Automatic Identification System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

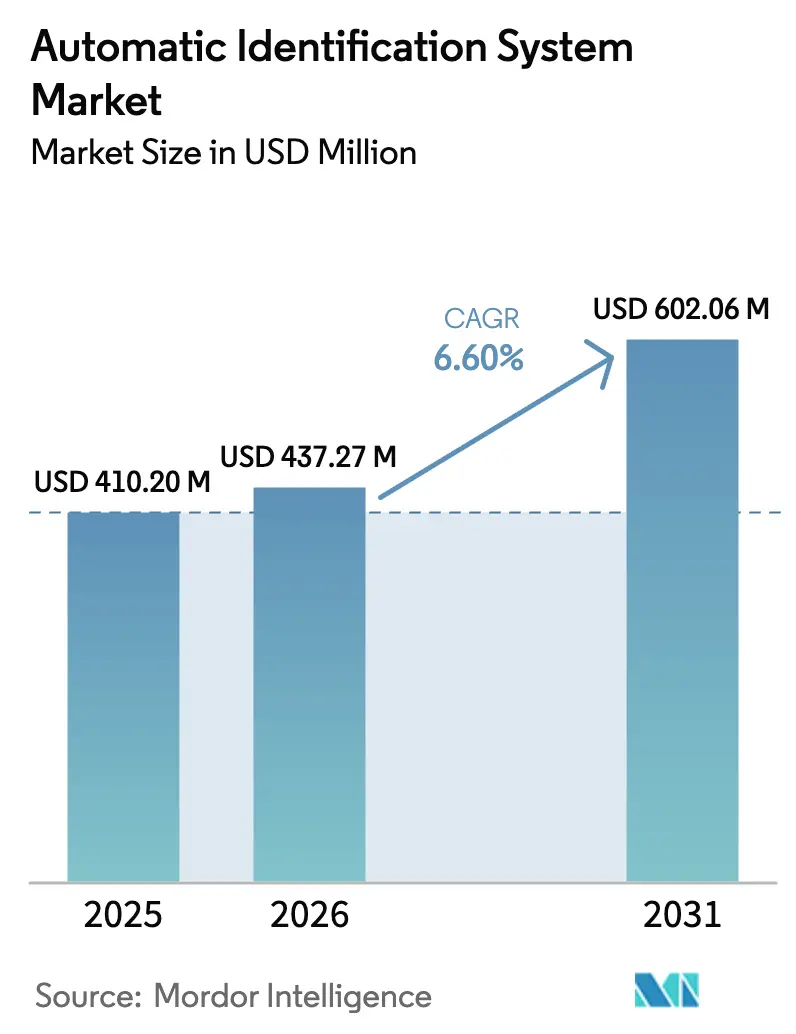

| Market Size (2026) | USD 437.27 Million |

| Market Size (2031) | USD 602.06 Million |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automatic Identification System Market Analysis by Mordor Intelligence

The Automatic Identification System market size is expected to grow from USD 410.2 million in 2025 to USD 437.27 million in 2026 and is forecast to reach USD 602.06 million by 2031 at 6.6% CAGR over 2026-2031. The Automatic Identification System market is expanding because regulators now require wider carriage of AIS equipment, satellite operators are closing historical coverage gaps, and vessel owners demand richer analytics to navigate volatile trade routes. Asia-Pacific ports are automating faster than ever, environmental reporting now relies on AIS-driven data sets, and insurers are embedding AIS feeds into dynamic-premium models. Competitive intensity is sharpening as equipment makers, satellite constellations, and software vendors converge on integrated offerings that bundle hardware, connectivity, and analytics. Spectrum policy uncertainty and spoofing incidents temper the growth outlook, yet the Automatic Identification System market remains on a firm upward trajectory, propelled by digitalization budgets and climate-compliance mandates.

Key Report Takeaways

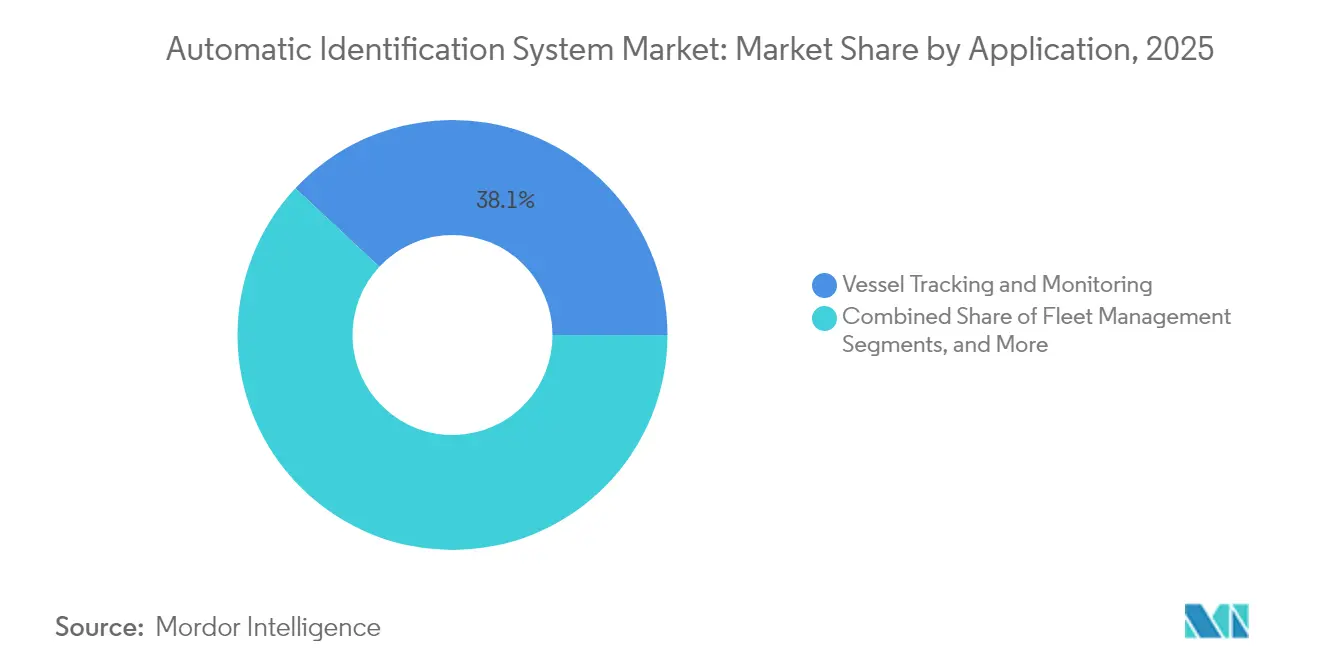

- By application, Vessel Tracking and Monitoring led with 38.05% revenue share in 2025, while Maritime Security and SAR is projected to post the fastest 7.55% CAGR to 2031.

- By platform, vessel-based transponders held 71.95% of the Automatic Identification System market share in 2025; On-Shore-Based Stations are expanding at a 7.42% CAGR through 2031.

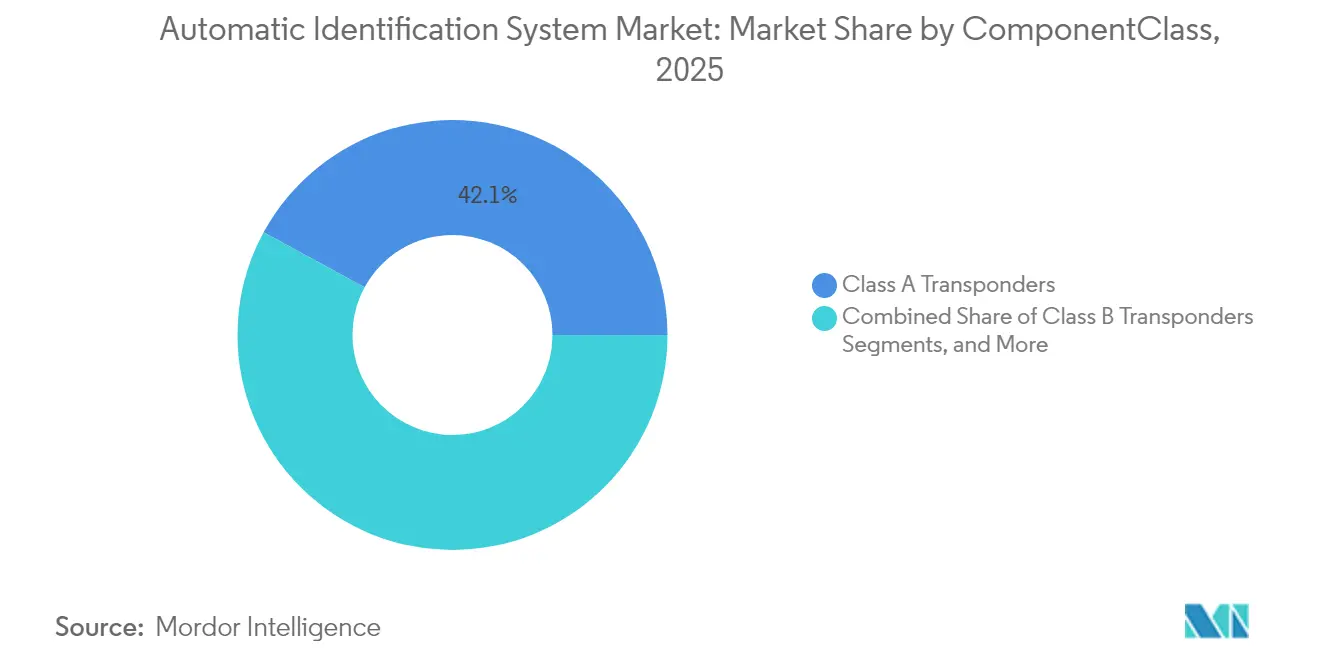

- By component/class, Class A Transponders held 42.08% of the Automatic Identification System market share in 2025; Class B Transponders are expanding at a 7.47% CAGR through 2031.

- By solutions, Terrestrial AIS held 58.05% of the Automatic Identification System market share in 2025; Satellite AIS (Sat-AIS) is expanding at an 7.86% CAGR through 2031.

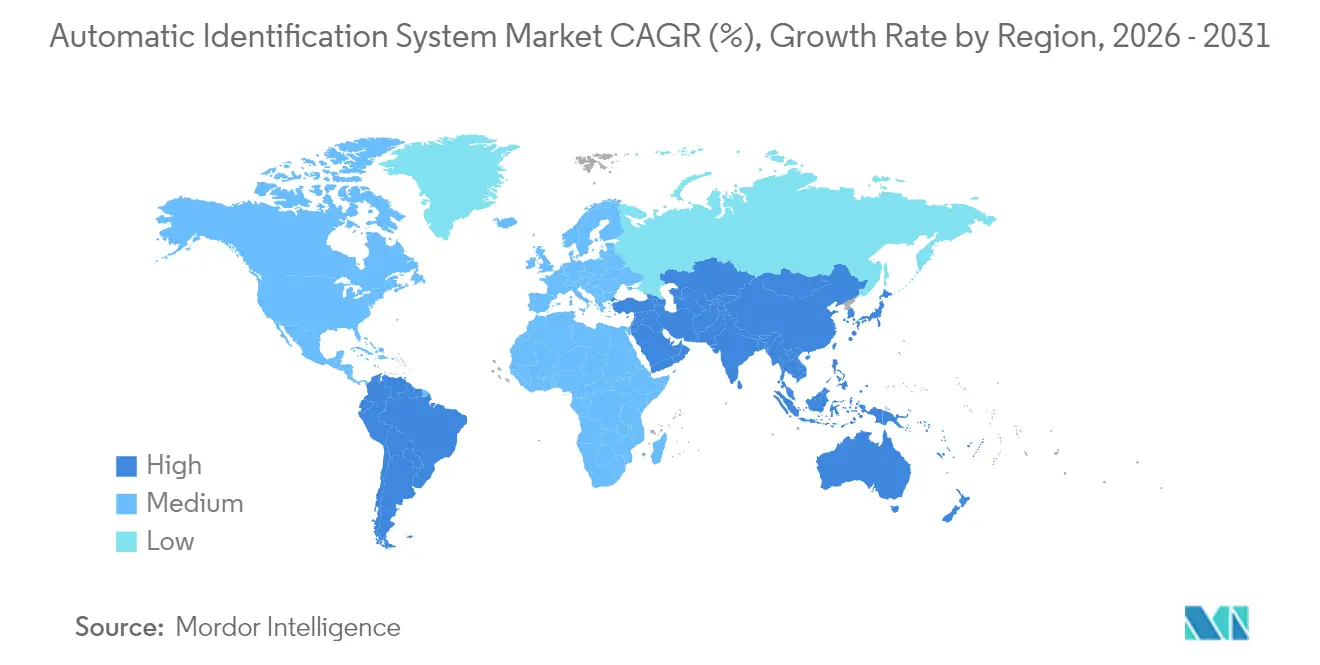

- By geography, Asia-Pacific commanded a 41.78% share in 2025, whereas South America is on track for a 7.47% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automatic Identification System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IMO 2024 mandate for 24 m fishing vessels | +1.2% | Global, concentrated in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Rising maritime trade and traffic volumes | +1.8% | Global, strongest in Asia-Pacific trade corridors | Medium term (2-4 years) |

| Port-call optimization via AIS analytics | +0.9% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Arctic shipping lanes demand long-range AIS | +0.7% | Arctic regions along the Northern Sea Route | Long term (≥ 4 years) |

| AIS-driven dynamic insurance premiums | +0.5% | Europe and North America, spreading globally | Medium term (2-4 years) |

| CII/GHG reporting needs AIS-based data | +1.1% | IMO member states worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

IMO 2024 Mandate Expands Fishing Vessel Coverage

The International Maritime Organization now compels fishing vessels longer than 24 m to carry AIS, capturing a fleet previously outside the original SOLAS rules.[1]International Maritime Organization, “AIS Transponders,” IMO Safety Division, imo.org Compliance activity is most intense in Europe, where 85% of eligible boats already carry Class B transponders, and in Asia-Pacific yards that are working through retrofit backlogs. The regulation is framed as an enforcement weapon against illegal, unreported, and unregulated fishing that drains USD 20 billion annually. Satellite operators benefit because remote-water fishing fleets seldom sail within range of terrestrial towers. Demand will remain elevated into 2025, given the phased roll-out and the large installed base of older vessels needing cost-sensitive equipment. Growth also ripples into analytics subscriptions because fisheries agencies want real-time maps and alerting dashboards rather than raw positions.

Rising Maritime Trade Volumes Drive Infrastructure Digitalization

Maritime cargo returned to pre-pandemic velocity, and port calls for container ships in Africa and tanker calls worldwide rose 20% and 38%, respectively, between 2018 and 2023.[2]United Nations Conference on Trade and Development, “Africa: Stronger Maritime Industry Drives Resilient Trade,” unctad.org The rebound exposed operational blind spots: drought-fueled congestion at the Panama Canal and armed drone threats in the Red Sea both pushed operators toward AIS-enabled situational awareness. Authorities from Abu Dhabi to Lagos are installing vessel-traffic-management suites that ingest high-density AIS feeds and publish arrival predictions to trucking portals. For suppliers, every new tower and analytics license renews the Automatic Identification System market opportunity at a higher value per endpoint. Equipment refresh cycles accelerate because ports cannot optimize berth allocation without centimeter-accurate, low-latency tracking.

Port Optimization Analytics: Transform Operational Efficiency

Advanced machine-learning models now hit 99% accuracy in predicting vessel arrival times, shrinking berth idle time that costs USD 2-4 billion globally after singular disruptions such as the MV Dali bridge collision. The shift from raw positions to predictive analytics means value migrates to software subscriptions; port authorities in Singapore and Rotterdam award multi-year analytics contracts bundled with cloud hosting. Classification societies like Bureau Veritas are embedding predictive AIS data into surveyor scheduling algorithms, compressing inspection lead-times and lowering fuel burn during waiting periods. The Automatic Identification System market gains incremental revenue from these analytics tiers, commanding per-vessel ARPU that is 3-4 times higher than basic transponder data plans.

Arctic Shipping Routes Demand Extended AIS Coverage

The volume of trans-Arctic voyages has climbed 25% since 2013 as melting sea ice shortens Asia-to-Europe passages. Terrestrial towers cannot operate consistently at 70° N, so operators rely on store-and-forward satellite AIS complemented by new polar-orbit microsats. Norway’s Ice Service fuses AIS with synthetic aperture radar to warn crews about shifting floes, underscoring why satellites dominate the Automatic Identification System market above the Arctic Circle.[3]Frontiers in Marine Science, “The MET Norway Ice Service,” frontiersin.org Equipment vendors are hardening receivers to withstand −40 °C and intermittent power, a niche that allows premium gross margins. Autonomous vessel trials in polar waters further stretch satellite bandwidth because self-navigating craft must stream telemetry every few seconds for shore-based command centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data congestion and spoofing incidents | -1.3% | Global, concentrated in high-traffic lanes | Short term (≤ 2 years) |

| Range/coverage gaps in dense and remote seas | -0.8% | Remote oceans and developing coastlines | Medium term (2-4 years) |

| Coastal 5G VHF spectrum re-allocation risk | -0.6% | Advanced 5G markets in Europe, North America, East Asia | Long term (≥ 4 years) |

| Sat-AIS latency for autonomous navigation | -0.4% | Worldwide; acute in autonomous-shipping corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Integrity Challenges Undermine System Reliability

Spoofing frequency escalated as bad actors camouflaged sanction-evading tankers and illegal fishing fleets; AIS lacks native encryption, making it vulnerable to identity swaps and phantom ship insertions. Detection is difficult amid spectrum crowding in the Singapore Strait and Strait of Hormuz. Insurers worry about liability when collision investigations reveal falsified tracks. Satellite imagery fusion tools like Mitsubishi Heavy Industries’ AIRIS flag discrepancies between AIS position and hull silhouette, but adoption costs remain high. Unless the VDES upgrade rolls out quickly, lingering trust deficits could restrain the Automatic Identification System market, especially for safety-critical autonomous navigation.

VHF Spectrum Reallocation Threatens Traditional AIS Operations

Telecom regulators carving spectrum for coastal 5G fixed-wireless services threaten the VHF slots on which AIS relies. Europe’s forthcoming Class M beacon rule forces leisure-craft operators to upgrade by January 2025, exposing the Automatic Identification System market to compliance friction.[4]Marine Rescue Technologies, “What Is Class-M?” smrtsos.com VDES promises 32 times the throughput of legacy AIS, but requires fleet-wide hardware refresh and multinational spectrum coordination. Ports weighing whether to invest in new shore stations confront regulatory ambiguity: will 5G win further VHF concessions in the next auction cycle? This uncertainty may defer capital spending, especially in OECD coastal economies where spectrum is prized.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Vessel Tracking and Monitoring Leads While Environmental Monitoring Accelerates

Vessel Tracking and Monitoring accounted for USD 156.05 million, translating into 38.05% of the Automatic Identification System market in 2025. Operators integrate AIS feeds with engine-room telemetry to benchmark carbon intensity and reroute vessels away from congestion, cutting bunker bills and emissions simultaneously. The segment will keep its numerical lead because liner shipping alliances roll out end-to-end control towers that require real-time position data for thousands of boxes. The Automatic Identification System market benefits as liners move from annual license purchases to multi-year software-as-a-service contracts that bundle AIS with predictive scheduling and decarbonization dashboards.

Maritime Security and SAR is the breakout opportunity, projected to expand at a 7.55% CAGR on the back of IMO’s greenhouse-gas strategy, which mandates Carbon Intensity Indicator reporting beginning in 2026. Regulators and charterers now demand voyage-granular CO₂ baselines; AIS offers the time-stamped speed and distance inputs that populate these formulas. The Automatic Identification System market size attributable to emissions compliance tools could triple as more flag states adopt market-based measures like the European Union’s emissions trading scheme. Vendors selling overlay APIs that calculate well-to-wake CO₂e per voyage extract high recurring revenue, distancing themselves from pure hardware competitors.

By Platform: Vessel-Based AIS Transponders Dominance Continues Amid Satellite Acceleration

Vessel-based transponders represented 71.95% of the Automatic Identification System market revenue because SOLAS regulations obligate every cargo ship above 300 GT to broadcast identity and position at least every 6 seconds. The mandatory nature of carriage locks in a replacement cycle of roughly five years for Class A units. Manufacturers are shipping VDES-ready models with embedded encryption chips, commanding 15-20% price premiums.

On-Shore-Based Stations, though still less than one-third the size, is charting a robust 7.42% CAGR, propelled by expanding polar trade, offshore wind construction, and defense surveillance contracts. Each new microsatellite adds revisit frequency, lowering latency toward near-real-time service levels essential for autonomous-vessel corridors. For hybrid operators, satellite fills the black holes where coastal towers cannot hear. This hybridization cements the Automatic Identification System market as both a hardware and connectivity play, insulating suppliers from commoditization.

By Component/Class: Class A Transponders Anchor Commercial Fleet Adoption

Class A Transponders represented 42.08% of the Automatic Identification System. Class A units dominate because international voyages require higher power, frequent messaging, and navigational sensor integration specified by IMO performance standards. Vendors differentiate by adding dual GNSS receivers and tamper-detection firmware that logs attempts to disable transmitters. The Automatic Identification System market size for Class A transponders will hold steady as newbuilding deliveries backfill fleet losses and retrofits address cybersecurity requirements.

Class B equipment, priced 60% lower, attracts fishing vessels and workboats newly swept into the regulatory net. Demand spikes coincide with the 2024 fishing-fleet mandate, driving volume but compressing margins. Coast stations and AIS gateways serve as the land-based backbone feeding traffic-management centers; they earn revenue through maintenance contracts and software upgrades rather than initial hardware sales. Overall, component diversity shields the Automatic Identification System market from single-segment shocks.

By Solution: Terrestrial Networks Persist with Rapid Satellite Integration

Terrestrial AIS networks capture most revenues because their low-latency 162 MHz channels underpin collision-avoidance mandates. They represented 58.05% of the Automatic Identification System. Port authorities upgrade towers with phased-array antennas and edge compute nodes that filter congestion and push curated tracks to harbor pilots. This keeps terrestrial outlays buoyant even as satellite share rises.

Satellite AIS solutions gathered momentum when Spire Global scored a USD 10 million investment from Signal Ocean to co-develop maritime-intelligence dashboards. Deep-sea mining consortia and offshore energy majors buy satellite coverage bundles to police exclusion zones thousands of nautical miles from shore. Hybrid services that auto-switch between VHF and satellite eliminate blind spots and enable machine-learning models to operate continuously, reinforcing the Automatic Identification System market’s role as foundational digital infrastructure.

Geography Analysis

Asia-Pacific generates the largest slice of revenue, 41.78% in 2025, because it hosts nine of the world’s ten busiest container ports and channels vast Belt and Road investments into digital-port upgrades. China deploys shore-based towers along Silk Road maritime nodes, while Japan funds AI-steered ferry pilots that ingest AIS feeds for collision-avoidance algorithms. India’s Navy is wiring USD 125 million worth of coastal surveillance towers to U.S.-donated data-fusion centers, amplifying defense demand for AIS intelligence. Singapore, ranked top on the UN port-performance index, licenses value-added AIS analytics to terminal operators who target berth-turnaround times below 15 hours. This confluence of commercial freight, naval security, and government-mandated emissions tracking ensures Asia-Pacific remains the anchor of the Automatic Identification System market.

Europe holds a 27.12% share, driven by stringent safety codes and decarbonization policy. The forthcoming Class M beacon rule pushes pleasure-craft owners into the Automatic Identification System market, expanding the addressable base beyond commercial shipping. Norway’s Ice Service showcases Europe’s specialized Arctic competence, blending AIS with radar and optical satellites to safeguard polar voyages. EU green-deal funding channels grants to start-ups like Windward that analyze AIS behavioral patterns to flag sanctions-evading “shadow fleets,” turning compliance pain points into software-subscription revenue.

North America maintains a 23.96% share on the back of the U.S. Coast Guard’s strict AIS carriage rules and substantial defense procurement for maritime domain awareness. Tech partnerships, such as Saildrone with Palantir, feed classified data lakes that rely on AIS fingerprints. Canada’s CII reporting guidance aligns with IMO methodology and triggers procurement of rule-ready data platforms.

South America, while smaller, is the Automatic Identification System market’s fastest-growing geography at 7.47% CAGR, thanks to Brazilian offshore rigs and Argentine grain terminals that digitize export corridors. Middle East and African initiatives, including AD Ports’ next-gen VTMIS, add incremental tower installations and analytics licenses.

Competitive Landscape

The Automatic Identification System market is moderately fragmented. Legacy marine-electronics giants such as Saab, Furuno, and Kongsberg ship SOLAS-certified transponders through entrenched distributor networks. Satellite-first specialists, Spire Global, exactEarth (now part of Spire), and ORBCOMM, compete on revisit rate and latency. Analytics-native challengers like Windward and NukkAI monetize predictive insights layered over raw AIS feeds. Market boundaries blur as hardware vendors bundle data plans and software firms white-label OEM radios.

M&A momentum shows in Kpler’s late-2024 bid for Spire’s ship-tracking unit, which drew antitrust scrutiny because it would combine commodity tracking with price-forecast analytics. Strategic partnerships proliferate: Saildrone ties autonomous surface vehicles to Palantir’s AI cloud, while Bureau Veritas embeds NukkAI’s algorithmic schedulers into classification workflows. Equipment suppliers hedge against commoditization by shipping VDES-ready radios with over-the-air firmware upgrade paths.

Differentiation pivots toward cyber-secure architecture, machine-learned anomaly detection, and seamless satellite handoff. The Automatic Identification System market thus rewards players who command both hardware intellectual property and scalable cloud analytics. As port authorities and defense agencies bundle procurement, mid-tier vendors face consolidation pressure or risk relegation to niche aftermarket segments.

Automatic Identification System Industry Leaders

Saab AB

Furuno Electric Co. Ltd

Spire Global, Inc.

ORBCOMM Inc.

Kongsberg Gruppen ASA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Saildrone and Palantir formed a strategic alliance to fuse autonomous-vehicle data with AI cloud analytics for maritime security.

- January 2025: The U.K. deployed Nordic Warden, an AIS-driven AI tool that tracks shadow fleets in 22 Northern European zones.

- January 2025: Bureau Veritas partnered with NukkAI to optimize surveyor scheduling using AIS-derived arrival forecasts.

- December 2024: KVH unveiled TracNet Coastal terminals with embedded eSIM, offering 300 Mbps coastal connectivity in 135 countries.

Global Automatic Identification System Market Report Scope

The Automatic Identification System (AIS) is a short-range coastal tracking system currently used on ships. It was developed to provide identification and positioning information to both vessels and shore stations. The market is defined by the revenue generated from the Automatic Identification System offered by different market players worldwide.

The Automatic Identification System Report is Segmented by Application (Fleet Management, Vessel Tracking and Monitoring, Maritime Security and SAR, Other Applications), Platform (Vessel-based AIS Transponders, On-Shore-based Stations), Component/Class (Class A Transponders, Class B Transponders, AIS Base Stations, AIS Receivers/Gateways), Solution (Terrestrial AIS, Satellite AIS, Hybrid AIS Services), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Fleet Management |

| Vessel Tracking and Monitoring |

| Maritime Security and SAR |

| Other Applications |

| Vessel-based AIS Transponders |

| On-Shore-based Stations |

| Class A Transponders |

| Class B Transponders |

| AIS Base Stations |

| AIS Receivers / Gateways |

| Terrestrial AIS |

| Satellite AIS (Sat-AIS) |

| Hybrid AIS Services |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Application | Fleet Management | ||

| Vessel Tracking and Monitoring | |||

| Maritime Security and SAR | |||

| Other Applications | |||

| By Platform | Vessel-based AIS Transponders | ||

| On-Shore-based Stations | |||

| By Component / Class | Class A Transponders | ||

| Class B Transponders | |||

| AIS Base Stations | |||

| AIS Receivers / Gateways | |||

| By Solution | Terrestrial AIS | ||

| Satellite AIS (Sat-AIS) | |||

| Hybrid AIS Services | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Malaysia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Automatic Identification System market in 2026?

The Automatic Identification System market size is USD 437.27 million in 2026 and is forecast to reach USD 602.06 million by 2031.

Which application contributes the most revenue?

Vessel Tracking & Monitoring leads, accounting for 38.05% of 2025 revenue, thanks to liners integrating AIS into real-time operational control towers.

Which segment is growing the fastest?

Satellite AIS (Sat-AIS) is projected to expand at an 7.86% CAGR through 2031,

Why is satellite AIS adoption accelerating?

Satellite AIS usage is rising at a 7.86% CAGR because it fills coverage gaps in polar and remote oceans where terrestrial towers cannot reach.

Page last updated on: