Electric Coolant Pump Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

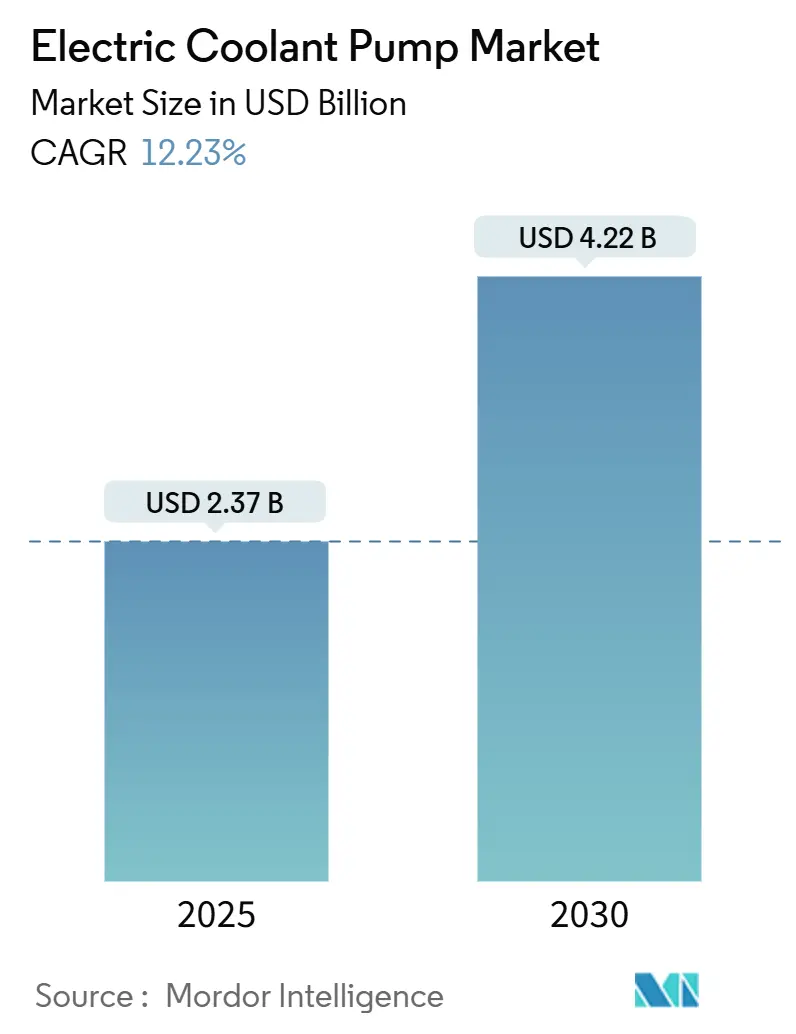

| Market Size (2025) | USD 2.37 Billion |

| Market Size (2030) | USD 4.22 Billion |

| Growth Rate (2025 - 2030) | 12.23% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

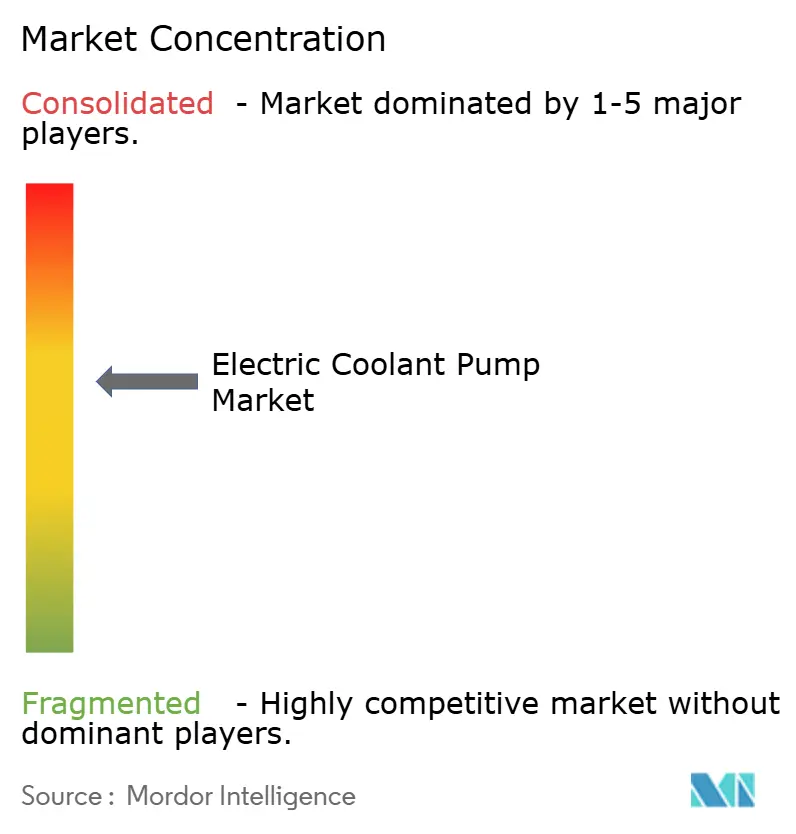

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Coolant Pump Market Analysis by Mordor Intelligence

The electric coolant pump market size is USD 2.37 billion in 2025 and is forecasted to reach USD 4.22 billion by 2030, advancing at a 12.23% CAGR. Rising electric-powertrain penetration, stricter emissions rules, and the need for precise battery temperature control collectively underpin this rapid expansion. Electric pumps decouple coolant flow from engine speed, unlocking energy-saving algorithms that help automakers meet carbon-reduction targets while improving cabin comfort in start-stop traffic. Multiplying coolant loops in battery electric vehicles (BEVs) elevate the number of pumps per vehicle, further boosting unit demand. The market also benefits from 48 V auxiliary architectures that reduce wiring mass and enable high-flow, low-current pump operation. Moderate industry concentration allows mid-tier suppliers to carve niches in integrated thermal modules, while raw-material cost volatility and service-skill gaps temper near-term adoption.

Key Report Takeaways

- By pump type, horizontal designs held 48.59% of the electric coolant pump market share in 2024; vertical pumps are projected to expand at a 13.13% CAGR through 2030.

- By voltage, 12 V units accounted for 64.79% of the electric coolant pump market size in 2024, whereas the 48 V+ segment is forecasted to rise at a 22.52% CAGR to 2030.

- By vehicle type, passenger cars led with 61.96% of the electric coolant pump market share in 2024, while medium and heavy commercial vehicles are projected to advance at a 14.67% CAGR over the same period.

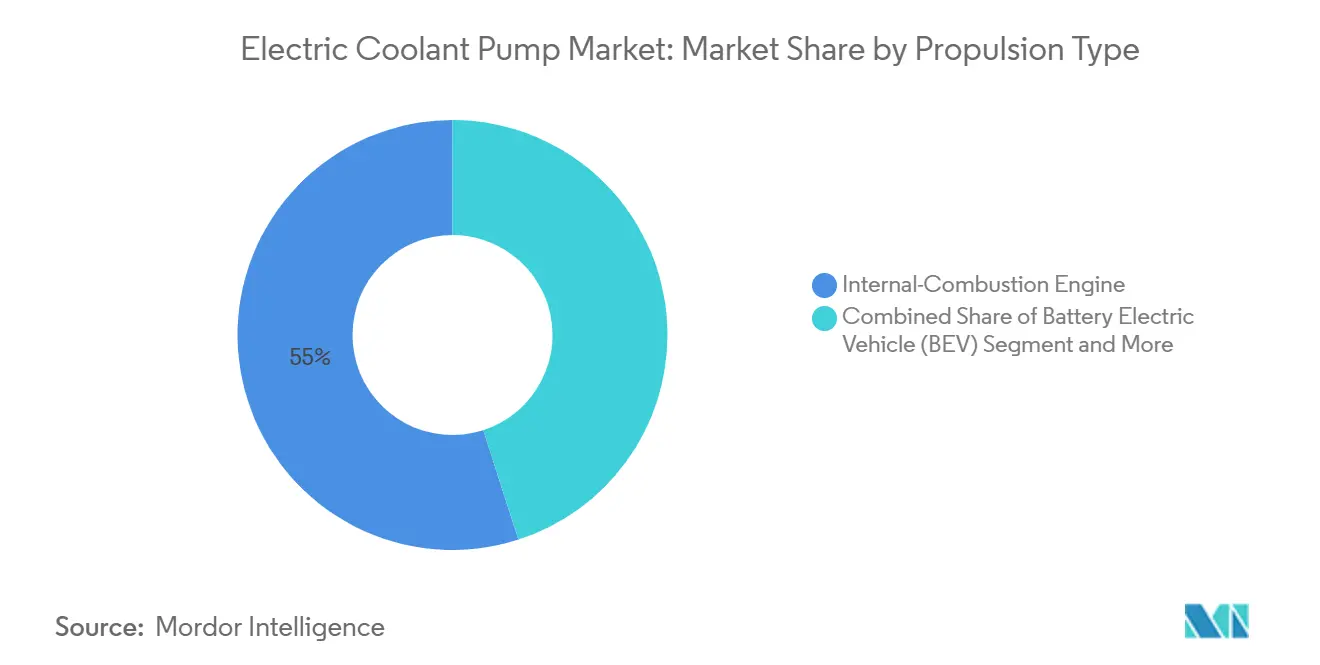

- By propulsion type, internal-combustion platforms commanded 54.97% of the electric coolant pump market share in 2024; BEVs are projected to record the highest projected CAGR at 24.36% through 2030.

- By sales channel, OEMs dominated 73.39% of the electric coolant pump market share in 2024, and expected to grow at 13.06% CAGR to 2030.

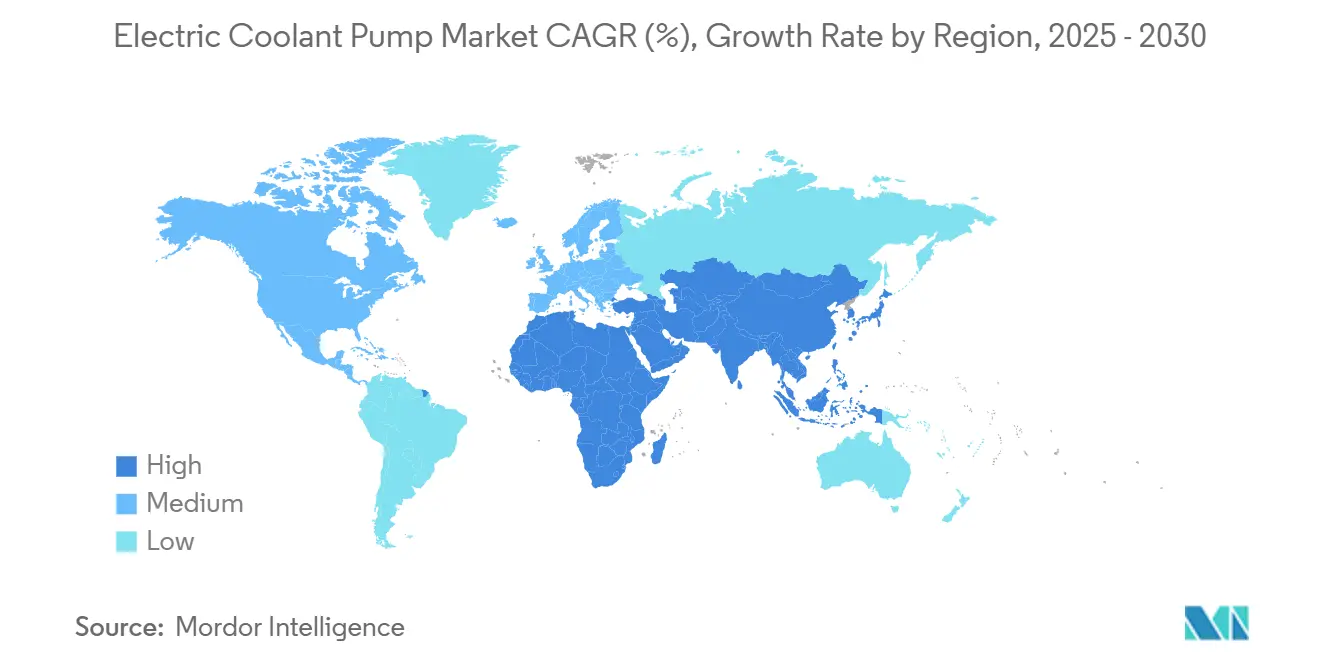

- By geography, Asia-Pacific captured 47.38% of the electric coolant pump market share in 2024, while, the Middle East and Africa is projected to record the fastest CAGR of 13.58% through 2030.

Global Electric Coolant Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Production Volumes | +2.5% | Global, with APAC leadership and MEA acceleration | Medium term (2-4 years) |

| Fuel-Efficiency Mandates | +2.2% | Europe and North America core, expanding to APAC | Long term (≥ 4 years) |

| Integrated "Super-Bottle" Thermal Modules | +2.1% | Global, early adoption in premium segments | Medium term (2-4 years) |

| Lower-Vibration Auxiliaries | +1.9% | Global, premium and luxury segments leading | Short term (≤ 2 years) |

| 48 V Mild-Hybrid Buses and Trucks | +1.7% | Europe and China core, India emerging opportunity | Medium term (2-4 years) |

| Rising Replacement Cycles | +1.3% | Global commercial vehicle segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Ramp-Up of Global EV Production

Surging EV output multiplies thermal-management complexity as battery capacities rise and ultrafast charging accelerates heat generation. Automakers now specify two or more electric pumps per BEV, handling battery conditioning, power-electronics cooling, and heat-pump loops, to safeguard component life and vehicle range. Independent pump control trims auxiliary energy draw, improving overall drive-cycle efficiency. Major Asian OEMs localize pump sourcing to mitigate logistics risk, while North American startups favor modular pump assemblies that simplify plant integration. The scale effects across these programs underpin the market’s double-digit growth trajectory.

Emissions-Focused Fuel-Efficiency Mandates

Regulators cap tailpipe CO₂ and tighten particulate limits, pushing automakers to shrink parasitic losses from belt-driven accessories. U.S. greenhouse-gas standards now credit variable-speed pumps that cut idle energy consumption, spurring OEM retrofit programs for next-generation platforms[1]“Final Rule: Greenhouse Gas Emissions Standards for Model Years 2027-2032 Light-Duty Vehicles,” Environmental Protection Agency, epa.gov. In Europe, Euro 7 legislation drives the same shift, with fleet-average penalties high enough to justify the component cost premium. Emerging APAC markets emulate these rules, widening the addressable customer base.

Adoption of Integrated “Super-Bottle” Thermal Modules

Automotive thermal management evolves toward consolidated "super-bottle" architectures that integrate coolant reservoirs, pumps, valves, and control electronics into single assemblies, reducing packaging complexity and improving serviceability. Tier-1s co-develop these modules with OEM platform teams, embedding software that dynamically reroutes coolant to pre-warm batteries or scavenge inverter heat for cabin comfort. The trend accelerates the pump value content per vehicle and rewards firms that offer compact, multi-orientation designs.

OEM Demand for Quieter, Lower-Vibration Auxiliaries

Premium vehicle segments drive demand for electric coolant pumps as NVH (noise, vibration, harshness) requirements intensify, particularly in luxury EVs where engine noise no longer masks auxiliary component sounds. Accordingly, premium brands specify acoustic targets under 35 dB(A) at 1 m. Brushless pump motors, resin-encapsulated stators, and rubber-isolated mounts help meet these metrics while improving reliability. Some OEMs also integrate active noise-cancellation algorithms that predict pump pulsations and invert sound waves via door speakers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Cost Volatility | -1.7% | Global, with supply chain concentration in APAC | Short term (≤ 2 years) |

| Cooling-Loop Complexity | -1.5% | Global, acute in emerging markets | Medium term (2-4 years) |

| Reliability Concerns | -0.9% | Global aftermarket, emerging market focus | Long term (≥ 4 years) |

| Pending PFAS Bans | -0.7% | North America & Europe regulatory focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Automotive Raw-Material Costs

Raw material price instability creates margin pressure and supply chain disruption risks for electric coolant pump manufacturers, particularly given copper's central role in motor windings and electronic control systems. Copper, aluminum, and rare-earth magnets face supply tightness as electrification accelerates. Commodity analysts project copper demand to outstrip supply through the decade, driving price spikes that compress pump-maker margins[2]“The Copper Opportunity in the Energy Transition,” BHP, bhp.com. Suppliers hedge exposure via dual-sourcing and lightweight designs that cut conductor mass, yet sudden tariff shifts keep cost risks elevated.

Cooling-Loop Complexity vs. Service-Skill Gaps

Electric vehicle thermal management systems introduce multi-circuit complexity that exceeds traditional automotive technician training, creating service bottlenecks and reliability concerns in aftermarket channels. Modern EVs incorporate up to four independent coolant circuits versus one in legacy ICE models. Workshop technicians require high-voltage safety training and specialized diagnostic tools, but such programs remain scarce in many emerging markets. Delayed repairs erode consumer confidence and may prompt OEMs to limit certain pump technologies to regions with adequate service infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Horizontal Designs Lead Integration

Horizontal pumps held a 48.59% of the electric coolant pump market share in 2024 due to their low-profile geometry, which fits neatly beneath ICE intake manifolds and within hybrid powertrain cradles. OEM engineers appreciate the simplified air-bleeding procedure that horizontal impellers enable, reducing assembly time and warranty claims. Conversely, vertical pumps are gaining traction on skateboard EV platforms where dedicated thermal trays favor upright mounting that eases hose routing. Several tier-1 suppliers now offer reversible-flow vertical models allowing bidirectional coolant movement for battery pre-conditioning.

Horizontal pumps will maintain leadership through mid-decade, but vertical units are projected to grow at 13.13% CAGR as integrated thermal modules adopt stacked layouts. These modules install pumps, valves, and sensors in a vertical stack, shortening coolant pathways and enabling gravity-assisted degassing. Advancements in polymer composite housings improve vertical-pump heat tolerance, while sensor-fusion control boards monitor vibration to predict bearing wear. Suppliers investing in dual-orientation impeller designs position themselves to serve both architectures, smoothing revenue volatility.

By Voltage: 12 V Dominance Faces 48 V Disruption

The 12 V segment controlled 64.79% of the electric coolant pump market share in 2024 because most global light-vehicle architectures still operate on legacy power networks. Lower component cost and mature supply chains keep 12 V relevant, particularly in price-sensitive models. Nonetheless, 48 V+ units are surging at 22.52% CAGR as automakers adopt mild-hybrid systems that recuperate braking energy and power electric superchargers.

High-voltage auxiliaries alleviate copper mass by cutting current draw, an advantage that becomes critical as vehicle wire lengths climb with advanced driver-assistance systems. Suppliers now integrate smart MOSFET drivers and galvanic isolation to meet functional-safety targets. Market-entry barriers remain moderate because brushless motor know-how transfers from 12 V designs; however, inverter cooling requirements in 800 V BEVs call for specialized high-flow pumps. Early movers in silicon-carbide gate electronics gain efficiency headroom that differentiates performance offerings.

By Vehicle Type: Commercial Segments Accelerate

Passenger cars represented 61.96% of the electric coolant pump market share in 2024, reflecting the sheer volume of global light-vehicle production. Yet medium and heavy commercial vehicles (MHCVs) form the fastest-growing slice at 14.67% CAGR due to regulatory pressure to decarbonize last-mile logistics. Fleet operators seek pumps with higher flow rates and reinforced shafts to cope with rapid battery charging and extended duty cycles.

Light commercial vehicles (LCVs) act as a bridge market where van electrification programs require flexible pump output programming to balance range and cargo-area temperature control. MHCV adoption of fuel-cell range extenders introduces sub-ambient coolant circuits that keep hydrogen stacks within optimal thermal windows, further multiplying pump count per vehicle. Suppliers develop modular platforms that scale from 600 W passenger-car units to 4 kW truck pumps, sharing electronics to maximize economies of scale.

By Propulsion Type: BEV Growth Transforms Thermal Architecture

Internal-combustion engines (ICEs) retained 54.97% of the electric coolant pump market share in 2024 because global vehicle production remains ICE-weighted. Nevertheless, BEVs exhibit the highest growth, advancing at 24.36% CAGR as battery prices decline and charging infrastructure expands. Pump duty cycles change significantly: instead of operating near-constant at engine idle, BEV pumps modulate flow in milliseconds based on inverter temperature, fast-charge state, and cabin heat-pump demand.

Plug-in hybrids (PHEVs) and conventional hybrids combine ICE and electric loops, often requiring two pumps to manage dual heat sources. Fuel-cell electric vehicles introduce still more complexity, necessitating sub-50 °C coolant for the stack plus higher-temperature loops for drive motors. Pump makers thus broaden material portfolios to include iron-less bearings and fluoropolymer impellers resistant to de-ionized water corrosion. Software updates delivered over-the-air adjust pump maps as battery chemistries evolve, extending component life without mechanical change.

By Sales Channel: OEM Integration Dominates Strategy

OEMs accounted for 73.39% of the electric coolant pump market share in 2024 and are projected to grow at a 13.06% CAGR to 2030, as thermal management shifted from an optional accessory to a mission-critical system. Automakers integrate pumps early in platform design, optimizing hose routing and software control algorithms to reclaim every watt of saved energy. Tier-1s co-locate engineering teams at OEM tech centers to accelerate validation cycles and secure multi-year sourcing agreements.

Aftermarket channels face hurdles; rising pump intelligence embeds CAN or LIN communication for diagnostics, making drop-in replacements difficult. Independent workshops demand plug-and-play kits that include pre-filled coolant and quick-connect fittings to avoid air pockets. Some suppliers now offer “white-label” variants of OEM pumps with simplified firmware, balancing price sensitivity with reliability. Despite complexity, the aftermarket still expands as the global in-use BEV fleet climbs, creating long-tail service revenue.

Geography Analysis

Asia-Pacific captured 47.38% of the electric coolant pump market share in 2024, buoyed by China’s vertically integrated battery supply chain, which slashes pump logistics costs and speeds design iterations. Government subsidies and local-content rules foster tier-1/tier-2 partnerships that colocate pump, inverter, and battery-pack production. India’s adoption of 48 V mild-hybrid commercial fleets adds incremental volume, while Japan and South Korea contribute high-precision micro-motor technology and advanced resin sealing expertise. Regional OEMs increasingly source pumps from domestic suppliers to mitigate exchange-rate risk and ensure just-in-time inventory.

The Middle East and Africa region records the fastest CAGR at 13.58% as national diversification agendas allocate sovereign capital to EV assembly plants and high-voltage component lines. Saudi Arabia’s giga-projects mandate local content for thermal sub-assemblies, attracting joint ventures between global pump specialists and regional conglomerates. Ambient temperatures exceeding 50 °C challenge coolant pump durability; hence, suppliers offer larger impeller clearances and high-boil-point coolant compatibility. South Africa leverages established automotive zones to export pumps across the African Continental Free Trade Area, easing tariff burdens and shortening lead times.

Europe and North America deliver steady, premium-focused growth. EU automakers emphasize range optimization in cold climates, demanding pumps capable of delivering low-flow, high-head pressure for battery warming during overnight parking. North American OEMs pour capital into domestic semiconductor fabs that supply silicon-carbide MOSFETs for pump motor controllers, shortening supply chains and unlocking higher efficiency. Both regions advance low-GWP coolant mandates, compelling pump makers to certify new elastomer blends and stainless-steel shafts that resist novel glycol mixtures. Manufacturing footprints expand near final-assembly plants to satisfy localized-content incentives and circumvent logistics bottlenecks.

Competitive Landscape

The electric coolant pump market exhibits moderate concentration, creating opportunities for specialized thermal management innovators to capture white-space segments through integrated "super-bottle" solutions and advanced control algorithms. Bosch capitalizes on system-level know-how, offering integrated “e-Axle plus thermal” packages that bundle pump, inverter, and motor cooling. Aisin leverages Toyota's affiliation to lock multi-platform pump contracts through 2030. Mahle and Valeo focus on compact, magnet-free motor pumps that sidestep rare-earth pricing swings, while Rheinmetall scales production of high-voltage units for battery-electric trucks.

Strategic alliances increasingly center on software and power-electronics integration. Bosch’s 2025 investment in U.S. silicon-carbide capacity supports vertically integrated pump controllers that raise efficiency by 3–5 percentage points. Valeo partners with Mahle to co-develop predictive-control algorithms analyzing route elevation, ambient temperature, and driver behavior, pre-conditioning coolant flow before thermal spikes occur. Raw-material hedging emerges as a defensive tactic; suppliers lock multi-year copper contracts or substitute aluminum windings in certain models.

New entrants exploit niches such as fuel-cell stack cooling or submersible battery-tray pumps for skateboard architectures. Semiconductor manufacturers embed micro-pumps within power modules, potentially displacing stand-alone units in low-power zones. Yet stringent automotive validation cycles and ISO 26262 functional-safety hurdles protect incumbents. Intellectual-property portfolios on seal geometries, cavitation modeling, and acoustic damping remain key competitive moats.

Electric Coolant Pump Industry Leaders

Robert Bosch GmbH

Aisin Seiki Co., Ltd.

Continental AG

Valeo SA

Mahle GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Rheinmetall won a mid-six-figure order for its CWA 2000 high-voltage pumps from a U.S. truck OEM, with deliveries slated for 2028-2035.

- February 2025: TI Fluid Systems debuted a 12 V pump tailored for BEVs, integrating closed-loop temperature control to optimize energy consumption.

- February 2025: Rheinmetall secured a EUR 26 million contract for CWA 2000 pumps to power an 800 V fuel-cell architecture supplied by an Asian engine maker.

Global Electric Coolant Pump Market Report Scope

| Horizontal Pumps |

| Vertical Pumps |

| 12 V |

| 24 V |

| 48 V + |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Internal Combustion Engine |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Pump Type | Horizontal Pumps | |

| Vertical Pumps | ||

| By Voltage | 12 V | |

| 24 V | ||

| 48 V + | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Propulsion Type | Internal Combustion Engine | |

| Battery Electric Vehicle (BEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Fuel-Cell Electric Vehicle (FCEV) | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is demand for electric coolant pumps growing between 2025 and 2030?

Global revenue is projected to climb from USD 2.37 billion in 2025 to USD 4.22 billion by 2030, reflecting a 12.23% CAGR.

Which vehicle class is the quickest-growing user of electric coolant pumps?

Medium and heavy commercial vehicles post the fastest uptake, registering a 14.67% CAGR as fleet electrification intensifies urban-delivery compliance.

Why are 48 V pumps gaining traction over 12 V models?

48 V architectures cut wiring mass, lower current draw, and enable higher flow rates needed for rapid battery charging, driving a 22.52% CAGR in the segment.

What is the biggest regional market for electric coolant pumps today?

Asia-Pacific leads with 47.38% of global revenue, propelled by China’s EV output scale and localized component ecosystems.

Which factor most threatens near-term pump profitability?

Volatile raw-material pricing, especially copper, squeezes margins and forces dynamic pricing strategies across the supply chain.

Are aftermarket channels keeping pace with OEM demand?

OEMs still dominate at 73.39% market share, but aftermarket sales expand as the BEV parc grows, provided service-skill gaps are addressed.

Page last updated on: