Automotive Mounted Bearing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.72 Billion |

| Market Size (2030) | USD 2.25 Billion |

| Growth Rate (2025 - 2030) | 5.54% CAGR |

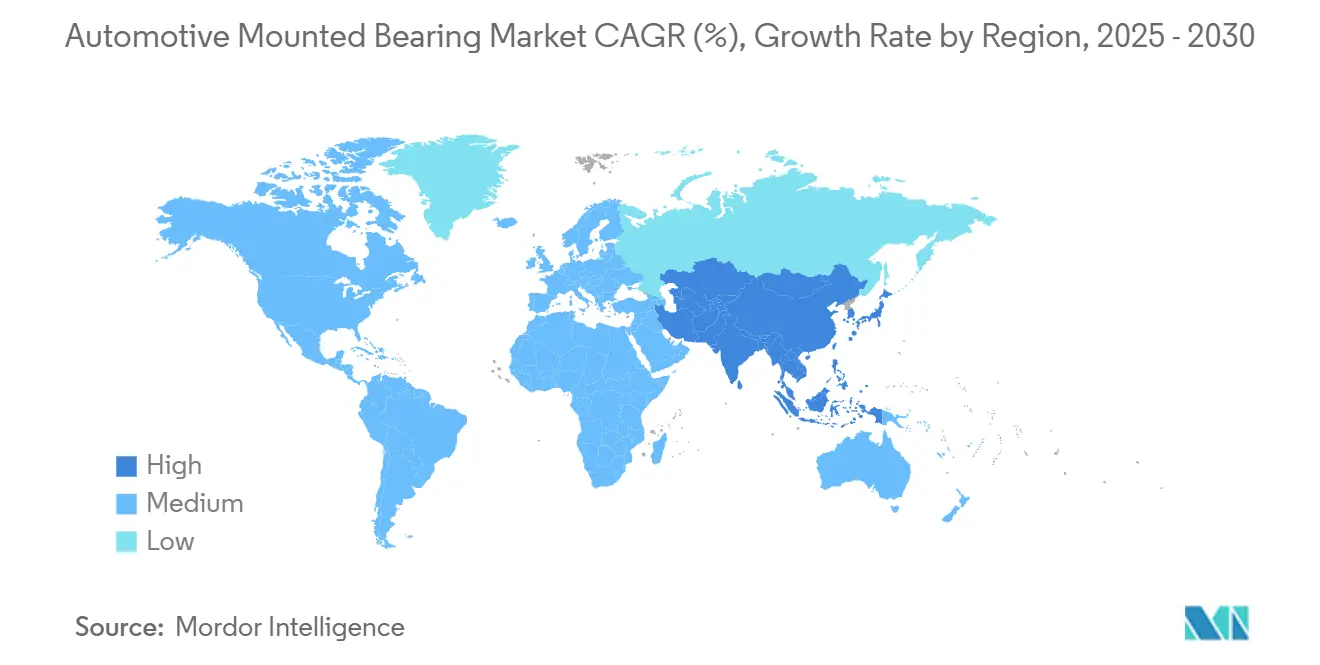

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

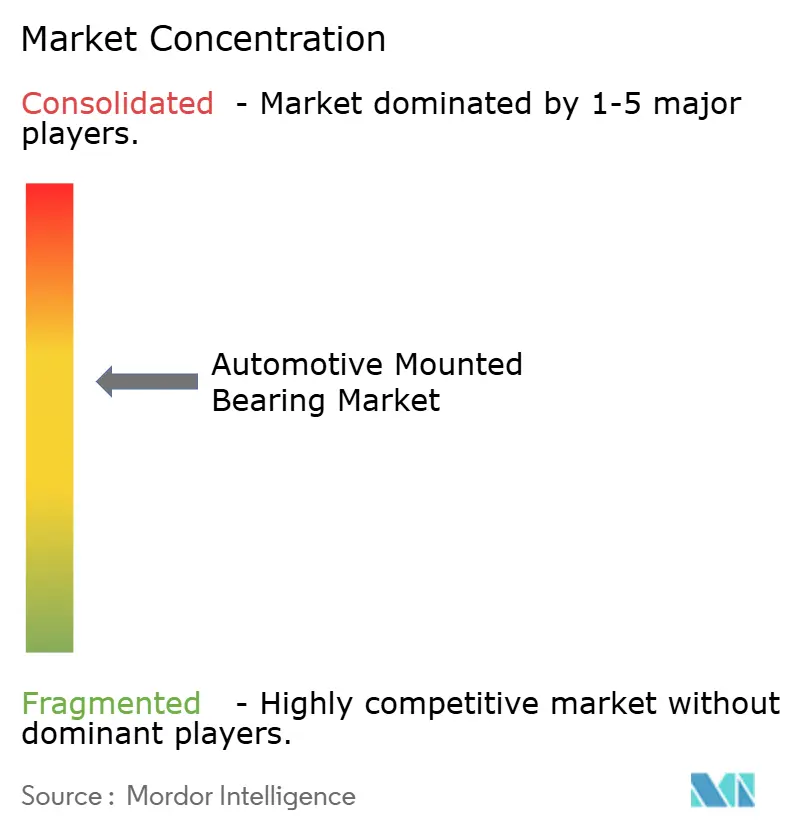

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Mounted Bearing Market Analysis by Mordor Intelligence

The automotive mounted bearings market size stands at USD 1.72 billion in 2025 and is forecast to reach USD 2.25 billion by 2030, registering a 5.54% CAGR. Robust demand from vehicle electrification, renewable energy build-outs, and factory automation continues to reshape performance expectations, pushing suppliers toward sensor-integrated, high-speed, and high-temperature solutions. Asia-Pacific retains scale leadership on the back of cost-competitive manufacturing and a widening local customer base. Meanwhile, Europe and North America defend their share through technology upgrades that embed predictive-maintenance capabilities. Roller designs attract faster adoption in heavy-duty industries requiring superior radial load capacity, even as ball bearings dominate volume. Tight raw-material markets and intensified pricing competition from low-cost Asian firms place a premium on vertically integrated supply chains and automation-enabled cost controls.

Key Report Takeaways

- By product type, ball bearings led the automotive-mounted bearings market with 61.82% of the share in 2024; roller bearings are projected to expand at a 6.23% CAGR through 2030.

- By equipment type, gearbox and transmission applications accounted for 31.73% of the automotive-mounted bearings market share in 2024, while mixer drives are advancing at a 6.18% CAGR to 2030.

- By housing type, plummer blocks held a 42.51% share of the automotive-mounted bearings market size in 2024; take-up blocks record the fastest projected CAGR at 6.12% through 2030.

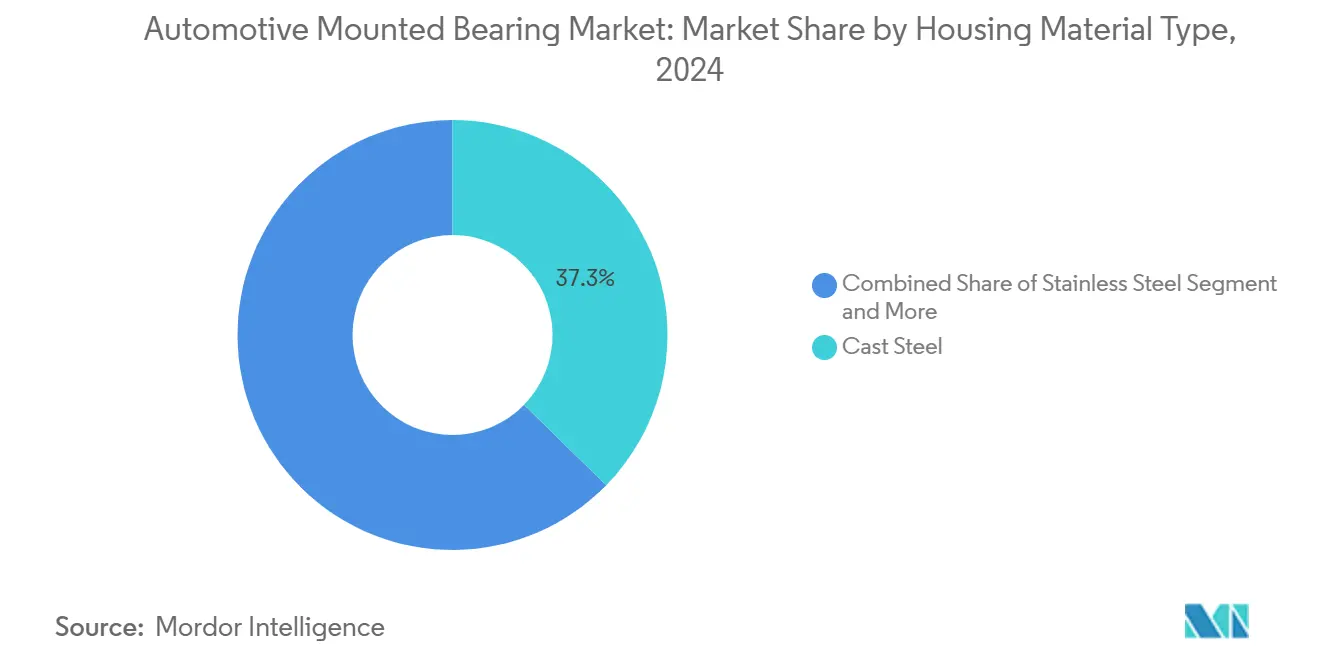

- By housing material, cast steel maintained a 37.35% of the automotive-mounted bearings market share in 2024; stainless-steel solutions are forecast to grow at a 6.83% CAGR to 2030.

- By distribution channel, OEM sales captured 73.63% of the automotive-mounted bearings market share in 2024, while the aftermarket is expanding at a 6.73% CAGR due to aging equipment fleets.

- By geography, Asia-Pacific commanded 36.31% of the automotive-mounted bearings market in 2024 and is expected to post a 6.34% CAGR by 2030.

Global Automotive Mounted Bearing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-Performance Bearings for EVs | +1.8% | North America and Europe, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Global Vehicle Production Surge | +1.2% | Global, Asia-Pacific core | Medium term (2-4 years) |

| Sensorized Bearings for Predictive Maintenance | +1.1% | North America and Europe | Medium term (2-4 years) |

| Emission and Fuel-Efficiency Regulations Driving Innovation | +0.9% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Expanding Automotive Aftermarket Demand | +0.8% | North America and Europe | Short term (≤ 2 years) |

| Lightweight Composite Bearing Housings | +0.7% | Global, automotive hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for High-Performance Bearings in Electric Vehicles

Motor speeds exceeding 15,000 RPM expose conventional cages to centrifugal forces, spark erosion, and lubrication foaming. Manufacturers respond with hybrid ceramic-steel solutions, advanced greases, and electromagnetic shielding that prevent electrical discharge machining. Firms that marry materials science with precision manufacturing upgrade the mounted bearings market landscape and earn premium margins[1]“Technical Paper on High-Speed Bearing Solutions,”, NSK Ltd., nsk.com.

Rising Global Vehicle Production Volumes

Recovering light-vehicle output reinforces demand for drivetrain, suspension, and auxiliary bearings in every central automotive region. Electric platforms amplify consumption further because each vehicle requires approximately 40–60% more rolling elements than an internal-combustion counterpart. Suppliers with flexible footprints in Mexico, Eastern Europe, and Southeast Asia gain the agility to satisfy automakers that diversify assembly networks away from single-country models. Finished-vehicle growth has a multiplier effect on the mounted bearings market[2]“Global Production Status,”, Toyota Motor Corporation, toyota-global.com.

Predictive-Maintenance Adoption of Sensorized Mounted Bearings

IoT-enabled bearings collect data on vibration, temperature, and speed, which machine learning models use to predict equipment lifespan. The collected data enables real-time monitoring of bearing performance and early detection of potential failures. This allows operators to reduce unexpected downtime and extend maintenance intervals, while manufacturers generate revenue through data analytics services. The predictive maintenance capabilities help optimize maintenance schedules, reduce operational costs, and improve overall equipment reliability. Additionally, the continuous monitoring of bearing conditions enables proactive maintenance decisions, minimizing the risk of catastrophic failures and ensuring optimal equipment performance.

Stringent Emission and Fuel-Efficiency Regulations Driving Drivetrain Efficiency

The Euro 7 emission standards and revised Corporate Average Fuel Economy (CAFE) regulations require automotive manufacturers to reduce mechanical losses in gearboxes, transfer cases, and accessory drives. These regulations aim to improve overall vehicle efficiency and reduce environmental impact. Adopting low-friction bearings with enhanced raceway geometry has expanded from automotive applications to compressors and industrial pumps, facilitating technology transfer across industries. This cross-sector implementation demonstrates the broader applicability of automotive engineering innovations in improving mechanical efficiency across various industrial applications. Regulatory certainty allows suppliers to justify multi-year capacity and R&D programs, smoothing revenue volatility otherwise typical of cyclical machinery markets[3]“Euro 7 Emission Standard Briefing,”, European Parliament, europarl.europa.eu.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility | -1.3% | Global, emerging market sensitivity | Short term (≤ 2 years) |

| Pricing Pressure from Low-Cost Asian Competitors | -0.9% | Global, commodity segments | Medium term (2-4 years) |

| Sensor Magnet Supply-Chain Risks | -0.6% | Global, China dependency critical | Medium term (2-4 years) |

| Slow Standardization of Composite Housings | -0.4% | Global, automotive focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw-Material Prices (Steel and Alloys)

Steel and specialty alloy costs represent roughly two-thirds of a bearing’s bill of materials, so monthly price swings translate directly into gross-margin variability. Tier-one suppliers mitigate exposure through hedging and multi-source contracts, but smaller firms struggle to secure volume discounts, exposing them to spot-market spikes. Prolonged volatility can slow capex plans and discourage new entrants, tightening competition in the mounted bearings market[4]“Short Range Outlook,”, World Steel Association, worldsteel.org.

Slow Standardization of Composite Housings

The automotive industry lacks standardized testing and interchangeability specifications for lightweight composites, which makes OEMs reluctant to approve these materials. The fragmented standards landscape increases validation time and tooling expenses, limiting composite adoption to small-scale programs. Automobile manufacturers face significant challenges in validating and implementing lightweight composites across their vehicle platforms without unified testing protocols and material standards. To address this challenge, suppliers are collaborating with material manufacturers and standards organizations to develop unified specifications and achieve cost efficiencies through scale. These collaborative efforts focus on establishing common testing methodologies, performance criteria, and material compatibility standards to streamline the approval process and enable broader adoption of lightweight composites in automotive applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ball Bearings Preserve Volume Leadership While Roller Demand Accelerates

Ball bearings accounted for 61.82% of the 2024 share, reflecting their versatility and lower friction profiles suitable for high-speed applications. Roller bearings, although starting from a smaller base, are forecast to advance at a 6.23% CAGR as mining, construction, and wind-turbine users seek greater radial load capacity. Hybrid designs that blend ceramic balls with precision rollers blur product boundaries, allowing suppliers to reposition portfolios without cannibalizing flagship lines.

Hybrid cages, advanced greases, and tighter tolerance classes close the historical performance gap between segments. As a result, buyers increasingly specify performance requirements rather than bearing type, giving manufacturers with multi-discipline R&D a larger wallet share across platforms. This convergence supports elevated average selling prices despite unit cost pressure from commodity producers. Market leaders integrate application engineering support to guide OEMs through trade-off decisions, improving customer retention within the mounted bearings market

By Equipment Type: Gearboxes Dominate Revenue While Mixer Drives Deliver Faster Growth

Gearbox and transmission assemblies consumed 31.73% of global bearing revenue in 2024, driven by widespread use in automotive powertrains, industrial drives, and wind-turbine yaw systems. The mounted bearings market share attached to gearbox applications benefits from design-in stickiness that lasts for the equipment life cycle. Variable-speed drives in industrial automation rely on low-friction, high-precision bearings to minimize energy losses, sustaining ASPs even amid volume fluctuations.

Though representing a smaller absolute base, Mixer drives register a 6.18% CAGR to 2030 as food, chemical, and pharmaceutical plants automate batch processes requiring hygienic and vibration-controlled bearing solutions. Suppliers that offer stainless-steel housings, food-grade lubrication, and sealed-for-life configurations secure higher margins than standard industrial SKUs. Fans, blowers, and conveyors round out mid-single-digit growth profiles. In contrast, crushers and ball mills are tied to the mining cycle around commodity pricing yet command premium pricing for heavy-load designs.

By Housing Type: Plummer Blocks Retain Scale Efficiency, Take-Up Blocks Gain Momentum

Plummer blocks held 42.51% revenue share in 2024 because maintenance teams favor their split-block design for quick bearing replacement without shaft removal. The mounted bearings market size linked to plummer blocks benefits from large installed bases in steel mills, paper plants, and aggregate operations. New product generations introduce polymer isolation and advanced sealing, improving contamination resistance and extending relubrication intervals.

Take-up blocks, often deployed on belt conveyors, post 6.12% CAGR to 2030 as e-commerce drives warehouse automation requiring longer conveyor runs and higher duty cycles. Flanged units service applications where spatial constraints dictate mounting geometry, while specialized pillow blocks address misalignment challenges in agricultural machinery. Each housing type increasingly incorporates condition-monitoring ports, aligning mechanical designs with digital-maintenance roadmaps.

By Housing Material: Cast Steel Dominates but Stainless Steel Outpaces Growth

Cast steel secured 37.35% of 2024 revenue thanks to favorable strength-to-cost ratios and well-established machining practices. Suppliers optimize metallurgical chemistry to balance toughness with machinability, ensuring dependable quality across high-volume lines. Stainless-steel housings, by contrast, represent the fastest-growing slice at 6.83% CAGR due to tighter food-safety and marine-corrosion rules. The mounted bearings market size for stainless variants is forecast to nearly double by 2030.

Composite and aluminum-titanium alloys capture attention where weight reduction and vibration damping deliver total-system gains bigger than initial price premiums. GGB’s high-load fiber-reinforced PTFE bushings illustrate how engineered polymers can outperform metals under certain static loads, opening space for disruptive competition. Material choice thus evolves from lowest cost to best lifecycle value, rewarding manufacturers with broad foundry and polymer-processing capabilities.

By Distribution Channel: OEM Still Commands Majority but Aftermarket Growth Accelerates

OEM transactions controlled 73.63% of global revenue in 2024 because design-in positions translate into guaranteed vehicle or machine life volumes. Early in the product-development cycle, project-based collaboration locks suppliers into multi-year agreements with price-escalation clauses tied to raw-material indices. Yet the aftermarket posts a faster 6.73% CAGR as industrial end-users invest in uptime and predictive-maintenance programs.

Digital storefronts, next-day fulfillment, and online technical support democratize access to premium brands, eroding historical barriers that favored local distributors. Suppliers respond by differentiating aftermarket stock-keeping units with upgraded seals or pre-filled grease, enabling price premiums that offset lower OEM margins. The resulting channel mix fosters hybrid go-to-market models that secure lifetime revenue capture within the mounted bearings market

Geography Analysis

Asia-Pacific generated 36.31% of 2024 revenue and is projected to rise at a 6.34% CAGR through 2030. China’s vertically integrated foundry-to-finish ecosystem supplies domestic customers and export programs, maintaining cost leadership even after logistics inflation. India accelerates on the back of infrastructure stimulus and a maturing automotive supply base, while Southeast Asia benefits from foreign direct investment that diversifies global value chains. Mature Japanese and South Korean manufacturers continue to export high-precision bearings for semiconductor and robotics lines, reinforcing Asia-Pacific’s end-to-end dominance.

North America maintains a technological edge in sensorized and high-load specialty bearings for aerospace, defense, and shale-gas equipment. Stringent intellectual-property regimes and Buy America provisions underpin relatively stable pricing despite lower absolute volumes. Reshoring initiatives in the United States reopen regional production lines, though workforce shortages require heavy investment in automation and workforce upskilling.

Europe balances high labor costs with engineering depth, leveraging Industry 5.0 initiatives integrating sustainability metrics into machine-tool and process-industry orders. Regulatory pressure accelerates the adoption of low-friction, recyclable, and lubricant-free designs, giving EU firms a first-mover advantage in ultra-clean manufacturing. Meanwhile, the Middle East and Africa provide greenfield potential as diversified economies invest in desalination, power generation, and bulk-material handling, where mounted bearings are mission-critical. South America’s mining and agriculture cycles remain volatile yet attractive for suppliers offering heavy-load, contamination-resistant solutions tailored to remote maintenance realities.

Competitive Landscape

The mounted bearings market exhibits moderate consolidation; SKF, NSK, and Schaeffler rely on multi-continent factory networks and deep application-engineering benches to deter new entrants. Vertical integration into steel tube, cage stamping, and heat treatment insulates gross margins from commodity price swings, a critical edge under recent raw-material volatility.

Strategic moves center on acquiring condition-monitoring expertise and additive-manufacturing capabilities. NSK’s 2025 purchase of Brüel & Kjær Vibro embeds real-time vibration analytics into mechanical offerings, while MinebeaMitsumi’s purchase of TN Linear Motion broadens precision-positioning portfolios for robotics. European houses such as JTEKT divest non-core units to streamline focus around electrified powertrain and industrial automation themes, underscoring a shift toward high-value niches rather than volume at any cost.

Asian contenders intensify price competition in standard ball-bearing SKUs by leveraging government-backed financing and lower labor overhead. To differentiate, incumbents introduce modular platforms engineered for rapid customization, shortening design-win lead times for OEM customers. Collaborative R&D hubs with universities and start-ups accelerate materials science breakthroughs, ensuring the mounted bearings market sustains a steady pipeline of incremental performance gains without dramatic technology disruptions.

Automotive Mounted Bearing Industry Leaders

SKF

Schaeffler AG

Timken Company

NSK Ltd.

NTN Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: JTEKT Corporation transferred its European needle-roller bearing operations to AEQUITA as part of its medium-term business restructuring strategy. This transfer aligns with JTEKT's efforts to optimize its operational portfolio and enhance business efficiency across European markets. The agreement encompasses the complete transfer of JTEKT's needle-roller bearing manufacturing, distribution, and service operations in Europe.

- May 2024: THK Co. Ltd. acquired Nippon Bearing Kiryu Co. Ltd., a move that indicates ongoing consolidation in the component manufacturing industry. This acquisition strengthens THK's market position and manufacturing capabilities in the bearings segment.

Global Automotive Mounted Bearing Market Report Scope

| Ball Bearings |

| Roller Bearings |

| Ball Mill Drives |

| Fans & Blowers |

| Gearbox & Transmission |

| Conveyors |

| Crushers |

| Mixer Drives |

| Others |

| Plummer Block |

| Flanged Block |

| Take-Up Block |

| Others |

| Cast Steel |

| Stainless Steel |

| Cast Iron |

| Composites |

| Others |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Ball Bearings | |

| Roller Bearings | ||

| By Equipment Type | Ball Mill Drives | |

| Fans & Blowers | ||

| Gearbox & Transmission | ||

| Conveyors | ||

| Crushers | ||

| Mixer Drives | ||

| Others | ||

| By Housing Type | Plummer Block | |

| Flanged Block | ||

| Take-Up Block | ||

| Others | ||

| By Housing Material | Cast Steel | |

| Stainless Steel | ||

| Cast Iron | ||

| Composites | ||

| Others | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the mounted bearings market in 2030?

The market is expected to reach USD 2.25 billion by 2030.

Which product type currently holds the largest share?

Ball bearings lead with 61.82% of 2024 global revenue.

Which region is forecast to grow fastest through 2030?

Asia-Pacific is set to post a 6.34% CAGR across the period.

How are suppliers addressing raw-material volatility?

Vertical integration, multi-source contracts, and hedging strategies protect margins against steel price swings.

Page last updated on: