Asia-Pacific Tire Pressure Monitoring System (TPMS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

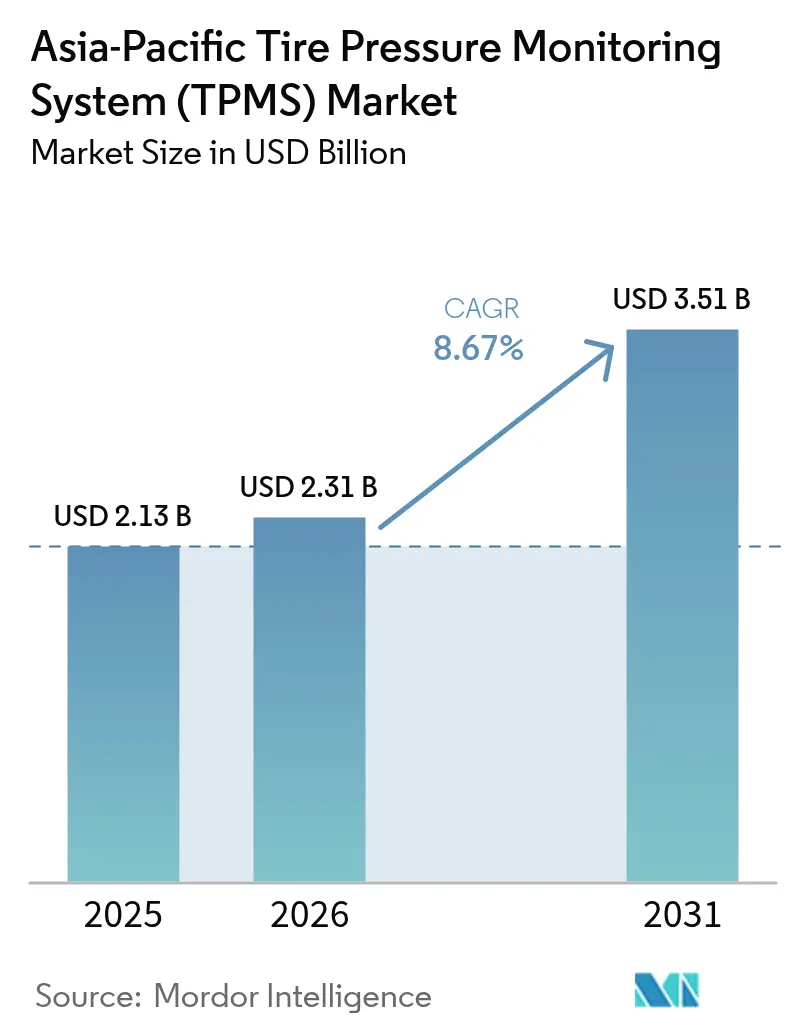

| Base Year Market Size (2025) | USD 2.13 Billion |

| Market Size (2026) | USD 2.31 Billion |

| Market Size (2031) | USD 3.51 Billion |

| Growth Rate (2026 - 2031) | 8.67% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Tire Pressure Monitoring System (TPMS) Market Analysis by Mordor Intelligence

The Asia Pacific automotive tire pressure monitoring system (TPMS) market size was valued at USD 2.13 billion in 2025 and estimated to grow from USD 2.31 billion in 2026 to reach USD 3.51 billion by 2031, at a CAGR of 8.67% during the forecast period (2026-2031). Regulatory mandates across China, Japan, and India create the spine of demand, while original-equipment manufacturers (OEMs) view accurate tire-pressure monitoring as a direct lever for fuel-saving and battery-range gains in electric vehicles (EVs). Frequency harmonization around 433 MHz in Japan lowers product-variant complexity, and Bluetooth Low Energy (BLE) sensors illustrate the shift toward software-defined vehicles. Localized micro-electro-mechanical-system (MEMS) fabrication in China and Japan eases average selling prices, helping smaller ASEAN markets adopt the technology through imported vehicles. On the competitive front, tier-one suppliers focus on vertical integration and secure over-the-air (OTA) update capabilities to comply with new regional cybersecurity requirements.

Key Report Takeaways

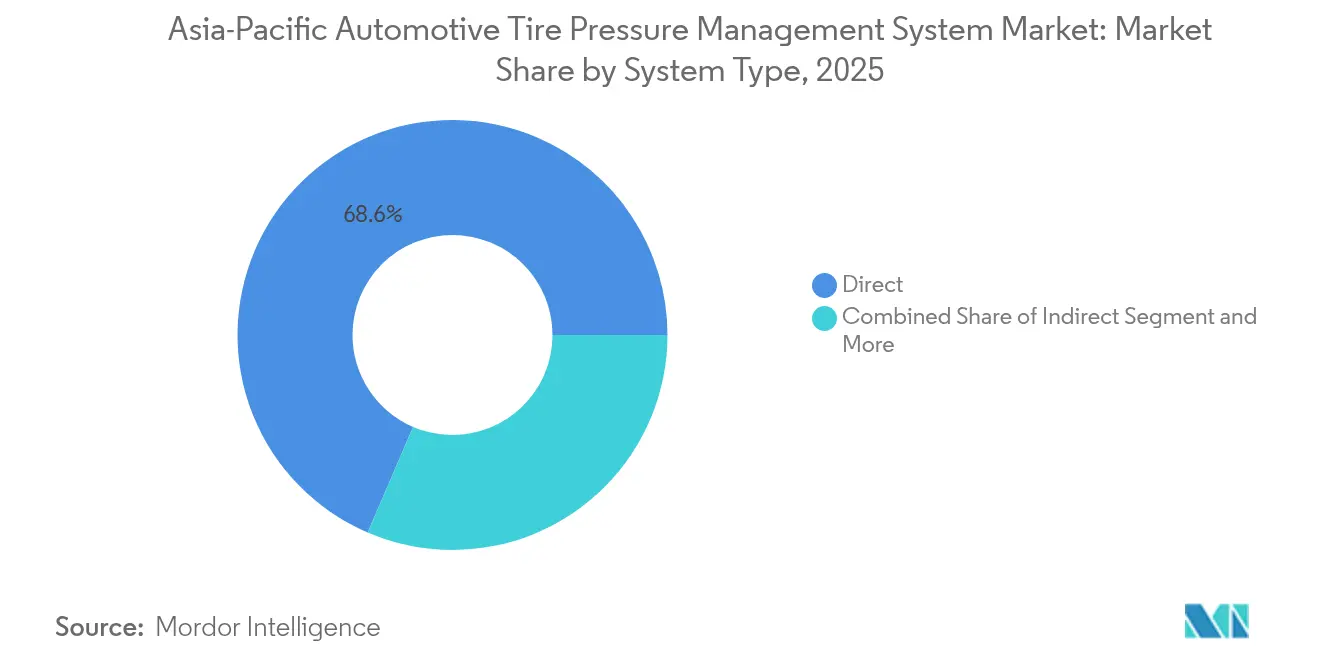

- By system type, direct TPMS held 68.55% of the Asia-Pacific automotive tire pressure monitoring system (TPMS) market share in 2025, while hybrid systems are projected to expand at an 11.02% CAGR through 2031.

- By sensor technology, MEMS-capacitive designs captured 52.60% of the Asia Pacific automotive TPMS market size in 2025 and will grow with the fastest CAGR of 9.12% through 2031.

- By fitting method, valve-stem (snap-in and clamp-in) held 61.40% share in 2025, while the embedded-tire module will expand at a 10.34% CAGR through 2031.

- By frequency band, 433 MHz accounted for a 70.60% share in 2025, while ≥2.4 GHz and UWB solutions are forecast to grow at an 10.78% CAGR between 2026 and 2031.

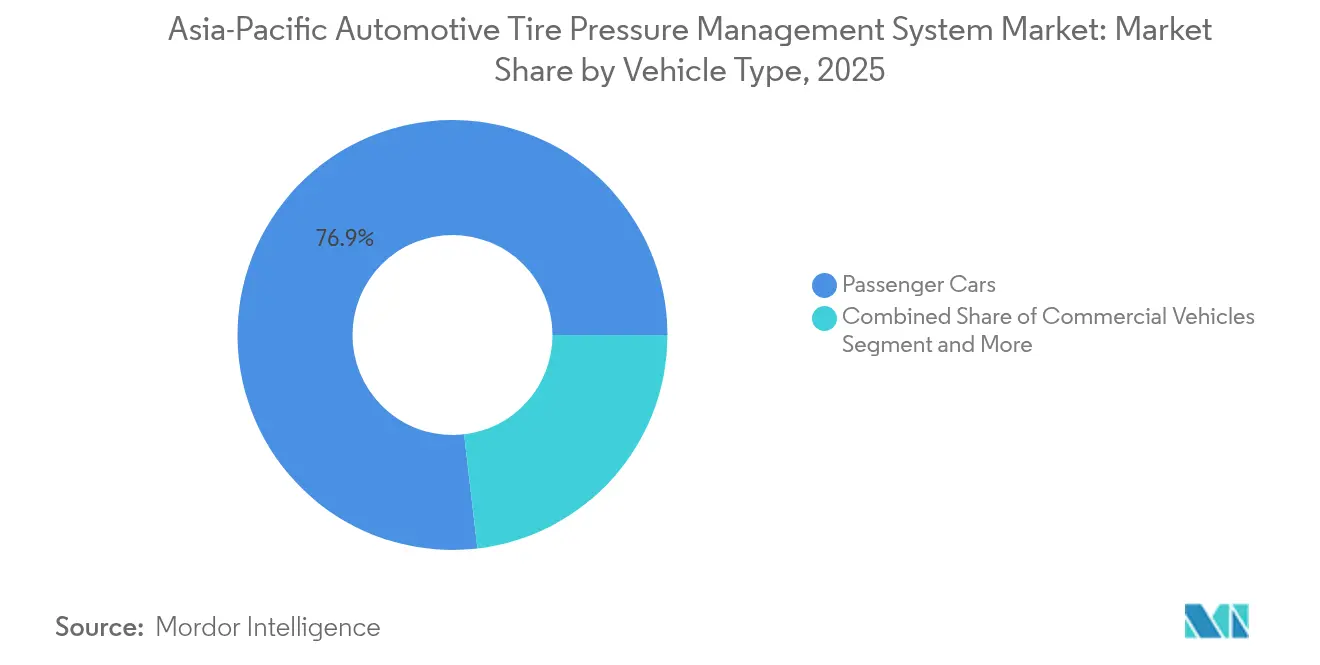

- By vehicle type, passenger cars accounted for 76.85% share of the Asia Pacific automotive TPMS market size in 2025 and are advancing at a 9.68% CAGR.

- By sales channel, OEM factory-fitted models accounted for an 82.50% share in 2025, while aftermarket retrofit solutions will advance at a 10.11% CAGR.

- By country, China held the dominant share of 51.80% in 2025 and will advance at a 9.21% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Asia representing one of the more structurally developed among them. The global report on automotive tpms market by Mordor Intelligence reflects how these regional layers combine into a single system.

Asia-Pacific Tire Pressure Monitoring System (TPMS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory TPMS Regulations | +2.8% | China, India, Thailand, Malaysia | Medium term (2-4 years) |

| OEM Fuel Efficiency Demand | +2.1% | China, Japan, South Korea | Long term (≥ 4 years) |

| BLE Battery-Less TPMS | +1.5% | China, Japan, South Korea | Medium term (2-4 years) |

| Fleet Telematics Integration | +1.2% | China, Japan, Australia, India | Medium term (2-4 years) |

| 433 MHz Harmonization | +0.9% | Japan, Australia, New Zealand | Short term (≤ 2 years) |

| Localized MEMS Production | +0.8% | China, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory TPMS Regulations Across China, India, and ASEAN

China’s GB 26149 made TPMS compulsory on all passenger cars from 2020, driving near-universal fitment [1]“GB 26149–2017 Technical Requirements for Tire Pressure Monitoring Systems,” Ministry of Industry and Information Technology, SAC, sac.gov.cn. India extended its Rule 115A deadline, simultaneously announcing substantial subsidies under the PM E-DRIVE initiative for electric vehicles, ensuring sustained medium-term volume. In ASEAN, JASIC-led meetings nudge Thailand, Malaysia, and Vietnam toward UN R141, though timelines remain uneven. OEMs must therefore design multi-frequency, software-configurable modules to comply with divergent rules while avoiding expensive hardware revisions. The combined regulations add significant percentage points to regional CAGR by guaranteeing baseline demand regardless of short-run economic swings, and they force lower-tier suppliers to invest in homologation labs and functional-safety documentation.

OEM Demand for Fuel Efficiency and EV Range Optimization

Maintaining correct pressure cuts rolling resistance, which directly boosts mileage for combustion cars and extends range for battery EVs. Michelin's e·PRIMACY tire, when properly inflated, boosts driving range significantly, offering a notable improvement in efficiency. Meanwhile, the Pilot Sport EV provides an even greater extension in driving range. Heavier EV curb weights heighten under-inflation penalties, so OEMs integrate direct sensors with algorithmic leak-rate estimation into energy-management software. Predictive alerts reduce warranty claims tied to uneven tire wear and protect fragile low-profile EV tires. As the push for efficiency intensifies, the demand for sensor accuracy has tightened. Furthermore, there's a growing appetite for Bluetooth Low Energy (BLE) links that relay data for cloud analytics, driving further advancements in the market.

BLE-Enabled Battery-Less TPMS for Fast-Growing EV Segment

Bluetooth Low Energy permits bidirectional, secured links between tire sensors, vehicle gateways, and smartphones, eliminating specialized RF receivers. Bosch’s SMP290 achieves a 10-year design life on a coin cell, while academic piezoelectric harvesters suggest full battery elimination [2]“SMP290: First MEMS TPMS with BLE Interface,” Bosch, Bosch Press, bosch.com. BLE supports firmware updates and advanced diagnostics, aligning with software-defined vehicle roadmaps. Premium EV makers deploy BLE sensors to merge tire data with keyless-entry antennas, cutting wiring weight and points of failure. OTA re-calibration enables continuous accuracy despite tire rotations or software changes, appealing to fleet operators. This architecture significantly enhances growth potential and improves multi-sensor fusion, enabling features like tread-depth and load monitoring.

Fleet-Telematics Integration for Predictive Maintenance

To minimize tire-related breakdowns, which contribute to unscheduled downtime, logistics fleets are now integrating TPMS with telematics. Goodyear TPMS Connect leverages existing cellular boxes to push leak predictions and geofenced service alerts, while Continental’s ContiConnect Lite uploads pressure, temperature, and tread data via smartphones. Such analytics allow maintenance to shift from mileage-based to condition-based intervals, saving fuel and extending casing life. Asset managers correlate pressure trends with load, road grade, and driver behavior, feeding AI tools that advise route or speed adjustments. Telematics-enabled TPMS, therefore, transforms a regulatory cost into an ROI-positive tool, adding significant points to CAGR, mainly in China, Japan, and Australia.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Sensitivity Two-Wheelers | -1.1% | India, Indonesia, Vietnam | Long term (≥ 4 years) |

| High Replacement-Battery Cost | -0.7% | China, India, ASEAN | Medium term (2-4 years) |

| Chip-Supply Volatility | -0.6% | Asia-Pacific | Short term (≤ 2 years) |

| RF-Hacking and Cybersecurity | -0.5% | China, Japan, South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity in Two-Wheelers and Entry-Level Cars

In India and Southeast Asia, the TPMS hardware can account for a small portion of a vehicle's retail price, which makes the removal of TPMS a tempting cost-saving measure in segments where enforcement is lax. While two-wheelers are the dominant mode of personal transport in the region, they are not legally mandated to have TPMS, which hampers scalability. Although software-only indirect solutions are available at a low cost, they offer slower detection and lack tire-specific alerts. As a result, OEMs are reluctant to promote them as safety enhancements. Consumers tend to prioritize features like infotainment, which are visible, over the less noticeable tire pressure monitoring. Furthermore, while government incentives are directed towards electrification, safety add-ons like TPMS don't receive the same attention. Banks also rarely associate insurance discounts with TPMS usage. This affordability challenge reduces growth potential across India, Indonesia, and Vietnam.

High Replacement-Battery Cost in Aftermarket

Direct sensors usually fail when their five-to-seven-year batteries deplete, so China’s 2020 fleet enters replacement cycles from 2026, triggering sticker shock for owners facing sensor, kit, and labor charges. Price-sensitive Indian and ASEAN drivers may ignore dash warnings, undermining safety and compliance. Schrader's universal sensors and BLE retrofit kits, while reducing inventory needs, still come with a relatively high installation cost. Although battery-less piezoelectric harvesters offer a promising solution, they are yet to reach the commercial stage [3]“Battery-Less TPMS Powered by Piezoelectric Harvesters,” IEEE, IEEE Xplore, ieeexplore.ieee.org . The absence of standardized pricing allows workshops to mark up parts, leading to an erosion of trust. Consequently, this aftermarket drag hampers growth and might prompt regulators to consider extending inspection grace periods, further delaying the turnover of sensors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Direct Dominates, Hybrid Surges

Direct architectures held the largest share of 68.55% of the Asia-Pacific automotive tire pressure monitoring system market in 2025, reflecting regulatory preferences for immediate pressure readings. Hybrid designs that pair direct sensors with predictive algorithms will log an 11.02% CAGR, the highest within the category, because they deliver redundancy and add cloud-based analytics without major hardware cost increases. OEMs also value hybrid flexibility, which supports incremental software upgrades through the vehicle life cycle. The Asia-Pacific automotive tire pressure monitoring system market size for indirect platforms remains smaller, yet software-only solutions continue to penetrate cost-sensitive entry models where regulations accept performance-equivalent alternatives.

Alongside factory installations, replacement and retrofit demand grow as fleets aim for predictive maintenance. Embedded analytics that forecast slow leaks or estimate tread depth strengthen the business case for hybrid platforms, encouraging tier-one suppliers to combine sensor fusion with over-the-air algorithm updates.

By Sensor Technology: MEMS-Capacitive Leads Evolution

MEMS-capacitive devices controlled 52.60% of the Asia-Pacific automotive tire pressure monitoring system market share in 2025 due to their robust thermal stability and attractive unit economics from regional foundry capacity. The segment will continue to dominate the market, expanding with a 9.12% CAGR through 2031. The Asia Pacific automotive tire pressure monitoring system (TPMS) market size for ultra-low-power BLE sensors relies heavily on this MEMS base, given its proven reliability in −40 °C to +125 °C automotive duty cycles. Advancements in miniaturization techniques, utilizing through-silicon-via stacking, are leading to the development of multi-parameter packages, each under 1 cm³, capable of measuring pressure, temperature, and acceleration within a single die stack.

In specialty vehicles, where ultra-high accuracy justifies the expense, alternatives to strain gauges maintain their niche status. Meanwhile, while still experimental, piezoelectric harvesters are garnering attention for their potential to eliminate batteries in embedded-tire applications.

By Fitting Method: Valve-Stem Still Predominant

Snap-in and clamp-in valve-stem sensors accounted for 61.40% OE volume because they integrate with mature tire-service procedures and require no mold changes. Embedded-liner modules, however, post the fastest CAGR at 10.34%, as OEMs seek tamper-proof placement and drag-free wheel designs for EVs. Tire makers now pilot BLE-enabled smart tires that carry pressure and identification data through the entire cradle-to-grave life cycle, delivering recycling traceability.

Band-mounted sensors offer significant retrofit flexibility for multi-axle fleets, as they can be installed without requiring the replacement of valve stems. This feature makes them particularly advantageous for fleet operators seeking cost-effective and efficient solutions to enhance vehicle monitoring systems. However, despite these benefits, the adoption of band-mounted sensors in passenger cars remains limited. The primary reason for this is the higher labor costs associated with their installation, which makes them less appealing for individual vehicle owners compared to other alternatives available in the market.

By Frequency Band: 433 MHz Dominates but 2.4 GHz Accelerates

The 433 MHz channel retains 70.60% shipment share after Japan abandoned 315 MHz in February 2025, allowing one hardware SKU across China and Japan. Nevertheless, ≥2.4 GHz BLE devices deliver the swiftest growth—10.78% CAGR—by merging TPMS with keyless entry and smartphone diagnostics. Bosch’s SMP290 and Melexis’s MLX91805 exemplify single-chip MEMS plus BLE designs that slash wiring and add secure OTA firmware.

Ultra-wideband pilots offer centimeter-level wheel localization and anti-relay-attack security but stay niche because of current BOM premiums and spectrum-licensing hurdles. Suppliers hedge by offering software-defined radios that handle both 433 MHz and BLE, streamlining inventory ahead of ASEAN frequency-allocation decisions.

By Vehicle Type: Passenger Cars Steer Uptake

Passenger cars controlled 76.85% share of the revenue in 2025, because TPMS is mandatory for M1 category vehicles in China, Japan, and Australia. EV proliferation amplifies sensitivity to rolling-resistance losses, pushing more accurate direct systems into mid-range models. Commercial-vehicle demand rises as UNECE Regulation 141 expands to trucks and buses, prompting dual-tire sensors and ISO 11992-2 trailer links.

Two-wheelers remain largely unregulated, yet India’s PM E-DRIVE subsidies and falling BLE prices create footholds for indirect software platforms. The Asia Pacific automotive TPMS market size for passenger cars is forecast to grow 9.68% CAGR, while heavy-duty segments advance on fleet telematics integration that monetizes predictive pressure analytics and tread-wear alerts.

By Sales Channel: Aftermarket Replacement Wave Builds

OEM factory-fitment accounted for 82.50% of 2025 units as mandates lock sensors into new-vehicle homologation. The aftermarket registers the fastest expansion—10.11% CAGR—beginning in 2026 when Chinese vehicles sold under the 2020 rule hit five-year battery life. Universal programmable sensors such as Schrader EZ-sensor and BLE retrofit kits shorten workshop dwell time and reduce stock-keeping units, improving installer economics.

Fleet operators in India and Australia retrofit trailers to pass automated testing-station inspections that now flag under-inflation. Cost sensitivity still tempers demand in two-wheeler channels, yet software-only indirect options priced under USD 10 attract ride-sharing fleets seeking basic compliance and app-based monitoring.

Geography Analysis

China commands 51.80% of 2025 revenue and grows 9.21% CAGR, propelled by GB 26149 enforcement, world-leading EV volumes, and domestic MEMS fabrication that pushes sensor prices. Shanghai Baolong’s local share shows how proximity and cost scaling foster supplier ascendancy. Cyber-security standard GB 44495-2024, effective 2026, raises compliance thresholds, favoring players with secure OTA stacks and embedded-security labs.

Japan’s February 2025 433 MHz alignment eliminates its legacy 315 MHz niche, letting OEMs unify global platforms and compress tooling expense. METI’s semiconductor roadmap strengthens onshore MEMS supply, while Sumitomo Rubber’s Sensing Core wins EV programs targeting wheel-detachment alerts. South Korea mirrors UNECE Regulation 141, extending coverage to heavy trucks after the 2024 EU rule changes, thereby widening addressable units.

India mandates fitment to 2026 but backs a significant EV push that funds 2.5 million electric two-wheelers and 14,028 buses. Automated testing stations now check tire inflation, nudging fleets toward retrofits despite cost concerns. Australia, New Zealand, and major ASEAN states import 433 MHz-compliant vehicles from Japan and China, creating de facto standardization even before local mandates finalize.

Competitive Landscape

The market remains top-heavy: Sensata, Continental, Pacific Industrial, and DENSO together account for a notable share of OEM volume. These firms leverage proprietary MEMS fabs, decades-old RF patents, and deep homologation experience to lock multiyear platform awards. Their vertical integration shields them from chip shortages and cybersecurity audits under GB 44495-2024 and UNECE R155.

Technology differentiation now centers on BLE and OTA-ready designs. Bosch and Melexis supply single-die sensors integrating microcontroller, RF, and cryptographic accelerators that fit software-defined vehicle roadmaps. Tire majors—Michelin, Bridgestone, and Goodyear—convert sensor data into subscription analytics, bundling TPMS inside fleet-care platforms that promise significant fuel-cost savings.

Disruptors such as Sumitomo Rubber, NIRA Dynamics, and Orange Electronic chase cost-sensitive niches with indirect or battery-less concepts. Universal aftermarket kits from Schrader and CUB address the upcoming Chinese replacement wave. Yet escalating security certification and trailer-protocol requirements raise barriers, making tier-one partnerships essential for full-function OEM awards.

Asia-Pacific Tire Pressure Monitoring System (TPMS) Industry Leaders

Schrader TPMS Solutions (Sensata Technologies)

Continental AG

Pacific Industrial Co., Ltd.

Huf Hülsbeck & Fürst GmbH & Co. KG

ZF Friedrichshafen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: JK Tyre unveiled India’s first embedded smart tires with integrated TPMS sensors, supplying live pressure and temperature data to a mobile app.

- September 2025: The Government of India announced that all new passenger vehicles sold from November 2025 must install TPMS.

- October 2024: Japan amended its Radio Act to allocate 433.795–434.045 MHz to vehicle TPMS and remote keyless entry systems.

- June 2024: Continental expanded passenger-vehicle TPMS production at its Bangalore plant and introduced a second-generation module with improved pressure accuracy.

Asia-Pacific Tire Pressure Monitoring System (TPMS) Market Report Scope

The scope includes segmentation by system type (direct, indirect, and hybrid), sensor technology (MEMS capacitive, strain-gauge, piezoelectric, and others), fitting method (valve-stem (snap-in and clamp-in), band/rim-mounted, embedded-tire module), frequency band (315 MHz, 433 MHz, and ≥ 2.4 GHz and UWB), vehicle type (passenger cars, commercial vehicles, and two-wheelers), sales channel (OEM factory-fit and aftermarket retrofit). The analysis also covers country-level segmentation, including China, Japan, India, South Korea, Australia, and the Rest of the Asia-Pacific. Market size and growth forecasts are presented by value in USD.

| Direct |

| Indirect |

| Hybrid |

| MEMS Capacitive |

| Strain-Gauge |

| Piezoelectric |

| Others (Optical, SAW, etc.) |

| Valve-Stem (Snap-In and Clamp-In) |

| Band / Rim-Mounted |

| Embedded-Tire Module |

| 315 MHz |

| 433 MHz |

| ≥ 2.4 GHz and UWB |

| Passenger Cars |

| Commercial Vehicles |

| Two-Wheelers |

| OEM Factory-Fit |

| Aftermarket Retrofit |

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By System Type | Direct |

| Indirect | |

| Hybrid | |

| By Sensor Technology | MEMS Capacitive |

| Strain-Gauge | |

| Piezoelectric | |

| Others (Optical, SAW, etc.) | |

| By Fitting Method | Valve-Stem (Snap-In and Clamp-In) |

| Band / Rim-Mounted | |

| Embedded-Tire Module | |

| By Frequency Band | 315 MHz |

| 433 MHz | |

| ≥ 2.4 GHz and UWB | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| Two-Wheelers | |

| By Sales Channel | OEM Factory-Fit |

| Aftermarket Retrofit | |

| By Country | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How fast is the Asia-Pacific automotive TPMS market expected to grow?

The market is projected to expand at a 8.67% CAGR from 2026 to 2031, climbing from USD 2.31 billion to USD 3.51 billion.

Which frequency band now dominates regional TPMS shipments?

The 433 MHz band continues to hold the largest shipment share after Japan aligned with the global standard in 2025.

Why are BLE-based TPMS sensors gaining traction?

BLE sensors simplify vehicle wiring, enable smartphone diagnostics, and support secure OTA updates, attributes valued by EV manufacturers.

What is the main cost restraint for TPMS adoption in India’s two-wheeler segment?

Upfront sensor and installation costs challenge adoption, making software-only indirect solutions more attractive for low-price models.

Page last updated on: