Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

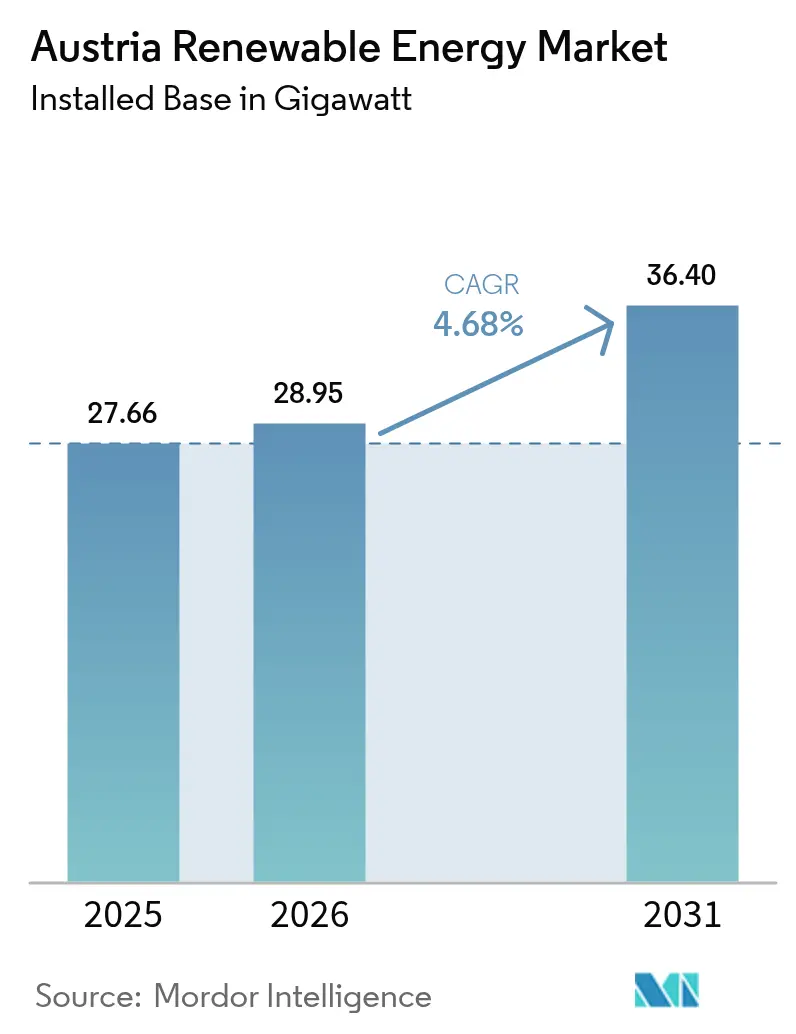

| Base Year Market Size (2025) | 27.66 gigawatt |

| Market Volume (2026) | 28.95 gigawatt |

| Market Volume (2031) | 36.4 gigawatt |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Renewable Energy Market Analysis by Mordor Intelligence

The Austria Renewable Energy Market size is expected to grow from 27.66 gigawatt in 2025 to 28.95 gigawatt in 2026 and is forecast to reach 36.4 gigawatt by 2031 at 4.68% CAGR over 2026-2031.

Faster capacity additions are driven by the Renewable Energy Expansion Act, Austria’s 100% renewable electricity target for 2030, and the broader ambition of achieving climate neutrality by 2040. Hydropower remains the backbone of electricity supply and grid stability, while solar photovoltaics and onshore wind register the steepest cost declines. National carbon pricing makes fossil fuels less competitive, public-sector financing cuts financing costs, and community-owned projects deepen citizen participation. Together, these forces keep the Austria renewable energy market on a high-growth trajectory despite grid congestion, land constraints, and labour shortages.

Key Report Takeaways

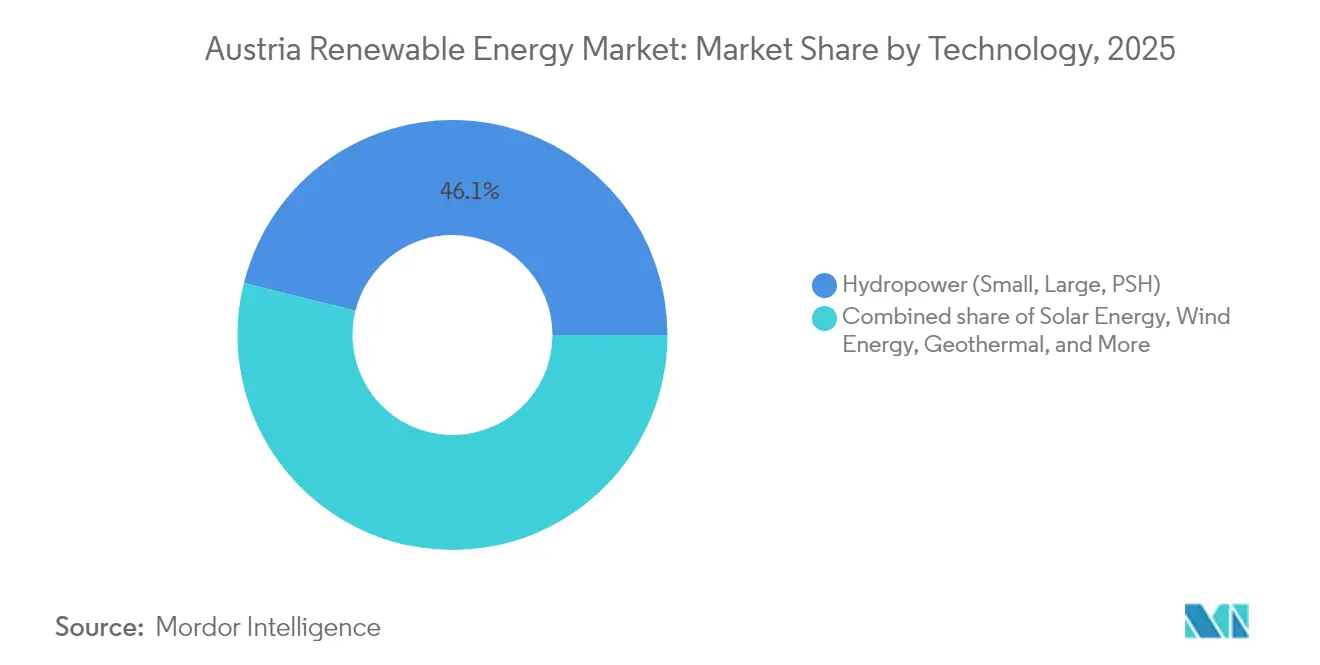

- By technology, hydropower led the Austrian renewable energy market with 46.12% of the market share in 2025, while geothermal is forecast to expand at a 36.2% CAGR through 2031.

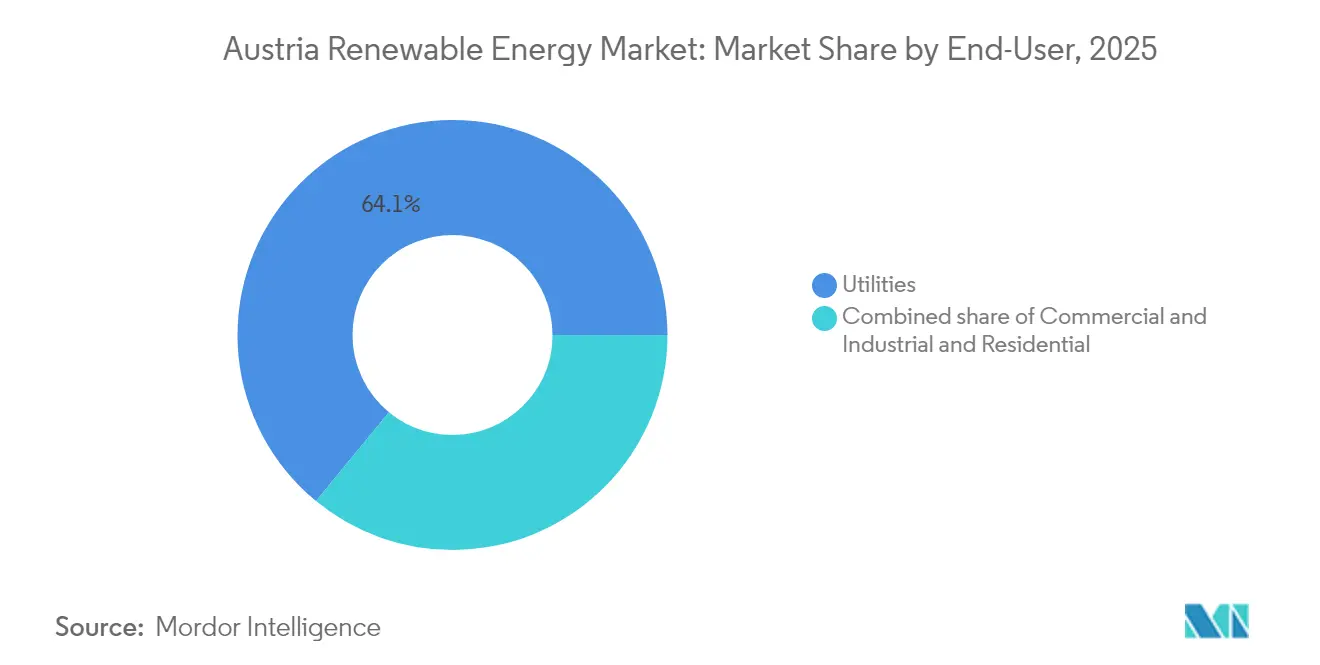

- By end-user, utilities held 64.05% of the Austria renewable energy market share in 2025, whereas the residential segment is advancing at a 10.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Austria Renewable Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed target of 100% renewable electricity by 2030 | +1.8% | National, accelerated deployment in Vienna, Lower Austria, Burgenland | Medium term (2-4 years) |

| Hydropower-anchored grid flexibility enabling VRE integration | +0.9% | Alpine regions (Tyrol, Salzburg, Carinthia) | Long term (≥4 years) |

| Rapid LCOE decline of solar-PV and onshore wind | +1.2% | Lower Austria, Burgenland, Styria | Short term (≤2 years) |

| EU ETS and national CO₂ pricing raising fossil-fuel costs | +0.7% | Cross-border markets with Germany, Italy, Czech Republic | Medium term (2-4 years) |

| VAT-free small-scale PV systems accelerating rooftop uptake | +0.6% | National, with higher penetration in urban centers (Vienna, Graz, Linz) | Short term (≤ 2 years) |

| Rise of "energy communities" & peer-to-peer trading platforms | +0.5% | National, with pilot implementations in rural communities across all states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-backed 100% Renewable-Electricity Target by 2030

Austria’s Renewable Energy Expansion Act mandates an extra 27 TWh, allocating 11 TWh to photovoltaics, 10 TWh to wind, 5 TWh to hydropower, and 1 TWh to biomass. Policy certainty unlocked a EUR 1.3 billion financing package for Burgenland Energie Group, illustrating how clear targets draw capital. ÖNIP allocates EUR 9 billion to transmission upgrades through 2034, easing bottlenecks.[1]Climate Ministry, “ÖNIP Netzinfrastrukturplan,” klimaschutzministerium.at Timelines are tight; Austria became a net electricity importer in August 2024, underscoring the urgency of the situation.

Hydropower-anchored Grid Flexibility Enabling VRE Integration

More than 3,000 hydropower plants, totaling 14.1 GW, equip Austria with unmatched flexibility. Facilities such as the 430 MW Reisseck II pumped-storage plant help balance wind and solar variability, while the Kronstorf substation upgrade is expected to introduce a 220-kV loop by 2030. This agility enabled renewables to supply 87% of the electricity in 2023, far exceeding the EU average.

Rapid LCOE Decline of Solar PV and Onshore Wind

Solar installations reached 2.22 GW in 2024, supported by falling equipment costs and new agrivoltaic models, which were financed by a EUR 80 million European Investment Bank loan to PÜSPÖK Group. Wind economics also improved, as evidenced by the 62 MW WEB Windenergie project in Lower Austria, which was backed by EUR 20.1 million in EIB funding. Technology gains, however, are offset by grid-connection fees and permitting delays.

EU ETS and National CO₂ Pricing Raising Fossil-Fuel Costs

Carbon pricing squeezes fossil fuel heating and transportation, accelerating the adoption of renewables. Heat-pump sales rose from 31,184 units in 2021 to 49,192 units in 2022 as carbon levies took hold. OMV invested almost EUR 200 million to co-process 160,000 tonnes of liquid biomass into renewable diesel at its Schwechat refinery, thereby reducing CO₂ emissions by 360,000 tonnes per year.[2]OMV, “Schwechat Biorefinery Fact Sheet,” omv.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion and lengthy permitting procedures | -0.8% | Lower Austria, Burgenland, Styria | Short term (≤2 years) |

| Insufficient storage capacity to absorb VRE peaks | -0.6% | Urban load centers (Vienna, Graz, Linz) | Medium term (2-4 years) |

| Skilled-labour shortages in RES installation & O&M | -0.4% | National, with particular impact in rural areas lacking technical training infrastructure | Short term (≤ 2 years) |

| Insufficient storage capacity to absorb VRE peaks | -0.3% | National, with grid stability challenges concentrated in high VRE penetration areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion and Lengthy Permitting Procedures

Redispatch volumes could sextuple by 2040 without coordination, the European Commission warns.[3]European Commission, “Recommendations on Austria NECP,” ec.europa.euSince 2018, the Germany-Austria congestion management system caps cross-border flows during peak periods. ÖNIP’s EUR 9 billion build-out will help, although completion is expected to stretch to 2034.

Limited Land Availability for Utility-Scale Wind and Solar

Mountainous terrain and dense settlement restrict the availability of greenfield sites. Agrivoltaics offers a workaround, for instance, on PÜSPÖK Group’s six dual-use farms in Burgenland. Regional planning instruments now earmark additional zones for renewables; yet, high-yield locations remain scarce, thereby inflating project costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Geothermal Leads the Next Wave of Additions

Geothermal capacity is projected to grow at a 36.2% CAGR through 2031, the fastest rate of any technology in the Austria renewable energy market, as deep wells in Vienna and Graz move from exploration to construction. Hydropower retained 46.12% of Austria's renewable energy market share in 2025, anchoring frequency stability even as solar and wind energy expand. Pumped-storage additions, such as the 480 MW Limberg III project, demonstrate how legacy hydro assets are being repurposed for long-duration flexibility. Utility-scale solar added 1.5 GW in 2024 and now benefits from levelized costs below EUR 40 per MWh, while onshore wind added 400 MW, with capacity factors above 35% in Burgenland. Bioenergy supplied 1 TWh in 2024 but faces feedstock constraints, limiting further growth.

The Austrian renewable energy market size for geothermal heat alone could surpass 0.54 GWth by 2031 if current drilling schedules hold, providing urban district-heating operators with a baseload alternative to natural gas. Solar rooftops continue to scale under zero-VAT rules, while hybrid solar-plus-storage plants, such as Energie AG's 50 MW site, illustrate the shift toward firm renewable energy sources. Wind repowering is gaining momentum as operators replace older 2 MW turbines with 4-6 MW machines on the same pads, maximizing output from increasingly scarce land. Small hydropower remains capped by environmental rules, although digital turbine retrofits are lifting efficiency at run-of-river plants. Together, the diversified portfolio mitigates weather risk and keeps Austria on track to achieve its 100% renewable electricity target.

By End-User: Residential Prosumers Accelerate Adoption

Utilities held 64.05% of the Austria renewable energy market share in 2025, but their dominance is eroding as households embrace rooftop solar and battery storage. Residential capacity is rising at a 10.1% CAGR thanks to VAT-free panels under 35 kW and grid-fee discounts of up to 57% for local peer-to-peer trades. Hybrid inverters launched by Fronius in 2024 enable prosumers to earn income from frequency regulation, reducing payback periods to under seven years. Commercial and industrial users are also expanding, led by Voestalpine’s 200 MW wind PPA that locks in low-carbon power for steel production.

Although the Austrian renewable energy market, controlled by utilities, is expected to continue growing in absolute terms, its share is anticipated to decline below 60% by 2031 as distributed generation expands. Utilities are responding with hybrid projects that blend solar, wind, and storage to offer firm capacity and ancillary services. Community-energy aggregators now bundle output from multiple rooftops to bid into balancing markets, further shifting revenue away from centralized assets. Industrial rooftops lag because of split-incentive barriers, yet energy-as-a-service contracts are starting to unlock that segment. The emerging mix of centralized hydro and decentralized solar, wind, and storage assets positions Austria for a more resilient, consumer-driven power system.

Geography Analysis

Lower Austria, Burgenland, and Upper Austria combine to form over half of the current renewable energy capacity, shaped by their flat terrain, high solar irradiation, and mature wind resources. Burgenland alone has secured EUR 1.3 billion to fund 700 MW of new solar and wind projects, and plans to double that figure by 2030. Hydropower-rich Alpine regions, such as Tyrol and Carinthia, feed surplus power into eastern load centers, their pumped-storage systems cushioning variability and underpinning regional trade.

Vienna pioneers urban renewables and is building a geothermal plant in Aspern to heat 20,000 households by 2028, removing 54,000 t of CO₂ annually. Energy-community pilots cluster here, coupling rooftop PV, battery storage, and peer-to-peer platforms. Upper Austria’s energy mix features 30% renewables led by biomass, matching its industrial heat demand while progressing on solar and wind targets

Austria’s EUR 9 billion ÖNIP transmission plan upgrades east-west corridors and integrates future hydrogen pipelines, creating a platform for cross-border power flows. The Austrian renewable energy market benefits as congestion eases, though the full benefits materialize post-2030.

Competitive Landscape

State-majority utility VERBUND generated EUR 10.4 billion in revenue in 2023 and owns approximately half of the national hydropower, aiming for climate neutrality by 2040. EVN aims to achieve a 3.8 TWh renewable energy output by 2030, expanding its wind and solar fleets. OMV is pivoting from hydrocarbons to geothermal, hydrogen, and renewable fuels, as demonstrated by the Schwechat biorefinery and its 4 TWh geothermal goal.

ANDRITZ supplies turbines and electromechanical equipment to hydropower plants worldwide, leveraging its Austrian engineering heritage. International actors such as Enphase deploy micro-inverters and batteries to capture the residential PV segment, while community-energy platforms challenge traditional retail models. Abundant EIB lending lowers weighted average capital cost, intensifying project competition. Taken together, the Austria renewable energy market shows moderate concentration and rising technological differentiation.

Austria Renewable Energy Industry Leaders

Verbund AG

Wien Energie GmbH

EVN AG

Energie AG Oberösterreich

Engie SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: OMV commissioned a EUR 200 million co-processing plant at Schwechat refinery, converting 160,000 t of biomass into renewable diesel.

- March 2025: Baker McKenzie advised Burgenland Energie Group on EUR 1.3 billion in renewable financing for 700 MW of wind and PV projects, expandable to 2,000 MW.

- March 2025: The Federal Government announced that the VAT exemption for PV systems will end on 1 April 2025, forecasting an additional EUR 175 million in revenue.

- November 2024: European Investment Bank lent EUR 80 million to PÜSPÖK Group for six agrivoltaic farms in Burgenland.

Austria Renewable Energy Market Report Scope

The scope of the Austrian renewable energy market report includes:

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-User

| Utilities |

| Commercial and Industrial |

| Residential |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-User | Utilities |

| Commercial and Industrial | |

| Residential |

Key Questions Answered in the Report

What is the current size of the Austria renewable energy market?

The Austria renewable energy installed capacity is 28.95 GW in 2026, and is projected to reach 36.4 GW by 2031, reflecting a 4.68% CAGR.

How fast is geothermal capacity expanding in the Austria renewable energy market?

Deep-geothermal projects are projected to grow at a 36.2% CAGR through 2031, the fastest rate among all technologies.

What share do utilities still hold in Austria's clean-power build-out?

Utilities controlled 64.05% of installed renewable capacity in 2025, though their share is expected to decline as residential and C&I segments scale.

Which regions face the worst grid congestion?

Lower Austria and Burgenland endure the most acute transmission bottlenecks, driving redispatch costs close to EUR 200 million annually.

Why are energy communities important in Austria?

More than 1,300 registered communities leverage grid-fee discounts and peer-to-peer trading, accelerating rooftop solar deployment and decentralizing market power.

What storage gap must Austria close by 2031?

The Austrian Energy Agency estimates an additional 3-5 GWh of short-duration and up to 15 GWh of long-duration capacity will be required to integrate rising VRE volumes.

Which hybrid project illustrates the future of firm renewables in Austria?

Energie AG's 50 MW solar farm paired with 10 MWh of batteries, commissioned in 2024, shows how PV plus storage can deliver frequency regulation and peak-shaving services.

Page last updated on: