Robotic Neurorehabilitation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

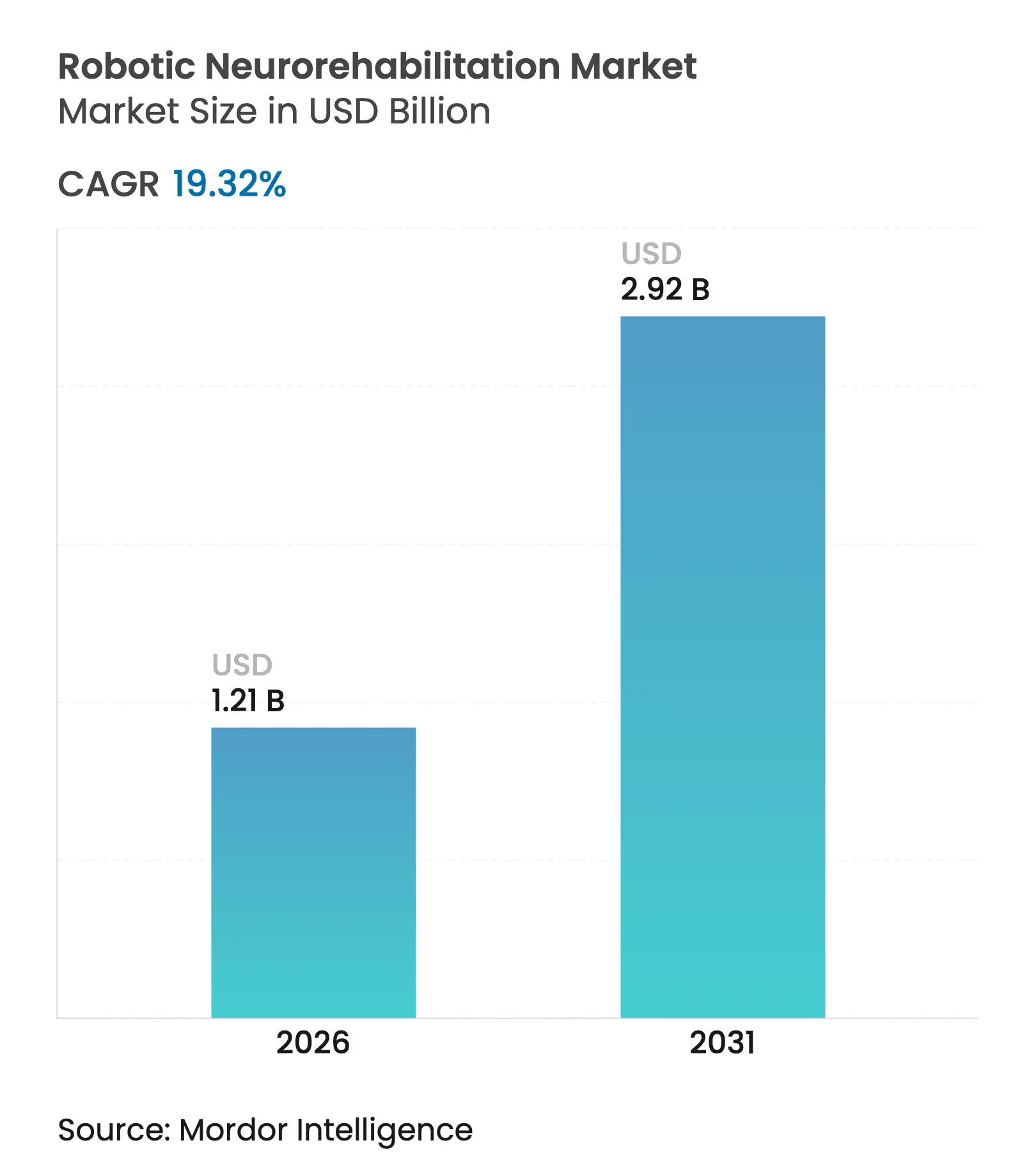

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 2.92 Billion |

| Growth Rate (2026 - 2031) | 19.32 % CAGR |

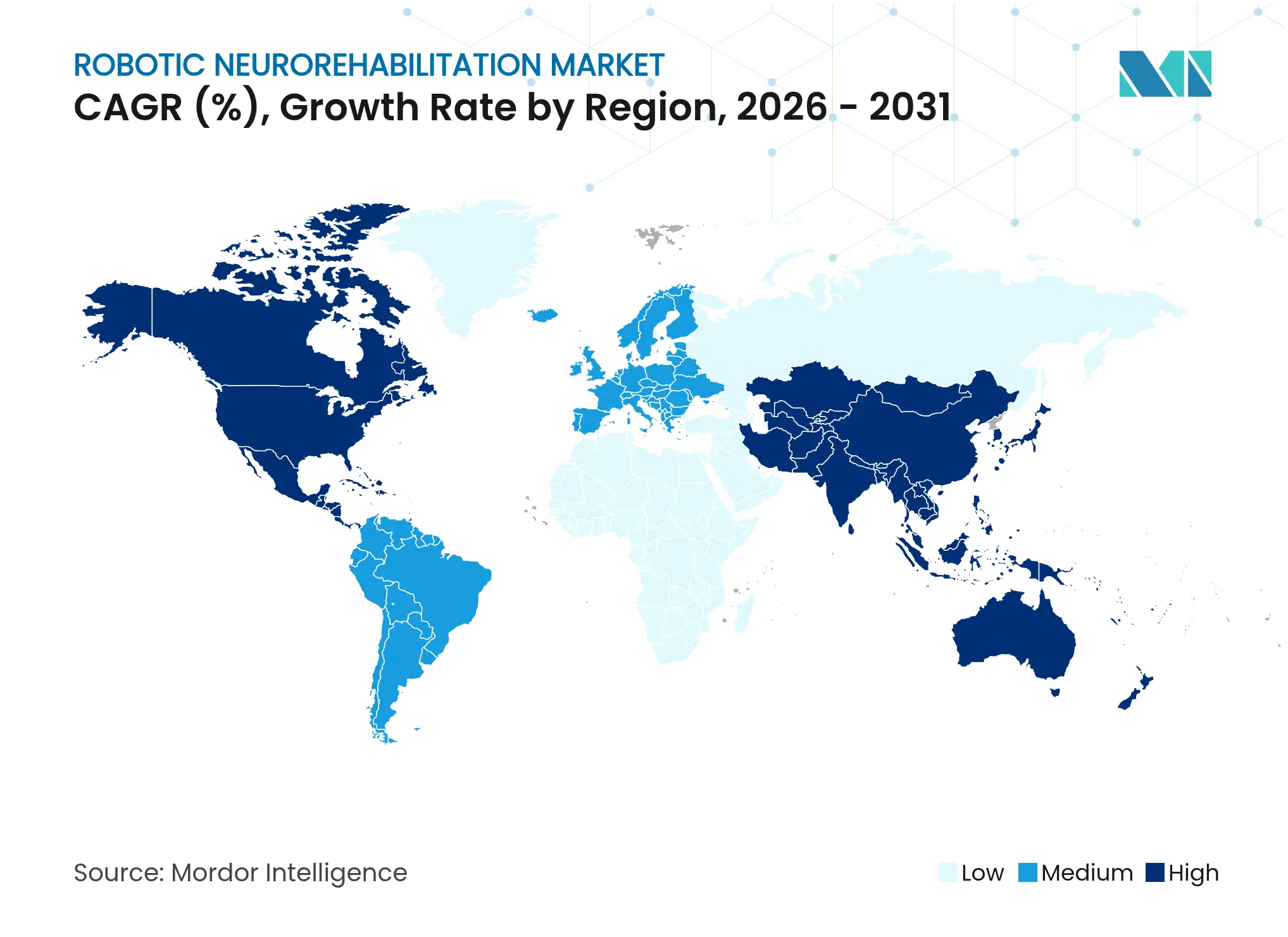

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

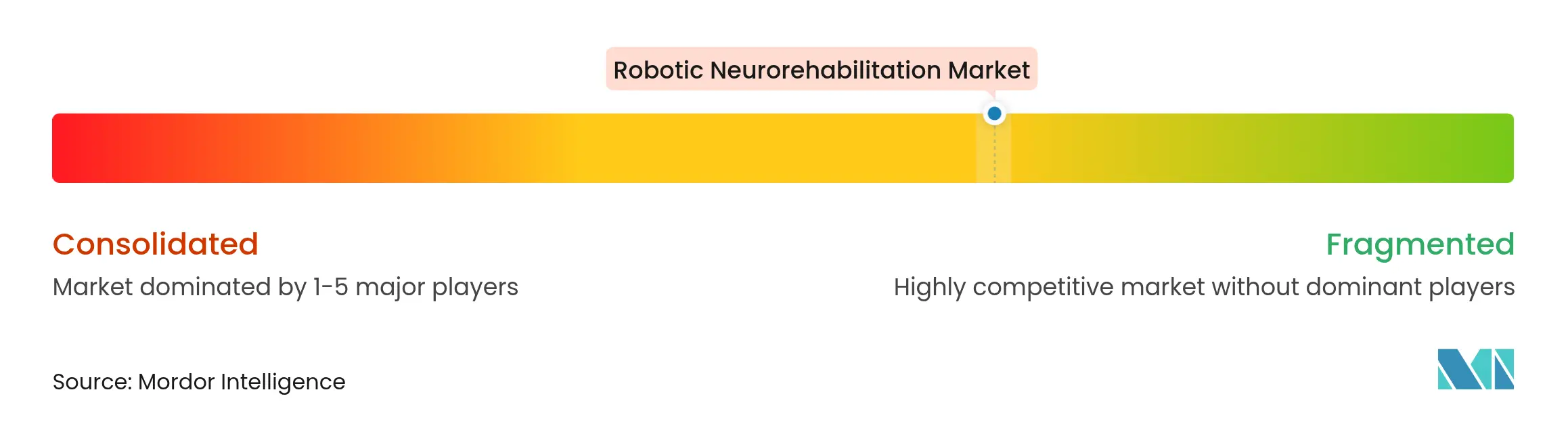

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Robotic Neurorehabilitation Market Analysis by Mordor Intelligence

The robotic neurorehabilitation market size was valued at USD 1.01 billion in 2025 and estimated to grow from USD 1.21 billion in 2026 to reach USD 2.92 billion by 2031, at a CAGR of 19.32% during the forecast period (2026-2031). Accelerated stroke incidence, value-based reimbursement reforms, and artificial-intelligence-enabled robotic platforms are converging to elevate demand, while clinical evidence showing superior functional outcomes encourages rapid clinical adoption [1]Nature Reviews Neurology, “Robotic Rehabilitation for Neurological Disorders,” nature.com. Hospitals and integrated health systems view these solutions as strategic assets that lower long-term care costs, and investors are channeling capital into firms that can scale home-based telerehabilitation programs. Competitive dynamics are characterized by ecosystem building, with hardware leaders partnering with software specialists to deliver end-to-end therapeutic solutions. North America anchors early-stage adoption, but Asia-Pacific’s health-technology modernization initiatives are set to redefine global revenue distribution over the next five years.

Key Report Takeaways

- By product type, devices led with 67.05% revenue share in 2025; software and services are projected to post a 20.20% CAGR to 2031.

- By technology, end-effector platforms accounted for 61.60% of the robotic neurorehabilitation market share in 2025, while exoskeleton systems are poised for a 19.85% CAGR through 2031.

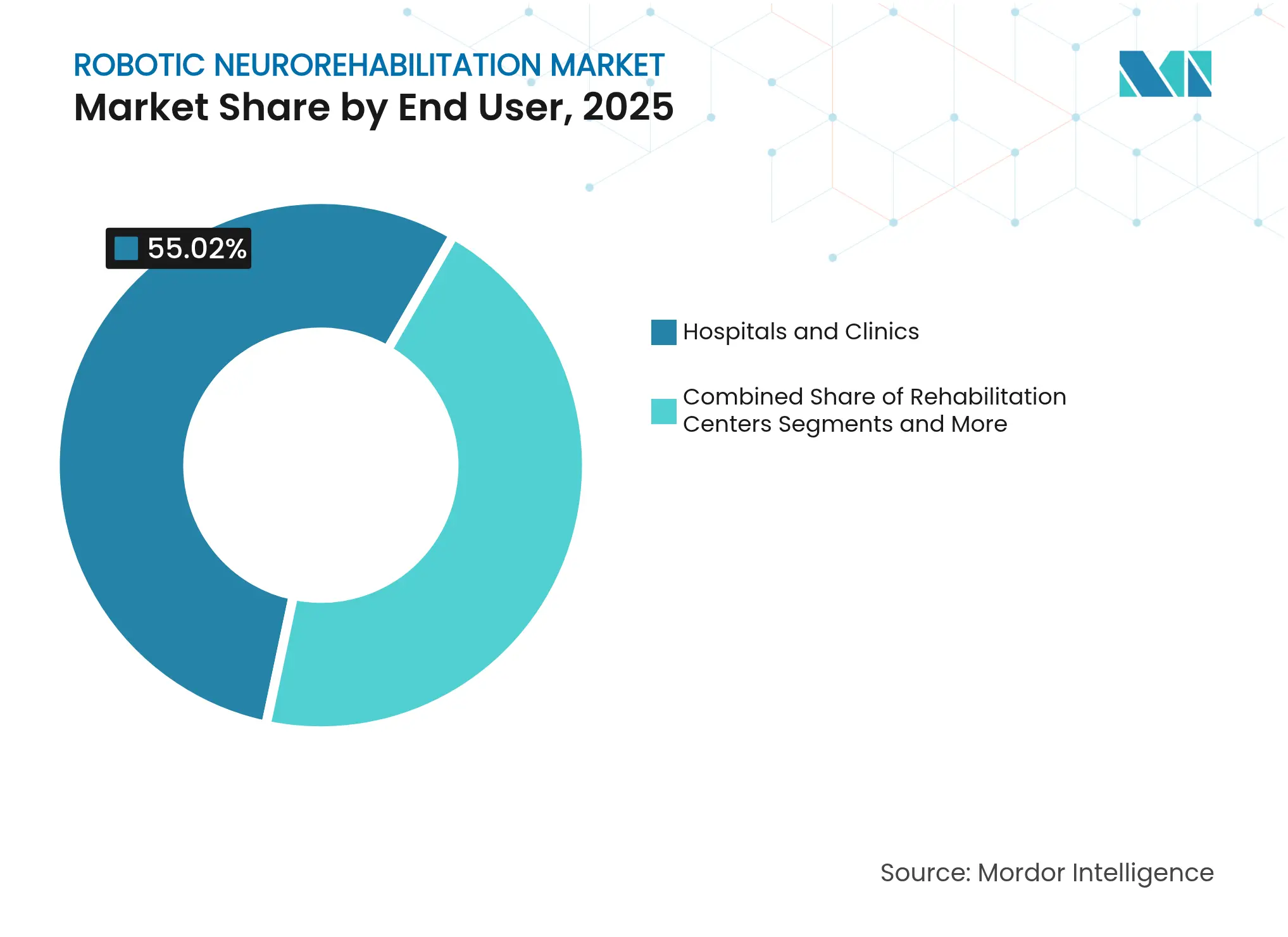

- By end user, hospitals and clinics held 55.02% share in 2025; rehabilitation centers will progress at a 20.05% CAGR to 2031.

- By application, stroke commanded 37.35% of the robotic neurorehabilitation market size in 2025, whereas spinal cord injury applications are forecast to expand at 19.90% CAGR to 2031.

- By geography, North America contributed 42.98% revenue in 2025; Asia-Pacific is advancing at a 20.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Robotic Neurorehabilitation Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing prevalence of stroke & neurological

disorders

Increasing prevalence of stroke & neurological

disorders

| +4.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+4.2%

|

Geographic Relevance

:

Global, with highest impact in North America & Europe

|

Impact Timeline

:

Long term (≥ 4 years)

|

Demonstrated superior clinical outcomes vs. conventional

therapy

Demonstrated superior clinical outcomes vs. conventional

therapy

| +3.8% | Global, early adoption in developed markets | Medium term (2-4 years) | |||

Technological advances in robotics, AI & sensing

Technological advances in robotics, AI & sensing

| +3.5% | North America & Europe core, spillover to APAC | Medium term (2-4 years) | |||

Rapidly ageing population with mobility impairment

Rapidly ageing population with mobility impairment

| +2.9% | Developed markets globally, Japan leading | Long term (≥ 4 years) | |||

Expansion of home-based telerehabilitation platforms

Expansion of home-based telerehabilitation platforms

| +2.1% | North America & Europe, emerging in APAC | Short term (≤ 2 years) | |||

Outcome-linked reimbursement reforms in EU & Japan

Outcome-linked reimbursement reforms in EU & Japan

| +1.8% | Europe & Japan, expanding to other developed markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Prevalence of Stroke & Neurological Disorders

Global neurological disease burdens climbed sharply between 2020 and 2024, with stroke incidence rising 15% and spinal cord injuries expanding 8% annually. Younger working-age cohorts (45–65 years) now represent a larger share of stroke survivors, requiring longer, more intensive rehabilitation that favors robotic protocols. Asia-Pacific’s urbanization has compounded lifestyle-related cerebrovascular risks, producing a wave of high-motivation patients eager for technologically advanced therapy. These epidemiological shifts sustain consistent demand for the robotic neurorehabilitation market and reinforce the multi-year growth trajectory.

Demonstrated Superior Clinical Outcomes vs. Conventional Therapy

A 2024 meta-analysis of 47 randomized trials recorded 23% greater motor-function improvement from robotic therapy versus standard care, with benefits persisting six months post-treatment [2]Journal of NeuroEngineering and Rehabilitation, “Meta-Analysis of Robotic Rehabilitation Efficacy,” biomedcentral.com . Insurance agencies increasingly reference these data when approving coverage, while the FDA granted breakthrough designation to three systems in 2024, reducing time-to-market hurdles. Cost-of-care studies show a 28% decline in long-term nursing expenses when robotic modalities are used early, aligning both clinical and economic incentives for providers.

Technological Advances in Robotics, AI & Sensing

Machine-learning algorithms now adapt therapy intensity in real time based on muscle activation data, individualizing patient pathways and boosting engagement. Sensor fusion combining inertial data, electromyography, and computer vision yields millimeter-level motion tracking, while soft-robotic architectures have trimmed device mass by 35% without sacrificing actuation strength. Cloud analytics enable therapists to adjust protocols remotely, supporting scalable home-care deployment that broadens the robotic neurorehabilitation market footprint.

Rapidly Ageing Population with Mobility Impairment

United Nations forecasts show a 45% jump in the ≥ 65-year cohort between 2025 and 2035, with Japan already at 32% in this demographic. As survival after neurological events improves, older adults require longer recovery horizons. Medicare records indicate robotic therapy recipients exhibit 31% fewer nursing-home placements within 24 months post-stroke, validating technology investments for budget-constrained health systems.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capital and maintenance cost of robotic systems

High capital and maintenance cost of robotic systems

| -2.8% | Global, most pronounced in emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-2.8%

|

Geographic Relevance

:

Global, most pronounced in emerging markets

|

Impact Timeline

:

Medium term (2-4 years)

|

Limited ADL evidence & reimbursement gaps

Limited ADL evidence & reimbursement gaps

| -2.1% | Developing markets, selective impact in developed regions | Short term (≤ 2 years) | |||

Shortage of therapists trained on robotic devices

Shortage of therapists trained on robotic devices

| -1.7% | Global, acute in rural and underserved areas | Medium term (2-4 years) | |||

Cyber-security & data-privacy risks in connected

robots

Cyber-security & data-privacy risks in connected

robots

| -1.2% | Developed markets with strict data regulations | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital and Maintenance Cost of Robotic Systems

Advanced multi-axis platforms range from USD 500,000 to USD 1.5 million, with annual service contracts adding another 12–15% of purchase value [3]Healthcare Financial Management Association, “Capital Planning for Robotics,” hfma.org . Mid-size centers often require ≥ 150 billable sessions per year to break even, a threshold many rural facilities cannot reach. Leasing options introduced in 2024 dropped upfront capital outlays by 60%, yet monthly fees of USD 15,000–25,000 remain prohibitive for facilities with thin margins.

Limited ADL Evidence & Reimbursement Gaps

While motor-score gains are well-documented, translation into activities-of-daily-living improvements remains under-evidenced for traumatic brain injury and degenerative disorders. U.S. insurers frequently cap authorized sessions at 30 per episode, citing insufficient longitudinal data. European health-technology assessors demand cost-effectiveness studies lasting up to 24 months, slowing coverage expansion timelines. These evidence gaps temper near-term growth for the robotic neurorehabilitation market in cost-sensitive regions.

Segment Analysis

By Product Type: Software Integration Drives Ecosystem Value

Devices sustained 67.05% of 2025 revenue, yet software and services are expanding at a 20.20% CAGR as providers prioritize data-driven platforms. The robotic neurorehabilitation market size for software is projected to widen materially as AI-powered treatment engines become integral to care pathways. Upper-extremity devices remain the installation backbone, treating diverse post-stroke impairments, whereas lower-limb systems are rapidly onboarding spinal cord injury patients. Disposable sensor consumables deliver a predictable revenue stream and elevate lifetime value per installation.

Advanced analytics suites, FDA-cleared in 2024, allow therapists to customize sessions remotely, knitting in virtual reality modules that raise patient motivation. Outcome-based pricing models, where providers pay only when pre-agreed functional gains are achieved, are emerging and favor SaaS-style contracts. These shifts underscore how digital capabilities, not hardware alone, now define competitive advantage within the robotic neurorehabilitation market.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Exoskeletons Challenge End-Effector Dominance

End-effector platforms held 61.60% market share in 2025, reflecting a mature evidence base and multi-indication flexibility. However, exoskeleton solutions are registering a 19.85% CAGR, buoyed by 40% weight reductions and improved battery life that enhance patient compliance. The FDA’s 2024 authorization of EksoNR for stroke expanded exoskeleton indications beyond spinal cord injury, opening the largest neurological rehab cohort to this technology.

Competitive blurring is intensifying as end-effector incumbents develop hybrid models incorporating thoraco-lumbar supports, while exoskeleton specialists secure patents that streamline gait biomechanics. Because portable exosuits allow partial weight-bearing therapy in outpatient settings, they broaden the robotic neurorehabilitation market penetration in lower-acuity care segments.

By End User: Specialized Centers Drive Innovation Adoption

Hospitals and clinics accounted for 55.02% revenue in 2025, leveraging integrated stroke units and multi-disciplinary teams to maximize throughput. These settings often bundle robotic therapy into bundled-payment episodes, aligning financial incentives with quicker patient discharge. Rehabilitation-center demand is scaling at 20.05% CAGR as stand-alone facilities seek technology differentiation to secure referral flows.

Home-care deployments remain nascent but strategic. Portable units combined with telerehabilitation platforms enable session continuity after inpatient discharge, reducing readmission risks and expanding the robotic neurorehabilitation market into chronic-phase care. Training programs, like Kinova’s 2024 therapist certification, aim to mitigate workforce constraints, a critical adoption determinant in non-academic settings.

Note: Segment shares of all individual segments available upon report purchase

By Application: Spinal Cord Injury Emerges as Growth Driver

Stroke maintained a 37.35% revenue share in 2025, anchored by well-established clinical pathways that incorporate robotics as early as 48 hours post-event. In contrast, spinal cord injury revenue is growing at 19.90% CAGR as younger patients pursue aggressive mobility restoration; this cohort’s longer life expectancy magnifies lifetime value per recovered function. Traumatic brain injury use cases grew following sports-league and military investment in evidence generation that links cognitive-motor integration to improved return-to-work metrics.

Regulatory acceptance broadened in 2024 when FDA added neurodegenerative disorders, such as multiple sclerosis, to several robotic device clearances, creating multi-year volume tailwinds. As clinical trials mature, disease-progression-slowing evidence could further enlarge the robotic neurorehabilitation market size in these sub-segments.

Geography Analysis

North America led with 42.98% of 2025 sales, supported by Medicare’s 2024 reimbursement expansion and 400+ installed systems across major U.S. centers. Canadian provinces integrate robotics into publicly funded stroke pathways, while Mexico’s medical-tourism hospitals adopt premium rehabilitation suites to attract foreign patients. FDA breakthrough designations streamline new product introductions and sustain the region’s innovation cycle.

Europe’s harmonized CE-marking regime accelerates multi-country rollouts, with Germany and the United Kingdom anchoring volume through statutory insurance and NHS stroke-care mandates. France and Italy are scaling deployments under regional modernization grants, and pan-EU outcome-based reimbursement schemes reward documented functional gains. Rigorous health-technology assessments add lead time but ultimately de-risk payer adoption, fostering predictable market expansion.

Asia-Pacific is the fastest-growing zone at 20.10% CAGR, driven by Japan’s national insurance coverage, South Korea’s smart-hospital investments, and China’s tier-1-city health-reform budgets. Australia’s Therapeutic Goods Administration offers a transparent approval route, while India’s private hospital chains pilot cost-sharing models around portable devices. Government technology-localization incentives and aging demographics suggest the region could claim a materially larger share of the robotic neurorehabilitation market by 2030.

Competitive Landscape

Market Concentration

The robotic neurorehabilitation market is moderately concentrated, with DIH (Hocoma) and Ekso Bionics holding significant portfolios validated through multi-center trials. Patent density in actuation mechanisms and AI control algorithms creates structural barriers for entrants, though smaller firms exploit software-only delivery that bypasses capital constraints. Strategic moves in 2024 included Hocoma’s USD 25 million AI module upgrade, Ekso’s pediatric breakthrough designation, and ReWalk’s partnership with Samsung for 5G-connected exoskeletons.

Players increasingly bundle hardware, software, and cloud analytics into subscription packages that align cost with usage and outcomes. Ecosystem collaborations—such as BIONIK’s virtual-reality integration and Tyromotion’s Singapore plant—highlight a pivot toward regional manufacturing and experience-rich digital platforms. Competitive white space remains in pediatric neurological conditions and neurodegenerative maintenance therapy, areas underserved by incumbent product configurations.

Ongoing therapist-training initiatives and asset-light portable designs lower adoption hurdles, enabling smaller providers to participate. Over time, outcome-linked pricing and at-home models may redistribute revenue toward software-centric challengers, reshaping the robotic neurorehabilitation market competitive hierarchy.

Robotic Neurorehabilitation Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Hocoma allocated USD 25 million to embed real-time AI-personalization in the Armeo platform, deepening data-driven therapy capabilities.

- September 2024: Ekso Bionics obtained FDA breakthrough designation for EksoNR pediatric use, opening cerebral palsy and spinal-injury indications.

- August 2024: ReWalk Robotics and Samsung Electronics committed USD 15 million to co-develop 5G sensor-rich exoskeletons for remote monitoring.

- July 2024: BIONIK Laboratories introduced InMotion ARM with immersive VR, securing CE marking and pending FDA clearance.

Table of Contents for Robotic Neurorehabilitation Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increasing prevalence of stroke & neurological disorders

- 4.2.2Demonstrated superior clinical outcomes vs. conventional therapy

- 4.2.3Technological advances in robotics, AI & sensing

- 4.2.4Rapidly ageing population with mobility impairment

- 4.2.5Expansion of home-based telerehabilitation platforms

- 4.2.6Outcome-linked reimbursement reforms in EU & Japan

- 4.3Market Restraints

- 4.3.1High capital and maintenance cost of robotic systems

- 4.3.2Limited ADL evidence & reimbursement gaps

- 4.3.3Shortage of therapists trained on robotic devices

- 4.3.4Cyber-security & data-privacy risks in connected robots

- 4.4Regulatory Landscape

- 4.5Technological Outlook

- 4.6Porter’s Five Forces Analysis

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product Type

- 5.1.1Devices

- 5.1.1.1Upper-Extremity

- 5.1.1.2Lower-Extremity

- 5.1.2Consumables & Accessories

- 5.1.3Software & Services

- 5.2By Technology

- 5.2.1End-Effector Robotics

- 5.2.2Exoskeleton Robotics

- 5.3By End User

- 5.3.1Hospitals and Clinics

- 5.3.2Rehabilitation Centers

- 5.3.3Home-Care Settings

- 5.3.4Other End Users

- 5.4By Application

- 5.4.1Stroke

- 5.4.2Spinal Cord Injury

- 5.4.3Traumatic Brain Injury

- 5.4.4Neurodegenrative Disorders

- 5.4.5Others

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4Australia

- 5.5.3.5South Korea

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration Analysis

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1DIH (Hocoma)

- 6.3.2Ekso Bionics

- 6.3.3Tyromotion GmbH

- 6.3.4BIONIK Laboratories

- 6.3.5Lifeward Inc.

- 6.3.6Humanware S.r.l.

- 6.3.7Rehab-Robotics Co. Ltd.

- 6.3.8Reha Technology AG

- 6.3.9Neofect

- 6.3.10AlterG Inc.

- 6.3.11Cyberdyne Inc.

- 6.3.12ReWalk Robotics

- 6.3.13Myomo Inc.

- 6.3.14Fourier Intelligence

- 6.3.15Motus Nova

- 6.3.16Kinova Inc.

- 6.3.17Barrett Technology

- 6.3.18G-EO Systems

- 6.3.19MagVenture Inc.

- 6.3.20Intellias (Icone)

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Global Robotic Neurorehabilitation Market Report Scope

Robot-assisted rehabilitation is a type of technology that helps the functional recovery of patients with stroke, traumatic brain injury, cerebral palsy, spinal cord injuries, Parkinson’s disease, and multiple sclerosis. Robotic neurorehabilitation devices are typically based on motor learning, which requires a patient’s effort and attention to perform intensive, repetitive, and task-oriented motor activities.

The robotic neurorehabilitation market is segmented into product type, end user, and geography. The market is segmented by product type into devices, consumables, accessories, and software and services. By devices, the market is segmented into upper extremity and lower extremity. By end user, the market is segmented into hospitals/clinics, cognitive care centers, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. The report also offers the market size and forecasts for 13 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD)