Europe Barbeque Grill Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

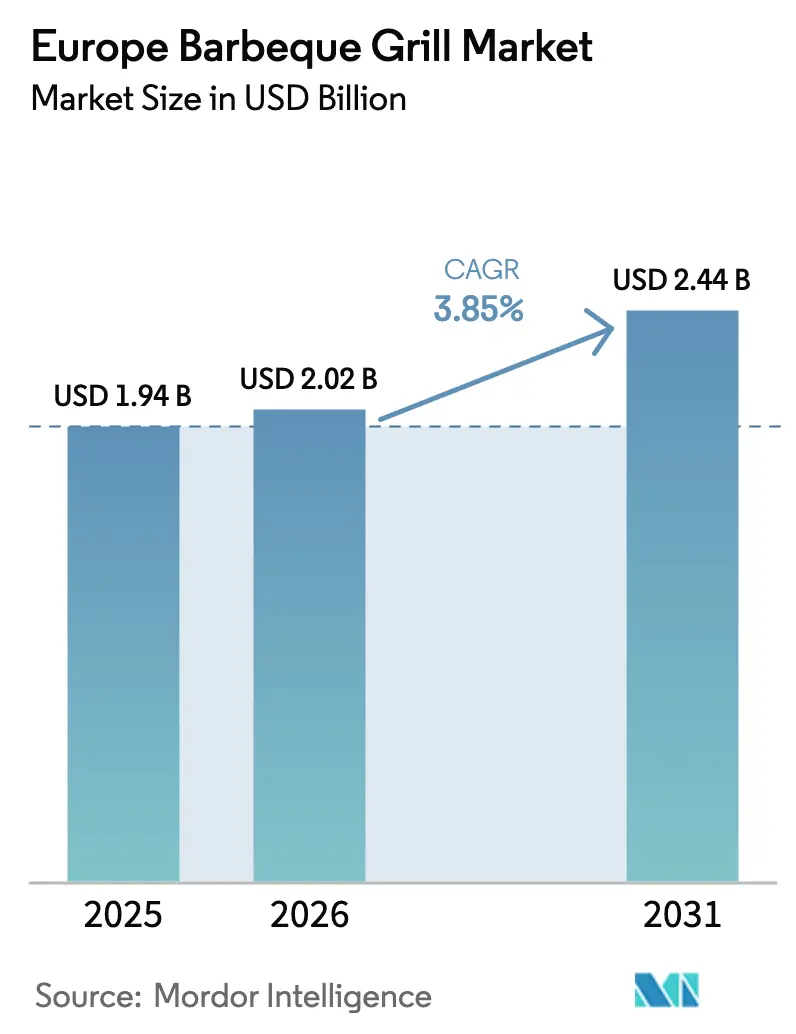

| Base Year Market Size (2025) | USD 1.94 Billion |

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 2.44 Billion |

| Growth Rate (2026 - 2031) | 3.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Barbeque Grill Market Analysis by Mordor Intelligence

The Europe barbeque grill market size reached USD 1.94 billion in 2025, is expected to reach USD 2.02 billion in 2026, and is forecast to achieve USD 2.44 billion by 2031 at a 3.85% CAGR. This trajectory reflects premiumization as brands integrate Wi-Fi thermometers, recipe apps, and modular side stations into gas, electric, pellet, and hybrid configurations to lift average selling prices. Buyers across Europe view outdoor cooking areas as lifestyle and property-value investments, which elevates demand for weather-sealed housings and TÜV-backed safety credentials. Regulatory focus on CE-GAR compliance and energy labeling further steers purchasing toward trusted brands that can meet these standards at scale. Germany, France, the UK, Spain, Italy, and the Nordics represent diverse use cases, from compact balcony-friendly formats in dense cities to all-season insulated systems in higher-latitude markets. European buyers also prize clarity in certification, and the Gas Appliance Regulation framework and CE pathways keep compliance central to product roadmaps[1]UL Solutions Editorial Team, “Gas Appliance Regulation and CE Marking for Gas-Fired Appliances,” UL Solutions, ul.com.

Key Report Takeaways

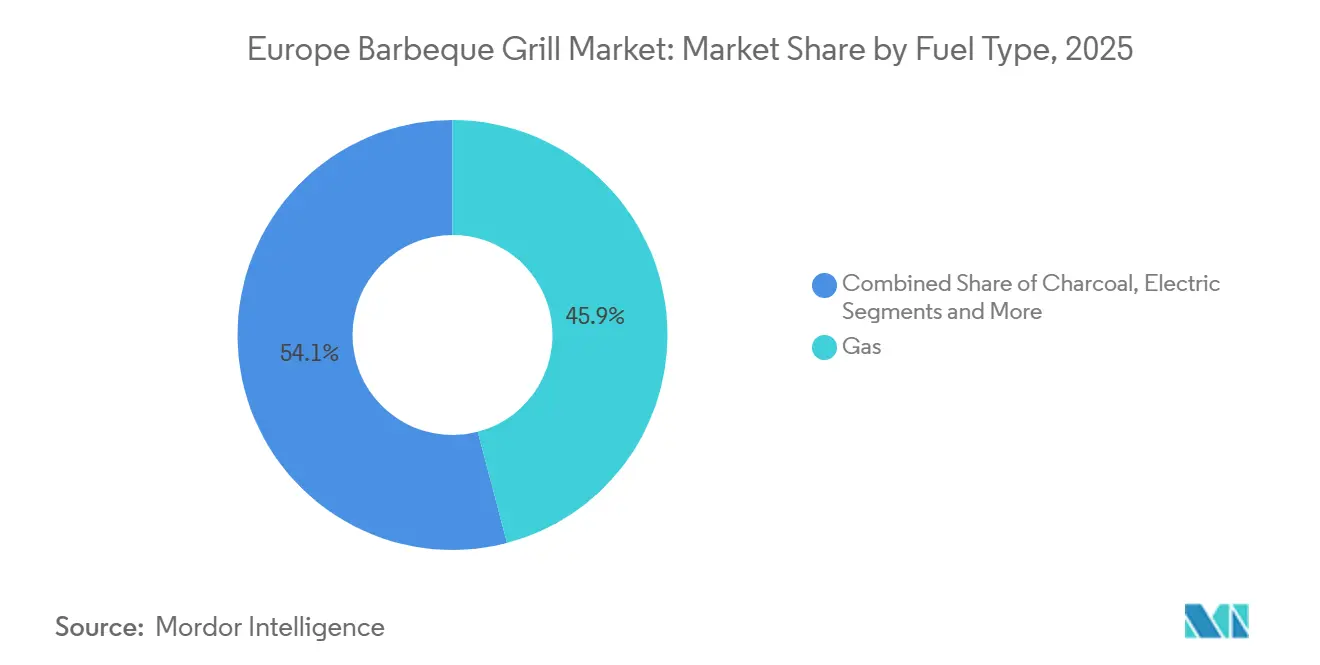

- By fuel type, gas grills led with 45.92% of Europe Barbeque Grill market share in 2025, while electric is projected to expand at a 4.68% CAGR through 2031.

- By product design, freestanding carts captured 57.34% of 2025 shipments, while portable units are forecast to grow at a 4.21% CAGR.

- By technology, conventional grills held 83.72% of the installed base in 2025, while smart-connected models are projected to advance at a 5.04% CAGR.

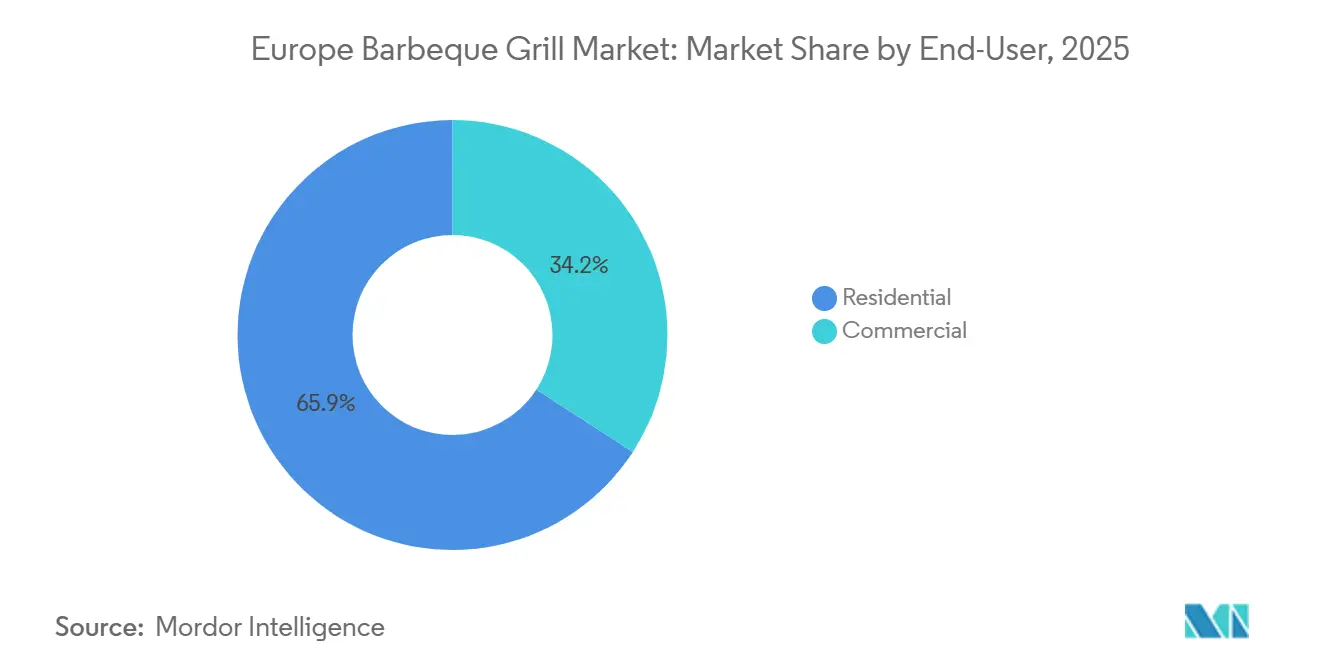

- By end-user, residential accounted for 65.85% of unit demand in 2025, while commercial is set to grow at a 4.03% CAGR.

- By distribution channel, B2C retail led with 68.12% share in 2025, while online-enabled channels are forecast to expand at a 2.97% CAGR through 2031.

- By geography, Germany held a 20.92% share in 2025, while Spain is projected to post the fastest growth at a 3.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global barbeque grill market data by Mordor Intelligence represents that combined structure.

Europe Barbeque Grill Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising outdoor living and staycation culture | +1.2% | Germany, UK, Nordics, Benelux | Medium term (2-4 years) |

| Shift to gas and electric for ignition and lower emissions | +0.9% | Urban centers in Germany, France, Italy | Short term (≤ 2 years) |

| Expansion of e-commerce and D2C with configurators and content | +0.6% | Germany, UK | Short term (≤ 2 years) |

| Smart-connected grills with IoT and app guidance | +0.8% | Germany, Scandinavia, UK, France, Benelux | Long term (≥ 4 years) |

| EU safety and CE-GAR compliance favoring trusted brands | +0.4% | Pan-European, strongest in Germany, France | Medium term (2-4 years) |

| All-season Nordic grilling enabled by insulated designs | +0.3% | Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Outdoor Living & “Staycation” Culture Driving Investment

Homeowners continue to allocate discretionary budgets to outdoor living, and grills function as centerpieces within modular islands, compact balconies, and terrace set-ups. Buyers focus on durable build quality, weather protection, and cohesive aesthetics that match outdoor cabinetry and surfaces. Integrated packages that combine grill heads with side burners, storage modules, and stone or porcelain worktops simplify planning and raise attachment rates for accessories. Brands that pre-bundle these elements shorten decision cycles and help retailers present complete, space-aware solutions in showrooms and online channels. This pattern remains visible across Germany and the United Kingdom, and it extends to Nordic markets where enthusiasm for all-season outdoor living solidifies year-round use cases. Modular solutions like Napoleon’s Oasis Compact series illustrate how multi-function setups are being streamlined for urban and suburban spaces[2]Napoleon Product Team, “Napoleon Grills Product Family,” Napoleon, napoleon.com .

Shift Toward Gas/Electric Grills for Immediate Ignition and Lower Emissions

Consumer preference continues to migrate from charcoal toward gas and electric platforms that deliver immediate ignition, precise heat control, and easier compliance with balcony codes that restrict open flames in dense urban areas. Electric grills are projected to expand at a 4.68% CAGR through 2031, supported by high urbanization and an emphasis on low emissions in shared residential spaces. Product innovation responds to historic performance gaps, with full-size electric systems delivering high-temperature searing comparable to propane alternatives. Smart-enabled electric models that pair with recipe libraries and guidance apps further reduce barriers for first-time buyers. Gas retains its leading share by serving suburban households that value BTU output, multi-zone burners, and accessory expandability. This two-track adoption pattern supports stable demand for gas while lifting electric growth in city cores.

Expansion of E-commerce & D2C Channels

Digital channels compress the research-to-purchase journey with how-to videos, live chat, and configuration tools that visualize options and price impacts in real time. Germany’s specialty retail ecosystem has built content-driven websites that replace in-store demonstrations and sustain conversion growth at scale. Configurators like Outdoorchef’s enable buyers to select burners, side tables, and finishes, then finalize delivery, which increases order values and improves online conversion rates. E-commerce penetration remains higher in markets such as Germany and the United Kingdom, where consumers are comfortable purchasing large appliances online once support and installation logistics are clear. Manufacturers leverage D2C launches to gather usage feedback and iterate features faster, as seen with connected accessories introduced through brand-owned sites. As e-commerce scales, virtual assistance and augmented visualization tools become part of the standard pre-purchase workflow.

Innovation in Smart-Connected Grills with IoT Functionality

Smart-connected grills are advancing at a projected 5.04% CAGR as IoT features transform outdoor cooking from manual oversight to app-guided precision with alerts, timers, and guided recipes. Germany and Scandinavia lead in early adoption, given near-universal smartphone penetration and a willingness to pay premiums for connectivity and cooking intelligence. Connected gas and pellet models now support remote monitoring, firmware updates, and multi-probe temperature tracking through companion apps. Product lines from leading brands integrate cloud-linked status indicators and algorithmic heat management that reduce fuel consumption while improving consistency. Electric and pellet systems also align with EU energy-efficiency goals and labeling expectations, which amplifies their positioning on sustainability and precise control. Privacy concerns are addressed by local data processing and EU-hosted telemetry, which help sustain consumer trust.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel and aluminum input price volatility and carbon tariffs | -0.7% | Global, acute in Germany, Italy | Medium term (2-4 years) |

| Short grilling season concentrates sales in Q2 | -0.5% | Germany, Nordics, Benelux | Short term (≤ 2 years) |

| Charcoal non-compliance with EN 1860-2 tightening enforcement | -0.3% | Pan-European, notably Southern Europe and Germany | Medium term (2-4 years) |

| CE/GAR certification costs extend the time-to-market | -0.2% | Pan-European, broad entry barrier | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Steel and Aluminium Input Price Volatility

Metals cost volatility remains a headwind as aluminum and steel are core in housing, burners, frames, and side tables. EU policy adds cost pressure through the Carbon Border Adjustment Mechanism, which imposes duties on imports with high embedded emissions, altering sourcing economics for aluminum and steel inputs. Regional steel pricing has stayed elevated, with European hot-rolled coil indications in leading markets during early 2026 highlighting the role of energy costs and compliance in price formation. Copper, an input for ignition systems and smart-control boards, has also experienced price peaks that lift electronics costs. Manufacturers have diversified production and supply relationships to reduce exposure to tariffs and logistics risk, including shifts into facilities within Europe and Southeast Asia. Larger brands hedge input costs and lock contracts for specific steel grades, while mid-tier players face tougher tradeoffs between retail pricing and margin preservation.

Charcoal Quality Non-Compliance Driving Stricter Enforcement

Testing by EU authorities identified widespread quality issues across charcoal and briquette products, with many samples failing fixed-carbon requirements and others exceeding ash or moisture thresholds. These findings triggered recommendations to strengthen standards and tighten third-party verification, with compliance enforcement expected to intensify across member states. The EU Deforestation Regulation adds mandatory traceability for wood-based inputs, with deadlines that are phased by company size and that require geolocation-backed due diligence declarations. Non-compliance will carry sanctions that range from product seizure to significant fines, which will reshape supplier bases and favor vertically integrated or audited sources. Retailers are responding by tightening inbound checks and rationalizing assortments toward certified offerings. These changes may also influence consumer transitions toward formats that avoid combustion particulates in dense urban environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Electric’s Urban Surge Challenges Gas Dominance

Gas accounted for 45.92% of revenue in 2025, driven by instant ignition, strong heat output, and the wide availability of propane and natural gas infrastructure across suburban markets. This entrenched base reflects long investment in burner technology, grease management, and ignition reliability that households trust for frequent gatherings. Multi-zone controls and infrared accessories extend the cooking range from low-and-slow to high-heat searing, increasing usage frequency among families and hosts. Electric models are gaining traction in cities that restrict open flames on balconies, and they are projected to grow at a 4.68% CAGR through 2031 as designs reach searing temperatures with better thermal distribution. Smart-guidance features and precise temperature management make electric attractive to new users who want predictable results without fuel storage. Pellet systems remain a premium niche that blends wood-smoke flavor with digital control and remote adjustments for long cooks.

Urban growth dynamics support electric penetration, while gas remains the preferred choice for larger patios and gardens where space and ventilation are not constrained. Charcoal continues to appeal to enthusiasts who prioritize traditional flavors, yet tighter quality enforcement and air-quality rules are shifting some urban buyers toward electric and pellet categories[3]European Commission Staff, “EN 1860-2 and Related Charcoal Standards,” European Commission, ec.europa.eu . Manufacturers offer hybrid and modular solutions that let owners experiment with different heating modes without committing to multiple standalone devices. Across the Europe barbeque grill industry, fuel-format choice increasingly reflects local building codes, neighborhood density, and sustainability preferences rather than simple legacy habits. The resulting mix maintains a broad base for gas while creating room for electric momentum within apartment and townhome settings.

By Product Design: Portable Units Capitalize on Micro-Living Trend

Freestanding carts captured 57.34% of shipments in 2025, reflecting their versatility, integrated storage, and easy movement from patio to garage during off-season months. Suburban buyers favor freestanding systems that anchor outdoor cooking zones and accommodate add-ons, covers, and fuel storage. The format also suits family-scale cooking with enough surface area and accessory compatibility to handle varied menus. Specialty stores stage freestanding displays with full load-outs, which helps buyers visualize permanent placement at home. Portable and tabletop grills are rising at a 4.21% CAGR on the back of micro-living and frequent day trips to parks and beaches. Folding legs, compact burners, and small propane cartridges support easy transport and fast set-up for small-group meals.

Design preferences increasingly track available space and mobility needs rather than simple price tiers. Portable solutions appeal to cyclists, campers, and city dwellers who want occasional outdoor cooking without a permanent footprint, while freestanding carts continue to dominate among homeowners with larger terraces. Built-in systems sit at the premium end and tie into complete outdoor kitchens with refrigeration, sinks, and storage, although certification, ventilation, and installation requirements add planning steps. European buyers also show interest in modular kits that can start with a single cooking surface and scale to multi-appliance configurations over time. These modular and portable pathways keep the Europe barbeque grill market accessible to renters and homeowners across a range of dwelling types.

By Technology: IoT Connectivity Commands Premiums

Conventional grills account for 83.72% of the installed base in 2025, supported by familiarity, ease of maintenance, and a perception of reliability without firmware or app dependencies. Households that prioritize durability and straightforward operation continue to choose mechanical igniters and manual temperature control. At the same time, smart-connected models are projected to advance at a 5.04% CAGR as app-guided recipes, probe-based cooking, and remote alerts improve outcomes for complex dishes. Platform ecosystems that bring together guided cooks, firmware updates, and energy-saving modes help justify higher upfront prices. As brands standardize low-power wireless components and refine UX, smart features are moving from high-end flagships into broader mid-tier lineups.

Germany, Scandinavia, and the United Kingdom lead smart adoption, reflecting strong smartphone penetration and consumer comfort with connected appliances. Buyers who previously hesitated over complexity gain confidence through companion apps that simplify setup and provide visual cooking steps. Connectivity also links hardware to accessory ecosystems, which drives recurring purchases of probes, griddles, and racks. Energy labeling and consumer attention to standby power further differentiate solutions that implement auto-shutoff and efficient heat management. These shifts suggest the Europe barbeque grill market will keep a large conventional base while steadily expanding the connected cohort as features mature.

By End-User: Hospitality Recovery Lifts Commercial Demand

Residential buyers represented 65.85% of unit demand in 2025, with households investing in balcony and backyard solutions as part of broader outdoor living upgrades. Specialty retailers curate assortments for different dwelling types, climates, and code environments, and this advisory role remains a differentiator. The Europe barbeque grill market benefits from steady residential replacement cycles tied to wear, feature upgrades, and household moves. Portable formats add new entry points for first-time buyers who want flexibility and low storage requirements. Higher up the curve, built-in systems reflect long-term renovation plans where grills are integrated with cabinetry and refrigeration.

Commercial demand is gaining momentum at a 4.03% CAGR as restaurants, hotels, and caterers expand outdoor dining and event capacity. Food service operators specify industrial-grade gas and electric appliances to meet hygiene, duty-cycle, and ventilation requirements under applicable standards. Resorts and event venues favor large-format units that support high throughput and menu variety. Rooftop cafés and multi-tenant properties lean toward electric systems that comply with building rules on fuel storage and smoke. As outdoor hospitality experiences mature, accessory sales and maintenance services create recurring revenue opportunities for suppliers.

By Distribution Channel: Specialty Stores Defend Margins Through Expert Curation

B2C retail held 68.12% share in 2025 and is growing at a 4.26% rate as buyers value hands-on evaluation of build quality, grates, and ignition systems before committing to larger purchases. Specialist formats provide demonstrations and Q&A that influence model selection and accessory bundles. Hypermarkets and multi-category outlets display wide assortments and often bundle covers, brushes, and fuel connections, which appeals to price-sensitive shoppers. Online channels remain essential for research and are projected to expand at a 2.97% CAGR as content depth, live chat, and configuration tools improve buyer confidence. Retailers in Germany and the United Kingdom have built strong omnichannel workflows with store pickup, scheduled installation, and post-sale support.

Manufacturers leverage D2C to launch new features, test pricing, and gather feedback, while still partnering with retailers for national coverage and seasonal promotions. Configurators that present burner counts, finish options, and side tables with real-time pricing show a clear conversion advantage versus static pages. As online volumes expand, brands invest in virtual assistance and AR visualization to close experience gaps with showrooms. B2B direct ordering supports hotels and caterers that require multi-unit purchases and service agreements, which are not practical to replicate on consumer retail shelves. This mixed model underpins distribution resilience across the Europe barbeque grill market.

Geography Analysis

Germany anchored the region with a 20.92% share in 2025, supported by high household incomes, strong safety-conscious purchasing, and an established outdoor cooking culture across both suburban and urban settings. Southern states with larger gardens sustain premium freestanding and built-in formats, while northern urban centers show the fastest uptake of compact electric units that meet balcony rules. Germany also exhibits the highest smart-connected penetration in Europe, reflecting a technology-forward consumer base that values app-guided results and energy efficiency. Urban codes that limit smoke and open flames drive interest in electric and pellet models, while specialty retailers maintain a decisive advisory role for model and accessory pairing. Germany’s regulatory orientation and TÜV influence keep certification as a top-three purchase factor. These attributes position Germany as both the largest demand center and an early adopter of connected, compliant designs within the Europe Barbeque Grill Market.

Spain is projected to post the region’s fastest growth at a 3.92% CAGR during 2026–2031 on the back of an extended grilling season, improving household purchasing power, and tourism-driven hospitality demand. Coastal and resort areas value large-format equipment for al fresco service, while urban centers balance preferences between compact gas and electric formats due to multi-unit building codes. The household segment accelerates as outdoor upgrades become a higher priority in home improvement budgets. Spain’s climate naturally spreads purchases across more months compared with Northern Europe, which eases Q2 concentration in retail operations. This more even seasonal profile helps manufacturers and retailers plan inventory with fewer spikes. As performance and durability features migrate into mid-tier price points, adoption broadens across new and replacement cycles.

France, the UK, Italy, the Nordics, and Benelux form a sizable mid-tier bloc, each with distinct product preferences and regulatory nuances. French buyers favor planchas and cast-iron searing surfaces alongside gas burners, reflecting culinary focus on seafood and vegetables. The UK leans toward compact gas and electric formats that suit terraced gardens and patios, with outdoor living increasingly integrated into home renovations. Italy shows strong enthusiasm for outdoor cooking aesthetics and materials, with brands balancing style, corrosion resistance, and energy labeling in product pitches. The Nordics demonstrate the fastest electric growth rates in Europe and high smart-home alignment that supports connected pellet and electric systems for year-round use. Benelux markets mirror Germany’s appetite for connectivity and safety certification. Pan-European CE-GAR pathways streamline time-to-market, while country-specific gas pressure requirements and local ordinances still shape model configurations. These combined dynamics sustain broad participation across the Europe Barbeque Grill Market.

The barbeque grill market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for Germany, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The Europe Barbeque Grill Market is moderately fragmented, with Weber-Stephen, Napoleon, Traeger, and Char-Broil holding a combined share of one-half, supported by long-standing brand equity, multi-country retail relationships, and investment in ignition, heat management, and connectivity platforms. Regional players such as Landmann, Enders Colsman, Campingaz, and Outdoorchef compete through local certifications, product tailoring to balcony and compact applications, and value pricing. Across the portfolio, leading vendors expand attachment ecosystems with modular accessories and connected probes, which increase lifetime value and encourage platform loyalty. Specialty retailers partner with incumbents for store exclusives and omni-present support, while online channels bring discovery and customization at scale.

Weber’s combination with Blackstone in 2025 brought griddle depth and supply chain diversification, alongside balance sheet moves recorded in regulatory filings. The integrated portfolio broadens coverage across fuel types, including griddles, pellets, smart gas, and charcoal accessories, with cross-brand innovation on controls and user interfaces. Traeger continues to invest in connected features and extended product families that expand the brand’s reach beyond core pellet offerings. Napoleon emphasizes performance and design across freestanding and built-in systems, adding connected controls and multi-probe cooking support. Together, these strategies reflect an industry focus on feature-rich models that justify higher ASPs while keeping entry options available for first-time buyers.

Across the Europe Barbeque Grill Market, product roadmaps concentrate on three priorities. First, energy efficiency and safety compliance to satisfy CE-GAR, labeling, and local codes. Second, connectivity that improves results, reduces fuel use, and enables accessories and services. Third, format innovation spanning smaller footprints for balconies and modular kits for full outdoor kitchens. Brands also continue to diversify manufacturing locations and supplier relationships to manage tariff, freight, and input-cost risks[4]Weber Investor Relations, “Regulatory Filings and Transaction Updates,” U.S. Securities and Exchange Commission, sec.gov . Retail partnerships remain a cornerstone for scale, while D2C is used surgically for launches and feedback loops. These moves sustain moderate competition intensity with clear differentiation on technology, certification, and service.

Europe Barbeque Grill Industry Leaders

Weber Inc.

Napoleon (Wolf Steel Ltd.)

Char‑Broil (W.C. Bradley Co.)

Campingaz (Newell Brands)

Broil King (Onward Manufacturing)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Current Backyard (W.C. Bradley Co.) released a Wi-Fi-enabled dual-zone smart electric grill capable of 700°F searing, integrating app-guided recipes and precise heating controls targeting urban consumers restricted by balcony fire codes; the product builds on the Model G's "Smart Home Honoree" recognition at CES 2024, which generated 800 million PR impressions and a 4,464% website traffic surge, signaling strong demand for premium electric solutions in space-constrained European markets.

- May 2025: Newell Brands (parent of Campingaz) announced an offering of USD 1 billion senior unsecured notes due 2028, with proceeds intended to redeem USD 1 billion of outstanding 4.200% senior notes due 2026 and cover related fees, strengthening the balance sheet to support Campingaz's European outdoor cooking operations amid elevated interest-rate environments.

- April 2025: WMF launched its Edition One Plancha and modular outdoor kitchen lineup, targeting European consumers seeking scalable systems that begin with basic griddles and expand through drawer cabinets, beverage centers, and gas-bottle storage; the product line marks WMF's entry into exterior cooking spaces, leveraging its premium cookware reputation to compete with Weber and Napoleon in the built-in segment.

- April 2025: Traeger launched the FLATROCK 2 ZONE griddle, expanding its portfolio beyond pellet grills to capture the growing flatrock cooking category; the dual-zone design permits simultaneous high-heat searing and low-heat warming, appealing to food trucks and mobile catering operations serving corporate events and festival circuits.

Europe Barbeque Grill Market Report Scope

A barbecue grill is a piece of equipment that uses heat applied from below to cook food. Barbecue grills can be powered by gas, charcoal, smoke, hybrid, or electricity, depending on the heat source. A complete background analysis of the European barbecue grill market, which includes an assessment of the industry associations, the overall economy, emerging market trends by segments, significant changes in the market dynamics, and a market overview, is covered in the report.

The Europe Barbecue Grill Market Was Segmented By Product (Gas, Charcoal, And Electric), By Application (Household, Commercial), By Distribution Channel (Online Stores, Offline Stores), And By Geography (Germany, The United Kingdom, Poland, France, Italy, And The Rest Of Europe). The Report Offers Market Size And Forecasts For The Europe Barbeque Grill Market In Value (USD) For All The Above Segments.

| Gas Grills |

| Charcoal Grills |

| Electric Grills |

| Pellet Grills |

| Hybrid/Alternative Fuel |

| Infrared |

| Built-In |

| Freestanding |

| Portable / Table-top |

| Disposable / Single-use |

| Conventional |

| Smart/Connected |

| Residential |

| Commercial |

| B2B/Direct from the Manufacturers | |

| B2C/Retail | Specialty Stores |

| Home Centers & DIY Stores | |

| Mass Merchandisers | |

| Online | |

| Other Distribution Channels |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Fuel Type | Gas Grills | |

| Charcoal Grills | ||

| Electric Grills | ||

| Pellet Grills | ||

| Hybrid/Alternative Fuel | ||

| Infrared | ||

| By Product Design | Built-In | |

| Freestanding | ||

| Portable / Table-top | ||

| Disposable / Single-use | ||

| By Technology | Conventional | |

| Smart/Connected | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2B/Direct from the Manufacturers | |

| B2C/Retail | Specialty Stores | |

| Home Centers & DIY Stores | ||

| Mass Merchandisers | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the Europe barbeque grill market size in 2026, and how fast is it growing?

The Europe barbeque grill market size is USD 2.02 billion in 2026 and is projected to reach USD 2.44 billion by 2031 at a 3.85% CAGR.

Which fuel type leads sales in Europe and which is growing fastest?

Gas leads with a 45.92% share in 2025, while electric is the fastest-growing at a projected 4.68% CAGR through 2031.

What design formats are most popular among European buyers?

Freestanding carts captured 57.34% of 2025 shipments, and portable units are rising at a 4.21% CAGR as micro-living and travel needs increase.

Which countries anchor demand and which are expanding quickest?

Germany held 20.92% of the regional share in 2025, and Spain is projected to be the fastest-growing at a 3.92% CAGR to 2031.

How is connectivity changing purchase decisions across Europe?

Smart-connected grills are advancing at a 5.04% CAGR as app guidance, probes, and remote monitoring improve results and confidence, especially in Germany and Scandinavia.

Which channels dominate sales, and what role does e-commerce play?

B2C retail led with 68.12% share in 2025, and online-enabled channels are projected to expand at a 2.97% CAGR as configurators and live support enhance digital confidence.

Page last updated on: