Automotive Airbag Fabric Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.72 Billion |

| Market Size (2030) | USD 3.39 Billion |

| Growth Rate (2025 - 2030) | 4.51% CAGR |

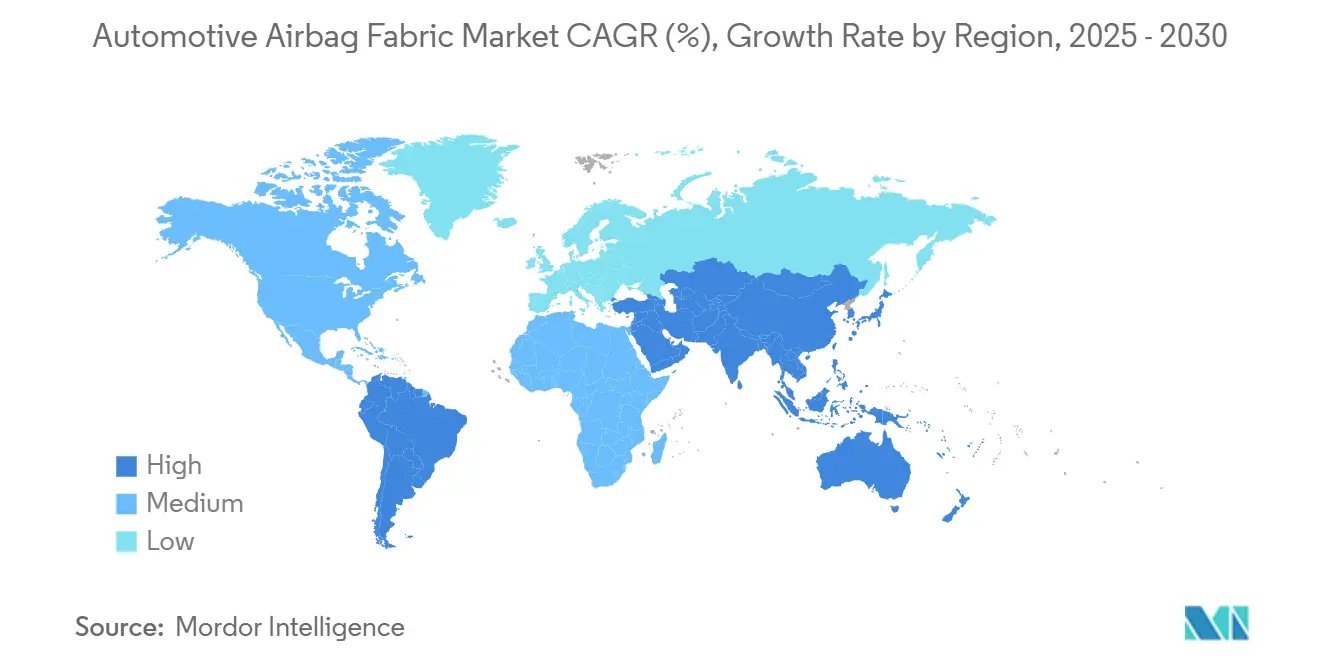

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Airbag Fabric Market Analysis by Mordor Intelligence

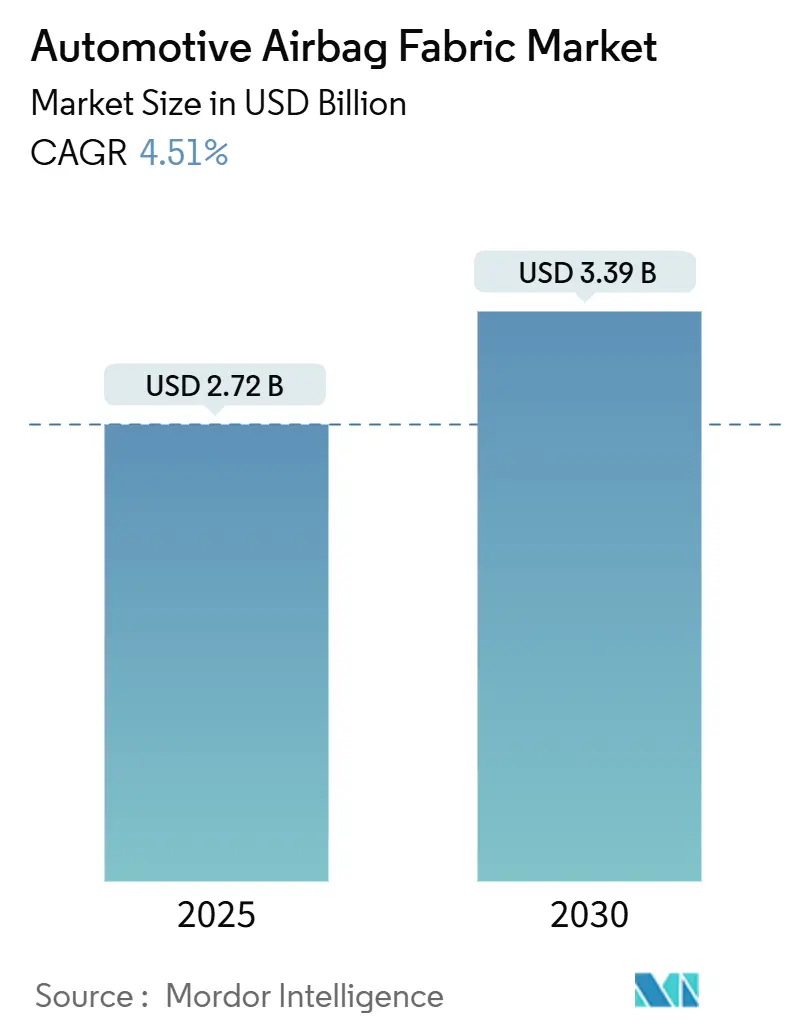

The Automotive Airbag Fabric Market size is estimated at USD 2.72 billion in 2025, and is expected to reach USD 3.39 billion by 2030, at a CAGR of 4.51% during the forecast period (2025-2030). Steady demand stems from national safety mandates, robust SUV and light commercial vehicle (LCV) production, and continuous improvements in high-tenacity weaving and silicone-coating processes that heighten gas-tight performance. Polyamide yarn retains broad preference for its heat and abrasion resistance, yet polyester is gaining traction as automakers look for lower-density, lower-carbon alternatives. Fabric suppliers able to scale recycled-content polyamide, integrate advanced coatings, and guarantee vertical control of raw materials occupy a defensible competitive position. Meanwhile, pedestrian-protection and battery-shielding airbags create avenues for specialty external fabrics with UV and weather durability requirements.

Key Report Takeaways

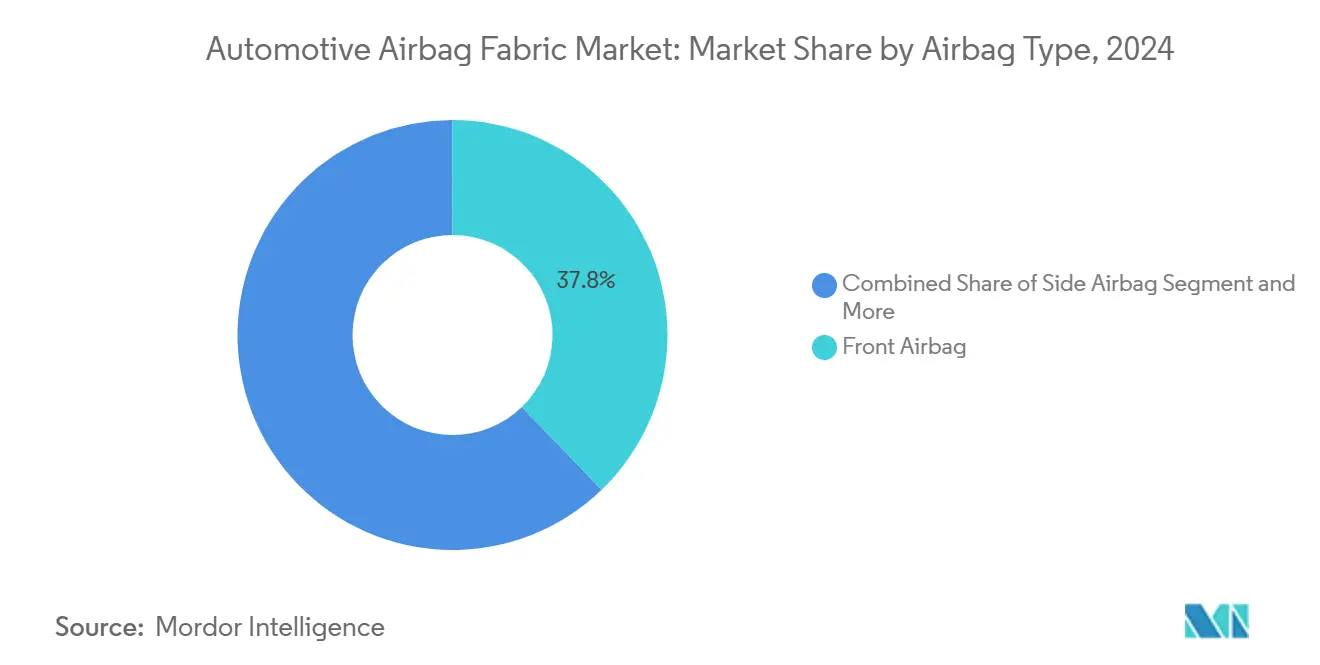

- By airbag type, front airbags led with 37.83% of the automotive airbag fabric market share in 2024, while the curtain airbags segment is expected to grow at a 4.53% CAGR during the forecast period (2025-2030).

- By yarn type, polyamide captured 64.31% share of the automotive airbag fabric market in 2024; polyester is projected to expand at a 4.58% CAGR during the forecast period (2025-2030).

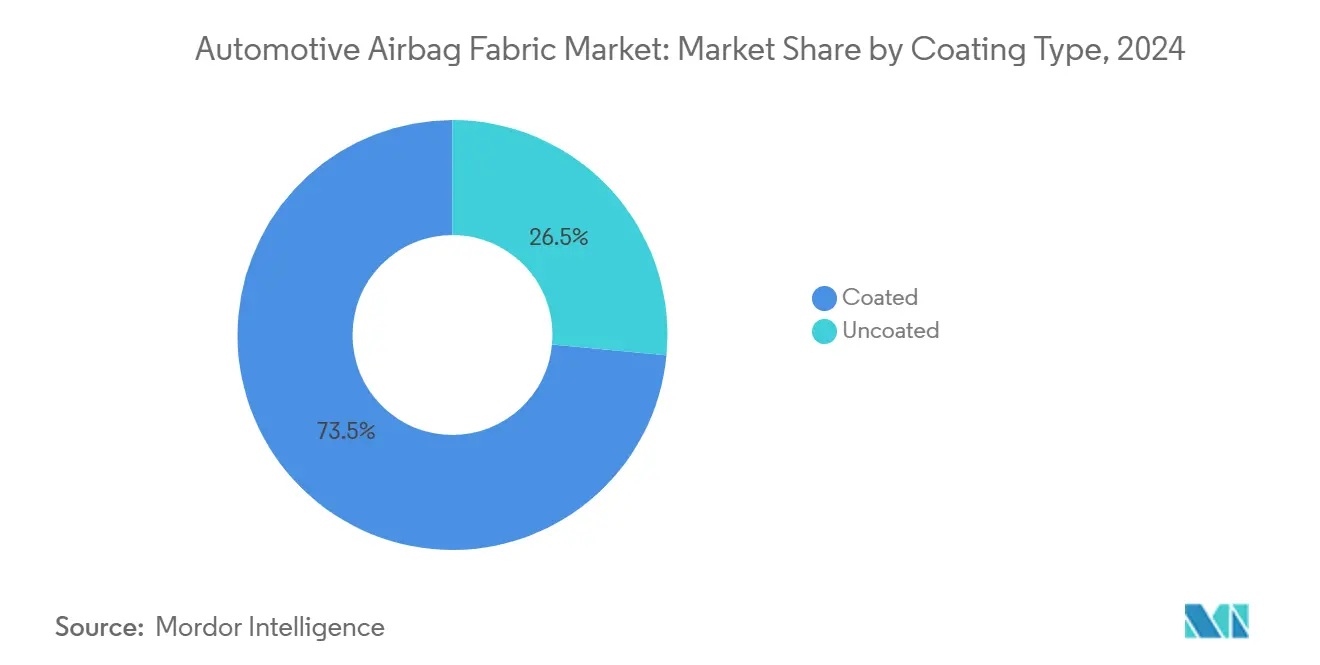

- By coating type, coated fabrics commanded a 73.48% share of the automotive airbag fabric market in 2024, whereas the uncoated fabrics segment is expected to grow at a 4.61% CAGR during the forecast period (2025-2030).

- By vehicle type, passenger cars held a 66.33% share of the automotive airbag fabric market in 2024; the light commercial vehicles segment is expected to grow at a 4.55% CAGR during the forecast period (2025-2030).

- By geography, Asia-Pacific accounts for a 39.82% share of the automotive airbag fabric market in 2024; the South America segment is expected to grow at a 4.52% CAGR during the forecast period (2025-2030).

Global Automotive Airbag Fabric Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Safety Mandates | +1.2% | Global, with early gains in India, EU, China | Medium term (2-4 years) |

| Rising Vehicle Production Volumes | +0.9% | Asia Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Increasing Adoption Of Side and Curtain Airbags | +0.8% | Global, led by developed markets | Medium term (2-4 years) |

| Advances In High-Tenacity Weaving Technologies | +0.6% | Global manufacturing hubs | Long term (≥ 4 years) |

| Lightweight Fabric Demand | +0.5% | Global, concentrated in EV markets | Medium term (2-4 years) |

| Emergence Of Pedestrian-Protection External Airbags | +0.4% | Japan, EU early adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Safety Mandates In Major Markets

Global regulations now stipulate broader airbag coverage, reshaping the automotive airbag fabric market. India’s six-airbag rule for all new passenger vehicles, effective October 2024, adds fabric demand for a good number annually [1]“Gazette Notification on Airbag Requirements,” Ministry of Road Transport and Highways, morth.nic.in . Euro NCAP’s 2026 protocol introduces pedestrian-protection scoring, incentivising external airbags crafted with weather-resistant textiles. China continues to tighten occupant-protection norms, and NHTSA’s FMVSS 305a covers battery-compartment protection. Each standard also prescribes deployment timing and gas retention benchmarks, prompting automakers to specify silicone-coated, high-tenacity weaves. Consequently, fabric suppliers that align products precisely to these evolving performance metrics secure higher value contracts.

Rising Vehicle Production Volumes, Especially SUVs & LCVs

SUVs generally integrate six to eight airbags versus four to six in sedans, lifting per-vehicle fabric surface requirements. Recovering production in India, China, and the United States amplifies volume demand across the automotive airbag fabric market. LCV electrification brings new customers prioritising safety ratings for lower insurance premiums and regulatory compliance, creating fresh orders for oversized cushions. Higher throughput lets manufacturers realise economies of scale in high-strength yarns and advanced coating lines, stabilising margins even as unit prices edge lower.

Increasing Adoption Of Side & Curtain Airbags

Modern crash-test protocols emphasise occupant head protection during rollover and side impacts, accelerating curtain-airbag installation. Curtain cushions extend across multiple seating positions and call for fabrics engineered for controlled tear propagation, precise tethering, and extended inflation. Side airbags, squeezed into door panels, need ultra-thin textiles that still tolerate fast gas flow. India’s new mandate explicitly targets side-impact protection, widening global demand. Automakers also integrate rollover sensors and pre-crash logic, so fabrics must perform reliably under multi-stage inflation.

Advances In High-Tenacity Weaving & Silicone-Coating Technologies

Weaving improvements boost strength-to-weight ratios, enabling lighter cushions that meet burst-pressure thresholds. Innovative silicone formulations seal fabrics with lower permeability for long-duration external airbags while offering fire retardancy essential for battery-shielding applications. Water-borne coatings reduce volatile organic compound emissions, helping OEMs meet sustainability metrics. Suppliers that invest in inline infrared spectroscopy for coating-thickness control report scrap-rate reductions and consistent fabric grammage—key attributes when OEM audits intensify.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Polyamide and Silicone Raw-Material Prices | -0.7% | Global, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Supply-Chain Concentration | -0.5% | Global, with Asia Pacific exposure | Medium term (2-4 years) |

| Product Recalls and Litigation Risk | -0.5% | Global, with heightened exposure in North America and EU | Medium term (2-4 years) |

| Shift Toward Advanced Seat-Belt Load Limiters | -0.4% | Developed markets, led by EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility In Polyamide & Silicone Raw-Material Prices

Polyamide cost swings track crude-oil derivatives and plant-utilisation rates, crimping margins even for integrated suppliers. INVISTA’s Shanghai expansion doubled Nylon 6,6 capacity to 400,000 tonnes but did not eliminate feedstock sensitivity [2]“Shanghai Nylon 6,6 Polymer Expansion Completed,” INVISTA, invista.com . Silicone dispersions add another volatile component, as few producers can meet automotive-grade purity and rheology specs. Automakers often demand fixed-price contracts, so fabric makers shoulder raw-material risk and currency exposures that erode profitability.

Supply-Chain Concentration In A Handful Of Yarn Makers

Three producers—INVISTA, BASF, and Hyosung—control most automotive-grade polyamide yarn lines, heightening dependence on their allocation strategies. Capital intensity and quality requirements deter new entrants, while sustainability imperatives narrow the field to suppliers offering recycled content. Trade disputes or force-majeure events can suddenly curtail yarn deliveries, compelling fabric mills to prolong inventory cycles and carry higher working capital.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Airbag Type: External Systems Drive Innovation

Front airbags retained a 37.83% share of the automotive airbag fabric market in 2024, underscoring their core role in the target market. Curtain airbags, however, are forecast at a 4.53% CAGR during the forecast period (2025-2030), as regulators prioritise head-impact mitigation. Additional demand for square-meter fabric arises from the curtain’s cabin-spanning geometry, encouraging mills to refine weave uniformity along bolt widths to preclude weak tear lines. External airbags for pedestrian protection demand specialised silicone encapsulation that ensures rapid deployment while resisting ultraviolet degradation and temperature swings.

Automakers experimenting with multi-deployment logic require fabrics that tolerate repeated gas pulses without delamination. Front cushions remain cost-sensitive, pushing suppliers toward lean production and rigid statistical-process controls. Curtain units offset lower volumes with higher unit margins because of advanced material requirements. Side, knee, and thorax airbags hold steady demand, yet pedestrian-oriented cushions signify the next revenue runway as Euro NCAP attaches rating points to their adoption.

By Yarn Type: Polyamide Dominance Faces Sustainability Pressure

Polyamide yarn held a 64.31% share of the automotive airbag fabric market in 2024. Heat resistance, elongation at break, and abrasion durability maintain its primacy for both interior and emerging exterior airbags. Polyester’s 4.58% CAGR during the forecast period (2025-2030) arises from its density advantage and lower greenhouse-gas footprint, appealing to automakers’ lightweighting and scope-3 emission goals. Manufacturers weave polyester into cost-constrained LCV cushions, especially in geographies with limited prolonged high-temperature exposure.

Research centres emphasise recycled polyamide pellets derived from post-industrial fibre scrap, overcoming viscosity loss via chain-extending additives. Asahi Kasei’s PFAS-free grade demonstrates how novel formulations can answer regulatory pressures while sustaining mechanical performance. Blended-yarn warps containing polyamide and polyester also appear in pilot trials, balancing heat resistance and cost. Until polyester’s melting temperature can withstand multi-stage gas pulses, polyamide remains requisite for critical external shields and rollover curtains.

By Coating Type: Gas-Tight Performance Drives Coated Demand

Coated fabrics captured 73.48% of the automotive airbag fabric market share in 2024. Silicone layers as thin as 30 µm cut permeability below 0.2 L/decimeter per minute, assuring consistent pressure retention even under cold-soak conditions. Advanced water-borne dispersions meet volatile-organic-compound limits while reducing bake-oven dwell times, thereby trimming energy consumption.

Uncoated cushions, projected at a 4.61% CAGR during the forecast period (2025-2030), continue in low-permeability front-airbag platforms where cost overrides extended hold-time requirements. External and pedestrian airbags need dual-layer coatings: one for gas seal, another for hydrophobicity and UV resilience. Mills invests in inline laser micrometers that verify dry-film thickness every meter, minimising overusing expensive silicone. Coating uniformity also facilitates thinner base fabrics, indirectly lowering total cushion mass and packing size.

By Vehicle Type: Commercial Segments Accelerate Growth

Passenger cars represented 66.33% of global revenue in 2024. Safety ratings and consumer demand keep volumes high, yet the 4.55% CAGR expected in LCVs during the forecast period (2025-2030), outpaces passenger-car growth. Electrified vans introduce battery-underbody shields that double as side-impact barriers, thus expanding fabric consumption per chassis.

Medium-duty trucks increasingly outfit side and rollover curtains to manage insurance premiums and comply with fleet-buyer policies. India’s Bharat NCAP extends crash-test coverage to pickup platforms, spurring fabric uptake in traditionally price-sensitive segments. Public-transport buses also add passenger head-protection curtains, leveraging the same high-tenacity weaves designed initially for SUVs. Larger cab volumes of North American pickups demand higher fabric square meters per vehicle than compact sedans, bolstering regional demand elasticity.

Geography Analysis

Asia-Pacific contributed 39.82% of global 2024 revenue, anchored by China’s high-volume assembly plants and India’s six-airbag mandate that amplifies per-vehicle cushion count. Japanese OEMs pioneer external airbags, making the region a testbed for weather-resistant fabrics that must survive typhoon-season humidity. Vertical integration in polyamide yarn production, capped by INVISTA’s Shanghai expansion, confers local supply security that trims lead times for cushion stitching lines.

Europe remains a premium-car stronghold where buyers and regulators value five-star safety ratings. Euro NCAP’s 2026 update elevates pedestrian-protection metrics, steering fabric demand from interior to exterior applications requiring UV-stable silicone coatings. Environmental legislation favours recycled polyamide content, prompting European mills to qualify secondary-feedstock grades without compromising burst pressure.

North America sees steady growth tied to strong SUV and pickup demand; larger cabin volumes translate into greater fabric usage per unit. NHTSA’s focus on electric-vehicle battery containment fosters niche cushions adjacent to pack enclosures. South America, led by Brazil, posts the fastest 4.52% CAGR as domestic assemblers adopt global passenger-protection standards and integrate side airbags into low-cost platforms. The Middle East and Africa advance more slowly, yet high solar load spurs interest in UV-resistant external fabrics for desert climates.

Competitive Landscape

Toray Industries, Toyobo, and Hyosung Advanced Materials collectively held slightly above half of 2024 revenue, evidencing moderate consolidation in the automotive airbag fabric market. Vertical control over polyamide spinning lines allows these firms to hedge raw-material volatility and assure yarn quality traceability. Capital-intensive looms employing air-jet technology deliver high-tenacity weaves at scale, while proprietary silicone recipes differentiate coating uniformity.

Mid-tier suppliers such as Kolon Industries and Seiren focus on regional OEM programs, balancing cost with localised technical support. They exploit process know-how in lean weaving to lower gram-per-square-meter metrics without sacrificing tensile strength. White-space entrants, including speciality coating houses, court external-airbag contracts by offering UV-stable dual-layer systems that incumbent mills still pilot.

Patent activity continues: General Motors filed a fender-mounted pedestrian cushion design, whereas Toyota explores hood-edge airbags integrating shape-memory alloys for rigidized deployment. Sustainability imperatives drive collaboration; European OEMs encourage mills to certify recycled-content yarns under ISO 14067 carbon-footprint audits. Competitive intensity, therefore, revolves around balancing price, sustainability readiness, and rapid customisation for next-generation deployment scenarios.

Automotive Airbag Fabric Industry Leaders

Toray Industries Inc.

Toyobo Co., Ltd.

Hyosung Advanced Materials

Teijin Limited

Kolon Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Asahi Kasei announced PFAS-free polyamide resin grades to be showcased at K 2025, targeting automotive airbags requiring low-friction performance and environmental compliance.

- April 2025: Subaru introduced the world’s first cyclist-protection external airbag in the 2025 Forester for the Japanese market, utilising a U-shaped cushion that deploys at the hood-windshield junction.

- August 2024: INVISTA completed a RMB 1.75 billion expansion at Shanghai Chemical Industry Park, doubling Nylon 6,6 capacity to 400,000 tonnes for automotive fabric applications.

Global Automotive Airbag Fabric Market Report Scope

| Front Airbag |

| Side Airbag |

| Knee Airbag |

| Curtain Airbag |

| Other Airbags |

| Polyamide |

| Polyester |

| Coated |

| Uncoated |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy-duty Trucks |

| Buses and Coaches |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Airbag Type | Front Airbag | |

| Side Airbag | ||

| Knee Airbag | ||

| Curtain Airbag | ||

| Other Airbags | ||

| By Yarn Type | Polyamide | |

| Polyester | ||

| By Coating Type | Coated | |

| Uncoated | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy-duty Trucks | ||

| Buses and Coaches | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the automotive airbag fabric market?

The market is valued at USD 2.72 billion in 2025 and is forecast to rise to USD 3.39 billion by 2030.

Which airbag type is growing the fastest?

Curtain airbags exhibit the highest 4.53% CAGR due to heightened head-protection regulations.

Why are coated fabrics preferred?

Silicone-coated fabrics seal gas efficiently, achieving 73.48% 2024 revenue and meeting rigorous retention standards for newer external airbags.

How will electric vehicles influence demand?

EVs need lightweight yet heat-resistant fabrics to offset battery mass and shield packs, driving uptake of thinner high-tenacity weaves.

Which region leads consumption?

Asia-Pacific commands 39.82% of 2024 revenue, propelled by India’s six-airbag rule and China’s large-scale vehicle output.

Who are the leading suppliers of polyamide yarn?

INVISTA, BASF, and Hyosung dominate global Nylon 6,6 capacity, underpinning much of the supply for automotive airbag fabrics.

Page last updated on: