Rail Mounted Gantry Crane Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

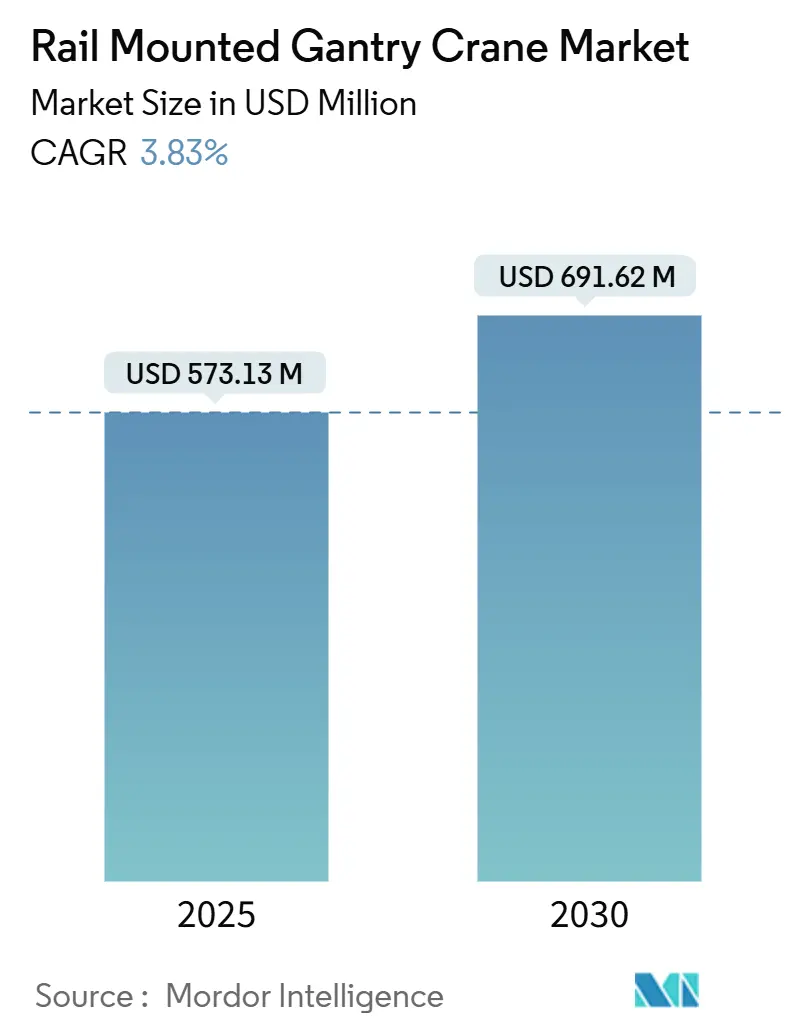

| Market Size (2025) | USD 573.13 Million |

| Market Size (2030) | USD 691.62 Million |

| Growth Rate (2025 - 2030) | 3.83% CAGR |

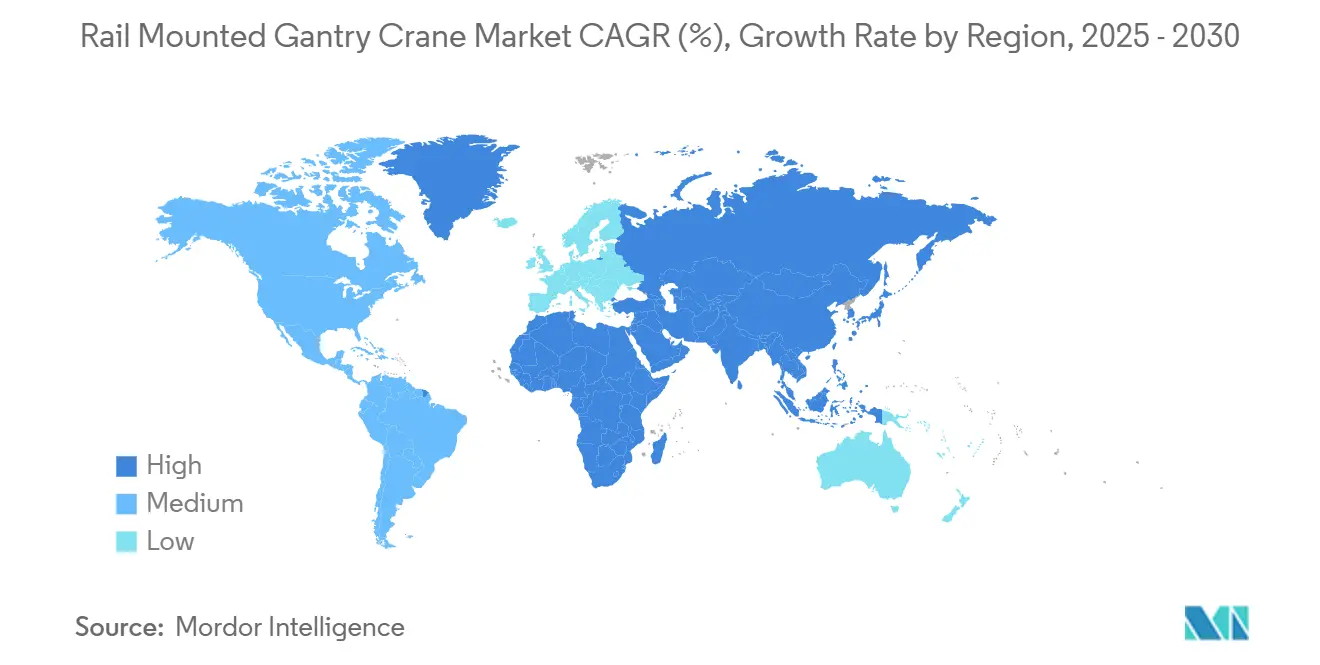

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

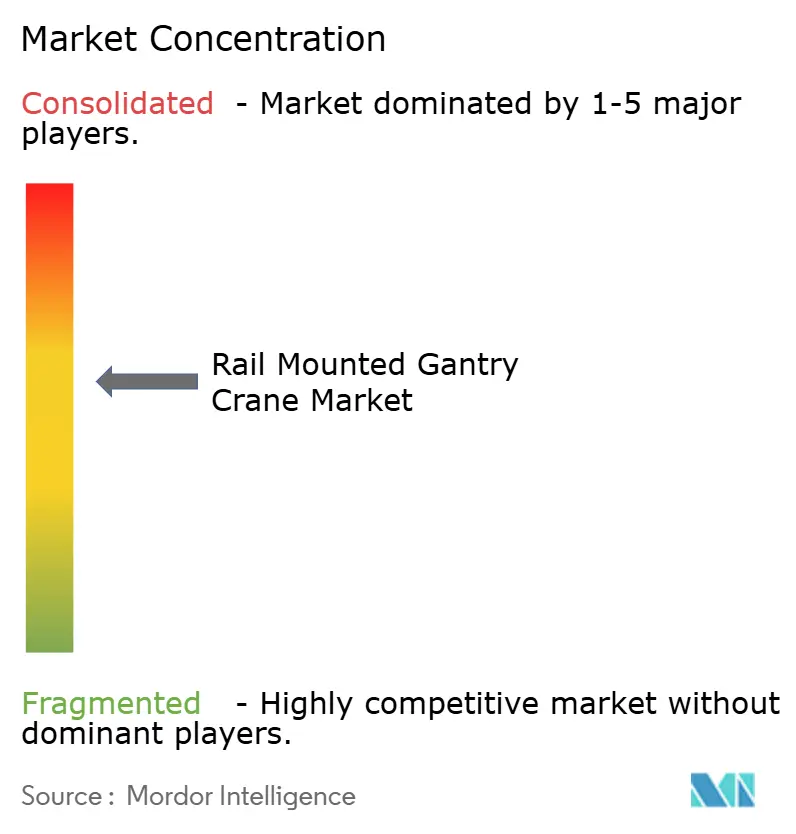

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rail Mounted Gantry Crane Market Analysis by Mordor Intelligence

The rail mounted gantry crane market size reached USD 573.13 million in 2025 and is forecasted to advance to USD 691.62 million by 2030, registering a CAGR of 3.83% during the forecast period (2025-2030). Robust port automation programs and continuing infrastructure modernization underpin steady demand[1]“Port Statistics and Reports,” Port of Long Beach, polb.com. Increased electrification initiatives cut operating expenses, while advanced automation raises terminal productivity, making capital investment in these cranes more attractive despite high upfront costs. Asia-Pacific sustains leadership through scale, integrated supply chains, and supportive government investment, whereas Africa posts the fastest growth as trade corridors diversify and PPP projects unlock funding. Rising adoption in offshore wind, larger lifting capacities, and wide-span designs illustrate how end users are tailoring specifications to heavier, more varied cargo profiles. Moderate market concentration allows leading manufacturers to preserve pricing power, yet the pivot toward software, predictive maintenance, and low-emission operation sharpens competition.

Key Report Takeaways

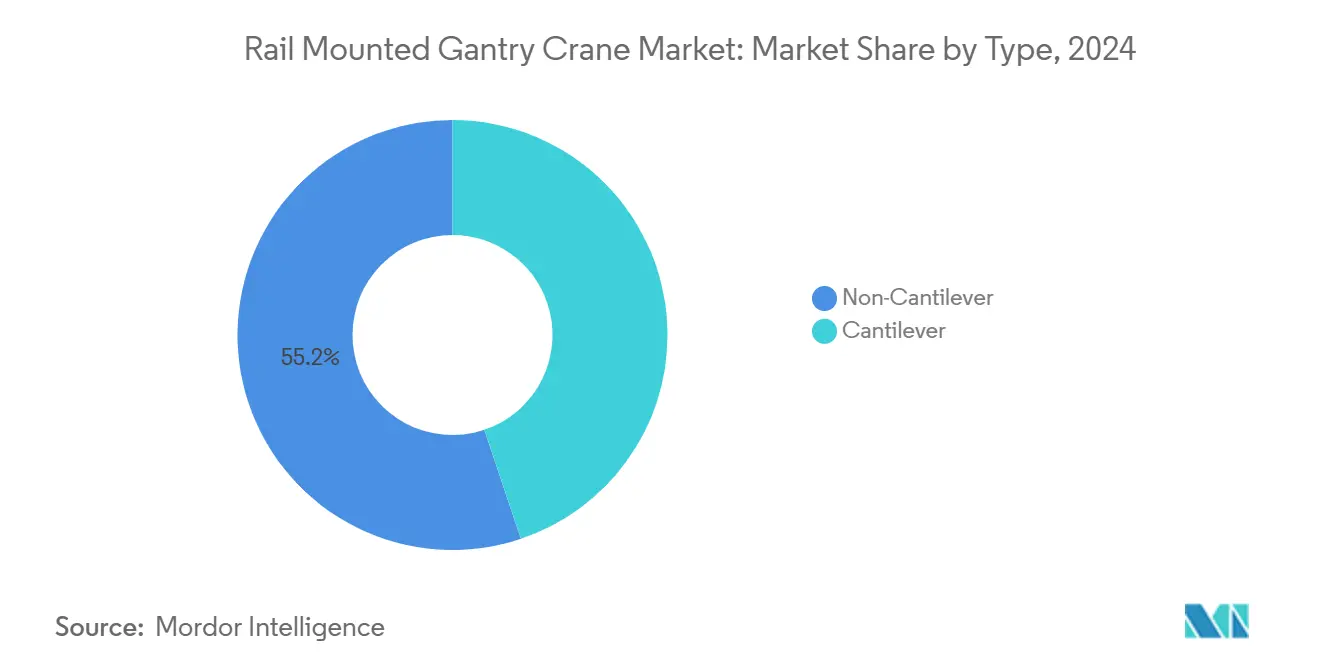

- By type, non-cantilever configurations captured 55.16% of the rail-mounted gantry crane market share in 2024. Meanwhile, cantilever designs are expected to be on track for a 4.56% CAGR during the forecast period (2025-2030).

- By end-use industry, ports and terminals led with 41.88% revenue share of the rail mounted gantry crane market in 2024; offshore wind is projected to expand at a 5.49% CAGR during the forecast period (2025-2030).

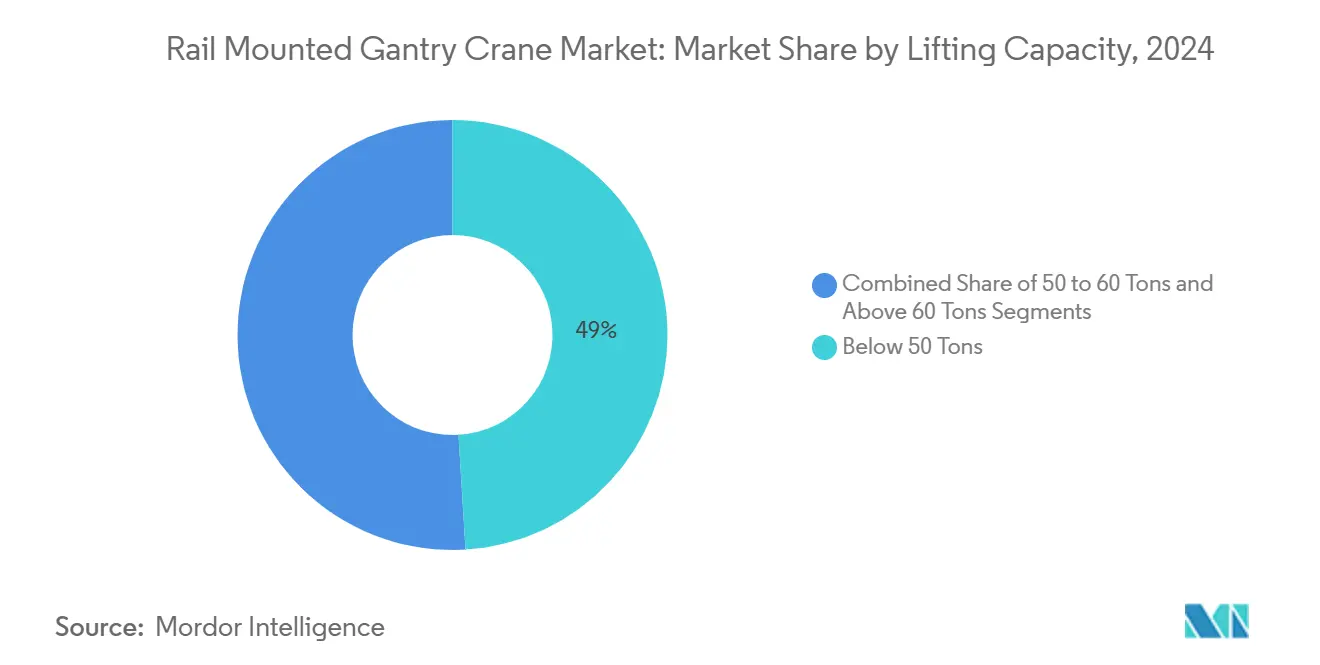

- By lifting capacity, the below-50-ton segment accounted for 49.03% of the rail-mounted gantry crane market size in 2024, but the above-60-ton range is advancing at a 5.21% CAGR during the forecast period (2025-2030).

- By span width, 30-40 m systems held a 48.01% share of the rail mounted gantry crane market in 2024, whereas above 40 m spans are growing at a 4.73% CAGR during the forecast period (2025-2030).

- By geography, Asia-Pacific commanded a 53.73% share of the rail mounted gantry crane market in 2024, and Africa is expected to post the highest 4.67% CAGR during the forecast period (2025-2030).

Global Rail Mounted Gantry Crane Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Container-Throughput | +1.2% | Global, with APAC core concentration | Short term (≤ 2 years) |

| Electrification and Hybridization | +0.8% | North America & EU leading, APAC following | Medium term (2-4 years) |

| Automation and Remote-Operation Mandates | +0.6% | Global, early adoption in developed markets | Medium term (2-4 years) |

| PPP Investment Pipelines | +0.5% | Asia-Pacific, Middle East, Africa, South America | Long term (≥ 4 years) |

| Hydrogen-Powered Crane Pilots | +0.3% | Europe, with spillover to North America | Long term (≥ 4 years) |

| AI-Based Predictive-Maintenance | +0.2% | Global, technology-advanced markets first | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Container Throughput at Mega-Ports

Global ports processed record volumes in 2024, intensifying yard congestion and driving urgent investment in higher-capacity rail mounted gantry cranes. The scale advantage favors mega-ports that already possess rail infrastructure, as smaller sites struggle to match service levels. Operators are upgrading to taller, faster cranes that maximize stacking density within fixed footprints. Asia-Pacific benefits disproportionately because 15 of the top 20 container ports are located in the region, reinforcing its dominant share. Procurement cycles have consequently shortened, pushing OEMs to expand production capacity and modularize designs for quicker delivery schedules.

Rapid Electrification and Hybridization of Yard Equipment

Terminal operators accelerated electrification to meet decarbonization targets, with electric rail mounted gantry systems cutting energy costs by up to 70% compared with diesel. Regenerative braking technology further lowers net consumption by as much as 30%. European ports lead adoption under strict emissions rules; North American facilities follow through with Clean Air Act compliance and state incentives. Where grid capacity lags, hybrid battery-assisted cranes provide a transitional path, smoothing peak loads and reducing reliance on diesel gensets. These dynamics boost demand for advanced power-management software and modular battery packs, creating new revenue streams for component suppliers.

Automation and Remote-Operation Mandates by Top Terminal Operators

Major operators, including APM Terminals and DP World, now specify remote-operation and collision-avoidance systems in new tenders, citing gains of 25-30% in container moves per hour and lifecycle labor savings near 50%. The result is a technology race among OEMs to embed AI algorithms, high-resolution vision systems, and redundant safety architectures. Early adopters highlight productivity wins at facilities such as Peru’s Chancay port. Software expertise has become as critical as mechanical engineering, influencing M&A activity aimed at acquiring niche automation firms.

Port-Led PPP Investment Pipelines (Asia, MEA, South America)

Public-private partnership frameworks unlocked multiple port projects, with China’s Belt and Road Initiative contributing heavily[2]“China’s Belt and Road Initiative: Observations on Large-Scale Infrastructure Financing,” U.S. Government Accountability Office, gao.gov. Long-tenure concessions help spread capital costs for rail-mounted gantry equipment, ensuring a steady order flow. Governments stipulate technology transfer and local assembly, encouraging OEMs to form joint ventures and establish regional service hubs. Indonesia, Egypt, and several Gulf states exemplify this model, coordinating multi-terminal expansions that bundle crane procurement with training and maintenance contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CAPEX and Long Pay-Back Period | -0.7% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Skilled-Operator Shortage | -0.4% | Africa, South America, Southeast Asia | Medium term (2-4 years) |

| Grid-Capacity Constraints | -0.3% | Emerging markets with limited infrastructure | Medium term (2-4 years) |

| Volatile Steel Prices | -0.2% | Global, affecting all manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Long Payback Period

Rail-mounted gantry systems require substantial initial investments, with payback periods extending 7-10 years in typical terminal operations. This capital intensity creates financing challenges for smaller port operators and emerging market terminals, where access to long-term credit remains limited despite strong operational demand. Equipment-as-a-service models are emerging, shifting capital cost to multiyear operating leases, yet lender familiarity with such structures remains limited, slowing scale-up.

Skilled-Operator Shortage at Emerging Ports

Emerging market ports face acute shortages of qualified RMG operators and maintenance technicians, with African ports specifically citing "lack of skilled labour" as a primary constraint preventing them from capitalizing on trade growth opportunities. Training programs for conventional crane operators span six to twelve months, while automated-system technicians require even deeper digital proficiency. Maritime academies and OEM-run training centers are multiplying, but the pipeline still lags demand. Staffing shortfalls cause lower utilization rates for newly installed equipment, restraining productivity gains that justify investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cantilever Growth Accelerates Despite Non-Cantilever Dominance

Non-cantilever designs represented 55.16% of the rail-mounted gantry crane market share in 2024, driven by their structural simplicity and lower maintenance requirements in high-volume container terminals. These systems offer superior stability for repetitive lifting operations and reduced structural complexity, making them preferred for standardized container handling applications where operational predictability outweighs flexibility considerations. Cantilever variants are forecast to grow at a 4.56% CAGR to 2030 as ports require side-reach flexibility for mixed cargo.

Cantilever cranes incorporate variable-geometry booms and dual-trolley setups that adapt to irregular loads, enabling single equipment fleets to service both container bays and project cargo. Recent product launches with active load-balancing and sway control illustrate how technology is closing performance gaps with traditional models. As terminals diversify revenue streams, cantilever market penetration is expected to rise gradually, shifting procurement specifications in upcoming tenders.

By End-Use Industry: Offshore Wind Drives Fastest Growth Beyond Port Dominance

Ports and terminals captured 41.88% revenue of the rail-mounted gantry crane market size in 2024, underscoring container handling as the core application that anchors the rail-mounted gantry crane market. Most Tier 1 and Tier 2 ports use standardized below-50-ton units, ensuring high base demand. Offshore wind, however, is poised for a 5.49% CAGR through 2030 as turbine components grow heavier and require precise land-side handling.

Project developers are specifying above-60-ton capacity cranes with fine positioning systems for nacelle and blade logistics. The rail mounted gantry crane market size tied to offshore wind is projected to triple this decade, supported by national renewable-energy targets and coastal yard expansion. OEMs able to certify cranes for harsh-environment corrosion resistance and synchronous tandem lifting are increasingly shortlisted.

By Lifting Capacity: Heavy-Lift Demand Accelerates Infrastructure Evolution

Below-50-ton machines dominated 49.03% of the rail-mounted gantry crane market size in 2024, owing to standardized container dimensions and high production volumes. This segment benefits from economies of scale in manufacturing and standardized operational procedures across global terminals. Mid-range 50-60-ton units serve specialized container-plus-break-bulk operations. Above-60-ton cranes are forecast to achieve a 5.21% CAGR as the shipping and energy sectors shift toward oversized cargoes.

The heavier class integrates high-precision load-moment protection and digital twins for stress simulation. Growth in shipyard modernization and modular offshore construction is broadening the customer base. As mixed cargo flows become routine, many ports plan split fleets that blend light, fast container units with fewer but powerful heavy-lift gantries to optimize berth utilization. The segment evolution suggests terminals will increasingly require mixed-capacity fleets to handle diverse cargo profiles efficiently.

By Span Width: Wide-Span Systems Enable Terminal Density Optimization

The 30 to 40 m span width category held 48.01% share of the rail-mounted gantry crane market size in 2024, representing the optimal balance between structural efficiency and operational coverage for standard terminal layouts. These systems align with typical container stacking configurations and rail spacing standards established at major ports worldwide. Below-30 m spans cater to inland depots and constrained brownfield sites. Systems above 40 m will climb at 4.73% CAGR as terminals pursue higher stacking density and operational efficiency through wider coverage areas.

Advanced finite-element design and high-strength steels allow above-40 m cranes to maintain stiffness without excess weight. Ports facing land scarcity adopt these wide-span units to boost stacking density, often pairing them with automated guidance for collision avoidance. Wide-span RMG systems enable terminals to maximize land utilization by reducing the number of required rail tracks while maintaining operational coverage, particularly valuable in land-constrained port environments where real estate costs are prohibitive.

Geography Analysis

Asia-Pacific sustained 53.73% revenue share of the rail-mounted gantry crane market in 2024, propelled by a dense cluster of top-tier container ports and integrated manufacturing ecosystems that lower the total cost of ownership. Shanghai handled 50 million TEU in 2024, exemplifying how mega-ports create continuous demand for rail-mounted gantry upgrades. Regional governments continue to fund berth expansions and smart-port pilots, keeping order backlogs healthy. Japan and South Korea emphasize precision heavy-lift variants for shipbuilding, while Southeast Asian nations invest to capture transshipment flows siphoned from primary hubs.

Africa records the highest 4.67% CAGR for 2025-2030, underpinned by expanding corridors such as the West Africa growth ring and the modernization of South African logistics nodes. Although skilled-labor shortages and limited grid capacity temper full-electric adoption, PPP structures are channeling capital into crane procurement bundled with training and maintenance. Egypt’s canal corridor zones and Nigeria’s deepwater projects illustrate shifting trade gravity that favors larger, automated yards.

Europe and North America are mature, with 2.32% and 2.81% CAGRs, respectively. Investment centers on replacement and technological retrofits rather than greenfield capacity. The Port of Cleveland’s USD 94 million Clean Ports award in 2024 accelerates electrified crane procurement and underscores federal commitment to emissions reduction. European operators lead in hydrogen pilots and fully automated stacking, leveraging regulatory incentives and skilled labor advantages. Western Asia (mainly GCC countries) posts 3.76% CAGR, fueled by logistics diversification away from hydrocarbons and strategic positioning between East-West trade lanes.

Competitive Landscape

The Rail Mounted Gantry Crane Market exhibits moderate concentration, creating oligopolistic dynamics that enable sustained pricing power while limiting competitive intensity. Shanghai Zhenhua Heavy Industries leverages large-scale integrated production and cost control to anchor most high-volume port projects. Konecranes differentiates through proprietary remote-monitoring software that locks clients into long-term service plans. Liebherr ranks secured orders that demand custom engineering and heavy-lift capability. Regional specialists such as Doosan and SANY capture niche opportunities, especially in domestic public–private partnership contracts that favor local content.

Competition is shifting from mechanical strength to digital performance. Terminal bids now require integrated collision-avoidance, energy-management, and predictive-maintenance modules as baseline features rather than add-ons. Konecranes bundles its TRUCONNECT analytics subscription with every new unit, boosting recurring revenue and creating switching costs for customers. ZPMC counters with vertically integrated automation suites that pair cranes with yard-management software, allowing a single-vendor solution from quay to stack.

Strategy also revolves around alternative financing and lifecycle partnerships. Liebherr signed a 20-year asset-management agreement with Transnet in 2025, ensuring stable parts and service income while guaranteeing uptime metrics. ZPMC offers build-operate-transfer models in Belt and Road markets, trading near-term margin for multi-decade concession revenue. New entrants such as Huisman focus on equipment-as-a-service contracts that shift capital expense to operating leases, appealing to smaller ports with tight budgets. Battery suppliers and hydrogen integrators are forging alliances with crane OEMs to co-develop low-emission models, signaling deeper convergence between heavy machinery and clean-tech ecosystems.

Rail Mounted Gantry Crane Industry Leaders

Shanghai Zhenhua Heavy Industries (ZPMC)

Konecranes Plc

Liebherr-International AG

Kalmar (Cargotec)

SANY Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Transnet Port Terminals signed a ten-year partnership with Liebherr covering multiple crane types and a 20-year asset-management program to raise reliability across South African ports.

- June 2025: Huisman announced its first order for rail mounted yard gantry cranes, emphasizing lifecycle serviceability in new ASC and RMG designs.

- April 2025: RIKON completed installation of a rail mounted gantry crane at Uzbekistan’s First Dry Port Terminal, signaling rising demand in Central Asian intermodal hubs.

- February 2025: Rijeka Gateway received its final two ship-to-shore cranes from ZPMC, completing yard equipment deliveries ahead of terminal launch.

Global Rail Mounted Gantry Crane Market Report Scope

| Cantilever |

| Non-Cantilever |

| Shipbuilding |

| Offshore Wind |

| Ports and Terminals |

| Power Generation |

| Mining |

| Other Industries |

| Below 50 Tons |

| 50 to 60 Tons |

| Above 60 Tons |

| Below 30 m |

| 30 to 40 m |

| Above 40 m |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Cantilever | |

| Non-Cantilever | ||

| By End-Use Industry | Shipbuilding | |

| Offshore Wind | ||

| Ports and Terminals | ||

| Power Generation | ||

| Mining | ||

| Other Industries | ||

| By Lifting Capacity | Below 50 Tons | |

| 50 to 60 Tons | ||

| Above 60 Tons | ||

| By Span Width | Below 30 m | |

| 30 to 40 m | ||

| Above 40 m | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What was the global value of the rail mounted gantry crane market in 2025?

The rail mounted gantry crane market size stood at USD 573.13 million in 2025.

Which region holds the largest share of revenue?

Asia-Pacific accounted for 53.73% of global revenue in 2024, reflecting its concentration of high-volume container ports.

What segment is growing fastest by end use?

Offshore wind applications are forecast to expand at a 5.49% CAGR between 2025 and 2030 as turbine components become heavier.

How fast is the above 60 tons lifting-capacity segment growing?

Cranes rated above 60 tons are projected to grow at 5.21% CAGR through 2030, driven by heavy-lift demand in shipbuilding and energy.

Page last updated on: