Automotive Engineering Services Outsourcing Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 150.03 Billion |

| Market Size (2031) | USD 212.69 Billion |

| Growth Rate (2026 - 2031) | 7.23% CAGR |

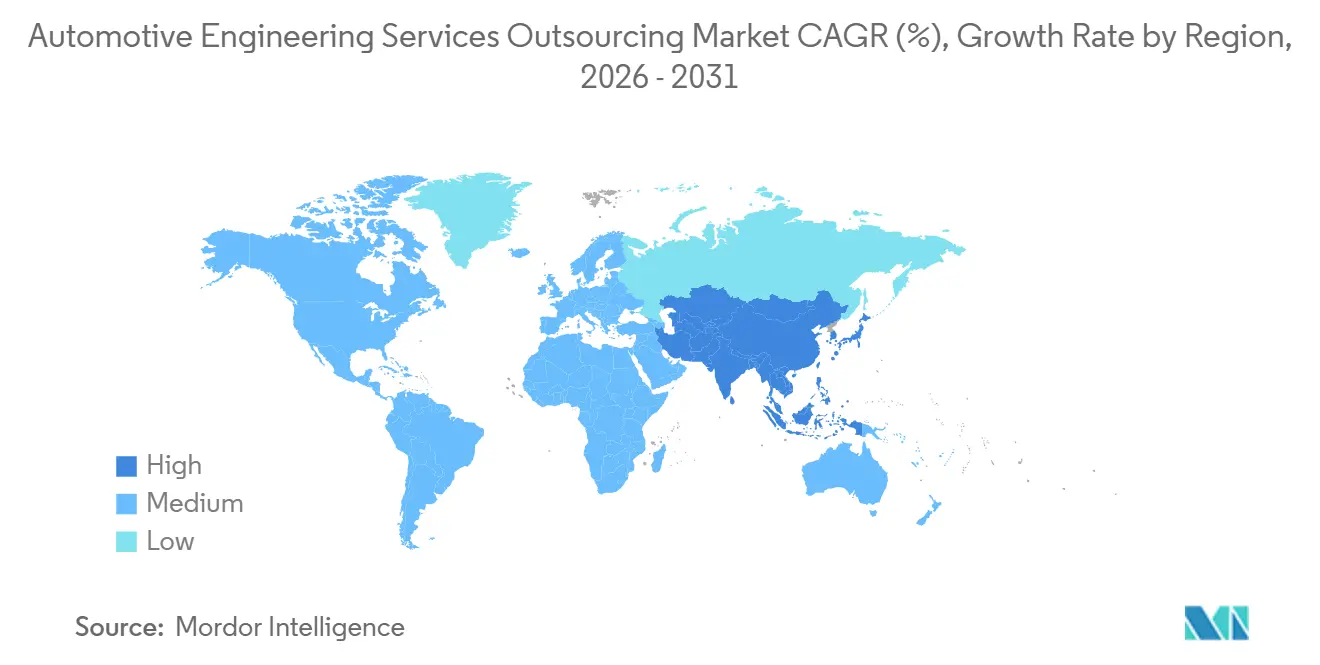

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

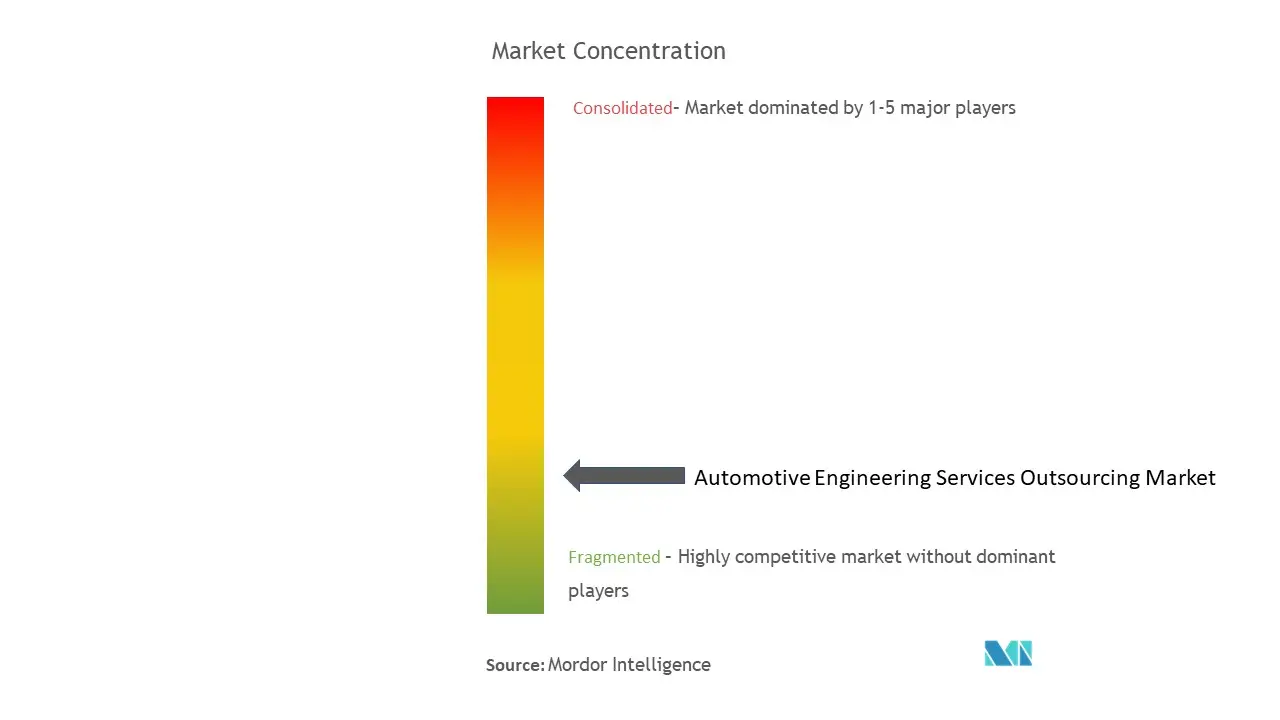

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Engineering Services Outsourcing Market Analysis by Mordor Intelligence

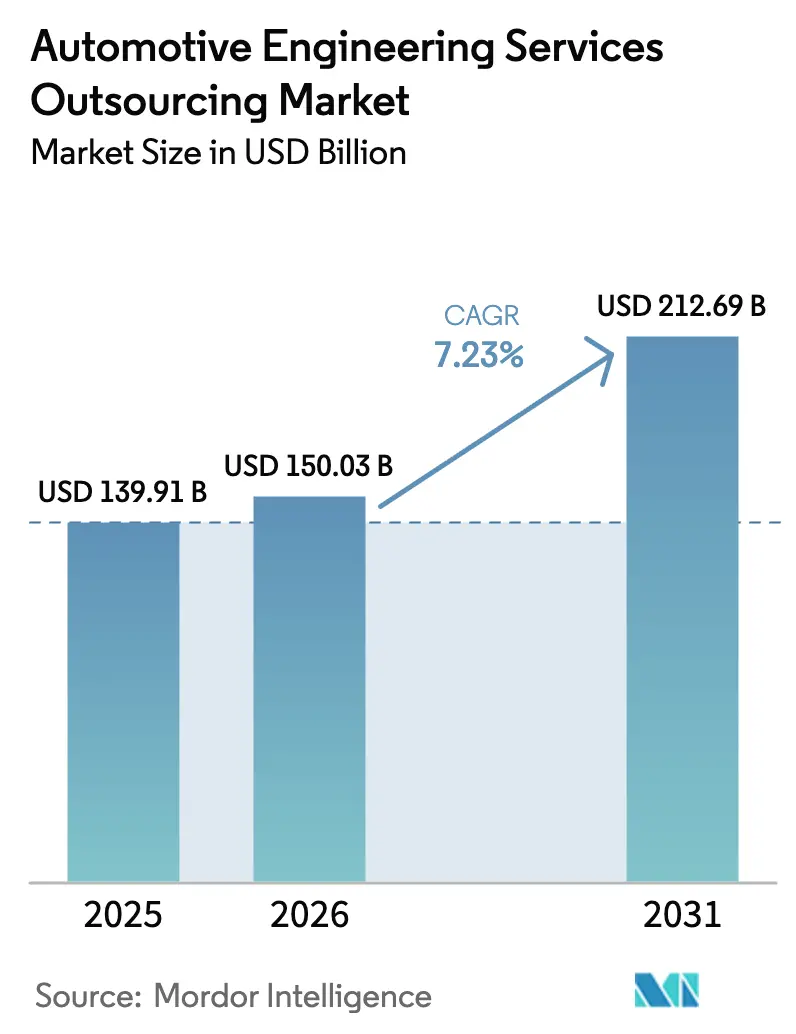

The automotive engineering services outsourcing market size is expected to grow from USD 139.91 billion in 2025 to USD 150.03 billion in 2026. It is forecast to reach USD 212.69 billion by 2031 at a 7.23% CAGR over 2026-2031. Growing preference for software-defined vehicle platforms, battery-cell innovation, and zonal electrical-electronic architectures is encouraging original equipment manufacturers (OEMs) to redirect capital away from routine design and toward higher-value software and systems projects, leaving specialized providers to absorb prototyping, validation, and systems-integration workstreams. Shifting regulatory environments—especially UNECE WP.29 cybersecurity rules and ISO 26262 functional-safety audits—have increased validation workloads, while digital-twin platforms are reducing the coordination penalty historically associated with offshore teams, allowing OEMs to arbitrage labor costs without slowing iteration. In parallel, re-shoring incentives inside the United States Inflation Reduction Act and the European Union Important Projects of Common European Interest are stretching in-house engineering bandwidth, triggering near-shore engagements that satisfy local-content thresholds.

Key Report Takeaways

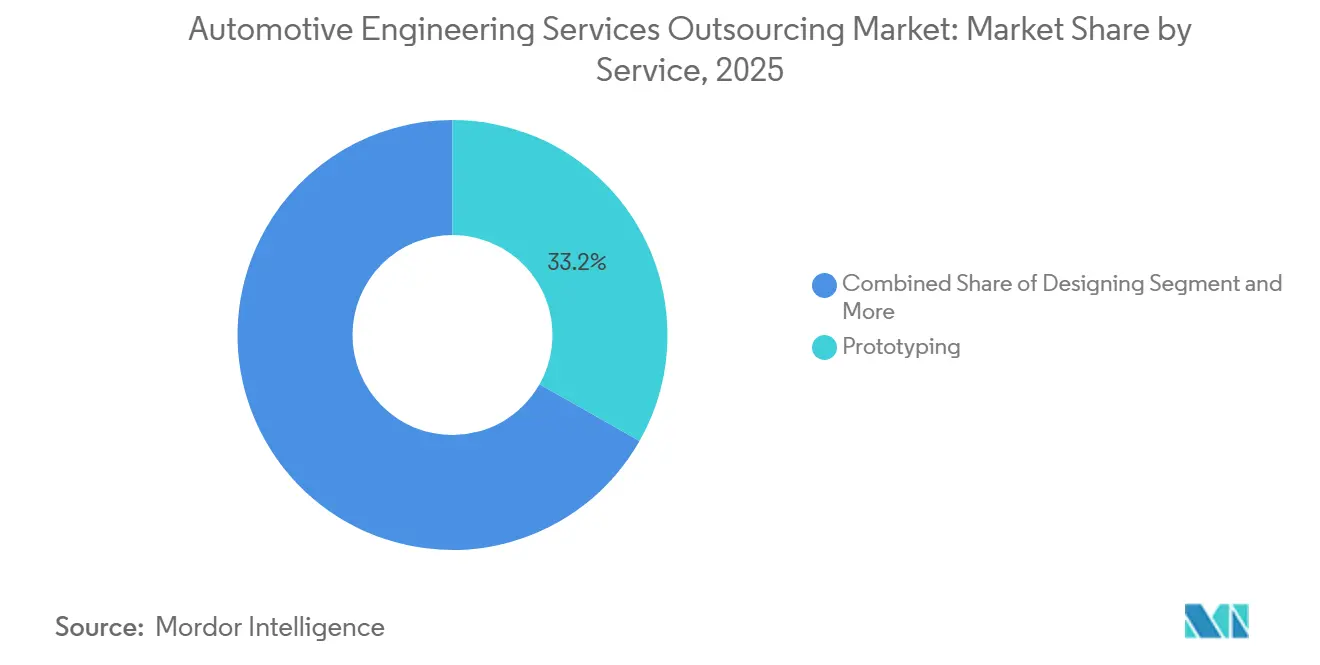

- By service, prototyping accounted for 33.21% of 2025 revenue, while testing is the fastest-growing service, with a 9.48% CAGR during 2026-2031.

- By location, onshore services accounted for 57.85% of 2025 spend, yet offshore services delivered the steepest rise at an 8.14% CAGR over 2026-2031.

- By application, autonomous-driving features led with 35.33% of 2025 revenue and are advancing at 10.76% CAGR through 2031.

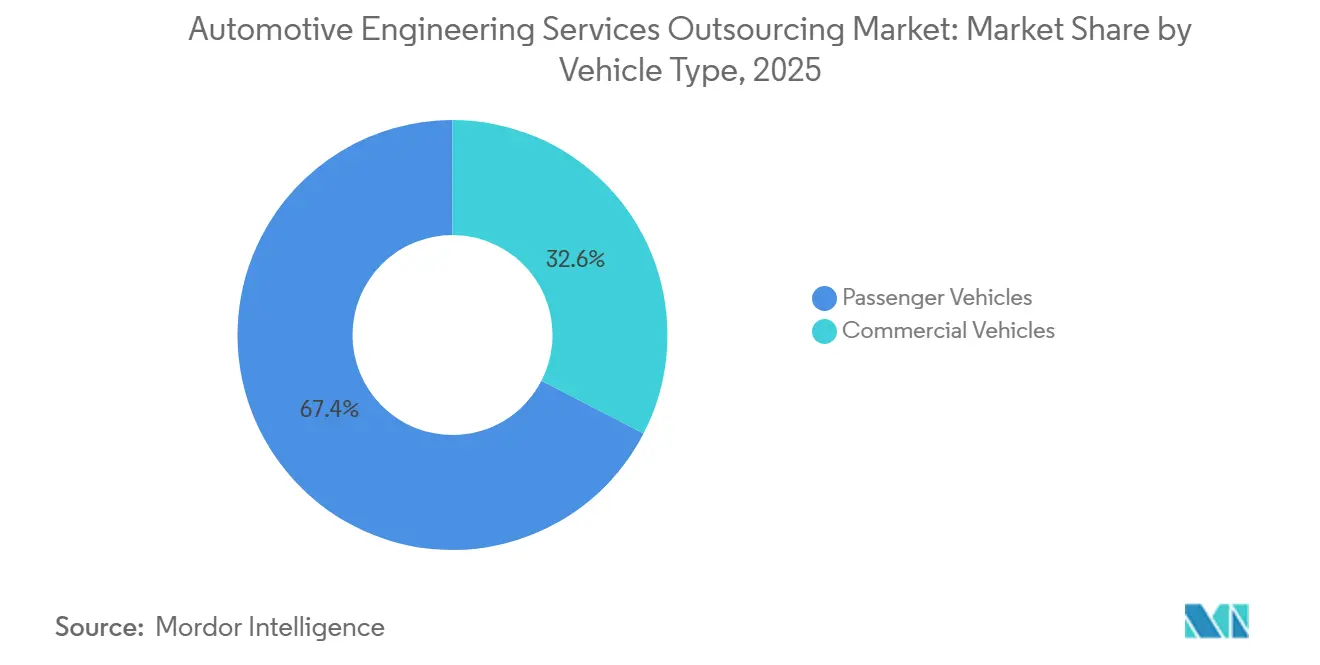

- By vehicle type, passenger vehicles accounted for 67.42% of 2025 volume and posted the highest growth rate at a 10.81% CAGR to 2031.

- By propulsion, internal-combustion programs retained 74.22% of 2025 spend, whereas electric-vehicle engineering is scaling fastest at 11.05% CAGR through 2031.

- By geography, Asia-Pacific accounted for 44.33% of 2025 revenue and is projected to grow at an 8.36% CAGR through 2031, outpacing every other region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Engineering Services Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for EV Engineering Expertise Rises | +2.8% | Global, strongest in China, EU, North America | Medium term (2-4 years) |

| OEMs and Tier-1s Focus on Cost Optimization | +2.1% | Global, strongest in Asia-Pacific and Eastern Europe | Short term (≤2 years) |

| Global Safety and ADAS Rules Tighten | +1.9% | EU, North America, Japan, South Korea | Medium term (2-4 years) |

| Modular Chassis and Zonal E/E Architectures Boost Outsourcing | +1.6% | North America, EU, China | Long term (≥4 years) |

| Digital Twin and AI Simulations Enable Collaboration | +1.2% | Global | Medium term (2-4 years) |

| US and EU Re-Shoring Strains Engineering Capacity | +0.9% | North America, EU | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Demand For EV-Specific Engineering Expertise

Battery-pack integration, thermal-management modeling, and high-voltage safety validation have become core workstreams that internal-combustion-engine teams cannot immediately repurpose, pressing OEMs to lease capacity from AVL, FEV, Ricardo, and similar firms. AVL inaugurated a battery-testing center in South Korea, successfully cycling cells through thermal-abuse scenarios [1]“Battery Test Center Opens in South Korea,” AVL List GmbH, avl.com. This move helped clear homologation backlogs for both lithium-iron-phosphate and nickel-manganese-cobalt chemistries. Tata Technologies inked a multi-year deal for a battery-enclosure program with a luxury OEM in Europe [2]“European Luxury OEM Awards Multi-Year EV Contract,” Tata Technologies, tatatechnologies.com. This highlights a trend in which Tier-1 suppliers are shifting their focus from low-margin mechanical tasks to software-centric endeavors. FEV expanded its hydrogen fuel-cell offerings, foreseeing a bifurcated evolution of commercial vehicles: battery-electric systems for urban routes and fuel cells for long-haul routes. This strategic pivot emphasizes engineering's shift towards electrical architecture and software, contributing additional growth to the baseline.

Cost-Optimization Focus Among OEMs and Tier-1s

Automotive operating margins have narrowed as raw-material inflation, battery warranty provisions, and software overruns pressure profitability. Procurement teams globally benchmark labor rates, with providers in India certified to ISO 26262 ASIL-D offering designs at significantly lower costs than Western Europe, enabling substantial savings on revenue-driving features. Alten Group has expanded its presence in Eastern Europe, establishing a nearshore hub that ensures GDPR compliance and operates within aligned time zones. Stellantis has announced plans to reduce engineering roles while increasing outsourced spending, effectively shifting from fixed costs to variable capacity. Similarly, Bosch and Continental have redirected additional work to Indian partners to mitigate the impact of rising wage inflation in Germany. This cost-driven strategy has an immediate positive effect on the compound annual growth rate.

Tightening Global Safety / ADAS Regulations

UNECE WP.29 regulations mandate cybersecurity management systems and over-the-air update controls. These regulations are extending validation cycles and steering businesses towards compliance specialists. Audits under ISO 26262 have broadened to encompass machine-learning perception, compelling providers to ensure comprehensive validation of their neural networks. Elektrobit unveiled a pre-certified ASIL-D middleware bundle that integrates intrusion detection. This innovation is projected to significantly accelerate OEM integration. Ricardo bolstered its UK cybersecurity lab, gearing up for anticipated Vehicle-to-Everything security audits. Additionally, homologation processes, which previously took less time, have now taken considerably longer. This shift has heightened testing demand and contributed to medium-term growth.

Modular Chassis and Zonal E/E Architectures Boost Systems-Integration Outsourcing

Continental introduced a zonal gateway capable of merging Ethernet, CAN-FD, and FlexRay traffic into a unified backbone[3]“High-Bandwidth Zonal Gateway Demonstration,” Continental AG, continental.com. In a strategic collaboration, Aptiv partnered with Qualcomm to develop a zonal compute platform based on Snapdragon-Ride, aimed at production vehicles. This partnership effectively integrates hardware and software, enhancing profit margins. Stellantis, leveraging its STLA Large platform, is adopting a zonal architecture that reduces wiring-harness weight and assembly time. However, this advancement requires extensive lines of code, leading Stellantis to assign integration testing to Capgemini Engineering. Meanwhile, IAV introduced a zonal-simulation environment that accelerates fail-operational validation, contributing to growth with strong long-term potential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IP and Data Security Concerns | -1.4% | Global, strongest in North America and EU | Medium term (2-4 years) |

| Talent Shortage Raises Costs | -1.1% | Global, most severe in Germany, US, Japan | Medium term (2-4 years) |

| Coordination Issues in Distributed Teams | -0.7% | Global | Short term (≤2 years) |

| Export Laws Restrict Offshore Operations | -0.5% | North America, EU, Japan | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

IP- and Data-Security Concerns

OEMs prioritize vehicle architectures, battery-management algorithms, and perception logic as key differentiators. However, the need for information sharing in outsourcing often leads to hesitation. Volkswagen has decided to restrict offshore access to its MEB platform compute modules, limiting the potential scope for third parties. Export-control regulations prevent certain LiDAR and radar datasets from crossing specific borders. As a response, Capgemini Engineering is set to invest in ISO 27001 air-gapped centers, despite these precautions trimming margins. While blockchain-based configuration systems from IBM and SAP offer tamper-proof trails, they've only seen limited adoption. This lag results in a dip in CAGR until secure collaboration standards are fully established.

Scarcity of Functional-Safety & Cybersecurity Talent Inflating Costs

TÜV SÜD reported a significant decline in the number of qualified functional-safety auditors in Germany, as both the aerospace sector and industrial automation compete for the same pool of experts. In the United States, hourly rates for ASIL-D engineers have risen considerably, challenging the previously held belief in the cost benefits of offshoring. To address the growing demand, L&T Technology Services launched a functional-safety academy to certify additional professionals annually. However, the academy continues to face high attrition rates. Globally, SAE International identifies a limited number of professionals with both automotive cybersecurity credentials and practical penetration-testing experience. Furthermore, wage inflation is expected to negatively impact forecasted growth in the coming years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Testing Outpaces Prototyping Growth

Prototyping retained 33.21% of market share in 2025, highlighting its critical path role—but its growth moderates as digital twins eliminate multiple physical iterations. Testing services are expanding at a 9.48% clip through 2031, according to UNECE WP.29 and ISO 26262, as the frameworks multiply checkpoints, on a faster trajectory than any other category in the automotive engineering services outsourcing market.

Design services, encompassing CAD, finite-element, and CFD analysis, play a significant role in the market, driven by OEMs retaining core styling functions in-house. System integration is experiencing strong growth due to the increasing complexity of middleware in zonal architectures. Simulation services are gaining momentum, supported by cloud-based platforms from industry leaders such as Siemens and Ansys that enable concurrent validation across crash, NVH, and aerodynamics. Embedded software development is accelerating as software-defined vehicles demand extensive coding requirements. The market is undergoing a fundamental shift from traditional physical builds to a focus on virtual validation, marking a transformative trend in the automotive engineering services outsourcing landscape.

By Location: Off-Shore Gains Share Despite Security Concerns

On-shore retained 57.85% of 2025 revenue, reflecting the persistent premium placed on early-stage concept and regulated programs that demand in-person collaboration. Offshore work is advancing at an 8.14% CAGR by 2031, faster than onshore, as AI simulation tools narrow coordination gaps, sustaining labor-cost arbitrage that helps OEMs reallocate budgets.

India remains a pivotal player in the offshore growth arena. Tata Technologies, L&T Technology Services, and HCL Technologies are producing ISO 26262-certified outputs at costs significantly lower than those in Western Europe. However, due to ITAR and dual-use restrictions, projects with highly classified perceptions are kept onshore. This constraint limits total offshore penetration to less than half. Alten's acquisition of multiple Eastern European firms underscores the significance of near-shoring in balancing security needs with cost efficiency.

By Application: Autonomous Driving Dominates Spend

Autonomous-driving programs captured 35.33% of market share in 2025 spend and are growing at a 10.76% CAGR, the fastest growth rate in the automotive engineering services outsourcing market. Electrification follows closely at 11.2% as battery-pack and high-voltage safety tasks multiply. As regulators expand the scope of ISO 26262, spending on safety systems has increased significantly, now accounting for a notable share of total expenditure. In a market increasingly leaning towards commoditization, infotainment and connectivity have shown steady growth.

Meanwhile, spending on body and chassis has risen more slowly. Traditional powertrain work, once a primary focus, now lags as the industry's attention shifts toward advancements in battery and motor engineering. The continuous evolution of ADAS (Advanced Driver Assistance Systems) algorithms has driven demand for simulation platforms, particularly those that leverage radar- and LiDAR-based scenarios, such as Applied Intuition's engines.

By Vehicle Type: Passenger Segment Sustains Lead

Passenger vehicles accounted for 67.42% of market share in 2025, and the segment remains on a 10.81% growth path as electrification compresses launch schedules and forces external capacity leasing. Commercial vehicles are experiencing steady growth, with heavier platforms increasingly adopting battery-electric systems for urban use and fuel cells for long-haul applications. This transition has generated a niche demand for advanced expertise in thermal management and charging solutions. A key example of this trend is Daimler Truck's decision to outsource the design of the eCascadia battery enclosure to EDAG, showcasing a convergence with engineering strategies commonly used in passenger cars.

By Propulsion Type: EV Engineering Closes the Gap

Internal-combustion projects still accounted for 74.22% of 2025 spend, as OEMs sunset pure ICE programs. Electric vehicles are growing at 11.05% through 2031, driven by battery integration, thermal modeling, and high-voltage validation, areas where legacy powertrain groups lack tooling. AVL’s South Korean test center and FEV’s hydrogen focus are visible proof points. Euro 7 and China 7 standards keep combustion calibration relevant—through hybridization—yet the propulsion split is visibly migrating toward full electrification.

Geography Analysis

Asia-Pacific accounted for 44.33% of 2025 revenue and is projected to grow at an 8.36% CAGR by 2031. India, with a significant number of Global Capability Centers, employs a large workforce of engineers. Meanwhile, China's substantial EV-R&D fund focuses on battery management, motor control, and Vehicle-to-Grid systems. Japan and South Korea, with major players like Toyota, Honda, Hyundai, and Kia, are deepening their commitments to ADAS outsourcing.

North America has seen advancements driven by policies requiring a higher percentage of domestically produced battery components. This has pushed OEMs to initiate concurrent engineering programs for new gigafactories, spurring nearshore demand. Addressing capacity gaps, technical centers have been established in key locations. Additionally, leveraging proximity to Detroit and trade agreements, Canadian firms like MAGNA International have secured body-and-chassis mandates.

Europe has faced challenges such as wage inflation and talent scarcity, prompting a shift toward cost-effective near-shore resources within the EU. Strategic acquisitions in countries like Poland and Romania highlight this trend. The UK has seen companies like Ricardo and Horiba MIRA overseeing battery and ADAS validation for local OEMs. French automotive giants Stellantis and Renault have expanded their contracts with engineering firms, focusing on zonal architecture and digital-twin technologies. Meanwhile, South America, the Middle East, and Africa, led by Brazil's flex-fuel and ethanol-hybrid initiatives, have collectively contributed to the market's growth.

Competitive Landscape

The revenue in the automotive engineering services outsourcing market is concentrated among the top providers: Tata Technologies, L&T Technology Services, Capgemini Engineering (Altran Technologies, SA), Alten Group, AVL, Bertrandt, FEV, Ricardo, HCL Technologies, and Tech Mahindra. To address slowing demand in the enterprise-software vertical, Indian IT giants Wipro, Infosys, and Cognizant are expanding their automotive practices, effectively leveraging established client relationships to secure engineering contracts.

Competitive strategies differ: some, like Alten, focus on geographic diversification in Eastern Europe, while others, such as Elektrobit, emphasize capability specialization by offering ISO-qualified middleware at premium pricing. Emerging opportunities are evident in hydrogen fuel-cell validation, solid-state battery prototyping, and Vehicle-to-Grid integration, though only a limited number of vendors provide comprehensive fuel-cell services. Tata Elxsi’s Coalesce digital twin platform is transforming ADAS scenario validation, enabling clients to simulate extensive virtual kilometers daily, significantly reducing test time, and supporting a recent expansion for a European luxury OEM. While Chinese firms Neusoft and HiRain Technologies aim to enter Europe and North America, they face restrictions related to ITAR and dual-use regulations. Additionally, the high certification costs for ISO and UNECE standards act as substantial entry barriers, strengthening the position of established players.

Automotive Engineering Services Outsourcing Industry Leaders

Bertrandt AG

IAV GmbH

AVL List GmbH

EDAG Group

Capgemini Engineering (Altran Technologies, SA)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Arrow Electronics, a global technology solutions provider, has unveiled its new Engineering Solutions Center (ESC) in Bangalore, India. This move underscores Arrow's dedication to democratizing access to pivotal technologies like IoT, edge computing, and intelligent sensing. Furthermore, it bolsters the engineering prowess of local tech manufacturers in India and in regions such as Southeast Asia, South Korea, and Japan. Key sectors benefiting from this initiative include industrial, automotive and transportation, energy management, and aerospace and defense.

- June 2025: Volvo Cars has selected HCLTech, a prominent global technology firm, as one of its key partners for engineering services. This collaboration highlights HCLTech's expertise in delivering innovative engineering solutions and reinforces its position as a trusted partner in the automotive industry.

Global Automotive Engineering Services Outsourcing Market Report Scope

The automotive engineering services outsourcing market report is segmented by service (designing, prototyping, testing, system integration, simulation, and embedded software development), location (on-shore and off-shore), application (body and chassis, powertrain, automotive testing, autonomous driving features, infotainment and connectivity, safety systems, electrification, and others), vehicle type (passenger vehicles and commercial vehicles), propulsion type (ICE and EV), and geography. The market forecasts are provided in value (USD).

| Designing |

| Prototyping |

| Testing |

| System Integration |

| Simulation |

| Embedded Software Development |

| On-shore |

| Off-shore |

| Body and Chassis |

| Powertrain |

| Automotive Testing |

| Autonomous Driving Features |

| Infotainment and Connectivity |

| Safety Systems |

| Electrification |

| Others |

| Passenger Vehicles |

| Commercial Vehicles |

| Internal-Combustion Engine (ICE) Vehicles |

| Electric Vehicles (EV) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| APAC | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Service | Designing | |

| Prototyping | ||

| Testing | ||

| System Integration | ||

| Simulation | ||

| Embedded Software Development | ||

| By Location | On-shore | |

| Off-shore | ||

| By Application | Body and Chassis | |

| Powertrain | ||

| Automotive Testing | ||

| Autonomous Driving Features | ||

| Infotainment and Connectivity | ||

| Safety Systems | ||

| Electrification | ||

| Others | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| By Propulsion Type | Internal-Combustion Engine (ICE) Vehicles | |

| Electric Vehicles (EV) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| APAC | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the automotive engineering services outsourcing market in 2026?

The automotive engineering services outsourcing market is valued USD 150.03 billion in 2026.

Which application captures the biggest share of outsourced engineering budgets?

Autonomous-driving features led with 35.33% of 2025 spending and are growing at 8.76% CAGR to 2031.

What service category is expanding fastest through 2031?

Testing services, supported by stringent UNECE WP.29 and ISO 26262 compliance cycles, advance at 9.48% CAGR.

Why is Asia-Pacific gaining share?

A combination of India’s low-cost, ASIL-certified talent pool and China’s state-funded EV-R&D ecosystem lifts the region at 8.36% CAGR.

What is the outlook for internal-combustion engineering work?

ICE projects still form 74.22% of 2025 spend but slow growth as OEMs divert resources toward electric-vehicle programs.

Page last updated on: