Automotive Brake Valve Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 27.74 Billion |

| Market Size (2030) | USD 33.05 Billion |

| Growth Rate (2025 - 2030) | 3.41% CAGR |

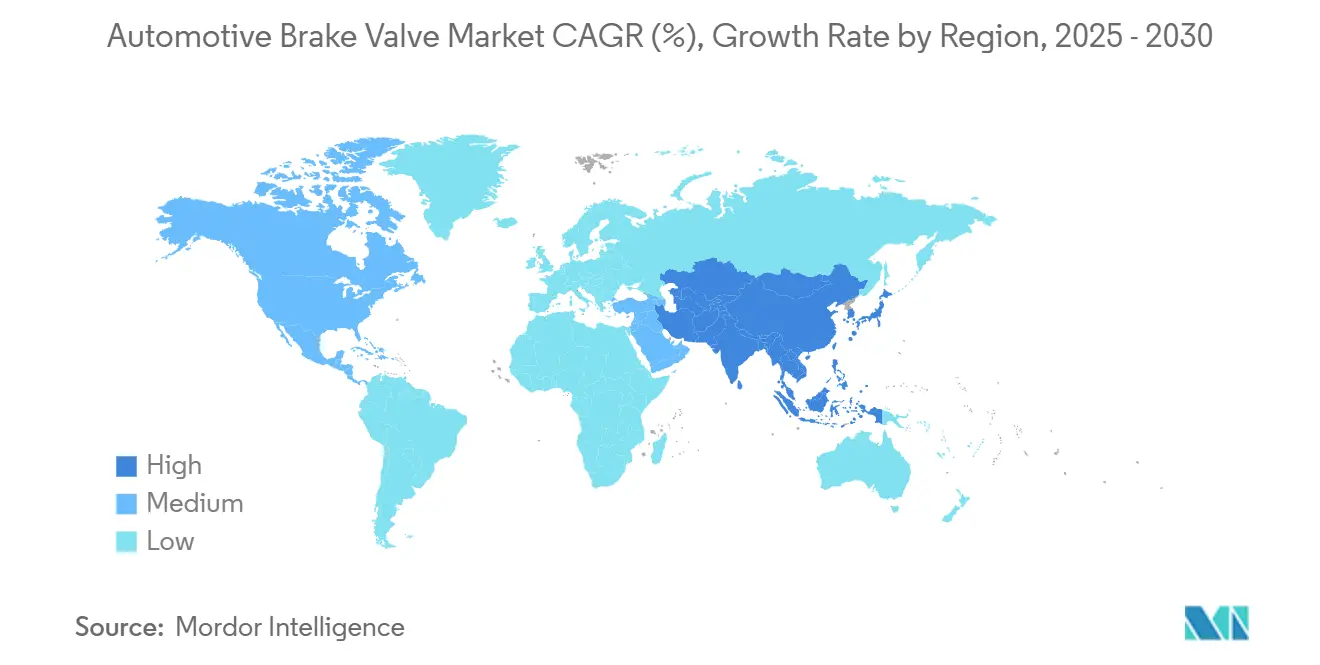

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Brake Valve Market Analysis by Mordor Intelligence

The automotive brake valve market size is USD 27.74 billion in 2025 and is forecast to reach USD 33.05 billion by 2030 at a 3.41% CAGR, with growth propelled by stricter safety regulations, accelerating electrification, and deeper integration of brake-by-wire platforms. Commercial vehicle demand, electronic valve adoption, and rising composite material penetration are reshaping the competitive calculus while supply chain volatility and regulatory compliance costs temper near-term margin expansion. Notably, electronic brake valves are gaining share as automakers coordinate braking, regenerative energy capture, and driver-assistance functions in real time. Composite housings, sensor-embedded assemblies, and software-defined control logic elevate average selling prices, tilting the value pool toward suppliers that bridge mechanical components with advanced electronics. Asia-Pacific remains both the largest production base and the fastest-growing demand center, ensuring that regional design preferences and regulatory frameworks increasingly dictate global product roadmaps.

Key Report Takeaways

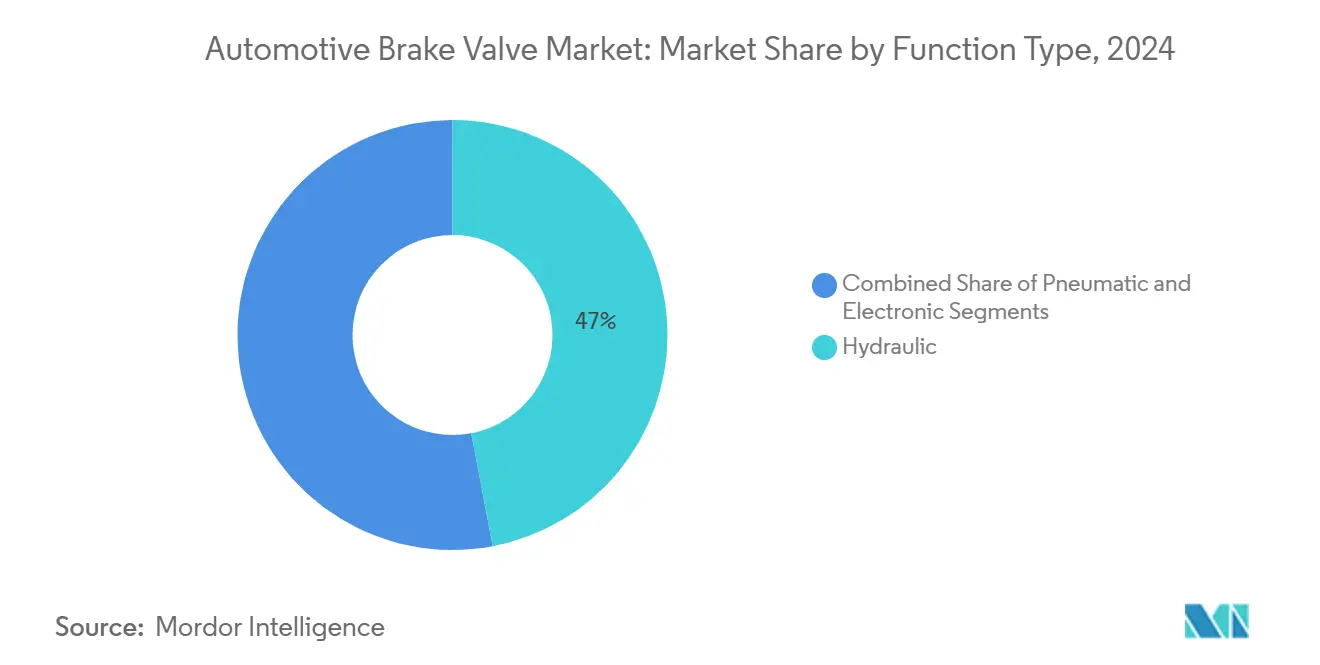

- By function type, hydraulic valves held 47.03% of the automotive brake valve market share in 2024, whereas electronic valves are advancing at an 8.90% CAGR through 2030.

- By material, steel dominated with a 62.14% of the automotive brake valve market share in 2024, while composites are expanding at a 10.60% CAGR to 2030.

- By vehicle type, passenger cars accounted for 57.28% of the automotive brake valve market share in 2024, but light commercial vehicles are projected to post the fastest 7.80% CAGR.

- By technology, conventional braking systems controlled 64.09% of the automotive brake valve market share in 2024, whereas regenerative systems are set to register a 12.40% CAGR over the forecast horizon.

- By sales channel, the OEM segment contributed 78.22% of the automotive brake valve market in 2024 revenue, while the aftermarket is growing at a 9.50% CAGR due to rising component complexity.

- By geography, Asia-Pacific commanded 41.37% of the automotive brake valve market share in 2024 and is forecast to expand at a 9.20% CAGR through 2030.

Global Automotive Brake Valve Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Electrification Increasing Demand for Electronically-Controlled Brake Valves | +1.2% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| ADAS Penetration Driving Shift to Brake-By-Wire Architectures | +0.9% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Emission-Linked Safety Regulations Tightening After Euro 7 and China VII | +0.8% | Europe, China, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Global Freight Growth in E-Commerce Boosting Air-Brake Valve Volumes in Heavy Trucks | +0.6% | Global, concentrated in Asia-Pacific and North America | Short term (≤ 2 years) |

| Integration of Smart Health-Monitoring Sensors in Valves | +0.7% | Global, adoption led by premium OEMs in Europe and United States | Long term (≥ 4 years) |

| 48-V Mild-Hybrid Platforms Creating Niche Demand for Low-Pressure Electro-Hydraulic Valves | +0.5% | Europe and Asia-Pacific, limited penetration in United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Emission-Linked Safety Regulations Drive Electronic Valve Adoption

Euro 7 and China VII emission standards, effective from 2025-2026, mandate brake dust particle monitoring that fundamentally alters valve design requirements beyond traditional pressure modulation functions. These regulations compel integration of particulate sensors within brake valve assemblies, creating demand for electronically-controlled units capable of real-time emission data transmission to vehicle control networks. The regulatory framework extends beyond passenger vehicles to commercial trucks, where air brake valve systems must incorporate electronic monitoring capabilities previously absent in pneumatic-only architectures.

Compliance necessitates valve designs with embedded diagnostic capabilities, shifting from purely mechanical operation toward hybrid electro-pneumatic systems that can interface with vehicle emission control modules. The standards create a regulatory moat favoring suppliers with electronic integration capabilities, as traditional pneumatic valve manufacturers face substantial re-engineering costs to achieve compliance certification from regulatory bodies, including the European Commission and China's Ministry of Ecology and Environment.

Electrification Accelerates Electronic Brake Valve Integration

Vehicle electrification fundamentally redefines brake valve requirements as regenerative braking systems demand seamless coordination between friction and energy recovery modes through electronically-controlled pressure modulation. Electric vehicles require brake valves capable of rapid pressure adjustments to optimize energy recovery while maintaining stopping performance, necessitating response times under 10 milliseconds compared to 50-100 milliseconds for conventional hydraulic systems[1]"Automated Fluid Control in Modern Vehicles - The Role of Solenoid Valves,"electricsolenoidvalves.com.. The transition eliminates vacuum brake boosters in favor of electro-hydraulic systems, creating demand for high-speed solenoid valves and electronic pressure control units that can modulate brake force independently at each wheel.

Battery electric commercial vehicles present unique challenges, requiring air brake valve systems that operate efficiently on limited electrical power while maintaining fail-safe pneumatic backup capabilities. This technological shift favors suppliers with expertise in electronic control integration, as traditional hydraulic valve manufacturers must develop new competencies in motor control algorithms and sensor fusion technologies.

ADAS Integration Demands Brake-By-Wire Architecture Evolution

Advanced driver assistance system penetration drives fundamental changes in brake valve architecture, as autonomous emergency braking and adaptive cruise control require millisecond-precision pressure modulation, which is impossible with traditional hydraulic systems. Brake-by-wire systems eliminate mechanical linkages between the brake pedal and wheel-end actuators, necessitating electronically-controlled valve arrays that execute complex braking algorithms without driver input. The technology enables individual wheel pressure control essential for vehicle stability systems, requiring valve designs with integrated position feedback sensors and fail-safe mechanical backup systems.

Level 3+ autonomous vehicles demand redundant brake valve systems that maintain full braking capability despite single-point electronic failures, driving development of dual-circuit electronic valve architectures with independent power supplies. This evolution creates opportunities for suppliers capable of integrating valve hardware with sophisticated control software, while traditional mechanical valve manufacturers face displacement unless they develop electronic system capabilities.

E-Commerce Freight Growth Expands Commercial Vehicle Valve Demand

Global e-commerce expansion drives unprecedented demand for commercial vehicle brake systems as freight volumes surge and delivery vehicle utilization intensifies, creating sustained replacement demand for air brake valves in heavy-duty applications. Last-mile delivery optimization requires frequent stop-start cycles that accelerate brake valve wear, particularly in urban environments where regenerative braking integration becomes essential for operational efficiency. The shift toward electric commercial vehicles in urban freight applications necessitates specialized valve designs capable of coordinating pneumatic brake systems with electric motor regeneration, creating a niche market for hybrid electro-pneumatic valve assemblies.

Commercial vehicle manufacturers increasingly specify electronically-controlled air brake systems to enable fleet management integration and predictive maintenance capabilities, driving demand for valve assemblies with embedded diagnostic sensors and wireless communication capabilities. This trend particularly benefits suppliers capable of providing integrated valve and control system solutions, as fleet operators seek to minimize component complexity while maximizing operational visibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Shortages Delaying Advanced Valve Roll-Outs | -0.6% | Global, strongest impact in Asia-Pacific and United States supply chains | Short term (≤ 2 years) |

| Reliability Concerns Over Regenerative Braking Valves in Extreme Climates | -0.5% | Cold-weather markets in Europe, Canada, and Northern Asia | Medium term (2-4 years) |

| Raw-Material Price Volatility (Steel and Aluminum) Squeezing Supplier Margins | -0.4% | Global, affecting Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Slow Retrofitting Rate in Legacy Vehicle Parc Limits Aftermarket Electronic Valves | -0.3% | North America and Europe, mature vehicle markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility Constrains Supplier Margin Expansion

Steel and aluminum price volatility creates persistent margin pressure on brake valve manufacturers as commodity costs represent 35-45% of production expenses, with suppliers unable to fully pass through price increases due to long-term OEM contracts with fixed pricing structures. The challenge intensifies for composite material adoption, where carbon fiber and advanced polymer costs fluctuate more dramatically than traditional metals, creating uncertainty in new product development investments. Smaller regional suppliers face a disproportionate impact as they lack the purchasing power to secure favorable raw material contracts or implement hedging strategies available to larger multinational competitors.

Supply chain disruptions in steel production, particularly from China's environmental regulations affecting steel mills, create periodic shortages that force brake valve manufacturers to source materials at premium prices or face production delays. This dynamic favors vertically integrated suppliers with captive material sources or those with sufficient scale to negotiate long-term supply agreements, while constraining growth opportunities for emerging market entrants.

Legacy Vehicle Parc Retrofit Limitations Slow Electronic Valve Adoption

The installed base of vehicles with conventional hydraulic brake systems presents a significant barrier to aftermarket electronic valve adoption, as retrofit installations require extensive system modifications beyond simple component replacement. Legacy vehicles lack the electrical infrastructure and control modules necessary to support electronically-controlled brake valves, making upgrades economically unviable for most vehicle owners compared to traditional hydraulic component replacement. This creates a bifurcated aftermarket where electronic brake valve demand remains concentrated in newer vehicle segments, limiting overall market expansion potential.

The challenge is particularly acute in developing markets where vehicle age profiles skew older and owners prioritize cost over advanced functionality. Fleet operators with mixed-age vehicle populations face compatibility challenges when attempting to standardize on electronic brake systems, often choosing to maintain conventional hydraulic systems across entire fleets to simplify maintenance and parts inventory requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function Type: Electronic Systems Challenge Hydraulic Dominance

Hydraulic brake valves commanded 47.03% market share in 2024, reflecting their established position in conventional braking architectures, while electronic variants are projected to expand at 8.90% CAGR through 2030 as automakers prioritize integration with vehicle control networks. The electronic segment's growth trajectory stems from regulatory mandates requiring brake system integration with emission monitoring and advanced driver assistance systems, creating demand for valves capable of real-time data transmission and remote diagnostic capabilities. Pneumatic systems remain relevant primarily in heavy commercial vehicle applications where air brake systems remain preferred for their fail-safe characteristics and maintenance simplicity. However, even this segment faces pressure to incorporate electronic control elements for fleet management integration.

Recent patent filings reveal intensifying innovation in hybrid electro-hydraulic valve designs that combine traditional hydraulic reliability with electronic control precision, as suppliers seek to bridge the gap between conventional and fully electronic architectures[2]"SYSTEM FOR MANAGING THE ELECTRIC POWER FLOW IN BATTERY PACKS OF AN ELECTRIC OR HYBRID VEHICLE," Brembo S.p.A., patentguru.com.. The transition creates opportunities for suppliers capable of manufacturing valve assemblies with integrated sensors and control electronics, while traditional hydraulic valve manufacturers face margin pressure as their products become commoditized components in increasingly sophisticated brake systems. Electronic brake valves enable advanced features such as individual wheel pressure control and predictive maintenance capabilities, justifying premium pricing that supports higher profit margins compared to conventional hydraulic alternatives.

By Material Type: Composite Innovation Disrupts Steel Leadership

Steel maintains a 62.14% market share in 2024 due to cost advantages and established manufacturing processes, while advanced composite materials are experiencing a 10.60% CAGR growth through 2030, driven by automaker demands for weight reduction and corrosion resistance in brake valve assemblies. The composite segment's expansion reflects broader industry trends toward lightweighting as vehicle electrification increases sensitivity to component weight impacts on battery range and performance. Aluminum applications continue growing in premium vehicle segments where cost premiums are acceptable for weight savings, while brass remains confined to specialized applications requiring specific thermal and corrosion resistance properties.

Carbon fiber reinforced polymer composites represent the fastest-growing material subsegment, particularly in high-performance and luxury vehicle applications where brake valve weight reduction contributes meaningfully to overall vehicle dynamics. Manufacturing challenges in composite brake valve production create barriers to entry that favor suppliers with advanced materials expertise and specialized production capabilities. The material transition also enables integration of embedded sensors and electronic components directly within valve housings, creating opportunities for suppliers to differentiate through integrated functionality rather than competing solely on traditional performance metrics.

By Vehicle Type: Commercial Vehicle Growth Outpaces Passenger Segment

Passenger vehicles hold a 57.28% market share in 2024, yet light commercial vehicles are projected to grow at a 7.80% CAGR through 2030, driven by the rapid expansion of e-commerce delivery fleets and urban freight transportation. The commercial vehicle segment's growth stems from increasing vehicle utilization rates that accelerate brake valve replacement cycles, combined with fleet operators' willingness to invest in advanced brake systems that reduce maintenance costs and improve operational efficiency. Medium and heavy commercial vehicles represent a stable but slower-growing segment where air brake valve systems remain dominant due to regulatory requirements and operational advantages in high-duty-cycle applications.

Fleet electrification in commercial vehicle segments creates demand for specialized brake valve designs capable of integrating with regenerative braking systems while maintaining the reliability and fail-safe characteristics essential for commercial operations. The trend toward autonomous commercial vehicles, particularly in logistics and delivery applications, drives demand for brake-by-wire systems with redundant valve architectures capable of maintaining full braking capability despite single-point failures. This creates opportunities for suppliers capable of developing valve systems that meet both current commercial vehicle requirements and future autonomous vehicle standards.

By Technology: Regenerative Systems Drive Innovation

Conventional braking systems maintain a 64.09% market share in 2024, while regenerative braking systems represent the fastest-growing technology segment at 12.40% CAGR through 2030, requiring brake valve designs that enable seamless coordination between friction and energy recovery modes. The regenerative segment's rapid expansion reflects accelerating vehicle electrification and hybrid adoption, where brake valve systems must modulate friction braking to optimize energy recovery without compromising stopping performance. Advanced braking systems, incorporating features such as electronic stability control and anti-lock functionality, continue steady growth as these technologies become standard equipment across vehicle segments.

The integration of regenerative braking creates complex control requirements that favor electronically-controlled valve systems capable of rapid pressure modulation and precise coordination with electric motor controllers[3]Nicolae Vasiliu, "Digital Electrohydraulic Braking Systems in Automotive Engineering," Intechopen, intechopen.com.. Suppliers developing valve systems for regenerative applications must address unique challenges, including thermal management during rapid switching between friction and regenerative modes, and fail-safe operation when regenerative systems become unavailable. This technological evolution creates barriers to entry that favor suppliers with expertise in electronic control systems and automotive software development, while traditional mechanical valve manufacturers face displacement unless they develop new competencies.

By Sales Channel: OEM Integration Drives Aftermarket Evolution

The OEM channel commanded 78.22% market share in 2024, reflecting automakers' preference for integrated brake valve solutions that interface seamlessly with vehicle control systems, while the aftermarket segment is projected to grow at 9.50% CAGR through 2030 as vehicle complexity drives more frequent component replacements. OEM demand increasingly focuses on valve systems with embedded diagnostic capabilities and electronic integration, creating opportunities for suppliers capable of providing complete brake system solutions rather than individual components. The aftermarket expansion stems from growing vehicle parc complexity and increasing consumer awareness of brake system maintenance requirements, particularly as electronic brake systems require specialized service procedures and diagnostic equipment.

Electronic brake valve adoption in the aftermarket faces challenges from service technician training requirements and diagnostic equipment costs, creating opportunities for suppliers that provide comprehensive service support and training programs alongside their products. The channel evolution favors suppliers capable of supporting both OEM integration requirements and aftermarket service needs, as traditional component-only suppliers face margin pressure from increasing service and support demands. Regulatory compliance requirements for brake system modifications also create barriers to aftermarket electronic valve adoption, favoring suppliers with established relationships with certification bodies and regulatory expertise.

Geography Analysis

Asia-Pacific, with 41.37% revenue in 2024, commands both scale and growth Power. China’s China VII regulation compels electronic particulate-monitoring valves, while India nurtures domestic supply chains via joint ventures such as the USD 60 million Brakes India-ADVICS facility. Japan and South Korea leverage electronics expertise to lead brake-by-wire R&D, ensuring that the automotive brake valve market in the region expands at 9.20% CAGR through 2030.

North America hosts a technologically mature yet opportunity-rich landscape. The National Highway Traffic Safety Administration’s FMVSS 127 mandate embeds automatic emergency braking across new vehicles, catalyzing electronic valve adoption. Electric pickup rollouts and autonomous freight pilots spur redundant electro-pneumatic valve architectures. The aftermarket remains vibrant thanks to extensive distribution networks and aging vehicle fleets.

Europe anchors regulatory leadership with Euro 7, pushing particulate-sensing valve systems. Germany’s engineering base and Italy’s braking heritage foster agile innovation; suppliers like Brembo pioneer composite housings and sensor-rich modules. Urban freight restrictions heighten demand for low-noise, low-dust valve designs, favoring vendors with proven roadworthiness under aggressive emission and safety checks.

Competitive Landscape

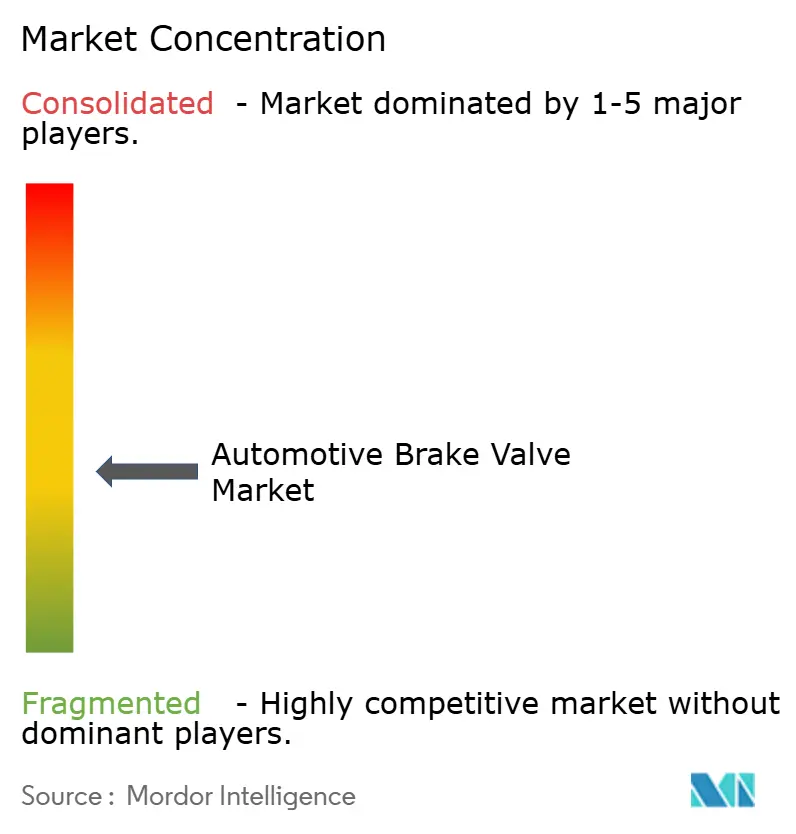

The automotive brake valve market exhibits moderate consolidation: the leading few suppliers include Bosch, Continental, ZF, Knorr-Bremse, and others contribute a significant portion of global share. Scale advantages allow these firms to invest in silicon sourcing, cybersecurity, and functional safety certification, erecting formidable barriers. Smaller hydraulic specialists pivot toward niches like motorsports or regional aftermarket supply.

Technological differentiation shifts toward software-defined braking. Continental demonstrated a dual-circuit brake-by-wire module with independent power rails, eliminating mechanical redundancy yet meeting fail-safe mandates. ZF introduced an integrated electro-pneumatic valve stack for heavy trucks, embedding Telematics gateways that stream health data into fleet dashboards. Brembo’s composite valve housings reduce unsprung mass in high-performance EVs, marrying materials science with digital sensing.

New entrants from the semiconductor realm, such as NXP and Infineon, bundle microcontrollers, pressure sensors, and networking chips into reference designs, courting tier-one integrators. Patent activity around solenoid arrays, motor-driven piston cylinders, and cloud-based brake analytics underscores an arms race to secure intellectual property positions, with over 300 valve-related patents filed between 2024-2025 alone

Automotive Brake Valve Industry Leaders

-

Robert Bosch GmbH

-

Continental AG

-

ZF Friedrichshafen AG

-

Knorr-Bremse AG

-

Aisin Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: ZF CV Systems Europe BV filed an international PCT application (PCT/EP2024/082346, published as WO/2025/114024) for a method of operating a valve assembly that activates an electropneumatic parking brake at a standstill.

- October 2024: Cummins Drivetrain and Braking Systems (CDBS), a division of Cummins Inc.’s Components segment, is significantly boosting its production capacity for air disc brakes (ADBs) and rear axles with strategic investments exceeding USD 190 million. This move highlights Cummins’ dedication to addressing the surging demand for sophisticated braking and axle solutions in the commercial vehicle arena.

Global Automotive Brake Valve Market Report Scope

| Hydraulic |

| Pneumatic |

| Electronic |

| Steel |

| Aluminum |

| Brass |

| Composite Materials |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Conventional Braking Systems |

| Advanced Braking Systems |

| Regenerative Braking Systems |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Function Type | Hydraulic | |

| Pneumatic | ||

| Electronic | ||

| By Material Type | Steel | |

| Aluminum | ||

| Brass | ||

| Composite Materials | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Technology | Conventional Braking Systems | |

| Advanced Braking Systems | ||

| Regenerative Braking Systems | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

Which valve technology is expanding the fastest?

Regenerative braking valve systems are advancing at a 12.40% CAGR as EV adoption accelerates.

Why are electronic brake valves gaining share in commercial vehicles?

Fleet electrification and telematics integration demand electronically-controlled air brakes that support predictive maintenance and energy recovery.

What material trend is disrupting traditional steel valves?

Composite housings, particularly carbon-fiber reinforced polymers, are growing 10.60% annually thanks to their lightweight and corrosion-resistant properties.

Which region offers the highest growth potential through 2030?

Asia-Pacific, already holding 41.37% share, is forecast to expand at a 9.20% CAGR owing to regulatory shifts and manufacturing scale.

How are suppliers responding to raw-material price volatility?

Leading firms hedge commodities, pursue vertical integration, and redesign valves with composite or aluminum alternatives to cushion cost spikes.

Page last updated on: