Automotive Airbag Inflator Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 5.63 Billion |

| Market Size (2031) | USD 8.17 Billion |

| Growth Rate (2026 - 2031) | 7.73% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Airbag Inflator Market Analysis by Mordor Intelligence

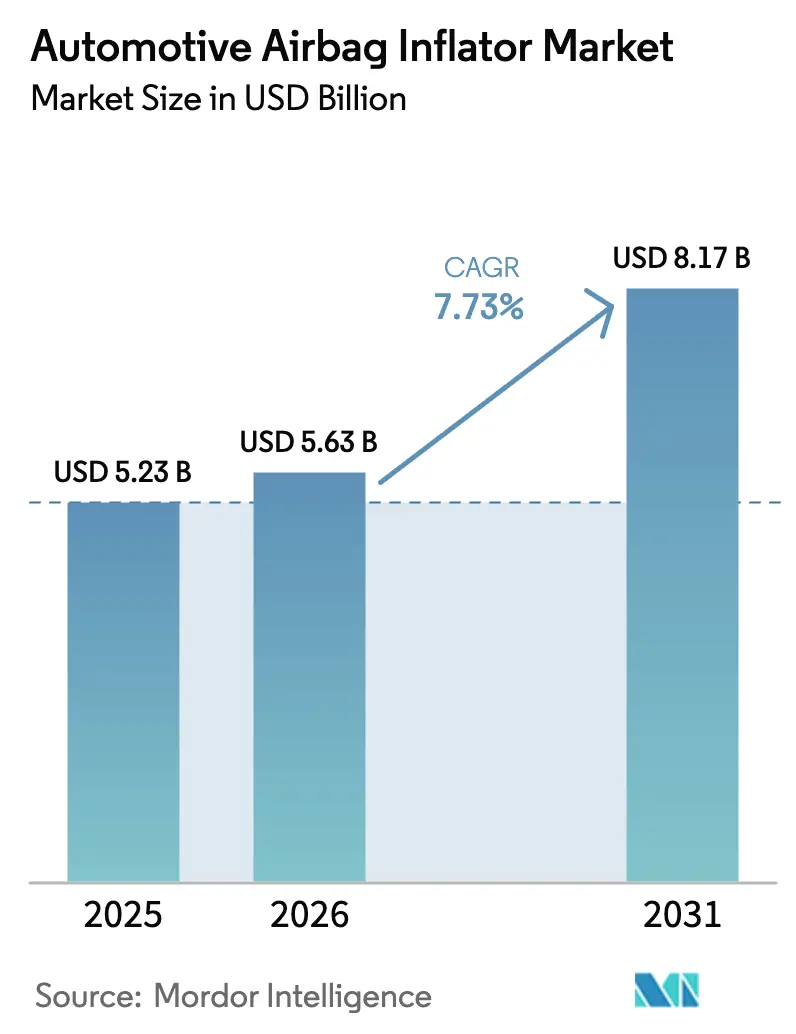

The automotive airbag inflator market size was valued at USD 5.23 billion in 2025 and is estimated to grow from USD 5.63 billion in 2026 to reach USD 8.17 billion by 2031, at a CAGR of 7.73% during the forecast period (2026-2031). Growth stems from electric-vehicle (EV) chassis that favor ultra-slim side-curtain modules, regulatory mandates for autonomous-driving safety, and production scale-ups across Asia-Pacific. Costlier helium has begun to shift buyer preference toward hybrid inflators, while non-azide propellants are gaining ground as hazardous-substance rules tighten across the European Union and Japan. Suppliers are also redesigning multi-stage architectures to meet the requirements of ISO/TS 5083:2025 for adaptive restraint systems. Competitive intensity remains high, pushing smaller firms toward tier-one partnerships and captive OEM programs.

Key Report Takeaways

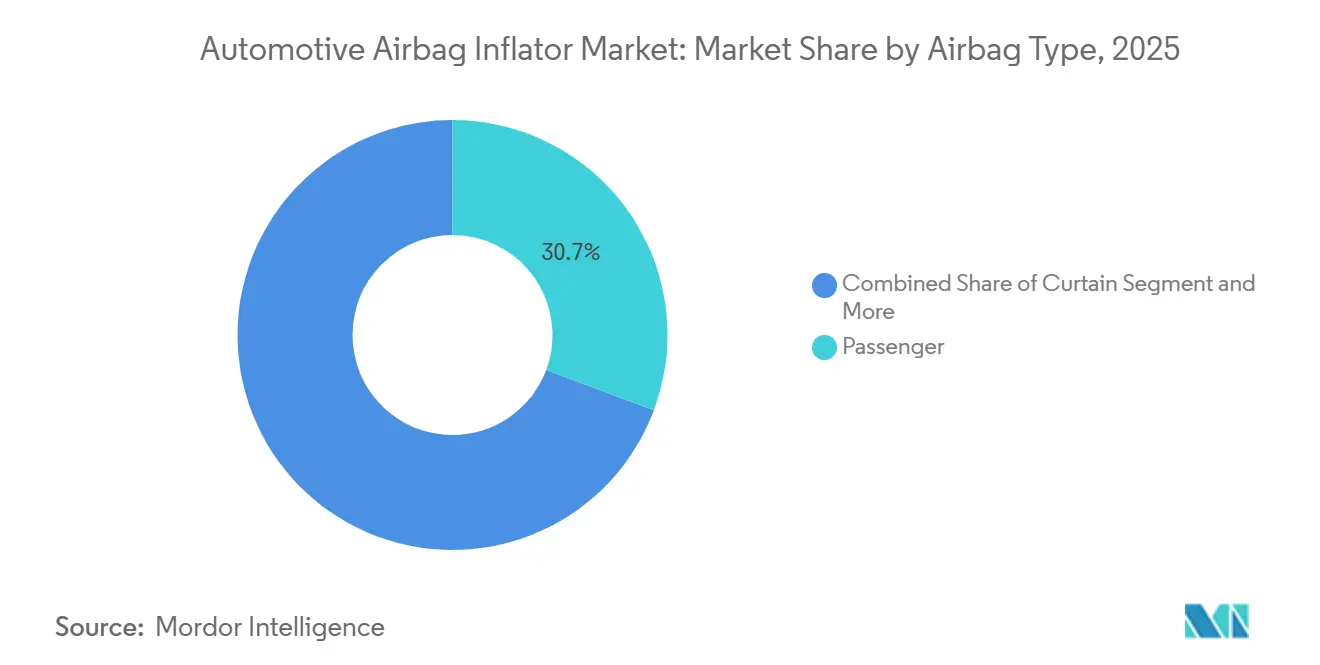

- By airbag type, passenger airbags remained the largest with 30.69% revenue share in 2025, while pedestrian-protection airbags represented the quickest-growing airbag type at a 9.82% CAGR.

- By inflator type, pyrotechnic inflators captured 66.56% of the automotive airbag inflator market share in 2025, whereas hybrid inflators are expanding at an 8.27% CAGR through 2031.

- By vehicle type, Passenger cars commanded 75.71% of the automotive airbag inflator market size in 2025, yet commercial vehicles are advancing at a 10.07% CAGR to 2031.

- By propellant chemistry, azide-based formulations accounted for 38.67% of the automotive airbag inflator market in 2025, while non-azide-based formulations are set to grow at an 8.48% CAGR to 2031.

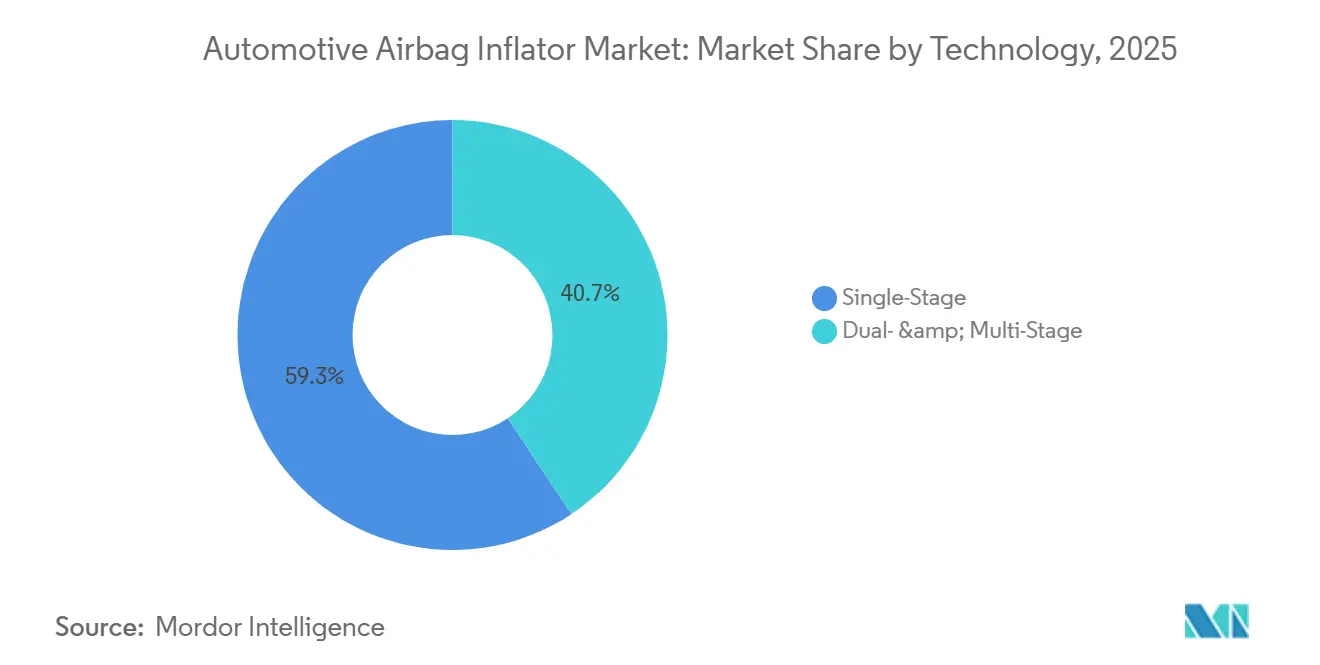

- By technology stage, single-stage inflators led with 59.34% share in 2025, whereas dual- and multi-stage inflators show an 8.89% CAGR to 2031.

- By sales channel, OEM-fitted units represented 72.64% of shipments in 2025; aftermarket and recall replacements are poised for an 8.63% CAGR through 2031.

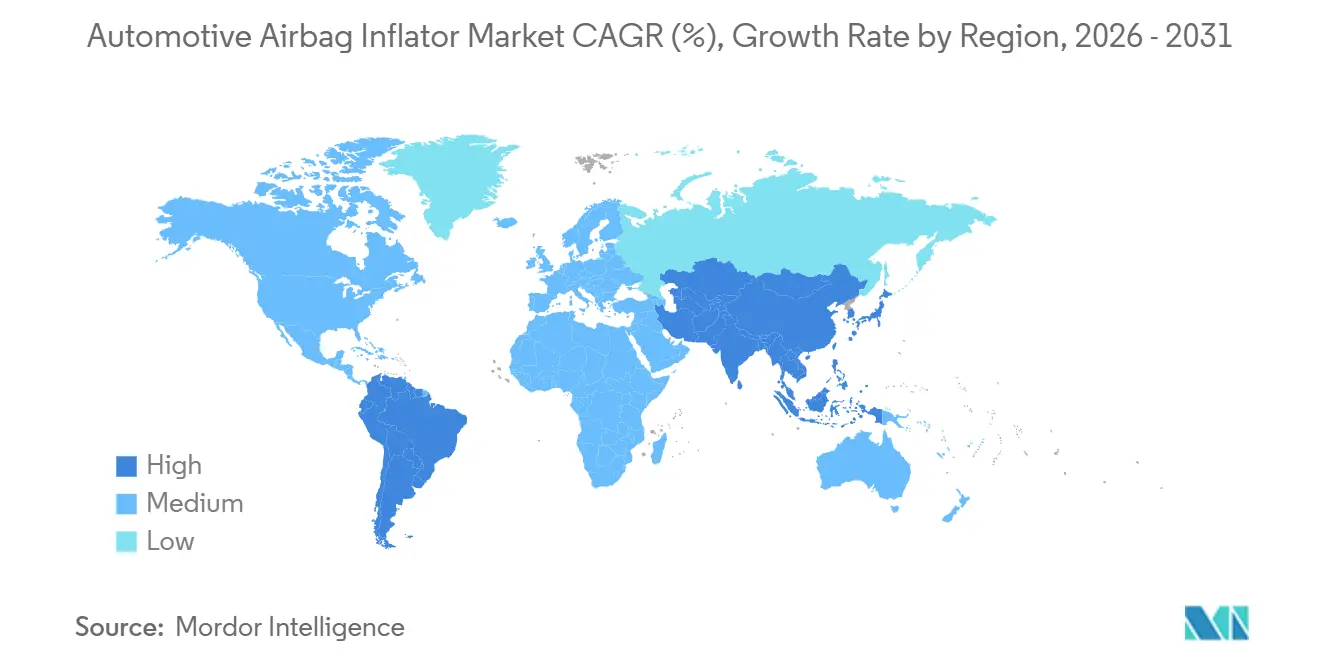

- By geography, Asia-Pacific accounted for 38.88% of global revenue in 2025, and is forecasted to post a 9.42% CAGR, the fastest worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Airbag Inflator Market Trends and Insights

Drivers Impact Analysis Table*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Giga-Casting Chassis | +2.1% | Global, led by China & North America | Medium term (2-4 years) |

| Adoption of Multi-Stage Inflators | +1.8% | APAC core, spill-over to South America | Short term (≤ 2 years) |

| L4/L5 Autonomous Vehicle Rollout | +1.5% | North America & EU, pilot zones in Japan | Long term (≥ 4 years) |

| Elevated Captive Inflator Off-take | +1.2% | India, with exports to ASEAN & Middle East | Medium term (2-4 years) |

| Phase-out of Azide Propellants | +0.9% | EU & Japan | Short term (≤ 2 years) |

| UN-R155 Cyber-Security Compliance | +0.6% | North America, EU adoption by 2027 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV Giga-Casting Chassis Creating Need for Ultra-Slim Curtain Inflators

Tesla's Cybertruck and Model Y utilize single-piece rear underbodies, cast in massive presses. This innovation removes traditional B-pillar reinforcement zones and significantly reduces the space available for side-curtain inflators. Similarly, BYD's Seagull and Dolphin lines employ mega-castings, which drastically cut the body-in-white part count but result in a more constrained space for restraint hardware. In response, Hyundai Mobis introduced door-mounted curtain modules in 2024, designed to meet ejection-mitigation standards[1]"Hyundai Mobis Unveils the World's First Airbags Designed for PBVs," Hyundai MOBIS, hyundaimotorgroup.com. As a result, suppliers are shifting from cylindrical pyrotechnic inflators to hybrid flat-pack devices. These newer devices combine compressed gases, such as argon or nitrogen, with a wafer-style solid charge, enabling faster deployment and lower peak temperatures. This transition reflects the growing preference for hybrid inflators, even as pyrotechnic units remain widely used in existing installations.

ADAS-Led Adoption of Multi-Stage Inflators in Chinese Mid-SUVs

Sensor-rich mid-SUVs manufactured by Chinese brands fuse crash-severity data with inflator logic, allowing tailored gas releases that protect a wider occupant range. Five-star New Car Assessment Program scores support showroom appeal and showcase multi-stage inflators as visible proof of ADAS value. Automakers that lag in multi-stage deployment risk negative showroom comparisons, creating fast-follower pressure. Software updates allow future calibration tweaks, shielding OEMs from retooling costs. Component suppliers leverage the trend to upsell firmware maintenance contracts, adding an annuity-style revenue layer. Therefore, the convergence of sensor fusion and inflator modulation sustains premium price points within the automotive airbag inflator market.

L4/L5 Autonomous Vehicle Rollout Demanding Multi-Directional Inflator Arrays

Waymo introduced its latest-generation robotaxi in Phoenix and San Francisco, designed with advanced safety features to protect passengers from lateral or rearward impacts. UN Regulation 155, effective across the EU, requires manufacturers to implement robust cybersecurity management systems to safeguard restraint-system electronic control units from tampering. Additionally, EU Regulation 2024/1257 expands these anti-tamper measures to include inflator communication lines. This regulatory shift is expected to drive the adoption of encrypted smart modules, which are anticipated to play a significant role in enhancing vehicle safety and security in the coming years.

Emergence of Indian Export Hubs

India exported 6,659 side-airbag consignments between October 2023 and September 2024, mainly to Vietnam, South Korea, and Turkey. High-utilisation rates justify fresh propellant-mixing towers, unlocking cost savings that strengthen India’s price competitiveness. Local Tier-2 suppliers move upstream into precision stamping and ignition-element assembly, deepening the value chain. Export contracts typically request dual-chemistry capacity, helping buyers hedge helium volatility. Regional testing facilities in Chennai and Pune cut homologation waiting times, securing model-year awards ahead of Western rivals. The clusters, therefore, underpin a long-term structural lift in India’s share of the automotive airbag inflator market.

Restraints Impact Table*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Helium Supply Crunch | -1.4% | Global, acute in Europe & North America | Short term (≤ 2 years) |

| Lithium-ion Battery Fire Risks | -1.1% | Global, concentrated in EV-heavy markets | Medium term (2-4 years) |

| EU Carbon Border Tariff | -0.8% | EU, indirect impact on ASEAN exporters | Short term (≤ 2 years) |

| Proliferation of Counterfeit Inflators | -0.5% | Middle East & Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Helium Supply Crunch

Geopolitical disruptions lifted industrial-grade helium spot prices, inflating the bill of materials for stored-gas inflators and squeezing margins. Exploration campaigns in Tanzania seek green helium, with preliminary flow-rate data suggesting a viable commercial supply for safety-system producers. OEMs respond by shifting procurement toward hybrid inflators that dilute helium with pyrotechnic gas. Contract clauses now include helium-price adjustment formulas, transferring part of the risk back to suppliers. While temporary, cost spikes have already slowed new design iterations for stored gas, moderating near-term growth for that subsegment of the automotive airbag inflator market.

Lithium-Ion Battery Fire Risks Delaying EV Airbag Integration

In 2024-2025, NHTSA launched investigations into thermal runaway incidents involving major automakers, including Tesla, General Motors, and Ford[2]“Electric-Vehicle Battery Fire Investigations,” National Highway Traffic Safety Administration, nhtsa.gov. These incidents caused pack fires that reached extremely high temperatures, leading to damage in critical components such as airbag wiring harnesses. To address these issues, manufacturers implemented design changes, including the use of shielded cabling and thermal barriers. While these measures enhanced safety, they also introduced additional challenges, such as increased vehicle weight and extended validation timelines, which have impacted the short-term demand for EV inflators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Airbag Type: Curtain Strength and Knee-Airbag Momentum

Passenger airbags represented 30.69% of the automotive airbag inflator market share in 2025. Their dominance rests on star-rating protocols that mandate robust side-impact protection. Recent refreshes reveal interest in segmented gas channels that enhance fill uniformity along narrow roof rails. Emerging giga-cast EV frames create slimmer rails, so oval-section cylinders preserve gas volume without raising roof-height constraints. The automotive airbag inflator market continues to reward platforms that mix shape innovation with reliable chemistry.

Pedestrian-protection airbags register the fastest 9.82% CAGR to 2031. Crash dummies that weigh more on lower-leg injuries and insurance scoring models reinforce uptake. Suppliers now offer one-piece housings that clip into existing under-dash beams, trimming line-side assembly minutes. Fleet buyers highlight lower worker-compensation claims when knee protection is present, boosting specification rates. Growing traction strengthens the long-term diversity of the automotive airbag inflator industry, which benefits from multiple growth vectors rather than a single dominant category.

By Inflator Type: Pyrotechnic Scale and Hybrid Upside

Pyrotechnic inflators remained the anchor with a 66.56% share in 2025, supported by well-established supply chains and cost advantages over stored-gas alternatives. However, rising helium prices and the need for adaptive control systems have driven increased interest in hybrid inflators, with the segment gaining traction at an 8.27% CAGR. Stored-gas units, which rely on 300-bar helium-argon blends, lose favor as EU sanctions squeeze supply. Hybrid designs fuse a compact solid charge with a gas reservoir, enabling two-stage inflation that balances rapid bag fill and extended pressure for rollover events. ZF and Autoliv are field-testing flat-pack hybrid modules for electric SUVs whose giga-castings allow only 35 mm of package depth.

Pyrotechnic inflators still inflate a 60-liter bag within 30 ms, but EU REACH directives drive a pivot toward low-toxicity guanidine-nitrate propellants. Stored-gas inflators occupy niche luxury programs that accept cost premiums for quieter deployment. Hybrid inflators are forecast to capture 18% share by 2031, driven by UN R155 cybersecurity rules that pair electronic control units with variable-pressure valves.

By Vehicle Type: Passenger-Car Dominance and Commercial-Vehicle Upswing

Passenger cars accounted for 75.71% of the automotive airbag inflator market in 2025. Side-torso and far-side airbags are increasingly standard in mass-market hatchbacks and sedans, proving that safety content is no longer confined to luxury trims. Consumer awareness programs publish comparative injury scores, and resale-value studies reveal premiums for multi-stage systems. OEMs answer by integrating restraint content early in platform lifecycles, locking in inflator volumes over seven-year runs.

Commercial vehicles display the fastest CAGR of 10.07% to 2031. Fleet operators specify curtain plus steering-wheel airbags to reduce driver-injury downtime, and insurers reward such packages with lower premiums. Heavy-truck cabins in North America now list airbags as baseline, a marked shift from prior optional status. Retrofit programs also sweep older fleets, swelling replacement revenue. The sub-segment’s growth diversifies the automotive airbag inflator market, smoothing demand across economic cycles.

By Propellant Chemistry: Non-Azide Formulations Accelerate

Azide propellants retained a 38.67% share in 2025, yet regulatory headwinds are pushing automakers toward alternatives that avoid toxic residues. Non-azide-based blends are expanding at an 8.48% CAGR because they decompose into inert gases and water vapor, easing disposal concerns. European Union REACH rules and Japan’s updated hazardous-substance limits both penalize azide use, prompting suppliers to retool lines for cleaner chemistries. Tier-one companies emphasize lifecycle compliance by marketing non-azide inflators as a route to lower warranty-reserve requirements and smoother end-of-life recycling. Market messaging now centers on sustainability credentials rather than sheer cost savings, framing the switch as a long-term liability hedge.

Tetrazole and ammonium-nitrate blends round out the non-azide portfolio, offering faster burn rates that shorten bag-fill times in side-impact crashes. These recipes, however, generate higher combustion temperatures, so manufacturers must integrate heat-resistant housings and optimized venting to safeguard bag fabrics. Insurance underwriters in North America and Europe increasingly surcharge vehicles that still carry azide inflators, accelerating OEM timetables for guanidine-nitrate adoption. China’s GB 38900-2020 standard for EV safety also gives weight to low-toxicity propellants, nudging domestic brands to leapfrog directly to non-azide options.

By Technology Stage: Single-Stage Scale and Multi-Stage Innovation

Single-stage inflators held 59.34% of installations in 2025, reflecting their long-standing reputation for simplicity and low unit cost. Even so, dual- and multi-stage variants are advancing at an 8.89% CAGR as global crash-test protocols reward adaptive pressure curves that temper deployment for lighter occupants. ISO/TS 5083:2025 establishes performance criteria for Level-3 and Level-4 automated vehicles, effectively locking traditional single-charge igniters out of many future platforms. Suppliers now bundle micro-electromechanical sensors, microcontrollers, and encrypted firmware into multi-stage modules, highlighting real-time occupant-classification and crash-pulse analytics as differentiators. Automakers promote these adaptive systems in showroom marketing, citing reduced injury metrics in offset-frontal and oblique collisions.

Entry-level passenger cars and cost-sensitive light commercial vehicles still rely on single-stage hardware, but higher-tier trims pivot to dual-stage driver bags as a perceived baseline for safety credibility. Premium SUVs and emerging robotaxis take the next step, specifying triple-charge curtain modules that remain pressurized throughout rollover events. Cost gaps continue to narrow as silicon prices decline, allowing OEM purchasing teams to justify multi-stage upgrades without major budget overruns. Regulatory bodies further erode single-stage appeal by tightening allowances for out-of-position occupants and rear-seat passengers.

By Sales Channel: Aftermarket Surges on Recall Cycles

OEM-fitted inflators accounted for 72.64% of 2025 revenue, benefiting from integrated validation during vehicle development and synchronized, just-in-time logistics. The aftermarket, however, is climbing at an 8.63% CAGR as sodium-azide units leave service under phased recall programs. Dealers and certified repair chains capitalize on this wave by stocking non-azide replacements that meet revised regulatory thresholds. Independent distributors also report higher turnover as older vehicles exceed the airbag system’s design life and trigger insurance-driven replacements. Supply-chain digitalization, including barcode and RFID tagging, helps shops verify provenance and avoid counterfeit stock.

Recall momentum meshes with insurer requirements that repairs use propellants compliant with EU and Japanese toxicity limits, reinforcing the aftermarket’s shift toward guanidine-nitrate formulations. Blockchain-based traceability pilots show early promise in dissuading gray-market inflators that once plagued regions with lax customs oversight. OEMs, wary of brand-damage risks, now extend goodwill programs that subsidize replacement labor for recalled modules, effectively steering customers toward franchised service centers. Meanwhile, tier-one suppliers secure revenue by licensing production to certified aftermarket specialists rather than competing head-to-head on final-mile distribution. As legacy sodium-azide inventories dwindle, growth expectations remain firmly in the replacement lane rather than in new-vehicle assembly.

Geography Analysis

Asia-Pacific owned 38.88% of global revenue in 2025 and is on track for a 9.42% CAGR through 2031, the steepest among all regions. China alone accounted for 28% of the automotive airbag inflator market in 2025; stringent 2024 C-NCAP rules mean 76% of new Chinese passenger cars already feature dual-stage driver modules. India’s inflator segment benefits from the Production-Linked Incentive plan, which has prompted investments such as ZF Rane’s 3 million-unit plant in Tamil Nadu[3]"ZF Rane Inaugurates Inflator Manufacturing and Sled Test Facility at Trichy, Tamil Nadu," Rane Group, ranegroup.com. Japan leads pedestrian-protection penetration at 68% as revised JNCAP scoring incentivizes external airbags.

South America follows with a 7.23% CAGR, as Brazil’s Rota 2030 mandates most local content for restraint systems starting in 2026, encouraging in-country inflator assembly. Argentina’s automakers leverage MERCOSUR export routes, while local subsidiaries of global suppliers open smaller plants to bypass tariffs. North America grows at 4.76%; although driver-passenger airbags saturate at 98% fitment, EV platform launches and ongoing Takata replacements sustain nominal upticks.

Europe posts a 5.44% CAGR as the Carbon Border Adjustment Mechanism raises costs on Asian imports from January 2026, motivating tier-ones to establish lower-carbon sites in Poland and Romania. Sodium-azide’s share has already dropped to 26% in Europe, reflecting accelerated REACH compliance. The Middle East and Africa wrestle with counterfeit inflator influxes that depress supplier confidence, while Russia’s 3.51% CAGR lags due to sanctions cutting helium supplies vital for stored-gas modules.

Competitive Landscape

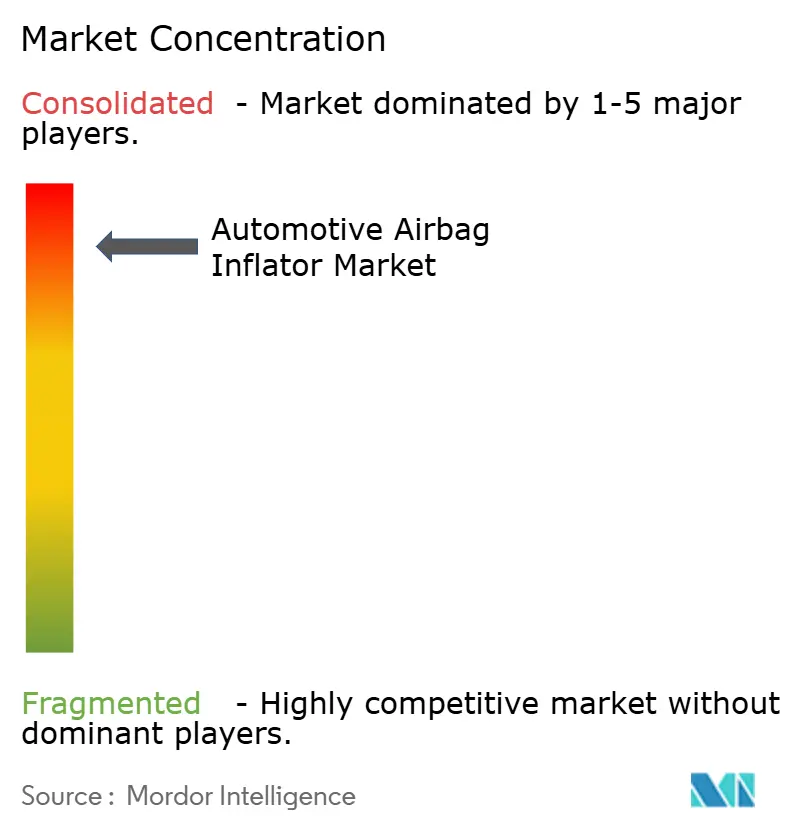

The automotive airbag inflator market is defined by high concentration, with ZF Friedrichshafen, Autoliv, Daicel, and Joyson Safety Systems together accounting for the majority of global revenue. Scale advantages enable these incumbents to align production rhythms with OEM assembly schedules, ensuring dependable, just-in-time deliveries. Their dominance also stems from decades of intellectual property portfolios covering initiator design, propellant formulation, and module integration. Barriers to entry remain steep because new contenders must simultaneously clear stringent homologation tests and forge deep supply-chain ties. As a result, smaller firms often choose to partner with incumbents rather than challenge them outright.

Technology differentiation increasingly shapes competitive dynamics. Patent filings concentrate on hybrid flat-pack inflators that conserve space inside gigacast EV body structures while maintaining steady pressure during long-duration rollovers. Cyber-secured smart modules are gaining momentum after UN Regulation 155 mandated encrypted communication between crash sensors and inflator igniters. Incumbents secure early mover status by embedding microcontrollers that enable over-the-air firmware updates tied to evolving safety logic. These capabilities let suppliers pitch inflators as upgradable components, mirroring trends seen in vehicle infotainment. In parallel, cross-licensing deals reduce litigation risk and accelerate standardization of critical safety features across brands.

Cost-led disruption still bubbles under the surface, particularly from Indian manufacturers that leverage Production-Linked Incentive subsidies. ZF Rane’s new plant in Tamil Nadu reportedly targets production costs 15–18% lower than European equivalents, raising pressure on established firms to localize or risk margin erosion. Sustainability credentials also enter the equation, with suppliers racing to certify low-carbon manufacturing lines to sidestep tariff exposure under the EU Carbon Border Adjustment Mechanism. Counterfeit mitigation strategies remain a unifying priority: Autoliv and ZF are piloting blockchain-based provenance programs that trace every inflator from the initiator assembly to vehicle installation. Collectively, these moves show that even in a concentrated field, innovation routes to fresh competitive angles remain open.

Automotive Airbag Inflator Industry Leaders

-

Autoliv Inc.

-

ZF Friedrichshafen AG

-

Joyson Safety Systems

-

Daicel Corporation

-

ARC Automotive Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Toyota South Africa Motors launched “Don’t Risk it, Fix it,” an expanded Takata airbag recall campaign to replace suspect inflators across Toyota, Lexus, and Hino models.

- June 2025: Toyoda Gosei unveiled a deployable motorcycle-airbag system expected to incorporate faster inflators, lighter fabrics, and smart sensors in subsequent testing phases.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the automotive airbag inflator market as worldwide sales of new pyrotechnic, stored-gas, and hybrid inflators that fill driver, passenger, side, curtain, knee, and pedestrian airbags in passenger cars and commercial vehicles. Revenue is captured at OEM transfer price in U.S. dollars.

Scope Exclusion: Inflators installed during recall repairs or refurbished units aid validation but sit outside the baseline.

Segmentation Overview

-

By Airbag Type

- Passenger

- Curtain

- Knee

- Side

- Pedestrian Protection

-

By Inflator Type

- Pyrotechnic

- Stored-Gas

- Hybrid

-

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

-

By Propellant Chemistry

- Azide-Based

- Non-Azide (e.g., Guanidine Nitrate)

-

By Technology Stage

- Single-Stage

- Dual-Stage & Multi-Stage

-

By Sales Channel

- OEM Fitted

- Aftermarket / Recall Replacement

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- India

- China

- Japan

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- Egypt

- South Africa

- Rest of Middle-East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed module integrators, propellant chemists, and fleet safety managers across Asia, Europe, and the Americas to verify inflator-per-vehicle ratios, hybrid uptake, and price bands that desk sources could not confirm.

Desk Research

Open sources (UN Comtrade HS-950710 trade flows, OICA builds, FMVSS defect files, WHO crash logs, and EU road-safety dashboards) connect rules, production, and inflator need. Company 10-Ks, investor decks, Questel patents, plus D&B Hoovers and Marklines schedules refine technology mix and geography. The list is illustrative; many other references guided our work.

Market-Sizing & Forecasting

We blend top-down and bottom-up logic. Regional light-vehicle builds are multiplied by mandated bag counts and observed fitment, then converted to inflator demand using interview-confirmed ratios. Supplier call-offs, recall tallies, and sampled ASP multiplied by volume anchor value. Key variables include hybrid share, China dual-stage rollout, EV platform mix, propellant costs, and side-curtain penetration. Multivariate regression with scenario analysis projects 2025-30 demand and adds sensitivity bands.

Data Validation & Update Cycle

Outputs face checks versus customs exports, recall volumes, and OEM invoices. Senior analysts review anomalies; models refresh yearly, with interim updates after material events.

Why Mordor's Automotive Airbag Inflator Baseline Earns Trust

Published estimates differ because firms choose unlike scopes, currencies, or refresh rhythms. We exclude recall replacements, apply only validated ratios, and recalibrate each year. Elsewhere, hybrid inflators are often missed and baselines left stale.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.93 B (2025) | Mordor Intelligence | - |

| USD 5.86 B (2024) | Global Consultancy A | counts recall units |

| USD 5.40 B (2024) | Industry Association B | omits hybrid share |

| USD 4.85 B (2023) | Regional Consultancy C | dated production base |

These contrasts show how our refresh cycle and clear scope give decision-makers a balanced baseline traceable to clear inputs.

Key Questions Answered in the Report

What is the current value of the automotive airbag inflator market?

The automotive airbag inflator market equals USD 5.63 billion in 2026.

How fast is the automotive airbag inflator market expected to grow?

The market is projected to post a 7.73% CAGR and reach USD 8.17 billion by 2031.

Which inflator type is growing the quickest?

Hybrid inflators are expanding at an 8.27% CAGR as they balance rapid inflation and sustained pressure.

Which region offers the strongest growth outlook?

Asia-Pacific leads with a 9.42% CAGR, propelled by Chinese ADAS uptake and India’s manufacturing incentives.

Page last updated on: