Engine Air Filter Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

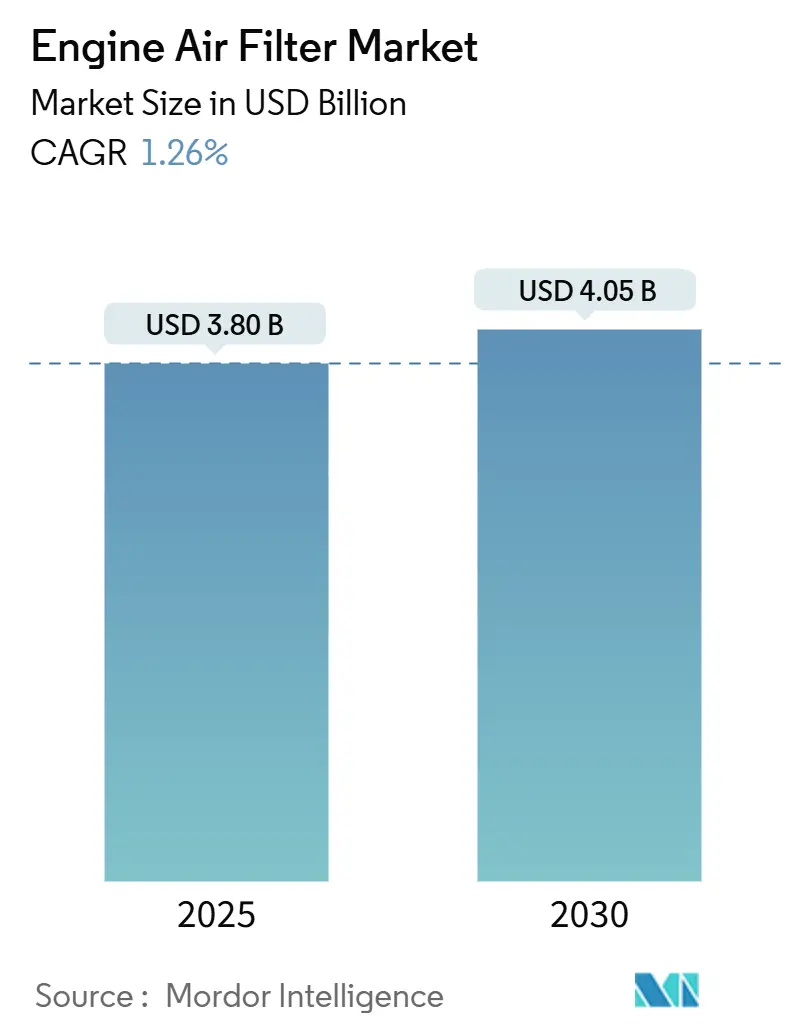

| Market Size (2025) | USD 3.80 Billion |

| Market Size (2030) | USD 4.05 Billion |

| Growth Rate (2025 - 2030) | 1.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Engine Air Filter Market Analysis by Mordor Intelligence

The engine air filter market size stands at USD 3.8 billion in 2025 and is set to reach USD 4.05 billion by 2030, reflecting a 1.26% CAGR during the forecast period. This outlook underscores a maturing industry in which replacement volumes grow steadily despite the headwinds posed by accelerating battery-electric vehicle adoption. Demand resilience stems from tighter global emission rules that lift filtration performance standards, the growing pool of high-utilization commercial fleets that shorten replacement cycles, and technology shifts toward synthetic and nanofiber media. At the same time, the industry must navigate raw-material cost swings and the structural volume loss that accompanies electric-powertrain penetration. Competitive intensity remains moderate as leading suppliers defend share through proprietary media, wider manufacturing footprints, and expanding service propositions connected to predictive maintenance.

Key Report Takeaways

- By filter type, paper filters led with 39.62% of the engine air filter market share in 2024, while synthetic oil filters are projected to expand at a 3.26% CAGR through 2030.

- By material type, paper media accounted for 41.23% of the engine air filter market share in 2024, whereas synthetic media will record the fastest growth at a 3.28% CAGR to 2030.

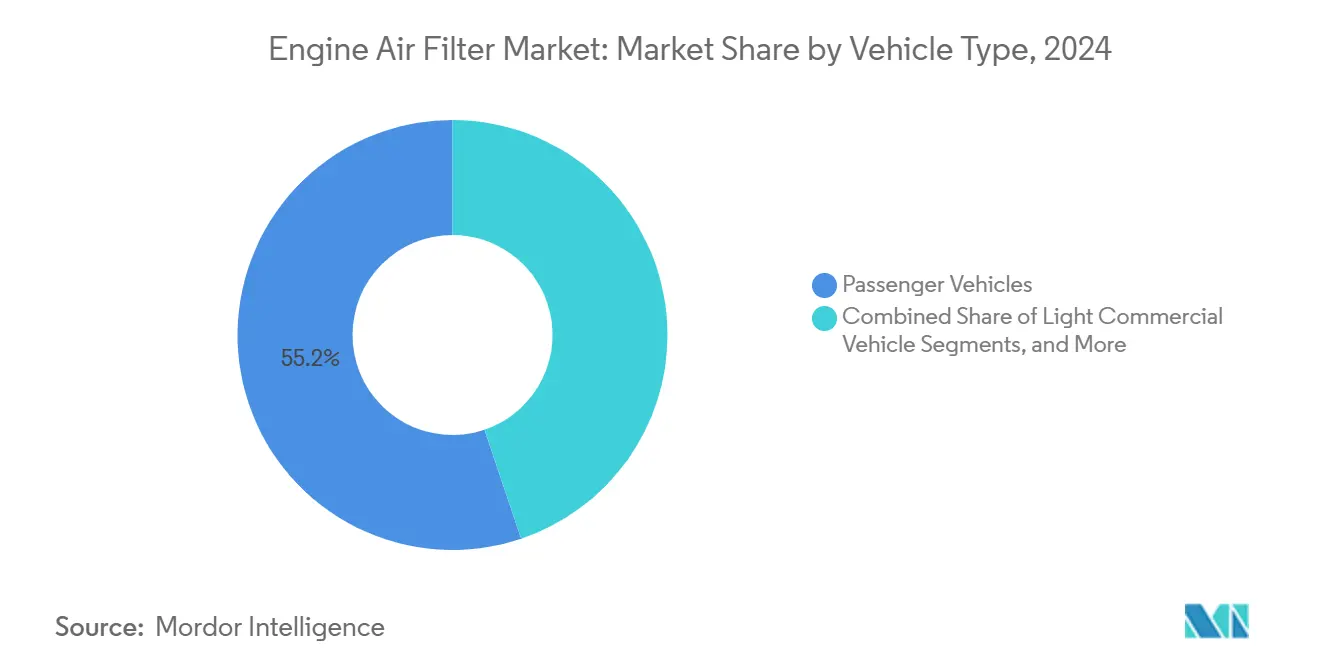

- By vehicle type, passenger cars held 55.18% of the engine air filter market share in 2024, and light commercial vehicles will post the highest forecast CAGR at 2.88% through 2030.

- By distribution channel, OEM fitments captured 63.72% of the engine air filter market share in 2024, yet the aftermarket is expected to advance at a 2.96% CAGR during the forecast period.

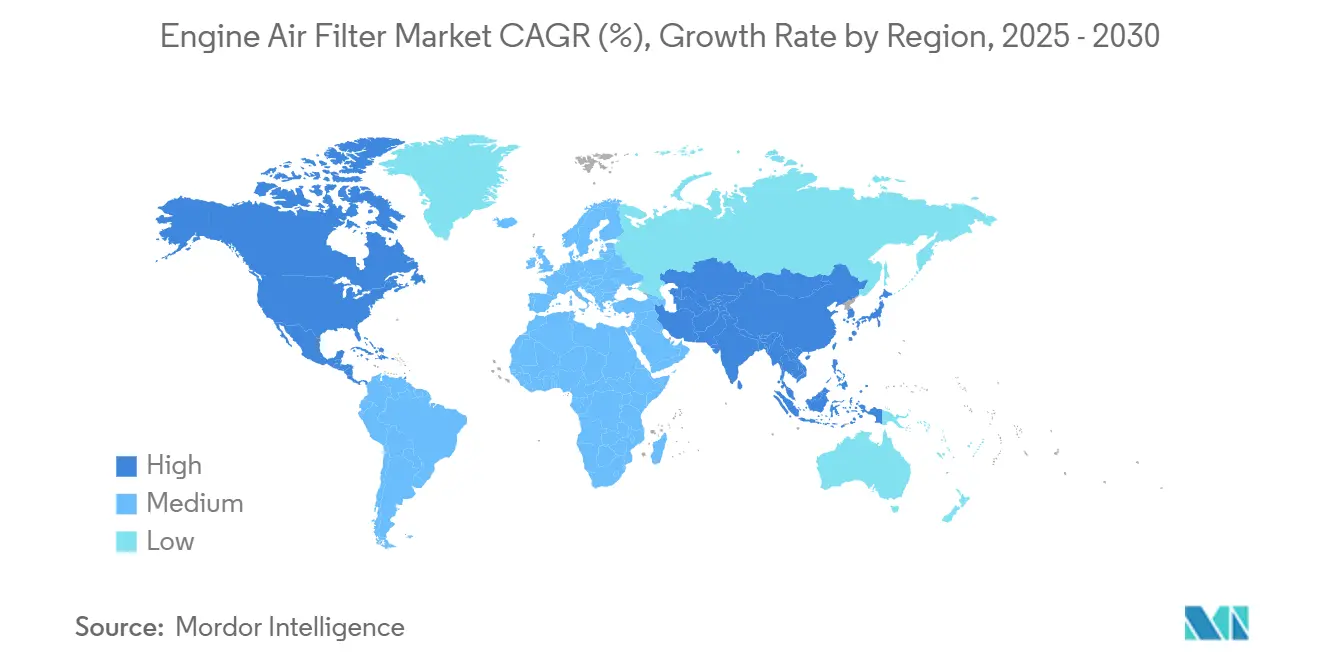

- By geography, Asia-Pacific commanded 45.43% of the engine air filter market share in 2024 and is on track for a 3.86% CAGR through 2030.

Global Engine Air Filter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Global Emission Standards | +0.4% | EU, North America early; global roll-out | Medium term (2-4 years) |

| Expanding Global ICE Vehicle Parc | +0.3% | Core Asia-Pacific, spill-over to Middle East and Africa and South America | Long term (≥ 4 years) |

| Advancements in Synthetic and Nanofiber Media | +0.3% | Global, fastest uptake in developed markets | Medium term (2-4 years) |

| After-Sales Maintenance Awareness Surge | +0.2% | North America and EU, emerging in Asia-Pacific cities | Short term (≤ 2 years) |

| High-Utilization E-Commerce Logistics Fleets | +0.2% | North America, EU and Asia-Pacific metropolitan areas | Short term (≤ 2 years) |

| Smart Sensor-Enabled Intake Modules | +0.1% | Premium vehicle segments worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Global Emission Standards

Worldwide regulations now target filtration efficiency near 99.0% for particles above 0.3 microns under frameworks such as Euro 7 and EPA Tier 3. OEMs have therefore shifted sourcing toward synthetic and nanofiber media that meet the higher capture thresholds while preserving airflow[1]“Bosch develops high-efficiency multi-layer media,”, Robert Bosch GmbH, bosch.com. Compliance timelines stretching to 2026 in Europe and similar schedules in North America underpin steady specification upgrades across new models. Emerging markets follow with India’s BS-VII rules planned for 2028, extending demand momentum. Retrofits on older vehicles create an additional revenue stream for suppliers offering certified upgrade kits. Sustainable manufacturing credentials audited under ISO 14001 increasingly factor into tier-1 sourcing decisions.

Expanding Global ICE Vehicle Parc

Even as the world pivots to electrification, developing nations still significantly increase their annual intake of internal combustion engine (ICE) vehicles[2]“Global ICE Vehicle Parc Growth Outlook,”, UFI Filters, ufi-filters.com. Longer vehicle life—now often exceeding 15 years- means the cumulative parc requiring replacement filters keeps rising. Commercial trucks grow briskly with freight demand, generating high-frequency service cycles. Aged vehicles exiting warranty migrate to independent repair channels, where filter change intervals shorten, supporting aftermarket unit growth. Fleet operators quantify fuel-economy gains from timely filter maintenance and increasingly specify premium media.

Advancements in Synthetic and Nanofiber Media

Setting new performance benchmarks, synthetic and nanofiber filtration technologies offer remarkably high filtration efficiency and a prolonged service life compared to paper alternatives, positioning them as a premium yet cost-effective solution over the ownership cycle[3]“FormulaUFI Synthetic Media Technical Sheet,”, UFI Filters, ufi-filters.com. Proprietary multi-layer designs reduce pressure drop, enhancing combustion efficiency. Mass-production investments have lowered per-unit costs, accelerating adoption beyond luxury segments. Suppliers promote total-cost-of-ownership savings to fleet managers, reinforcing the migration from traditional cellulose media. As volumes scale, synthetic filters are expected to overtake paper in complex powertrains requiring stable airflow under variable load.

After-Sales Maintenance Awareness Surge

Higher-income households increasingly adopt do-it-yourself (DIY) vehicle maintenance to manage repair costs. Budget concerns and access to online guides and e-commerce kits drive this shift, reshaping service norms and expanding personal vehicle care. Digital tutorials highlight the link between clean intake air and reduced fuel consumption, encouraging proactive filter changes. Mobile service models add convenience by performing replacements at home or work and lifting attachment rates. Independent workshops report a rise in filter-specific bookings as motorists favor preventive care over costly engine repairs. The aftermarket gains volume, even in regions with high dealership density.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid BEV Penetration | -0.5% | Led by EU and China, spreading worldwide | Medium term (2-4 years) |

| Raw-Material Price Volatility | -0.2% | Global, most acute in cost-sensitive emerging markets | Short term (≤ 2 years) |

| Adoption of Washable/Re-Usable Filters | -0.1% | Performance segments, broadening gradually | Long term (≥ 4 years) |

| Counterfeit Products in Aftermarket | -0.1% | Emerging markets, online channels globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid BEV Penetration

Battery-electric vehicles dominated in China during 2024, and European policy targets aim for 100% zero-emission sales by 2035, structurally removing the need for engine air filters. Early adoption concentrates on premium models traditionally using higher-value filters, eroding revenue faster than unit volumes suggest. Commercial fleets also electrify, compounding the impact. Hybrid growth offsets some losses because those powertrains still rely on combustion air handling, yet the overall effect remains a headwind over the forecast window.

Raw-Material Price Volatility

Synthetic fiber costs jumped in 2024 with petrochemical supply disruptions, while pulp prices for paper media climbed. Currency swings intensify margin pressure for globally integrated suppliers. Manufacturers respond by localizing production where feasible and realigning portfolios toward higher-margin synthetic lines. However, price sensitivity in emerging markets restricts full pass-through, threatening profitability when input spikes persist. Strategic stockpiling and long-term supply contracts are increasingly employed to stabilize costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Filter Type – Synthetic Technologies Drive Innovation

Paper/Cellulose filters retained a 39.62% engine air filter market share in 2024, thanks to cost advantages and universal OEM acceptance. Synthetic oil filter recorded the swiftest expansion at a 3.26% CAGR and is on track to outpace paper volumes beyond 2030. The engine air filter market benefits from synthetic media’s ability to sustain airflow under higher contamination loads, making them attractive for turbocharged and direct-injection engines. Gauze and foam designs serve niche off-road and motorcycle uses where washability or oil impregnation is valued. Stainless-steel mesh variants occupy specialized industrial engines that operate in abrasive environments. Suppliers showcase synthetic lines as the mid-term mainstream, citing total-cost-of-ownership savings that offset higher shelf prices.

The segment continues to absorb R&D spending to balance pore-size uniformity with low pressure drop. Bosch’s FILTER+pro cabin filter launch in 2024 hints at cross-application material synergies likely to spill into intake filtration. Technology migration follows a top-down pattern: performance cars adopt first, followed by light commercial fleets and eventually entry-level models. As manufacturing scale expands, unit pricing converges with paper, catalyzing broader adoption across the engine air filter market.

By Material Type – Paper Dominance Faces Synthetic Challenge

Paper media commanded 41.23% share of the engine air filter market in 2024, reflecting mature manufacturing networks and acceptance in price-sensitive segments. Synthetic material recorded a 3.28% CAGR, making it the fastest-growing slice of the engine air filter market through 2030. Cotton gauze products, popular among performance enthusiasts, retain modest volume but outsized revenue because of premium pricing and extended service life. Foam and metal mesh address special-purpose engines, especially in agriculture and construction. Advances in polymer science allow blended multilayer constructs that pair synthetic fibers with fine cellulose to achieve both low restriction and high dust-holding capacity.

OEM engine downsizing and turbocharging raise the importance of maintaining stringent airflow metrics, pushing the shift toward synthetics. Regulatory pressure for recyclable content also favors non-cellulose blends that integrate bio-based polymers. Suppliers report that 100% of new OE quotations in 2025 require sustainability disclosures, indicating that material choice will continue to evolve in tandem with environmental priorities.

By Vehicle Type – Commercial Segments Accelerate Growth

Passenger cars delivered a 55.18% share of the engine air filter market in 2024, underscoring their numeric dominance. Light commercial vehicles, buoyed by e-commerce logistics, exhibit a 2.88% CAGR to 2030, outpacing every other segment. Utilization intensity—often triple that of personal cars—quickly saturates paper elements, prompting fleet operators to migrate to synthetic units that double service intervals. Medium and heavy trucks maintain stable demand tied to macro freight trends, benefiting the engine air filter market size as ton-kilometers expand in developing economies. Two-wheeler filters remain a large but low-value volume contributor, especially in Asia, though emission rules there will steadily pivot the segment toward better media.

Replacement parts pricing for commercial fleets rose in 2024, with air filters singled out among the fastest-inflating items. Fleet managers counter by negotiating bulk contracts and demanding predictive-maintenance dashboards that minimize unplanned downtime. Suppliers respond with high-capacity cartridges and telematics-ready sensor packs, reinforcing ecosystem lock-in.

By Distribution Channel – OEM Leadership Meets Rising Aftermarket

OEM installations represented a 63.72% share of the engine air filter market in 2024 because every new vehicle ships with a filter. However, driven by an aging global parc, the aftermarket is set to register a CAGR of 2.96% through 2030. DIY culture, especially in North America, accelerates that shift as owners install filters during driveway service sessions. In developing markets, informal workshops steer customer choices toward economy brands, but major awareness campaigns are nudging adoption of certified products to counter counterfeit risk.

OEMs defend post-sale share via bundled service packages and extended warranties, including filter changes. Nevertheless, once vehicles exit warranty, price sensitivity drives channel migration. Suppliers thus hedge by maintaining dual portfolios: OE-spec lines for dealerships and value ranges for independent outlets. Digital fitment guides and quick-ship models improve end-customer experience, helping the aftermarket close perceived quality gaps inside the engine air filter market.

Geography Analysis

Asia-Pacific is the most extensive production base and the fastest-growing consumption arena for the engine air filter market, capturing 45.43% share of the engine air filter market in 2024 and advancing at a 3.86% CAGR through 2030. Growth drivers include robust light-vehicle output, expanding aftermarket networks, and increasingly stringent local emission regulations. China’s sizable vehicle parc aging beyond warranty amplifies replacement demand, while India’s forthcoming BS-VII norms redefine media requirements.

North America shows slow but steady unit growth supported by an entrenched maintenance culture. The region benefits from Tier 3 regulatory consistency and heightened consumer awareness of fuel-economy gains linked to clean intake filtration. DIY share gains, captured in Circana’s research, feed online parts channels that feature aggressive same-day delivery promises. Near-shoring in Mexico and the U.S. South reduces lead times for OE programs, encouraging filtration suppliers to co-locate media and assembly operations.

Europe faces mixed signals. Euro 7 rules elevate filtration specifications, yet rapid BEV uptake removes future unit volumes. Regional suppliers promote washable and recyclable media to align with the circular-economy ethos championed by regulators. Meanwhile, Eastern European factories provide cost-competitive export bases to support global customer programs, partially offsetting volume declines in Western markets.

Competitive Landscape

The engine air filter market is characterized by moderate concentration. A handful of leading suppliers hold significant global revenue, leveraging proprietary media technology, diversified geographic capacity, and deep ties with global OEMs. Vertical integration remains preferred as companies secure raw fiber supply, develop in-house media, and operate downstream assembly lines to safeguard margins. Recent moves such as Sogefi’s business sale to Pacific Avenue Capital Partners underscore private-equity interest in the filtration value chain.

Technology differentiation pivots on three pillars: higher capture efficiency at lower pressure drop, longer service intervals, and smart-sensor integration that supports predictive maintenance. UFI Filters is extending its filtration expertise into hydrogen fuel-cell stacks, illustrating that adjacency plays a role beyond combustion engines. Hengst, Bosch, and MANN+HUMMEL invest in end-of-life recyclability, offering filter elements with reduced CO₂ footprints to meet OEM sustainability scorecards. Counterfeit mitigation has become a competitive battleground, with QR-code product authentication and blockchain pilot programs aiming to protect brand equity in digital marketplaces.

Regional capacity expansion reduces logistics risk and supports JIT supply. Bosch’s semiconductor and component investments in the United States align with broader localization. Meanwhile, Asian firms scale aggressively within ASEAN to capture late-cycle ICE volume that global brands may vacate. Suppliers also court fleets directly with subscription models that bundle filters, telematics, and analytics in flat-fee contracts, blurring the traditional boundaries between OE and aftermarket channels across the engine air filter market.

Engine Air Filter Industry Leaders

MANN+HUMMEL

Donaldson Company, Inc.

MAHLE GmbH

DENSO Corporation

Sogefi SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Doowon Refrigeration, a global leader in automotive cooling systems, inaugurated its first plant in Apodaca, Nuevo León, Mexico, with an initial investment of USD 18 million. The new facility manufactures advanced automotive components, including air intake systems, engine air filters, and air conditioning hoses and tubes.

- May 2024: UFI Filters Group inaugurated UFI GREEN, a USD 45 million facility in Jiaxing, China, adding 42,000 square meters of capacity aimed at 9.4 million units per year.

Global Engine Air Filter Market Report Scope

| Gauze Filter |

| Paper/Cellulose Filter |

| Synthetic Oil Filter |

| Stainless-Steel Mesh Filter |

| Foam Filter |

| Paper |

| Foam |

| Cotton |

| Synthetic |

| Metal |

| Passenger Car |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Filter Type | Gauze Filter | |

| Paper/Cellulose Filter | ||

| Synthetic Oil Filter | ||

| Stainless-Steel Mesh Filter | ||

| Foam Filter | ||

| By Material Type | Paper | |

| Foam | ||

| Cotton | ||

| Synthetic | ||

| Metal | ||

| By Vehicle Type | Passenger Car | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the engine air filter market in 2025?

The engine air filter market size is USD 3.8 billion in 2025 with a 1.26% CAGR projected through 2030.

Which filter type is growing the fastest?

Synthetic oil filters record the highest growth, advancing at a 3.26% CAGR on superior efficiency and extended service intervals.

Why does Asia-Pacific lead global demand?

Asia-Pacific combines massive vehicle production with aging fleets and tightening emission norms, capturing 45.43% share in 2024 and growing at 3.86% CAGR.

How is electrification affecting demand?

Rapid BEV penetration eliminates intake filter needs, but hybrids and ICE dominance in developing regions moderate the impact.

What technologies will shape future product design?

Synthetic and nanofiber media, IoT-enabled sensor modules, and recyclable material architectures are expected to define next-generation intake filters.

Page last updated on: