Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 35.82 Billion |

| Market Size (2026) | USD 40.02 Billion |

| Market Size (2031) | USD 69.71 Billion |

| Growth Rate (2026 - 2031) | 11.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bancassurance In ASEAN Market Analysis by Mordor Intelligence

The Bancassurance In ASEAN Market size is expected to grow from USD 35.82 billion in 2025 to USD 40.02 billion in 2026 and is forecast to reach USD 69.71 billion by 2031 at 11.08% CAGR over 2026-2031.

The trajectory reflects rising integration between banks and insurers on mobile channels and API-enabled underwriting, stronger regulatory emphasis on data portability, and a clearer product suitability regime in leading hubs that favors simpler protection products and health riders. Life coverage continues to dominate premium pools while health riders accelerate due to demographic aging and a greater willingness to pay for catastrophic care among affluent and mass affluent segments. Country regulators are also tightening sector governance and capital standards, most visibly in Indonesia, which has strengthened solvency and sharia governance to stabilize confidence and pave the way for consistent asset growth. Strategic partnerships remain the primary route to scale, with leading insurers deepening multi-year agreements to secure distribution, technology integration, and shared analytics capabilities that raise conversion and persistency. The bancassurance in the ASEAN market is set to benefit from embedded protection inside retail and SME financial products, from family takaful to credit risk transfer programs that de-risk new lending and extend protection to underserved segments.

Key Report Takeaways

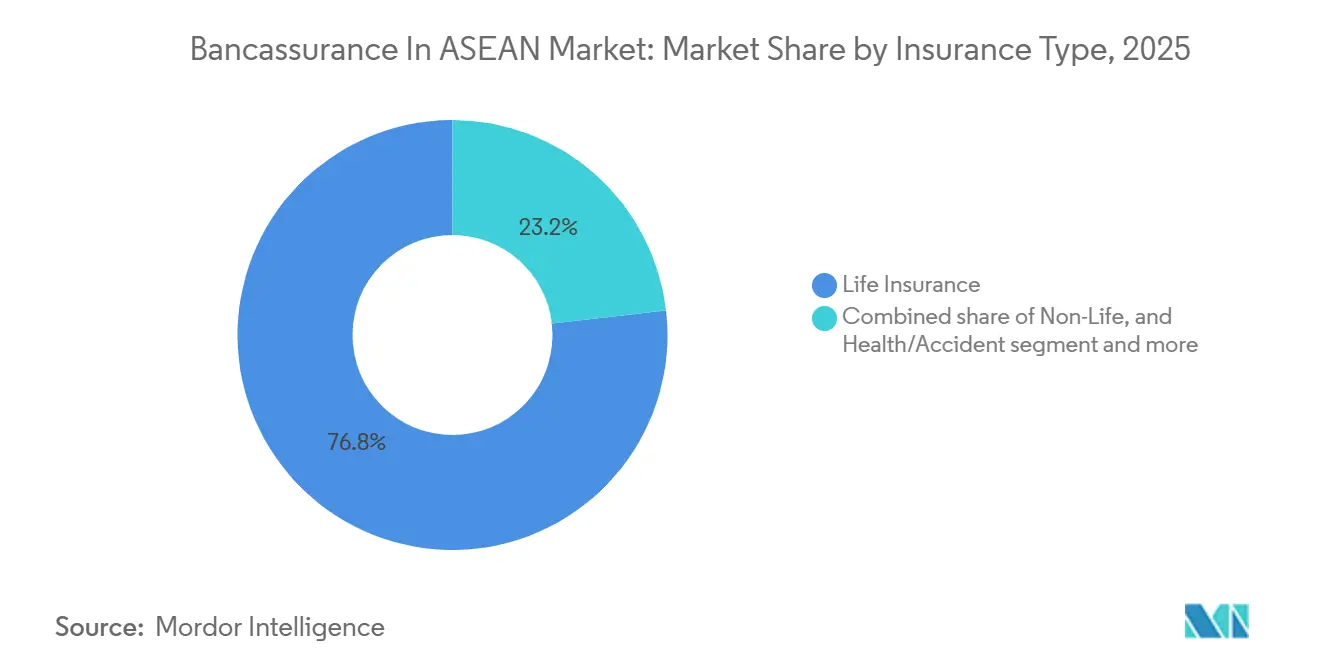

- By insurance type, life insurance led with 76.82% of the bancassurance in the ASEAN market share in 2025, while health insurance is projected to expand at a 12.56% CAGR through 2031.

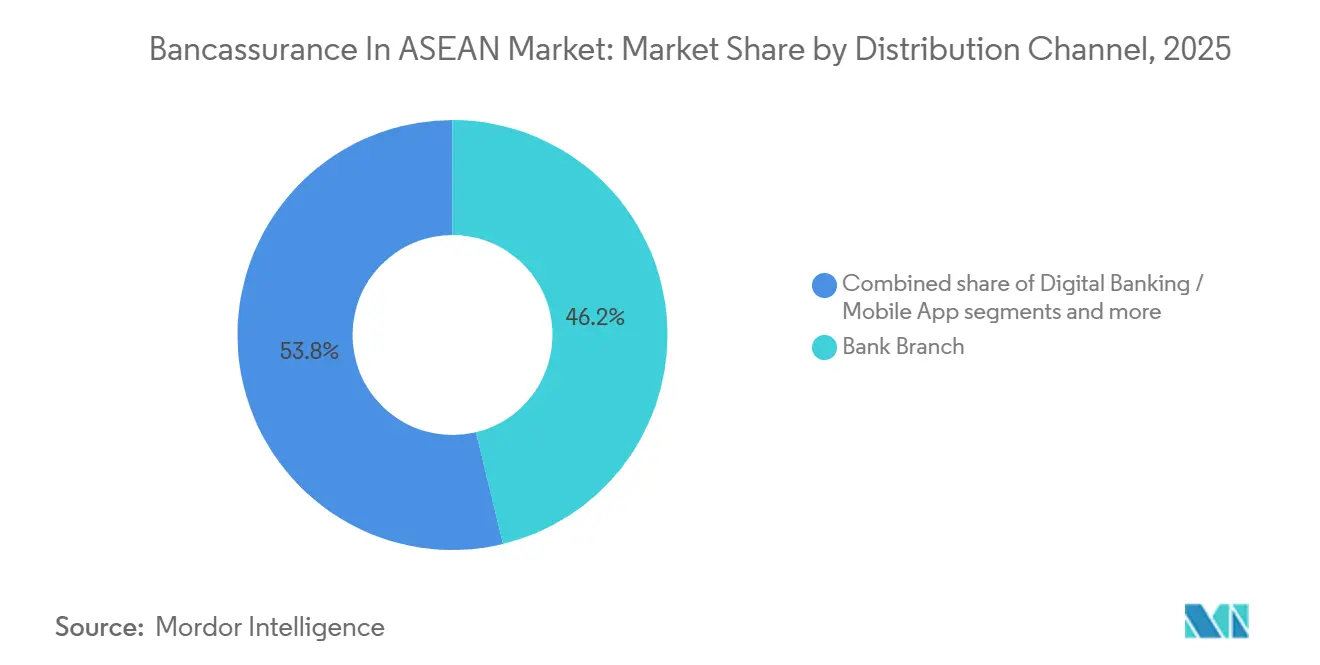

- By distribution channel, branch or in person accounted for 46.23% of the bancassurance in the ASEAN market share in 2025, while mobile banking apps are projected to grow at a 13.72% CAGR through 2031.

- By end user, retail customers held 65.51% of the bancassurance in the ASEAN market size in 2025, while SMEs are projected to advance at an 11.73% CAGR through 2031.

- By geography, Thailand held 34.45% of the bancassurance in the ASEAN market size in 2025, while Singapore is projected to register the fastest growth at 11.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bancassurance In ASEAN Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of life-insurance penetration in the emerging ASEAN | +2.8% | Philippines, Vietnam, Indonesia, spill-over to Thailand, Malaysia | Medium term (2-4 years) |

| Aging population & retirement-wealth demand | +2.5% | Singapore, Thailand lead, Malaysia, Vietnam follow | Long term (≥ 4 years) |

| Digital banking platforms enabling integrated sales | +2.3% | Global ASEAN, Singapore, Philippines, Malaysia mature fastest | Short term (≤ 2 years) |

| Islamic digital banks accelerating takaful uptake | +1.6% | Malaysia, Indonesia, Brunei, and emerging in Singapore, Philippines | Medium term (2-4 years) |

| SME-credit embedded insurance via supply-chain platforms | +1.4% | Indonesia, Malaysia, Thailand, and expanding to the Philippines, Vietnam | Short term (≤ 2 years) |

| Open-finance APIs powering real-time underwriting | +1.2% | Singapore, Malaysia lead, Thailand, Philippines are deploying | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Life-Insurance Penetration in Emerging ASEAN

Lower penetration in several ASEAN economies continues to underpin a multi-year runway for new protection sales, with consumer awareness and regulatory scrutiny building confidence for simpler life and health propositions distributed through banks. A commissioned study by a leading insurer estimated that a 50% increase in life insurance uptake by 2050 could lift GDP per capita and total GDP in the six core ASEAN markets, which reinforces the role of bancassurance as a channel that links household resilience with macro performance. [1]Prudential plc, “Prudential Report Reveals ASEAN Economic Boost Linked to Life and Health Insurance Growth,” Prudential plc, prudential.com. Indonesia’s market reforms have stabilized the operating base as most local insurers raised capital to meet updated standards and delivered year-end asset growth that strengthens balance sheets for long-term expansion and product innovation. Singapore’s life segment recorded higher weighted new business premiums in 2025, supported by strong demand for health-related coverage and structured protection, which signals how bank-led distribution can scale when data quality and eKYC are robust. Sharia-compliant offerings are broadening reach as new takaful products are introduced in markets with meaningful Muslim populations, expanding the funnel for bancassurance cross-sell to both retail savers and family-owned SMEs. These conditions keep the bancassurance in the ASEAN market aligned to a long demand cycle for core protection and health-linked products that complement bank savings and advisory journeys.

Aging Population & Retirement Wealth Demand

Aging demographics across Asia are reshaping household financial priorities and product mixes, resulting in greater demand for lifetime protection, annuities, and critical illness coverage that banks can embed into wealth conversations. Wealth managers in the region continue to pivot toward advisory-led models that integrate risk solutions within diversified portfolios, which elevates the strategic value of insurance partnerships for banks that serve affluent and emerging affluent customers. In Singapore, total life industry metrics for 2025 show broad-based growth and a notable rise in individual health premium volumes, signaling durable consumer appetite for private care access and comprehensive riders [2]Life Insurance Association Singapore, “Industry Performance for FY2025,” Life Insurance Association Singapore, lia.org.sg. Insurers are also reinforcing their high net worth propositions to meet complex cross-border needs, and banks can leverage these specialist platforms to deepen fee income while addressing longevity and estate planning gaps. As the cohort aged 65 and over expands, bancassurance in the ASEAN market propositions that translate savings into lifetime income streams and pair protection with investment advice are likely to see higher conversion and persistency. The net effect is a deeper linkage between retirement adequacy goals and bancassurance product suites, which support consistent premium growth across the forecast period.

Digital Banking Platforms Enabling Integrated Sales

Open finance and data sharing frameworks are accelerating straight through, API first bancassurance origination, which shortens underwriting timelines and enhances product suitability within mobile banking sessions. As institutions align standardized consent and data access, insurers can verify income and liabilities quickly, then tailor recommendations and installment schedules that match cash flow patterns and risk tolerance. Life insurers are also investing in platform capabilities that orchestrate partner APIs and enable real-time claims and underwriting, which banks treat as table stakes for in-app protection journeys and embedded sales. Singapore’s life sector performance points to the upside of higher data quality and seamless verification for digital origination, as insurers can pair advisory with instant execution in ways that enrich customer experience and reduce dropout. With product testing and suitability rising on the regulatory agenda region-wide, API driven validation and disclosure becomes a core advantage for bancassurance distributors that need to sustain compliance while growing volume at speed. These shifts put the bancassurance in the ASEAN market on a more scalable digital footing as banks transition from paper-based journeys to mobile-first sales that integrate protection within everyday banking tasks.

Islamic Digital Banks Accelerating Takaful Uptake

Takaful is scaling as regulators encourage digital infrastructure and as insurers launch new Sharia-compliant wealth and protection options that address religious preferences and expand financial inclusion. Malaysia’s supervisory focus on AI deployment and open finance has enabled insurers and takaful operators to automate contributions, sharia compliance checks, and surplus distribution with greater transparency, which supports faster product rollout with lower friction [3]Bank Negara Malaysia, “AI in Insurance and Takaful Operators,” Bank Negara Malaysia, bnm.gov.my. Product innovation is evident as insurers reenter or extend investment-linked takaful lines that pair long-term savings with protection, with early examples in Singapore highlighting cross-border appeal among regional customers. The Philippines has also seen Sharia-compliant protection launches targeted at Muslim communities that were previously underserved by conventional products, allowing banks to present broader coverage menus in Islamic finance corridors. In parallel, Indonesia has tightened sharia governance for insurers, which strengthens consumer trust and standardizes digital distribution, including inside mobile channels of Islamic banks. Together, these developments reinforce a high growth takaful lane inside the bancassurance in the ASEAN market, particularly in Malaysia and Indonesia, where the customer base is sizable, and bank penetration is deep.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tighter commission & fair-dealing rules | -1.1% | Singapore, Hong Kong spillover, Philippines reforms pending | Short term (≤ 2 years) |

| Declining branch footfall | -0.9% | Indonesia, Thailand lead decline, Malaysia, Philippines moderate | Medium term (2-4 years) |

| Certified advisor talent shortages | -0.7% | Singapore, Malaysia, Vietnam, Philippines are emerging | Medium term (2-4 years) |

| Super-apps cannibalizing bank channel | -0.6% | Indonesia, Vietnam, and regional expansion | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Certified Advisor Talent Shortages

Advisor capability requirements are rising as banks and insurers adopt data-driven suitability, digital disclosures, and API based sales flows that require hybrid skills in advice, compliance, and technology. High net worth solutions also demand cross-border structuring expertise, which insurers are building through dedicated platforms that coordinate estate planning, trusts, and multi-jurisdiction requirements with private banks. As new business growth concentrates in bank channels, distributors are expanding training programs to lift competency in machine-assisted underwriting, claims triage, and omnichannel service, which lengthens ramp-up time and raises operating costs during transition. Supervisors are encouraging broader use of AI and data standards for insurance and takaful operations, which necessitates new processes and governance that further elevate the skill threshold for frontline and back office roles. These capacity constraints can slow new product launches and limit the cadence of consultant-led sales, especially in markets where advisor recruitment lags demand for in-app advisory. AIA. As a result, talent scarcity can modestly temper short-term growth in the bancassurance in the ASEAN market even as digitization improves medium-term productivity.

Super Apps Cannibalizing Bank Channel

Platform ecosystems that aggregate payments, commerce, and mobility increasingly embed protection alongside lending and savings, which can divert first contact for simple insurance products away from traditional bank channels. In response, leading insurers are doubling down on partner API orchestration so bank apps can surface relevant coverage precisely when users transact, which narrows the convenience gap with lifestyle platforms. Embedded protection for SMEs and trade flows is also expanding through risk-sharing facilities that route capacity from insurers to lending programs, creating alternative funnels for commercial lines that sit outside retail bank distribution. Product innovation in takaful and investment-linked offerings is giving banks differentiation levers within their own ecosystems, although price transparency and instant settlement remain areas where super apps set the pace for customer expectations. Over time, banks that integrate claim adjudication and dynamic pricing into everyday banking journeys will defend share more effectively, but near-term share leakage can occur in light-touch micro protection. These dynamics keep competitive pressure elevated in the bancassurance in the ASEAN market and sustain a premium on technology partnerships that compress origination and service friction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Health Riders Reshaping Product Mix

Life insurance accounted for 76.82% of the bancassurance in the ASEAN market share in 2025, while health insurance is projected to expand at a 12.56% CAGR through 2031, cementing riders and medical benefits as the fastest-moving product lane. The bancassurance in the ASEAN market is therefore anchored by long-duration savings and protection, but incremental growth is increasingly linked to medical expense inflation, private healthcare access, and demographic aging that favor add-on coverage at policy issuance or renewal. Singapore’s life sector reported a rise in individual health premium volumes in 2025, indicating that customers are attaching more riders to core policies as they prioritize access and financial security in the event of serious illness. Indonesia’s regulatory consolidation and asset growth further underpin the outlook for sustainable product expansion and better governance across health insurance, life, and non-life insurance lines, which benefits bank-led distribution focused on everyday savers. Takaful launches in both Singapore and the Philippines, broadening the eligible customer pool for family protection and savings, which banks can present alongside conventional life in jurisdictions with diverse customer preferences. As a result, product portfolios are tilting toward simpler protection with optional riders that complement structured savings, positioning the bancassurance in the ASEAN market for steady mix improvement and better persistency.

Non-life products remain strategically important as banks cross-sell property, travel, and motor insurance that offer immediate utility and service touchpoints, which reinforce engagement and retention even when ticket sizes are smaller. Life and health continue to anchor premium pools, but commercial lines distributed through bank channels can scale as SME ecosystems adopt embedded risk covers for logistics and receivables that plug into business banking portals. Singapore’s strong activity in protection and riders suggests that affluent and mass affluent households accept bundled configurations that blend hospital access with savings goals, which banks can operationalize during account opening and renewal cycles. Indonesia’s governance upgrades create a sturdier foundation for future cross-sell of non-life products through rural and urban bank networks, helping to stabilize household risk exposures across a broader set of perils. As takaful providers expand product menus with investment-linked options, banks can differentiate on religious compliance, transparency, and digital onboarding, which will further diversify premium flows within the bancassurance in the ASEAN market.

By Distribution Channel: Mobile Apps Disrupting Branch Hegemony

Branch or in-person distribution held 46.23% in 2025, although mobile banking apps are projected to grow at a 13.72% CAGR through 2031 as open finance and instant underwriting streamline origination inside digital journeys. As mobile sessions concentrate daily banking activity, banks are matching this engagement with embedded protection prompts and pre-filled forms that reduce time to bind and minimize abandonment. Insurers that invest in partner-first platforms can support straight-through authentication, premium calculation, and claims initiation, which raises conversion in app contexts where attention spans are short. Singapore’s 2025 life data show how robust identity verification and reliable data improve digital cross-sell outcomes, particularly for riders who require dynamic matching of coverage to personal circumstances. Over the forecast period, this channel mix should continue to favor mobile-first interactions for simpler and mid-complexity products, while branches and relationship managers focus on affluent and high-net-worth cases requiring bespoke structuring.

Contact centers, relationship managers, and financial advisors remain critical for complex needs analysis, especially when products involve cross-border tax, trust structures, or multi-beneficiary configurations. Embedded coverage inside SME transaction and lending flows is another growth lever, supported by risk-sharing agreements that route insurer capacity to business borrowers at the point of credit approval. Islamic banks and takaful operators are also adding digital touchpoints for selection and contribution management, which improve transparency and allow families to review options in tandem with savings goals. As insurers scale their API orchestration and machine-assisted adjudication, banks gain a wider catalog of protection that they can present contextually inside their mobile user interfaces. These steps support the sustained rise of in-app origination while preserving high-touch advisory for customers with complex financial planning needs in the bancassurance in the ASEAN market.

By End User: SMEs Emerging as High-Growth Frontier

Retail customers accounted for 65.51% in 2025, while SMEs are projected to grow at an 11.73% CAGR through 2031 as supply chain platforms and bank portals embed coverage into working capital and trade finance journeys. The bancassurance in the ASEAN market is positioned to capture this shift because banks control account relationships, payment flows, and credit data that allow automated pricing and instant issuance for credit, goods in transit, and key person coverage. Risk transfer facilities that pair multilateral institutions with global insurers can channel capacity to underserved borrowers, which opens premium growth outside traditional retail life and health lines. IFC. In parallel, takaful expansion addresses the coverage needs of family-owned and sharia compliant enterprises that historically faced product gaps or distribution friction, creating a complementary growth stream. ETIQA. These dynamics lift the relevance of bank ecosystems for SMEs, where bundled insurance inside everyday finance tools reduces complexity and strengthens business continuity.

Corporate and affluent clients remain strategically important due to higher ticket sizes and multi-product relationships that blend wealth management with estate and succession planning. Leading insurers have reported stronger partnership distribution metrics, with banks providing the scale and data context needed to support in-app onboarding and advisory for both mass and affluent segments. As advisors deepen skills across tax, trust, and cross-border compliance, affluent propositions can grow faster, but talent scarcity will keep the focus on digital tools that compress case design and approval times. For SMEs, the increasing availability of embedded protection inside lending platforms should raise take-up and persistence as coverage links directly to invoice cycles and credit maturities. These patterns indicate that while retail remains the volume anchor, SMEs and affluent customers together will lift value capture for the bancassurance in the ASEAN market across the forecast horizon.

Geography Analysis

Thailand retained the largest country position with 34.45% share in 2025, while Singapore is projected to lead growth at 11.92% CAGR to 2031 as strong digital infrastructure and affluent demographics support consistent premium expansion. Singapore’s life sector posted higher weighted new business premiums in 2025, with individual health premiums also rising, which underscores the impact of robust identity verification, data standards, and distribution discipline. Insurers are building specialist HNW platforms in the city state to compete for regional wealth flows and to integrate cross-border tax and trust solutions into advisory, which banks can leverage to deepen wealth relationships. Product innovation is visible in sharia compliant wealth and protection, including investment-linked takaful options with digital onboarding that appeal to cross-border clientele. These conditions sustain a favorable growth profile in Singapore within the bancassurance in the ASEAN market and help explain the projected outperformance in the forecast window.

In Malaysia, regulatory support for open finance and AI adoption has improved straight-through processing for both conventional insurance and takaful, which advances speed, transparency, and suitability in bancassurance distribution. Operators have moved quickly to apply machine learning for contribution calculations and Sharia screening, which reduces friction for customers and allows banks to present options inside mobile banking journeys. Partnerships remain central to strategic execution, with insurers investing in healthcare integration and HNW expansion to control claims costs and enhance value for affluent customers. Singapore’s HNW initiatives and Malaysia’s takaful modernization together illustrate how the region balances affluent wealth solutions with inclusion through sharia compliant products. Taken together, these developments reinforce the bancassurance in the ASEAN market as a multi-speed landscape where regulatory clarity and platform readiness dictate country-level growth trajectories.

Indonesia’s insurance sector ended 2025 with higher total assets and broader compliance with new capital standards, which stabilizes the operating base and supports onward growth in bank-delivered life and health products. OJK. Enhanced sharia governance improves consumer trust and standardizes product practices, which in turn supports digital distribution and family takaful through Islamic bank channels. Regional partnership momentum is also notable in frontier markets such as Cambodia, where a long-duration exclusive tie-up is being rolled out across a nationwide banking footprint, signaling confidence in bancassurance as the route to early scale. Across ASEAN, multilateral initiatives are helping unlock new credit capacity for SMEs through risk transfer mechanisms that channel insurer capacity to lenders, which benefits banks aiming to embed coverage into business finance. These patterns point to sustained expansion potential in the bancassurance in the ASEAN market as governance strengthens, digital rails deepen, and partnerships extend across both mature and emerging country contexts.

Competitive Landscape

The competitive field is fragmented with moderate concentration and few players with decisive pricing power, so long-term partnerships function as the principal moat by combining distribution access with co-investment in technology and analytics. A leading insurer signed a 10-year exclusive agreement with a major Cambodian bank to cover the entire physical network within a defined rollout window, which exemplifies early mover strategies in frontier markets. AIA. Another global insurer has deepened multi-market alliances with international banks to secure cross-border distribution and embed protection into wealth journeys that span multiple ASEAN jurisdictions. In Singapore and Malaysia, insurers are sharpening HNW propositions and integrating health services to raise customer value and control claims, which banks can monetize through advisory and relationship pricing. Growth in Asia remains central to large multinationals, with reported increases in new business value and core earnings that align with the banking sector’s pivot to advisory-led protection and wealth solutions.

Technology readiness has become a key differentiator in bancassurance partnerships across the region, as banks prioritize insurers that can orchestrate partner APIs, support machine-assisted underwriting, and complete claims steps inside apps. AIA. Strategic consolidation is also evident as insurers raise stakes in high-growth markets to improve alignment between product manufacturing and distribution execution. Multilateral facilities that route risk capacity into SME lending portfolios create new channels for commercial lines and expand insurer relevance beyond retail protection. In aggregate, these moves underscore that the bancassurance in the ASEAN market rewards scale, technology integration, and cross-border coordination more than standalone product features. Performance in 2025 showed strong partnership distribution outcomes for select leaders, reinforcing the value of exclusive or near-exclusive bank access in the competition for digital shelf space.

Large global players continue to calibrate portfolios, existing or restructuring positions in markets where trust rebuilding or distribution economics require longer horizons, while concentrating capital in hubs with stable regulatory environments and deeper wealth pools. HNW and cross-border wealth flows remain a contested battleground as insurers roll out specialized advisory platforms to complement private banks in Singapore and Malaysia. Product innovation in takaful expands the addressable base and provides differentiation in Muslim majority and mixed markets, which favors banks that can offer both conventional and Sharia-compliant menus under unified digital experiences. The continuing maturation of open finance regimes supports standardized data sharing and efficient onboarding, raising the strategic bar for partnership competencies on both sides of the bank insurer relationship. Together, these elements point to a competitive pattern where winning share in the bancassurance in the ASEAN market hinges on the orchestration of channels, data, and capital rather than one-off product launches.

Bancassurance In ASEAN Industry Leaders

AIA Group

Prudential plc

AXA Mandiri Financial Services

Etiqa (Maybank)

Great Eastern Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Great Eastern launched Great Eastern Private to serve high-net-worth individuals across Asia with cross-border estate planning, trusts, and multi-jurisdiction solutions. The platform complements private banks and helps anchor wealth relationships with holistic protection and advisory. It positions the insurer to capture a greater share of regional wealth flows through bank partnerships.

- January 2026: Prudential completed the acquisition of an additional 19% interest in SHS, parent of Prudential Assurance Malaysia, raising its ownership to 70% and consolidating control in a priority ASEAN market. The move tightens alignment between manufacturing and distribution and supports deeper integration of digital underwriting and bancassurance processes. Management framed the transaction within a broader strategy to grow Asia's profit pools and reinforce long-duration bank partnerships.

- November 2025: AIA signed a 10-year exclusive bancassurance partnership with Cambodia’s KB PRASAC Bank to roll out across the full branch network by a defined mid-2026 target. The agreement embeds digital underwriting tools and co-branded interfaces to accelerate scale in a frontier market. It exemplifies infrastructure-level co-creation that goes beyond transactional product placement.

- January 2025: Etiqa introduced Invest Future in Singapore, the first takaful investment-linked product in the market in over a decade. The launch expands sharia compliant wealth and protection choices and signals growing cross-border demand among regional customers. The product supports bank partners that serve multinational customer bases and Islamic finance corridors.

Bancassurance In ASEAN Market Report Scope

Bancassurance is a strategic collaboration where banks utilize their branches, digital platforms, and customer networks to distribute insurance products. This model enables banks to generate fee-based revenue while providing insurers with extensive customer access, reducing their reliance on traditional sales channels.

The Bancassurance in ASEAN market is segmented by insurance type (life insurance, non-life (P&C), health/accident), distribution channel (branch/in-person, digital banking/mobile app, mobile banking apps, contact-center/phone, affinity & embedded (fintech/retail)), end-user (retail customers, small & medium enterprises (SMEs), corporate & affluent), and geography (Singapore, Malaysia, Indonesia, Thailand, Philippines, Vietnam, Rest of ASEAN). The market forecasts are provided in terms of value (USD).

By Insurance Type

| Life Insurance |

| Non-Life (P&C) |

| Health / Accident |

By Distribution Channel

| Branch / In-Person |

| Digital Banking / Mobile App |

| Mobile Banking Apps |

| Contact-Centre / Phone |

| Affinity & Embedded (FinTech / Retail) |

By End User

| Retail Customers |

| Small & Medium Enterprises (SMEs) |

| Corporate & Affluent |

By Geography

| Singapore |

| Malaysia |

| Indonesia |

| Thailand |

| Philippines |

| Vietnam |

| Rest of ASEAN |

| By Insurance Type | Life Insurance |

| Non-Life (P&C) | |

| Health / Accident | |

| By Distribution Channel | Branch / In-Person |

| Digital Banking / Mobile App | |

| Mobile Banking Apps | |

| Contact-Centre / Phone | |

| Affinity & Embedded (FinTech / Retail) | |

| By End User | Retail Customers |

| Small & Medium Enterprises (SMEs) | |

| Corporate & Affluent | |

| By Geography | Singapore |

| Malaysia | |

| Indonesia | |

| Thailand | |

| Philippines | |

| Vietnam | |

| Rest of ASEAN |

Key Questions Answered in the Report

What is the outlook for the bancassurance in the ASEAN market through 2031?

The bancassurance in the ASEAN market size is expected to grow from USD 35.82 billion in 2025 to USD 40.02 billion in 2026 and reach USD 69.71 billion by 2031 at 11.08% CAGR over 2026?2031.

Which products are set to expand the fastest within the bancassurance in the ASEAN market?

Health insurance and medical riders are projected to grow the fastest with a 12.56% CAGR through 2031, while life insurance remains the largest pool by premiums.

How is the distribution mix changing in the bancassurance in the ASEAN market?

Branch or in-person remains large, but mobile banking apps are projected to grow at a 13.72% CAGR, supported by open finance, API-first underwriting, and straight-through claims.

Which customer segments will drive the most growth in the bancassurance in the ASEAN market?

Retail remains the volume anchor at 65.51% in 2025, while SMEs are the fastest-growing at 11.73% CAGR due to embedded protection in credit and trade-finance journeys.

Which ASEAN geographies lead in share and growth, and why?

Thailand leads by share at 34.45% in 2025, while Singapore leads by growth with 11.92% projected CAGR as digital infrastructure and affluent demographics support consistent premium expansion.

What capabilities do banks prioritize when selecting insurance partners in the region?

Banks prioritize partner API orchestration, instant underwriting, and real-time claims within app experiences, alongside long-term exclusivity and aligned product roadmaps.

Page last updated on: