Automotive Automatic Tire Inflation System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

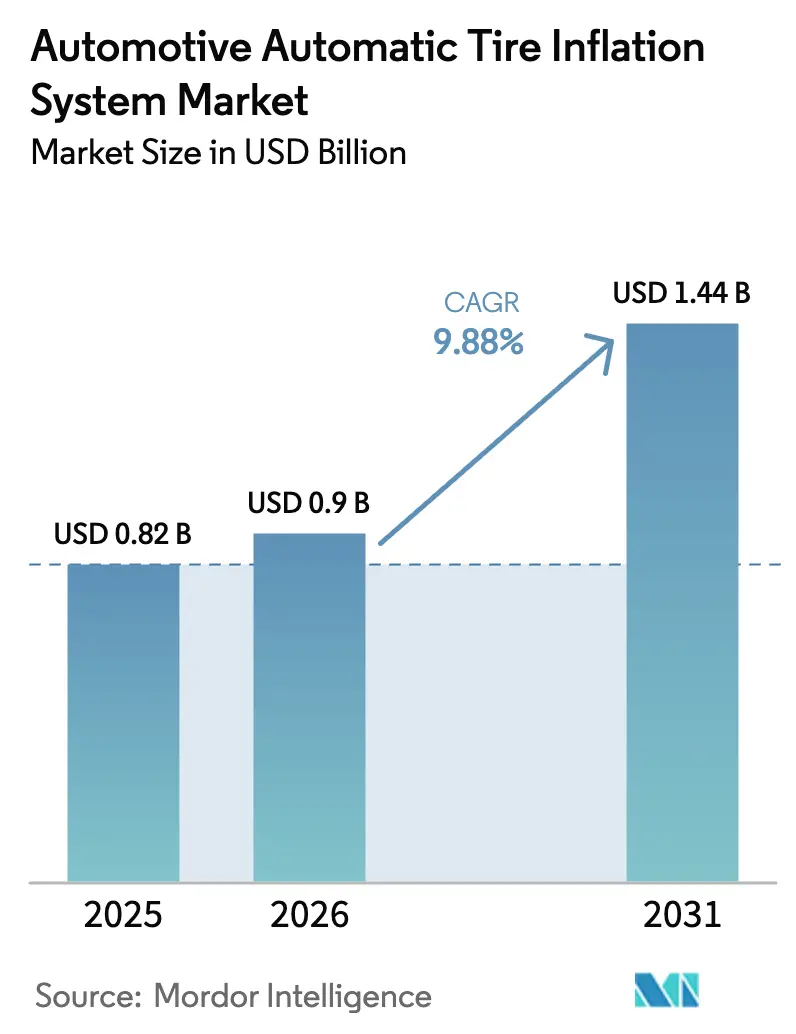

| Market Size (2026) | USD 0.9 Billion |

| Market Size (2031) | USD 1.44 Billion |

| Growth Rate (2026 - 2031) | 9.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Automatic Tire Inflation System Market Analysis by Mordor Intelligence

Automotive automatic tire inflation system market size in 2026 is estimated at USD 0.9 billion, growing from 2025 value of USD 0.82 billion with 2031 projections showing USD 1.44 billion, growing at 9.88% CAGR over 2026-2031. Growth reflects coordinated safety regulations, fleet cost-reduction imperatives, and tighter integration with connected-vehicle architectures. North American fleets must comply with 49 CFR 393.75 cold-inflation rules, while the European Union’s General Safety Regulation II requires tire-pressure monitoring across all new vehicles, indirectly cementing demand for fully automatic inflation capabilities. Commercial fleets realize up to 1.4% fuel savings when tires remain at correct pressure, sharpening return on investment for automatic systems [1] “Tire Pressure Best Practices, ” North American Council for Freight Efficiency, nacfe.org. In parallel, agricultural and construction equipment makers embed central pressure control to meet soil-conservation mandates and precision-farming needs, as seen in Fendt’s VarioGrip that varies pressure from 8.7 to 36.3 PSI while in motion. Investment momentum is buoyed by venture funding, illustrated by Aperia Technologies’ USD 45 million raise that targets hub-mounted self-powered inflators.

Key Report Takeaways

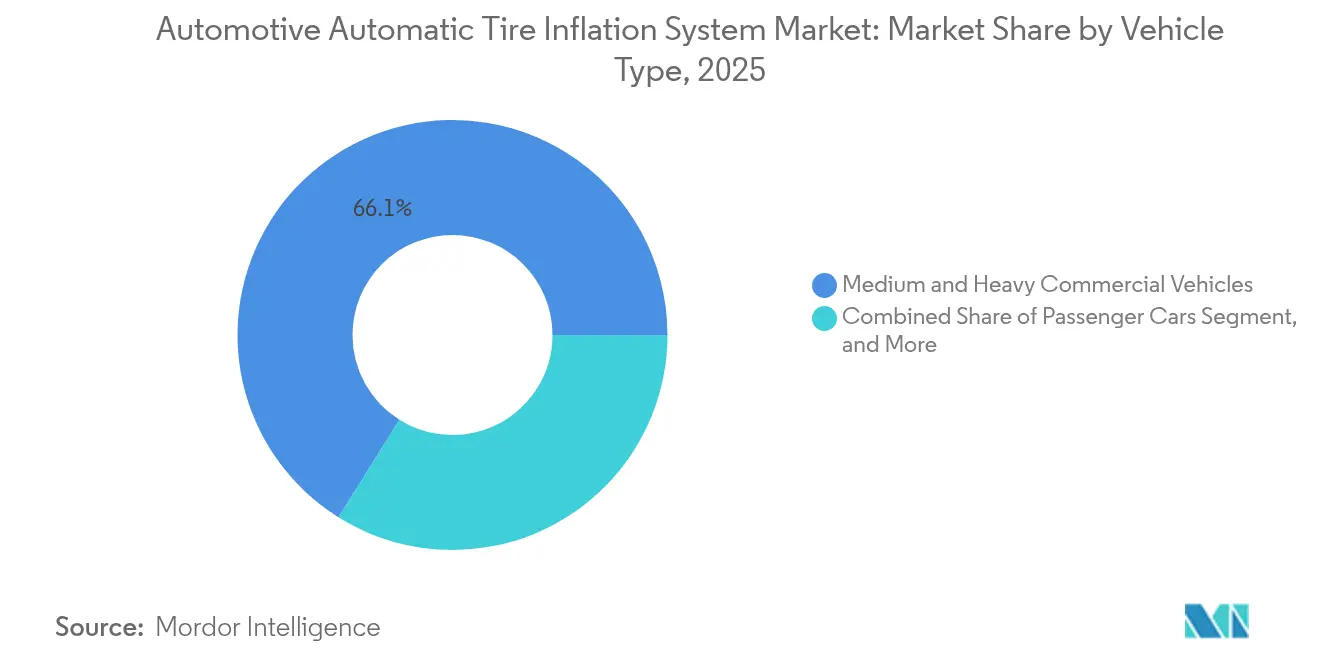

- By vehicle type, medium and heavy commercial vehicles led the automotive automatic tire inflation system market with a 66.10% revenue share in 2025; off-highway vehicles are projected to expand at an 11.43% CAGR through 2031.

- By application, on-road tires accounted for 71.65% of the automotive automatic tire inflation system market size in 2025, while off-road tires are advancing at a 11.90% CAGR to 2031.

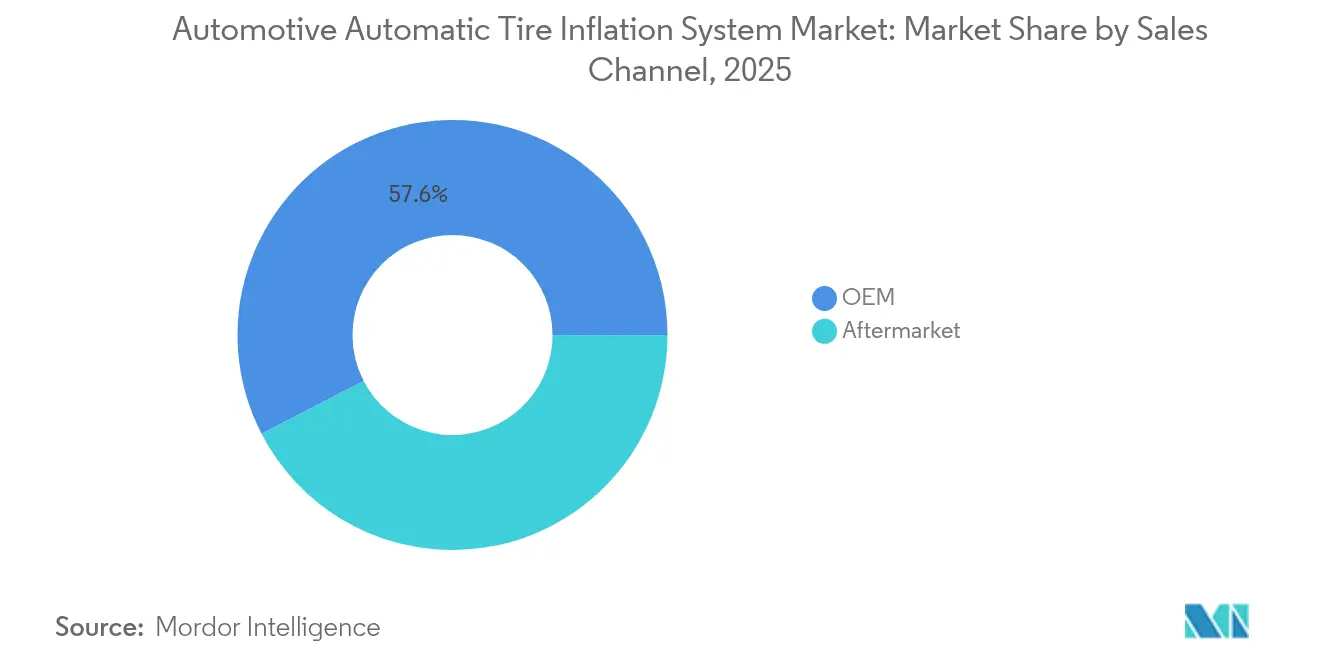

- By sales channel, the OEM segment held 57.60% of the automotive automatic tire inflation system market share in 2025; the aftermarket channel records the highest projected CAGR at 11.15% through 2031.

- By product type, central tire inflation systems led the automotive automatic tire inflation system market, capturing 61.40% revenue share in 2025; self-powered hub inflators are forecast to grow at a 12.25% CAGR.

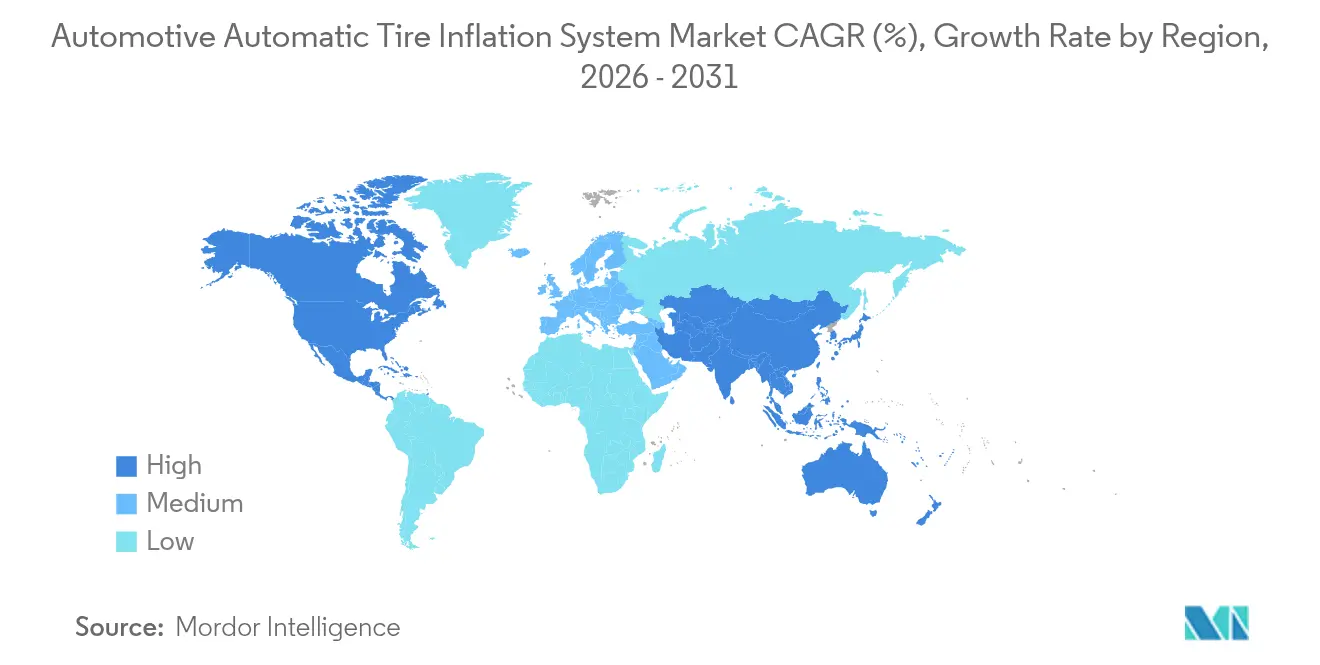

- By geography, North America dominated the automotive automatic tire inflation system market with 39.25% share in 2025, while Asia-Pacific is forecast to grow at a 11.78% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Automatic Tire Inflation System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet Focus on Fuel and Tire-Wear Cost Reduction | +2.8% | Global, strongest in North America and Europe | Medium term (2–4 years) |

| Stringent Tire-Safety Regulations | +2.1% | Global, early uptake in North America and EU | Short term (≤ 2 years) |

| Expanding Commercial-Vehicle Parc and Freight Activity | +1.9% | Asia-Pacific core, spill-over to MEA | Medium term (2–4 years) |

| OEM Integration with TPMS and Connected Platforms | +1.7% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Autonomous-Trucking Demand for Predictive Tire Health | +1.2% | North America and EU, pilot programs in APAC | Long term (≥ 4 years) |

| Agricultural Shift to On-the-Go Soil-Conserving Pressure Control | +0.6% | Global, concentrated in agricultural regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Fleet Focus on Fuel and Tire-Wear Cost Reduction

Tire expenditures represent 15–20% of heavy-truck operating budgets, and under-inflation generates up to 95% of roadside tire failures. Pressure Systems International quantifies 1.4% mean fuel gains and 10% tire-life extension when automatic inflation is installed [2]” Cummins Inc., “Automatic Inflation Efficiency Study, cummins.com. Data-rich platforms deliver live pressure, temperature, and load information, letting dispatchers optimize speed profiles and maintenance windows. Long-haul carriers accrue the greatest absolute benefit because incremental savings compound across annual mileages that exceed 120,000 miles per tractor. Consequently, procurement teams embed total cost-of-ownership models that prioritize automatic inflation during tractor and trailer replacement cycles.

Stringent Global Tire-Safety Regulations

Worldwide statutes are elevating tire-maintenance discipline. The EU General Safety Regulation II, effective July 2024, mandates tire-pressure monitoring on every newly homologated vehicle category except M1, creating a universal baseline that encourages automatic inflation upgrades. Complementary Euro 7 rules set tire-abrasion caps with 2032 compliance deadlines [3] “Euro 7 Proposal Briefing, ” International Council on Clean Transportation, theicct.org. In the United States, Federal Motor Carrier Safety Administration inspectors enforce cold-inflation minimums during roadside checks, prompting large fleets to deploy automated systems to avoid citations. Similar provisions are cascading into South America and Southeast Asia as export-oriented OEMs harmonize with EU standards. As a result, fleet managers perceive automotive automatic tire inflation system market adoption as a compliance necessity that also unlocks operational savings.

Expanding Commercial-Vehicle Parc and Freight Activity

Asia-Pacific truck registrations continue to climb with e-commerce and infrastructure outlays. Heavy-duty fleets in India seek efficiency tools to curb fuel use that drives 12% of national energy-related CO₂ emissions. Regional OEMs now bundle integrated tire management with connected dashboards on battery-electric and gas-powered rigs, mindful that rolling resistance erodes driving range. Governments incentivize adoption through green-freight programs that score fleets on energy intensity, effectively nudging operators toward automotive automatic tire inflation system market solutions.

OEM Integration with Advanced TPMS and Connected Platforms

Manufacturers move beyond standalone modules toward holistic tire intelligence. Continental’s ContiConnect stitches pressure and temperature data into drive-line diagnostics, enabling predictive alerts that slot into existing telematics workflows. TDK partners with Goodyear to embed multi-axis MEMS sensors inside tire cavities, widening datasets for load estimation and tread-wear analytics. Integrated architectures raise switching costs for fleets and sideline niche vendors that lack deep software stacks. Over the long term, converged platforms will dominate the automotive automatic tire inflation system market as autonomy features rely on continuous tire-health assurance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost and Integration Complexity | -1.8% | Global, sharper in emerging economies | Short term (≤ 2 years) |

| Reliability and Maintenance Issues in Harsh Duty Cycles | -1.2% | Global, intense in off-highway segments | Medium term (2–4 years) |

| Limited Global Aftermarket Service Ecosystem | -0.9% | Global, acute in emerging markets and rural areas | Medium term (2–4 years) |

| Cyber-Security Vulnerabilities in Connected ATIS | -0.7% | Global, concentrated in connected vehicle applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Integration Complexity

System packages range from USD 1,500 to USD 5,000 per vehicle. Retrofit projects add labor hours and potential downtime that many small carriers cannot absorb. Commercial tire dealers note budget-constrained operators delaying upgrades until capex cycles align, even though break-even analysis often shows payback inside 18 months. Training technicians, calibrating sensors, and harmonizing software with legacy electronic control units further slow adoption in price-sensitive regions.

Reliability and Maintenance Issues in Harsh Duty Cycles

Mining, forestry, and military vehicles face vibration, debris, and temperature swings that stress valves, compressors, and harnesses. Field reports show a higher failure rate compared to on-road tractors, leading to unplanned downtime and increased spare parts costs. Remote project sites lack specialized service centers, forcing fleet managers to keep inventory and train staff on-site, which reduces the total cost benefits offered by the automotive automatic tire inflation system industry. Vendors that ruggedize components and simplify service routines will gain market share in these demanding sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Dominance Drives Market Evolution

Medium and heavy commercial vehicles accounted for 66.10% of the automotive automatic tire inflation system market revenue in 2025, underscoring the sector’s outsized influence on the automotive automatic tire inflation system market. Elevated annual mileage, multi-axle configurations, and fuel-spend sensitivity combine to produce compelling investment cases for automatic inflation. Remote diagnostics and over-the-air pressure calibration let dispatchers minimize roadside service calls and preserve delivery schedules. Adoption is now filtering into regional haul and final-mile trucks as OEMs standardize inflation ports and data protocols across model lines. Off-highway equipment exhibits the sharpest trajectory at an 11.43% CAGR through 2031. Precision agriculture mandates gentle soil loading to protect yield, while construction and military vehicles require fast adjustments between asphalt, gravel, and mud. Fendt’s in-cab VarioGrip toggles pressure inside seconds, boosting tractive efficiency and cutting compaction, and similar offerings from John Deere and CNH Industrial signal an industry shift toward embedded pressure control. Light commercial vans and passenger cars participate more modestly, yet EU safety rules and consumer preference for advanced driver-assistance features are nudging OEMs to incorporate scaled-down automatic inflation modules.

By Application: On-Road Dominance with Off-Road Growth Acceleration

On-road tires secured 71.65% of the automotive automatic tire inflation system market revenue in 2025, anchored by cross-continental trucking, where under-inflation steals fuel economy on every highway mile. Automated systems continuously regulate cold-inflation levels regardless of ambient swings that might lead to chronic under-pressure in conventional weekly-check routines. Fleet telematics dashboards integrate pressure KPIs alongside hours-of-service readouts, and managers benchmark depots on compliance percentages that correlate directly with diesel spend. Off-road tires are climbing at a 11.90% CAGR, reflecting investment in smart machinery for quarrying, forestry, and agriculture. Michelin’s central system posts up to 4% productivity lifts and 10% fuel savings by tailoring pressure to soil type. Studies show that correct pressure can trim soil compaction depth by one-third, preserving arable land and reducing tillage energy. Similarly, wheel-loader operators report lower tire-related downtime after installing closed-loop inflation that alerts them before sidewall pinch damage occurs. These benefits cement future demand even as upfront pricing remains a barrier for smaller contractors.

By Sales Channel: OEM Integration Shifts Market Dynamics

The OEM pathway captured 57.60% revenue of the automotive automatic tire inflation system market in 2025, illustrating how automatic inflation is becoming an integral chassis subsystem. Heavy-duty brands such as Daimler Truck and Volvo Group bundle inflation kits on premium trim levels, and trailer manufacturers follow suit to differentiate equipment in a saturated leasing market. OEM integration ensures wiring harnesses and electronic control units are factory-matched, reducing warranty disputes. Aftermarket uptake, growing at 11.15% CAGR, addresses the immense installed base of tractors and trailers already on the road. Independent service dealers broaden portfolios to include inflation installation, calibration, and telematics configuration. The automotive automatic tire inflation system market size for retrofit kits benefits from modular hub designs that require no compressor plumbing, shrinking installation windows. However, retrofit complexity still rises on vehicles older than 10 years that lack CAN bus gateways, compelling distributors to offer bundled hardware-plus-installation financing to accelerate close rates.

By Product Type: Center Tire Inflation System (CTIS) Leadership with Hub-Inflator Innovation

Central tire inflation systems held 61.40% revenue share of the automotive automatic tire inflation system market in 2025 because they deliver full-vehicle coverage and integrate easily with onboard air lines. Multi-channel controllers manage steer, drive, and trailer axles concurrently, supplying balanced pressure that curbs irregular wear patterns and enhances braking stability. Self-powered hub inflators register the fastest CAGR of 12.25%. Aperia’s Halo harvests wheel rotation to energize a miniature pump, eliminating airlines and reducing potential leak points. Continuous wheel-end inflators straddle the middle ground, appealing to fleets that desire simplicity without giving up per-wheel regulation. Product selection often hinges on fleet mix: tractors with frequent trailer swaps favor hub devices for ease of installation, while dedicated vocational trucks lean toward CTIS to accommodate wide operating-pressure bands.

Geography Analysis

North America secured 39.25% revenue of the automotive automatic tire inflation system market in 2025, buoyed by well-defined regulatory frameworks and mature telematics penetration. Federal enforcement of tire-pressure rules prompts carriers to adopt automatic solutions as insurance against roadside fines. Large for-hire fleets cite 1–3% diesel savings and 15–20% tire-life gains, outcomes that reinforce board-level sustainability pledges. The region also hosts expansive pilots for driverless freight corridors, and autonomous developers require redundant tire-health systems that remove the driver from the maintenance loop. Asia-Pacific posts the quickest ascent at 11.78% CAGR through 2031. Explosive e-commerce shipping volumes, extensive highway build-outs, and the push for electrified powertrains sharpen the economic rationale for automatic inflation. India’s logistics overhaul seeks to trim the 12–14% GDP drain tied to freight costs, and correcting tire pressure is a visible lever. Chinese OEMs such as FAW and Sinotruk integrate inflation valves on new energy trucks to extend battery range, positioning the automotive automatic tire inflation system market as a standard efficiency measure. Europe remains consistent, guided by Union-wide safety and environmental directives. Regulation II obliges TPMS on every new vehicle, and Euro 7 introduces abrasion limits that depend heavily on optimum pressure. Operators in Germany and France combine inflation data with carbon reporting to satisfy customer Scope 3 disclosure requests. The Middle East and Africa trail in overall penetration, yet oil-exporting economies funnel infrastructure funds into vocational fleet upgrades, which lifts baseline demand even if service-center density lags.

Regulatory Landscape

The regulatory environment shaping automotive automatic tire inflation system (ATIS) adoption is anchored by tire-pressure monitoring requirements and commercial-vehicle safety enforcement. In the United States, NHTSA administers FMVSS 138 (49 CFR 571.138), which sets performance requirements for tire pressure monitoring systems (TPMS) on passenger vehicles and light trucks (within the standard scope). This creates a baseline for continuous pressure awareness that supports OEM integration paths for automatic pressure maintenance. For commercial operations, roadside enforcement of tire condition and inflation-related defects under programs aligned with Federal Motor Carrier Safety Administration practices keeps fleet attention on solutions that reduce under-inflation risk and associated violations.

Internationally, UNECE vehicle regulations provide a harmonization pathway across many markets that type-approve vehicles under WP.29. UN Regulation No. 141 (TPMS) is a key reference point, and in April 2026 UNECE WP.29 GRBP advanced a proposal (Supplement 3 to the 01 series of amendments to UN R141) that includes testing and procedural provisions for vehicles with automated driving systems, plus specific considerations for towed vehicles. The proposal also references how central tire inflation systems (CTIS) and tire pressure refill systems are treated within testing procedures. These updates reinforce the need for ATIS suppliers to align inflation and refill functionality, deactivation behavior in test modes, and system diagnostics with evolving type-approval expectations.

Value Chain Analysis

The ATIS value chain starts with upstream component suppliers providing compressors (where applicable), rotary unions, seals, high-precision valves, pressure and temperature sensors, electronic control units, wiring/connectors, and ruggedized air-line hardware for on-road and off-highway duty cycles. Midstream, ATIS system manufacturers and integrators package these into CTIS, wheel-end inflators, and self-powered hub inflators, increasingly bundling embedded software and data services. Industry standards and validation practices for maintenance-type systems in medium and heavy-duty highway applications shape design choices for pressure correction behavior, diagnostics, and test methods, including through standards such as SAE J2848/2.

Downstream, OEM fitment channels (truck, trailer, and off-highway equipment manufacturers) drive a major share of installations, supported by partnerships with axle, wheel-end, and chassis subsystem suppliers to simplify factory integration. Aftermarket routes run through fleet service networks, tire dealers, and installers that handle retrofits and calibration, with telematics providers and fleet-management platforms becoming more visible as ATIS data is integrated into maintenance workflows. Key bottlenecks and cost drivers typically cluster around durable wheel-end sealing and sensing reliability in harsh environments, compressor and valve availability for centralized architectures, and software integration with vehicle networks and connected platforms, which together affect total installed cost and serviceability across regions.

Competitive Landscape

The automotive automatic tire inflation system market features moderate fragmentation. Continental AG, Bridgestone Corporation, and Pressure Systems International leverage vertical integration, blending tires, sensors, and cloud analytics to secure lifecycle contracts with global fleets. Continental’s ContiConnect couples pressure and temperature inputs with predictive algorithms that issue maintenance work orders directly to depot systems.

Aperia Technologies occupies the innovation vanguard with its self-powered Halo platform, attracting USD 45 million in growth capital in 2023 to scale production. Hub-centric design sidesteps brake-chamber airlines, simplifying retrofits and positioning the firm as a preferred solution for trailer leasing companies that shun complex plumbing. Pressure Systems International partners with axle makers to factory-fit its systems, assuring OEM pull-through and a sizeable installed base ripe for software-upgrade subscriptions.

Cybersecurity emerges as a differentiation axis. Rutgers University demonstrated that inflated wireless packets can spoof legacy TPMS lacking cryptographic signatures. Vendors race to embed authenticated messaging and intrusion detection, reassuring fleet operators who manage mixed telematics stacks. Players that deliver end-to-end encrypted architectures without sacrificing battery life will gain procurement advantages, particularly among autonomous and high-value cargo haulers.

Automotive Automatic Tire Inflation System Industry Leaders

Aperia Technologies, Inc.

Meritor, Inc.

Pressure Systems International, Inc.

Dana Incorporated

STEMCO Products Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Commercial fleet compliance and uptime incentives continue to open whitespace for ATIS retrofits and deeper integration with digital maintenance workflows. A concrete catalyst is the Commercial Vehicle Safety Alliance (CVSA) update effective April 1, 2024 to the North American Standard Out-of-Service Criteria, which allows certain non-steering tires with tread-area leaks to remain in service when a functional ATIS maintains pressure above a defined threshold. This directly links ATIS presence to fewer roadside service interruptions and inspection outcomes, offering fleets a clearer adoption pathway that is tied to out-of-service risk, especially in high-mileage trailer and tractor operations where maintaining correct pressure supports fuel and tire-wear economics.

Technology and product roadmaps also point to opportunity in software-defined tire intelligence and simplified sensor integration, which can reduce retrofit complexity while expanding diagnostic value. In 2026, Michelin publicized a software-enabled tire digital twin approach that leverages existing in-vehicle data to infer tire state, and Continental Tires Americas introduced Sensor Ready commercial tires with integrated sensor pockets to ease deployment of digital tire ecosystems. These developments support more scalable coupling between monitoring and automatic inflation. On the standardization side, SAE J2848/2 provides a clearer engineering and validation baseline for maintenance-type ATIS on medium and heavy-duty vehicles, helping procurement teams compare systems on consistent performance criteria. Overall, these proof points support opportunities for vendors that bundle ATIS hardware with telematics integration, inspection-friendly features, and service models aligned to both OEM and aftermarket channels.

Recent Industry Developments

- March 2026: Aperia Technologies introduced a Halo automatic tire inflation offering for steer tires, expanding its coverage beyond traditional trailer-focused applications to include safety-critical wheel positions. Broadening ATIS capability across all wheel positions strengthens full-vehicle standardization opportunities for fleets and OEM spec packages.

- March 2025: Aperia Technologies entered an exclusive partnership with Goodyear to connect Halo Connect i3 with Goodyear's Tires-as-a-Service platform. The tie-up pushed ATIS further into bundled tire-and-service programs where monitoring, maintenance actions, and inflation performance are managed as a unified offering.

- August 2024: Freudenberg Sealing Technologies unveiled central tire inflation seals designed to self-adjust across terrain changes. Improved sealing performance targets durability and leakage reduction, which addresses reliability concerns that can limit CTIS adoption in harsh-duty operating cycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers automatic tire inflation systems used on vehicles to keep tire pressure within a set range during operation, using air supply hardware and control logic that can add air when pressure drops.

Scope exclusions: It does not include standalone tire inflators or tire pressure monitoring only systems that do not actively inflate tires.

Segmentation Overview

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- Off-Highway Vehicles (Agricultural, Construction, Military)

- By Application

- On-the-Road Tires

- Off-the-Road Tires

- By Sales Channel

- OEM

- Aftermarket

- By Product Type

- Central Tire Inflation Systems (CTIS)

- Continuous/Wheel-End Inflators

- Self-Powered Hub Inflators

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping where ATIS demand shows up, and then collecting a small set of dependable public indicators that can be tracked every year. We mainly use sources such as US DOT and NHTSA material on tire safety, US EPA fuel economy-related datasets, Eurostat vehicle and freight statistics, UN Comtrade trade flows for relevant pneumatic parts, and SAE technical papers that describe system architectures and use cases.

These sources are then supplemented with company filings, investor presentations, product literature, and reputable press coverage to clarify adoption timing for commercial fleets and off-highway equipment. In a few cases, paid subscriptions are used for company financials and intelligence, patent databases, and shipment-level import and export checks to confirm component movement and supplier activity. The desk research sources listed here are illustrative, and we also reviewed additional public references for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focuses on validating what portion of commercial and off-highway vehicles typically fit ATIS, and how OEM and aftermarket mixes shift by region and vehicle duty cycle. We speak with system and component stakeholders, fleet maintenance leaders, and channel participants across APAC, EMEA, and the Americas so the assumptions around pricing, replacement rates, and penetration can be stress-tested before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | APAC: 47% |

| Mid tier: 52% | Functional/Unit leaders: 38% | EMEA: 31% |

| Smaller Players: 15% | Managers: 49% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool, where commercial and off-highway vehicle parc and new sales are translated into an addressable fitment base using penetration assumptions for ATIS-ready applications. Those totals are then converted to value using typical system price ranges and expected replacement timing for key wear parts, followed by a split across OEM and aftermarket based on buying patterns discussed in interviews.

To keep the model grounded, we track inputs such as medium and heavy commercial vehicle production, off-highway equipment activity signals, fleet utilization patterns, safety and maintenance emphasis around tire upkeep, and the share of vehicles that run long-haul or harsh-terrain duty cycles. We also run a selective bottom-up check to sense-check the headline number, based on sampled supplier revenues, channel checks on average selling prices, and installed-base logic in a few higher-adoption countries. Where company disclosures are limited, gaps are handled by using peer averages and adjusting for product focus and region exposure.

For forecasting, scenario analysis is applied, and the scenarios are anchored to how fast ATIS penetrates fleets, how pricing moves with electronics content, and how OEM fitment changes versus retrofit cycles. The final outlook is aligned to the direction and speed that primary respondents expect across on-road and off-road applications.

Data Validation & Update Cycle

Outputs are validated through cross-checks against independent signals such as commercial vehicle builds, trade flows for relevant pneumatic and control components, and observed adoption in fleet maintenance practices. If a region shows an unusual jump, we revisit the penetration and pricing drivers, then re-check assumptions with follow-up expert touchpoints before sign-off.

A multi-step internal review is done so calculations, inputs, and conversions stay consistent across regions and years. Reports are refreshed annually, and interim updates are made when material events affect vehicle production, regulations, or supply availability. Before delivery, a final analyst pass is completed so clients receive the most current view of the market.

Mordor Intelligence's Automotive Automatic Tire Inflation System Atis Market Size Measured Against Other Published Estimates

Published market sizes for ATIS often do not match because each study defines the scope differently around what counts as an automatic inflation system and which vehicle groups are included. Differences also come from the base year selected, how average selling prices are trended, and whether OEM fitment is treated separately from retrofit demand.

Some external estimates stay closer to on-highway automotive fitment and keep off-highway equipment and tougher duty-cycle use cases less visible in the totals. In Mordor Intelligence's approach, ATIS value is counted only when the system actively maintains tire pressure using integrated air and control hardware across on-road and off-road vehicles, and tire pressure monitoring only setups are excluded.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.90 B (2026) | |

| Industry Publisher A | USD 0.73 B (2023) | Uses an earlier base year and may emphasize on-highway vehicle fitment more than off-highway equipment, which reduces the counted demand pool when penetration is still developing. |

| Global Publisher B | USD 0.88 B (2025) | Uses a different base year and a longer forecast window, and near-term totals can shift if OEM fitment timing and aftermarket replacement cycles are treated with simplified pricing progression. |

The spread across the table is mainly explained by year selection and which vehicle types and channels are included in the addressable demand pool. Our checks keep the sizing tied to observable vehicle activity and realistic adoption, which also makes it easier to refresh when new production or fleet signals change.

Key Questions Answered in the Report

What is driving the strong CAGR in the automotive automatic tire inflation system market?

Stringent safety mandates in the United States and European Union, coupled with fleet demands for fuel and tire-wear savings, underpin the 9.88% CAGR.

Which vehicle class captures the largest share of global revenue?

Medium and heavy commercial trucks lead with 66.10% revenue because high mileage and multiple tire positions maximize cost-saving potential.

How big is the opportunity in off-highway equipment?

Off-highway vehicles post an 11.43% CAGR to 2031 as farming, mining, and defense operators adopt real-time pressure control for traction and soil protection.

Why are self-powered hub inflators growing faster than central systems?

Hub inflators avoid external airlines, shorten retrofit time, and suit high-volume trailer fleets, which explains their 12.25% forecast CAGR.

Page last updated on: