Mink Oil Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

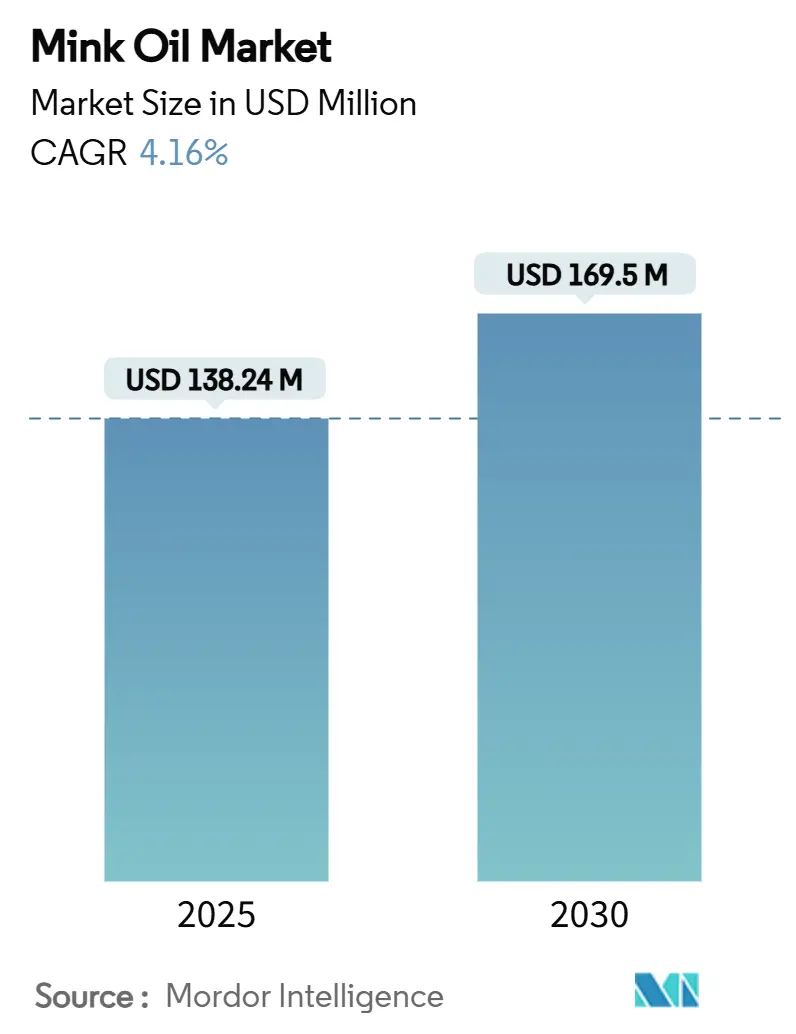

| Market Size (2025) | USD 138.24 Million |

| Market Size (2030) | USD 169.5 Million |

| Growth Rate (2025 - 2030) | 4.16% CAGR |

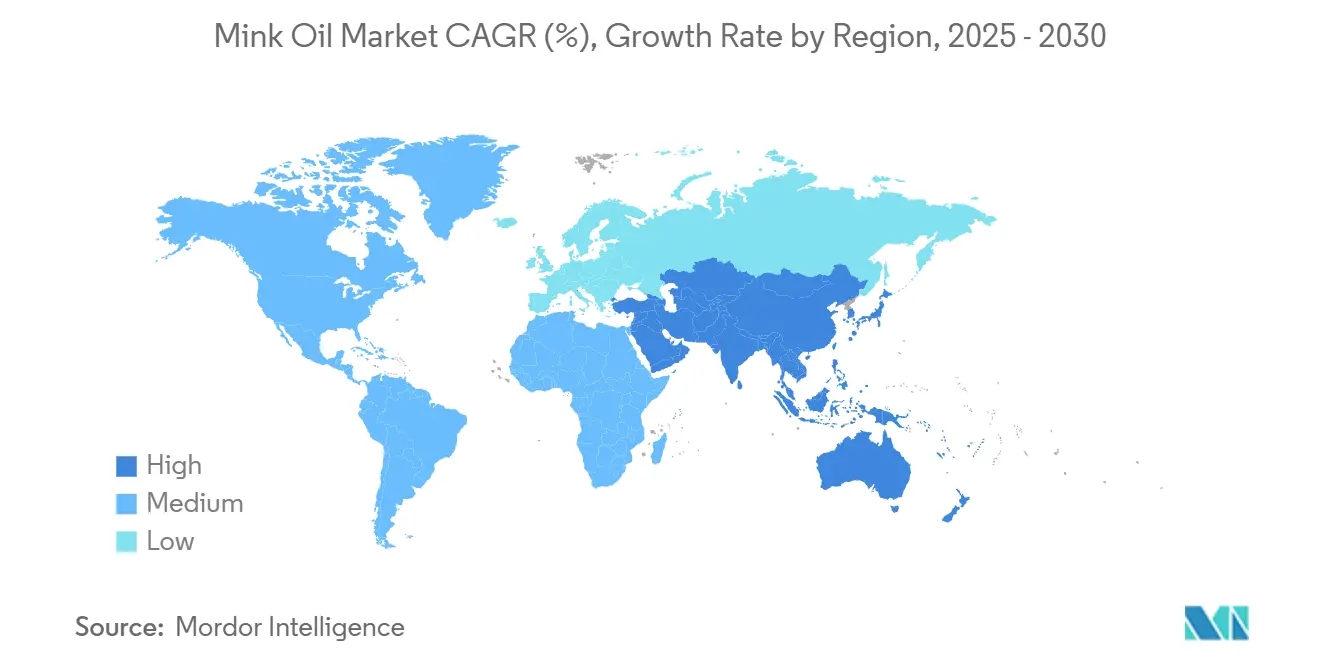

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mink Oil Market Analysis by Mordor Intelligence

The mink oil market size is estimated at USD 138.24 million in 2025 and is projected to reach USD 169.50 million by 2030, growing at a 4.16% CAGR over the forecast period. Despite supply shocks from COVID-19 culls in Denmark, which led to the elimination of 17 million animals and a 25% dip in global raw-skin output, the market's expansion remains unscathed. This resilience is attributed to price premiums, inventory buffers, and a diversification in end-uses that continue to draw in investments. While industrial buyers have traditionally driven demand, valuing the oil's oxidative stability, there's a noticeable shift towards consumer channels. These channels not only emphasize ethical sourcing narratives but also boast a robust e-commerce presence. In the realm of packaging, a competitive dynamic is unfolding: metal cans reign supreme in B2B transactions, yet PET bottles are carving out a larger share. Retailers are increasingly gravitating towards these lightweight, recyclable options, aligning with broader sustainability commitments. Geographically, North America stands at the forefront, bolstered by established leather-care and cosmetics brands. Meanwhile, Asia-Pacific is rapidly ascending, fueled by China's trajectory towards accounting for 50% of global luxury consumption and India's push for premiumization in personal-care categories.

Key Report Takeaways

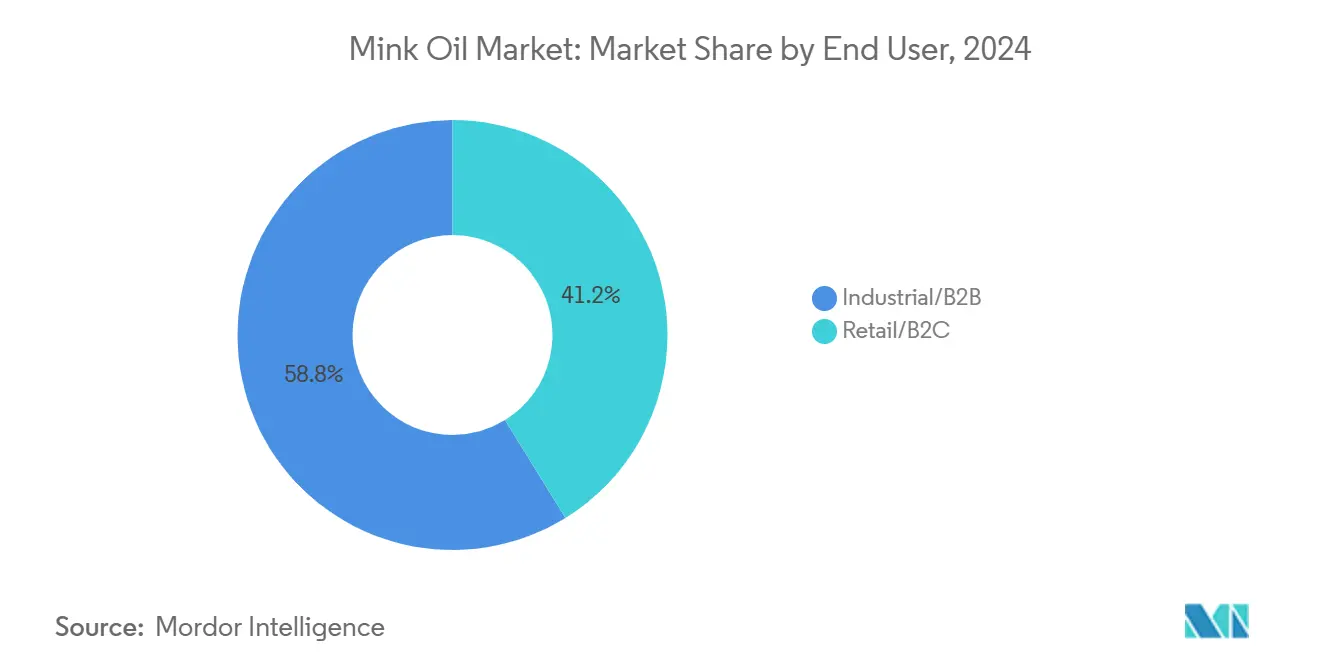

- By end user, the industrial segment controlled 58.83% of the mink oil market share in 2024, and retail channel is projected to grow at a 4.85% CAGR to 2030.

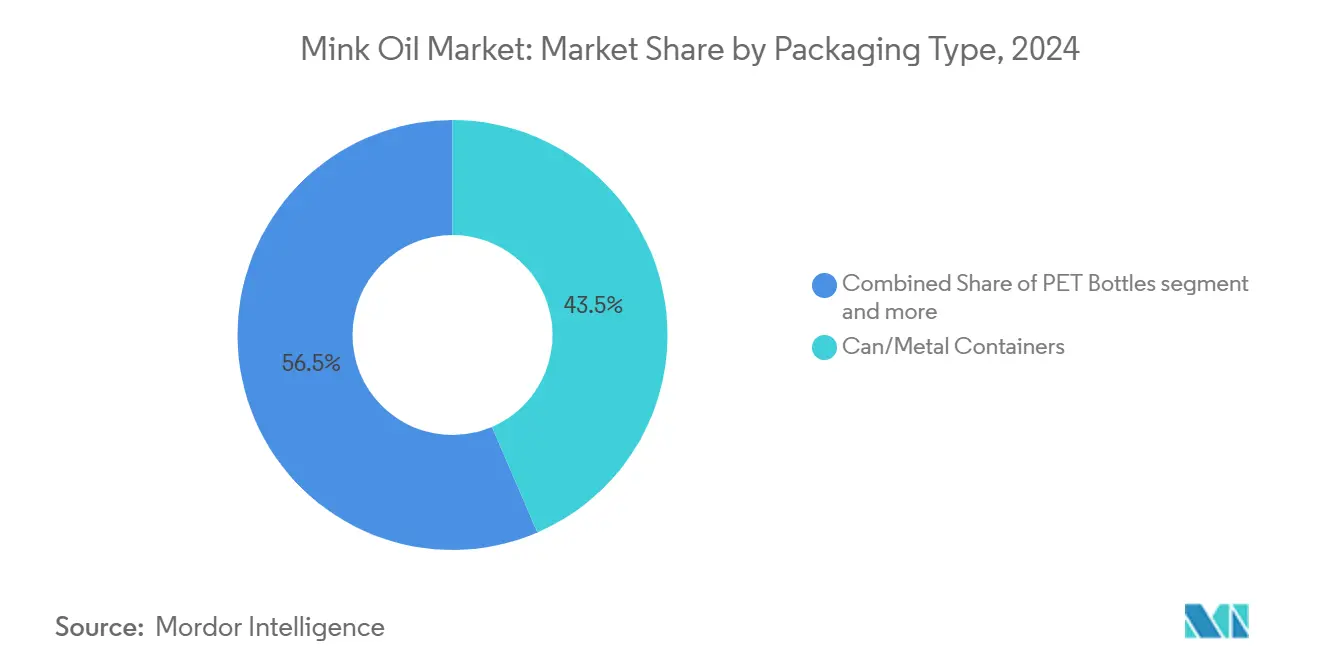

- By packaging, metal containers captured 43.54% of the mink oil market size in 2024, whereas PET bottles are set to advance at a 4.63% CAGR through 2030.

- By geography, North America commanded 35.84% revenue share in 2024; Asia-Pacific is expected to expand at a 5.14% CAGR between 2025-2030.

Global Mink Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in premium leather-care demand | +1.2% | Global, high in North America and Europe | Medium term (2-4 years) |

| Rising adoption of natural cosmetics | +0.8% | Core Asia-Pacific, spill-over to North America and Europe | Long term (≥ 4 years) |

| Surge in pet-care formulations | +0.6% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Low-cost feedstock from fur industry scaling | +0.4% | Europe and North America | Short term (≤ 2 years) |

| Niche demand for biodegradable lubricants | +0.3% | Developed markets | Long term (≥ 4 years) |

| Awareness of therapeutic properties | +0.2% | North America and Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in premium leather-care demand

Luxury leather owners have transitioned from basic preservation methods to performance-driven routines, now emphasizing water repellency, pliability, and color fastness. In 2024, the United States imported leather and leather products valued at USD 653 million.[1]Source: United States Census, "U.S. International Trade in Goods and Services, July 2025", bea.gov. These coveted properties are naturally provided by the fatty acid profile of mink oil, enhancing both the durability and aesthetic appeal of leather products. By 2025, China is expected to account for half of the global luxury market expenditure, increasing the demand for professional-grade conditioners to meet the needs of discerning consumers. Industrial tanneries are increasingly adopting mink oil for their premium footwear and handbag lines, ensuring top-notch quality and longevity. E-commerce platforms, preferred by 80% of Chinese luxury buyers, are allowing craft brands to engage directly with consumers, presenting customized solutions and niche offerings. Restoration studios, prioritizing material integrity, often advocate for mink oil on heirloom pieces, aiding in the preservation of their value and condition. This robust demand, combined with a pronounced willingness to pay and a lack of alternative chemistries, has resulted in double-digit price premiums throughout the supply chain, cementing mink oil's market dominance.

Rising adoption of natural cosmetics

Ingredient transparency significantly influences purchasing decisions in beauty aisles. Formulators, supported by U.S. FDA monographs, emphasize mink oil's non-comedogenic and hypoallergenic properties to strengthen "clean" labels, which are increasingly sought after by consumers prioritizing safe and effective products. In India, the combination of rising disposable incomes and growing awareness through social media platforms is driving a noticeable shift from mass-produced synthetic products to premium natural alternatives. This trend is not only increasing segment revenues but also broadening distribution networks across the country. Mink oil, rich in linoleic acid, plays a crucial role in enhancing skin barrier repair and delivering anti-aging benefits. These attributes enable brands to position their products as effective alternatives to synthetic esters, ensuring high performance without compromising on quality. Additionally, dermatology specialists are reinforcing this narrative by recommending these topical formulations for patients with sensitive skin. Their endorsements provide medical validation, further strengthening the credibility of marketing claims and appealing to a more informed consumer base.

Surge in pet-care formulations

As the global pet-food market continues its annual expansion, a heightened demand for functional ingredients, particularly those promoting dermatological health, has emerged. By 2025, an estimated 94 million U.S. households, as reported by the American Pet Products Association (APPA) National Pet Owners Survey, will have at least one pet[2]Source: American Pet Product Association, "The American Pet Products Association (APPA) Releases 2025 State of the Industry Report", americanpetproducts.org. Veterinarians are increasingly turning to mink oil, celebrated for its anti-inflammatory omega-9 fatty acids, incorporating it into shampoos, oral supplements, and targeted treatments to combat common pet skin issues like dryness, irritation, and inflammation. Clear FDA pathways for additives not only streamline product launches but also offer regulatory certainty, cut down time-to-market, and guarantee compliance. Moreover, a trend towards premiumization empowers brands to set higher prices by introducing high-quality, specialized products tailored for discerning pet owners. As pet guardians increasingly regard their pets as family members, the humanization trend not only boosts repeat purchases but also resonates with their quest for natural wellness solutions. This evolution mirrors a broader societal shift, with pet owners gravitating towards products that echo their preferences for health-consciousness, sustainability, and ethical sourcing, further propelling innovation and growth in the pet-food market.

Low-cost feedstock from fur industry downscaling

Global pelt output is on the decline. In 2024, the U.S. produced 771,200 pelts, marking a staggering 80% drop from the 3.75 million pelts produced in 2015[3]Source: National Association of State Departments of Agriculture, "MINK SURVEY - MAY 2025", nasda.org. This significant reduction in production reflects the ongoing challenges faced by the industry, including regulatory pressures, declining demand, and the closure of farms. Pelts that would have otherwise gone to waste are now being repurposed as low-cost feedstock for oil extraction. This strategic utilization enables processors to uphold their profit margins, even as finished goods fetch premium prices due to their scarcity. Meanwhile, Denmark's mandated cull and the Netherlands' 2024 phase-out have resulted in a temporary influx of raw fat to EU refineries, albeit at discounted rates. However, this surplus is expected to diminish as farms continue to shut down permanently. In response to these challenges, forward-looking industry players are proactively securing supply contracts in Asia, where production remains more stable, or pivoting toward lipids sourced from biotechnology, which offers a sustainable and innovative alternative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ethical shift toward plant-based substitutes | -0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Tightening animal-welfare regulations | -0.7% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Disease-driven supply volatility | -0.5% | Concentrated in major farming regions | Short term (≤ 2 years) |

| Legislative bans on mink farming | -0.4% | Europe, creeping toward North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ethical shift toward plant-based substitutes

As consumers increasingly value the social implications of their purchases, they're gravitating towards formulations derived from castor, soybean, rapeseed, and palm. These plant-based ingredients are perceived as more sustainable and ethical, aligning with the growing demand for environmentally friendly products. Cosmetics brands, keen on appealing to younger audiences, are prominently showcasing vegan labels, securing both shelf space and heightened visibility on social media. The vegan label not only resonates with the ethical preferences of younger demographics but also serves as a key differentiator in a competitive market. Additionally, these brands leverage influencer marketing and digital campaigns to amplify their reach and engage with socially conscious consumers. In tune with public sentiment, dermal specialists and veterinary clinics are frequently endorsing botanical alternatives, even in cases where efficacy varies. This shift is carving out a significant portion of the market traditionally dominated by mink oil, as consumers increasingly prioritize ethical considerations over traditional formulations. Furthermore, the adoption of botanical analogs reflects a broader industry trend toward transparency and sustainability, which is expected to drive innovation and reshape product portfolios in the forecast period.

Tightening animal-welfare regulations

Fourteen EU nations have either prohibited or are in the process of phasing out mink farming. This move has led to heightened compliance costs and a collapse of the local supply, significantly impacting the industry. In North America, operators who continue the practice are now mandated to adopt stricter biosecurity measures and enrichment protocols, which include enhanced disease prevention systems and improved living conditions for the animals. These requirements have pushed their break-even thresholds higher, making operations less economically viable. Additionally, trade barriers complicate sourcing; jurisdictions with stringent welfare laws are limiting imports from regions with more lenient regulations, creating supply chain disruptions. The capital expenditure burden, which includes investments in infrastructure and certifications, is a deterrent for new entrants. This scenario potentially shifts bargaining power towards integrated processors capable of shouldering the costs of ethical certifications, as they are better positioned to meet evolving regulatory and consumer demands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging: Metal Containers Retain Performance Edge

In 2024, metal containers dominated the market, capturing 43.54% of the revenue share. Their lead can be attributed to their superior barrier properties against oxygen and light, crucial for preserving fatty acids. This is particularly vital for industrial leather-care products and lubricant blenders, which store bulk volumes for extended periods. Moreover, metal containers seamlessly integrate with high-speed filling lines and adhere to global standards for transporting hazardous goods, underscoring their practicality for large-scale applications. The robust recyclability of metal packaging further cements its significance, especially for high-specification uses. These advantages have consistently reinforced metal containers' status as the top choice for bulk and industrial markets. Even with rising competition, the durability and regulatory compliance of the metal segment ensure its stronghold.

Conversely, PET bottles are rapidly emerging as the packaging segment with the highest growth rate, boasting a 4.63% CAGR. This surge is driven by a confluence of factors favored by both consumers and retailers. Retailers are drawn to PET for its aesthetic appeal on shelves, cost savings on freight, and its recyclability. Meanwhile, consumers value the clarity of PET bottles, which allows them to verify product purity, a growing concern with increasing ingredient scrutiny. In response to PET's rising popularity, many manufacturers are innovating, introducing BPA-free linings and easy-pour spouts to safeguard their market share. Additionally, partnerships between logistics providers and PET suppliers are yielding stackable designs that resist temperature changes without risking chemical leaching. While regulatory mandates for minimum recycled content might challenge PET's cost edge, continuous innovation ensures its competitiveness. The burgeoning e-commerce landscape further propels the diversification of packaging formats, with marketers fine-tuning pack geometry to curtail dimensional-weight shipping fees.

By End User: Industrial Applications Sustain Volume Leadership

In 2024, industrial buyers led the mink oil market, capturing 58.83% of the total turnover. Key applications driving this segment include leather-care compounds, cosmetics base-stocks, specialty lubricants, and veterinary preparations. Manufacturers, bolstered by consistent quality standards, confidently scale production. Contractual volume agreements ensure processors have a reliable off-take, justifying their investments in refining equipment. Within industrial applications, leather finishing stands out as the primary volume consumer, ensuring steady demand. Meanwhile, emerging niches like biodegradable hydraulic fluids are gaining momentum. OEM endorsements bolster their credibility, and regulatory mandates, such as the U.S. Vessel General Permit, are making these eco-friendly fluids a necessity for marine operators, further amplifying demand.

On the other hand, the retail channel, while accounting for a smaller revenue share, is the fastest-growing segment, boasting a 4.85% CAGR. This growth is largely attributed to heightened consumer awareness and education. Online tutorials and premium pet-grooming routines have spotlighted the benefits of mink oil to a broader audience. Direct-to-consumer brands are carving a niche by emphasizing origin transparency, small-batch production, and carbon-balanced logistics, resonating with environmentally-conscious buyers. To bolster retail success, brands are heavily investing in consumer education. Many are adopting QR-code packaging that links to usage tutorials, aiming to dispel skepticism surrounding plant oils. In a bid to enhance product appeal, pet-food blenders are rolling out micro-encapsulated mink oil variants for controlled nutrient release. Concurrently, cosmetics formulators are prioritizing higher-purity mink oil fractions to obtain dermatological approvals, fueling the retail segment's growth.

Geography Analysis

In 2024, North America accounted for 35.84% of global sales, underscoring the tight-knit collaboration among raw-material processors, leather-goods manufacturers, and specialty chemical distributors. With heightened consumer awareness, brands in the region can command premium prices. Furthermore, clear regulations bolster ongoing applications in cosmetics and veterinary fields. However, as local fur farms consolidate, there's a growing reliance on feedstock from Northern Europe and Asia, intensifying supply pressures. Yet, currency stability and advanced logistics networks mitigate these challenges, ensuring the U.S. remains central to price discovery for bulk contracts.

Asia-Pacific, with a robust 5.14% CAGR, is set to redefine global volume distribution. China's luxury market boom invigorates both industrial purchasers and niche retailers. Concurrently, India's shift towards premium personal-care products is driving demand for high-quality skin-care emulsions. Japanese firms, capitalizing on their intense research and development efforts, are producing pharmaceutical-grade derivatives, expanding their therapeutic uses. Meanwhile, government import duties play a pivotal role; a relaxation in tariffs on refined animal oils could significantly boost regional adoption.

Europe grapples with farm closures and a societal shift towards cruelty-free products. Yet, niche demand endures in Italy and France's heritage leather-craft hubs, where artisans prioritize performance over ethics. Additionally, Scandinavian bio-lube producers continue to source oils for machinery operating in frigid temperatures. While rising disposable incomes in South America and the Middle East and Africa present opportunities, challenges like infrastructure and cold-chain constraints slow down market penetration. This geographic diversification not only shields the mink oil market from regional disruptions but also enhances its resilience.

Competitive Landscape

Market concentration remains moderate, with heritage leather-care houses, Asian refineries, and European specialty-chemicals firms vying for dominance. Integrated players, overseeing farming, rendering, and fractionation, not only enjoy cost leadership but also provide traceability certificates, a growing demand from luxury conglomerates. Recent maneuvers include forging forward contracts with a shrinking number of certified farms, acquiring niche lubricant formulators, and collaborating with biotech labs on research and development for cell-culture lipids.

Innovation efforts are honing in on refining technology to reduce peroxide values and employing enzymatic trans-esterification to customize viscosity for marine lubricants. The uptick in patent filings related to micro-encapsulation hints at a strategy to expand into pet supplements and cosmetic serums. Collaborations between Japanese pharmaceutical firms and North American ranchers are focused on ensuring a medical-grade supply via closed-loop husbandry. As firms release life-cycle assessments of mink oil versus plant and mineral counterparts, they bolster their sustainability claims by enlisting third-party auditors to verify carbon footprints.

Botanical alternatives intensify the competitive landscape; castor-oil refiners are championing high-ricinoleic variants as substitutes for leather conditioners. In response, mink-oil producers highlight their product's superior penetration depth and water repellency, backed by ASTM test results. Marketing strategies are shifting towards digital micro-influencers, those who restore vintage boots or groom show dogs, crafting genuine endorsements that resonate more than traditional ads. Meanwhile, global logistics intermediaries are consolidating distribution channels, negotiating exclusive import rights, and navigating the complexities of customs, especially with the changing landscape of animal-product regulations.

Mink Oil Industry Leaders

-

Angelus Brand

-

Touch of Mink

-

Fiebing’s

-

Mermac Mink Oi lProduct

-

Red Wing Shoe Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Better World Fragrance House company launched its new mink oil-based perfume product in the United States, named Summer Mink. Summer Mink is an amber woody scent that invites wearers to indulge in the luxury of mink during the heat of summer.

- January 2025: Katsu Leather Co. introduced a QR-code traceability platform that lets consumers view batch-level sourcing details for all mink-oil conditioners sold in Japan, aiming to pre-empt regulatory transparency mandates.

Global Mink Oil Market Report Scope

| Can/Metal Containers |

| PET Bottles |

| Others |

| Industrial/B2B | Leather Care |

| Cosmetics and Personal Care | |

| Pet Care | |

| Industrial Lubricants | |

| Others | |

| Retail/B2C |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Packaging | Can/Metal Containers | |

| PET Bottles | ||

| Others | ||

| End user | Industrial/B2B | Leather Care |

| Cosmetics and Personal Care | ||

| Pet Care | ||

| Industrial Lubricants | ||

| Others | ||

| Retail/B2C | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large is the mink oil market in 2025?

The sector is valued at USD 138.24 million in 2025, reflecting resilience despite supply disruptions.

What is the forecast CAGR for mink oil through 2030?

Sales are projected to expand at a 4.16% CAGR between 2025 and 2030.

Which region is growing the fastest?

Asia-Pacific leads with a 5.14% CAGR on the strength of luxury-goods and premium beauty demand.

Which packaging type gains most momentum?

PET bottles exhibit the highest growth at a 4.63% CAGR due to e-commerce suitability and recyclability.

Page last updated on: