Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2019 - 2024 |

| Market Size (2026) | USD 5.80 Billion |

| Market Size (2031) | USD 7.95 Billion |

| Growth Rate (2026 - 2031) | 6.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Mobile Crane Market Analysis by Mordor Intelligence

The Asia-Pacific mobile crane market size reached USD 5.80 billion in 2026 and is projected to touch USD 7.95 billion by 2031, registering a 6.50% CAGR over the forecast period. Momentum stems from an unprecedented pipeline of infrastructure megaprojects, offshore wind arrays, urban high-rise programs, and a pronounced shift toward rental procurement. Chinese original equipment manufacturers (OEMs) continue to leverage domestic scale, yet demand in India, Indonesia, and Vietnam is rising faster as sovereign budgets favor metro rail, port upgrades, and renewable-energy hubs. Heavy-lift crawler cranes able to hoist 300 tons and beyond are seeing notable demand growth, pushed by petrochemical complexes and tall-turbine installations. At the same time, hybrid-drive and 5G-enabled tele-operation technology are trimming fuel bills, boosting uptime, and improving job-site safety. The Asia-Pacific mobile crane market is therefore evolving from a volume game to a value-driven contest where lifecycle cost, digital connectivity, and compliance with tightening emission rules decide purchase and rental awards.

Key Report Takeaways

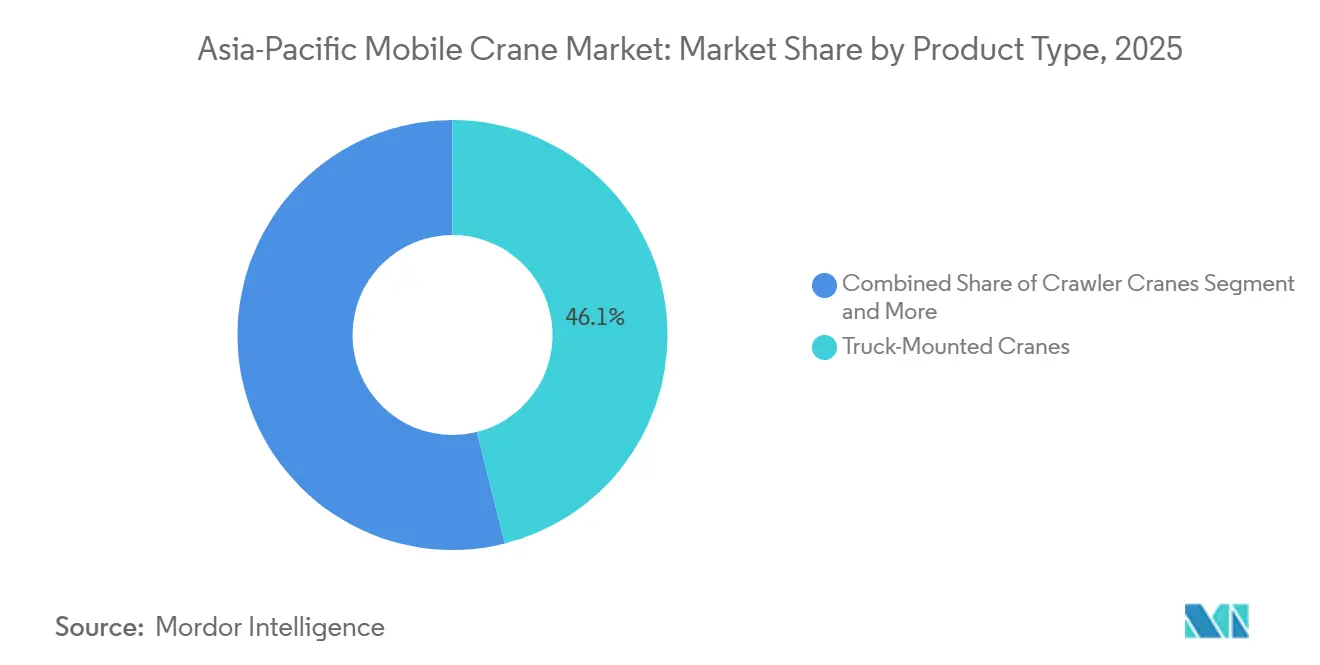

- By product type, truck-mounted units led with 46.13% of the Asia-Pacific mobile crane market share in 2025, while crawler cranes are forecast to expand at a 9.03% CAGR through 2031.

- By application, construction commanded a 56.22% share of the Asia-Pacific mobile crane market size in 2025, and marine and offshore lifting is advancing at an 8.12% CAGR to 2031.

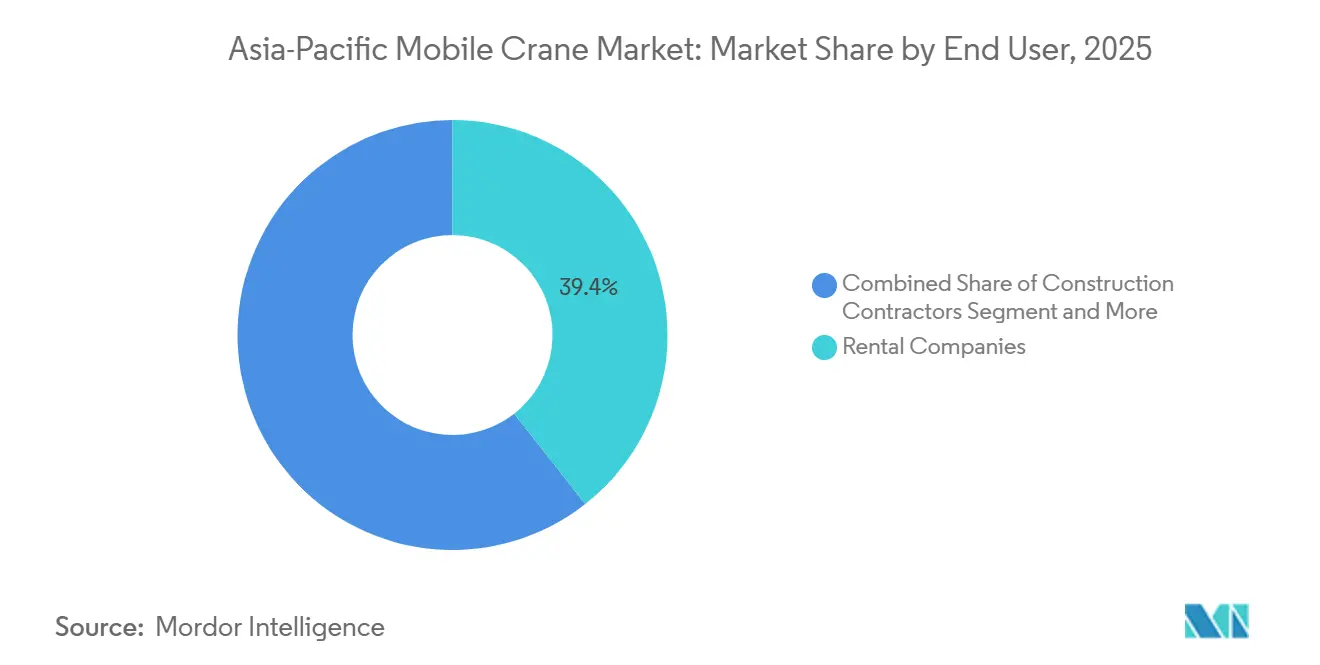

- By end user, rental companies accounted for 39.41% of 2025 spending, whereas government and municipal buyers recorded the highest projected CAGR at 7.85% through 2031.

- By lifting capacity, cranes below 50 tons held a 47.11% share in 2025, and the above-300-ton class is projected to grow at a 9.68% CAGR over 2026-2031.

- By country, China owned a 59.24% share in 2025, but India is forecast to post a 7.41% CAGR, the region’s fastest pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Mobile Crane Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Megaproject Spending Growth | +1.8% | China, India, Indonesia, Vietnam | Long term (≥ 4 years) |

| Renewable-Energy Lifting Demand | +1.5% | China, Taiwan, Japan, South Korea | Long term (≥ 4 years) |

| Accelerating Urban High-Rise Construction | +1.2% | China, India, Singapore, South Korea | Medium term (2-4 years) |

| Growth of Rental / Leasing Business | +1.0% | Singapore, Malaysia, India, Thailand | Medium term (2-4 years) |

| Push for Hybrid/E-Cranes | +0.6% | Japan, Singapore, South Korea | Medium term (2-4 years) |

| 5G-Enabled Tele-Operations | +0.4% | China, Japan, South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infrastructure Megaproject Spending Surge

Regional infrastructure investment climbed significantly in 2025 and is underpinned by multi-year rail, road, and port programs that keep crane utilization high. India’s National Infrastructure Pipeline earmarks a significant amount for metro corridors in tier-2 cities, where viaduct segments weighing over 200 tons demand heavy-duty crawler cranes[1]“National Infrastructure Pipeline,” Government of India, india.gov.in. China’s Belt and Road ventures continue to mobilize fleets across Southeast Asia; the Jakarta–Bandung high-speed rail alone used several mobile cranes during bridge works. Indonesia’s sovereign wealth fund allocated USD 20 billion in 2025, including port upgrades that require rough-terrain models able to maneuver on reclaimed land. These long-dated schemes anchor rental contracts and foster predictable fleet-replacement cycles.

Renewable-Energy Lifting Demand (Wind and Solar)

Contractors in Taiwan, Japan, and South Korea are reserving crawler cranes for 150-meter hub heights, as offshore wind capacity is expected to experience significant growth in the coming years. Taiwan’s 1,022 MW Hai Long 2 project specifies crawler units with corrosion-resistant hydraulics for monopile handling. Japan targets 10 GW of offshore wind by 2030 and 30-45 GW by 2040, prompting local OEMs to develop marine-rated variants obeying stringent wave-compensation rules [2]“Offshore Wind Outlook 2025,” International Energy Agency, iea.org. Large-scale solar parks in India and Australia also drive steady truck-mounted crane demand as modules and inverters arrive prefabricated. Renewable developers sign multi-year power-purchase agreements, enabling crane lessors to lock in revenues with lower default risk than speculative real-estate work.

Accelerating Urban High-Rise Construction

Asia-Pacific's urbanization rate is projected to grow significantly by 2030, with China and India contributing a substantial increase in urban residents. Tier-1 cities in China have approved numerous high-rise towers, each requiring heavy-duty cranes for steel erection. Residential launches in key Indian cities are witnessing notable growth, with developers increasingly adopting modular construction methods that rely on precision lifting. In Singapore, the approval of mixed-use towers comes with stringent sustainability certifications, encouraging contractors to utilize hybrid-drive cranes to minimize on-site emissions [3]“Green Mark Framework,” Building and Construction Authority Singapore, bca.gov.sg.

Growth of Rental / Leasing Business Models

End users are increasingly adopting asset-light strategies. Rental operators have been capturing a growing share of spending as contractors prioritize conserving working capital for bids instead of depreciating equipment. Tat Hong Holdings, the largest fleet owner in Southeast Asia, significantly improved utilization after expanding yards in Singapore and Malaysia. In China, rental penetration remains limited, with an oversupply leading to depressed pricing for aerial work platforms. This has prompted local firms to venture into India and Indonesia, where penetration is still relatively low. Meanwhile, Japan's rental segment is experiencing consolidation around regional champions that are scaling up maintenance and logistics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel Prices and Cost Inflation | -0.9% | China, India, South Korea, Japan | Short term (≤ 2 years) |

| Skilled-Operator Shortages and Gaps | -0.7% | India, Indonesia, Vietnam, Thailand | Medium term (2-4 years) |

| Port Congestion Delaying Supply | -0.5% | China, Singapore, Malaysia | Short term (≤ 2 years) |

| Insurance Costs in Typhoon Zones | -0.3% | Philippines, Taiwan, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Steel Prices and Cost Inflation

In early 2025, hot-rolled coil prices experienced a notable increase compared to the previous year. This rise was driven by supply constraints caused by Chinese output curbs and restrictions on nickel ore exports from Indonesia. Typically, higher steel costs lead to an increase in ex-factory crane prices, which puts pressure on margins for original equipment manufacturers (OEMs), particularly those with weaker brand power. Industry leaders like Liebherr and Manitowoc have addressed these challenges by localizing fabrication in India and China, while smaller firms face difficulties in managing freight volatility due to their limited scale. To address these risks, buyers are increasingly negotiating fixed-price contracts with longer validity periods, transferring the burden back to producers.

Skilled-Operator Shortages and Certification Gaps

As the workforce ages, India is experiencing a significant shortage of certified crane operators, leading to increased wages in metro projects. In Japan, the average age of crane operators is relatively high, with a notable shortfall anticipated unless training initiatives are expanded. Licensing regimes show stark contrasts: Singapore mandates a structured training and recertification process, while Indonesia's regulations differ across provinces. In Tokyo's high-rises, a trial of remote operation using advanced technology allows a single operator to manage multiple cranes, though safety codes have not yet caught up with these technological advancements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Crawler Cranes Gain on Heavy-Lift Projects

Crawler models are rising and are forecast to expand at a 9.03% CAGR through 2031, signaling demand for 300-ton-plus lifts on petrochemical plants and offshore wind sites. Truck-mounted cranes dominate mixed urban work because road mobility and quick setup outweigh brute capacity, holding a 46.13% share of the Asia-Pacific mobile crane market size in 2025. Sany’s 4,000-ton SCC40000A demonstrated single picks of 1,200-ton tank sections, validating the shift toward super-heavy duty. All-terrain cranes bridge highway speed and off-road access, suiting wind-farm access roads in India, while rough-terrain units fill low-infrastructure jobsites in Indonesia and the Philippines. Product innovation now targets hybrid drivelines, longer telescopic booms, and factory-installed telematics that let rental firms monitor usage hours in real time.

Hybrid-ready all-terrain cranes from Liebherr and Manitowoc cut diesel use significantly, qualifying for Green Mark incentives in Singapore. Tadano’s GR-1000XLL-4 extends 60 m without full outrigger deployment, permitting lifts in alleys surrounded by high-rise façades. Manufacturers are thus converging around flexible platforms that can shift from infrastructure pours to wind-farm nacelle lifts without major re-rigging. As a result, rental fleets lower capital expenditure per usable crane-hour, improving return metrics as utilization cycles tighten.

By Application: Marine and Offshore Outpace Traditional Construction

Construction still accounts for 56.22% of 2025 demand, yet marine and offshore tasks are scaling faster at an 8.12% CAGR because offshore wind and port dredging require specialized lifting. The Asia-Pacific mobile crane market benefits as Taiwan installs 1 GW-plus offshore parks where monopile foundations exceed 2,000 tons. Japan’s 10 GW offshore aim by 2030 nudges domestic OEMs to build corrosion-resistant coastal models. Mining and excavation stay relevant in Australia’s iron-ore pits and Indonesia’s nickel assets, where crawler cranes service haul-truck maintenance bays.

Power utilities hire truck-mounted units for grid-modernization, while shipping terminals favor mobile harbor cranes for container moves. Growth in marine lifting is helped by governments granting feed-in tariffs, letting contractors sign multi-season crane charters that secure cash flow. Industrial clients such as petrochemical complexes schedule shutdowns years ahead, letting crane providers plan fleet rotation. Shipping and port authorities now specify ISO 4309 rope inspection, raising equipment-quality thresholds and sidelining informal operators. These factors widen the compliance gap, enabling premium rental firms to raise rates.

By End User: Government Procurement Accelerates

Rental companies led 2025 spending at 39.41%, but public authorities will be the fastest riser at 7.85% CAGR through 2031 as sovereign plans fund metros, highways, and energy parks. The Asia-Pacific mobile crane market finds a dependable customer in state entities that issue multiyear build-operate contracts. In a bid to lighten their balance sheets, contractors are turning to outsourcing for lifting tasks. A 2024 survey conducted in Japan highlighted a strong preference among contractors for renting equipment for shorter-duration projects.

Industrial operators maintain captive fleets for turnarounds, yet even they supplement with leased super-heavy cranes during peak outages. Public procurement often imposes local-content quotas and low-emission rules, steering buyers toward hybrid models and suppliers with regional service depots. Fleet owners respond by retiring Tier 2 diesel cranes and importing Stage V-compliant units that command significantly higher daily rates. Government demand, therefore, reinforces the revenue streams of professional rental houses, while small single-owner fleets struggle to meet emission norms.

By Lifting Capacity: Super-Heavy Segment Surges

Cranes under 50 tons remain ubiquitous on house-building, utility, and light-industrial sites, holding 47.11% of revenue. However, the above-300-ton class is growing 9.68% annually, reflecting the rise of prefabricated modules and 10 MW wind turbines. Super-heavy units like Zoomlion’s 800-ton ZAT8000H allow single picks where dual cranes once worked, shrinking rigging cost and permitting sites with tight lay-down space.

In the 50-150 ton band, demand is steady for bridge girders and metro viaducts, while 151-300 ton cranes fill high-rise and refinery niches. Modern tenders mandate ISO 9927 safety audits, pushing owners to invest in higher-spec machines that survive rigorous inspection cycles, lifting overall product value inside the Asia-Pacific mobile crane market.

Geography Analysis

China commanded a 59.24% share in 2025 through an enormous domestic build program, but oversupply in certain rental segments pressures margins. Stage IV emission rules add cost yet favor top OEMs that can certify after-treatment systems. Offshore wind demand along Guangdong and Fujian shores lifts corrosion-proof crawler orders and sustains the Asia-Pacific mobile crane market despite cyclical real-estate soft spots. India’s 7.41% CAGR is anchored by its National Infrastructure Pipeline and a significant residential launch rebound in 2025. Operator shortages push wages higher, encouraging 5G-assisted remote control pilots.

Japan’s market is smaller yet technologically advanced. The country’s 10 GW offshore wind aim by 2030 forces OEMs to reinforce booms against salt spray. With an aging workforce, there is a growing focus on investing in autonomous positioning and remotely piloted systems. In Tokyo, advancements in 5G remote-control technology highlight a significant leap in safety and productivity. Meanwhile, as South Korea's semiconductor industry continues to expand, there is an increasing demand for heavy-cleanroom construction requiring vibration-controlled lifts. In Busan, shipyards are actively procuring telescopic units designed for deck lifts.

Rest of Asia-Pacific, covering Indonesia, Vietnam, Thailand, Malaysia, the Philippines, and Australia, enjoys nominal growth powered by port upgrades and mining. Indonesia’s Surabaya and Makassar port plan sustains rough-terrain purchases that can work on reclaimed fill. Australia’s iron-ore mines added several crawler cranes in 2024 to stretch mine life in the Pilbara. Vietnam’s North–South Expressway bids will absorb all-terrain and crawler models up to 300 tons through 2028. These markets lean on rental fleets due to capital constraints, reinforcing the cross-border equipment flow managed from Singapore hubs.

Competitive Landscape

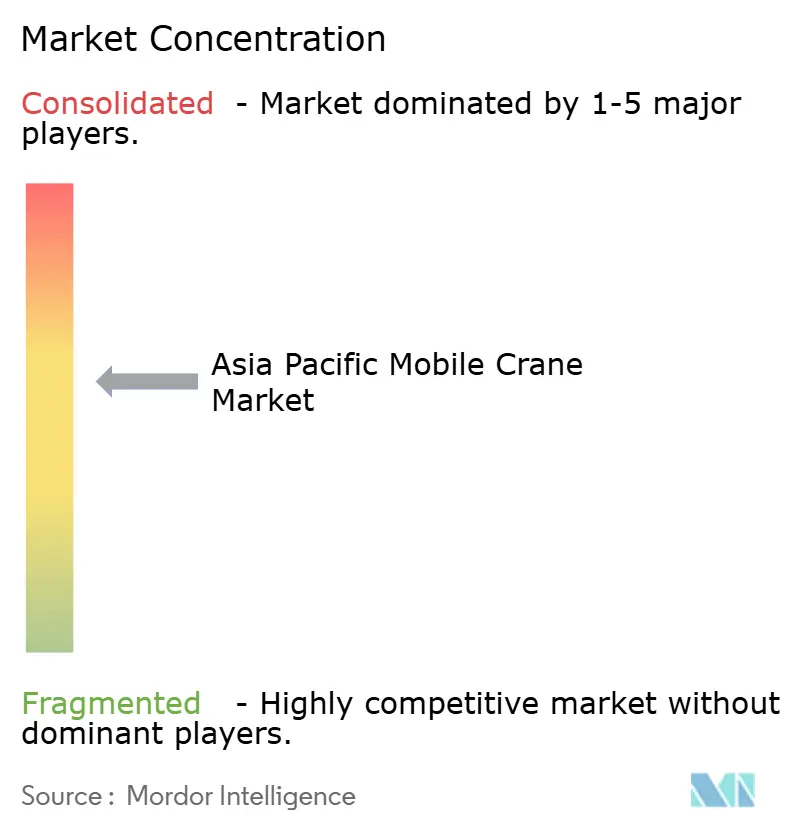

The Asia-Pacific mobile crane market is moderately concentrated, with the top five suppliers - Xuzhou Construction Machinery Group, Zoomlion, Sany, Liebherr, and Tadano - controlling a major share of revenue in 2025. Chinese firms compete on cost and domestic scale, whereas European and Japanese rivals stress hybrid drives, telematics, and lifetime service plans.

Zoomlion’s 5G tower-crane system, active on Shanghai high-rises since 2024, cuts unscheduled downtime and supports predictive maintenance. Liebherr’s 700-ton LTM 1650-8.1 hybrid all-terrain model reduces idle fuel consumption, helping contractors meet Green Mark rules in Singapore. Tat Hong Holdings consolidates rental share by acquiring smaller fleets and bundling rigging and logistics, erecting entry barriers for new entrants.

White-space potential lies in battery-electric cranes for noise-restricted urban sites and modular driveline kits that retrofit diesel units with hybrid modules. Niche challengers such as India’s Action Construction Equipment and Japan’s Furukawa UNIC focus on pick-and-carry and compact truck-mount designs. Patent filings for autonomous control and digital-twin lifting simulation are rising; Mitsui E&S unveiled its CARMS IoT suite in 2024 to optimize motion paths and shave cycle times. Compliance with ISO 4309 and ISO 9927 is baked into new government tenders, favoring brands owning dense service networks able to guarantee rope inspection and on-site audits.

Asia-Pacific Mobile Crane Industry Leaders

Xuzhou Construction Machinery Group Co., Ltd.

Zoomlion Heavy Industry Science & Technology Co., Ltd.

Sany Heavy Industry Co., Ltd.

Liebherr

Tadano Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Denzai ordered a second Liebherr LR12500-1.0 crawler crane with a ballast-wagon configuration using Cometto MSPE60-t self-propelled trailers, lifting capacity 2,500 tons, scheduled to arrive in March 2026 for offshore wind and power-plant projects.

- March 2025: XCMG delivered certified pre-owned XGC85 and XGC55 crawler cranes to support infrastructure jobs in Southeast Asia, reinforcing the circular-economy push.

- March 2025: Tadano unveiled the AC 5.250L-2 all-terrain crane with a 79 m boom aimed at urban lifts that need both reach and compact road dimensions.

- September 2024: Zoomlion opened its Hoisting Machinery Park and launched a record 4,000-ton all-terrain crane capable of installing wind turbines at 185 m hub height.

Asia-Pacific Mobile Crane Market Report Scope

The scope of the report includes segmentation by product type (truck-mounted cranes, trailer-mounted cranes, crawler cranes, all-terrain cranes, rough-terrain cranes, others), application (construction, mining and excavation, industrial applications, marine and offshore, utility, and shipping and port building), end user (rental companies, construction contractors, government and municipalities, and industrial operators), and lifting capacity (below 50 tons, 50-150 tons, 151-300 tons, and above 300 tons). The analysis also covers country-level segmentation, including China, India, Japan, South Korea, and the Rest of the Asia-Pacific. Market size and growth forecasts are presented by value in USD and volume in units.

By Product Type

| Truck-Mounted Cranes |

| Trailer-Mounted Cranes |

| Crawler Cranes |

| All-Terrain Cranes |

| Rough-Terrain Cranes |

| Others |

By Application

| Construction |

| Mining and Excavation |

| Industrial Applications |

| Marine and Offshore |

| Utility |

| Shipping and Port Building |

By End User

| Rental Companies |

| Construction Contractors |

| Government and Municipalities |

| Industrial Operators |

By Lifting Capacity

| Below 50 Tons |

| 50-150 Tons |

| 151-300 Tons |

| Above 300 Tons |

By Country

| China |

| India |

| Japan |

| South Korea |

| Rest of Asia-Pacific |

| By Product Type | Truck-Mounted Cranes |

| Trailer-Mounted Cranes | |

| Crawler Cranes | |

| All-Terrain Cranes | |

| Rough-Terrain Cranes | |

| Others | |

| By Application | Construction |

| Mining and Excavation | |

| Industrial Applications | |

| Marine and Offshore | |

| Utility | |

| Shipping and Port Building | |

| By End User | Rental Companies |

| Construction Contractors | |

| Government and Municipalities | |

| Industrial Operators | |

| By Lifting Capacity | Below 50 Tons |

| 50-150 Tons | |

| 151-300 Tons | |

| Above 300 Tons | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large will crane demand be in Asia-Pacific by 2031?

The Asia-Pacific mobile crane market size is forecast to reach USD 7.95 billion by 2031, growing at a 6.50% CAGR from 2026 to 2031.

Which capacity class is expanding fastest?

Cranes above 300 tons are projected to grow at a 9.68% CAGR as offshore wind and petrochemical projects need heavier lifts.

What share does rental procurement hold today?

Rental companies accounted for 39.41% of 2025 spending and continue to gain ground as contractors pursue asset-light models.

Why are crawler cranes gaining popularity?

Crawler units offer stability on soft ground and lift 300 tons or more, suiting petrochemical, offshore wind, and mining applications that are expanding across the region.

Which country will see the quickest growth?

India leads with a projected 7.41% CAGR through 2031, fueled by its National Infrastructure Pipeline and rapid metro expansion.

Page last updated on: