Australia Crop Protection Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.60 Billion |

| Market Size (2026) | USD 1.68 Billion |

| Market Size (2031) | USD 2.16 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

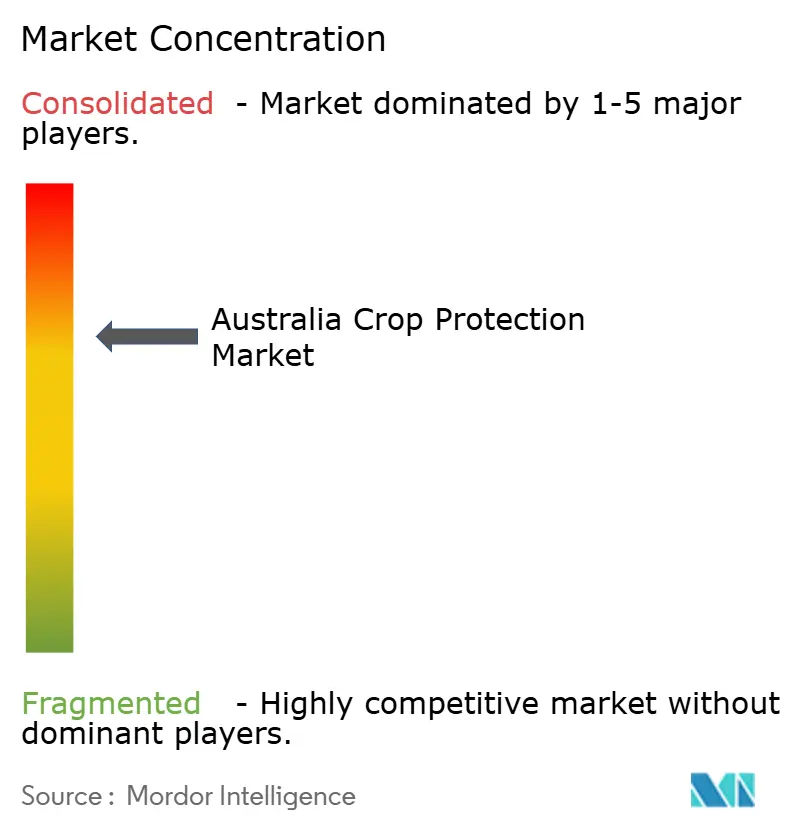

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Crop Protection Market Analysis by Mordor Intelligence

The Australia crop protection market size is expected to grow from USD 1.60 billion in 2025 to USD 1.68 billion in 2026 and is forecast to reach USD 2.16 billion by 2031 at 5.14% CAGR over 2026-2031. This trajectory underscores the market’s ability to withstand regulatory turbulence, climate volatility, and supply-chain disruption while preserving Australia’s role as a major agricultural exporter. Demand strength is anchored in 70% of farm output moving to overseas buyers, creating constant pressure to keep weeds, diseases, and insects in check[1]Source: Australia Trade and Investment Commission, “Australia Agribusiness Overview,” trade.gov. Regulatory reforms now underway at the Australian Pesticides and Veterinary Medicines Authority (APVMA) are projected to raise near-term approval bottlenecks but ultimately deliver greater long-term confidence. Rising drought frequency in southern states and excessive rainfall on the eastern coast are narrowing optimal spray windows, which in turn fuels the adoption of precision application tools and low-volume formulations. Competitive activity is intensifying as multinationals expand portfolios and digital agronomy platforms, with herbicide-resistance, drone-based spraying, and carbon farming incentives shaping product pipelines through 2030.

Key Report Takeaways

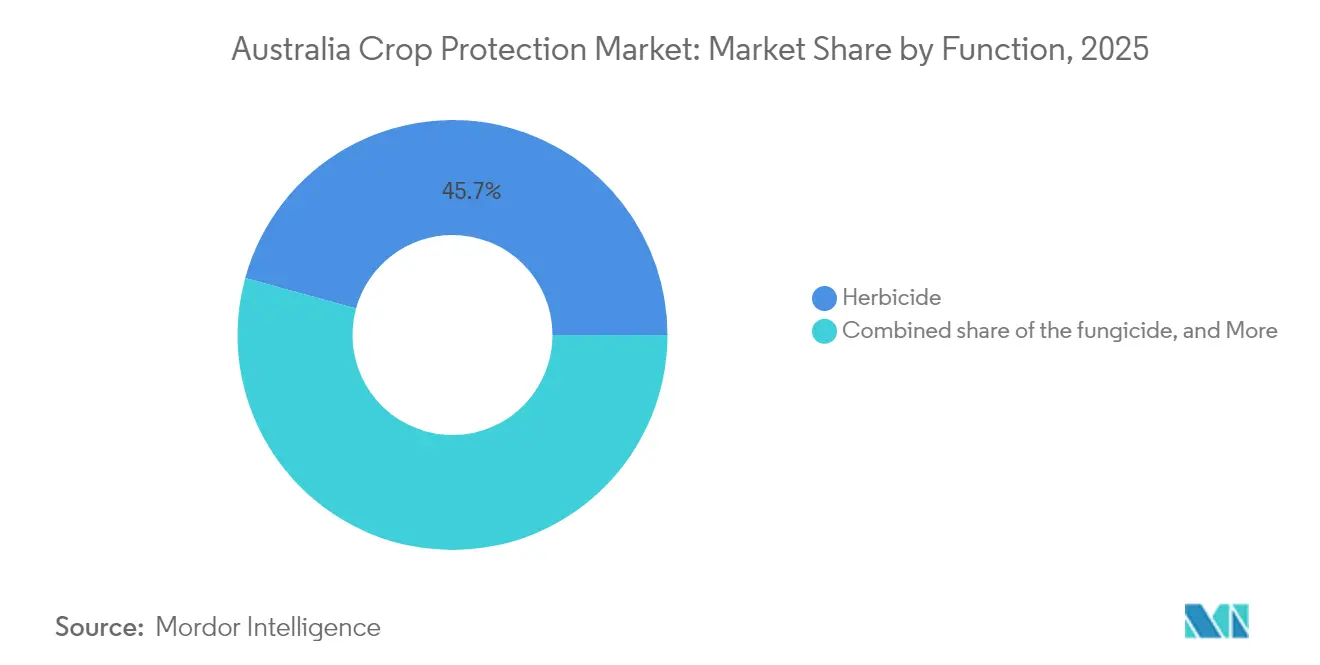

- By function, herbicides led with 45.72% of Australia crop protection market share in 2025, while fungicides are advancing at a 12.32% CAGR through 2031.

- By application mode, foliar spray captured 40.02% revenue in 2025, and seed treatment is projected to expand at a 10.27% CAGR to 2031.

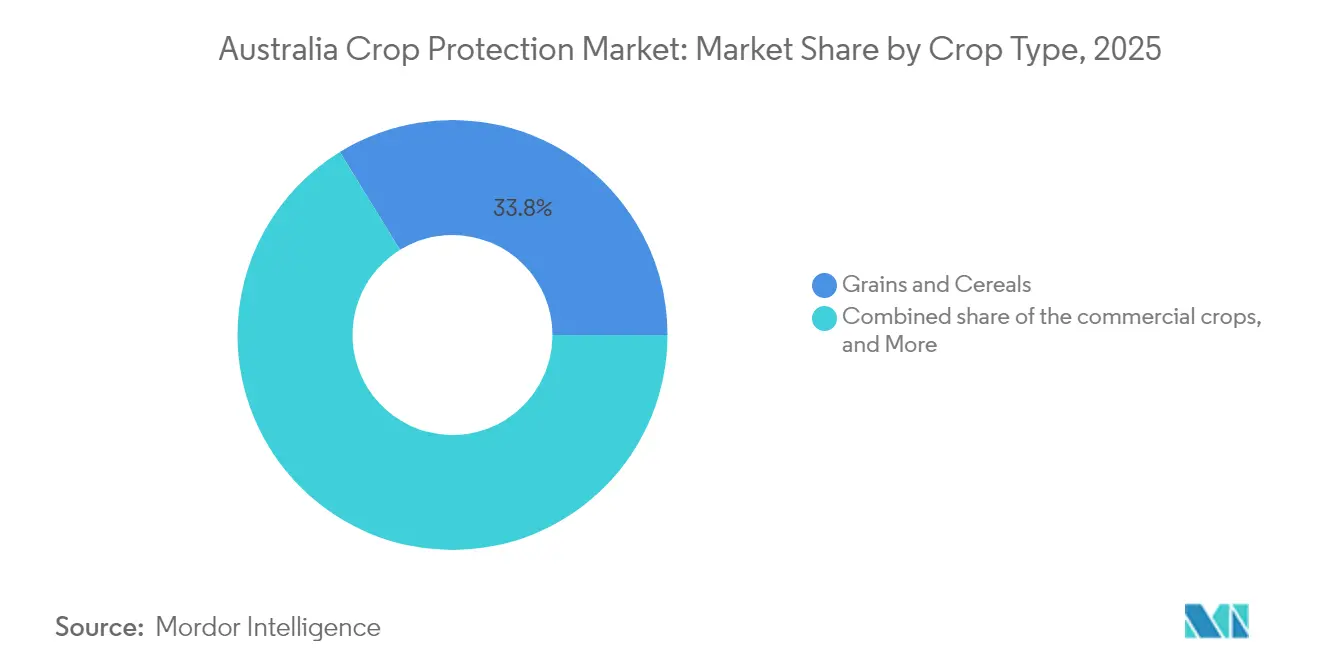

- By crop type, grains and cereals accounted for a 33.78% share of the Australia crop protection market size in 2025, and fruits and vegetables are growing at an 8.44% CAGR of through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Crop Protection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising food-demand pressure on limited arable land | +1.2% | National, concentrated in high-productivity zones | Medium term (2-4 years) |

| Rapid pipeline of herbicide-tolerant crop traits | +0.8% | Grain belt regions, Western Australia, and NSW | Short term (≤ 2 years) |

| Pesticide R&D cost reductions via AI-enabled molecular screening | +0.6% | National, early adoption in Victoria and South Australia | Long term (≥ 4 years) |

| Surge in drone-based ultra-low-volume spraying services | +0.9% | Large-scale operations, Queensland, and Western Australia | Medium term (2-4 years) |

| Government fast-track registrations for "reduced-risk" actives | +0.7% | National, aligned with APVMA priority review pathways | Short term (≤ 2 years) |

| Carbon-credit incentives for regenerative farming inputs | +0.5% | Southern Australia, Murray-Darling Basin | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Food-Demand Pressure on Limited Arable Land

The switch toward higher-value horticulture, evidenced by the 8.5% CAGR in fruits and vegetables, raises tolerance for costly but targeted crop protection programs. Taken together, constrained land supply and strong balance sheets will keep investment in advanced solutions buoyant across the Australia crop protection market. Only 369 million hectares of farmland are available, yet domestic output must continue to rise to meet export contracts and growing Asian demand[2]Source: Australian Bureau of Statistics, “Agricultural Land Use,” abs.gov.au. With land expansion capped, growers prioritize yield-intensification tools that protect each hectare from weed and disease loss. Cash-flow capacity is improving as cropping farm profits are projected to climb to USD 262,000 per operation in 2024-25, enabling purchase of premium herbicide stacks and in-season fungicide passes[3]Source: Department of Agriculture Fisheries and Forestry, “Farm Performance Forecast,” agriculture.gov.au. Precision variable-rate platforms already reduce chemical volume by up to 30% while maintaining output, demonstrating that efficiency, rather than spray volume, drives productivity.

Rapid Pipeline of Herbicide-Tolerant Crop Traits

The commercialization of multi-trait tolerant cotton, canola, and cereal varieties is providing growers with wider spray windows and new mode-of-action combinations. The Commonwealth Scientific and Industrial Research Organisation (CSIRO) Bollgard 3 XtendFlex cotton preview in 2024 exemplifies the trend by stacking tolerance to multiple herbicides, thereby relieving resistance pressure in Australia’s no-till systems [4]Source: CSIRO, “Bollgard 3 XtendFlex Launch,” csiro.au. Growers facing ryegrass and wild oat resistance now gain an extra season of efficacy from existing active ingredients, protecting their return on past chemistry investments. In the 2022-23 season, wheat output reached 41.2 million metric tons, valued at USD 13.5 billion. Therefore, even modest yield gains translate into significant demand for chemistry. Seed companies and basic manufacturers are co-marketing trait-chemistry bundles, strengthening their lock-in with distributors. As more multi-stack varieties pass APVMA review, the Australia crop protection market will lean on trait innovation to delay costly resistance crises.

Pesticide R&D Cost Reductions via AI-Enabled Molecular Screening

Artificial intelligence shortens discovery cycles from years to months, cutting lab and field iterations and boosting pipeline throughput. Machine-learning models now predict bioactive compound success with up to 96% accuracy, enabling small companies to screen thousands of microbes quickly. APVMA preference for reduced-risk registrations dovetails with consumer pressure for residue-free products, making economics and regulation mutually reinforcing. As algorithmic screening gains trust, it will claim a higher share of fungicide and insecticide programs, bolstering revenue diversity within the Australia crop protection industry.

Surge in Drone-Based Ultra-Low-Volume Spraying Services

The drone market is projected to expand globally by 2030, and Australia ranks among the fastest adopters. Units like the DJI Agras T30 can cover 8 hectares per hour, operating when ground rigs cannot enter wet paddocks. State rebate schemes offset capital cost and accelerate adoption across Queensland fruit blocks and Western Australian broadacre grains. Ultra-low-volume techniques slash water haulage, permit night applications, and reduce operator exposure. Integration with AI crop-scouting flights closes the loop from detection to treatment, raising overall system effectiveness and driving incremental sales of drone-formulated crop protection products.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating APVMA registration fees | -0.8% | National, affecting all product categories | Short term (≤ 2 years) |

| Pending paraquat and glyphosate restrictions | -1.1% | National, concentrated impact on broadacre systems | Medium term (2-4 years) |

| Chronic shortage of rural agronomists | -0.6% | Regional areas, remote farming districts | Long term (≥ 4 years) |

| Sea-freight volatility elevating import costs | -0.9% | National, affecting imported active ingredients | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating APVMA Registration Fees

APVMA’s cost-recovery model obliges applicants to fund complex evaluations upfront, which can exceed USD 500,000 for new chemical classes. Smaller innovators struggle to capitalize on programs, delaying or canceling niche products for minor crops. Staff relocation to Armidale cut experienced assessor numbers, elongating timelines and adding resubmission fees that can lift total outlays by another 15%. Faced with uncertain payback, many registrants prioritize large-acreage herbicide labels over specialty fungicides, narrowing grower options. Fee escalation, therefore, stifles portfolio diversity and could erode 0.8% of forecast CAGR for the Australia crop protection market.

Pending Paraquat and Glyphosate Restrictions

In July 2024, the regulator released draft decisions that may curtail paraquat volumes and strengthen glyphosate stewardship, echoing trends in overseas litigation. Broadacre growers depend on these cost-effective actives for conservation tillage. Removal would force shifts to pricier or less efficacious modes of action. Distributors face inventory risk during the transition period, and R&D programs rebalance toward alternative chemistries, which raises costs. Market uncertainty freezes purchasing decisions and suppresses growth until clarity emerges, slicing an estimated 1.1% from potential CAGR across the Australia crop protection market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Herbicide Dominance Faces Fungicide Momentum

Herbicides represented 45.72% of Australia crop protection market share in 2025, fueled by the nation’s 36 million metric tons of wheat program and extensive no-till acreage. This leading position is reinforced by the grower's reliance on chemical weed control as mechanical tillage declines to conserve soil moisture. The arrival of Group 14 pre-emergence options extends control of resistant ryegrass, sustaining herbicide headroom. Fungicides are experiencing rapid growth with a projected CAGR of 12.32% through 2031, driven by increased rainfall in eastern regions and expanded horticultural cultivation. Disease outbreaks in lentils and pulses have increased fungicide usage even in typically arid regions, expanding their application across the Australian crop protection market.

Insecticide demand is stabilizing as IPM tactics take share, though fall armyworm incursions in northern states keep baseline volume intact. Nematicides and molluscicides remain niche but critical for cotton and leafy-green systems battling root-knot and slug outbreaks. Suppliers therefore balance broadacre herbicide investment with high-margin fungicide innovation, ensuring the Australia crop protection industry maintains portfolio resilience.

By Application Mode: Foliar Spray Leads While Seed Treatment Accelerates

Foliar application delivered 40.02% of 2025 revenue, a testament to aerial fleets and self-propelled sprayers blanketing millions of hectares in narrow windows. Its dominance owes much to post-emergence herbicide and curative fungicide programs that require canopy coverage. However, seed treatment logged a 10.27% CAGR outlook as growers adopt multi-mode insecticide and fungicide coatings seeking early-season insurance. This surge redirects some demand away from in-crop sprays but simultaneously drives higher per-hectare spend, expanding the Australia crop protection market.

Chemigation uptake increases in irrigated horticulture, merging water and input delivery to trim labor. Soil fumigation holds steady within the strawberry and tomato sectors, aiming for export-grade residue standards. As drone-ready formulations emerge, low-volume foliar techniques may reclaim momentum, yet seed treatment’s convenience and efficiency ensure its ascent across rotation crops in the Australia crop protection market.

By Crop Type: Grains Anchor Revenue While Horticulture Outpaces

Grains and cereals secured 33.78% of the 2025 value, mirroring the nation’s export-oriented wheat, barley, and canola complex. These broadacre systems rely on cost-effective herbicide regimes and prophylactic fungicides to safeguard commodity margins. Yet, fruits and vegetables are advancing at an 8.44% CAGR to 2031, powered by rising Asian consumer demand for safe, premium produce and domestic health-food trends. High unit revenue per hectare justifies intensive spraying schedules, lifting the contribution to the Australia crop protection market size.

Cotton and sugarcane remain regionally important, with treated cotton sustaining insecticide volume despite bollworm resistance. Pulses and oilseeds diversify rotations, requiring nuanced pest control. Turf and ornamentals, though small, tap into urbanization and sports-field maintenance budgets. Diversification across crop types shields the Australia crop protection market from single-commodity shocks and underpins steady aggregate growth.

Geography Analysis

New South Wales and Victoria jointly accounted for nearly half of the nation's sales in 2025, as mixed-farming enterprises demanded robust herbicide and fungicide programs. Drought stress in inland Victoria has intensified fungicide frequency on moisture-stressed cereals, while the coastal strip copes with disease pressure from prolonged humidity. The presence of mature distribution hubs and research stations further concentrates demand.

Queensland is projected to be the fastest-growing region through 2031, driven by subtropical horticulture and increasing adoption of drone services across sugarcane and cotton valleys. Rice output in the state increased to 618,000 metric tons in 2024, underscoring the uptake of seed treatments and targeted insecticides to combat rice blast. Government grants supporting AgTech accelerate technology transfer, positioning the state as a showcase for precision spraying.

Western Australia contributes a substantial volume of herbicides, given its expansive wheat belt, yet faces logistical hurdles due to port distances and a limited agronomic workforce. Seasonal variability prompts growers to adopt flexible, higher-value mixes, which support gains in fungicide and seed treatment. South Australia and Tasmania round out the market with specialized needs. Wine-grape fungicide programs and brassica insect control sustain steady albeit smaller demand. Together, regional diversity cushions the Australia crop protection market against localized weather shocks, ensuring nationwide resilience.

Regulatory Landscape

Australia regulates crop protection products through the Australian Pesticides and Veterinary Medicines Authority (APVMA) under the National Registration Scheme, principally the Agricultural and Veterinary Chemicals (Administration) Act 1992 and the Agricultural and Veterinary Chemicals Code Act 1994. Registration decisions are anchored to safety, efficacy, and trade considerations. Applicants can use prescribed, listed, and reserved pathways, including routes intended to reduce burden for some minor-use needs.

The system is in an active reform cycle led by the Department of Agriculture, Fisheries and Forestry (DAFF) and the APVMA, following the government detailed response released on 4 November 2024. Governance reforms were implemented from August 2025, with an updated performance framework scheduled for the 2025-26 reporting period. In March 2026, the Agricultural and Veterinary Chemicals (MRL Standard for Residues of Chemical Products) Amendment Instrument (No. 1) 2026 updated maximum residue limits (MRLs) for specific compounds, strengthening residue compliance requirements for domestic supply and export market access. Cost recovery remains a key operational feature of the regime, with APVMA guidance indicating a fixed fee of AUD 116,501 and an 18-month statutory timeframe for a full assessment (Item 1) for a new agricultural product containing a new active constituent.

Competitive Landscape

The market is moderately concentrated. The top four multinationals captured more than half of 2024 sales, while the domestic champion, Nufarm, remains a pivotal challenger. Syngenta Group leverages its CROPWISE digital platform to bundle chemistry with imagery and advisory services, locking in distributor loyalty. Bayer AG continues rolling out Fluroxypyr-based stacks aimed at resistant broadleaf weeds, complementing its industry-leading glyphosate franchise.

BASF SE and Corteva Inc. are investing aggressively in novel modes of action to preempt regulatory threats, with the launches of Cimegra and Isoflex highlighting momentum toward resistance-breaking herbicides. Nufarm’s local formulation plants cut lead times and allow rapid reformulation to suit APVMA label tweaks, sustaining competitive parity on price and service. Partnerships, such as Syngenta Group’s Pesticide alliance with Lavie Bio, underscore a strategic pivot toward lower-toxicity portfolios that align with APVMA fast-track priorities.

Price competition intensifies on generic molecules as Chinese supply returns post-pandemic, yet freight volatility keeps on-the-ground inventory valuable. Companies with strong balance sheets secure buffer stocks, whereas smaller importers risk stockouts. R&D spend averages 7-10% of sales, channelled toward digital agronomy, formulation technology and discovery. Market power will accrue to firms integrating chemistry, data and service, reinforcing current leadership dynamics within the Australia crop protection market.

Australia Crop Protection Industry Leaders

BASF SE

Corteva Inc.

Bayer AG

Nufarm Limited

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory tightening and higher compliance costs are increasing demand for technologies and products that deliver more performance per litre, particularly where legacy herbicides face constraints. APVMA restrictions on paraquat announced in June 2026 (including lower application rates and prohibitions on certain application methods) are pushing growers and service providers toward integrated weed management mixes and precision application tools, which reduce operator exposure and chemical load while maintaining control across broadacre and horticultural systems.

Precision weed control is also emerging as a commercialization path that is supported by grower-led adoption and coordinated industry programs. Green-on-green spot spraying is gaining traction for herbicide and labor savings, while GRDC-backed WeedSAT provides a lower-capex pathway by using satellite imagery with existing boom sprayers and section/nozzle control, broadening access beyond early adopters of optical sprayers. On the regulatory interface, collaboration among Nufarm, the GRDC, and the APVMA on GLP and GAP protocols for green-on-green applications creates space for registrants to extend labels and support claims with fit-for-purpose data packages, particularly in resistance-pressured grains and in higher-value horticulture where residue and stewardship requirements are strict. Separately, APVMA actions in 2026 (including the March 2026 MRL amendment instrument and February 2026 gazettal of new registrations such as Folpan 800 WG and Basta Ultra/Liberty Ultra) indicate ongoing approvals for products aligned with stewardship and residue compliance, which is shaping near-term portfolio priorities.

Recent Industry Developments

- June 2026: Nufarm highlighted capital prioritization and growth platforms, including the expansion of its carinata oil offtake arrangements with bp, in a strategy update delivered to investors. The focus underscored how suppliers are pairing crop-input portfolios with downstream demand in renewable fuel value chains, influencing resource allocation alongside core crop protection activities in Australia.

- May 2026: BASF launched Basta ULTRA herbicide in Australia, using its Glu-L technology and positioned for weed control in horticultural crops such as tree crops, vineyards and vegetables, following APVMA registration. The launch broadened BASF's non-selective herbicide offering for high-value cropping systems where stewardship, application performance, and label flexibility are central to distributor uptake.

- October 2024: APVMA cancelled all chlorthal dimethyl products, withdrawing 12 registrations across vegetable, turf and cotton uses. The regulatory action forced immediate substitution and reformulation decisions for affected users and suppliers, tightening availability of certain pre-emergent weed control options and increasing the importance of alternative modes of action and updated labels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of crop protection pesticides used in Australia to control weeds, insects, and crop diseases. Measurement is at the point of sale into agricultural use, and tracking follows the main on-farm application practices across the crop calendar.

Scope exclusions: It excludes fertilizers, adjuvants sold as standalone products, and non-crop uses such as household pest control.

Segmentation Overview

- By Function

- Herbicide

- Fungicide

- Insecticide

- Nematicide

- Molluscicide

- By Application Mode

- Chemigation

- Foliar Spray

- Fumigation

- Seed Treatment

- Soil Treatment

- By Crop Type

- Commercial Crops

- Fruits and Vegetables

- Grains and Cereals

- Pulses and Oilseeds

- Turf and Ornamentals

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the guardrails for the model, especially for what products are registered and how usage changes by season. Public references included APVMA registration listings and publications, Australian Bureau of Statistics agriculture datasets, ABARES outlook materials, Australian customs and trade statistics, and FAOSTAT for contextual benchmarks.

We also reviewed company annual reports and investor presentations, association websites, and trusted agriculture press to track active ingredient trends and category shifts, including resistance management strategies. For price and volume sanity checks, we used subscriptions that provide company financials and intelligence, along with shipment-level import and export data and patent databases where needed. The sources listed above are illustrative only, and additional public and paid references were used to collect, validate, and clarify the final assumptions.

Primary Interviews and Surveys

Primary work focused on validating the demand story behind each pesticide group, then pressure-testing the price and mix assumptions that can swing the totals. We spoke with formulators, distributors, agronomists, and large farm operators across major growing belts in Australia, and we used follow-up questions when desk research signals conflicted with what was seen in-field. This helped align model inputs such as treated area and dose intensity with real purchase behavior, not only shipment movement.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 15% | |

| Mid tier: 51% | Functional/Unit leaders: 28% | |

| Smaller Players: 18% | Managers: 57% |

Market-Sizing & Forecasting

Sizing starts from a top-down build that reconstructs the addressable pesticide spend using cropped area by crop group, typical treatment intensity, and the split by chemistry type. That spine is converted into value using observed price bands. After the core view is set, selective bottom-up approximations are used as a check, such as rolling up supplier and channel indicators, and testing sampled average selling price (ASP) times implied volumes for key product groups.

Key inputs we track include planted and harvested area, weather-linked pest and disease pressure, herbicide resistance related rotation behavior, application method mix (for example, seed treatment versus foliar), and import availability signals that can tighten supply. For forecasting, scenario analysis was used around rainfall variability and pest cycles, with ASP progression guided by primary feedback on formulation mix, input cost pass-through, and timing of seasonal programs. Where direct volume proxies were thin, gaps were handled by using crop-level treatment benchmarks and cross-checking them against trade and market-share signals before finalizing.

Data Validation & Update Cycle

Model outputs are triangulated against independent signals, including trade movement, cropping season conditions, and category-level adoption notes gathered from interviews. Outliers are flagged, and then the assumptions behind them are revisited, which can trigger re-contact with respondents to confirm whether it was a one-off season effect or a structural shift.

Before sign-off, the work goes through multi-step analyst reviews where calculation logic, unit conversions, and year mapping are checked again. The report is refreshed annually, and interim updates are added when material events occur such as major regulation changes, sharp currency moves, or abnormal pest outbreaks. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Australia Crop Protection Pesticides Market Size Measured Against Other Published Estimates

Published market values for Australia crop protection pesticides can look far apart because each publisher draws the market boundary differently and then applies its own timing for price and currency conversion. Differences also show up when one study uses wholesale trade values while another targets on-farm realized pricing after seasonal programs.

The biggest gap drivers are usually (a) whether biopesticides and seed treatment revenues are counted inside the same total, (b) whether the number is built from treated-area demand signals versus import and production values, and (c) how the ASP curve is refreshed across the season when exchange rates and input costs move. To reduce drift, the estimate is tied to agriculture season checks and then reconciled back to trade and category mix signals, a refresh-led discipline used by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.68 B (2026) | |

| Global Consultancy A | USD 1.23 B (2025) | This figure is typically closer to a chemicals-only definition that groups revenue by broad product type and may not consistently include seed treatment and smaller categories like molluscicides and nematicides, which lowers the total. |

| Trade Journal B | USD 1.40 B (2024) | This estimate is aligned to nominal wholesale market value built from trade and unit-value series, which can understate in-season farmgate pricing effects and can shift year-to-year based on currency timing and import mix. |

The table shows that the spread is mainly explained by what is counted in-scope and how prices are translated into USD for a given year. When the scope is aligned across pesticide groups and the pricing is refreshed with season-accurate checks, the final number becomes easier to trace and to replicate in future updates.

Key Questions Answered in the Report

How large is the Australia crop protection market in 2026?

The Australia crop protection market size is USD 1.68 billion in 2026 and is forecast to reach USD 2.16 billion by 2031.

Which function leads spending?

Herbicides command 45.72% of sales, reflecting heavy reliance on chemical weed control across broadacre grains.

What is the fastest-growing segment by function?

Fungicides show the fastest growth, expanding at a 12.32% CAGR through 2031 due to rising disease pressure.

Which state is projected to grow quickest?

Queensland is projected to deliver the highest regional CAGR at 6.32% between 2026 and 2031, driven by horticulture expansion and drone adoption.

How are regulatory shifts affecting product pipelines?

APVMA fast-track lanes for reduced-risk actives shorten approval times, but higher registration fees and pending glyphosate decisions add cost and uncertainty.

Page last updated on: