Autonomous Cranes Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.37 Billion |

| Market Size (2030) | USD 9.43 Billion |

| Growth Rate (2025 - 2030) | 11.93% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autonomous Cranes Market Analysis by Mordor Intelligence

The autonomous crane market size reached USD 5.37 billion in 2025 and is forecast to advance at an 11.93% CAGR, elevating value to USD 9.43 billion by 2030. Robust growth stems from AI-enabled navigation, IoT monitoring, 5G-edge orchestration, and retrofit autonomy kits that upgrade legacy fleets without full replacement. Infrastructure legislation, renewable-energy expansion, and tightening safety rules accelerate adoption, while service-based business models lower capital barriers and create recurring revenue. Competitive focus has shifted toward software sophistication, sensor fusion, and platform ecosystems rather than hardware alone, and operators increasingly view autonomy as the quickest path to mitigating labor shortages and improving project certainty. Cyber-security exposure and high up-front costs temper growth but are being addressed through stronger standards, financing innovations, and value-proven pilot programs[1]“Safe Features for Overhead Cranes,” Konecranes, konecranes.com.

Key Report Takeaways

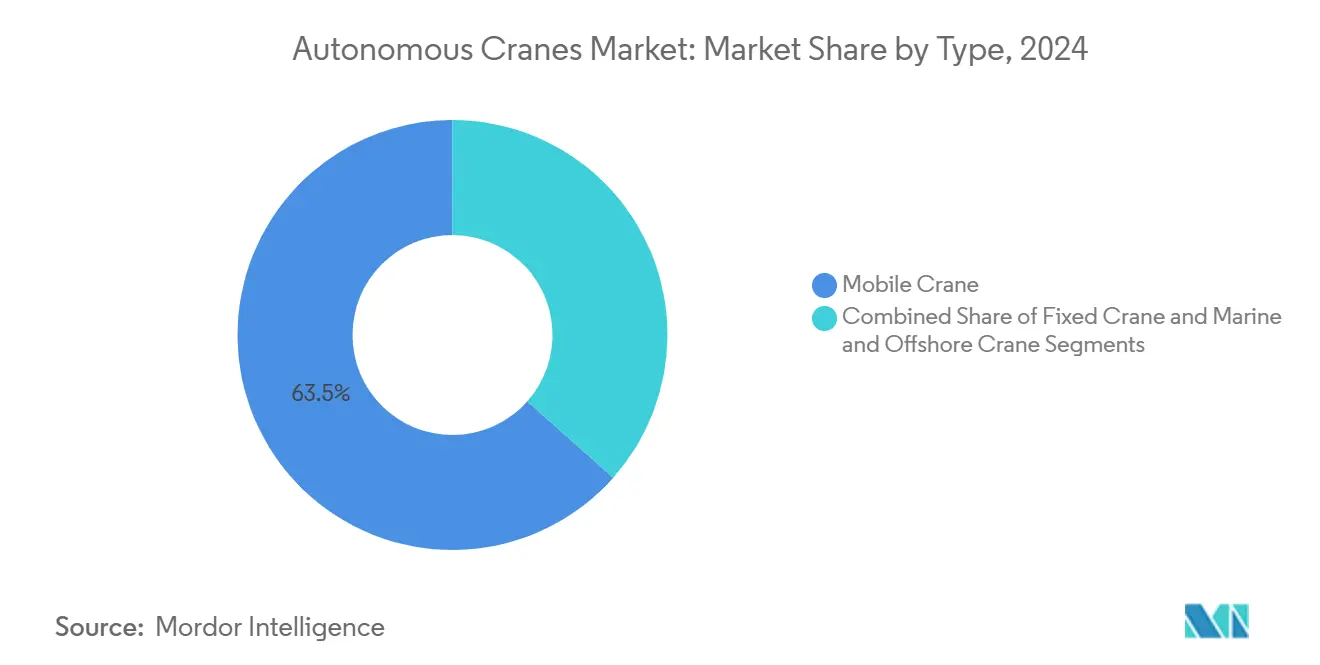

- By type, mobile cranes held 63.45% of autonomous crane market share in 2024, whereas marine and offshore cranes are projected to expand at a 15.01% CAGR through 2030.

- By capacity, the 51–150 ton class accounted for 38.89% of the autonomous crane market size in 2024, while above-300-ton models are projected to lead growth at a 12.56% CAGR to 2030.

- By power source, diesel units retained 65.51% share in 2024; fully electric variants are set to rise at an 18.59% CAGR over the forecast period.

- By technology, IoT-enabled monitoring commanded 47.08% share in 2024, and predictive-maintenance platforms will post the fastest 21.45% CAGR through 2030.

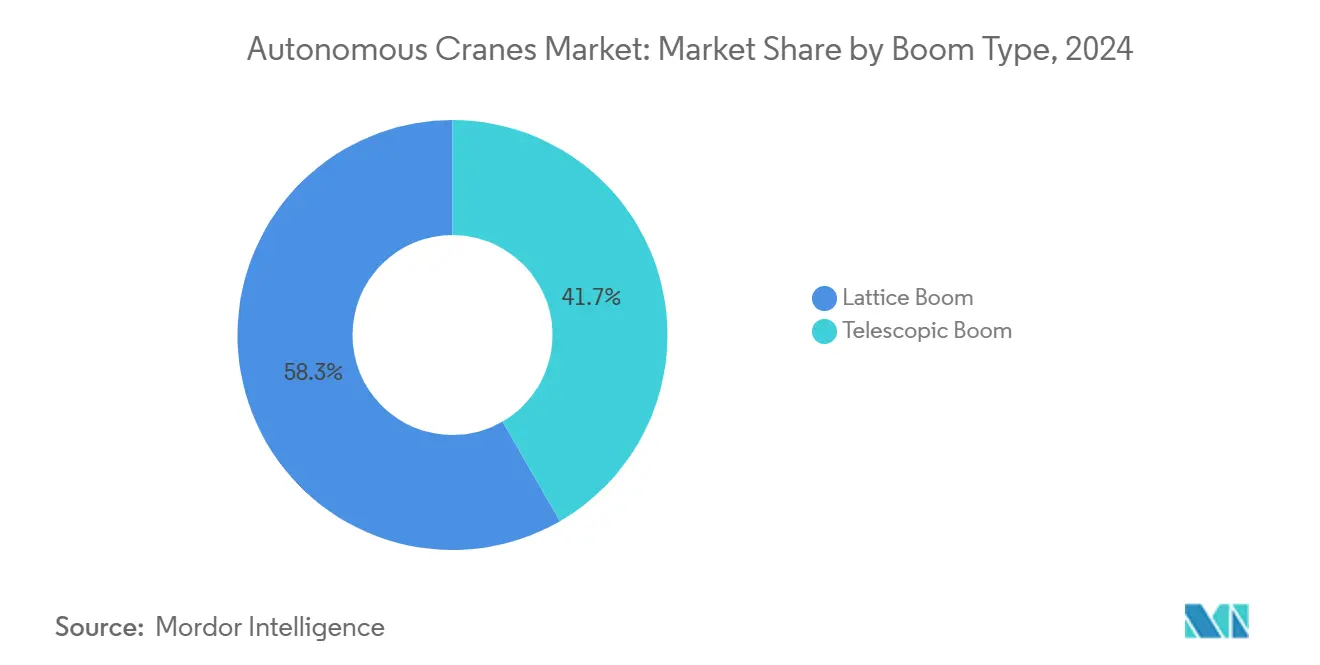

- By boom type, lattice configurations captured 58.34% share in 2024, whereas telescopic systems will progress at a 13.38% CAGR to 2030.

- By application, construction and mining generated 47.08% of 2024 revenue, yet logistics and warehousing is poised for a 17.16% CAGR through 2030.

- By geography, North America led with 33.77% revenue in 2024, while Asia-Pacific is on track for a 12.22% CAGR during 2025-2030

Global Autonomous Cranes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Spending Boom | +2.8% | Global, with early gains in North America, China, India | Medium term (2-4 years) |

| Labor Shortages and Safety Rules | +1.9% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Renewable-Energy Lift Requirements | +1.5% | Global, concentrated in Europe, APAC offshore wind zones | Long term (≥ 4 years) |

| Digitization and Fleet Optimization | +1.2% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| 5G-Edge Orchestration | +0.9% | APAC core, selective North America & EU ports | Medium term (2-4 years) |

| Retrofit Autonomy Kits | +0.7% | Global, with early adoption in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infrastructure Spending Boom and Urbanization

Global megaproject pipelines are now tied directly to autonomy-ready lifting solutions, because precision, uptime, and data traceability have moved from value-adds to bid requirements. U.S. federal infrastructure outlays are steering contractors toward fleet modernization that embeds autonomous safety layers from day one[2]“Infrastructure Investment and Jobs Act,” The White House, whitehouse.gov. Parallel urban-renewal programs in China and India incorporate autonomous cranes into smart-site specifications, guaranteeing steady demand visibility. Large civil packages, including metro expansions and high-speed rail, require mobile units able to reposition quickly yet operate with centimeter-level accuracy. Combined, these forces supply the strongest positive push on the autonomous crane market.

Labor Shortages and Stricter Safety Rules

Aging operator pools, high turnover, and escalating insurance premiums have pivoted contractors toward autonomous substitution strategies. In North America and Europe, advanced driver-assistance features such as area scanning, automatic load leveling, and geo-fenced work zones shorten training time and satisfy regulatory audits. Suppliers now bundle tele-operation stations that allow skilled operators to manage multiple cranes remotely, reducing labor bottlenecks. Alignment with stricter EU Machinery Regulations further accelerates the move from manual to AI-assisted lifting.

Renewable-Energy Lift Requirements

Offshore wind nacelles weighing 1,000 tons or more demand synchronized motion control and wave-compensating algorithms that manual systems cannot match. Tier-1 turbine OEMs increasingly specify autonomous cranes for tower segment staging and blade mounting in floating docks. Onshore solar-PV and battery-storage fields leverage autonomy for repetitive component placement in remote sites where labor logistics are challenging. Steady gigawatt-scale build-outs keep heavy-lift utilization rates high, protecting ROI trajectories for automated fleets through the next decade.

Digitization and IoT-Enabled Fleet Optimization

Fleet managers use real-time telemetry to balance crane assignments across multiple job sites, trimming idle time and shrinking total equipment footprints. Digital twins let project teams rehearse picks virtually, slash risk, and pre-set autonomous routines that execute on site without delay. Predictive parts-replacement cycles built from IoT data have cut unscheduled downtime below 2% on early adopter fleets, strengthening the business case for autonomy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CAPEX and ROI Uncertainty | -1.8% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| Cyber-Security Vulnerabilities | -1.2% | Global, heightened in critical infrastructure | Medium term (2-4 years) |

| AI-Specific Safety Standard Lack | -0.9% | Global, regulatory lag in developing markets | Long term (≥ 4 years) |

| GNSS Performance Gaps | -0.6% | Urban centers globally, dense metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and ROI Uncertainty

Autonomous conversions still require multi-year payback commitments at a time when interest rates hover near decade highs. Small and mid-size fleet owners face credit hurdles, prompting OEMs to launch usage-based leasing and revenue-sharing models that lower entry thresholds. Broader proof sets from completed projects are beginning to de-risk ROI calculations, but financial caution remains pronounced in cost-sensitive markets.

Cyber-Security Vulnerabilities

Remote command channels and cloud dashboards enlarge the attack surface for malign actors, especially in port and energy settings deemed critical infrastructure. Recent penetration tests uncovered weaknesses in protocol encryption and user-credential management. Vendors now ship cranes with zero-trust architectures, hardened gateways, and over-the-air patch pipelines; however, rising insurance premiums and compliance audits continue to dampen near-term adoption curves[3]“SIMOCRANE Crane Management System,” Siemens, siemens.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Mobile Dominance Drives Versatility Premium

Mobile units contributed 63.45% of 2024 revenue, underlining their primacy in mixed-use construction and infrastructure tasks that demand fast relocation. This preeminence anchors overall autonomous crane market growth, with many contractors considering mobile models the preferred entry point into autonomy due to straightforward retrofits and clear productivity paybacks. Versatility spans pick-and-carry operations, confined urban sites, and bridge-deck lifts, making mobiles the workhorse across core end-markets.

Marine and offshore cranes represent the high-growth frontier, advancing at a 15.01% CAGR as offshore wind and autonomous vessel support scale. Adoption leans on dynamic-positioning control systems, wave-motion compensation, and tele-operation from on-shore centers, all enabled by edge computing and low-latency links. Fixed cranes keep relevance in factories and shipyards where cycles are repetitive and environmental variables limited, allowing quick ROI on full autonomy stack installations.

By Capacity: Mid-Range Segments Balance Performance and Economics

Mid-capacity machines in the 51–150 ton class captured 38.89% of 2024 turnover, reflecting their alignment with mainstream bridge, metro, and industrial builds. Their moderate size allows on-highway mobility while providing lift ratings sufficient for prefabricated modules and steel assemblies. Contractors value the flexible deployment profile, ensuring high utilization ratios that justify autonomy upgrades.

Above-300-ton behemoths, although lower in volume, are projected to post a 12.56% CAGR on demand from wind-energy erection and petrochemical turnarounds. These units integrate multi-sensor arrays, redundant safety PLCs, and AI-based load-sway dampening to ensure mission-critical reliability. Component telemetry generates deep datasets that OEMs monetize through predictive-service subscriptions, reinforcing the shift toward outcome-based business models.

By Power Source: Electrification Accelerates Despite Diesel Dominance

Diesel configurations maintained 65.51% revenue share in 2024, reflecting established infrastructure and proven reliability for demanding applications, though this dominance faces increasing pressure from electrification trends. The installed base continues to receive autonomy bolt-ons that reduce fuel consumption through optimized duty cycles. Hybrid systems provide transitional solutions that combine diesel reliability with electric efficiency, particularly valuable for applications requiring extended operation periods with intermittent high-power demands.

Fully electric cranes, however, showcase an 18.59% CAGR propelled by port-emission mandates, silent-zone ordinances, and total-cost-of-ownership advantages in high-utilization fleets. Battery-swap stations and on-site microgrids minimize downtime, while regenerative-braking systems recapture energy to extend shifts. Battery technology improvements and charging infrastructure development continue reducing barriers to electric crane adoption across diverse application segments.

By Technology: IoT Monitoring Establishes Autonomous Foundation

IoT-enabled monitoring leads technology adoption at 47.08% market share in 2024, providing the data foundation necessary for predictive maintenance and autonomous operation capabilities. Sensors capture vibration signatures, hydraulic pressures, and boom deflection, enabling cloud dashboards that alert crews before faults escalate. Edge computing capabilities enable real-time decision-making without cloud connectivity dependencies, addressing reliability concerns in remote or challenging environments.

Predictive maintenance technology exhibits the highest growth rate at 21.45% CAGR, reflecting operators' focus on uptime optimization and cost reduction through proactive maintenance scheduling. AI-navigation stacks bolster risk mitigation in congested sites by executing centimeter-level moves that comply with geo-fenced work envelopes. Remote-operation stations leverage high-fidelity video and haptic feedback so one skilled driver can supervise multiple cranes sequentially, drastically improving labor productivity in mega-projects.

By Boom Type: Lattice Structures Dominate Heavy Applications

Lattice boom cranes dominate the market with a 58.34% share in 2024, underscoring their advantages in heavy lifting and their entrenched position in construction and industrial sectors. While lattice designs excel in load capacity and stability for rigorous tasks, telescopic systems stand out for their swift deployment and enhanced flexibility. The decision between boom types is increasingly shaped by specific application needs and the push for autonomous system integration. Telescopic systems shine in scenarios demanding frequent reconfiguration, whereas lattice systems are the go-to for maximizing capacity.

Telescopic boom systems are set to expand at a robust 13.38% CAGR through 2030. This growth is fueled by the operational ease and benefits of autonomous integration, which streamline setup and positioning. With autonomy, articulation control becomes a breeze, slashing setup times and boosting accuracy when picking near other structures. Both boom configurations benefit from advanced materials and design tweaks, achieving weight reductions and strength gains. This evolution supports the trend towards autonomous integration, all while maintaining top-notch lifting performance.

By Application: Construction Leads While Logistics Accelerates

Construction and mining applications dominate with 47.08% market share in 2024, reflecting the sector's scale and diverse lifting requirements that benefit from autonomous system capabilities. High-rise builds, tunnel segments, and open-pit operations deploy autonomous cranes to reduce accident frequency and keep schedules intact amid workforce volatility. Shipbuilding and port operations benefit from autonomous systems' ability to operate in challenging marine environments with consistent performance.

Logistics and warehousing exhibits the fastest growth at 17.16% CAGR, driven by e-commerce expansion and automated fulfillment center development that requires precision material handling. Autonomous overhead and gantry cranes synchronize with AGV fleets, forming continuous material-flow loops that slash staging time. Energy-sector use cases—especially wind-turbine component handling—will swell as OEMs standardize crane autonomy in installation protocols.

Geography Analysis

North America retained 33.77% revenue leadership in 2024 on the back of federal infrastructure appropriations, oil-and-gas field upgrades, and proactive safety legislation. Contractors embrace autonomous features to assure compliance, mitigate labor shortages, and cut premiums, while U.S. crane OEMs leverage domestic supply chains for rapid deployment cycles. Canadian resource projects in the Alberta oil sands and British Columbia hydropower installations further anchor demand. OEM after-sales networks intensify retrofit penetration across the aging fleet, ensuring sustained pull-through for software and analytic modules.

Asia-Pacific is projected to register a 12.22% CAGR, reflecting China’s Belt and Road corridor builds, India’s highway and metro expansions, and Southeast Asia’s port modernization programs. Government stimulus for smart-factory transitions fuels orders for overhead autonomous cranes in electronics and automotive clusters. Local telecom giants roll out 5G macro-cell grids that enable low-latency control loops, supporting autonomous spreader cranes in mega-ports. Japanese and South Korean shipbuilders adopt AI-enhanced cranes for block assembly, responding to heightened global competition.

Europe ranks third in overall volume but leads niche segments such as offshore wind installation and hybrid-electric drives. Stringent EU Green Deal directives trigger investment in zero-emission port equipment, catalyzing electric crane conversions. German machine-tool plants adopt autonomy to overcome demographic shifts and maintain global quality benchmarks. Scandinavian nations incorporate autonomous lattice booms into floating wind expansion roadmaps, cementing regional know-how that routes export opportunities into emerging Atlantic and Asian offshore markets.

Competitive Landscape

The autonomous crane market exhibits moderate fragmentation with established equipment manufacturers leveraging existing customer relationships and distribution networks to introduce autonomous capabilities. Established brands wield legacy customer trust and global service footprints, but the competitive axis has migrated toward software ecosystems, sensor suites, and AI algorithms. Early-mover OEMs embed edge-computing modules that run proprietary vision pipelines, enabling features such as real-time swing suppression and automated rig-up sequences.

Strategic partnerships between crane builders and cloud providers produce integrated dashboards that monetize uptime data, predictive-parts demand, and operator-performance analytics. High-growth retrofit specialists supply white-label autonomy kits engineered for multi-brand compatibility, shifting bargaining power toward software-centric firms. Meanwhile, hardware-only entrants face margin compression as autonomy layers become the primary differentiation and procurement criterion.

Pricing levers pivot from unit sales to subscription models covering software, cyber-security monitoring, and fleet-optimization analytics. Service-level agreements guaranteeing over 90% availability gain traction, echoing trends in construction equipment telematics. Vendors also invest in cyber-hardening certifications to reassure critical-infrastructure buyers who now mandate compliance with emerging IEC 62443 and ISO 23247 frameworks.

Autonomous Cranes Industry Leaders

Liebherr-International AG

Konecranes Plc

The Manitowoc Company, Inc.

Tadano Ltd.

Xuzhou Construction Machinery Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Croatian logistics specialist Paklog commissioned a Konecranes X-series overhead crane featuring radio control, hook-centering, and sway-control modules, achieving double-digit throughput gains.

- April 2025: Wolffkran debuted WOLFF Intuitive Control, a wireless joystick system that lets operators steer loads precisely without compensating for jib geometry.

- September 2024: China Construction Eighth Engineering Division unveiled an autonomous tower crane in Qingdao that executes lifts via 3-D path planning and active obstacle avoidance.

Global Autonomous Cranes Market Report Scope

| Mobile Crane | All-terrain Crane |

| Rough-terrain Crane | |

| Crawler Crane | |

| Truck-mounted Crane | |

| Other Mobile Cranes | |

| Fixed Crane | Monorail and Under-hung |

| Overhead Track-mounted | |

| Tower Crane | |

| Marine and Offshore Crane | Mobile Harbor Crane |

| Fixed Harbor Crane | |

| Offshore Crane | |

| Ship Crane |

| Up to 50 T |

| 51 to 150 T |

| 151 to 300 T |

| Above 300 T |

| Diesel |

| Hybrid |

| Fully Electric |

| AI-Powered Navigation |

| IoT-Enabled Monitoring |

| Predictive Maintenance |

| Remote Operation Systems |

| Lattice Boom |

| Telescopic Boom |

| Construction and Mining |

| Energy and Utilities |

| Shipbuilding and Ports |

| Industrial Manufacturing |

| Logistics and Warehousing |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Mobile Crane | All-terrain Crane |

| Rough-terrain Crane | ||

| Crawler Crane | ||

| Truck-mounted Crane | ||

| Other Mobile Cranes | ||

| Fixed Crane | Monorail and Under-hung | |

| Overhead Track-mounted | ||

| Tower Crane | ||

| Marine and Offshore Crane | Mobile Harbor Crane | |

| Fixed Harbor Crane | ||

| Offshore Crane | ||

| Ship Crane | ||

| By Capacity | Up to 50 T | |

| 51 to 150 T | ||

| 151 to 300 T | ||

| Above 300 T | ||

| By Power Source | Diesel | |

| Hybrid | ||

| Fully Electric | ||

| By Technology | AI-Powered Navigation | |

| IoT-Enabled Monitoring | ||

| Predictive Maintenance | ||

| Remote Operation Systems | ||

| By Boom Type | Lattice Boom | |

| Telescopic Boom | ||

| By Application | Construction and Mining | |

| Energy and Utilities | ||

| Shipbuilding and Ports | ||

| Industrial Manufacturing | ||

| Logistics and Warehousing | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the autonomous crane market in 2025?

The autonomous crane market size is USD 5.37 billion in 2025 and is projected to reach USD 9.43 billion by 2030.

Which crane type leads adoption of autonomous technology?

Mobile cranes dominate, accounting for 63.45% of 2024 revenue thanks to their versatility across construction and infrastructure projects.

What region is growing fastest for autonomous cranes?

Asia-Pacific shows the highest growth, with a forecast 12.22% CAGR on smart-port investment and rapid urbanization.

Which power source is expanding most quickly?

Fully electric cranes exhibit an 18.59% CAGR as ports and urban sites push for zero-emission equipment.

Why are predictive-maintenance systems important?

They underwrite a 21.45% CAGR within the technology segment by minimizing unplanned downtime and lowering life-cycle costs.

Page last updated on: