Gen Z Mental Health Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

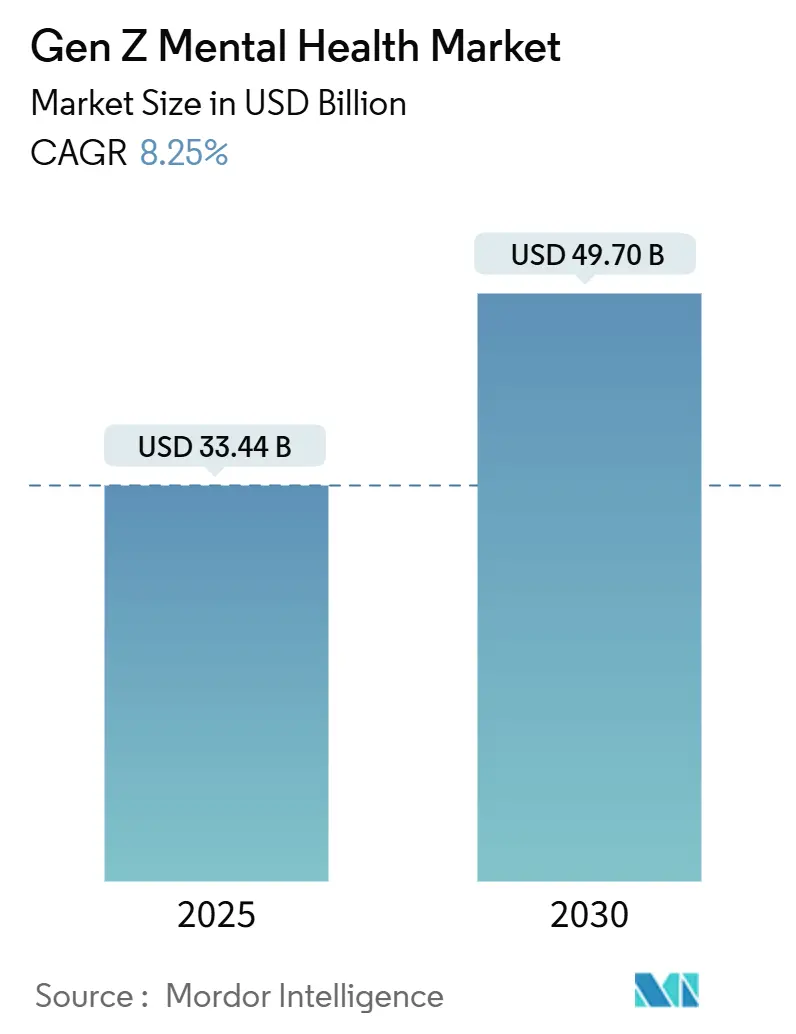

| Market Size (2025) | USD 33.44 Billion |

| Market Size (2030) | USD 49.70 Billion |

| Growth Rate (2025 - 2030) | 8.25% CAGR |

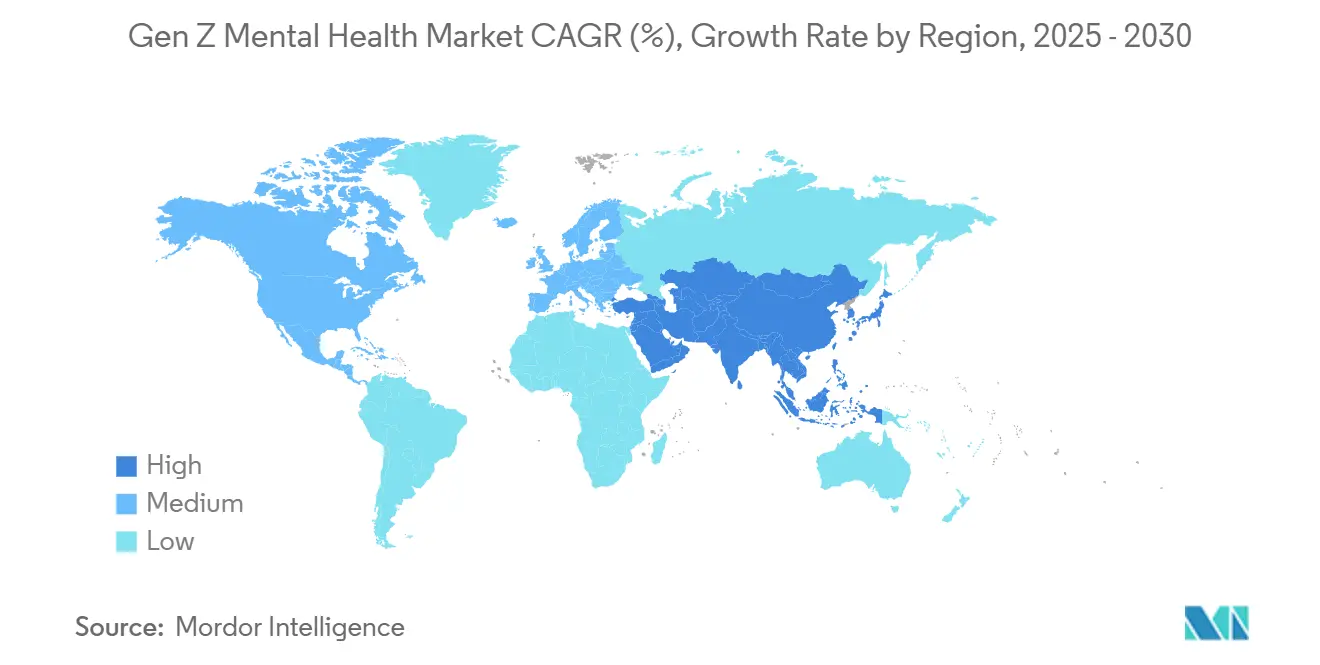

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gen Z Mental Health Market Analysis by Mordor Intelligence

The Gen Z Mental Health Market size is estimated at USD 33.44 billion in 2025, and is expected to reach USD 49.70 billion by 2030, at a CAGR of 8.25% during the forecast period (2025-2030).

Demand accelerates as three-quarters of Gen Z describe themselves as happy yet large cohorts report anxiety and depression, prompting institutions to expand digital therapeutic options. Corporate wellness mandates, widening insurance reimbursement, and FDA validation of prescription apps encourage enterprises, payers, and regulators to treat mental wellness as essential infrastructure. North America holds leadership because of regulatory progressiveness and venture funding, while Asia-Pacific posts the fastest expansion as smartphone saturation converges with shifting cultural attitudes. Product innovation orbits immersive VR/AR experiences, emotion-sensing wearables, and AI-enabled CBT, matching Gen Z preferences for instant, customized, and gamified support.

Key Report Takeaways

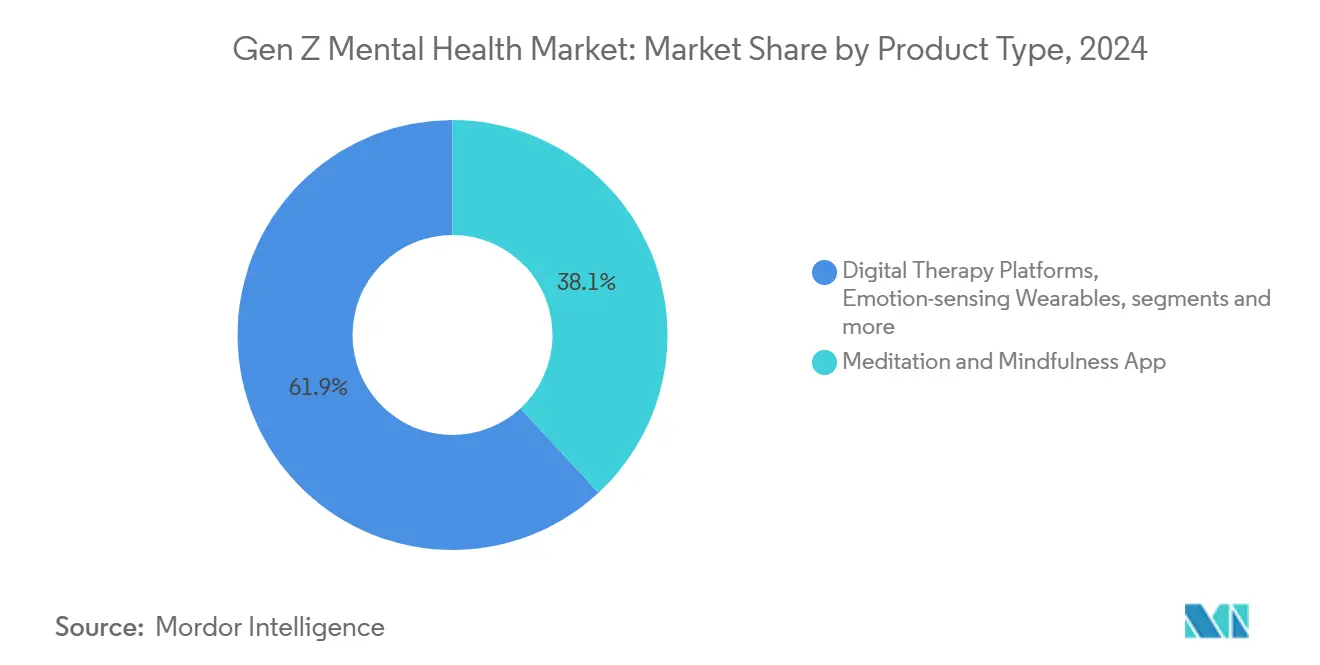

- By product type, Meditation & Mindfulness Apps led with 38.12% revenue share in 2024, whereas VR/AR Mental Wellness Solutions are projected to advance at a 9.78% CAGR to 2030.

- By delivery mode, Mobile Applications captured 69.45% of the Gen Z mental health market share in 2024, while In-person Hybrid models record the highest projected CAGR at 10.43% through 2030.

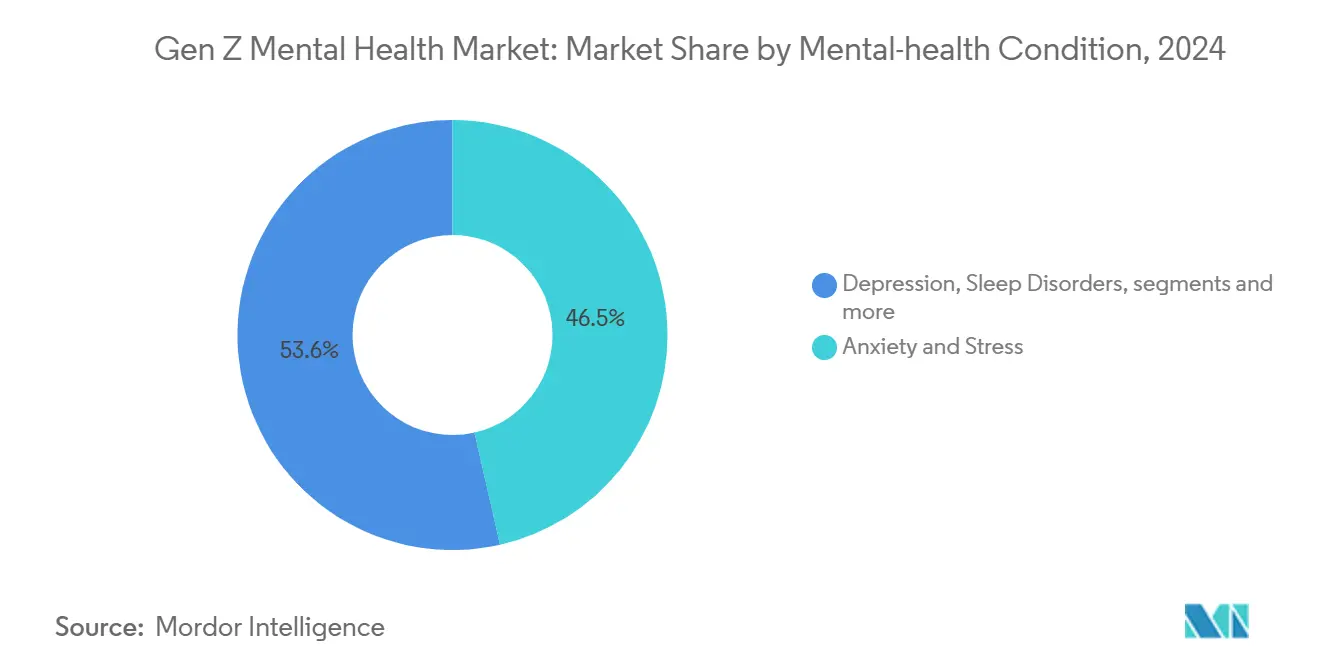

- By mental-health condition, Anxiety & Stress interventions commanded 46.45% concentration in 2024; PTSD & Trauma therapies are expanding at an 11.07% CAGR to 2030.

- By end user, Individual Consumers accounted for 64.78% share of the Gen Z mental health market size in 2024, yet Enterprises & Employers segment is growing at an 11.72% CAGR through 2030.

- By geography, North America held 43.46% revenue share in 2024, whereas Asia-Pacific is set to post a 10.87% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gen Z Mental Health Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-enabled CBT platforms | +1.8% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Corporate wellness mandates | +2.1% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Gamified mindfulness for Gen-Z | +1.4% | Global, particularly strong in APAC & North America | Medium term (2-4 years) |

| Insurance reimbursement expansion | +1.7% | North America & EU core markets | Long term (≥ 4 years) |

| Emotion-sensing wearables integration | +1.2% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Investor preference for neuro-tech | +0.9% | Global venture capital markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-enabled CBT platforms

AI-guided Cognitive Behavioral Therapy delivered through chatbots and adaptive lesson modules is reshaping the Gen Z mental health market by mirroring on-demand behavioral cues and tailoring content in real time. FDA clearance of Rejoyn in 2024 created a pathway for prescription digital therapeutics that merge CBT with machine-learning algorithms, allowing companies such as Otsuka to demonstrate regulatory compliance and clinical value. Emotion AI from Feel Therapeutics augments these platforms with wearable data, improving mood tracking accuracy.[1]Feel Therapeutics, “US Patent 11,967,339 Wearable Emotion Detection,” feeltherapeutics.com Gen Z acceptance is high because 70% prefer digital tools over traditional therapy settings, yet long-term efficacy studies remain scarce, tempering payer confidence.

Corporate wellness mandates

Workplace expectations from Gen Z employees push employers to incorporate structured mental health programs beyond legacy Employee Assistance models. Survey data indicate that 61% of Gen Z employees would switch jobs for better benefits.[2]Society for Human Resource Management, “Gen Z Workers and Mental Health Benefits,” shrm.org In response, enterprises adopt bundled app subscriptions and hybrid coaching that integrate seamlessly with health plans. Expanded mental-health parity regulation obliges insurers to reimburse digital therapies at parity with physical health, sparking rapid deployment of enterprise-grade platforms and forming a fast-growing revenue channel for vendors.

Gamified mindfulness for Gen Z

Gamification reframes meditation into reward-based tasks that parallel mainstream gaming loops. Titles such as Zengence blend rhythmic breathing with interactive challenges, tapping dopamine pathways to sustain engagement. University-led VR trials demonstrate meaningful anxiety reduction when immersive environments layer multisensory cues onto breathing exercises.[3]Carnegie Mellon University, “VR Stress-Management Simulations,” cmu.edu Social leaderboards and community missions complement solitary practice, aligning with Gen Z’s desire for peer connection. Clinical validation is mixed, prompting regulators to delineate wellness versus medical claims.

Insurance reimbursement expansion

Centers for Medicare & Medicaid Services introduced new digital-therapy payment codes effective 2025, legitimizing prescription mental-health software as reimbursable benefits. Private payers tend to mirror Medicare, so broad coverage is expected to narrow cost barriers that have historically driven many Gen Z users toward free apps. CPT 96127 now reimburses brief behavioral screens, encouraging primary-care physicians to integrate mental-health triage in routine visits. Administrative complexity and member education remain hurdles, signaling opportunities for simplified billing and digital-literacy tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical-evidence deficit | -1.9% | Global, particularly affecting regulatory approval markets | Medium term (2-4 years) |

| Digital-fatigue churn | -1.3% | North America & EU, emerging in APAC urban centers | Short term (≤ 2 years) |

| Data-sovereignty regulations | -1.1% | EU core, expanding to global markets | Long term (≥ 4 years) |

| Unequal broadband access | -0.8% | Rural areas globally, pronounced in developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clinical-evidence deficit

Many popular apps rely on engagement metrics rather than randomized controlled trials, leaving insurers wary of broad reimbursement. While Rejoyn’s approval proved feasibility, its modest outcome data underline the field’s evidence gap. Systematic reviews in peer-reviewed journals report that most AI-driven tools lack longitudinal data, limiting claims of durable effect. Gen Z’s trust in digital health solutions can erode if promised results do not materialize, making rigorous validation an urgent commercial imperative.

Digital-fatigue churn

Gen Z’s high screen exposure results in app abandonment and periodic “digital detox” cycles. Studies indicate 40% feel technology harms their mental health. The same devices that deliver help also contribute to anxiety, creating a paradox. Platforms are addressing fatigue with audio-only modes, adaptive usage nudges, and integrations that encourage offline activities, yet churn remains a structural headwind to lifetime-value growth

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Immersive Solutions Accelerate Innovation

Meditation & Mindfulness Apps held the largest slice of the Gen Z mental health market at 38.12% in 2024 as self-guided breathing and journaling resonated with mobile-first lifestyles. The segment is mature but faces saturation. By comparison, VR/AR Mental Wellness Solutions, though smaller, are forecast to expand at a 9.78% CAGR, fueled by hardware cost declines and research that validates exposure therapy for anxiety and PTSD. The Gen Z mental health market size for VR/AR applications is projected to climb steadily over the forecast period as universities and employers adopt immersive modules for stress inoculation. Digital Therapy Platforms sit between consumer and clinical realms, offering structured sessions with licensed clinicians via secure portals. Emotion-sensing Wearables remain emerging; patents such as Feel Therapeutics’ US 11,967,339 suggest a move toward passive mood sensing that continuously feeds apps with physiological markers, promising closed-loop behavioral interventions. AI Chatbots & Companion Apps round out the category, providing 24 / 7 conversational support that appeals to Gen Z’s immediacy expectations. Competition centers on evidence generation rather than basic feature differentiation as payers and regulators insist on outcome-based metrics for reimbursements.

The next growth wave relies on converging product categories into cohesive ecosystems. Meta’s collaboration with Headspace on Headspace XR shows how platform providers supply hardware while mental-health specialists deliver content. Universities apply VR to simulate stress scenarios such as public speaking, giving students a safe rehearsal space that later translates to real-world resilience. As immersive tools mature, product bundling with meditation content will nurture cross-sell synergies, producing multi-modal engagement that reduces digital fatigue by varying sensory inputs. Price remains a barrier but is falling, suggesting wider household adoption by late decade, especially once employer subsidy programs include hardware.

By Delivery Mode: Hybrid Combinations Build Stickiness

Mobile Applications dominated in 2024 with 69.45% share of the Gen Z mental health market. Always-on smartphones facilitate quick mood check-ins, micro-meditations, and asynchronous texting with coaches. Yet pure-mobile models encounter retention challenges, driving providers toward hybrid offerings. The In-person Hybrid approach — digital intake plus optional face-to-face therapy — is expected to grow fastest at 10.43% CAGR because it blends convenience with relational depth. The Gen Z mental health market size attached to hybrid models benefits from employers’ willingness to pay for richer service bundles that lower absenteeism. Web-based portals maintain relevance for longer counseling sessions and group workshops, while traditional in-person clinics pivot to virtual triage followed by on-site follow-ups, optimizing capacity utilization.

Gen Z prefers autonomy but not isolation. Headspace Health’s text-based coaching illustrates how human interaction can be delivered on demand without scheduling friction. The same trend appears in therapist-led group sessions inside community-centric apps where peers share coping strategies. Providers report that hybrid users churn less than app-only users because relational anchors deepen engagement. Investment is shifting toward omnichannel infrastructure, allowing data to flow between app, browser, and clinic, giving clinicians a unified view of each client’s mood trajectory.

By Mental-health Condition: Trauma-informed Care Gains Ground

Anxiety & Stress solutions dominated focus areas at 46.45% in 2024 as academic pressure, economic precarity, and social injustice drove everyday anxiety among Gen Z. Depression remained critical, reinforced by pandemic fallout and social isolation. Sleep Disorders are increasingly recognized as co-morbid with anxiety; Gen Z instruction on “sleepmaxxing” highlights that better rest correlates with mood stability. PTSD & Trauma interventions are set to rise fastest at an 11.07% CAGR, reflecting increased awareness of collective trauma from school violence, climate anxiety, and pandemic disruptions. Consequently, the Gen Z mental health market size for trauma-specific digital therapies could expand markedly as VR exposure therapy and peer-support gaming communities gain reimbursement codes. Other conditions, such as social media addiction, capture early attention but lack clear diagnostic frameworks, leaving room for innovation once consensus definitions emerge.

Market players differentiate by tailoring content to cultural factors. Trauma-informed modules increasingly address systemic oppression and intergenerational stressors, matching Gen Z’s social-justice outlook. Research published in Nature confirms that VR exposure can significantly reduce avoidance behaviors in anxiety disorders, bolstering reimbursement arguments. Providers that link sleep tracking with psychotherapy display higher adherence, as users see real-time correlations between routines and mental health scores. Ongoing expansion into trauma care underscores the market’s transition from general wellness toward condition-specific, clinically grounded interventions.

By End User: Institutional Purchase Pathways Multiply

Individual Consumers still accounted for 64.78% of spending in 2024 because app stores and subscription models empower direct access. However, Enterprises & Employers are expanding fastest at an 11.72% CAGR as talent retention hinges on mental-health offerings. The Gen Z mental health market share for consumer purchases will gradually yield space to institutional buyers once insurers routinely cover digital therapies. Healthcare Providers adopt digital platforms more cautiously due to evidence requirements but represent eventual high-value customers once clinical outcomes prove durable. Educational Institutions adopt campus-wide packages that include screening, peer communities, and emergency telepsychiatry, striving to stem counseling waitlists. The Gen Z mental health market size influenced by universities will likely rise as accreditation bodies embed wellness metrics into quality benchmarks.

Corporate programs increasingly tie mental-health goals to performance indicators such as absenteeism and productivity. Spring Health’s ability to show USD-denominated employer savings on medical claims strengthens the enterprise value proposition. Universities deploy stepped-care models: automated chat triage escalates to group coaching or teletherapy depending on severity, optimizing stretched counselor capacity. Start-ups that integrate enterprise, education, and consumer channels through single sign-on arrangements gain scale efficiencies and cross-sector resilience.

Geography Analysis

North America maintained 43.46% share in 2024 due to FDA leadership on digital-therapy approvals, Medicare reimbursement pilots, and abundant venture funding. Early adopters include corporations that view wellness as a retention lever and payers that face regulatory parity rules requiring equal mental and physical health coverage. Rural broadband gaps still hinder access; counties with limited connectivity hold three times fewer resources, prompting federal grants to subsidize infrastructure. Market vendors respond with low-bandwidth modalities such as SMS-based CBT to reach underserved Gen Z populations.

Europe forms a sizeable market where stringent privacy laws both impose compliance costs and elevate user trust. The UK Medicines and Healthcare products Regulatory Agency published guidance defining evidence thresholds for digital therapeutics, offering clearer commercial pathways. The EU’s GDPR keeps privacy high on Gen Z priority lists, with 73% ranking data protection when choosing mental-health apps. Political attention is rising: France declared mental health a national cause for 2025, and cross-sector frameworks like “Mental Health in All Policies” embed welfare considerations into transport, education, and labor agendas. Vendors that bake privacy-by-design architectures into apps enjoy smoother approvals and stronger brand credibility.

Asia-Pacific is forecast to record a 10.87% CAGR through 2030, making it the fastest-growing regional cluster. Smartphone penetration combined with cultural shifts toward individual well-being fuels rapid uptake. Nations such as Japan and South Korea pioneer emotion-sensing wearables that feed biofeedback loops into mindfulness apps. Indonesia’s “healing” trend signifies burgeoning demand for self-care micro-retreats. Mental-health stigma persists, yet the sizable disability-adjusted life year (DALY) burden — 37.2% from depressive disorders and 21.5% from anxiety — shapes government agendas, opening public-private collaboration opportunities. Cross-border regulatory divergence remains a barrier; companies rely on country-by-country localization, which slows rollout but elevates culturally tailored content quality.

Competitive Landscape

The Gen Z mental health market displays moderate fragmentation. Headspace, Calm, BetterHelp, and Talkspace command strong brand recognition in meditation and teletherapy, but VR/AR and AI niches teem with start-ups. Consolidation is underway: Teladoc acquired UpLift to integrate reimbursement-friendly therapy pipelines, and NeuroFlow merged with Owl, extending its measurement footprint to 17 million covered lives. Patent activity in emotion-sensing wearables suggests future competitive advantage will derive from proprietary signal processing more than content libraries. Traditional clinics simultaneously face disruption and partnership opportunities as digital players seek licensed clinicians for hybrid models.

Strategic alliances blur industry boundaries. Headspace Health’s USD 3 billion merger with Ginger fused coaching, therapy, and psychiatric services, creating an end-to-end continuum that meets Gen Z expectations for seamless escalation paths. Meanwhile, device manufacturers collaborate with content providers: Meta supplies the hardware, while mental-health brands produce clinically informed VR modules. The FDA’s stance that software can qualify as a medical device encourages incumbents equipped with regulatory muscle, while smaller consumer-only apps may struggle to finance evidence trials, nudging them toward acquisition or niche positioning.

Market differentiation hinges on evidence and equity. Players that publish peer-reviewed outcomes leverage those studies in payer negotiations. Equity considerations resonate with Gen Z’s social-justice ethos; apps that offer sliding-scale models or community sponsorships gain reputational capital. Intellectual property around biosensors could become a moat, as demonstrated by Feel Therapeutics’ recent patent. Investors remain bullish on neuro-tech, but due diligence increasingly scrutinizes retention and outcome metrics over pure download counts.

Gen Z Mental Health Industry Leaders

BetterHelp

Headspace Inc.

Brightside Health Inc.

Talkspace Inc.

Mindstrong Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Teladoc acquired UpLift for USD 30 million, adding insurance-based therapy to BetterHelp’s portfolio to serve 100 million covered lives

- May 2025: Eleos Health raised USD 60 million Series C funding to expand its AI behavioral-health platform

- January 2025: Avel eCare purchased Amwell Psychiatric Care, extending crisis support to 46 states.

Global Gen Z Mental Health Market Report Scope

As per the scope of the report, generation Z is defined as individuals born between 1997 and 2012. The Gen Z mental health market is segmented by age, gender, disease, and geography. By age, the market is segmented into 12-16 years, 17-21 years, and 22-27 years. By gender, the market is segmented into male and female. By disease, the market is segmented into anxiety, depression, substance use disorders, eating disorders, and other disorders (attention deficit hyperactivity disorder, post-traumatic stress disorder, etc.). By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers market sizes and forecasts in value (USD) for the above segments.

| Meditation & Mindfulness Apps |

| Digital Therapy Platforms |

| Emotion-sensing Wearables |

| VR/AR Mental Wellness Solutions |

| AI Chatbots & Companion Apps |

| Mobile Application |

| Web-based |

| In-person Hybrid |

| Anxiety & Stress |

| Depression |

| Sleep Disorders |

| PTSD & Trauma |

| Others |

| Individual Consumers |

| Enterprises & Employers |

| Healthcare Providers |

| Educational Institutions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Meditation & Mindfulness Apps | |

| Digital Therapy Platforms | ||

| Emotion-sensing Wearables | ||

| VR/AR Mental Wellness Solutions | ||

| AI Chatbots & Companion Apps | ||

| By Delivery Mode | Mobile Application | |

| Web-based | ||

| In-person Hybrid | ||

| By Mental-health Condition | Anxiety & Stress | |

| Depression | ||

| Sleep Disorders | ||

| PTSD & Trauma | ||

| Others | ||

| By End-user | Individual Consumers | |

| Enterprises & Employers | ||

| Healthcare Providers | ||

| Educational Institutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Gen Z mental health market?

The market is valued at USD 33.44 billion in 2025 and is projected to reach USD 49.70 billion by 2030.

Which product category leads revenue generation?

Meditation & Mindfulness Apps hold 38.12% share, making them the largest product segment.

Why are enterprises investing so heavily in Gen Z mental health benefits?

Surveys show 61% of Gen Z employees would leave jobs lacking adequate mental-health support, driving employer adoption of digital wellness programs.

What makes VR/AR therapeutics attractive for Gen Z users?

Immersive environments align with gaming preferences and create controlled exposure scenarios that ease anxiety and PTSD symptoms.

How fast is the Asia-Pacific market expanding?

Asia-Pacific is expected to grow at a 10.87% CAGR through 2030, the highest regional rate in the forecast period.

Page last updated on: