Pakistan Automotive Lubricants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

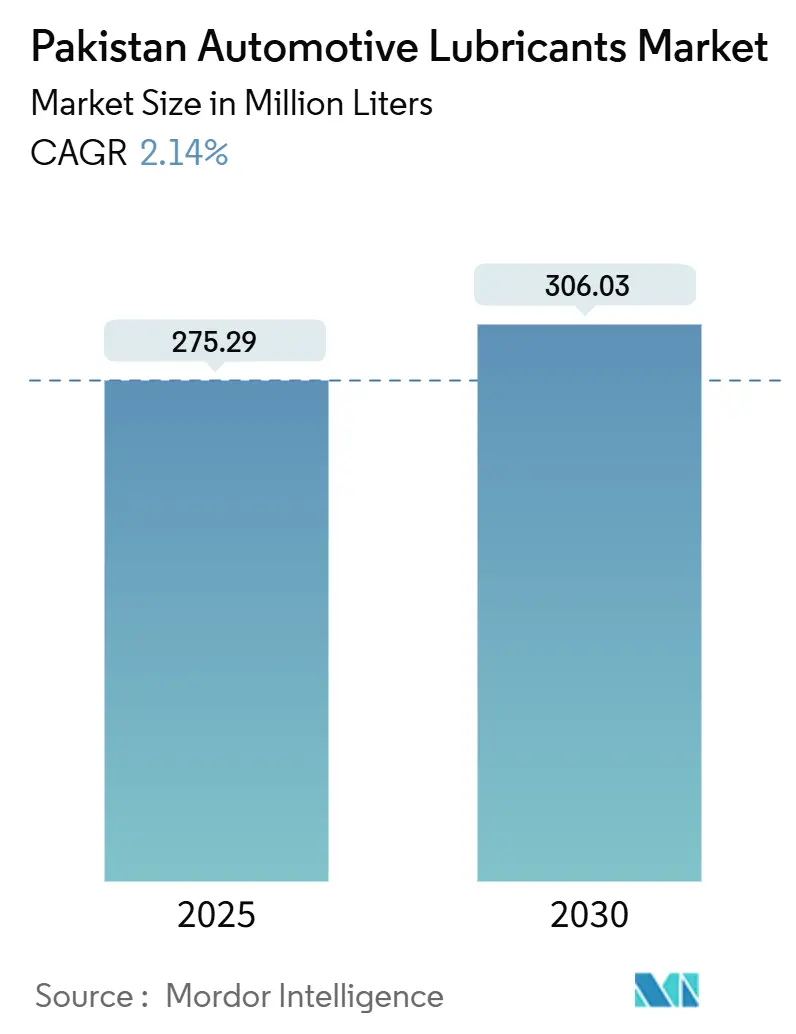

| Market Volume (2025) | 275.29 Million liters |

| Market Volume (2030) | 306.03 Million liters |

| Growth Rate (2025 - 2030) | 2.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Automotive Lubricants Market Analysis by Mordor Intelligence

The Pakistan Automotive Lubricants Market size is estimated at 275.29 million liters in 2025, and is expected to reach 306.03 million liters by 2030, at a CAGR of 2.14% during the forecast period (2025-2030). This measured expansion reflects a maturing demand base that now grows more in line with macro-economic fundamentals than with rapid motorization spurts. A sharp rebound in new-vehicle sales since 2024 has revived first-fill demand, while an aging national parc underpins steady aftermarket consumption. Continued highway upgrades along the China-Pakistan Economic Corridor (CPEC) increase freight mileage, thereby amplifying the volumes of diesel engine oils required by heavy-duty trucks. On the supply side, a heavy reliance on imported Group II/III base oils exposes input costs to global price swings and rupee depreciation. Counterfeit brands continue to siphon share from legitimate blenders, compressing margins and delaying broader migration toward synthetics.

Key Report Takeaways

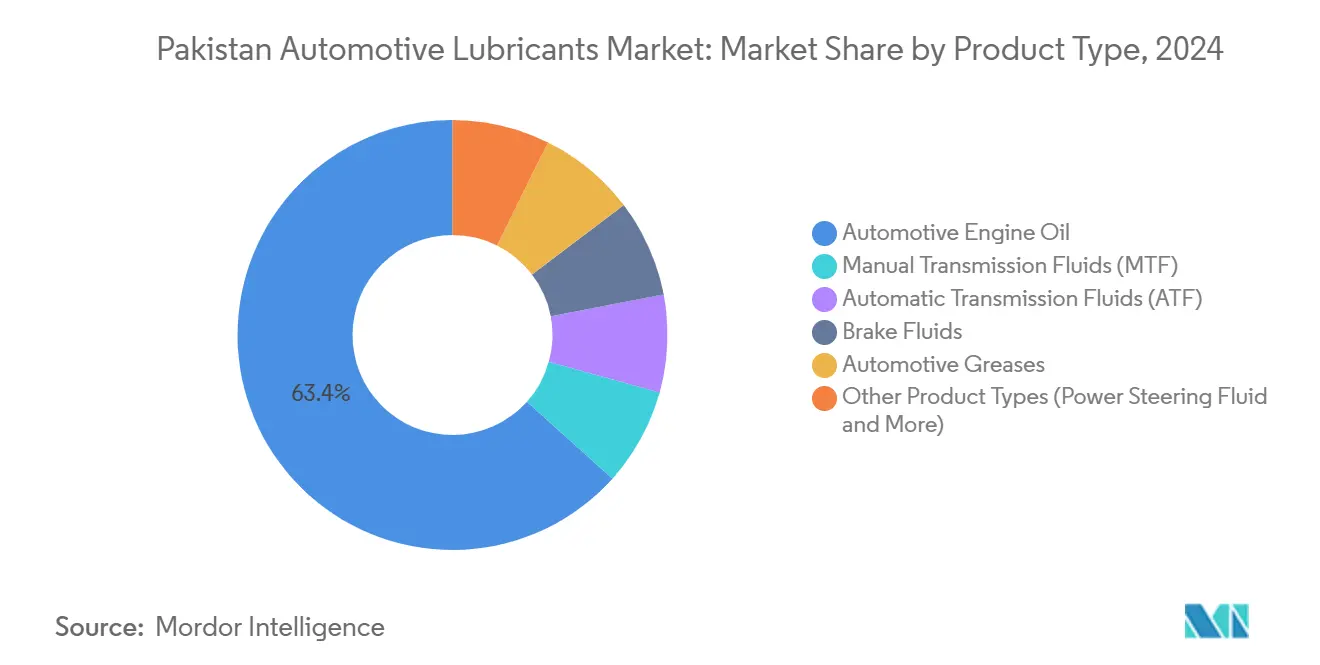

- By product type, automotive engine oil led with a 63.36% share of Pakistan's automotive lubricants market in 2024, while automatic transmission fluids are projected to grow at the fastest rate, with a 2.41% CAGR through 2030.

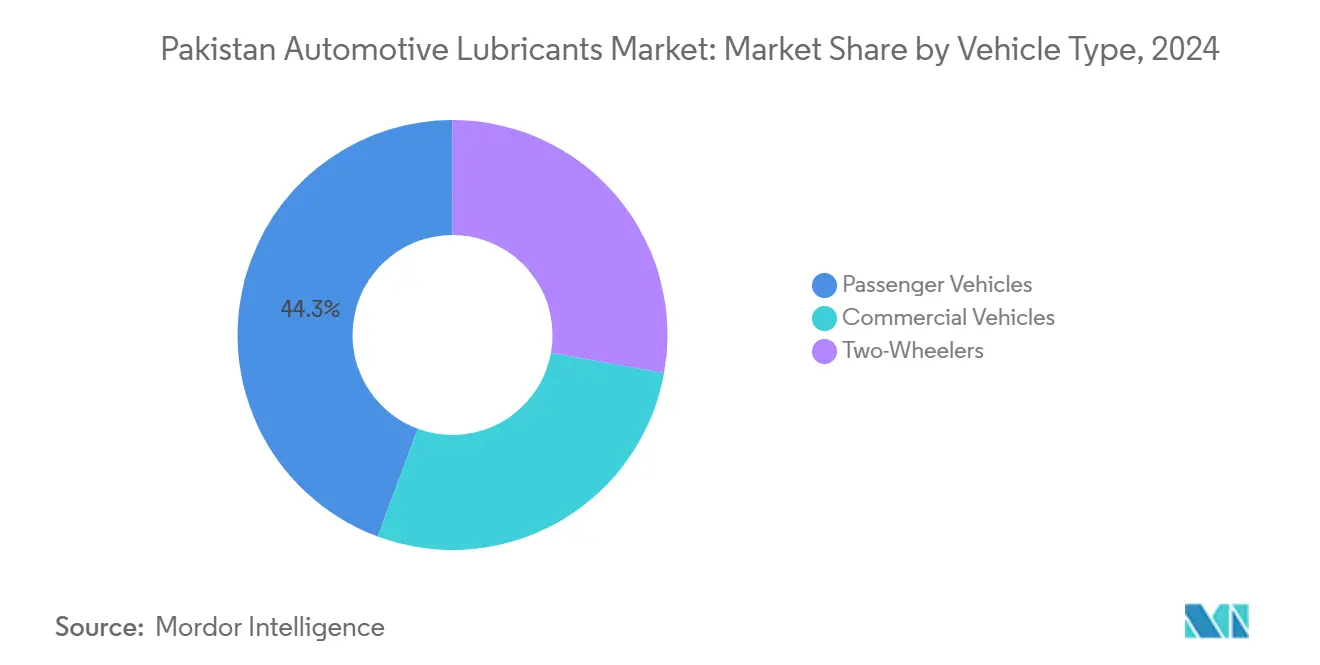

- By vehicle type, passenger vehicles accounted for 44.35% of the Pakistan automotive lubricants market size in 2024; commercial vehicles are forecast to post the quickest 2.32% CAGR between 2025 and 2030.

Pakistan Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding vehicle parc sustains aftermarket demand | +0.8% | Punjab and Sindh urban corridors | Medium term (2-4 years) |

| Rising freight and logistics fleet activity | +0.6% | Karachi–Lahore–Faisalabad highway axes | Short term (≤2 years) |

| High-temperature operations push synthetics | +0.4% | Major urban heat islands | Long term (≥4 years) |

| OEM–lube marketer partnerships | +0.3% | Nationwide dealer networks | Medium term (2-4 years) |

| Euro-V compliance accelerates low-viscosity grades | +0.2% | Nationwide | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Expanding Vehicle Parc Sustains Aftermarket Lubricant Demand

Pakistan has recorded four consecutive quarters of double-digit growth in new passenger-car registrations since mid-2024, and every car that rolls off a dealer lot eventually becomes a recurring customer for engine oil, coolant, brake fluid, and greases. Two-wheelers remain the numerically dominant mode of personal transport, yet each motorcycle consumes far smaller lubricant volumes per service interval than a car or truck. Because motorcycles typically receive basic mineral formulations, blenders focus on maintaining value rather than upgrading to premium formulations. Passenger-car owners, by contrast, now stretch drain intervals out to 9,000–10,000 km, prompting manufacturers to endorse semi-synthetics to safeguard warranty compliance. Every additional kilometre driven on crowded urban roads multiplies oil oxidation rates, anchoring resilient baseline demand even as engines become more efficient. Taken together, the enlarging parc and moderate shift toward higher-quality products elevate the Pakistan automotive lubricants market beyond purely population-driven growth.

Rising Freight and Logistics Fleet Activity Increases Diesel-Engine Oil Use

Freight movement accelerated once the Sukkur-Multan motorway opened under CPEC, slicing transit times between Karachi Port and Punjab’s industrial heartland. Each incremental ton-kilometer worked by a Class 8 truck requires roughly 18–20 liters of 15W-40 diesel engine oil at every 25,000 km interval, dwarfing the 4–5 liters filled into a typical passenger car. Fleet operators now evaluate lubricants based on life-cycle cost rather than sticker price; accordingly, premium CK-4 synthetics are gaining traction because they extend drain intervals to 40,000 km, reduce unplanned downtime, and marginally improve fuel efficiency. Gear oils, transmission fluids, and hydraulic fluids for truck-mounted cranes witness parallel gains as logistics yards mechanize cargo handling. Incremental growth in retail e-commerce adds final-mile vans to the operating fleet, further broadening the Pakistan automotive lubricants market footprint in the commercial segment.

Growing Penetration of Synthetics Amid High-Temperature Operation

Summer temperatures in Karachi, Multan, and Jacobabad routinely climb past 45 °C. Under such thermal stress, conventional SN-grade mineral oils shear down quickly, oxidize, and form deposits that choke variable-valve timing passages. OEMs are therefore revising owner's manual specifications toward 5W-30 or even 0W-30 API SP synthetics that maintain viscosity across a wider temperature range. Shell Helix Ultra and Mobil 1 continue to lead in brand recognition, but more affordable semi-synthetic blends from local blenders are gaining market share at independent workshops. Wafi Energy reported double-digit unit growth for its premium portfolio in 2024, despite overall market sluggishness, attributing the sales momentum to consumer education campaigns that highlighted lower total maintenance costs over a six-month cycle[1]Business Recorder Staff, “Wafi Energy Posts Record Volume Growth in Pakistan,” businessrecorder.com. Nonetheless, price-sensitive motorists still default to basic 20W-50 mineral grades, limiting synthetic penetration to roughly 11% of total retail volumes in 2025.

OEM Partnerships Bolster Brand Loyalty and Premium Product Uptake

Honda Atlas recommends a proprietary 0W-20 semi-synthetic oil, branded as “Honda Genuine Oil,” for all newly delivered City and Civic models. Each of the company’s 38 dealerships stocks only the specified formula. This controlled supply chain assures lubricant quality, reinforces brand experience at routine service events, and allows a 12% price premium over off-the-shelf competitors. Similar factory-fill alliances exist between Toyota Indus and Caltex Havoline, Suzuki Pakistan and TotalEnergies Quartz, anchoring consistent pull-through demand for partner brands. Fleet-service contracts take it one step further by bundling oil, filters, and extended warranty coverage into a single invoice, thereby locking in supplier volumes over multi-year horizons. Because warranty compliance is high on both personal and commercial vehicle owners’ priority lists, these OEM endorsements funnel customers toward higher-end formulations, gradually recalibrating the value mix inside the Pakistan automotive lubricants market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of counterfeit/illegal blending undermines quality | −0.5% | Rural and peri-urban markets nationwide | Short term (≤ 2 years) |

| High import dependence on base oils fuels cost volatility | −0.4% | Nationwide manufacturing and blending facilities | Medium term (2-4 years) |

| Currency depreciation squeezes lubricant affordability | −0.3% | All provinces, most acute in price-sensitive segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Prevalence of Counterfeit and Illegal Blending Undermines Quality

Estimates from national trade associations indicate that substandard or counterfeit lubricants accounted for nearly 22% of rural retail shelves in 2024. Small-scale mixers repackage recycled base oils, dilute additive concentrations, and affix labels that mimic reputable international brands. Price differentials run as high as 40% compared with genuine goods, luring budget-constrained farmers, motorcyclists, and three-wheeler operators. Because many buyers lack easy access to laboratory testing or OEM recommendations, brand equity erodes across the market. Genuine marketers respond with tamper-proof QR-coded caps, random batch audits, and consumer hotlines, but enforcement still lags. Investigations by the Oil & Gas Regulatory Authority (OGRA) shut down 17 clandestine blending sites in 2024, yet the economic incentive to operate in the gray market remains strong whenever rupee weakness inflates legitimate product pricing. Over the near term, counterfeit trade subtracts up to half a percentage point from the achievable CAGR of the Pakistan automotive lubricants market by dragging total addressable volume into informal channels.

High Import Dependence on Base Oils Fuels Cost Volatility

Local refineries only supply roughly 20–25% of national Group I demand and virtually no Group II/III base oils, forcing manufacturers to import cargoes from the United Arab Emirates, Saudi Arabia, and South Korea. Every US 1-cent rise in the CFR Persian Gulf Group III spot quote translates into USD 0.8 million in additional annual feedstock cost for a mid-tier blender operating at 8 million liters per year. A 9%-rupee depreciation against the U.S. dollar in FY 2024/25 amplified landed-cost inflation, compelling price hikes that outpaced nominal wage growth. Manufacturers attempted partial hedging via forward exchange contracts, but only the largest conglomerates possess adequate credit lines to lock in rates. As a consequence, retail shelf prices can fluctuate by 5–7% within a single quarter, complicating distributor inventory planning. Persistent reliance on feedstock dampens capital expenditure for local hydrotreating upgrades, delaying the country’s ability to internalize higher-grade base-oil production and curtail exposure for the Pakistani automotive lubricants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oil Retains Commanding Share While ATF Accelerates

Engine oils accounted for 63.36% of the total Pakistan automotive lubricants market share in 2024, with consumption across passenger cars, trucks, motorcycles, and agricultural vehicles. Consumption traces directly to maintenance culture; newer cars receive 5W-30 semi-synthetic blends every 8,000–10,000 km, taxis undergo mineral top-ups at shorter intervals, and heavy-duty trucks use CH-4 or CK-4 multigrades every 500 operating hours. The Pakistan automotive lubricants market size attributable to engine oils alone is projected to rise from 174 million liters in 2025 to 193 million liters in 2030 as freight ton-kilometres advance and rural motorcycle ownership deepens. Within the service-fill channel, promotional bundling with oil filters and coolant bottles encourages larger checkout sizes, strengthening retail throughput for authorized outlets. Local blending capacity continues to expand; Hi-Tech Lubricants operates an 80,000-ton facility jointly with SK EnMove, ensuring in-country supply of Group II-based semi-synthetics that satisfy Euro-V viscosity standards.

Automatic transmission fluids (ATFs) expand at a 2.41% CAGR, the fastest among all categories, as automatic gearboxes penetrate entry-level sedans and sub-compact SUVs. Each automatic gearbox fill requires 7–9 liters of premium fluid, compared with roughly 2 liters for a manual unit, which compounds the revenue opportunity. OEMs increasingly specify proprietary viscosity profiles, such as Toyota's WS and Honda's HMMF, driving brand-specific aftermarket pull. Domestic ATF blenders rely on ester-based additive packs that must be imported from Japan or Germany, keeping unit costs high while protecting margins against down-trading prevalent in the mineral engine oil segment. Brake fluids and greases, although fundamentally essential for safety and chassis maintenance, develop more slowly because average vehicle replacement cycles lengthen; nonetheless, each incremental light-vehicle sale eventually contributes to periodic brake-fluid flushes and chassis lubrication demand, anchoring stable baseline volumes within the Pakistani automotive lubricants market.

By Vehicle Type: Commercial Vehicles Set the Growth Pace Amid Passenger-Car Dominance

Passenger vehicles accounted for 44.35% of the Pakistan automotive lubricants market size in 2024, supported by the largest installed base of approximately 4.9 million cars and SUVs registered nationwide. Each passenger car consumes 3.5–4.5 liters of engine oil per service, plus minor quantities of power steering and brake fluid, ensuring dependable service fill turnover at franchised dealerships and independent workshops. The segment benefits from bank financing schemes that revive showroom traffic; however, rising engine-technology sophistication pushes drain intervals longer, moderating pure volume growth over the forecast horizon. Brand-loyalty programs introduced by Indus Motor Company and local Nissan distributors bundle genuine oils with extended warranties, fostering a premium skew and elevating the average selling price rather than the number of liters sold.

Commercial vehicles are the fastest-growing segment, expanding at a 2.32% CAGR through 2030, driven by CPEC logistics projects and e-commerce, which sustain road freight utilization. A single 6×4 prime mover can demand up to 28 liters of SAE 15W-40 at every change, dwarfing passenger-car fills. Every truck also carries differential oils, coolants, and often grease cartridges for chassis lubrication, multiplying per-unit lubricant demand. Fleet managers use telematics to track oil-life indicators, transitioning to condition-based maintenance that prefers high-quality synthetics capable of up to 60,000 km drains. As a result, commercial vehicles contribute disproportionately to revenue even at lower unit numbers. Meanwhile, the two-wheeler fleet of nearly 25 million units remains a volume cornerstone, yet its 0.9-litre average oil-sump capacity and increasing drain intervals temper aggregate litre growth. Nonetheless, rural two-wheeler owners exhibit brand loyalty toward PSO’s “Mehfooz” 20W-40 mineral range, ensuring c.ontinued engagement for the Pakistan automotive lubricants market

Geography Analysis

Punjab anchors the largest provincial share of lubricant consumption, housing over 55% of registered vehicles and hosting assembly plants for Honda, Toyota, and Suzuki. Lahore, Faisalabad, and Gujranwala form a manufacturing triangle where ancillary component manufacturers cluster, ensuring a steady supply of factory-produced cars and motorcycles. The province’s dense highway network funnels inter-city trucks that replenish diesel engine oil at service plazas along the M-2 and M-3 motorways. Sindh, spearheaded by Karachi, follows as the second-largest consuming region. The port city not only serves as the gateway for imported base oils and packaged lubricants but also sustains high-temperature urban driving, which accelerates oil-degradation cycles. Karachi’s heavy cargo traffic, emanating from Kemari and Port Qasim operations, prompts a high demand for heavy-duty lubricants, hydraulic oils, and greases used in cranes and container handlers.

Khyber Pakhtunkhwa (KPK) and Balochistan collectively hold a smaller yet rising share as roadway connectivity improvements unlock mining, quarrying, and cross-border trade with Afghanistan and Iran. The Quetta-Zhob highway generates new commercial-vehicle traffic, requiring mid-route grease points and gear-oil top-ups, which creates nascent distribution nodes for lubricant marketers that have historically focused on coastal and central markets. Retail pricing differentials emerge because freight charges increase landed costs in these mountainous terrains; still, limited competition affords reputable brands higher gross margins per liter than in saturated Punjab bazaars. Gilgit-Baltistan and Azad Kashmir remain minimal in volume terms but are targeted for specialized low-temperature synthetics designed to perform in sub-zero alpine routes. Collectively, regional disparities underscore the need for segmented channel strategies within the Pakistani automotive lubricants market, aligning product portfolios and pack sizes with local vehicle mixes and climate conditions.

Competitive Landscape

The Pakistan automotive lubricants market is moderately consolidated, with Pakistan State Oil (PSO) retaining the largest single-company position in 2024, leveraging a nationwide network of more than 3,500 retail outlets that anchor both fuel and lubricant sales. Its “Premium Motor Oil” and “Mehfooz” sub-brands appeal to fleet operators and two-wheeler owners, respectively, ensuring broad market coverage. Medium-tier local blenders collaborate with technology alliances to access Group III base oils and advanced additive packs without incurring the costs of standalone research and development. These cooperative structures enable the production of cost-competitive semisynthetic grades suitable for Euro-V engines, yet priced below full imports —a delicate balance in a price-sensitive consumer landscape. On the innovation front, companies position premium blends around three key vectors: extended drain capability, fuel economy gains, and emissions compliance. Marketing increasingly taps into digital channels; mobile-app loyalty programs capture service-interval data and trigger push notifications for oil-change reminders, locking consumers into brand ecosystems. The mosaic of local and foreign participation, coupled with supply-chain upgrades, tilts the Pakistan automotive lubricants market toward moderate consolidation over the medium term.

Pakistan Automotive Lubricants Industry Leaders

Shell plc

Pakistan State Oil

Caltex Pakistan

Hi-Tech Lubricants Limited

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Wafi Energy finalized the acquisition of 77.42% of Shell Pakistan, injecting Gulf capital to modernize blending and retail assets.

- August 2024: ENOC Group signed an exclusive agreement with Flow Petroleum to distribute the full ENOC lubricant range across Pakistan.

Pakistan Automotive Lubricants Market Report Scope

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

What is the current volume of the Pakistan automotive lubricants market?

It stands at 275.29 million liters in 2025 and is forecast to reach 306.03 million liters by 2030.

Which lubricant segment holds the highest share?

Automotive engine oil commands 63.36% share thanks to its universal application across all vehicle classes.

Which product type is expanding fastest?

Automatic transmission fluids are projected to grow at a 2.41% CAGR through 2030 as automatic gearboxes spread.

Why are commercial vehicles important to lubricant growth?

Each heavy truck consumes far higher oil volumes per service and the segment is forecast to grow at a 2.32% CAGR.

How does import dependence affect lubricant pricing?

With 70–80% of base oils imported, price and currency swings directly raise landed costs and retail prices.

What strategic move did Chevron announce recently?

Chevron will invest USD 30 million in a fully automated domestic blending plant to cut import reliance.

Page last updated on: