Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 21.95 Billion |

| Market Size (2031) | USD 25.47 Billion |

| Growth Rate (2026 - 2031) | 3.02% CAGR |

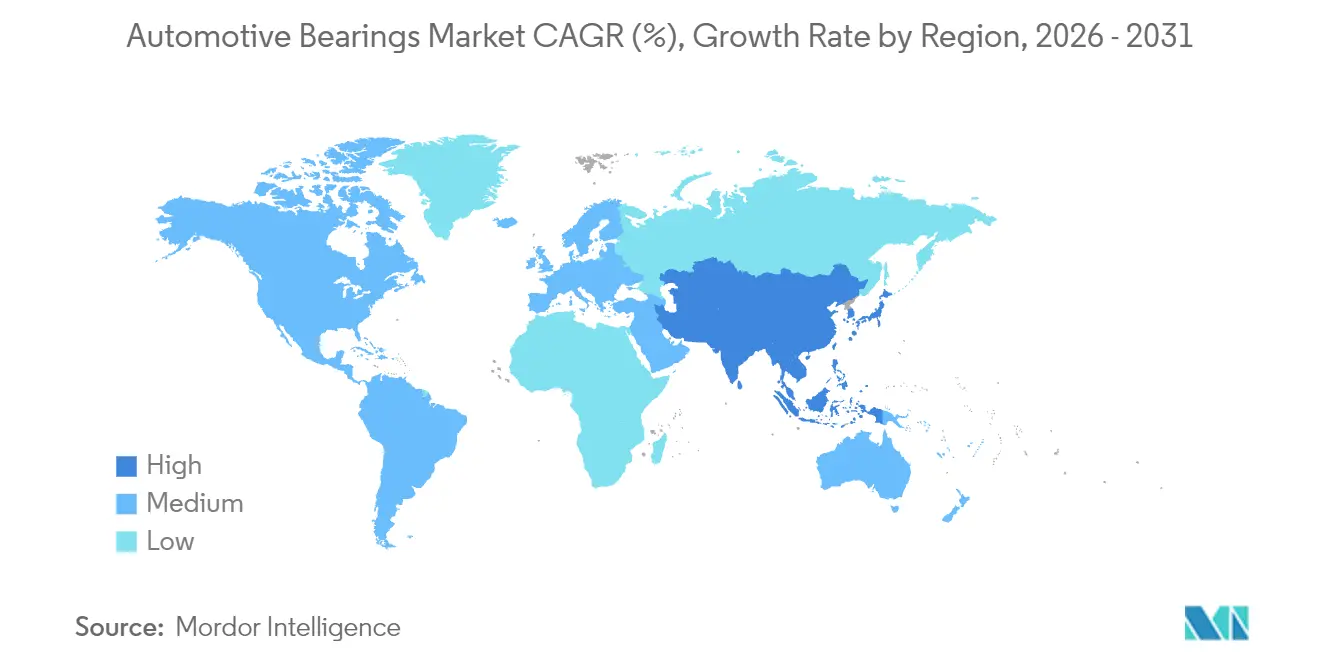

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

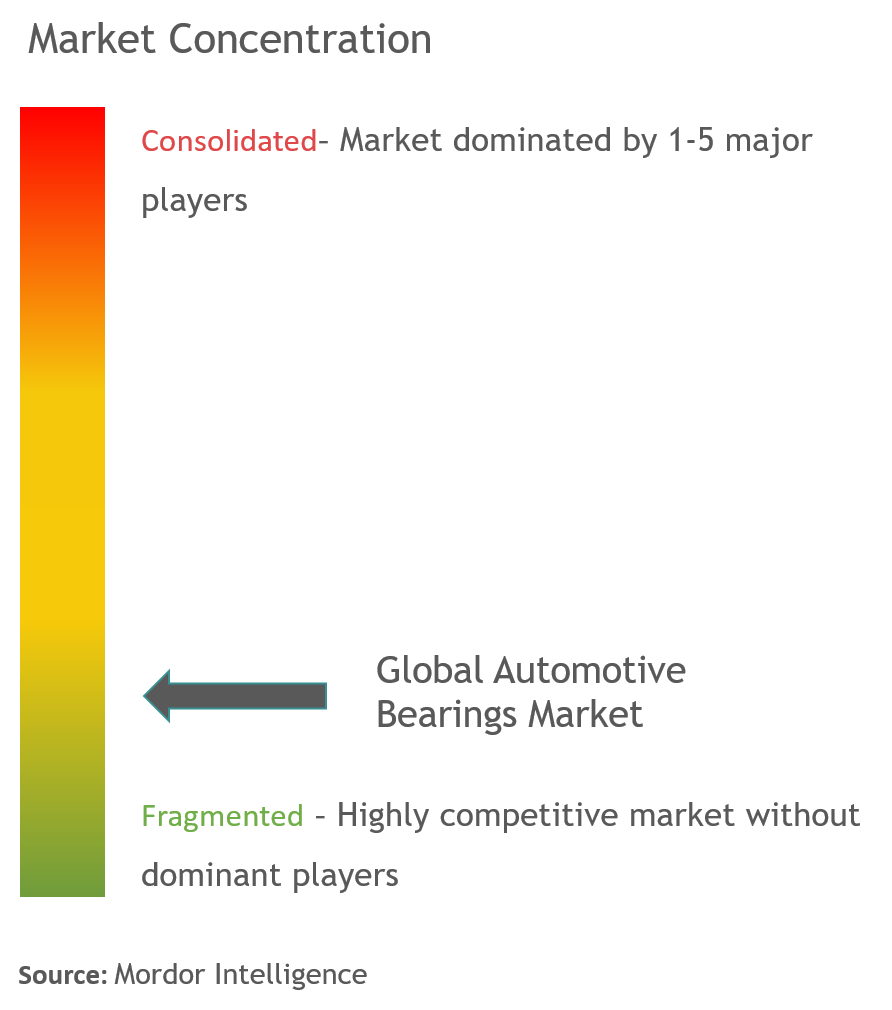

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Bearings Market Analysis by Mordor Intelligence

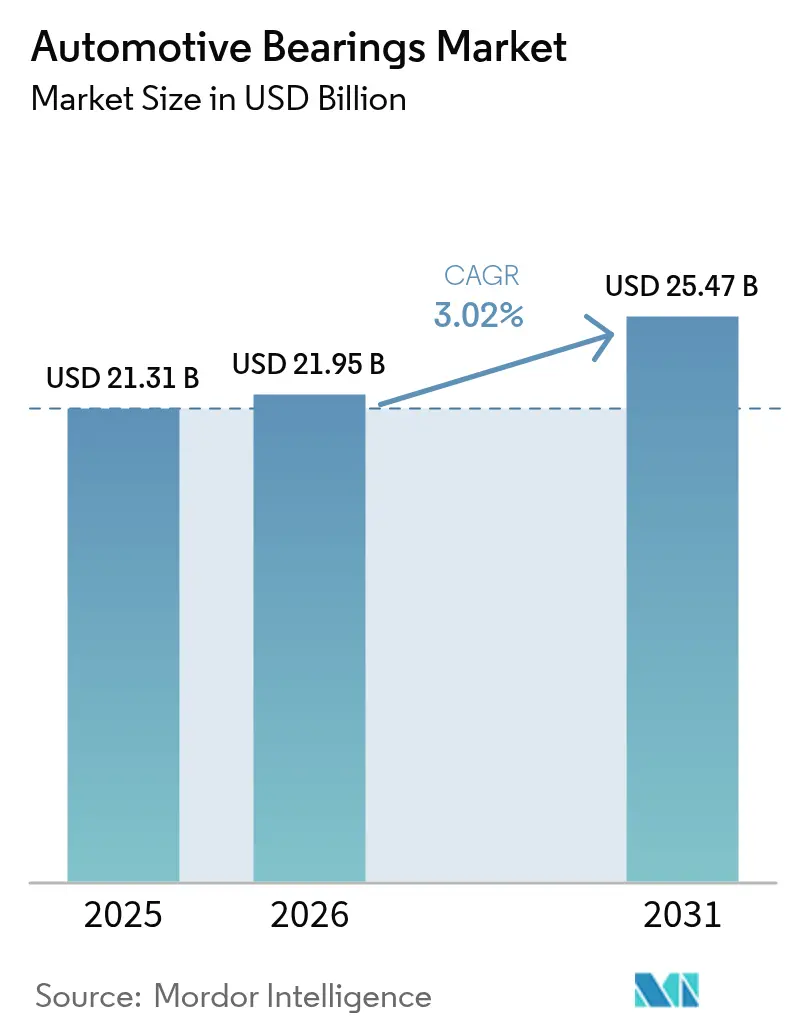

The automotive bearing market size is expected to grow from USD 21.37 billion in 2025 to USD 21.95 billion in 2026 and is forecast to reach USD 25.47 billion by 2031 at a 3.02% CAGR over 2026-2031. Rising EV output, premium pricing for insulated and sensor-integrated designs, and Asia’s outsized vehicle production collectively support topline growth even as EV driveline simplification curbs unit demand. OEMs are prioritizing compact hub units that shave vehicle weight, while integrated sensors feed ADAS controllers, locking suppliers into long-term platforms. Raw-material volatility and Section 301 tariffs inflate cost bases yet also encourage regionalized production that shields margins. Competitive intensity is shifting toward technology, with Tier-1 incumbents bundling coatings, sensors, and logistics into turnkey modules that raise OEM switching costs.

Key Report Takeaways

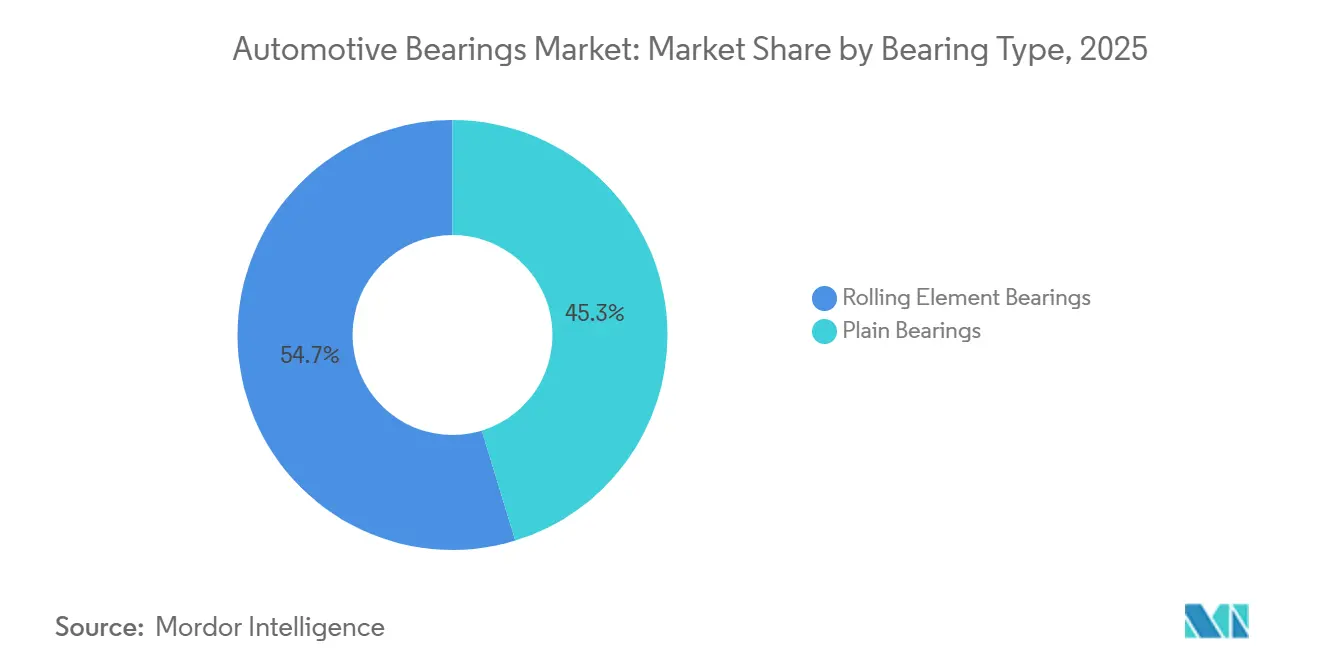

- By bearing type, rolling-element designs led with 54.72% of the automotive bearings market revenue share in 2025, and are projected to expand at a 5.38% CAGR through 2031.

- By material, steel accounted for 73.12% of the 2025 value, while ceramic and hybrid bearings posted a 6.28% growth pace to 2031.

- By vehicle type, passenger cars captured a 65.28% of the automotive bearings market share in 2025 and are advancing at 6.42% through 2031.

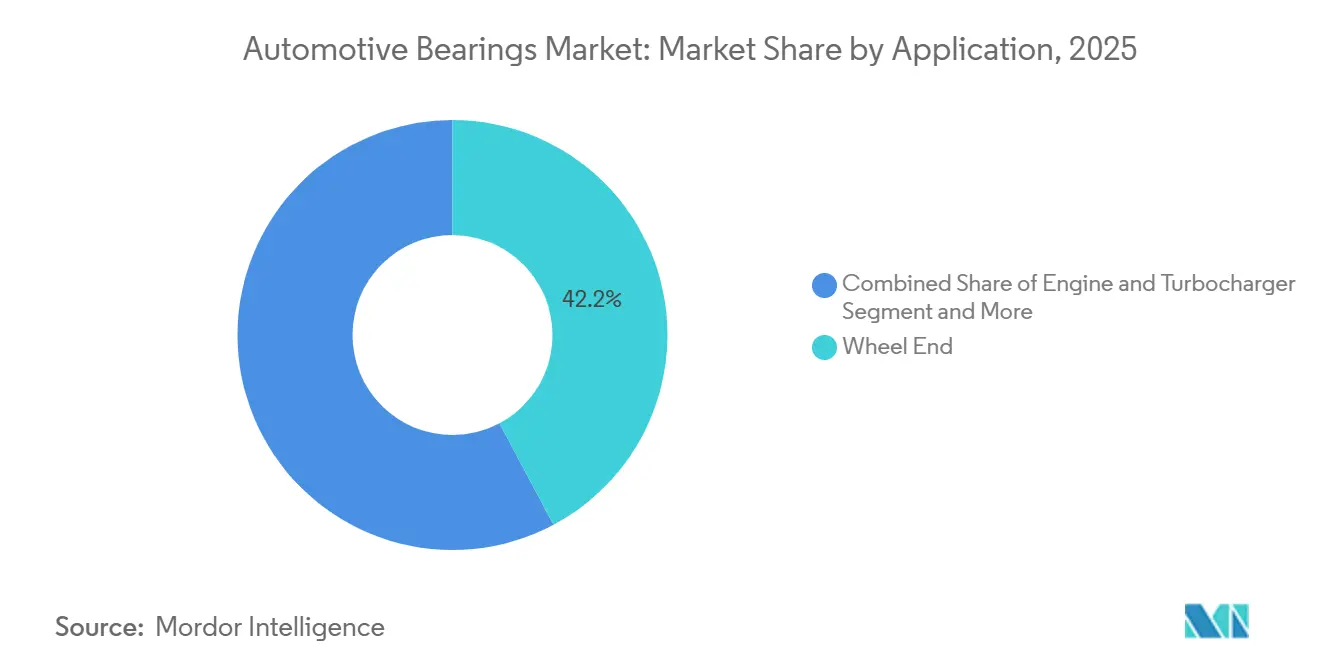

- By application, wheel-end units accounted for 42.21% of 2025 revenue; transmission and driveline remain the fastest-growing applications at a 6.39% CAGR.

- By sales channel, OEM supply accounted for 75.83% in 2025 and is growing at 5.82%, whereas aftermarket growth lags at 3-4%.

- By geography, Asia-Pacific held a 43.92% share in 2025 and is forecast to grow at 6.91%, the steepest regional rate.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Bearings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Asia's Vehicle Production Fuels Demand | +1.2% | China, India, ASEAN core, Middle East and Africa spill-over | Short term (≤ 2 years) |

| Electrification Drives E-Powertrain Bearings | +0.8% | Global focus in China, Europe, North America | Medium term (2-4 years) |

| Sensor Bearings Enable ADAS and Autonomy | +0.7% | North America, Europe, China | Medium term (2-4 years) |

| OEMs Focus on Lightweight Integration | +0.6% | Premium OEMs in Germany, Japan, South Korea | Medium term (2-4 years) |

| Aftermarket Grows with Longer Lifespans | +0.5% | North America and Europe | Long term (≥ 4 years) |

| Additive Manufacturing Boosts RPM Designs | +0.3% | Global niche, racing and performance segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Vehicle Production Growth in Asia Driving Volume Demand

China remains a dominant player in vehicle production, with India and the ASEAN corridor also contributing significantly to automotive bearing demand. India's Production-Linked Incentive scheme has been instrumental in driving capacity expansions by major manufacturers such as Maruti Suzuki and Tata Motors. In China, the market exhibits clear segmentation: coastal cities favor premium Tier-1 bearings, while inland regions prioritize cost-effective domestic brands. Japanese OEMs are increasingly relocating their production facilities to countries such as Thailand, Indonesia, and Vietnam, where labor costs are substantially lower than in coastal China. This strategic shift helps sustain production volumes in the region, even as the growing adoption of electric vehicles reduces unit requirements. Asia continues to play a pivotal role in counterbalancing global challenges, reinforcing its position as a key driver of growth in the automotive bearing market.

Electrification-Led Demand for Low-Friction E-Powertrain Bearings

EV e-motors spin near 20,000 RPM and generate stray currents that pit unprotected raceways, so OEMs now specify insulated or ceramic-hybrid bearings that extend life to warranty thresholds. SKF's eDrive series significantly reduces torque loss, enhancing driving range and influencing consumer preferences in markets where range is a critical factor [1]“eDrive Low-Friction Portfolio,” SKF Group, skf.com. Policies promoting electric vehicles have driven a notable increase in the adoption of premium e-powertrain bearings, particularly in regions with stringent environmental regulations. These developments reflect a shift in the automotive industry, with rising demand for advanced bearing solutions. Although the number of bearings per vehicle has decreased, the value of individual units has increased substantially, ensuring steady growth for the automotive bearing market.

Integrated Sensor Bearings Enabling ADAS and Autonomy

Under the EU’s General Safety Regulation, mandatory ADAS functions, such as automatic emergency braking, depend on real-time wheel-speed data from sensor bearings[2]“General Safety Regulation Text,” European Commission, ec.europa.eu. NSK offers advanced sensor variants that ensure rapid data transmission and meet high safety certification standards. In China, C-NCAP awards top ratings exclusively to vehicles equipped with electronic stability control and tire pressure monitoring, reinforcing the importance of sensor bearings even in entry-level vehicle trims. Schaeffler’s innovative encoder-in-hub design eliminates the need for separate tone rings, significantly improving assembly efficiency. With the growing adoption of Level 2+ autonomy, the automotive bearing market is seeing increased use of redundant sensing architectures. This development enhances the value of bearing content, mitigates the impact of unit attrition, and supports the growth of revenue streams.

Aftermarket Expansion from Longer Vehicle Service Life

The average United States vehicle age climbed to 12.6 years in 2024, while the EU average reached 12.1 years, expanding the pool of in-service vehicles beyond OEM warranty coverage. A longer service life widens the replacement window, even as improved sealing stretches intervals to 120,000-150,000 miles. Timken and Tenneco broadened SKU portfolios to cover platforms dating back two decades, capturing durable, higher-margin aftermarket revenue. EV penetration, however, threatens the long-term aftermarket, as fewer wear items translate into lower parts turnover after 2027. Still, in the near term, ageing ICE fleets will buoy aftermarket demand and stabilize cash flows for suppliers within the automotive bearing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Driveline Simplification Cuts Bearings | -0.9% | China, Europe, North America main EV adopters | Long term (≥ 4 years) |

| Fluctuating Alloy and Specialty-Steel Prices Squeeze Margins | -0.6% | Europe, North America, global supply chains | Short term (≤ 2 years) |

| Trade Tensions and Logistics Costs Disrupt Supply | -0.5% | US-China corridors, EU-Asia lanes | Short term (≤ 2 years) |

| Counterfeit Bearings Erode Revenues | -0.4% | Asia-Pacific, Middle East, Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV Driveline Simplification Reducing Bearing Count per Vehicle

Compared to a similar ICE sedan, a Tesla Model 3 uses significantly fewer bearings, resulting in a substantial reduction per unit. This shift underscores the broader trend of reduced component requirements in BEVs, which could lead to stagnant volumes unless offset by a premium price mix. Regions such as China and Europe have already demonstrated significant adoption of BEVs, further intensifying this challenge for the automotive bearing market. In response, suppliers are focusing on enhancing the value of each bearing by incorporating advanced features such as coatings, sensors, and ceramic elements. However, these innovations often conflict with OEM cost targets, creating additional pressure. To address the structural decline in unit demand, the automotive bearing market is increasingly relying on growth opportunities in Asia, the development of system-level modules, and sustained aftermarket demand.

Counterfeit Low-Cost Bearings Eroding OEM/Aftermarket Revenue

According to the International Anti-Counterfeiting Coalition, counterfeits significantly impact legitimate bearing revenues each year. Original equipment manufacturers (OEMs) face damaged reputations and reduced margins due to warranty claims resulting from premature failures. While SKF and NSK have introduced blockchain-traceable QR codes on their packaging, adoption remains inconsistent, particularly in markets where consumers prioritize lower initial costs. The rise in counterfeits is eroding trust in independent repair networks and reducing the aftermarket segment. This situation has created a "race-to-the-bottom" dynamic, complicating revenue forecasts for the automotive bearing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bearing Type: Rolling Element Bearings Sustain Load-Speed Superiority

Rolling elements accounted for 54.72% of 2025 revenue, supported by lower friction and higher load capacity than plain bushings, which keeps them indispensable for wheel-end, e-motor, and transmission duty cycles. Cylindrical, tapered, and needle configurations address divergent radial-axial load mixes, while deep-groove ball units dominate alternators and HVAC compressors that exceed 10,000 RPM. Schaeffler’s tapered-roller hub cartridge combines bearing, seal, and sensor, reducing assembly time by 40% and achieving quicker ISO 26262 validation. The automotive bearing market for rolling elements is projected to grow 5.38% through 2031, comfortably outpacing the overall market pace. While plain bearings remain in suspension pivots, the rise of electrification solidifies the supremacy of ceramic-hybrid ball bearings at motor shafts. Here, the constraints of high rotational speeds and the presence of electrical discharge currents preclude the use of metallic contact surfaces. As electric vehicle (EV) adoption deepens, the focus increasingly shifts towards rolling elements. Even with a decline in unit counts, this shift ensures a steady revenue stream for manufacturers, driven by the superior performance and reliability of these components.

In a related development, compact second-generation hub units are emerging that integrate preload, grease, and magnetic encoders. NSK’s latest variant achieves a significant weight reduction compared to its predecessor, without compromising durability or performance. Rigorous testing has validated its ability to withstand demanding operational conditions. The introduction of integrated seals has significantly reduced water ingress failures, enhancing the overall reliability of the units. Additionally, the inclusion of laser-etched serials improves traceability, offering a clear advantage during quality audits. Suppliers are increasingly adopting dual-sourcing strategies for key raw materials like nickel and chromium to mitigate price volatility risks. However, the design intellectual property (IP) remains a critical competitive advantage, ensuring the sustained dominance of rolling elements. As a result, rolling elements are expected to maintain their leading position in the automotive bearing market for the foreseeable future.

By Material: Steel Dominates Cost Curve, Ceramics Accelerate in Performance Niches

Steel’s 73.12% slice of 2025 value anchors the cost-sensitive volume segments served by mass-market Asian OEMs. Heat-treated 52100 alloy is widely used in the automotive industry, while silicon-nitride balls represent a more advanced, more expensive alternative. The significant cost difference between these materials underscores the challenges of achieving cost parity in low-volume ceramic production. Hybrid combinations that integrate steel rings with ceramic balls offer notable advantages, such as reduced friction and the ability to withstand extreme temperatures. These attributes make them essential for high-performance applications like turbochargers and electric motors operating at exceptionally high speeds. NSK has demonstrated the potential of ceramic balls to significantly extend component lifespans in demanding environments, encouraging broader adoption despite the higher costs. Polymer composites, including PTFE-lined sleeves, offer additional benefits by protecting fuel-pump components from corrosion and reducing noise in seat tracks, though their use remains limited to specific applications.

Material strategies in the automotive sector are evolving. Premium OEMs in regions like Europe and North America are increasingly adopting ceramic-hybrid bearings in performance electric vehicles, where energy efficiency is a critical factor. On the other hand, OEMs in emerging markets continue to rely on steel bearings due to their cost-effectiveness. The supply chain dynamics for ceramics are complex, as they depend on specialized feedstock and advanced manufacturing processes concentrated in a few key regions, which introduces potential geopolitical risks. Even so, ceramic-hybrids are on a 6.28% growth path to 2031, carving incremental value without dislodging steel’s commanding automotive bearing market size.

By Vehicle Type: Passenger Cars Anchor Demand, Commercial Fleets Diversify Mix

Passenger cars represented 65.28% of 2025 revenue and were growing at a CAGR of 6.42% through 2031, propelled by China’s million-unit output and India’s rebound. Fleet electrification in Europe and China’s dual-credit policy elevate content per car through insulated, sensorized bearings, even as overall counts slide. Light commercial vehicles (LCVs) are benefiting significantly from the growth of e-commerce. Ford's E-Transit, featuring sealed, low-friction hubs, offers extended service intervals, making it an attractive option for municipal fleet buyers who prioritize minimizing total cost of ownership. Although heavy trucks account for fewer units, they require larger bearings. The redistribution of axle loads due to battery mass has created a demand for upgraded tapered-roller bearings with higher load ratings. This specialized segment offers significantly higher margins per bearing than passenger cars, making it a lucrative area for manufacturers.

The two-wheeler market is heavily concentrated in regions such as India and Indonesia, where demand remains strong. The increasing adoption of electric scooters is driving the use of sealed bearings, which are particularly effective in preventing water ingress in areas with heavy rainfall. Meanwhile, global infrastructure investments are fueling growth in off-highway machinery, including tractors, excavators, and mining haulers. Caterpillar, a leading player in this segment, specifies triple-lip sealed rollers designed to withstand abrasive conditions, enabling suppliers to command premium pricing and improve profitability. While the automotive bearing market share for passenger cars is gradually declining as LCVs and off-highway segments grow faster, passenger cars continue to play a critical role in maintaining volume scale and leveraging platform efficiencies.

By Application: Wheel-End Units Dominate, Transmission & Driveline Lead Growth

Wheel-end hubs accounted for 42.21% of 2025 revenue because every axle requires them, and Tier-1 modules embed seals, grease, and encoders. NTN’s third-generation hub cuts assembly by 30% and eliminates preload errors, lowering warranty incidents by double digits. Yet transmission and driveline claim the fastest 6.39% CAGR on dual-clutch and CVT proliferation. These gearboxes demand multiple precision bearings, meticulously machined to sub-micron tolerances. In China, where smooth acceleration is highly valued in congested traffic, the growing popularity of dual-clutch transmissions further boosts the automotive bearing market for transmissions.

In emerging markets where internal combustion engines (ICEs) continue to dominate, engines and turbochargers play a pivotal role. Turbo ball bearings utilize ceramic balls and polymer cages to effectively manage high-temperature oil coking. As vehicle production increases, the demand for steering and suspension bearings also rises. Notably, electric power-steering columns are transitioning to ceramic-hybrid spindles, achieving reductions in both weight and noise. Meanwhile, HVAC and alternator accessories are shifting towards maintenance-free sealed units. This change aligns with OEMs' efforts to enhance the durability and efficiency of vehicle components. Overall, while some units may fade from fully electric vehicle (BEV) platforms, the diverse range of applications helps stabilize revenue streams.

By Sales Channel: OEM Contracts Provide Volume Certainty, Aftermarket Extends Lifecycle Revenue

OEM channels accounted for 75.83% of the 2025 value and are growing at a CAGR of 5.82% through 2031, bolstered by platform contracts spanning 5-8 years that lock suppliers into value-engineering partnerships. At Volkswagen and BMW, Schaeffler and SKF have embedded cross-functional teams, effectively streamlining design processes and strengthening customer retention by creating higher switching barriers.

Chinese OEMs are increasingly shifting toward domestic brands, such as ZWZ, to achieve significant cost efficiencies. This strategic move is gradually reducing the dominance of multinational companies in the automotive bearing sector. Although the aftermarket is experiencing slower growth due to enhanced product durability, which is extending replacement cycles, the aging vehicle fleet in regions such as North America and Europe is driving growing demand for maintenance and repair services. E-commerce is transforming traditional distribution channels by enabling direct-to-consumer sales through platforms like Amazon and Alibaba. However, this evolution also increases the risk of counterfeit products entering the market. Suppliers that combine advanced authentication technologies, such as QR code verification, with rapid order fulfillment, as demonstrated by Timken’s ASEAN network, are well-positioned to gain a competitive edge and expand their market presence.

Geography Analysis

Asia-Pacific owned 43.92% of 2025 revenue and is forecast to grow at a 6.91% CAGR, buoyed by China’s scale, India’s double-digit assembly additions, and ASEAN’s fast-rising supplier networks. Chinese OEMs integrate locally produced hybrid-ceramic hubs to meet EV warranty requirements, while India’s Make-in-India drive reduces import dependence from 40% to 25% by mid-decade. Government subsidies for battery electric two-wheelers broaden demand for compact deep-groove products, reinforcing the region’s contribution to the automotive bearings market.

North America sustains a sizeable share anchored by high pickup and SUV output plus a mature replacement cycle. The Biden-era tariff landscape adds USD 18 billion in annual component costs, nudging suppliers like Schaeffler to open the USD 230 million Ohio e-axle plant, thereby shortening supply chains and securing OEM approvals. Mexico’s cost-effective machining clusters attract ring-forging investments that backfill U.S. shortages, while Canada leverages raw-steel availability. The region’s aftermarket remains resilient as average vehicle age climbs past 12.8 years, propping revenue inside the automotive bearings market despite volatile new-car sales.

Europe holds a significant share of the market. However, unit demand is declining as Germany's production remains stagnant, and the United Kingdom faces challenges in maintaining its output due to post-Brexit impacts[3]“UK Car Production Data 2025,”, Society of Motor Manufacturers and Traders, smmt.co.uk. Europe wrestles with slower light-vehicle production while accelerating EV mandates that boost demand for sensor-integrated and hybrid-ceramic solutions. Germany leads R&D spending; Sweden-based SKF pilots circular-performance reclad programs that align with EU Green Deal objectives. Schaeffler’s consolidation—closing Austria’s Berndorf plant while upgrading Slovakia’s Kysuce site—highlights ongoing cost realignment. The United Kingdom, France, and Italy pursue localized e-axle builds that favor regional bearing sourcing, ensuring the continent holds strategic sway even as its share modestly contracts within the automotive bearings market.

Competitive Landscape

Global leadership remains moderately concentrated, with SKF, Schaeffler, NSK, NTN, and JTEKT claiming significant revenue. Schaeffler’s merger with Vitesco births a EUR 25 billion (USD 27.24 billion) powertrain heavyweight boasting integrated e-mobility, mechanical and mechatronic know-how that differentiates future bearing-motor assemblies. SKF adds lubrication-management scale via its John Sample Group acquisition, reinforcing lifecycle service propositions and expanding presence in India and Southeast Asia.

Innovation agendas pivot around low-friction coatings, ceramic hybrids, and innovative bearing ecosystems. NSK’s low-torque hub-unit debut reduces drag by 47 N·mm, extending EV range to compact cars. NTN deploys proprietary Servitopia cloud analytics to monitor bearing health across fleet assets, offering subscription models that shift revenue toward data services.

Rising material costs and counterfeits pressure margins, compelling alliances with steelmakers and stricter channel vetting. Additive-manufactured cages, standardized sensor protocols, and re-manufacturing plants deepen entry barriers, consolidating supply in favor of incumbents. Yet agile niche firms exploit motorsport, aerospace cross-overs, and advanced polymers to win targeted programs, preserving competitive tension within the automotive bearings industry.

Automotive Bearings Industry Leaders

JTEKT Corp.

NSK Ltd

Schaeffler AG

NTN Bearing Corporation

SKF Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: SKF India, a subsidiary of SKF, is set to expand its manufacturing capacities in Haridwar, Bangalore, and Pune. These investments are strategically aimed at catering to the surging demand for specialized bearings, pivotal for both internal combustion engines (ICE) and electric vehicle (EV) applications. Notably, the Haridwar and Bangalore facilities will hone in on bearings tailored for two-wheelers and EV powertrains.

- June 2025: NRB Bearings Limited, known for its needle and cylindrical roller bearings, unveiled key product innovations to bolster its foothold in advanced mobility and transmission sectors. Among the new offerings is a lightweight cylindrical roller bearing (CRB), treated with a specialized heat process, tailored for balancer shaft applications and planetary gearbox transmission shafts.

Global Automotive Bearings Market Report Scope

The automotive bearings market is segmented by bearing type (plain bearings and rolling element bearings), material (steel, ceramic and hybrid, and polymer and others), vehicle type (passenger cars, light commercial vehicles, heavy commercial vehicles, two-wheelers, off-highway (agriculture, construction, mining)), application/position (wheel end, engine and turbocharger, transmission and driveline, steering and suspension, and HVAC, alternator and other accessories), sales channel (OEM and aftermarket), and geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The market forecasts are provided in terms of value (USD).

By Bearing Type

| Plain Bearings | ||

| Rolling Element Bearings | Ball Bearings | |

| Roller Bearings | Cylindrical Roller | |

| Tapered Roller | ||

By Material

| Steel |

| Ceramic & Hybrid |

| Polymer & Others |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Heavy Commercial Vehicles (HCV) |

| Two-Wheelers |

| Off-Highway Vehicles (Agriculture, Construction, Mining) |

By Application/Position

| Wheel End |

| Engine and Turbocharger |

| Transmission and Driveline |

| Steering and Suspension |

| HVAC, Alternator and Other Accessories |

By Sales Channel

| OEM |

| Aftermarket |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Bearing Type | Plain Bearings | ||

| Rolling Element Bearings | Ball Bearings | ||

| Roller Bearings | Cylindrical Roller | ||

| Tapered Roller | |||

| By Material | Steel | ||

| Ceramic & Hybrid | |||

| Polymer & Others | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles (LCV) | |||

| Heavy Commercial Vehicles (HCV) | |||

| Two-Wheelers | |||

| Off-Highway Vehicles (Agriculture, Construction, Mining) | |||

| By Application/Position | Wheel End | ||

| Engine and Turbocharger | |||

| Transmission and Driveline | |||

| Steering and Suspension | |||

| HVAC, Alternator and Other Accessories | |||

| By Sales Channel | OEM | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle-East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| Turkey | |||

| Egypt | |||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Key Questions Answered in the Report

How fast is the automotive bearing market expected to grow through 2031?

Revenue is projected to rise from USD 21.31 billion in 2025 to USD 25.47 billion by 2031, reflecting a 3.02% CAGR over 2026-2031.

Which bearing type holds the largest share of global demand?

Rolling-element bearings led with 54.72% of 2025 revenue thanks to their load and speed advantages over plain bushings.

How will electrification affect bearing unit volumes?

BEVs use 40-60% fewer bearings than ICE vehicles; however, insulated and sens Schaeffler’s merger with Vitesco births a EUR 25 billion (USD 27.24 billion) variants carry 2-3× higher prices, cushioning revenue.

How are suppliers tackling counterfeit products?

Industry leaders deploy holographic labels, blockchain tracking and legal enforcement to protect revenue.

What role do sensor bearings play in ADAS adoption?

Integrated encoders deliver wheel-speed data with sub-10 ms latency, a prerequisite for ISO 26262 safety compliance and EU ADAS mandates starting 2024.

Page last updated on: