Cigar Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 59.73 Billion |

| Market Size (2031) | USD 77.39 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

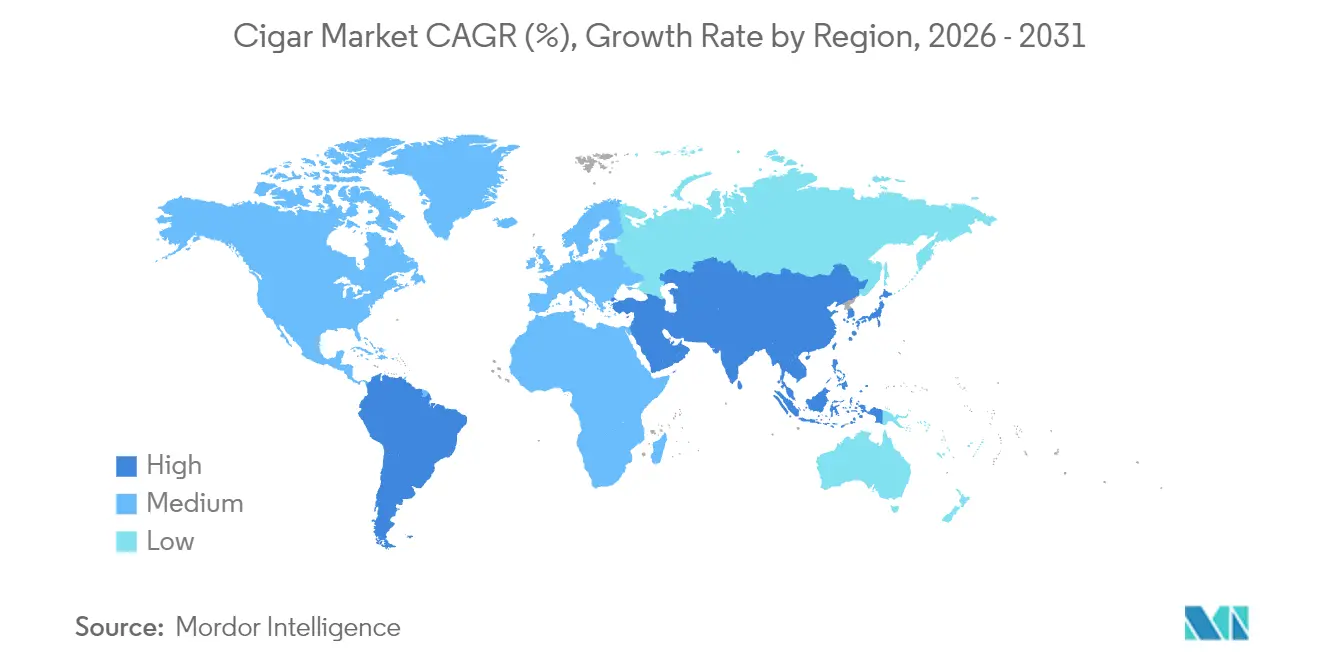

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cigar Market Analysis by Mordor Intelligence

The cigar market size is expected to grow from USD 56.70 billion in 2025 to USD 59.73 billion in 2026 and is forecast to reach USD 77.39 billion by 2031 at 5.34% CAGR over 2026-2031. Manufacturers in the market benefit from the premium pricing of hand-rolled and limited-edition cigars, which enables them to effectively manage the impact of increased taxation and rising raw material expenses. The Asia-Pacific region exhibits remarkable market expansion, driven by its substantial population of high-net-worth individuals, the ongoing recovery in international tourism, and the growing cultural acceptance of cigars as prestigious luxury items. To maintain their market position, manufacturers are investing in developing tobacco varieties from specific geographical regions and implementing advanced storage technologies, which ensures product quality and supports their premium pricing strategies in the market.

Key Report Takeaways

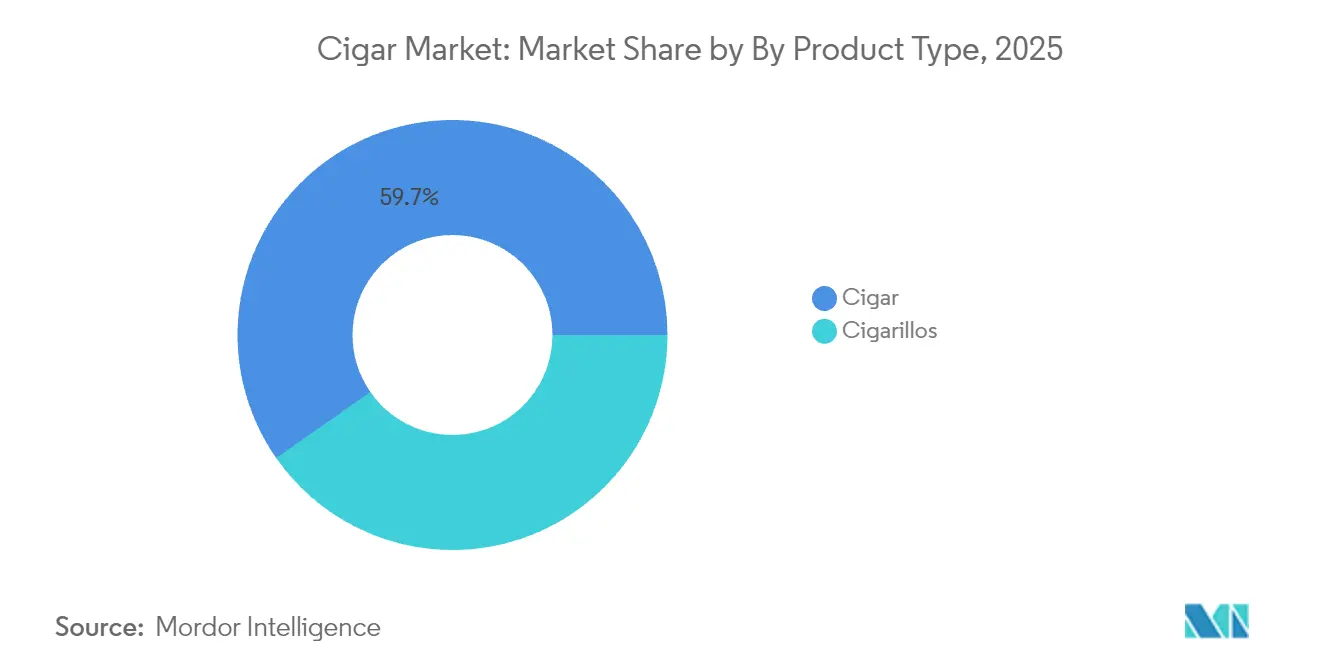

- By product type, traditional cigars led with 59.68% of global cigar market share in 2025, while cigarillos are set to climb at a 6.21% CAGR through 2031.

- By flavor, non-flavored variants accounted for 65.96% of global cigar market size in 2025; flavored offerings will pace ahead at a 6.53% CAGR to 2031.

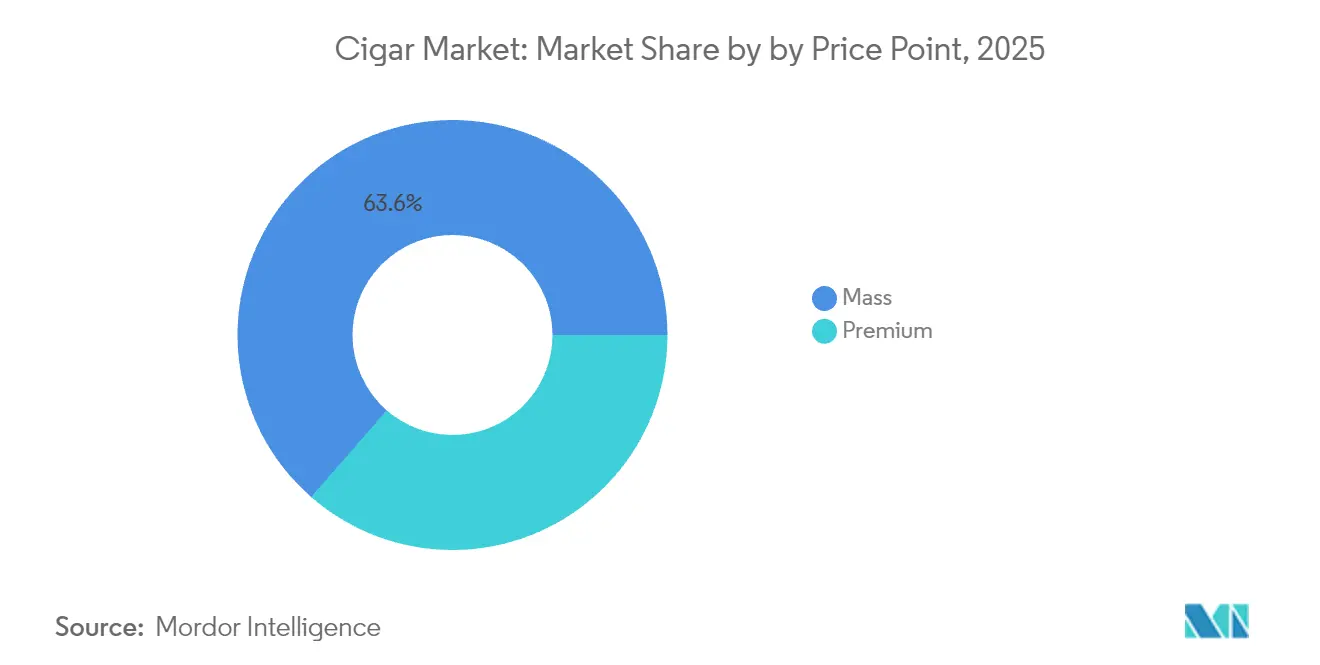

- By price point, mass-market cigars represented 63.58% of global cigar market size in 2025, whereas premium lines are projected to expand at a 6.44% CAGR through 2031.

- By distribution channel, offline retail stores controlled 87.94% of global cigar market share in 2025; online platforms will record the fastest 7.38% CAGR to 2031.

- By geography, Asia-Pacific held 54.21% of global cigar market share in 2025 and will maintain the highest 6.38% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cigar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Popularity of Premium and Hand-Rolled Cigars | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Product Innovation in Cigar Blends and Packaging | +0.8% | Global, led by Dominican Republic and Nicaragua | Long term (≥ 4 years) |

| Rising Consumer Preference for Luxury and Status Symbol Products | +1.1% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Growth of Boutique and Artisan Cigar Brands | +0.7% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Increasing Adoption of Humidor Technology for Better Preservation | +0.4% | Global, concentrated in premium segments | Short term (≤ 2 years) |

| Expansion of Online Retail Channels for Cigars | +0.6% | Global, fastest adoption in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Popularity of Premium and Hand-Rolled Cigars

Premium handmade cigars represent a small but highly valuable segment of the total cigar market, with United States imports showing steady growth in the current year. This segment demonstrates remarkable resilience during economic uncertainty, as consumers maintain their luxury tobacco purchases while reducing expenditure in other categories. Nicaragua maintains its position as the primary exporter of handmade cigars, while the Dominican Republic has experienced substantial growth in exports, indicating a significant shift in supply chain dynamics beyond traditional Cuban production. The market continues to evolve as mass-market consumers increasingly transition to artisanal products, influenced by social media engagement and changing consumption preferences focused on premium experiences. The pricing landscape has notably shifted upward, with entry-level premium cigars commanding higher price points, as tobacconists implement price adjustments in response to increased manufacturing costs.

Product Innovation in Cigar Blends and Packaging

The Dominican Republic's tobacco manufacturing sector has demonstrated remarkable progress, reaching USD 1.14 billion in exports during 2023 [1]Source: Observatory of Economic Complexity (OEC), “Cigars, cheroots and cigarillos, containing tobacco,” oec.world. This achievement stems from substantial investments in advanced climate-controlled facilities and robust quality assurance systems that align with rigorous international standards. Taking inspiration from the wine industry, manufacturers carefully select and promote specific growing regions and vintage tobacco leaves, creating distinctive products that resonate with premium market segments. Through meticulous attention to curing and fermentation processes, producers develop refined flavor profiles that meet consumer preferences. The industry has also embraced innovative packaging solutions, implementing sophisticated moisture control mechanisms and secure tamper-evident seals. These advancements ensure consistent product quality across extensive distribution networks, particularly benefiting the growing e-commerce sales channels.

Rising Consumer Preference for Luxury and Status Symbol Products

Cigar consumption has evolved into a significant social status indicator, moving beyond traditional tobacco use patterns, as consumers increasingly perceive premium cigars as sophisticated luxury items comparable to high-end wines or premium spirits. The Asia-Pacific region maintains a substantial 54.63% market share, demonstrating the rising affluence in emerging economies where premium cigars have become established symbols of professional achievement and cultural sophistication. The substantial recovery in Southeast Asian tourism, marked by a 32% increase in visitor arrivals during the first half of 2024, has strengthened the demand for luxury tobacco products across hotels, resorts, and upscale hospitality establishments [2]Source: Asian Development Bank, “Southeast Asia Outlook – September 2024,” adb.org. The prevalence of corporate gifting practices and special occasion consumption behaviors continues to support premium pricing strategies, effectively shielding manufacturers from the volume declines observed in mass-market segments. This transformation in consumption patterns enables companies to preserve their profit margins despite increasing regulatory oversight and tax implementations across major market regions.

Growth of Boutique and Artisan Cigar Brands

Small-batch cigar producers are gradually increasing their market share by focusing on meticulous craftsmanship, controlled production volumes, and fostering personal connections through direct-to-consumer sales channels. These boutique manufacturers effectively leverage social media platforms and immersive events to build strong customer relationships, particularly appealing to younger affluent consumers who value authenticity over mass production. By partnering with individual tobacco farms and specific growing regions, these companies develop origin-based narratives that support their premium pricing strategies and reinforce their unique market positioning. Additionally, the operational structure of artisan producers involves lower regulatory compliance costs compared to large-scale manufacturers, allowing them to respond swiftly to market demands and introduce product innovations efficiently. This shift in cigar production methods aligns with the broader consumer preference for artisanal products observed in the food and beverage industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Tobacco Regulations and Advertising Restrictions Globally | -1.8% | Global, most severe in Europe and developed markets | Long term (≥ 4 years) |

| High Taxation on Tobacco Products in Many Regions | -1.4% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Increasing Age Restrictions and Enforcement on Tobacco Sales | -0.6% | Global, strictest in developed markets | Short term (≤ 2 years) |

| Risks of Counterfeit and Smuggled Products Affecting Brand Trust | -0.4% | Global, concentrated in high-tax jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Tobacco Regulations and Advertising Restrictions Globally

The European Union's proposed tobacco taxation directive plans to increase cigar excise duties from EUR 12 to EUR 143 per thousand units, representing a potential 1,100% increase that may significantly impact medium-sized producers [3]Source: Jaeger, “Revision of the Tobacco Excise Tax Directive,” Taxpayers Association of Europe, taxpayers-europe.org. The European Commission's tax harmonization initiative, set to take effect in 2028, aims to standardize rates across member states and incorporate new products, including heated tobacco, into existing regulatory frameworks [4]Source: European Commision, “European Commission modernises Tobacco Taxation Directive,” commission.europa.eu. In the United States, Food and Drug Administration regulatory oversight imposes compliance requirements on premium handmade cigars, despite their small market share, requiring manufacturers to complete extensive approval processes for new products. Current advertising restrictions constrain brand development opportunities, particularly affecting boutique producers who depend on direct marketing channels. These regulatory requirements concentrate market influence among larger manufacturers with sufficient resources to manage compliance costs, potentially limiting innovation from smaller companies.

High Taxation on Tobacco Products in Many Regions

Germany's upcoming tobacco tax increases, scheduled for implementation at the start of the next fiscal year, will raise cigarette taxes and impose additional levies on other tobacco products, including cigars. China's recent implementation of substantial combined tariff rates on cigar imports and significant reduction in duty-free allowances for individual travelers has created barriers to market access. Tax harmonization efforts across European Union member states have created competitive disadvantages for producers in high-tax jurisdictions while potentially increasing illicit trade activities. The rising taxation disproportionately affects price-sensitive consumers in mass-market segments, accelerating premiumization as manufacturers shift toward higher-margin products that can better absorb tax increases. While these policies generate substantial government revenues, they also create opportunities for black market activities that undermine legitimate business operations and brand integrity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Traditional Cigars Anchor Market Value

The traditional cigar segment maintains its market leadership with a substantial 59.68% share in 2025, demonstrating the enduring appeal of full-size cigars among consumers who value traditional smoking experiences. This dominance reflects deep-rooted brand loyalty within premium segments, where customers appreciate the craftsmanship and ritual associated with traditional cigars. Meanwhile, the cigarillo segment is experiencing robust growth, projected at a 6.21% CAGR through 2031. This growth is primarily attributed to changing consumer preferences, as cigarillos offer a more time-efficient smoking experience that accommodates modern lifestyle constraints and workplace smoking policies. The market received additional momentum when Swisher entered the cannabis segment in Michigan during October 2024, introducing blunts with hemp wrappers that circumvent FDA tobacco regulations.

The manufacturing landscape significantly influences market dynamics, with cigarillo producers benefiting from cost-effective automated production methods compared to the labor-intensive process of handmade traditional cigars. Premium cigar manufacturers have recognized this opportunity and are strategically expanding their product portfolios to include cigarillo variants, enabling them to capture a broader consumer base while preserving their premium brand positioning. The regulatory environment also shapes market development, as traditional cigar producers face higher compliance costs due to comprehensive FDA oversight, while cigarillo manufacturers operate under more streamlined approval processes. These market conditions indicate an ongoing convergence between segments, as consumers increasingly gravitate toward products that balance premium quality with convenience and shorter consumption times.

By Flavor: Non-Flavored Dominance Faces Innovation Pressure

Non-flavored cigars accounted for a dominant 65.96% market share in 2025. This strong market position is attributed to traditional consumer preferences, which have remained consistent over time, and the regulatory advantages these products hold in regions with stringent flavor restrictions. Non-flavored cigars are often perceived as more authentic and closer to the original cigar experience, further solidifying their appeal among traditional consumers. Meanwhile, the flavored cigar segment is projected to grow at a compound annual growth rate (CAGR) of 6.53% through 2031. This growth is driven by manufacturers focusing on developing innovative products that align with regulatory requirements while catering to the evolving preferences of younger adult consumers who seek unique and diverse flavor options.

In the Philippines tobacco market, 58.49% of tobacco products feature flavor descriptors, with menthol being the most prominent category. This highlights a clear consumer preference for flavored tobacco products, which manufacturers are leveraging to expand their market presence. To address this demand, manufacturers are making strategic investments in advanced natural flavoring technologies and refined tobacco blending techniques. These innovations enable the creation of unique and appealing taste profiles that resonate with consumers while ensuring compliance with regulatory frameworks. Such efforts not only enhance product differentiation but also strengthen the competitive positioning of manufacturers in the market.

By Price Point: Mass Market Volume Supports Premium Growth

Mass-market products account for 63.58% of the market share in 2025, establishing a robust foundation for the industry's distribution network and manufacturing operations. This significant market presence enables companies to achieve substantial economies of scale, which in turn supports the broader industry infrastructure and operational efficiency.

The premium segment is projected to grow at a 6.44% CAGR through 2031, as consumers increasingly gravitate toward higher-priced products and manufacturers strategically focus on higher-margin offerings to counterbalance rising regulatory compliance costs and taxation. Imperial Brands' Backwoods brand demonstrates this trend effectively, having successfully positioned itself in the premium category within mass-market channels and continuing to gain market share despite economic headwinds. Market analysis of price elasticity reveals an interesting consumer behavior pattern - premium segment customers maintain their purchasing habits during economic uncertainty, while the mass-market segment experiences notable volume constraints due to increased taxation and regulatory restrictions.

By Distribution Channel: Offline Dominance Faces Digital Disruption

Physical retail stores maintain a dominant position with an 87.94% market share in 2025. This substantial market presence stems from strict regulatory requirements mandating in-person age verification for purchases. Additionally, many consumers prefer the traditional shopping experience, where they can physically examine and evaluate products before making purchasing decisions.

Online retail channels are projected to experience significant growth, with a 7.38% CAGR through 2031. This growth is driven by increasing consumer demand for convenient shopping options and access to a wider product selection than traditional stores can offer. Digital platforms have transformed the market landscape by enabling small-scale producers to reach international customers without investing in physical distribution networks. This shift has intensified market competition and is expected to accelerate further as potential FDA flavor restrictions could reduce convenience store inventory, compelling consumers to turn to online retailers for discontinued products.

Geography Analysis

Asia-Pacific currently dominates the global premium tobacco market, commanding a substantial 54.21% market share in 2025. The region's market leadership is underpinned by its large consumer base, established distribution networks, and the cultural significance of premium tobacco products. Japan serves as a notable example of the region's evolving market dynamics, where a significant 52.6% decline in cigarette sales from 2011-2023 has created new opportunities for premium cigars to position themselves as luxury alternatives.

North America demonstrates the fastest market development, characterized by its mature premium cigar culture and sophisticated distribution infrastructure. The region's growth is supported by a well-established network of specialty retailers, knowledgeable consumers, and a strong presence of boutique brand manufacturers. The market benefits from consistent demand patterns and a regulatory environment that has historically accommodated premium tobacco products.

Other regions present diverse market opportunities and challenges. Latin American production regions maintain their significance, with the Dominican Republic achieving USD 1.14 billion in export value and Nicaragua producing 210.9 million units, leveraging their favorable growing conditions and manufacturing expertise. European markets face potential restructuring due to proposed taxation directives, which may lead to market consolidation among larger manufacturers. The Middle East and Africa regions show promise as emerging markets, with increasing demand driven by rising tourism and growing affluent consumer segments.

Competitive Landscape

The cigar industry is experiencing significant transformation through strategic acquisitions and market consolidation. Japan Tobacco's substantial USD 2.4 billion acquisition of Vector Group in 2024 demonstrates this trend, as it successfully expanded its United States market presence from 2.3% to approximately 8%. This consolidation enables companies to build stronger market positions through economies of scale and geographic diversification, which helps them effectively manage increasing regulatory compliance costs and tax burdens while maintaining their competitive edge. Imperial Brands' strategic focus on five key markets, which generate 70% of its adjusted operating profit, showcases how geographic concentration and targeted resource allocation can optimize market penetration. Large manufacturers continue to leverage their established distribution networks and comprehensive brand portfolios to maintain market dominance, while boutique producers carve out their niche through specialized craftsmanship and direct customer relationships that circumvent traditional retail channels.

The integration of technology has become a crucial differentiator in the cigar industry, particularly in supply chain management, product preservation, and customer engagement. Companies are investing in advanced humidor systems and climate-controlled storage solutions to ensure consistent product quality and support premium positioning in the market. Digital marketing platforms have emerged as essential tools for targeted customer acquisition and retention strategies. This technological advancement is complemented by product innovation, as demonstrated by Swisher's development of cannabis blunt products using hemp wrappers, which showcases how companies can create new market segments while leveraging existing tobacco brand recognition. The online retail channel presents significant opportunities with a 7.53% CAGR, alongside growing potential in premium product categories and emerging geographic markets where regulatory environments remain conducive to industry growth.

The regulatory landscape continues to shape market dynamics and competitive intensity. The FDA's proposed flavor ban could significantly impact the industry by potentially eliminating up to half of convenience store inventory. This regulatory pressure is forcing manufacturers to compete more aggressively for reduced shelf space while simultaneously investing in product reformulation and enhanced compliance capabilities. Companies must navigate these challenges while maintaining their market position and exploring new growth opportunities.

Cigar Industry Leaders

Scandinavian Tobacco Group A/S

Imperial Brands PLC

China National Tobacco Corp.

Altria Group Inc.

Swisher International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Swisher International launched cannabis blunt products in Michigan market, using hemp wrappers to avoid FDA regulation while leveraging tobacco branding. The product innovation demonstrates regulatory arbitrage strategies and market expansion into adjacent cannabis categories

- April 2024: E.P. Carrillo announced the launch of the two additional lines under the Encore brand, Encore Edicion Unica I and Encore Noir. “Solidarios” under the Encore brand includes the Vitola of 56 x 6, pack of 10, which is uniquely designed by hand and long filler.

- March 2024: C.L.E. Cigar Company is rolling out new packaging for its core line of cigars, inspired by classic Cuban designs seen at The House of Grauer lounge in Geneva. The cigars will now be presented in nostalgic wooden boxes in a "half wheel" format with redesigned bands and tissue paper, aiming to better reflect the quality and heritage of the blends.

Global Cigar Market Report Scope

A cigar is defined as a roll of tobacco wrapped in leaf tobacco or in a substance that contains tobacco. Cigars differ from cigarettes in that cigarettes are rolls of tobacco wrapped in paper or in a substance that does not contain tobacco.

The cigar market is segmented by product type, distribution channel, and geography. The market is segmented by product type into conventional and premium cigars. The market is segmented by distribution channel into offline and online retail stores. By geography, the cigar market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms (USD) for all the above-mentioned segments.

| Cigarillos |

| Cigar |

| Flavored |

| Non-Flavored |

| Mass |

| Premium |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Cigarillos | |

| Cigar | ||

| By Flavor | Flavored | |

| Non-Flavored | ||

| By Price Point | Mass | |

| Premium | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global cigar market in 2026?

The global cigar market size is USD 59.73 billion in 2026 and is on track to reach USD 77.39 billion by 2031.

Which region leads cigar consumption?

Asia-Pacific commands 54.21% of global revenue, driven by rising incomes, tourism, and luxury positioning.

What is the outlook for flavored cigars?

Flavored variants are forecast to expand at 6.53% CAGR through 2031, although impending U.S. bans may accelerate reformulation toward naturally flavored blends.

Why are premium cigars growing faster than mass-market cigars?

Affluent consumers treat premium cigars as status goods, enabling 6.44% CAGR growth and higher margins despite regulatory costs.

Is online cigar retail significant?

Although offline shops still dominate, e-commerce is projected to rise 7.38% CAGR as age-verification tech and broader SKU access attract digital buyers.

Page last updated on: