Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

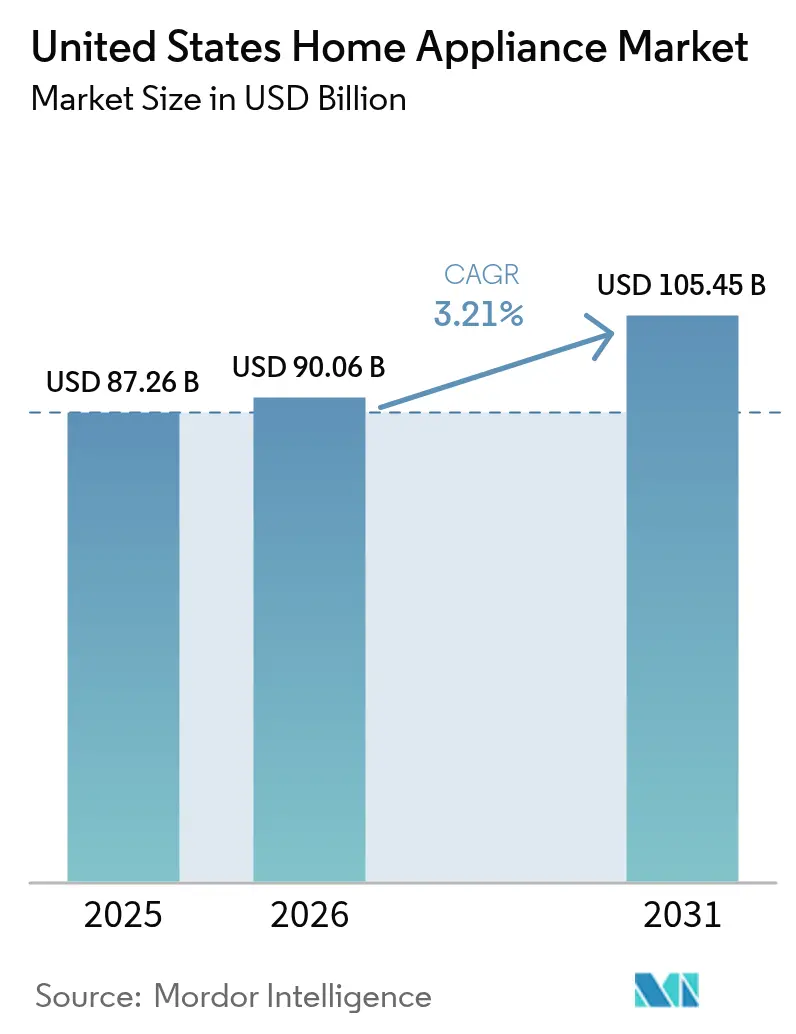

| Base Year Market Size (2025) | USD 87.26 Billion |

| Market Size (2026) | USD 90.06 Billion |

| Market Size (2031) | USD 105.45 Billion |

| Growth Rate (2026 - 2031) | 3.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Home Appliance Market Analysis by Mordor Intelligence

The United States home appliance market size is expected to grow from USD 87.26 billion in 2025 to USD 90.06 billion in 2026 and is forecast to reach USD 105.45 billion by 2031 at 3.21% CAGR over 2026-2031. Mature replacement demand remains the principal revenue engine, while advances in smart connectivity, energy-efficient designs, and domestic production capacity are reshaping product value propositions. Federal incentives, especially the Inflation Reduction Act’s heat-pump tax credits, accelerate adoption of high-efficiency models, and updated Department of Energy standards set a higher performance baseline for manufacturers to meet[1]U.S. Department of Energy, “DOE Finalizes Efficiency Standards for Water Heaters to Save Americans Over USD 7 Billion on Household Utility Bills Annually,” energy.gov. . Distribution dynamics continue to shift toward digital channels as consumers embrace virtual showrooms and frictionless delivery options, although multi-branded stores still dominate large-ticket purchases. Competitive intensity is mounting as leading brands expand U.S. manufacturing footprints to mitigate tariffs and logistics risks, and interoperability standards such as Matter 1.3 are lowering barriers for connected appliances.

Key Report Takeaways

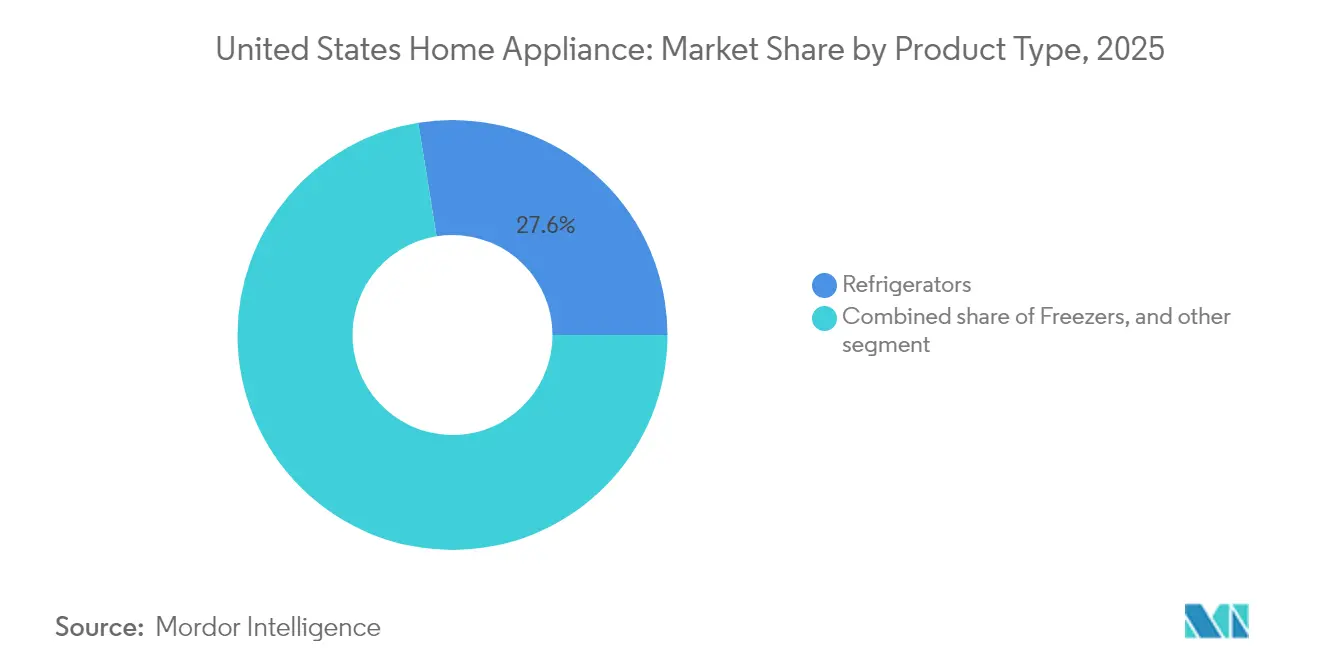

- Refrigerators led with 27.55% of the United States home appliance market share in 2025, while smart refrigerators are expanding at a 11.86% CAGR through 2031.

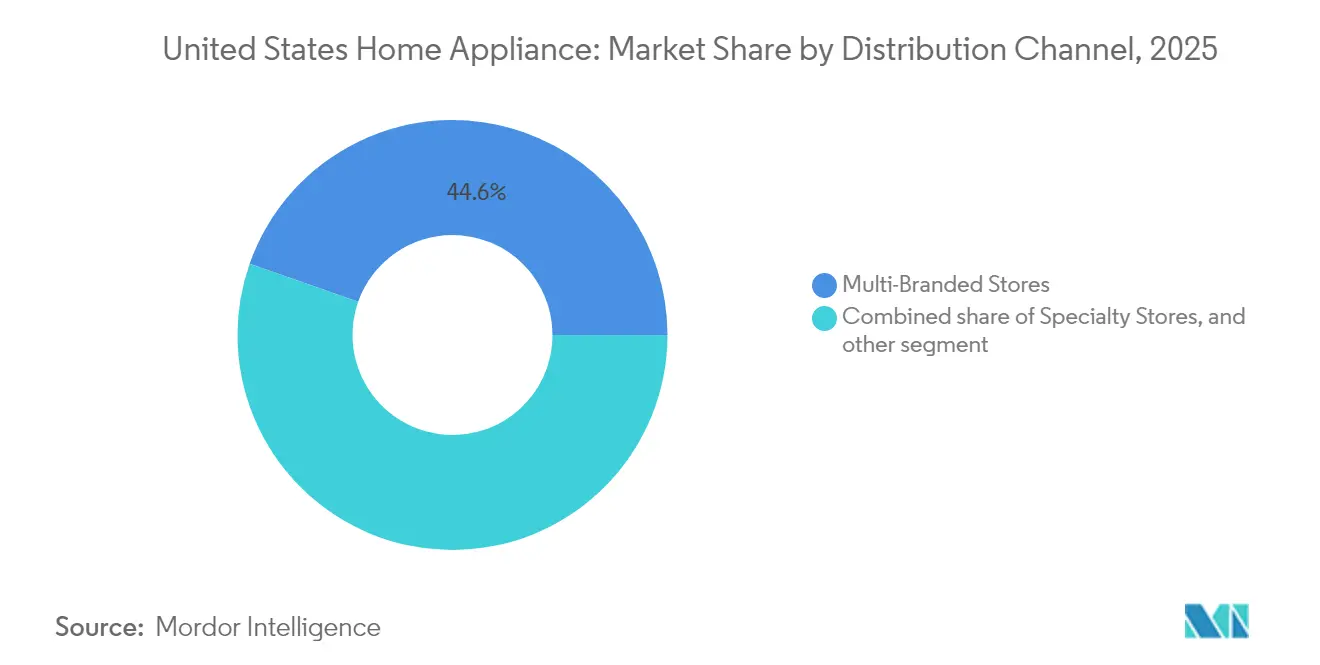

- Multi-branded stores held 44.62% of the United States home appliance market size in 2025, whereas e-commerce channels are advancing at a 13.05% CAGR to 2031.

- Conventional appliances accounted for 60.55% of the United States home appliance market size in 2025, yet smart and connected models show the highest momentum with a 15.95% CAGR.

- The South captured 36.35% of the United States home appliance market share in 2025; the West is outpacing all regions with a 5.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Home Appliance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ENERGY STAR & DOE-compliant appliance demand | +0.8% | National; strongest in California and Northeast | Medium term (2-4 years) |

| Smart/IoT-enabled white-goods adoption | +1.2% | National; early gains on West Coast and urban centers | Long term (≥ 4 years) |

| IRA heat-pump incentives | +0.6% | National; highest in cold-climate regions | Short term (≤ 2 years) |

| Social-media-driven premium small-appliance uptake | +0.4% | National; millennial-dense metro areas | Short term (≤ 2 years) |

| BNPL-financed replacements | +0.3% | National; stronger among younger cohorts | Medium term (2-4 years) |

| Electrification push for induction cooking | +0.2% | West Coast and Northeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand For Energy Star & Doe-Compliant Appliances

Federal efficiency mandates are generating a compliance-driven upgrade cycle that shortens traditional replacement timelines. The Department of Energy’s 2028 cooking-product standard will require electric cooktops to achieve at least 30% higher efficiency, delivering USD 1.6 billion in cumulative consumer savings[2]U.S. Environmental Protection Agency, “ENERGY STAR Most Efficient 2025 Criteria,” energystar.gov.. Manufacturers are fast-tracking ENERGY STAR Most Efficient 2025 models across heat pumps, washers, and refrigerators, while utilities leverage the standards to roll out targeted rebates. New water-heater regulations that mandate heat-pump technology for common electric units starting in 2029 are expected to double category efficiency and anchor long-term demand for high-performance models. Predictable compliance dates allow brands to optimize inventory transitions, and regional utilities align incentive budgets with federal timelines to maximize consumer uptake.

Accelerating adoption of smart/IoT-enabled white goods

Connected appliances are shifting from novelty status to ecosystem linchpins that enable whole-home energy management. Samsung’s 2025 Bespoke AI refrigerators integrate Voice ID, 9-inch displays, and Matter-ready connectivity, illustrating how premium design meets interoperability. GE Appliances’ partnership with ABB adds circuit-level monitoring through the SmartHQ app, giving builders and homeowners actionable insights on appliance loads. Yet 68% of IoT manufacturers cite development hurdles, underscoring competitive advantages for firms that solve integration pain points. With Matter 1.3 now covering kitchen and laundry specifications, consumer hesitation around vendor lock-in is steadily waning, positioning smart features as mainstream differentiators rather than niche add-ons.

IRA heat-pump incentives expanding dryer & HVAC categories

The Energy Efficient Home Improvement Credit grants up to USD 2,000 for heat-pump installs and USD 600 for high-efficiency AC units, while the High-Efficiency Electric Home Rebate Program offers as much as USD 14,000 in point-of-sale discounts for qualifying households[3]U.S. Department of the Treasury, “Heat Pumps Deliver Major Savings for American Families,” home.treasury.gov. . Panasonic’s CES 2025 OASYS system achieves 53% lower energy use than legacy HVAC, showcasing performance benefits that resonate with zero-energy-ready builders. Manufacturers now segment product lines by incentive thresholds, and staggered state rollouts are producing regional demand spikes that require agile production planning. As heat-pump dryers piggyback on HVAC awareness, cross-category bundling strategies are emerging for retailers targeting incentive-eligible consumers.

Social-media-led surge in premium small appliances

Digital content creation is driving appliance purchases beyond traditional replacement cycles, with social media platforms influencing product discovery and brand preference formation. Air fryer adoption reached 60% of American households by 2023, spurring a 90% increase in frozen food products featuring air fryer instructions and prompting brands like La Choy and Gorton's to launch dedicated product lines. This phenomenon extends to coffee equipment, where GE Appliances' Grind & Brew Coffee Maker and similar premium countertop appliances benefit from viral recipe content and influencer endorsements. The trend particularly impacts millennials and Gen Z consumers, who prioritize appliances that enhance their content creation capabilities and align with wellness-focused lifestyles. Manufacturers are responding by developing Instagram-worthy designs and partnering with food influencers to demonstrate product capabilities, creating marketing strategies that blur the lines between traditional advertising and user-generated content.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile steel & semiconductor costs | –0.7% | National; heaviest on domestic manufacturers | Short term (≤ 2 years) |

| Persistent logistics & parts shortages | –0.4% | Nationwide | Medium term (2-4 years) |

| Consumer cybersecurity concerns | –0.3% | National; privacy-sensitive segments | Medium term (2-4 years) |

| Higher future DOE compliance costs | –0.2% | National; smaller manufacturers most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile steel & semiconductor costs compress margins

Steel tariffs rose to 50% in June 2025, now covering appliance subcomponents, and pushed major-appliance shelf prices 4% higher in a single month[4]Alina Selyukh, “Appliances Face Steel Tariffs,” npr.org. . Major appliance prices increased over 4% in May 2025 alone, with companies like Samsung and LG facing significant cost pressures from imported materials. Hurricane Helene's disruption of North Carolina's Spruce Pine quartz mine, which supplies high-purity materials essential for semiconductor production, created additional supply chain vulnerabilities for smart appliance manufacturers. The semiconductor shortage particularly affects premium connected appliances, where advanced chips enable AI features and energy management capabilities that justify higher price points.

Persistent global logistics & parts shortages

Supply chain resilience remains compromised despite post-pandemic recovery efforts, with component availability creating production bottlenecks that limit manufacturers' ability to meet demand surges. The 2021-2024 Quadrennial Supply Chain Review identifies appliance-critical components among vulnerable supply chains, emphasizing the need for domestic manufacturing investment and supplier diversification. Power transformer shortages, with lead times extending to 2-4 years and 80% price increases since the pandemic, affect the electrical infrastructure supporting appliance manufacturing facilities. Manufacturers are responding through vertical integration strategies, with GE Appliances' USD 490 million Kentucky investment including in-house production of critical washer components to reduce external dependencies. The challenge is particularly acute for smaller manufacturers lacking the scale to secure priority supplier relationships or invest in backward integration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart features unlock premium refrigeration demand

Refrigerators held a commanding 27.55% share of the United States home appliance market in 2025, confirming their status as the category anchor for most retailers. Within that base, smart refrigerators are racing ahead at a 11.86% CAGR, fueled by AI-enhanced food tracking and voice-controlled user interfaces that allow consumers to minimize waste and manage energy use. The United States home appliance market size for refrigerators reached USD 24.04 billion in 2025, and incremental growth increasingly skews toward feature-rich variants. Washing machines followed with 24.95% share thanks to steady replacement cycles and shifts toward high-efficiency top loaders, while ovens captured 17.72% share as induction technology builds momentum in electrification-focused states.

Momentum is also evident in floor-care and countertop segments. Vacuum cleaners represented 9.48% of 2025 sales, but robotic units continue to outpace traditional formats as mapping accuracy and smart-home integration improve. Social-media-driven enthusiasm for air fryers, coffee systems, and multicookers widens the small-appliance addressable base and generates aftermarket opportunities for specialized accessories. GE Appliances’ Cookcam™ AI, which identifies food and recommends settings in real time, illustrates how embedded intelligence can differentiate even mature cooking appliances.

By Distribution Channel: Digital expansion erodes in-store dominance

Multi-branded stores accounted for 44.62% of the United States home appliance market share in 2025, reflecting entrenched consumer habits for tactile evaluation and bundled installation services. Yet e-commerce revenue is climbing at a 13.05% CAGR as virtual showroom tools close the experiential gap and last-mile carriers refine two-man delivery and haul-away services. Average online ticket size sits at USD 890 versus USD 940 in-store, indicating price transparency advantages for digital shoppers. Specialty showrooms secure 28.35% of value by curating premium assortments and leveraging white-glove services such as in-home consultations and warranty concierge support. Direct-to-consumer platforms post a 10.25% CAGR as manufacturers seek richer data and higher gross margins, while warehouse clubs like Costco leverage membership economics to punch above their 2% aggregate share with a 6% slot among club patrons.

Retailers continue heavy omnichannel investment. Home Depot’s appliance call-center integration and Lowe’s same-day pickup programs aim to blunt e-commerce leakage, while Best Buy pilots AR-enabled product visualization to revive lost share. As the United States home appliance market evolves, successful channels will synchronize personalized digital content with reliable in-home service execution.

By Technology: Interoperability accelerates connected-appliance rollout

Conventional platforms retained 60.55% of 2025 revenue, but the connected-appliance cohort is forecast to expand at a robust 15.95% CAGR through 2031 as Matter 1.3 resolves inter-brand compatibility friction. Smart units already command clear price premiums often 20%–30% above conventional peers and early adopters cite energy savings and automation convenience as top purchase drivers. Energy-efficient appliances captured 25.62% share and are growing 9.12% annually, bolstered by rebate stacking from utilities and state programs. The United States home appliance market size benefit from technology cross-pollination, where conventional insulation advances such as Whirlpool’s SlimTech™ reduce energy draw without necessitating connectivity.

Heat-pump water-heater mandates taking effect in 2029 will trigger a broad technology reset for the category, transforming once-niche units into default replacements. Brands balancing R&D between AI features, efficiency gains, and regulatory compliance should capture disproportionate share in the next product-refresh cycle.

Geography Analysis

The South dominated with 36.35% of United States home appliance market share in 2025 on the back of robust housing starts and population inflows. However, its projected 2.98% CAGR through 2031 trails the national average as price-sensitive customers temper smart-feature uptake, especially in rural areas where lower electricity tariffs reduce payback motivation. Texas and Florida anchor demand, with post-hurricane replacement surges creating opportunistic sales peaks that manufacturers address via flexible production scheduling. Builders in large suburban developments still favor conventional appliance bundles to manage cost, moderating short-term premium-segment penetration.

The West accounts for 28.15% of 2025 revenue but leads on growth at 5.48% CAGR, propelled by municipal gas bans and high electricity prices that make induction cooking and energy-monitoring features attractive. California’s Title 24 standards, combined with early EV adoption, elevate whole-home load management into a mainstream consumer requirement, strengthening value propositions for connected appliances and grid-interactive water heaters. Nevada’s 10% electrical-goods sales growth and marquee renewable-energy infrastructure projects signal broad regional upside, especially for heat-pump technologies tailored to desert climates.

The Northeast holds 18.55% of sales, characterized by an older housing stock that favors retrofit solutions. Stringent weatherization and electrification objectives underpin steady demand for heat-pump water heaters and induction ranges, while higher urban density supports e-commerce penetration despite last-mile delivery complexities. The Midwest rounds out the national picture with stable but slower expansion, buoyed by local manufacturing footprints that give Whirlpool and GE Appliances freight-cost advantages. Regional differentiation highlights how utilities, building codes, and climate profiles steer localized product mixes, requiring brands to maintain agile SKU assortments across sales territories.

Competitive Landscape

The market remains moderately concentrated, dominated by a handful of key players. Whirlpool holds a leading position, supported by its extensive product range and strong dealer network. GE Appliances follows closely, benefiting from Haier’s investment support and a major domestic expansion initiative announced in August 2025. LG and Samsung also maintain strong positions, successfully capitalizing on demand for premium smart features, even amid challenges like rising raw material costs. BSH strengthens niche leadership in dishwashers on the back of a 5.5% R&D spend ratio, underscoring the innovation premium in mature categories.

Strategic shifts toward domestic manufacturing are reshaping the competitive landscape. Manufacturers are increasingly investing in U.S. production to offset the impact of 50% steel tariffs and persistent bottlenecks in trans-Pacific shipping. LG’s $100 million expansion in Tennessee includes new refrigerator production lines and a 560,000-square-foot warehouse, improving logistics and service for Southeast U.S. dealers. Similarly, Miele’s Alabama facility reflects a broader reshoring trend, particularly in the premium cooking appliances segment. These moves not only improve supply chain resilience but also enhance brands’ responsiveness to regional demand.

The market now favors companies that combine localized production with advanced digital ecosystems. Home appliances are evolving from standalone products to connected service platforms, with interoperability and smart integration becoming key differentiators. Consumers increasingly expect appliances that seamlessly integrate into their smart homes and offer ongoing value through software updates and energy management features. This shift is creating opportunities for brands to build long-term customer relationships beyond the initial sale. As a result, the future of competition in the U.S. home appliance market will hinge on both technological innovation and supply chain agility.

United States Home Appliance Industry Leaders

Whirlpool Corporation

GE Appliances (Haier

LG Electronics USA

Samsung Electronics America

BSH Home Appliances (Bosch, Thermador)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: GE Appliances committed USD 3 billion to broaden U.S. manufacturing, encompassing 11 plants across five states and generating 1,000 jobs.

- June 2025: GE Appliances completed a USD 490 million washer facility in Louisville, Kentucky, reshoring production from China with advanced automation slated to go live in 2027.

- March 2025: Electrolux, under the Frigidaire brand, launched its inaugural air-purifier range to tap into indoor-air-quality demand.

- April 2024: Whirlpool closed its EMEA transaction with Arçelik, creating Beko Europe and unlocking USD 200–300 million in incremental free cash flow.

United States Home Appliance Market Report Scope

A complete background analysis of the United States Home Appliances Market, which includes a complete assessment of the market, key players, emerging market trends by segments, significant changes in the market dynamics, and the market overview is covered in the report. The United States home appliances market is segmented by Product (Major Appliances (Refrigerators, Freezers, Dishwashing Machines, Washing Machines, Ovens, Air Conditioners, and Other Major Appliances), Small Appliances (Coffee or Tea Makers, Food Processors, Grills and roasters, Vacuum Cleaners, Other Small Appliances)), and by Distribution Channel (Multibrand Stores, Exclusive Stores, Online, and Other Distribution Channels). The report offers market size and forecasts for the United States Home Appliances Market in value (USD Million) for all the above segments.

By Product Type

| Major Home Appliances | Refrigerators |

| Freezers | |

| Dishwashing Machines | |

| Washing Machines | |

| Ovens | |

| Air Conditioners | |

| Other Major Products (Electric Hobs, Ranges, etc.) | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Toasters | |

| Vacuum Cleaners | |

| Juicers & Blenders | |

| Other Small Appliances (Waffle Makers, Egg Cookers, Air Fryers, Kettles, etc.) |

By Distribution Channel

| Multi-Branded Stores |

| Specialty Stores |

| E-Commerce |

| Other Distribution Channels |

By Technology

| Smart / Connected Appliances |

| Energy-Efficient (? 5-Star, Inverter) Appliances |

| Conventional Appliances |

By Region (U.S.)

| Northeast |

| Midwest |

| South |

| West |

| By Product Type | Major Home Appliances | Refrigerators |

| Freezers | ||

| Dishwashing Machines | ||

| Washing Machines | ||

| Ovens | ||

| Air Conditioners | ||

| Other Major Products (Electric Hobs, Ranges, etc.) | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Toasters | ||

| Vacuum Cleaners | ||

| Juicers & Blenders | ||

| Other Small Appliances (Waffle Makers, Egg Cookers, Air Fryers, Kettles, etc.) | ||

| By Distribution Channel | Multi-Branded Stores | |

| Specialty Stores | ||

| E-Commerce | ||

| Other Distribution Channels | ||

| By Technology | Smart / Connected Appliances | |

| Energy-Efficient (? 5-Star, Inverter) Appliances | ||

| Conventional Appliances | ||

| By Region (U.S.) | Northeast | |

| Midwest | ||

| South | ||

| West | ||

Key Questions Answered in the Report

What is the current value of the United States home appliance market?

The United States home appliance market size stands at USD 90.06 billion in 2026.

Which product category holds the largest share?

Refrigerators lead with 27.55% share of 2025 revenue.

How fast are smart appliances growing?

Smart and connected models are expanding at a 15.95% CAGR through 2031.

Why is the West region growing quickest?

Electrification mandates, high electricity rates, and early smart-home adoption drive a 5.48% CAGR for the West.

What is the impact of steel tariffs on appliance pricing?

A 50% tariff implemented in 2025 pushed average major-appliance prices up 4% in a single month.

Which companies are expanding U.S. manufacturing?

GE Appliances, LG Electronics, Whirlpool, and Miele all announced significant U.S. capacity investments in 2025.

Page last updated on: