Aerial Work Platform Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

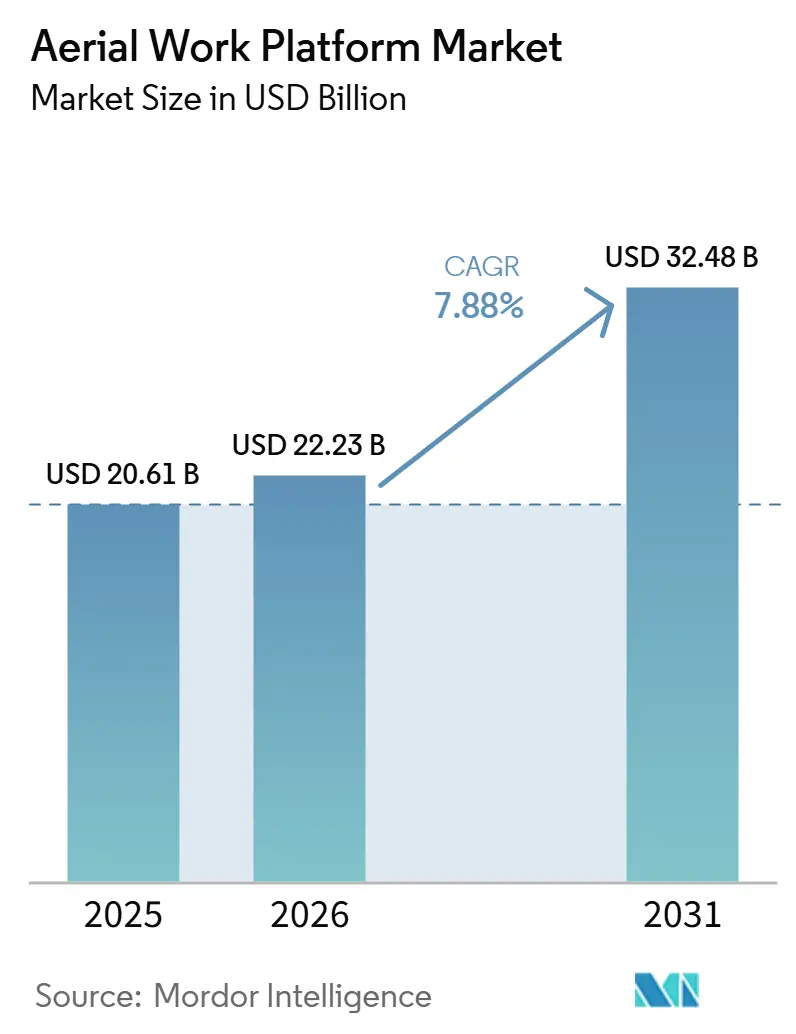

| Market Size (2026) | USD 22.23 Billion |

| Market Size (2031) | USD 32.48 Billion |

| Growth Rate (2026 - 2031) | 7.88% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerial Work Platform Market Analysis by Mordor Intelligence

The Aerial Work Platform Market size is expected to grow from USD 20.61 billion in 2025 to USD 22.23 billion in 2026, and is forecast to reach USD 32.48 billion by 2031, at a 7.88% CAGR over 2026-2031. Rising rental penetration, stricter job-site safety regulations, and mega-project construction pipelines are the prime forces sustaining this trajectory. Demand also benefits from the rapid verticalisation of warehouses; Amazon operates multiple mega-warehouses exceeding 2 million ft² and has more underway, many of which incorporate multiple mezzanine levels exceeding 32 ft. Technology upgrades, especially telematics-enabled diagnostics, are now standard purchase criteria, while hybrid and full-electric drivetrains are gaining share as contractors prepare for low-emission jobsites. Counter-pressures include higher liability insurance premiums due to an annual average of 26 aerial-lift fatalities in the United States construction industry, and lingering battery-metal supply constraints.

Key Report Takeaways

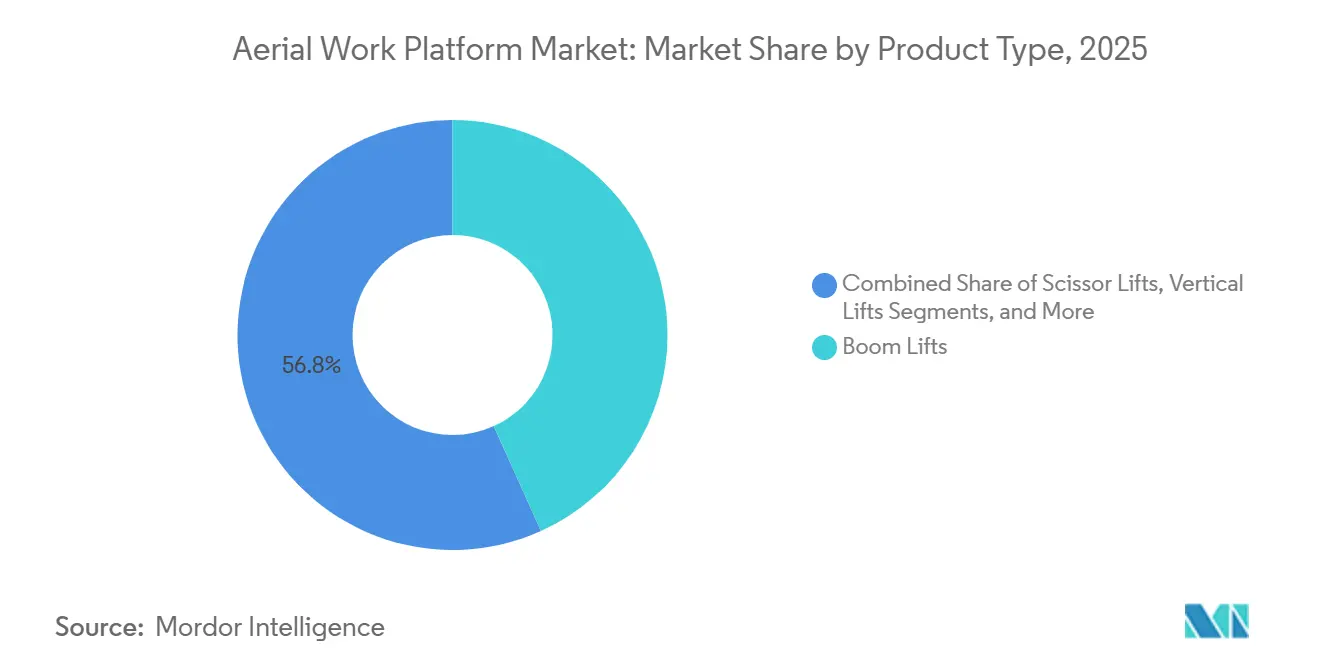

- By product type, boom lifts led with a 43.24% revenue share in 2025; vertical lifts are projected to grow at an 8.84% CAGR through 2031.

- By propulsion type, internal-combustion units retained 61.74% of the aerial work platforms market share in 2025, whereas electric models are forecast to post a 10.26% CAGR through 2031.

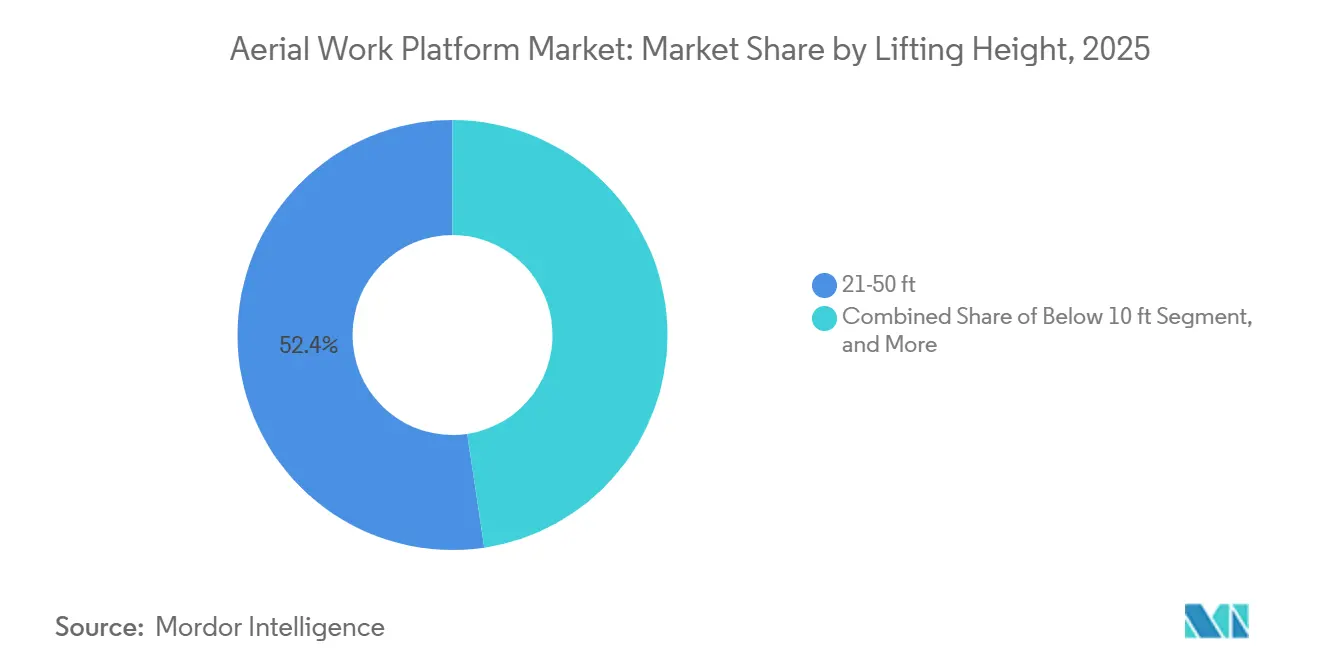

- By lifting height, the 21-50 ft band captured 52.36% of the aerial work platforms market size in 2025, while the above 100 ft segment is expected to grow at a 9.28% CAGR to 2031.

- By application, construction accounted for 57.28% of the aerial work platforms market in 2025; logistics and transportation is the fastest-growing use case, with an 8.78% CAGR through 2031.

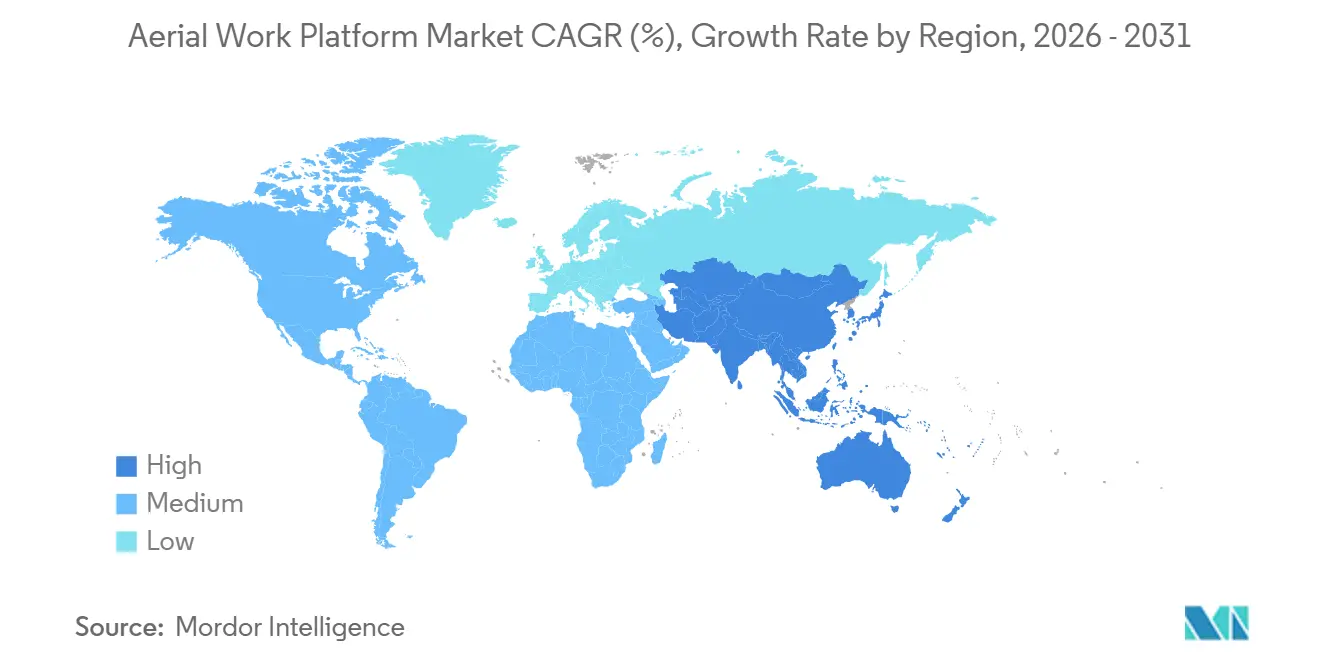

- By geography, North America commanded 34.76% of 2025 revenue, while Asia-Pacific is set to register the highest regional CAGR at 9.27% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aerial Work Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Infrastructure and Commercial Construction Boom | +1.8% | North America; Asia-Pacific | Medium term (2-4 years) |

| Growing Rental Penetration of AWPs | +1.5% | North America; Europe; Asia-Pacific | Long term (≥ 4 years) |

| Rapid Warehouse Automation in E-Commerce Logistics | +1.3% | Developed markets worldwide | Medium term (2-4 years) |

| Stricter Worker-Safety Regulations | +1.2% | North America; Europe | Short term (≤ 2 years) |

| Telematics-Enabled Predictive Maintenance | +0.8% | Initially North America; expanding globally | Long term (≥ 4 years) |

| Rising Use in Film/Media Production and Events | +0.4% | Major entertainment hubs | Short term (≤ 2 years |

| Source: Mordor Intelligence | |||

Global Infrastructure and Commercial Construction Boom

Mega-projects backed by infrastructure stimulus in the United States, Canada, and India inject sustained demand for fleet replacement into the aerial work platforms market[1]“US Infrastructure Act Drives Equipment Demand,”, International Rental News Editors, internationalrentalnews.com. The U.S. Infrastructure Investment and Jobs Act alone has unlocked multi-year funding that covers highways, bridges, and utility upgrades. Heightened structural complexity—data centers, gigafactories, and multi-story industrial plants—requires access equipment that combines long outreach with compact chassis footprints. Manufacturers are therefore debuting higher-capacity articulating booms fitted with secondary guarding and real-time load-sensing modules that comply with ANSI A92 safe-use rules. Rental companies pass these feature upgrades through to end users, and utilization rates have remained resilient even as broader construction spend ebbs in some sub-segments.

Stricter Worker-Safety Regulations

OSHA standards 1926.453 and 1910.67, and the 2018 ANSI A92 overhaul, require employers to provide machine-specific training, fall-arrest equipment, and documented inspections for all mobile elevating work platforms [2]“Standards 1926.453 & 1910.67,”, OSHA, osha.gov. The rule set has effectively raised the entry cost for older or uncertified units, steering contractors toward newer fleets that embed tilt alarms, platform load sensors, and automated descent controls. Compliance audits have become more frequent, and project owners increasingly pre-qualify subcontractors based on MEWP certification. Equipment makers answer this with innovations such as Haulotte’s FASTN lanyard-anchorage detection, which secured Best Safety Innovation honors in 2024. The ongoing safety culture shift thus reinforces premium pricing power for devices with integrated compliance features.

Telematics-Enabled Predictive Maintenance and Remote Diagnostics

IoT platforms such as JLG’s ClearSky Smart Fleet capture operating hours, battery voltage, and shock events in real time, giving fleet owners the data to schedule service before a fault triggers downtime. European rental firm NH Rental reported a threefold expansion of its fleet while cutting emergency call-outs once remote monitoring went live. Predictive algorithms can now flag declining battery State-of-Charge trends that jeopardize shift completion, enabling pre-emptive swaps. Such capabilities have become a standard requirement in tenders among top-tier contractors because time lost to unplanned repairs multiplies across interdependent project tasks. As a result, telematics helps equipment suppliers close premium-priced deals and positions them for ancillary subscription revenues tied to analytics dashboards.

Rising Use in Film/Media Production and Event Staging

Content streaming growth has pushed studios to erect new sound stages in Atlanta, Los Angeles, and Seoul, each requiring aerial lifts for lighting grid installation, set construction, and rigging adjustments. Event promoters equally rely on compact articulating booms to position LED walls and line-array speakers inside arenas during short venue turnarounds. Vendors such as Riwal now offer purpose-configured rental packages that bundle low-profile tires, blackout-compliant paint, and extended-duty battery packs suited to indoor filming environments. Although the volume remains niche, the segment provides year-round utilization, cushioning seasonal swings in construction activity, and sharpening overall fleet yield.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Costs Vs. Conventional Access Methods | -1.1% | Price-sensitive markets worldwide | Medium term (2-4 years) |

| Availability of Low-Cost Used Equipment and Substitutes | -0.9% | Mature markets | Short term (≤ 2 years) |

| Escalating Liability-Insurance Costs After Accidents | -0.8% | North America; Europe | Medium term (2-4 years |

| Battery-Metals Supply Bottlenecks for Electric Awps | -0.7% | Asia-Pacific most exposed | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Costs vs. Conventional Access Methods

List prices for new mid-range scissor lifts rose nearly 30% between 2020 and 2024 as steel and electronics costs spiked, widening the gap against scaffolding or ladder alternatives. Smaller trades, therefore, struggle to justify ownership, opting instead for short-term rentals or reverting to labor-intensive solutions for lower-height jobs. While automation and safety savings partly offset upfront outlays. Manufacturers are responding with modular components that reduce transport costs and multifunctional accessories, such as pipe racks or panel cradles, that increase the utilization of single machines.

Availability of Low-Cost Used Equipment and Substitutes

Auction volumes for five- to seven-year-old AWPs jumped after OEM supply shortages eased in 2023, dragging resale values for high-hour units down by double digits. Buyers in Latin America and Southeast Asia often favor these discounted imports over new builds that must comply with the latest-generation electronics and emissions packages. Drone-based façade inspections and mast-climbing work platforms also nibble at the aerial work platforms market, especially for straight-down visual or material-hoisting tasks that do not require full operator elevation. The influx of refurb specialists further intensifies pricing pressure on entry-level new models

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Boom Lifts Shape Market Transformation

Boom lifts held the largest share, at 43.24%, of the aerial work platforms market in 2025, a position they are projected to defend as multi-trade versatility remains paramount on congested job sites. Articulating models integrate outreach angles that enable operators to clear steel structures and HVAC ductwork without repositioning base vehicles, boosting cycle productivity. Haulotte’s HA20 RTJ PRO, launched in 2024, is emblematic of the category’s pivot toward performance metrics such as faster lift speeds and load-sensing chassis that enable full-height operation at full load capacity[3]“Haulotte Showcases HA20 RTJ PRO,”, Bauma CHINA Organisers, bauma-china.com. Scissor lifts dominate multi-worker indoor fit-out tasks, but steady commoditization keeps their price points under downward pressure. Vertical mast lifts are on track for the fastest 8.84% CAGR, driven by warehouse operators who value their zero-turn radii. Trailer-mounted booms remain relevant for utilities and telecoms maintenance, whereas self-propelled units would exceed weight limits in rural areas and breach road regulations.

Over time, manufacturers standardize telematics hardware across product families, enabling rental companies to consolidate boom-lift and scissor performance data into a single dashboard. Hybrid powertrains with engine-off electric creep modes are migrating from high-end booms into midsize scissors, aligning with city-center emissions bylaws. Because boom-lift resale values remain highest among all categories, fleet owners allocate disproportionate capital toward these units, reinforcing their primacy in the aerial work platforms market.

By Propulsion Type: Electric Transition Accelerates

Internal-combustion engines still capture 61.74% market share in the aerial work platforms market in 2025, yet electric variants capture an incremental share faster than any other propulsion cohort. The aerial work platforms market size for electric models is expanding at a double-digit 10.26% CAGR as urban ordinances phase out diesel on redevelopment sites. Lithium-ion packs now deliver full-shift autonomy for a 40-ft scissor at an energy cost about 30% lower than propane equivalents when charged overnight on the grid. Hybrid configurations provide bridge solutions in remote applications lacking charging infrastructure, combining downsized engines with regenerative braking to extend runtime.

OEMs face unavoidable exposure to battery-metal price surges, but many hedge by signing cathode-material contracts alongside automakers. On-site fast-charge stations are being trialed on United Kingdom. HS2 rail lots and will likely cascade into North American highways funded by federal infrastructure grants. Safety codes are also evolving; UL 2580 fire-resistance certification has become a purchasing criterion for rental majors following several high-profile lithium-pack fires. Consequently, electric adoption will reinforce the premium tier of the aerial work platforms market even as absolute battery costs gradually trend lower post-2027.

By Lifting Height: Mid-Range Dominance Continues

With 52.36% revenue share in 2025, the 21-50 ft class remains the workhorse zone of the aerial work platforms market. These heights align with most tilt-wall panel erection, drywall hanging, and racking installation tasks common to large warehouses and commercial builds. Demand will remain robust as e-commerce giants intensify mezzanine-heavy designs that require frequent mid-level access. Above-100-ft giants are forecast to log a 9.28% CAGR at the upper end as data-center cooling-tower construction and renewable-energy stack assembly proliferate. OEMs responded by adding envelope-control algorithms that automatically modulate boom speed near platform limits, reducing tip-load oscillation.

Conversely, sub-20-ft personnel lifts are targeted for industrial plants needing maneuverability under pipe racks. Although absolute volumes here are lower, adoption accelerates when safety managers outlaw ladders for tasks exceeding 15 ft. Meanwhile, the 51-100 ft tranche sees steady uptake among transmission-line contractors who must navigate terrain undulations while maintaining outreach. Height-specific design tweaks—such as secondary booms on 135-ft units—underscore how engineering innovation tailors performance envelopes to the widening use cases across the aerial work platforms market.

By Application: Construction Leads, Logistics Accelerates

Construction accounts for 57.28% of the aerial work platforms market share in 2025, driven by large-scale public infrastructure and private commercial projects, which will continue to anchor the market. Equipment utilization in this segment spikes when interior finishing overlaps with exterior façade work, demanding concurrent deployment of multiple platform types. Contractor preference for rental is particularly acute here, mitigating cap-ex risk across multi-phase timelines.

Logistics and transportation are the star growth engine with an 8.78% CAGR, propelled by fulfillment-center retrofits and greenfield builds that embed robotic shuttles and high-bay storage. The aerial work platforms market size for logistics platforms is expected to grow rapidly as omnichannel retailers replicate the Amazon mega-warehouse model worldwide. Utilities still leverage insulated booms for live-line maintenance, while film-and-events specialists tap compact articulating lifts for LED wall rigging. Manufacturing modernization in sectors such as food-processing further diversifies demand, illustrating how AWPs progress from niche construction tools to indispensable cross-industry assets

Geography Analysis

North America commanded 34.76% market share in the aerial work platforms market in 2025. Continuous replacement cycles driven by ANSI A92 compliance and large federal funding allocations sustain demand for new telematics-equipped fleets. Companies like United Rentals evidence the scale underpinning this geographic leadership. Canadian growth centers on resource-sector expansion and retrofit mandates in urban cores, whereas Mexico’s near-shoring boom stimulates purchases of mid-height electrics for automotive and electronics plants.

Asia-Pacific is on track to achieve the fastest CAGR at 9.27%, supported by rapid urbanization and industrial diversification. While China’s broader construction equipment market shrank in 2023, stabilization began in mid-2024, and policy credit easing is expected to rekindle AWP orders for metro projects and data-center corridors. The Indian market is growing through the expansion of mega rail and airport projects. Southeast Asian economies—Indonesia, Vietnam, and the Philippines—are emerging hotspots as regional e-commerce players replicate multi-level fulfillment hubs, fuelling appetite for 30- to 40-ft electrics.

Europe remains a mature but innovation-oriented market. Germany and Finland saw double-digit fleet additions in 2023, but southern states such as Spain wrestled with fiscal constraints, producing uneven recovery patterns. Stricter Stage V emissions standards accelerate replacement of diesel scissors with hybrid or fully electric alternatives, particularly in the Netherlands and Scandinavia, where zero-local-emission mandates apply to city-center projects. The Middle East is ramping up ultra-high-reach needs for giga-projects across Saudi Arabia’s NEOM zones. Africa and South America remain comparatively nascent, yet gain incremental imports of used units as infrastructure financing improves. Together, these regional nuances underline the non-uniform but overall upward trajectory of the aerial work platforms market.

Competitive Landscape

The aerial work platforms market is moderately fragmented but trending toward consolidation, as leaders acquire niche specialists to broaden their portfolios and geographic footprints. JLG’s 2024 acquisitions of Hinowa and AUSA extend its reach into track-mounted spider lifts and dumpers, respectively, illustrating a strategy of product-adjacency expansion. Haulotte continues to refresh its range with electric boom introductions, while Genie invests heavily in sensor-based secondary guarding and machine vision for collision avoidance. Regional manufacturers in China and Turkey add price competition at the low-spec end, yet struggle to match the global after-sales networks of incumbents.

Channel power largely resides with rental houses whose bulk-buy contracts influence equipment specification trends. Those firms, in turn, prioritize units that integrate open-architecture telematics so fleet data can sync with enterprise asset-management software. Subscription-based analytics unlock new recurring-revenue layers for OEMs; for example, predictive service alerts reduce parts inventory levels at depots, boosting ROI. Competition also intensifies around sustainability narratives: Haulotte joined a hydrogen equipment consortium in 2024, and Genie is piloting non-combustion, cobalt-free lithium packs. Patent filings clustered around platform-load calibration and autonomous driving hint at future semi-robotic lifts capable of self-positioning.

Despite competitive churn, barriers to entry remain high due to stringent design-safety certification and global support-network requirements. Smaller challengers, therefore, often partner with large distributors rather than pursue standalone international expansion. Looking ahead, white-space opportunities in renewable-energy erection, modular construction, and hyperscale data-center builds will reward suppliers offering tailored reach-and-capacity combinations. Overall, price rivalry co-exists with technology differentiation, positioning the sector for sustainable yet disciplined growth.

Aerial Work Platform Industry Leaders

JLG Industries (Oshkosh)

Genie – Terex Corporation

Haulotte Group

Skyjack – Linamar Corporation

Zhejiang Dingli Machinery

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: At Bauma, Faresin Industries unveiled the FS6.26 telehandler, touting it as the most compact and nimble addition to its range. The FS6.26 replaces the well-received FR6.26, which saw global sales surpass 2,000 units. Tailored for the evolving needs of today's construction, rental, and municipal sectors, the FS6.26 aims to set new standards in agility and performance.

- February 2025: Manitou has unveiled two new construction telehandler models, the MTA 1242 MAX and MTA 1242 MAX E74. Designed with increased power, stability, and efficiency, these models cater specifically to the needs of rental businesses and construction fleet managers. They boast enhanced lifting capacities and simplified maintenance.

- September 2024: After acquiring Hinowa, JLG swiftly moved to acquire AUSA. JLG seeks to expand its offerings in core and adjacent markets by partnering with these two trusted equipment firms. These markets encompass construction, material handling, agriculture, landscaping, and specialized equipment applications.

Global Aerial Work Platform Market Report Scope

| Boom Lifts |

| Scissor Lifts |

| Vertical Lifts |

| Trailer-Mounted Lifts |

| Internal-Combustion Engine (ICE) |

| Electric |

| Hybrid |

| Below 20 ft |

| 21 - 50 ft |

| 51 - 100 ft |

| Above 100 ft |

| Construction |

| Utilities |

| Logistics and Transportation |

| Manufacturing |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product | Boom Lifts | |

| Scissor Lifts | ||

| Vertical Lifts | ||

| Trailer-Mounted Lifts | ||

| By Propulsion Type | Internal-Combustion Engine (ICE) | |

| Electric | ||

| Hybrid | ||

| By Lifting Height | Below 20 ft | |

| 21 - 50 ft | ||

| 51 - 100 ft | ||

| Above 100 ft | ||

| By Application | Construction | |

| Utilities | ||

| Logistics and Transportation | ||

| Manufacturing | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the aerial work platforms market by 2031?

The market is forecast to reach USD 32.48 billion by 2031, reflecting a 7.88% CAGR from 2026.

Which product category currently leads the aerial work platforms market?

Boom lifts dominate, holding 43.24% of 2025 revenue due to their outreach versatility.

Why are electric aerial work platforms gaining traction?

Cities are mandating low-emission jobsites, and lithium-ion units cut energy costs by about 30% against propane models while delivering full-shift runtime.

How are telematics systems changing fleet management?

Platforms such as ClearSky Smart Fleet provide real-time diagnostics and predictive maintenance, reducing unplanned downtime and boosting utilization rates.

What safety regulations most affect the aerial work platforms market?

OSHA standards 1926.453 and 1910.67 in the U.S. and the ANSI A92 suite require machine-specific training and fall-protection systems, steering demand toward newer compliant equipment.

Page last updated on: