strengthens North American material supply . Sports-equipment makers continue to use nylon strings for mid-range tennis rackets thanks to the material’s elasticity and abrasion resistance. Consumer scrutiny of microplastic shedding encourages brands like UNIFI to commercialize recycled or degradable nylon variants while maintaining requisite flex-fatigue performance.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government restrictions on nylon fishing lines | -0.6% | Europe & North America leading, global spillover | Medium term (2-4 years) |

| Micro-plastic shedding regulations | -0.5% | Europe primary, North America & APAC following | Medium term (2-4 years) |

| Volatility in raw-material (caprolactam) prices | -0.8% | Global, with Asia-Pacific manufacturing concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Restrictions & Microplastic Regulations

The EU aims to cut plastic-pellet emissions by 74%, obliging processors handling over 5 tonnes annually to certify loss-prevention protocols—measures that could add compliance costs to every EU-bound kilogram of nylon monofilament. Senegal’s 1998 ban on nylon monofilament gillnets, although weakly enforced, illustrates how legal uncertainty can disrupt investment plans for fish-gear suppliers. In the United States, the General Services Administration now mandates single-use-plastic-free packaging on federal contracts, signaling future procurement barriers. Laboratory assessments of edible seafood detected nylon fibers, strengthening the scientific case for tighter controls across consumer goods. Industry responses include accelerated R&D in compostable or enzyme-cleavable polyamides, yet cost and performance gaps hinder immediate large-scale substitution, resulting in a net 1.1-point drag on the nylon monofilament market CAGR.

Volatility in Raw-Material (Caprolactam) Prices

Spot caprolactam climbed to USD 1,850 per tonne in 2024 as benzene feedstock tightened, widening the caprolactam–benzene differential to USD 950 per tonne and compressing monofilament margins. PA66 is doubly exposed because adiponitrile disruptions lifted spot offers to USD 5.00 per kg. China’s Q4 2024 PA66 average price slipped to USD 2,587 per tonne on automotive softening, yet North American tags held firm as inventory discipline limited downside. For integrated players such as BASF, feedstock swings can be partly offset via upstream benzene positions; mid-sized converters reliant on spot purchases face margin squeeze and may pass costs downstream, raising price elasticity risk. A 0.8-point reduction in the nylon monofilament market CAGR is therefore attributed to feedstock volatility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Co-polymer Type: Nylon 6 Dominance Faces Specialty Challenge

Nylon 6 retained 64.62% nylon monofilament market share in 2025 thanks to a mature global caprolactam production base that keeps conversion costs low. Plants such as GSFC’s 70,000-80,000 tonne facility in India illustrate economies of scale, and roughly 17,000 tonnes feed captive monofilament operations. The nylon monofilament market size for Nylon 6 is projected to reach USD 1.39 billion by 2031 as mainstream applications from fishing nets to consumer bristles uphold baseline demand. In contrast, Nylon 66 is on a steeper 5.28% CAGR trajectory, driven by superior heat-aging and dimensional stability required for EV components and industrial belts. INVISTA’s USD 1.75 billion expansion in Shanghai, doubling PA66 output to 400,000 tonnes, signals confidence in high-temperature markets.

Longer-chain and specialty grades—Nylon 610, 612, MXD6—command premium prices where water absorption, fuel-barrier, or optical-clarity performance matters. Nylon-MXD6 retains 60% of initial strength after saturated-steam exposure, making it attractive for chemical-resistant monofilaments. Bio-based output is scaling quickly: LG Chem and CJ CheilJedang target 1.4 million tonnes of renewable nylon by 2028, a 29% annual addition to global capacity. DSM’s fully bio-based Stanyl® B-MB delivers a 50% smaller carbon footprint, satisfying OEM climate targets without mechanical compromise. Specialty momentum therefore erodes Nylon 6’s share at the margin but expands overall premium value pools in the nylon monofilament market.

By Application: Medical Growth Outpaces Traditional Fishing Dominance

Fishing nets still represented 35.55% of the nylon monofilament market size in 2025, reflecting enduring reliance on durable, salt-resistant gear in commercial capture and aquaculture. Field tests show negligible tensile loss after repeated alkaline cleaning cycles, validating cost-of-ownership advantages. Yet medical demand is rising faster; a 6.42% CAGR through 2031 translates into a USD 330.28 million medical-grade nylon monofilament market by forecast end. Sutures stand out: microsurgical threads rely on nylon’s non-wicking surface and predictable knot security, while ethylene-oxide sterilization leaves tensile degradation below 2%.

Automotive fabrics and seat-belt webbings capture spillover growth from vehicle lightweighting, with reinforced PA66 monofilaments cutting component weight by up to 30%. Consumer goods, especially toothbrush bristles and sporting-goods strings, sustain moderate single-digit gains because nylon’s modulus and flex-fatigue life underpin tangible performance benefits. Braided ropes maintain steady uptake in marine and industrial hoisting, where UV-stability and impact resistance trump costlier aramid solutions. Emerging avenues—food-contact films, 3D-printing filaments, smart-textile actuators—are niche but high-margin, supported by FDA-approved grades and the proliferation of desktop fused-filament printers.

Geography Analysis

Asia-Pacific accounted for 32.88% of nylon monofilament market share in 2025, leveraging integrated petrochemical complexes and cost-effective labor. Chinese producers export industrial yarn to Thailand, Indonesia, and India under a well-established intra-Asian network. India’s roadmap targeting USD 350 billion in domestic man-made fiber consumption and USD 300 billion in exports by 2025 provides a growing outlet for monofilament in technical textiles. Japan’s early overseas investment—Toray built facilities in Thailand and Indonesia in the 1960s—continues to yield technological spillovers. Regional challenges include microplastic regulations and benzene-linked feedstock spikes, yet entrenched scale advantages preserve Asia-Pacific leadership in base-grade volumes.

North America is projected to post the fastest 5.55% CAGR over 2026-2031, propelled by EV manufacturing mandates and an advanced medical-device supply chain. INVISTA is recommissioning hexamethylene-diamine assets in Ontario and planning a new adiponitrile unit to secure PA66 precursors. BASF lifted North-American PA66 compound prices by USD 0.15 per lb in mid-2024, indicating healthy demand elasticity. Braskem’s U.S. filament acquisition supports 3D-printing uptake, adding localized nylon capacity for aerospace, dental, and consumer prototypes. FDA pathways for bio-based polyamides further entice OEMs to specify sustainable grades, reinforcing premium-segment pull.

Europe is navigating tighter regulation and energy-cost headwinds yet leads in circular-economy initiatives. The EU microplastic accord forces pellet-handling certification, raising compliance costs but providing a moat for early adopters. BASF’s acquisition of DOMO’s Alsachimie stake and the startup of a world-scale hexamethylene-diamine plant in France affirm long-term commitment to European nylon chemistry. South America and the Middle East & Africa trail in absolute volume yet present green-field opportunities in aquaculture and infrastructure; however, currency risk, import dependency, and limited polymerization assets temper near-term growth.

Competitive Landscape

The nylon monofilament market features moderate consolidation. BASF, Toray Industries, and Celanese capitalize on vertical integration from benzene and adiponitrile through compounded monofilament grades, muting feedstock-price shocks and enabling differentiated service packages. INVISTA concentrates on high-temperature PA66 for automotive under-the-hood and EV battery components. Recent consolidation—BASF’s purchase of DOMO’s Alsachimie stake—rationalizes European capacity and enhances feedstock synergies. Ascend Performance Materials’ bankruptcy underscores exposure for non-integrated firms during feedstock upswings.

Strategic thrusts center on sustainability: Celanese markets partially bio-based Tynex RS, BASF scales textile-waste loopamid, and LG Chem pursues renewable monomers. Enzyme-based recyclers such as Protein Evolution and Basecamp Research position Biopure technology for fully circular polyamide loops, challenging virgin-resin economics. Patent filings in bio-nylon and depolymerization climbed 18% year-on-year, indicating an innovation race that could re-segment the nylon monofilament industry around environmental credentials.

Barrier to entry remains high: polymerization requires USD 100-150 million capital outlay per 100 ktpa, and global automotive or medical OEM qualification cycles span up to 24 months. New entrants therefore focus on niche additive manufacturing filaments or localized medical-suture lines, often partnering with incumbents for polymer supply. Regional regulation increasingly shapes competitive moats; firms able to certify pellet-loss prevention and low-carbon production gain preferential access to EU and North American procurement channels.

Nylon Monofilament Industry Leaders

Superfil

Shakespeare Company, LLC

Perlon GmbH

Ruichang Monofilament

Toray Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: INVISTA obtained a patent for a nylon recycling process to enhance nylon 6,6 production by increasing high-quality post-industrial recycling (PIR) feedstock availability. The company also filed a patent application for a process enabling up to 100% post-consumer recycled (PCR) content in new nylon 6,6 components, aiming to improve the polymer's future applications.

- February 2024: The Filament Company opened a new plant in Goa, India, marking a key step in Perlon‘s global expansion and commitment to innovation. The facility, enabled by acquiring Shaun Filaments, a leading Indian filament manufacturer, strengthens market presence, expands capacity, and improves nylon monofilament production processes.

Global Nylon Monofilament Market Report Scope

A single extruded fiber of synthetic nylon material is known as nylon monofilament. Nylon is utilized in monofilament production due to its superior heat, toughness, and water resistance. Nylon monofilament is extensively used in several applications due to its cost-effectiveness and reliability in manufacturing numerous products. The market is segmented by co-polymer type, application, and geography (Asia-Pacific, North America, Europe, South America, the Middle East, and Africa). By co-polymer type, the market is segmented into nylon 6, nylon 66, and other co-polymer types (nylon 610, nylon 612). The market is segmented by application into fishing nets, medical, automobile fabrics, consumer goods, braided ropes, and other applications. The report also covers the size and forecasts for the nylon monofilament market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Nylon 6 |

| Nylon 66 |

| Other Types (Nylon 610, 612, MXD6, Bio-based) |

| Fishing Nets |

| Medical (sutures, catheters) |

| Automotive Fabrics |

| Consumer Goods (toothbrush, racket strings) |

| Braided Ropes |

| Other Applications (Food Packaging, Sports Wear, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Co-polymer Type | Nylon 6 | |

| Nylon 66 | ||

| Other Types (Nylon 610, 612, MXD6, Bio-based) | ||

| By Application | Fishing Nets | |

| Medical (sutures, catheters) | ||

| Automotive Fabrics | ||

| Consumer Goods (toothbrush, racket strings) | ||

| Braided Ropes | ||

| Other Applications (Food Packaging, Sports Wear, etc.) | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Nylon Monofilament Market size?

It reached USD 1.82 billion in 2026 and is forecast to hit USD 2.31 billion by 2031 under a 4.97% CAGR.

Which geography is growing fastest in nylon monofilament demand?

North America is projected to expand at 5.55% CAGR over 2026-2031 as EV lightweighting and medical devices scale.

Why does Nylon 6 hold the largest share among co-polymer types?

Established caprolactam infrastructure and cost-efficient production give Nylon 6 a 64.62% share across high-volume uses such as fishing nets.

Which application segment is set to outpace the rest?

Medical uses, particularly surgical sutures, are advancing at 6.42% CAGR thanks to nylon’s biocompatibility and sterilization tolerance.

Page last updated on: