Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

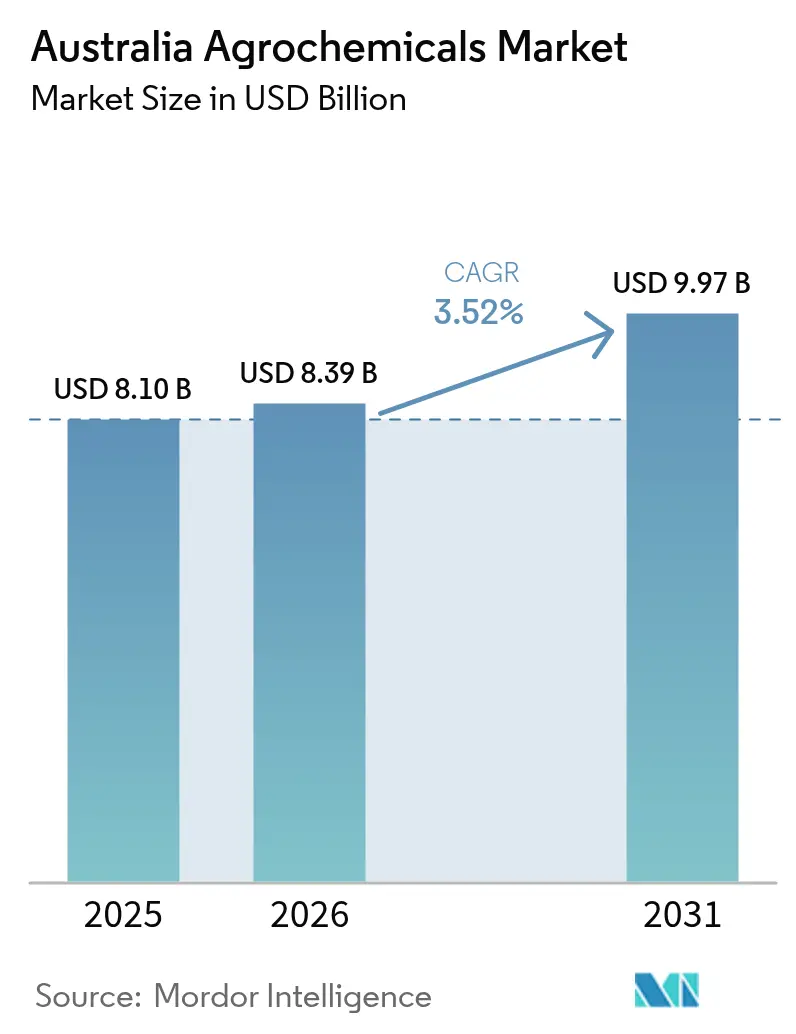

| Base Year Market Size (2025) | USD 8.10 Billion |

| Market Size (2026) | USD 8.39 Billion |

| Market Size (2031) | USD 9.97 Billion |

| Growth Rate (2026 - 2031) | 3.52% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Agrochemicals Market Analysis by Mordor Intelligence

Australia agrochemicals market size in 2026 is estimated at USD 8.39 billion, growing from 2025 value of USD 8.10 billion with 2031 projections showing USD 9.97 billion, growing at 3.52% CAGR over 2026-2031. Growing broadacre cropping in the Northern Territory, nationwide pressure to manage herbicide resistance, and a policy push for precision spraying technologies together sustain steady demand even as input cost volatility tempers spending plans. Investment in controlled-release fertilizers and the rising adoption of genetically modified herbicide-tolerant crops strengthen commercial confidence, while stricter review timelines at the Australian Pesticides and Veterinary Medicines Authority (APVMA) slow the entry of new chemistries. The Australian government's USD 53 million On Farm Connectivity Program supports precision agriculture adoption by offering up to 50% rebates for digital farming technologies. These technologies enable targeted chemical application and reduce environmental impact. The program, along with increased pest pressure due to climate variability in drought-affected regions of southern Australia, drives demand for crop protection solutions that meet both efficacy and environmental requirements. Market opportunities increasingly favor suppliers that pair crop-specific products with digital platforms capable of cutting chemical volumes by up to 96% without sacrificing yield.

Key Report Takeaways

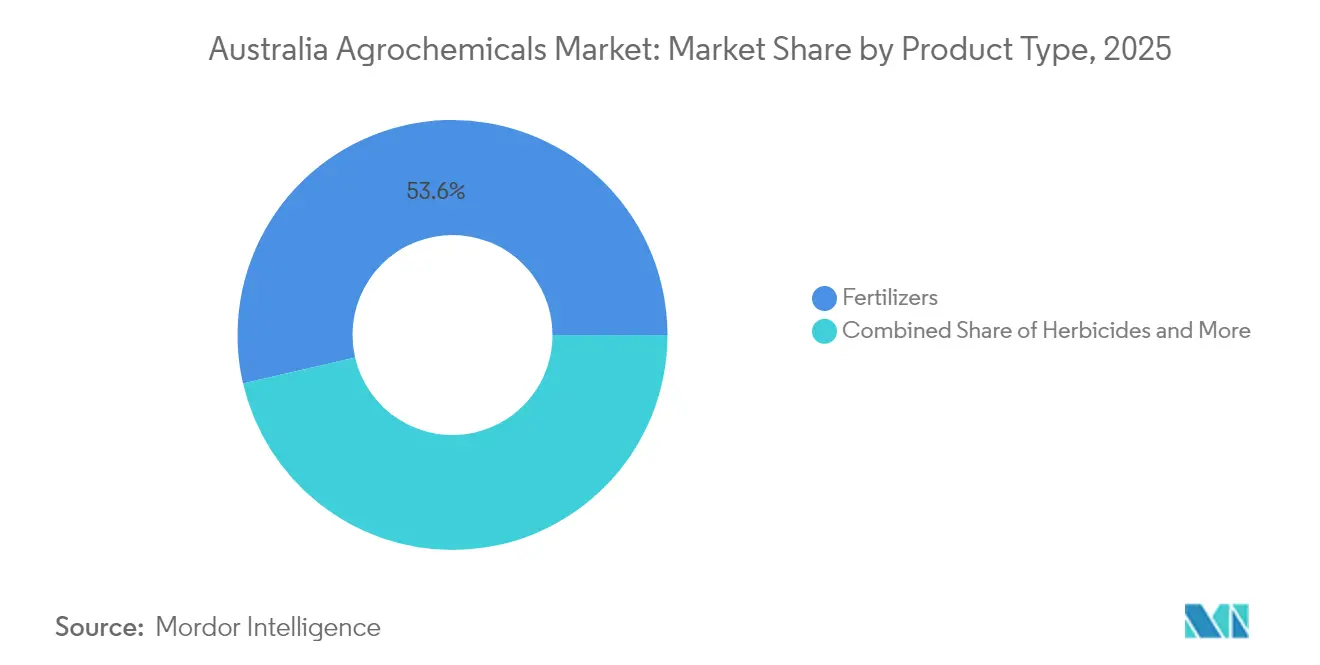

- By product category, fertilizers led with 53.62% of the Australia agrochemicals market share in 2025, while adjuvants posted the fastest growth with a 7.31% CAGR through 2031.

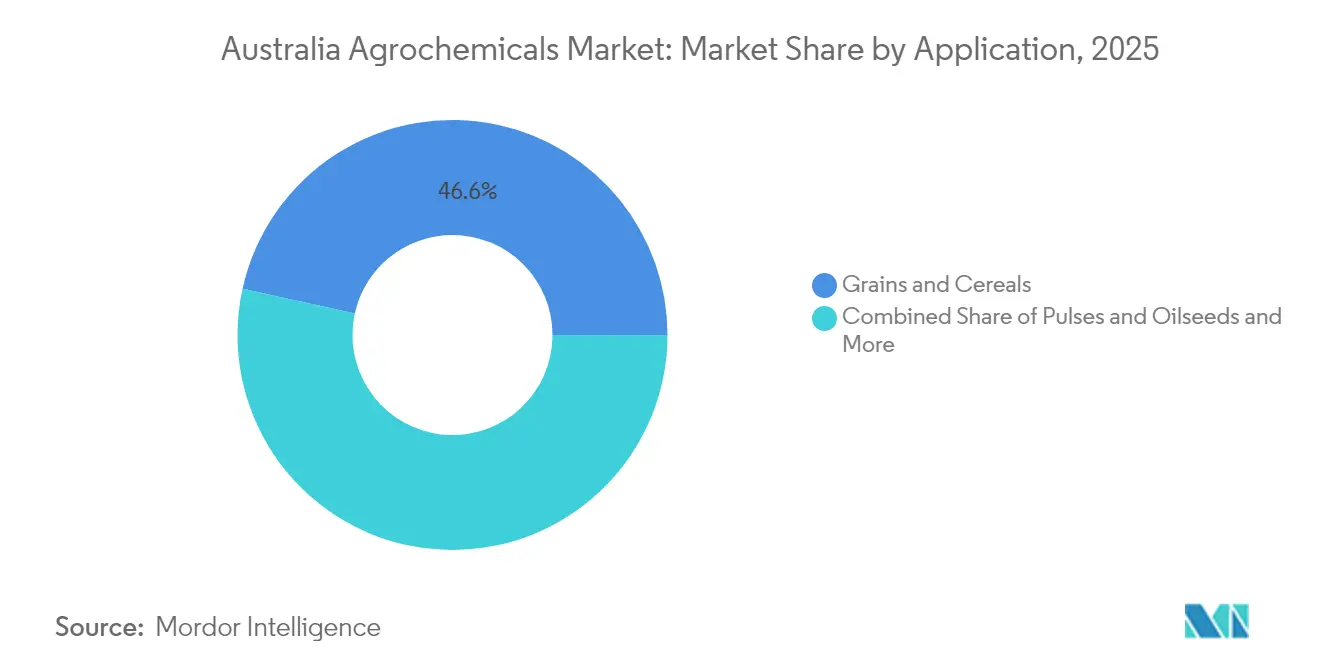

- By application, grains and cereals captured 46.55% of the Australia agrochemicals market size in 2025, while fruits and vegetables applications are advancing at a 6.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Agrochemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Synthetic herbicide-resistance management pressure | +0.8% | National, concentrated in Western Australia and New South Wales | Medium term (2-4 years) |

| Expansion of the broadacre cropping area in the Northern Territory | +0.6% | Northern Territory, spillover to Queensland | Long term (≥ 4 years) |

| Government rebates for precision spraying technologies | +0.4% | National, early adoption in Victoria, and South Australia | Short term (≤ 2 years) |

| Rising adoption of genetically modified herbicide-tolerant crops | +0.5% | National, excluding Western Australia and South Australia moratoria | Medium term (2-4 years) |

| Climate variability increasing pest infestation cycles | +0.7% | Southern Australia, Victoria and South Australia drought zones | Short term (≤ 2 years) |

| Investment in controlled-release fertilizer technologies | +0.3% | National, concentrated in high-value horticulture regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Synthetic herbicide-resistance management pressure

Australia records 154 confirmed herbicide-resistance cases, far exceeding neighboring countries, largely due to ryegrass infestation across 18 million hectares. Grower programs now combine new Group 14 herbicides, mechanical weed seed destruction, and AI-guided spot spraying to keep fields productive. Agrochemical companies capable of supplying novel modes of action while also providing digital scouting tools command premium pricing, because integrated programs lift control success and counteract escalating resistance costs. The APVMA’s emphasis on resistance stewardship elevates compliance barriers, giving incumbents with strong regulatory teams a clear edge.

Expansion of the broadacre cropping area in the Northern Territory

The Douglas Daly Stage Two plan targets an extra 60,000 hectares for irrigated and dryland crops, with cotton acreage set to rise from 90 hectares in 2024 to more than 35,000 hectares by 2029. New cotton systems require specialized herbicides that tolerate tropical humidity and soil types. Suppliers that establish extension services in the Territory benefit from early supplier lock-in as infrastructure spending of USD 1.6 billion channels inputs through dedicated hubs.

Government rebates for precision spraying technologies

The USD 53 million On-Farm Connectivity Program funds half the purchase cost of eligible digital hardware, leading more than 1,500 producers to adopt green-on-green spot sprayers and wireless weather stations in 2024.[1]Source: Australian Government, “On Farm Connectivity Program,” infrastructure.gov.au Demonstrated chemical savings and fast payback make rebate-assisted technology a near-mandatory upgrade, and suppliers bundling agronomy support with equipment gain rapid scale. As round-three grants roll out through 2025, the customer base for variable-rate herbicides and tailored adjuvant packs will broaden quickly.

Climate variability increasing pest infestation cycles

Southern drought stress shortens pest generation intervals, forcing growers to spray more frequently to protect yields. Pasture dieback driven by mealybugs already costs livestock producers more than USD 2 billion, highlighting the need for fast-acting insecticides. Seasonal forecasting tools funded by the Future Drought Fund help schedule sprays precisely, which raises demand for data-enabled crop protection subscription models that merge weather insight with product supply.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter APVMA reevaluation of endocrine-disrupting chemistries | -0.5% | National, affecting all agricultural sectors | Medium term (2-4 years) |

| Increasing farm input cost inflation linked to ammonia prices | -0.4% | National, concentrated in grain production regions | Short term (≤ 2 years) |

| Growing retailer preference for organic-labeled produce | -0.3% | National, strongest in urban supply chains | Long term (≥ 4 years) |

| Supply disruptions of key technical-grade actives | -0.2% | National, import-dependent regions most affected | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter APVMA reevaluation of endocrine-disrupting chemistries

The APVMA canceled chlorthal dimethyl products in October 2024 and extended paraquat reviews into late 2025, creating uncertainty that delays product launches and triggers reformulation costs. Multinationals with large regulatory budgets can navigate the changes, while smaller firms risk exit. Longer reviews also impede the rapid deployment of new resistance-breaking chemistries, potentially leaving growers without effective options.

Increasing farm input cost inflation linked to ammonia prices

Domestic granular urea prices in Australia reached AUD 865/ metric ton (USD 590/ metric ton) Free Carrier (FCA) Price in Geelong in the week ending June 20, marking an increase from AUD 745-750/ metric ton (USD 508-512/ metric ton) in 15 June 2025, as heightened buying activity from retailers actively securing supplies amid concerns over potential further price increases drove the surge.[2]Source: Argus Media Group, "Urea prices surge in Australia, prompt supply limited," argusmedia.com Orica’s potential closure of the Newcastle ammonia plant increases import reliance, exposing farmers to exchange-rate fluctuations. Australia Vegetable Growers March 2025 pricing update reflects ongoing input cost challenges affecting vegetable producers' profitability and investment capacity for advanced crop protection technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fertilizers Dominate Amid Import Dependency

Fertilizers captured 53.62% of the Australia agrochemicals market share in 2025 as complete reliance on imported urea inflated purchase volumes following Incitec Pivot Pty Ltd’s plant closure. Urea imports reached 768,800 metric tons in June 2024, 66% higher than the previous year. This intensity cements nitrogenous fertilizers at the core of the Australia agrochemicals market. Controlled-release coatings improve nutrient use efficiency, aligning with retailer sustainability demands and helping growers manage cost spikes. Phosphatic demand tracks grain acreage expansion, while potassic fertilizers gain from Western Australian potash mines that ease logistic costs. Precision soil testing prompts greater uptake of micronutrient blends, creating premium niches for customized formulations.

Pesticides remain the second-largest category. Herbicides account for most value because resistance pressures necessitate multiple modes of action and AI-guided spot spraying. The use of insecticides in cotton has decreased due to Bollgard 3 traits, which eliminate almost all broad-spectrum applications. Fungicide demand stays stable across cereals and horticulture, especially as wetter seasons return in eastern states. Adjuvants are the fastest-growing subsegment at 7.31% CAGR through 2031, fueled by precision sprayers that require specialized surfactants and drift inhibitors. Plant growth regulators have moderate but profitable adoption rates in horticulture, as fruit size and color significantly influence retail prices.

By Application: Grains Lead, Horticulture Accelerates

Grains and cereals account for 46.55% of 2025 consumption, reflecting the scale of wheat and barley exported from New South Wales, Victoria, and Western Australia. The Australia agrochemicals market size for grains is projected to expand steadily as Northern Territory cotton plantings move toward 35,000 hectares by 2029, pulling demand for defoliants, herbicides, and foliar fertilizers suited to tropical agronomy. Pulses and oilseeds maintain solid demand, particularly canola, where herbicide-tolerant traits call for companion chemistries that minimize volunteer persistence.

Fruits and vegetables deliver the highest growth at 6.55% CAGR through 2031 amid consumer pivot toward fresh and organic produce. Tasmania’s USD 10 billion (USD 7.0 billion) farm-gate ambition by 2050 relies on intensive horticulture enabled by smart irrigation and variable-rate fertigation systems. Commercial crops, chiefly cotton and sugarcane, remain heavy users of crop protection given their high gross margins. Pasture systems struggle with dieback, spurring research into integrated pest management tools rather than standard insecticides.

Geography Analysis

Demand in New South Wales and Victoria remains strong because growers rely on full-season crop protection programs to secure export-grade grain quality. Both regions show early adoption of AI-guided sprayers and controlled-release fertilizers that help manage rising input costs and stricter residue rules. The states’ proximity to major ports also reduces freight expense, allowing retailers to hold wider product ranges and replenish stocks quickly. Ongoing government incentives for connectivity upgrades improve data flow between growers and suppliers, supporting broader use of variable-rate application tools.

Western Australia ranks next in overall purchases, even as multi-year drought challenges yield potential and heighten pest pressure across its grain belt. Local debate over aerial spraying regulations encourages uptake of drift-reduction adjuvants and optical sensors that keep chemicals on target while satisfying community expectations. Queensland follows with a diversified cropping mix of cotton, sugarcane, and horticulture that drives year-round demand for insecticides, herbicides, and micronutrient blends. Expanding sugar exports also spur fertilizer sales because cane yields respond strongly to optimized nitrogen programs.

The Northern Territory's tropical climate enables multiple crop rotations throughout the year, allowing early-positioned suppliers to benefit from consistent sales of herbicides, adjuvants, and foliar fertilizers. Private investment in storage and processing infrastructure cuts logistics costs and accelerates product adoption in remote districts. South Australia and Tasmania remain smaller in volume yet strategically important because they serve premium wine grapes, apples, and high-value vegetables that require precise inputs and low residue thresholds.

Competitive Landscape

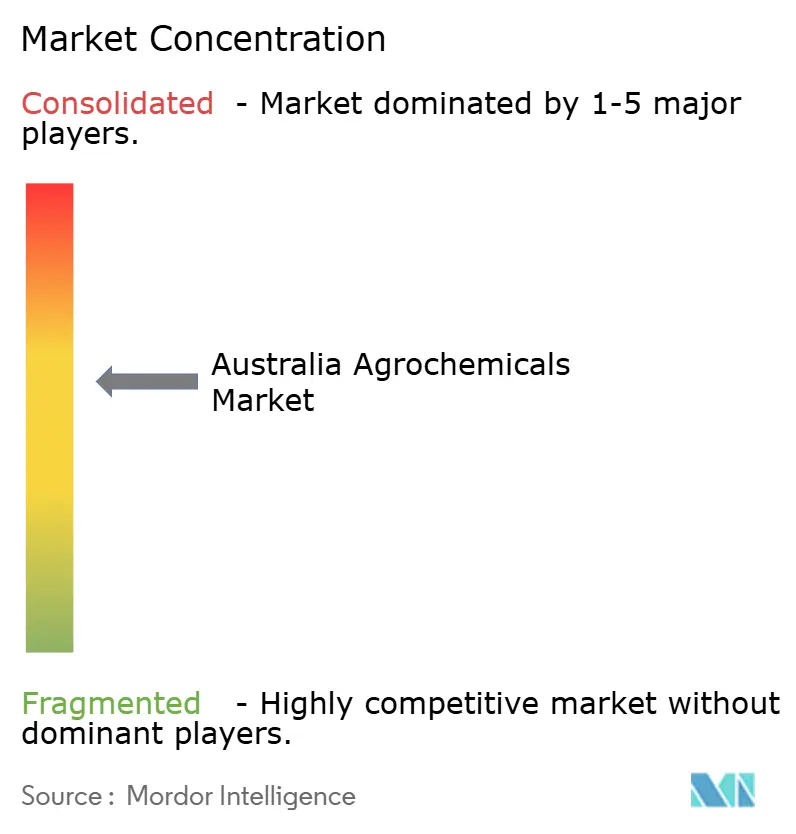

The competitive field is moderately concentrated, with the top five suppliers controlling a little over 60% of Australia agrochemicals market share through 2025. Nufarm leverages domestic manufacturing flexibility and an extensive rural retail network to defend core positions in herbicides and insecticides despite pressure from offshore generics. Bayer AG, Syngenta Group, and BASF SE rely on global discovery pipelines to introduce resistance-breaking active ingredients that meet the APVMA’s evolving safety standards. Nutrien and Yara International ASA reinforce their chemical catalogs with strong fertilizer footprints, letting them bundle crop nutrition and protection for large broadacre clients.

Strategy is shifting from simple price competition toward integrated agronomic support and digital enablement. BASF SE partnered with National Rural Independents in early 2024 to train twenty-two young agronomists who now promote its AI-ready Liberty ULTRA herbicide platform in cotton and canola systems. Syngenta Group’s sustained engagement during the paraquat and diquat reviews illustrates the value of experienced regulatory teams that help growers retain critical tools under stricter stewardship requirements. Bayer AG expands Climate FieldView coverage in New South Wales and Victoria, linking satellite imagery with prescription maps that cut chemical volumes while maintaining efficacy. Nufarm accelerates development of controlled-release formulations to capture value in the fast-growing adjuvant and specialty fertilizer niches.

Smaller innovators focus on narrow technology gaps that multinationals overlook. Local start-ups supply polymer coatings that regulate nutrient release in variable soil moisture. Imports of active ingredients remain vulnerable to Asian supply disruptions, so distributors hedge by carrying higher inventories and sourcing from secondary manufacturers in Saudi Arabia and the United Arab Emirates. Overall, companies able to combine strong regulatory compliance, digital agronomy services, and sustainable product portfolios are positioned to capture incremental share as the market continues its measured expansion.

Australia Agrochemicals Industry Leaders

-

Nufarm

-

Bayer AG

-

Incitec Pivot Pty Ltd

-

Nutrien

-

Yara International ASA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: APVMA amended Maximum Residue Levels via Gazette 10, altering compliance requirements for several active ingredients in agrochemicals. The APVMA’s updated MRLs in Gazette 10 enhance market access and regulatory clarity for agrochemical products, supporting safer and more compliant crop protection practices across Australia.

- September 2024: Albaugh registered its SPIROMAX 240 SC Insecticide in Australia, expanding its crop protection product portfolio in the Australian agricultural market. The registration demonstrates the company's commitment to providing crop protection products to Australian farmers.

- May 2024: BASF SE launched its insecticide Cimegra in Australia. The product contains the active ingredient Broflanilide, developed through BASF SE's technology. Cimegra provides effective and long-lasting control of insect pests across multiple crop varieties.

Australia Agrochemicals Market Report Scope

Agrochemicals are engineered chemical or biological formulations that improve crop quality and yield while preventing crop deterioration from insects, pest infestation, and disease. The Australian agrochemicals market is segmented by Product Type (Fertilizers, Pesticides, Adjuvants, and Plant Growth Regulators) and Application (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, Commercial crops, and Other Applications). The report offers market estimation and forecasts in value (USD) for the above-mentioned segments.

By Product Type

| Fertilizers | Nitrogenous |

| Phosphatic | |

| Potassic | |

| Other Fertilizers | |

| Pesticides | Herbicides |

| Insecticides | |

| Fungicides | |

| Other Pesticides | |

| Adjuvants | |

| Plant Growth Regulators |

By Application

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Commercial Crops |

| Other Applications |

| By Product Type | Fertilizers | Nitrogenous |

| Phosphatic | ||

| Potassic | ||

| Other Fertilizers | ||

| Pesticides | Herbicides | |

| Insecticides | ||

| Fungicides | ||

| Other Pesticides | ||

| Adjuvants | ||

| Plant Growth Regulators | ||

| By Application | Grains and Cereals | |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Commercial Crops | ||

| Other Applications | ||

Key Questions Answered in the Report

What is the current value of the Australia agrochemicals market?

The market stood at USD 8.39 billion in 2026.

How fast is the market projected to grow through 2031?

It is projected to expand at a 3.52% CAGR, reaching USD 9.97 billion by 2031.

Which product category holds the largest share?

Fertilizers lead with 53.62% share, largely due to the nations reliance on imported urea.

Why are adjuvants growing faster than other categories?

Precision sprayers need specialized surfactants and drift inhibitors, pushing adjuvants to a 7.31% CAGR.

Page last updated on: