Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

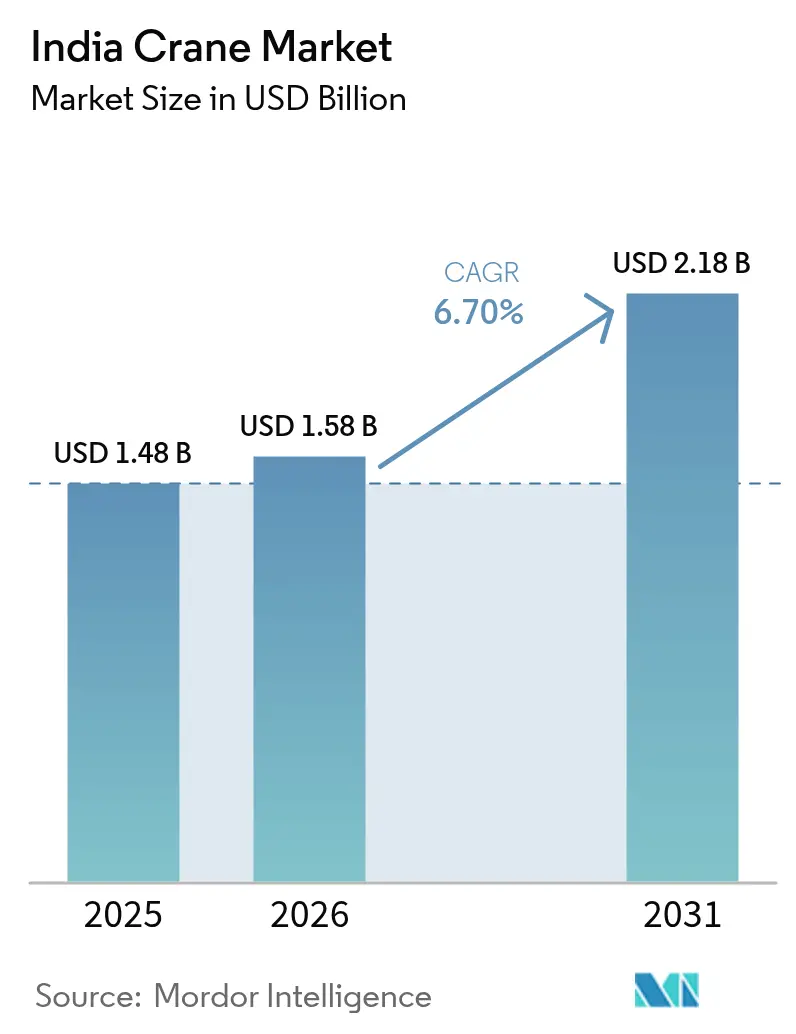

| Base Year Market Size (2025) | USD 1.48 Billion |

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.18 Billion |

| Growth Rate (2026 - 2031) | 6.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Crane Market Analysis by Mordor Intelligence

The India crane market size was valued at USD 1.48 billion in 2025 and estimated to grow from USD 1.58 billion in 2026 to reach USD 2.18 billion by 2031, at a CAGR of 6.70% during the forecast period (2026-2031). Rapid infrastructure modernization, the USD 1.4 trillion National Infrastructure Pipeline (NIP), and strong growth in renewable-energy installations anchor demand for mobile, crawler, and tower cranes across capacity classes[1]“Crane Market Sees Demand Surge on NIP Projects,”, Construction World Editorial Team, constructionworld.in. Contractor preference for mechanized lifting over labor-intensive methods accelerates fleet replacement with higher-capacity, telematics-enabled units. Public–private partnerships in metro-rail and regional rapid-transit corridors compress construction timelines, favoring rental-first procurement. Renewable-energy build-out, especially wind projects calling for 800-ton crawler cranes, deepens application diversity, while electric-power trains begin challenging diesel dominance as environmental standards tighten. Competitive intensity rises as Action Construction Equipment (ACE) defends its domestic stronghold against cost-competitive Chinese OEMs that localize production to manage rupee volatility and compliance with the Bureau of Indian Standards Scheme X.

Key Report Takeaways

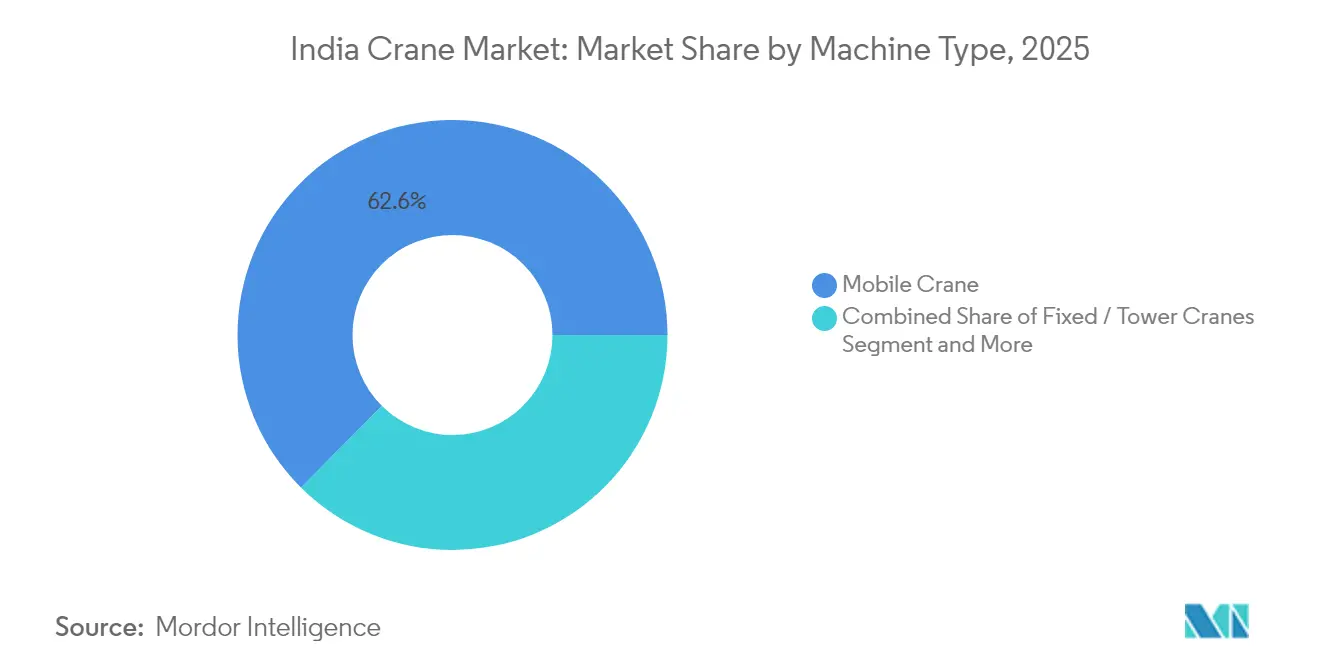

- By machine type, mobile cranes led with 62.55% of the India crane market share in 2025; crawler cranes recorded the fastest CAGR at 8.62% through 2031.

- By application, construction accounted for a 57.05% share of the India crane market size in 2025, while energy and utilities advanced at a 10.22% CAGR to 2031.

- By lifting capacity, 20-100 ton units held 45.74% of the India crane market size in 2025; above-300-ton units expanded at a 9.05% CAGR through 2031.

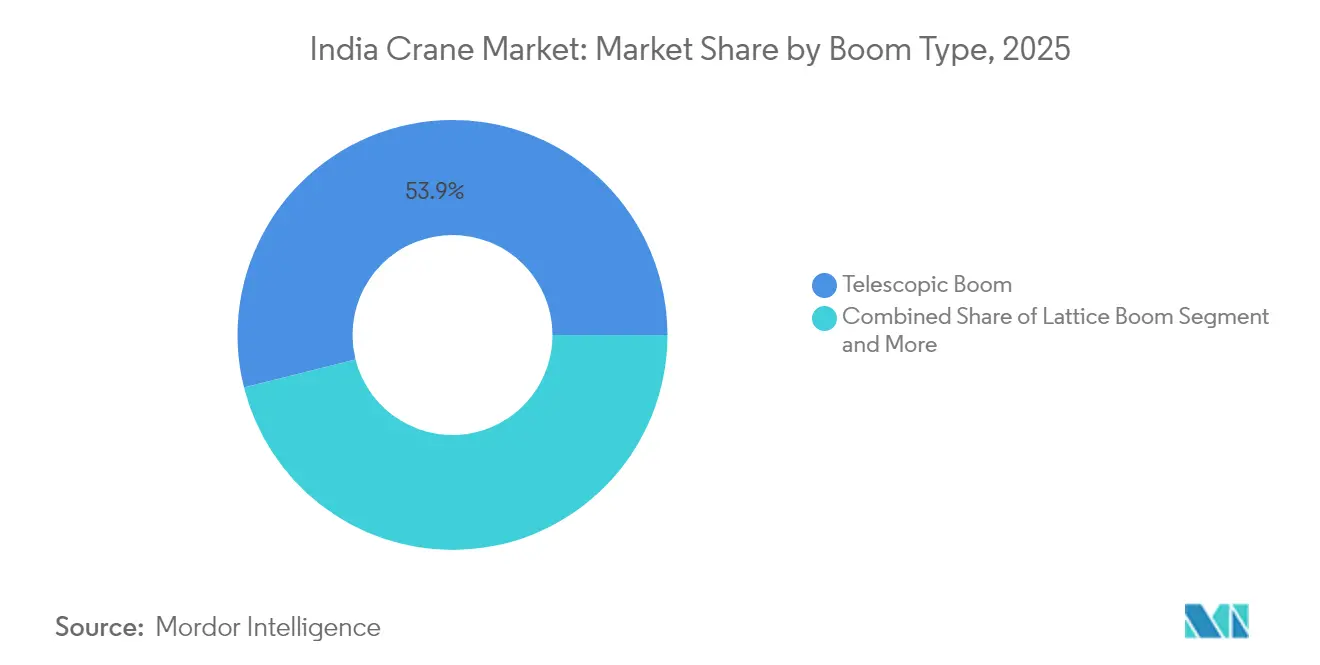

- By boom type, telescopic designs commanded 53.92% revenue share in 2025; lattice boom variants progressed at a 9.50% CAGR to 2031.

- By power source, diesel models captured 82.45% revenue in 2025; fully electric cranes climbed at a 10.18% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Crane Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NIP Investments | +1.2% | National; tier-1 and tier-2 cities | Long term (≥ 4 years) |

| Smart Cities Housing | +1.0% | 100 Smart Cities | Medium term (2-4 years) |

| Renewable Heavy-lift Demand | +1.1% | Gujarat; Rajasthan; Tamil Nadu; Karnataka; Maharashtra | Long term (≥ 4 years) |

| PPP Metro and RRTS | +0.8% | Delhi NCR; Mumbai; Bangalore; Chennai; Hyderabad | Medium term (2-4 years) |

| Rental-first EPC | +0.7% | Nationwide industrial corridors | Short term (≤ 2 years) |

| Telematics and Autonomy | +0.5% | Metro cities; industrial clusters; large projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in National Infrastructure Pipeline (NIP) Investments

The USD 1.4 trillion NIP funds highway, port, airport, and urban-transport projects, lifting annual crane demand by prioritizing mechanized construction over manual labor. Road works under Bharatmala and port upgrades via Sagarmala contribute 30-40% of all construction-equipment volumes. Contractors rely on rentals to ensure on-time availability, which underpins Sanghvi Movers’ double-digit fleet additions.

Housing-Led Urban Revitalization Under Smart Cities Mission

The Smart Cities Mission funnels over USD 20 billion into 8,000 active projects, generating dense urban core lifting needs suited to tower cranes and compact mobiles [2]“Smart City Projects Push Demand for IoT-Ready Cranes,”, NBM&CW Editors, nbmcw.com. With over 65% tower-crane share, ACE plans 25-ton flattop launches to address high-rise clusters. Sustainability mandates push electric and hybrid cranes that cut emissions and noise. Project management platforms demand IoT-ready lifting solutions, turning telematics from optional to essential.

24×7 Renewable-Energy Build-Out Driving Heavy-Lift Demand

India’s 500 GW non-fossil target boosts demand for 600- to 800-ton crawler cranes that erect 3 MW wind turbines with 168-meter boom systems. SANY’s SCC8000A handover in Gujarat evidences the shift toward super-heavy classes. Solar parks create high-volume mobile crane needs in remote terrains. Environmental clearances incentivize electric-drive cranes in ecologically sensitive zones.

Automation Push: Telematics and Autonomous Cranes Pilots

SANY’s E-Vision suite and Caterpillar IoT platforms provide real-time health diagnostics that shift maintenance from reactive to predictive. Cableless controls from AUTEC pave the way for semi-autonomous cranes that mitigate operator shortages. BIS standards are moving toward mandatory telematics for safety oversight, embedding connectivity in future purchase decision.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Operator Shortage | -0.8% | Nationwide; tier-2 and tier-3 cities | Short term (≤ 2 years) |

| Working-capital Strain | -0.6% | Regional MSME rental operators | Short term (≤ 2 years) |

| Rupee Volatility | -0.5% | Import-dependent OEMs nationwide | Short term (≤ 2 years) |

| Fragmented Safety Regs | -0.4% | State-level variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Crane Operators and Riggers

A shortfall in certified personnel limits fleet utilization as equipment sophistication outruns skill supply. The Infrastructure Equipment Skill Council offers 6- to 12-month courses, yet demand outstrips throughput. OEM-run academies train operators, but advanced wind-lift or metro-rigging expertise remains scarce, keeping labor a growth bottleneck[3]“Skill Shortage Hinders Crane Operations,”, NBMCW Editors, nbmcw.com.

High Working-Capital Cycle for Small Rental Fleets

Construction receivables often stretch 90-180 days, straining MSME fleet owners who must service loans while equipment sits idle[4]“Credit Risks Rise for Equipment Rentals,”, Autocar Professional Analysts, autocarprofessional.com. Illegal exports of pledged machinery heighten lender risk, tightening credit. Smaller players, therefore, stick to mid-capacity cranes with quicker payback, ceding super-heavy segments to large operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Mobile Cranes Lead Infrastructure Surge

The mobile-crane segment captured 62.55% of the India crane market size in 2025, thanks to fast deployment across road, port, and industrial sites. Its dominance persists as contractors demand versatile lifting that keeps pace with compressed project schedules. Fixed and Tower-crane demand, expanding at an 8.20% CAGR, mirrors growth in needing stable heavy-lift solutions. Fixed tower cranes remain staples in high-rise residential clusters under Smart Cities Mission, while marine cranes carve a niche through electric harbor installations such as Visakhapatnam’s twin Liebherr LHM 550 units.

Mobile-crane manufacturers tailor designs around all-terrain mobility and telematics, deepening rental appeal. Crawler-crane OEMs focus on 400- to 800-ton models featuring long booms and self-assembly systems that cut erection time. Importantly, crawler units face stricter BIS scrutiny under high-risk categories, making certification history a procurement criterion. As rental fleets chase utilization, diversified inventories encompassing mobiles for general works and crawlers for specialist lifts become a competitive necessity. Consequently, ACE sustains scale in mobile lines, while SANY, Liebherr, and Kobelco target crawler opportunities with localized production aimed at the India crane market.

By Application: Construction Dominance Faces Energy Challenge

Construction retained 57.05% of 2025 revenue, positioning it as the backbone of the Indian crane market. Housing, commercial complexes, and transport corridors anchor steady lifting needs spanning 20- to 100-ton mobiles and tower cranes. Energy and utilities, however, post a 10.22% CAGR as super-heavy crawlers support 3 MW wind turbine erection across Gujarat and Karnataka. Mining, marine, and industrial manufacturing trail yet contribute niche demand requiring specialized dimensions or environmental compliance.

Construction-sector growth remains tied to NIP project rollouts and PPP execution momentum. Meanwhile, the renewable boom brings geographically concentrated but capacity-intensive requirements, prompting rental operators to cluster heavy gear near wind corridors for sequential deployment. Crane OEMs respond by integrating quick-transport systems and modular counterweights that shorten mobilization between remote sites. As power-plant developers mandate lower carbon footprints, hybrid and electric drives penetrate utility applications faster than general building, adding technological diversity to the Indian crane market.

By Lifting Capacity: Mid-Range Dominance, Heavy-Lift Acceleration

Mid-range 20-100 ton models controlled 45.74% of 2025 shipments, constituting the workhorse class for general construction. The above 300-ton variants, propelled by wind-energy tasks, registered a 9.05% CAGR and represent the fastest-growing slice of India's crane market share. Sub-20-ton segments cater to inner-city redevelopment, while 100-300 ton units provide the transition toward specialized industrial assembly.

Rising hub heights and heavier nacelles amplify crawler-crane capacities, leading OEMs to debut 800-ton platforms with luffing-jib extensions surpassing 168 meters. Such super-heavy units often remain on long-term rental to recoup multimillion-dollar acquisition costs. Certification, ballast logistics, and operator skill requirements deepen barriers, leaving heavy-lift space to a handful of national fleet owners. Conversely, mid-range cranes remain the preferred entry point for MSME contractors and rental startups serving the expanding India crane market.

By Boom Type: Telescopic Efficiency Versus Lattice Reach

Telescopic booms delivered 53.92% revenue in 2025, favored for rapid setup and road mobility. Lattice booms’ 9.50% CAGR stems from superior reach-to-weight ratios valuable for erecting tall wind turbines and metro viaducts. Knuckle booms, though small in volume, solve space-constrained material handling in industrial plants and shipyards.

Telescopic innovations such as multi-section single-cylinder synchronization increase free-standing heights, challenging lattice supremacy in some mid-capacity lifts. Yet, lattice systems maintain low bending moments, supporting 120-meter hub installations. Rental owners therefore stock both boom types to match varying lift plans, ensuring utilization in the India crane market across infrastructure and industrial timelines.

By Power Source: Diesel Dominance Faces Electric Transition

Diesel cranes secured 82.45% revenue in 2025 as fuel access and refueling ease kept operating costs predictable. Electric cranes, however, posted a 10.18% CAGR, accelerated by port authorities and urban municipalities favoring zero-emission zones. Hybrid units bridge limitations, offering battery-assisted duty cycles that cut fuel use by up to 25% without sacrificing endurance.

Grid-connected projects, such as metro depots, now specify shore-powered electric crawlers to meet local air-quality rules, while harbor operators adopt battery cranes like Liebherr LHM 550 to curb marine-diesel particulate emissions. Infrastructure gaps in rural wind parks slow electric adoption, but OEMs develop containerized fast-charge stations to extend operational footprints. Policy incentives under FAME III could further tilt procurement, making drive-train choice a strategic variable in the India crane market.

Geography Analysis

Gujarat, Maharashtra, Tamil Nadu, and Karnataka collectively represent close significant share of crane demand, reflecting robust industrial corridors, port construction, and renewable capacity additions. Western India benefits from Sagarmala port modernization and petrochemical expansions that consume diversified lifting capacities. Northern India, spearheaded by Delhi NCR, channels metro-rail, RRTS, and Smart City projects that absorb a mix of tower, mobile, and crawler cranes.

Southern states propel wind-energy uptake, with Tamil Nadu and Karnataka hosting clustered turbine-installation campaigns requiring 600- to 800-ton crawlers. Bangalore’s IT hub and Hyderabad’s pharma clusters add steady industrial lifting. Eastern India, historically mining-centric, sees incremental gains from mechanized coal extraction and steel-plant upgrades, yet its aggregate share lags western and southern peers.

Regional rental hubs evolve near industrial parks, allowing fleet owners to redeploy assets swiftly among contiguous projects. Nevertheless, state-specific safety approvals create administrative hurdles for itinerant equipment, prompting larger fleets to maintain local compliance teams. Tier-2 and tier-3 urban centers emerge as untapped pockets where cost-sensitive mid-capacity mobiles dominate, widening the geographic dispersion of the India crane market.

Competitive Landscape

The India crane market remains moderately concentrated. ACE leverages an extensive dealer footprint and application-specific product tweaks to fend off global rivals. Chinese OEMs—SANY, XCMG, and Zoomlion—expand local assembly to dilute import duties and hedge rupee swings. SANY eyes INR 30,000 crore top-line by 2030 through portfolio diversification and Scheme X-compliant designs.

Collaborations intensify: ACE and Kato explore medium- and large-crane joint production, while Escorts Kubota aligns with Tadano for premium rough-terrain models. Technology becomes the next battleground as IoT diagnostics, autonomous controls, and electric drivelines differentiate offerings. Large rental firms influence road-maps by specifying telematics and quick-erection features. Regulatory rigor under BIS Scheme X consolidates share among capital-strong incumbents who can navigate certification costs, pointing to gradual upticks in overall concentration within the India crane market.

India Crane Industry Leaders

Action Construction Equipment Limited

Liebherr Group

Konecranes

Tata Hitachi

Kobelco Construction Equipment

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Green Energy Resources procured two electric Liebherr LHM 550 harbor cranes (124-ton SWL) for Visakhapatnam port EQ1A, spotlighting zero-emission marine lifting.

- January 2025: SANY delivered India’s first 800-ton SCC8000A crawler crane to Dwarkesh Transport for wind projects in Kutch, Gujarat.

- August 2024: Kobelco launched the SK80 excavator with 70% indigenous content, reinforcing India as a key export hub.

India Crane Market Report Scope

A crane is a type of heavy machinery that is primarily used for lifting and moving heavy or large objects

The Indian crane market is segmented by machine type and by application.By machine type the market is segmented into mobile cranes, fixed cranes, and marine and port cranes and by application the market is segmented into construction, mining and excavation, marine and offshore, industrial, and other applications. The report offers market size and forecasts for the Indian crane market in value (USD) for above all segments.

By Machine Type

| Mobile Cranes |

| Fixed / Tower Cranes |

| Marine & Port Cranes |

By Application

| Construction |

| Mining and Excavation |

| Marine and Offshore |

| Industrial Manufacturing |

| Energy and Utilities |

By Lifting Capacity

| Below 20 tons |

| 20 - 100 tons |

| 100 - 300 tons |

| Above 300 tons |

By Boom Type

| Telescopic Boom |

| Lattice Boom |

| Knuckle Boom |

By Power Source

| Diesel |

| Hybrid |

| Fully-Electric |

| By Machine Type | Mobile Cranes |

| Fixed / Tower Cranes | |

| Marine & Port Cranes | |

| By Application | Construction |

| Mining and Excavation | |

| Marine and Offshore | |

| Industrial Manufacturing | |

| Energy and Utilities | |

| By Lifting Capacity | Below 20 tons |

| 20 - 100 tons | |

| 100 - 300 tons | |

| Above 300 tons | |

| By Boom Type | Telescopic Boom |

| Lattice Boom | |

| Knuckle Boom | |

| By Power Source | Diesel |

| Hybrid | |

| Fully-Electric |

Key Questions Answered in the Report

What is the current value of the India crane market and its expected growth by 2031?

The market is valued at USD 1.58 billion in 2026 and is projected to reach USD 2.18 billion by 2031, reflecting a 6.70% CAGR.

Which crane type leads demand across India’s infrastructure projects?

Mobile cranes hold the largest share at 62.55% of 2025 shipments because their versatility suits roads, ports, and industrial sites.

Why are crawler cranes gaining momentum in India?

Crawler cranes post an 8.62% CAGR through 2031 due to renewable-energy and metro-rail projects requiring heavy-lift capabilities and long booms.

Which power source is growing fastest in Indian crane fleets?

Fully electric cranes record a 10.18% CAGR as ports, metro depots, and urban projects mandate lower emissions and quieter operations.

What is the biggest hurdle slowing crane deployment in India?

A shortage of certified operators and riggers constrains fleet utilization despite rising equipment availability.

Page last updated on: