Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

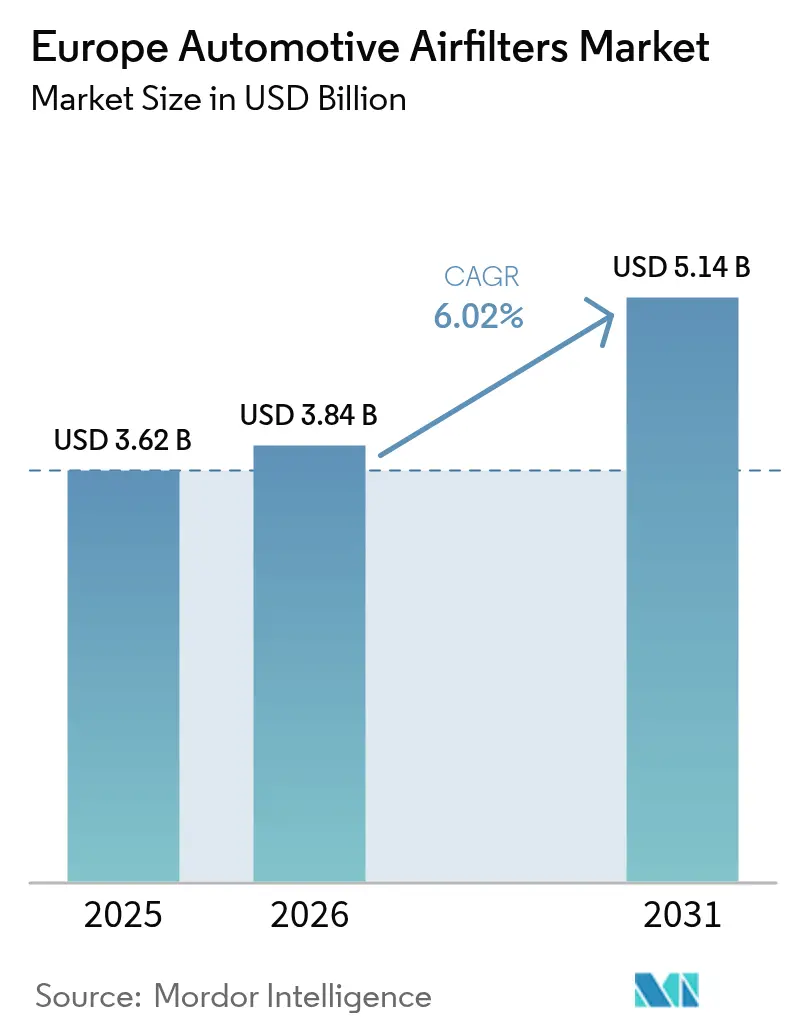

| Base Year Market Size (2025) | USD 3.62 Billion |

| Market Size (2026) | USD 3.84 Billion |

| Market Size (2031) | USD 5.14 Billion |

| Growth Rate (2026 - 2031) | 6.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Airfilters Market Analysis by Mordor Intelligence

The Europe Automotive Airfilters Market size was valued at USD 3.62 billion in 2025 and estimated to grow from USD 3.84 billion in 2026 to reach USD 5.14 billion by 2031, at a CAGR of 6.02% during the forecast period (2026-2031). Strong regulatory momentum around Euro 7, rapid expansion of city-level Low-Emission Zones, and persistent consumer health awareness anchor this expansion. Original-equipment manufacturers (OEMs) are redesigning intake and cabin filtration to meet nanometer-scale particulate limits, and independent aftermarket players are capitalizing on the continent’s aging approximately 280 million-unit vehicle-parc. The Europe automotive air filters market is therefore transitioning from commodity volumes toward value-added performance, positioning filtration as a compliance-critical, consumer-visible, and telemetry-enabled component of next-generation mobility.

Key Report Takeaways

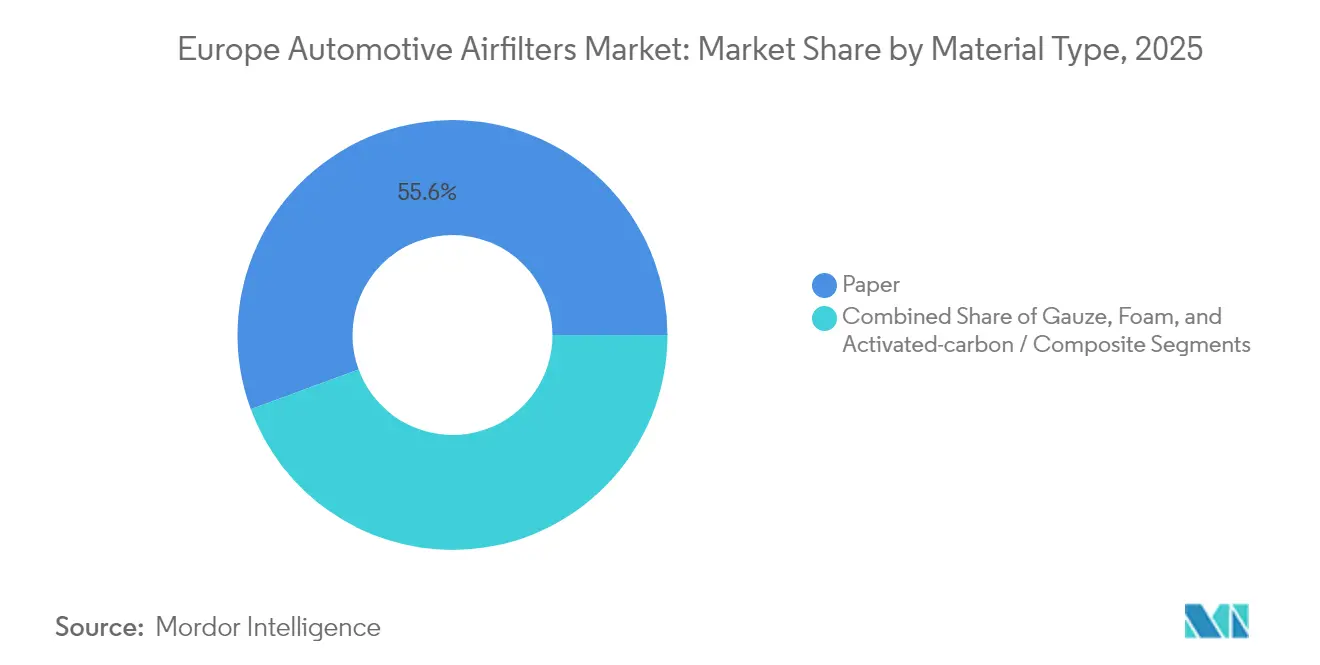

- By material type, paper-based filters dominated with 55.62% of the Europe automotive air filters market share in 2025, whereas activated-carbon and composite variants post the quickest rise at a 6.32% CAGR through 2031.

- By filter type, cabin filters accounted for 60.78% share of the Europe automotive air filters market size in 2025 and will expand at a 6.18% CAGR to 2031.

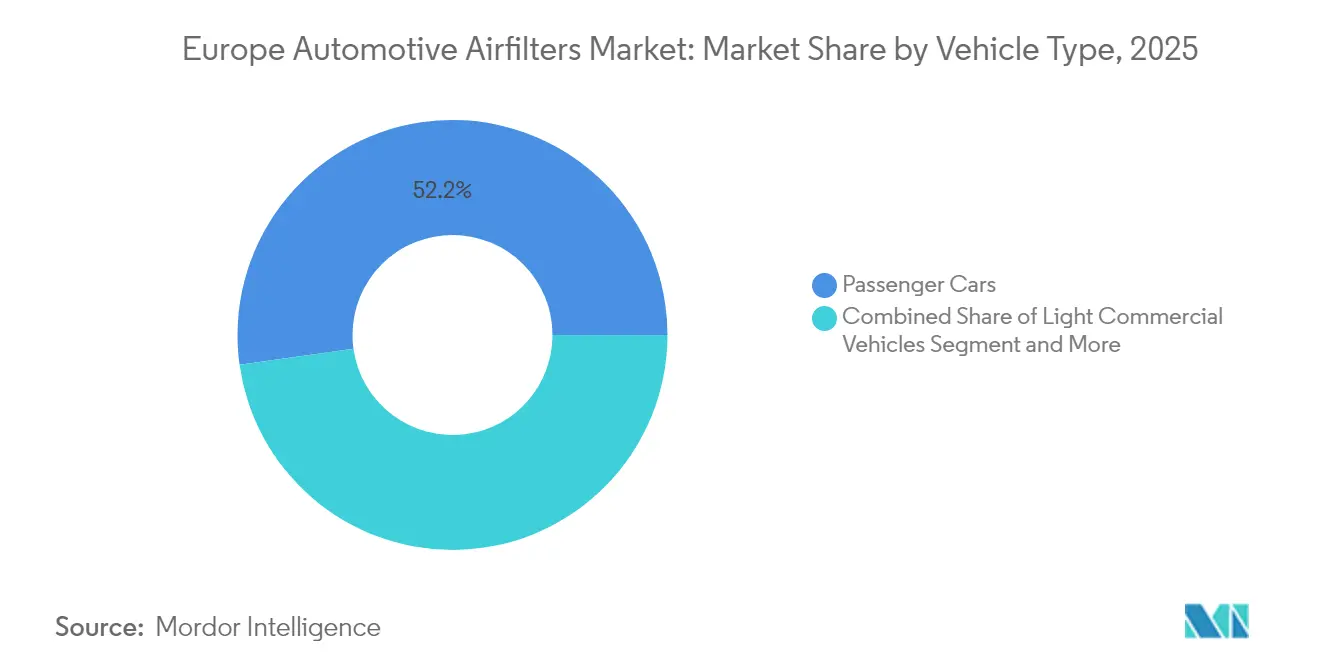

- By vehicle type, passenger cars held 52.21% of the European automotive air filters market share in 2025 while also registering the highest 6.45% CAGR over the forecast period.

- By sales channel, the aftermarket controlled 64.27% of the European automotive air filters market share in 2025; the OEM channel, though smaller, registers the fastest 6.34% CAGR owing to connected-service upsells.

- By country, Germany led with a 48.15% revenue share in 2025 and maintains a solid 6.27% CAGR due to its dense OEM footprint and early Euro 7 compliance preparations.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Automotive Airfilters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing car-parc expanding independent | +1.8% | Pan-European, concentrated in Western Europe | Long term (≥ 4 years) |

| Euro 7 and Euro VI-D emission norms | +1.2% | EU-wide, strongest in Germany, France, Italy | Medium term (2-4 years) |

| Heightened consumer focus on in-cabin air quality | +1.1% | Urban centers across EU, Nordic countries leading | Short term (≤ 2 years) |

| OEM drive for ultra-low pressure-drop media | +0.9% | Germany, Netherlands, Norway, UK | Medium term (2-4 years) |

| Expansion of city-level Low-Emission Zones | +0.8% | Major metropolitan areas, France leading with 40 zones | Short term (≤ 2 years) |

| Subscription-based OTA cabin-air-quality services creating recurring revenue | +0.4% | Premium segments in Germany, UK, Scandinavia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Car-Parc Expanding Independent Aftermarket Demand

Western Europe’s average vehicle age reached 12 years in 2025, while Eastern European fleets stretch to 15-20 years. Older internal-combustion-engine (ICE) models require frequent intake and cabin filter swaps, and independent garages capture a considerable share of the regional aftermarket by offering competitive pricing and broad SKU coverage. Even as BEV penetration removes future intake filter demand, the residual ICE fleet guarantees long-dated volume, keeping the Europe automotive air filters market robust through at least one more full replacement cycle. Aftermarket specialists respond by widening SKU assortments for legacy platforms, introducing private-label activated-carbon cabin elements, and adopting e-commerce marketplaces to reach dispersed rural owners.

Euro 7 and Euro VI-D Emission Norms Accelerating Filter Replacement Cycles

The European Commission published Euro 7 rules in May 2024, introducing 10-nanometer particulate thresholds for gasoline vehicles and lifetime compliance for both tailpipe and non-exhaust particles. Because on-board diagnostics now monitor filter degradation, intake and cabin elements must sustain efficiency far longer than legacy, compressing real-world replacement to as low as possible in high-mileage fleets. OEM-grade suppliers therefore bundle higher-margin, multilayer elements that carry regulatory certificates and embedded RFID tags, lifting revenue per unit and reinforcing the Europe automotive air filters market as a critical compliance lever rather than a discretionary maintenance part.

Heightened Consumer Focus on In-Cabin Air Quality and Allergies

Pandemic-era awareness transformed cabin filtration into a health feature. In July 2024, MANN+HUMMEL commercialized nanofiber cabin filters that remove up to 80% of ultrafine particles while embedding antimicrobial coatings.[1]“Nanofiber Filter Media for Automotive Applications,” MANN+HUMMEL, mann-hummel.com Urban commuters now accept 20-30% price premiums for ISO 18184-certified, allergy-relief filters. Bosch answered with FILTER+pro in January 2024, combining particle, activated-carbon, and anti-viral layers.[2]“FILTER+pro Cabin Air Filter Brochure,” Bosch, bosch.com OEMs bundle HEPA-rated cabin modules in premium trims, while subscription services push annual replacements synced to digital service records. This willingness to pay elevates cabin units from low-margin consumables to margin-rich upgrade items, anchoring CAGR momentum within the Europe automotive air filters market.

OEM Drive for Ultra-Low Pressure-Drop Media to Maximize EV Range

HVAC loads can shave around two fifth of the EV driving range during extreme temperatures, making pressure-drop minimization an energy-saving priority. Filter suppliers deploy pleated nanofiber media and low-tortuosity foams that trim blower energy draw without sacrificing more than 95% particulate capture. German, Dutch, and Norwegian assembly plants already specify less than or equal to 15 Pa pressure-drop cabin filters for next-generation EV programs, lifting demand for advanced synthetics over commodity cellulose. Collaborative testing between Tier-1s and HVAC module makers highlights quantifiable range benefits in type-approval dossiers, ensuring rapid OEM adoption and reinforcing premium-priced supply tiers inside the Europe automotive air filters market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BEV adoption shrinking demand | -1.5% | Norway, Netherlands, Germany leading EV adoption | Medium term (2-4 years) |

| Vehicle downsizing reducing number/size | -0.8% | Urban markets across EU, particularly France, Italy | Short term (≤ 2 years) |

| Supply bottlenecks for specialty non-woven | -0.6% | EU-wide, concentrated in Germany, Italy production hubs | Short term (≤ 2 years) |

| Rising adoption of washable performance filters | -0.3% | Germany, UK premium vehicle markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

BEV Adoption Shrinking Demand for Intake Engine Air-Filters

Battery-electric vehicles do not require combustion air filtration, removing entire intake filter bill-of-materials from new-vehicle demand. Germany assembled 1.35 million EVs in 2024 and is targeting 1.67 million units in 2025 under fleet-average CO₂ rules, while Norway’s new-car market reached majority of BEV share. The Europe automotive air filters market therefore confronts a structural volume headwind, chiefly in premium segments where electrification advances fastest. Counterbalancing growth arises in cabin filters, battery-pack cooling micro-filters, and air-drier cartridges—yet unit counts per vehicle fall on average. Medium-term revenue impact centers on high-value intake elements whose margins historically funded R&D budgets, compelling suppliers to pivot toward composite cabin and thermal-management niches.

Vehicle Downsizing Reducing Number/Size of Filter Elements

Urban congestion fees and rising fuel prices push automakers toward compact vehicle architectures with smaller HVAC housings and reduced filter footprints. In France and Italy, subcompact registrations rose during 2024-2025, enabling cost-driven OEMs to specify thinner filter cassettes or single-stage media where dual-stage designs once stood. The constraint lowers average material consumption per vehicle just as raw-material prices rise, squeezing gross margin even where unit shipments hold steady. Suppliers mitigate by integrating multifunctional layers that combine particulate, gas, and odor capture in one element, preserving ASP but pressuring production yields.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Paper Dominance Faces Composite Challenge

Paper-based filters captured 55.62% of Europe automotive air filters market share in 2025, producing dependable airflow resistance and cost efficiency across high-volume passenger car lines. This traditional substrate underpinned Europe automotive air filters market size for decades, benefitting from mature supply chains and regional pulp processing capacity. Activated-carbon and emerging composite variants, however, are outpacing at 6.32% CAGR to 2031 as consumers demand volatile-organic-compound (VOC) adsorption and allergen neutralization within constrained cabin spaces.

OEMs are layering nanofibers atop cellulose backbones, creating hybrid sheets that trap 10-nanometer particles while holding pressure drops below 15 Pa. Gauze and foam remain niche options in performance tuning and off-highway equipment, respectively, where oil-impregnated layers or oversized pores suit dusty environments. As Euro 7 matures, paper’s share erodes gradually but retains relevance due to recyclable composition and low embodied energy, ensuring coexistence rather than outright displacement inside the Europe automotive air filters market.

By Filter Type: Cabin Filters Lead Growth Trajectory

Cabin filters held 60.78% of the Europe automotive air filters market size in 2025, a position fortified by post-pandemic health concerns, urban smog episodes, and the marketing appeal of allergy certification. The segment grows at a 6.18% CAGR through 2031, outpacing intake filters, because replacement frequency can reach twice per year in polluted metropolitan zones. OEMs integrate filtration cartridge access behind glove boxes, simplifying do-it-yourself swaps and stimulating e-commerce sales by independent parts retailers.

Intake filters, covering the residual share, confront BEV substitution but still service Europe’s large legacy ICE fleet. Turbulence in unit demand pushes suppliers to diversify toward dual-function cabin and HVAC micro-particle elements. Within EVs, cabin filter selection affects HVAC energy draw; thus, advanced low-pressure-drop designs win high-margin factory installs. Connected vehicle dashboards now alert drivers when particulate accumulation spikes, triggering timely replacements and preserving premium unit values across the Europe automotive air filters market.

By Vehicle Type: Passenger Cars Drive Volume Growth

Passenger cars accounted for 52.21% of the Europe automotive air filters market share in 2025 and are set to record the swiftest 6.45% CAGR through 2031 as urban commuters prioritize cabin hygiene and regulatory conformity. Segment expansion leverages the sheer scale of Europe’s assembly total and pan-regional production hubs that standardize filter specifications. Passenger platforms also pilot value-added subscription bundles, further lifting lifetime spend per vehicle.

Light commercial vehicles (LCVs) contribute steady demand because high annual mileage accelerates filter wear, yet growth remains moderate while electrified vans replace diesel models. Heavy commercial vehicles (HCVs) and buses carry fewer units but larger, higher-priced cartridges, stabilizing revenue even as volumes trail passenger cars. Progressive regulatory steps on tire and brake dust emission for buses may unlock new filtration SKUs, sustaining relevance for the Europe automotive air filters market despite drivetrain shifts.

By Sales Channel: Aftermarket Strength Amid OEM Innovation

The aftermarket captured 64.27% of the 2025 European automotive air filters market size by serving an aging fleet via independent workshops and rapidly growing click-and-collect portals. Low switching costs and private-label offerings keep price points competitive, helping the channel retain older ICE models abandoned by branded service centers. Europe's automotive air filters market size for aftermarket ranges expanded with multi-layer cabin cartridges tailored to regional pollen calendars, a strategy fostering repeat purchases.

OEM channels, although smaller, rise at a 6.34% CAGR through 2031 as connected telematics cues predictive maintenance. Automakers bundle filter replacements within extended-service contracts and over-the-air (OTA) vehicle health notifications, shrinking the aftermarket’s share at the premium end. The takeover of Nissens Automotive by Standard Motor Products underscores consolidation as distributors scale to negotiate directly with material suppliers and fight for shelf space in digital marketplaces.

Geography Analysis

Germany accounted for a commanding 48.15% share of the Europe automotive air filters market in 2025, underpinned by 4.1 million passenger vehicles produced. With 1.35 million EVs assembled in 2024 and a 2025 goal of 1.67 million, German OEMs are first movers on Euro 7-compliant, nanofiber intake and cabin filters, due to which the country is also growing rapidly at a CAGR of 6.27% through 2031. Domestic suppliers such as MANN+HUMMEL and MAHLE export advanced media throughout the continent, translating R&D leadership into price premiums and making Germany the focal point of Europe automotive air filters market innovation.

The United Kingdom, France, Italy, and Spain collectively contributed roughly around two fifth of 2025 revenue. France accelerated Low-Emission Zone coverage from 25 to 40 areas in 2025, driving vehicle fleet turnover and higher cabin filter fitment rates. The UK boasts robust aftermarket warehouse distribution that feeds its premium-vehicle parc, making it fertile ground for washable performance filter kits. Italy retains strong filter manufacturing clusters around Turin, while Spain leverages emergent battery pack production in Catalonia, creating adjacent demand for thermal-management micro-filters. Each country aligns with EU harmonized regulations yet differentiates through local economic cycles, influencing replacement intervals and material mix across the Europe automotive air filters market.

The Rest of Europe segment encompasses Nordic and Eastern European states. Norway showcases a near-zero intake filter future, having achieved 90% BEV new-car share in 2024. Conversely, Poland, Romania, and Hungary balance older ICE fleets with slower EV penetration, preserving intake filter volume even as cabin filter upgrades accelerate. Nordic consumers, enjoying high disposable incomes, opt for HEPA-grade multilayer cabin elements despite lower mileage, while Eastern European workshops deliver budget paper media to extend vehicle life. The resulting mosaic demands agile supply chains capable of synchronizing diverse SKUs, regulatory timetables, and consumer price sensitivities within the Europe automotive air filters market.

Competitive Landscape

The Europe automotive air filters market shows moderate consolidation. German headquartered MANN+HUMMEL and MAHLE anchor the landscape, leveraging proprietary media technologies and deep OEM integration. Italian-based Sogefi and diversified conglomerate Robert Bosch bolster competition through cross-platform module offerings. Hengst Filtration widened its geographic reach by purchasing Canada-American Filter Company in June 2024, signaling strategic intent to capture share in cabin and thermal-management niches.

MANN+HUMMEL’s July 2024 nanofiber launch elevates filtration to near-HEPA levels with minimal airflow penalty, aiming squarely at EV HVAC efficiency metrics. Bosch’s FILTER+pro uses a triple-layer structure to neutralize allergens, odors, and viruses, resonating with post-pandemic consumer expectations. Suppliers increasingly embed RFID chips or QR codes on cartridges, enabling lifecycle tracking and predictive replacement prompts through OEM infotainment portals. Partnerships with sensor start-ups integrate real-time cabin air-quality dashboards that sell subscription upgrades alongside genuine filter kits, reinforcing sticky aftermarket revenue.

Simultaneously, independent aftermarketers face margin compression as online price transparency rises. Consolidators such as Standard Motor Products respond by absorbing regional distributors, achieving scale in procurement and logistics. New entrants, particularly materials-science firms capable of electro-spinning nanofiber webs or synthesizing bio-based activated carbons, threaten incumbents unless they secure long-term media supply contracts. Competitive advantage therefore pivots on rapid R&D cycles, vertically integrated media manufacturing, and digital service ecosystems that lock customers into proprietary replacement workflows within the Europe automotive air filters market.

Europe Automotive Airfilters Industry Leaders

Mann +Hummel

MAHLE

Sogefi Group (Purflux)

Robert Bosch GmbH

Donaldson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: MANN+HUMMEL launched nanofiber-based cabin air filters that capture 99.95% of ultrafine particles while extending service life.

- June 2024: Hengst Filtration acquired the Canadian-American Filter Company, adding North American production capacity and expanding product lines.

Europe Automotive Airfilters Market Report Scope

The Europe Automotive Airfilters Market report covers a detailed study on the latest trends and innovations in the market which Material Type (Paper Airfilters, Gauze Airfilters, Foam Airfilters and Others), by Type (Intake Filters and Cabin Filters) and by Vehicle type (Passenger Cars and Commercial Vehicles). Along with the major players, their strategies, innovations, technological advancements and financials are also covered in the report.

By Material Type

| Paper |

| Gauze |

| Foam |

| Activated-carbon / Composite |

By Filter Type

| Intake Filters |

| Cabin Filters |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles & Buses |

By Sales Channel

| OEM |

| Aftermarket |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Material Type | Paper |

| Gauze | |

| Foam | |

| Activated-carbon / Composite | |

| By Filter Type | Intake Filters |

| Cabin Filters | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles & Buses | |

| By Sales Channel | OEM |

| Aftermarket | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe automotive air filters market?

The market stands at USD 3.84 billion in 2026 and is projected to reach nearly USD 5.14 billion by 2031, reflecting a 6.02% CAGR.

How will Euro 7 rules influence filter demand?

Euro 7 imposes nanometer-scale particulate limits and lifetime compliance, shortening replacement intervals to roughly 10,000 km for high-mileage vehicles and elevating demand for premium, certified filters.

Which filter segment is growing the fastest?

Cabin filters lead growth at a 6.18% CAGR due to heightened consumer health concerns, subscription-based services, and their relevance in both ICE and EV platforms.

How does BEV adoption affect the market?

BEVs eliminate intake engine filters, reducing volumes in that segment, yet they increase demand for low-pressure-drop cabin filters and new battery-cooling micro-filters.

Why does Germany hold nearly half the regional market?

Germany’s dense OEM base, early Euro 7 preparedness, and leadership in EV production drive high domestic demand and exportable filtration innovations.

Are washable filters a threat to disposable filter sales?

Yes, especially within premium vehicle segments, as reusable units lengthen replacement cycles, but suppliers are countering with multi-layer disposable solutions offering superior gas and pathogen adsorption.

Page last updated on: